DEVELOPING FINANCIAL DECISION SUPPORT

FOR HIGHWAY INFRASTRUCTURE

SUSTAINABILITY

By

Kai Chen Goh B.Sc Construction (Hons), M.Sc Construction Management (UTM)

A thesis submitted in partial fulfillment of the requirements for the

degree of

Doctor of Philosophy

SCHOOL OF URBAN DEVELOPMENT

FACULTY OF BUILT ENVIRONMENT AND ENGINEERING

QUEENSLAND UNIVERSITY OF TECHNOLOGY

2011

II

STATEMENT OF ORIGINAL AUTHORSHIP

DECLARATION

The work contained in this thesis has not been previously submitted for a degree or

diploma at any other higher education institution. To the best of my knowledge and

belief, the thesis contains no material previously published or written by another

person except where due reference is made.

Signed : _____________________

Date : _____________________

III

ACKNOWLEDGEMENTS

I wish to express my sincerest appreciation and gratitude to Professor Jay Yang for

his wisdom, patients, calmness in my PhD journey. Without his persistent support,

this thesis may never have been completed on time nor would I have survived it.

Professor Jay Yang through his mentoring enabled me with passionate and self

possessed that this journey was indeed possible to complete.

My deepest appreciation also to Dr. Johnny Wong for his invaluable help in

developing ideas, checking sources and for his great and precise attention to detail

and for willingly sharing his expertise and in-depth knowledge.

I wish to also thank my fellow PhD student colleagues Melissa Chan, Mei Yuan, Mei

Li, Hu Yuan Luo and Riduan Yunus, who have helped to make this journey

somewhat easier through their friendship, continuous encouragement, sharing of

ideas and constructive feedback. Special thanks also to my first best mates in this

journey Asrul Masrom, Tien Choon Toh, Anna Wiewiora, Zhengyu Yang and Soon

Kam Lim for their support and friendship.

I would also like to make special mention to those individuals and organisations that

benevolently contribute their support, guidance, encouragement and contribution to

this research project. My appreciation and thanks to all. Finally, I wish to

acknowledge the support and encouragement received from my wife, Nyuk Sang

Kiew, my brothers, my parents and friends throughout this course of study.

IV

ABSTRACT

The development of highway infrastructure typically requires major capital input

over a long period. This often causes serious financial constraints for investors. The

push for sustainability has added new dimensions to the complexity in the evaluation

of highway projects, particularly on the cost front. This makes the determination of

long-term viability even more a precarious exercise. Life-cycle costing analysis

(LCCA) is generally recognised as a valuable tool for the assessment of financial

decisions on construction works. However to date, existing LCCA models are

deficient in dealing with sustainability factors, particularly for infrastructure projects

due to their inherent focus on the economic issues alone.

This research probed into the major challenges of implementing sustainability in

highway infrastructure development in terms of financial concerns and obligations.

Using results of research through literature review, questionnaire survey of industry

stakeholders and semi-structured interview of senior practitioners involved in

highway infrastructure development, the research identified the relative importance

of cost components relating to sustainability measures and on such basis, developed

ways of improving existing LCCA models to incorporate sustainability commitments

into long-term financial management. On such a platform, a decision support model

incorporated Fuzzy Analytical Hierarchy Process and LCCA for the evaluation of the

specific cost components most concerned by infrastructure stakeholders. Two real

highway infrastructure projects in Australia were then used for testing, application

and validation, before the decision support model was finalised. Improved industry

understanding and tools such as the developed model will lead to positive

sustainability deliverables while ensuring financial viability over the lifecycle of

highway infrastructure projects.

Keywords: sustainability, highway, infrastructure, life-cycle costing analysis, decision support.

V

TABLE OF CONTENTS

STATEMENT OF ORIGINAL AUTHORSHIP ................................................... II

ACKNOWLEDGEMENTS ..................................................................................... III

ABSTRACT .............................................................................................................. IV

TABLE OF CONTENTS .......................................................................................... V

LIST OF ABBREVIATIONS ................................................................................. XI

DEFINITION OF TERMS ..................................................................................... XII

LIST OF FIGURES .............................................................................................. XIII

LIST OF TABLES ................................................................................................. XV

CHAPTER 1: INTRODUCTION .......................................................................... 1

1.1 Research Background .................................................................................... 11.2 Research Questions ....................................................................................... 41.3 Research Objectives ...................................................................................... 51.4 Significance of the Research ......................................................................... 61.5 Scope and Delimitation ................................................................................. 71.6 Research Framework ..................................................................................... 9

1.6.1 Stage 1 - Developing a preliminary model ............................................ 91.6.2 Stage 2 - Developing the survey .......................................................... 101.6.3 Stage 3 - Developing a decision support model ................................... 11

1.7 Thesis Organisation ..................................................................................... 141.8 Chapter Summary ........................................................................................ 15

CHAPTER 2: LITERATURE REVIEW ............................................................. 17

2.1 Introduction ................................................................................................. 172.2 Sustainability and Transport ........................................................................ 17

2.2.1 Sustainable development principles and evolution .............................. 202.2.2 Highway infrastructure development in Australia ............................... 23

2.3 Long-Term Financial Prospects in Highway Development ........................ 252.3.1 Principle of engineering economics ..................................................... 25

2.3.1.1 Benefit cost analysis ..................................................................... 25

VI

2.3.1.2 Life-cycle costing analysis (LCCA) ............................................. 262.3.1.3 Differences between BCA and LCCA .......................................... 282.3.1.4 Decision support ........................................................................... 29

2.3.2 Life-cycle costing analysis and its application in highway infrastructure ………………………………………………………………………...30

2.3.2.1 Current LCCA models and programs in highway infrastructure .. 312.3.2.2 Limitations of existing LCCA studies in adopting sustainable measures …………………………………………………………………...36

2.3.3 Significance of incorporating sustainability-related cost components in LCCA ………………………………………………………………………...38

2.4 Cost Implications in Highway Infrastructure .............................................. 402.4.1. Sustainability-related cost components in highway projects ............... 40

2.4.1.1 Agency category ........................................................................... 422.4.1.2 Social category .............................................................................. 452.4.1.3 Environmental category ................................................................ 47

2.5 Research Gap ............................................................................................... 512.5.1 Challenges to improve long-term financial decisions .......................... 512.5.2 Critical cost components in Australian highway investments ............. 52

2.6 Chapter Summary ........................................................................................ 53

CHAPTER 3: RESEARCH METHODOLOGY AND DEVELOPMENT ......... 55

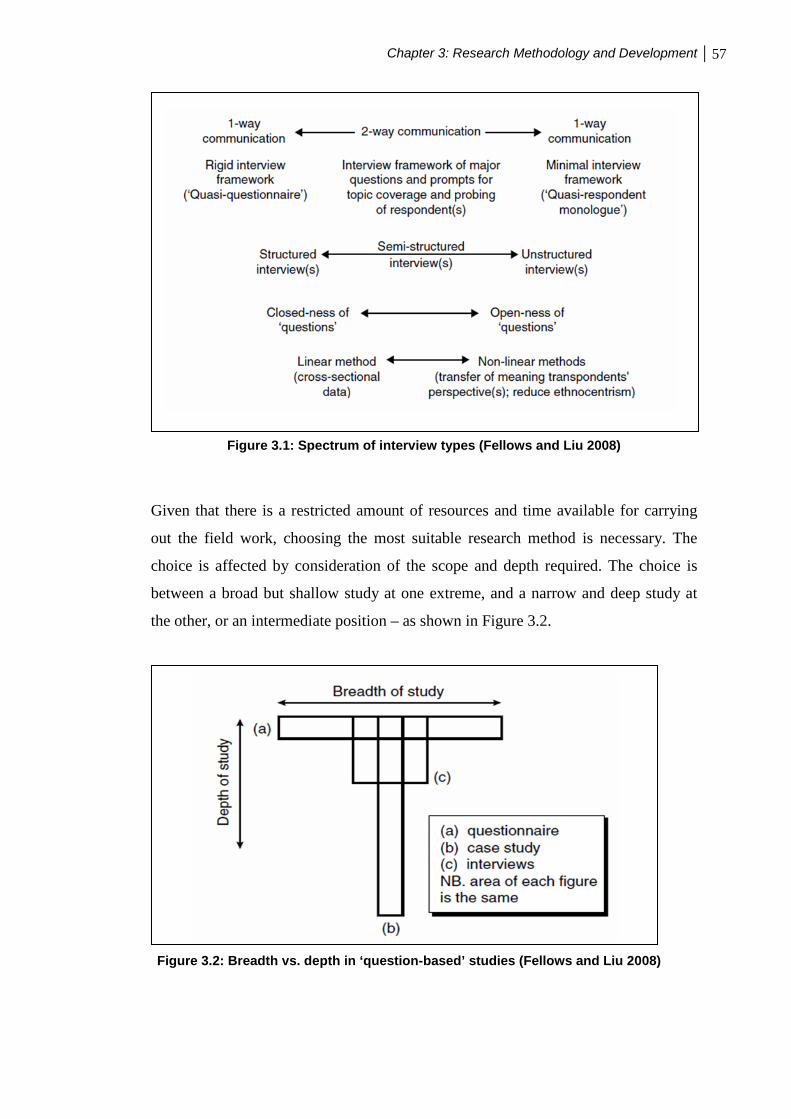

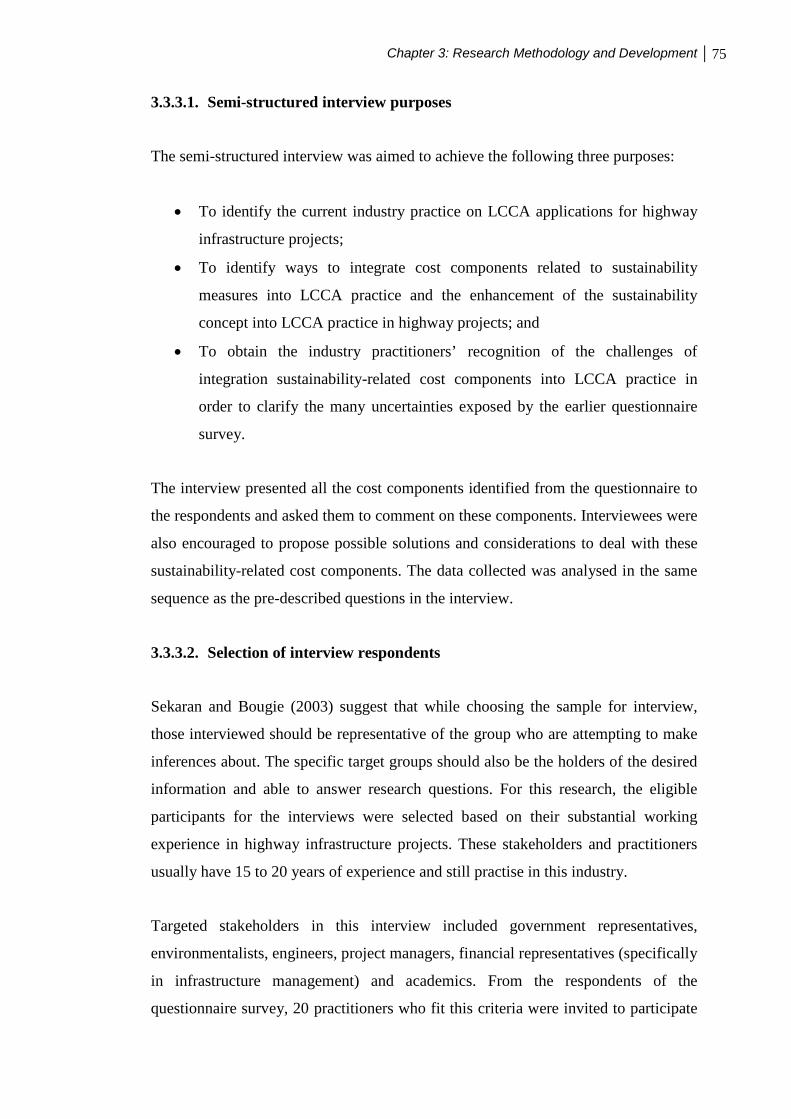

3.1 Introduction ................................................................................................. 553.2 Selection of Research Methods ................................................................... 56

3.2.1. Survey ................................................................................................... 583.2.2. Case study ............................................................................................ 59

3.3 Research Process ......................................................................................... 613.3.1. Literature review .................................................................................. 63

3.3.1.1. Literature review purposes ............................................................ 633.3.1.2. Literature review development ..................................................... 64

3.3.2. Questionnaire ....................................................................................... 653.3.2.1. Purposes of questionnaire ............................................................. 663.3.2.2. Selection of questionnaire respondents ......................................... 673.3.2.3. Questionnaire development .......................................................... 683.3.2.4. Data analysis ................................................................................. 70

3.3.3. Semi-structured interview .................................................................... 733.3.3.1. Semi-structured interview purposes .............................................. 753.3.3.2. Selection of interview respondents ............................................... 75

VII

3.3.3.3. Interview development ................................................................. 763.3.3.4. Data analysis ................................................................................. 78

3.3.4. Model Development ............................................................................. 793.3.5. Case Study ............................................................................................ 81

3.3.5.1. Case study purposes ...................................................................... 823.3.5.2. Selection of case projects .............................................................. 823.3.5.3. Case study development ............................................................... 843.3.5.4. Data analysis ................................................................................. 86

3.4 Ethical Considerations ................................................................................. 873.5 Chapter Summary ........................................................................................ 87

CHAPTER 4: COST IMPLICATIONS FOR HIGHWAY SUSTAINABILITY –

SURVEY STUDIES .................................................................................................. 89

4.1 Introduction ................................................................................................. 894.2 Profile of Respondents ................................................................................ 91

4.2.1 Respondents’ profiles - questionnaire survey ...................................... 914.2.2 Respondent’s profiles - semi-structured interview .............................. 94

4.3 Results and Findings ................................................................................... 954.3.1 Questionnaire survey results and findings ........................................... 95

4.3.1.1 Sustainability-related cost components: perspective of consultants …………………………………………………………………...96

4.3.1.2 Sustainability-related cost components: perspective of contractors …………………………………………………………………...98

4.3.1.3 Sustainability-related cost components: perspective of government agencies and local authorities ...................................................................... 1004.3.1.4 Integration of sustainability-related cost components in LCCA studies ………………………………………………………………….102

a. Agency category .......................................................................................... 104

b. Social category ............................................................................................. 105

c. Environmental category ............................................................................... 106

4.3.2 Summary of the questionnaire survey results and suggestions .......... 1074.3.3 Semi-structured interview results and findings .................................. 109

4.3.3.1. Current industry practice of LCCA application .......................... 1094.3.3.2. Ways to quantify cost related to sustainable measures ............... 1174.3.3.3. Challenges in integrating costs related to sustainable measures into LCCA practice ............................................................................................. 1204.3.3.4. Suggestions for enhancing sustainability in LCCA practice ...... 121

VIII

4.3.4 Summary of semi-structured interview results and suggestions ........ 1234.4 Chapter Summary ...................................................................................... 124

CHAPTER 5: A DECISION SUPPORT MODEL FOR EVALUATING

HIGHWAY INVESTMENT .................................................................................... 127

5.1 Introduction ............................................................................................... 1275.2 The Model Structure and Application ....................................................... 130

5.2.1. The model structure and development: stage 1 .................................. 1305.2.2. The model structure and development: stage 2 .................................. 132

5.3 The Fuzzy Analytical Hierarchy Process .................................................. 1335.3.1. Fundamentals of Fuzzy AHP ............................................................. 1355.3.2. Fuzzy AHP assessment procedure ..................................................... 136

5.4 Life-Cycle Cost Analysis ........................................................................... 1445.4.1. Life-cycle cost analysis in highway infrastructure ............................. 1445.4.2. LCCA calculation procedure .............................................................. 146

5.5 Final Decision Making Process ................................................................. 1495.6 Sensitivity Analysis ................................................................................... 1515.7 Chapter Summary ...................................................................................... 152

CHAPTER 6: MODEL APPLICATION THROUGH CASE STUDIES .......... 155

6.1 Introduction ............................................................................................... 1556.2 Selection of the Case Study Projects ......................................................... 157

6.2.1 Case study A: Wallaville bridge ..................................................... 1576.2.2 Case study B: Northam bypass ....................................................... 159

6.3 Significance of the Case Projects .............................................................. 1616.4 Model Application in Case Study A - Wallaville Bridge .......................... 162

6.4.1 Project alternatives ......................................................................... 1626.4.2 Fuzzy AHP for qualitative indicators ............................................. 163

6.4.2.1 Evaluation of criteria weight ................................................................ 163

6.4.2.2 Evaluation of alternatives ..................................................................... 166

6.4.2.3 Final scores of alternatives ................................................................... 169

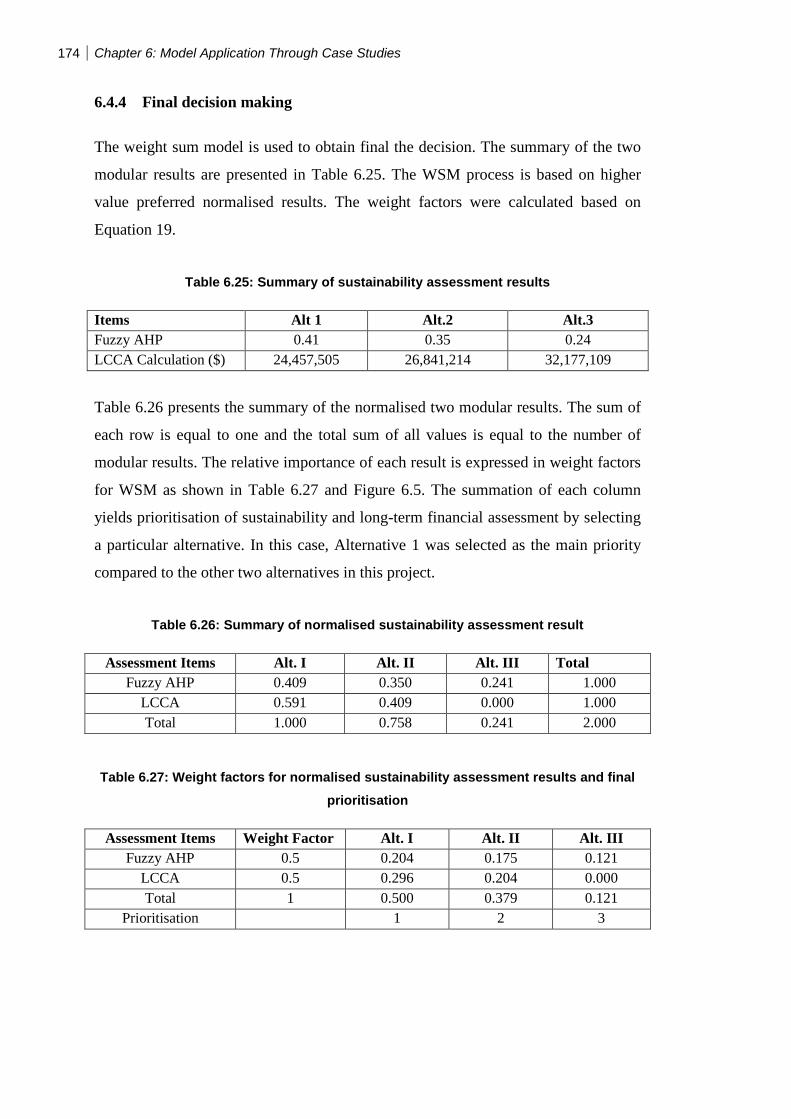

6.4.3 LCCA calculation for quantitative indicators ................................. 1716.4.4 Final decision making ..................................................................... 1746.4.5 Sensitivity analysis ......................................................................... 175

6.4.5.1 Sensitivity analysis for Fuzzy AHP ...................................................... 175

IX

6.4.5.2 Sensitivity analysis for LCCA ............................................................. 176

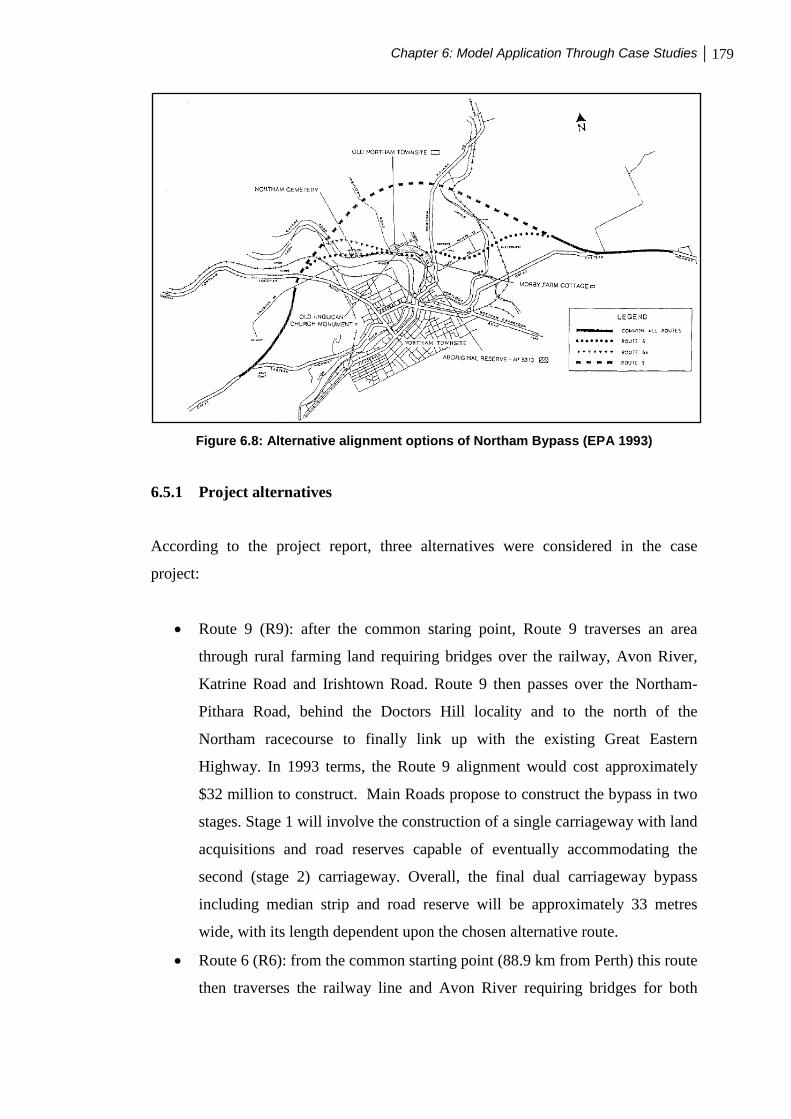

6.5 Model Application in Case Study B - Northam Bypass ............................ 1786.5.1 Project alternatives ......................................................................... 1796.5.2 Fuzzy AHP for qualitative indicators ............................................. 180

6.5.2.1 Evaluation of criteria weight ................................................................ 180

6.5.2.2 Evaluation of alternatives ..................................................................... 183

6.5.2.3 Final scores of alternatives ................................................................... 186

6.5.3 LCCA calculation for quantitative indicators ................................. 1876.5.4 Final decision making .................................................................... 1906.5.5 Sensitivity analysis ......................................................................... 191

6.5.5.1 Sensitivity analysis for Fuzzy AHP ..................................................... 192

6.5.5.2 Sensitivity analysis for LCCA ............................................................. 193

6.6 Summary of Model Application ................................................................ 1956.7 Validation of the Model ............................................................................ 1966.8 Chapter Summary ...................................................................................... 197

CHAPTER 7: FINDINGS AND MODEL FINALISATION ............................ 201

7.1 Introduction ............................................................................................... 2017.2 Synthesising Phases 1 to 4 for Interpretation and Discussion ................... 2027.3 Critical Sustainability-Related Cost Components ..................................... 203

7.3.1. Agency dimension of sustainability ................................................... 2047.3.2. Social dimension of sustainability ..................................................... 2057.3.3. Environmental dimension of sustainability ........................................ 205

7.4 Enhancement of LCCA for Sustainability Measures ................................ 2067.4.1. Industry practice of LCCA ................................................................. 2087.4.2. Challenges of incorporating sustainability into LCCA ...................... 210

7.5 Model Finalisation ..................................................................................... 2127.6 Chapter Summary ...................................................................................... 217

CHAPTER 8: CONCLUSION ........................................................................... 219

8.1 Introduction ............................................................................................... 2198.2 Review of Research Objectives and Development Processes ................... 2198.3 Research Objectives and Conclusions ....................................................... 220

8.3.1. Research objective 1 .......................................................................... 2208.3.2. Research objective 2 .......................................................................... 222

X

8.3.3. Research objective 3 ........................................................................... 2238.4 Research Contributions .............................................................................. 224

8.4.1. Contribution to academic knowledge ................................................. 2248.4.2. Contribution to the industry ............................................................... 225

8.5 Study Limitations ...................................................................................... 2258.6 Recommendations for Future Research ..................................................... 2268.7 Summary .................................................................................................... 227

REFERENCES ....................................................................................................... 229

APPENDIX A1: INVITATION LETTER-QUESTIONNAIRE ........................ 246

APPENDIX A2: SAMPLE OF QUESTIONNAIRE ........................................... 248

APPENDIX B1: INVITATION LETTER- SEMI-STRUCTURED INTERVIEW

.................................................................................................................................. 255

APPENDIX B2: SAMPLE OF CONSENT FORM ............................................ 257

APPENDIX B3: SAMPLE OF INTERVIEW ..................................................... 258

APPENDIX C1: INVITATION LETTER- FUZZY AHP QUESTIONNAIRE

.................................................................................................................................. 260

APPENDIX C2: SAMPLE OF FUZZY AHP QUESTIONNAIRE ................... 262

APPENDIX D: LIST OF PUBLICATIONS ........................................................ 266

XI

LIST OF ABBREVIATIONS

Austroads =

BCA

Association of Australian and New Zealand road transport and traffic authorities

= Benefit Cost Analysis BCR = Benefit Cost Ratio BTCE = BTRE

Bureau of Transport and Communications Economics = Bureau of Infrastructure, Transport and Regional Economics

Cal B/C = California Life-Cycle Benefit/ Cost CCP-PLUS = Cities for Climate Protection, Australia CCPTM = Cities for Climate ProtectionDEA

TM = Data envelopment analysis

FHWA

= Fuzzy AHP

Federal Highway Administration = Fuzzy Analytic Hierarchy Process

GEH = Great Eastern Highway HDM-4 = Highway Design and Maintenance Standards Model Version 4 HDM-III = Highway Design and Maintenance Standards Model Version III ISOHDM = International Study of Highway Development and Management IUCN = International Union for Conservation of Nature LCCA = Life-cycle cost analysis LCCOST = Pavement Life Cycle Cost Analysis Package LCCP = Life-cycle cost analysis program-Flexible Pavement LCCPR = Life-cycle cost analysis program-Rigid Pavement MCDM = Multi-Criteria Decision-Making PRLEAM = Pavement Rehabilitation Life-Cycle Economic Analysis QUT = Queensland University of Technology, Australia RTA = Road and Transport Authority, Australia UN = United Nations US = United States WCED = World Commission on Environment and Development WSM = Weighted Sum Model

XII

DEFINITION OF TERMS

For clearer understanding of the terms used in this research, the meanings are

extrapolates as follows:

Sustainable development – Sustainable development refers to a pattern of resource

use that aims to meet human needs while preserving the environment so that these

needs can be met not only in the present, but also for generations to come.

Life-cycle costing analysis (LCCA) - LCCA involves the analysis of the costs of a

highway infrastructure over its entire life span.

Long-term financial management – Long-term financial management means a long

term financial planning for entities providing services from infrastructure assets,

especially long lived (> 10 years) assets to assist these entities in managing service

delivery from infrastructure assets.

Cost component – Cost component involves sustainability-related cost elements

(quantifiable) and issues (qualitative), yet causing impacts to the environment,

society and economics.

Stakeholder – A stakeholder refers to a person, group, organisation, or system that

affects or can be affected by an organisation's actions.

XIII

LIST OF FIGURES

Figure 1.1: Variances leading to a sustainability-based life-cycle cost analysis model ...................................................................................................................................... 4

Figure 1.2: Structured infrastructure investment review process (DTF 2011) ............ 8Figure 1.3: Stage 1 - Developing a preliminary model .............................................. 10Figure 1.4: Stage 2 - Surveys development ............................................................... 11Figure 1.5: Stage 3 - Developing a decision support model ...................................... 12Figure 1.6: Research plan chart .................................................................................. 13Figure 2.1: Sustainability criteria for the transport sector (Basler and Partner 1998) 18Figure 2.2: UK sustainable development indicators (Bickel et al. 2003) .................. 19Figure 2.3: The three pillars of sustainable development (Koo 2007) ....................... 21Figure 2.4: Life-cycle costing procedure ................................................................... 27Figure 2.5: Typical life cycle of a road asset (Rouse and Chiu 2008) ....................... 43Figure 3.1: Spectrum of interview types (Fellows and Liu 2008) ............................. 57Figure 3.2: Breadth vs. depth in ‘question-based’ studies (Fellows and Liu 2008) ... 57Figure 3.3: Research process ..................................................................................... 62Figure 3.4: Questionnaire research flow chart (Statpac 1997) ................................... 66Figure 3.5: Case study process ................................................................................... 85Figure 4.1: Purpose of survey in overall research aim ............................................... 90Figure 4.2: Categories of respondent in questionnaire survey ................................... 92Figure 4.3: Respondents’ utilisation of LCCA in highway projects ........................ 110Figure 4.4: Types of data utilised by respondents in highway treatments ............... 115Figure 5.1: Integration of survey findings with model development ....................... 128Figure 5.2: Development of model based on research objectives and questions ..... 129Figure 5.3: Decision support model development process ...................................... 130Figure 5.4: Proposed assessment methods for the decision support model ............. 133Figure 5.5: Proposed application of the Fuzzy AHP ............................................... 134Figure 5.6: Hierarchy map of sustainability-related cost component assessment ... 137Figure 5.7: The linguistic scale of triangular numbers for relative importance ....... 138Figure 5.8: The intersection between C1 and C2 ..................................................... 142Figure 5.9: Timing of maintenance and rehabilitation ............................................. 144Figure 5.10: Agency costs associated with construction activities .......................... 145Figure 5.11: Social and environmental costs added to agency costs associated with construction activities ............................................................................................... 146Figure 6.1: Approach to model application and overall research aim ..................... 156Figure 6.2: Wallaville Bridge in flood (BTRE 2007a) ............................................ 158Figure 6.3: Tim Fischer Bridge (BTRE 2007a) ....................................................... 159Figure 6.4: Northam Bypass (BTRE 2007b) ............................................................ 161Figure 6.5: Final decision making by WSM ............................................................ 175Figure 6.6: Sensitivity analysis for Fuzzy AHP weight factor changes ................... 176Figure 6.7: Sensitivity analysis for LCCA weight factor changes ........................... 178Figure 6.8: Alternative alignment options of Northam Bypass (EPA 1993) ........... 179Figure 6.9: Final decision making by WSM ............................................................ 191Figure 6.10: Sensitivity analysis for Fuzzy AHP weight changes ........................... 193Figure 6.11: Sensitivity analysis for LCCA weight factor changes ......................... 194Figure 7.1: Critical sustainability-related cost components in Australian highway infrastructure projects ............................................................................................... 204

XIV

Figure 7.2: Platform for developing financial decision support model in highway infrastructure sustainability ...................................................................................... 213Figure 7.3: The finalised financial decision support model for highway infrastructure sustainability ............................................................................................................. 215

XV

LIST OF TABLES

Table 2.1: Differences between BCA and LCCA ...................................................... 28Table 2.2: Existing LCCA models and programs ...................................................... 33Table 2.3: Agency impacts and costs in highway projects ........................................ 43Table 2.4: Social impacts and costs in highway projects ........................................... 46Table 2.5: Environmental impacts and costs in highway projects ............................. 48Table 2.6: Sustainability-related cost components for highway infrastructure .......... 52Table 3.1: Characteristics of questions ...................................................................... 65Table 3.2: Stages and steps in model building (Richardson and Pugh, 1981) ........... 80Table 3.3: Case projects’ fulfillment of selection criteria .......................................... 83Table 4.1: Respondents’ roles in highway projects ................................................... 93Table 4.2: Respondents’ construction industry experience ....................................... 93Table 4.3: Consultants’ rating of sustainability-related cost components ................. 97Table 4.4: Contractors’ rating of sustainability-related cost components .................. 99Table 4.5: Government agencies and local authorities’ rating of sustainability-related cost components ....................................................................................................... 101Table 4.6: Perceptions of ‘importance level’ of cost components related to sustainable measures by industry stakeholders ........................................................ 103Table 4.7: Industry validated sustainability-related cost components in highway infrastructure ............................................................................................................ 108Table 4.8: Questions to identify current industry practice of LCCA ....................... 110Table 4.9: Relevant analysis period of LCCA ......................................................... 112Table 4.10: Maintenance treatments of highway infrastructure ............................... 113Table 4.11: Ways to quantify cost related to sustainable measures ......................... 118Table 4.12: Challenges to integrating costs related to sustainable measures into LCCA ....................................................................................................................... 120Table 4.13: Stakeholders’ suggestions for enhancing sustainability in LCCA ........ 122Table 4.14: Comparison of the survey results with literature findings .................... 125Table 5.1: Sustainability-related cost components for highway infrastructure ........ 131Table 5.2: Triangular fuzzy conversion scale .......................................................... 138Table 5.3: Assessment approach of critical sustainability cost components ........... 143Table 5.4: WSM calculation table for final decision making .................................. 150Table 6.1: The fuzzy evaluation matrix with respect to the goal ............................. 165Table 6.2: The relative importance of agency cost components .............................. 165Table 6.3: The relative importance of social cost components ................................ 165Table 6.4: The relative importance of environmental cost components .................. 165Table 6.5: Composite priority weights for sustainability-related cost components evaluation criteria ..................................................................................................... 167Table 6.6: Evaluation of the alternatives with respect to material costs .................. 167Table 6.7: Evaluation of the alternatives with respect to plant and equipment costs

.................................................................................................................................. 167Table 6.8: Evaluation of the alternatives with respect to major maintenance costs 167Table 6.9: Evaluation of the alternatives with respect to rehabilitation costs .......... 168Table 6.10: Evaluation of the alternatives with respect to road accident- internal costs

.................................................................................................................................. 168Table 6.11: Evaluation of the alternatives with respect to road accident- economic value of damage ....................................................................................................... 168Table 6.12: Evaluation of the alternatives with respect to hydrological impacts .... 168

XVI

Table 6.13: Evaluation of the alternatives with respect to loss of wetland .............. 168Table 6.14: Evaluation of the alternatives with respect to cost of barriers .............. 169Table 6.15: Evaluation of the alternatives with respect to disposal of material costs

.................................................................................................................................. 169Table 6.16: Priority weights of the alternatives with respect to agency aspects ...... 169Table 6.17: Priority weights of the alternatives with respect to social aspects ........ 170Table 6.18: Priority weights of the alternatives with respect to environmental aspects

.................................................................................................................................. 170Table 6.19: Final scores of the alternatives .............................................................. 170Table 6.20: Determination of activity timing ........................................................... 171Table 6.21: Estimated expenditures to keep old bridge open .................................. 172Table 6.22: Costs of agency and social category ..................................................... 173Table 6.23: Computation of expenditure by years ................................................... 173Table 6.24: Computation of life-cycle cost analysis ................................................ 173Table 6.25: Summary of sustainability assessment results ...................................... 174Table 6.26: Summary of normalised sustainability assessment result ..................... 174Table 6.27: Weight factors for normalised sustainability assessment results and final prioritisation ............................................................................................................. 174Table 6.28: Changes in prioritisation value by changing the Fuzzy AHP weight factors ....................................................................................................................... 176Table 6.29: Changes in prioritisation value by changing the LCC weight factors .. 177Table 6.30: The fuzzy evaluation matrix with respect to the goal ........................... 182Table 6.31: The relative importance of agency cost components ............................ 182Table 6.32: The relative importance of social cost components .............................. 182Table 6.33: The relative importance of environmental cost components ................ 182Table 6.34: Composite priority weights for sustainability-related cost components evaluation criteria ..................................................................................................... 183Table 6.35: Evaluation of the alternatives with respect to material costs ................ 184Table 6.36: Evaluation of the alternatives with respect to plant and equipment costs

.................................................................................................................................. 184Table 6.37: Evaluation of the alternatives with respect to major maintenance costs

.................................................................................................................................. 184Table 6.38: Evaluation of the alternatives with respect to rehabilitation costs ........ 184Table 6.39: Evaluation of the alternatives with respect to road accident- internal costs

.................................................................................................................................. 184Table 6.40: Evaluation of the alternatives with respect to road accident- economic value of damage ....................................................................................................... 185Table 6.41: Evaluation of the alternatives with respect to hydrological impacts .... 185Table 6.42: Evaluation of the alternatives with respect to loss of wetland .............. 185Table 6.43: Evaluation of the alternatives with respect to cost of barrier ................ 185Table 6.44: Evaluation of the alternatives with respect to disposal of material costs

.................................................................................................................................. 185Table 6.45: Priority weights of the alternatives with respect to agency aspects ...... 186Table 6.46: Priority weights of the alternatives with respect to social aspects ........ 186Table 6.47: Priority weights of the alternatives with respect to environmental aspects

.................................................................................................................................. 186Table 6.48: Final scores of the alternatives .............................................................. 187Table 6.49: Determination of activity timing ........................................................... 188Table 6.50: Costs of agency and social category ..................................................... 189Table 6.51: Computation of expenditure by years ................................................... 189

XVII

Table 6.52: Computation of life-cycle costs ............................................................ 189Table 6.53: Summary of weighted sum assessment results ..................................... 190Table 6.54: Summary of normalised weighted sum assessment results .................. 191Table 6.55: Weight factors for normalised weighted sum assessment results and final prioritisation ............................................................................................................. 191Table 6.56: Changes in prioritisation value by changing the Fuzzy AHP weight factors ....................................................................................................................... 192Table 6.57: Changes in prioritisation value by changing the Fuzzy AHP weight factors ....................................................................................................................... 194Table 6.58: Comparison of the case study results with literature and survey findings

.................................................................................................................................. 199

Chapter 1: Introduction 1

CHAPTER 1: INTRODUCTION

1.1 Research Background

Sustainable development has gained prominence over the last few decades across

various sectors including the construction industry (WCED 1987). In the

construction industry, the practice of sustainability has faced ongoing opportunities

and challenges in this period due to the globalisation of the business environment and

climate change, new materials and technologies, information and communication

technologies, and governance and regulation (Hampson and Brandon 2004).

For the business sector to embrace sustainable development, there is a need to create

increasing economic values while using natural resources sustainably and making a

broader contribution to the community’s social aims and objectives (Bourdeau 1999).

This change extends beyond the traditional concern of business, which is about

profitability and increasing shareholder value. Consequently, there is also a great of

need for tools to enable business to monitor, manage and report performance.

Sustainable development is about making societal investments that are sensitive to

the natural environment and at the same time financially viable in the long term. In

the construction industry, the development of a project from the client perspective

needs to be consistent with the benefits produced. Over a facility lifetime, there are

many opportunities to minimise the impacts of operations on natural environment.

Therefore, it is important to examine the sustainable approaches in its design,

construction, operation, maintenance and replacement or retirement. This study aims

to investigate the financial implication of sustainability measures in infrastructure

development, with a particular focus on highway construction.

Infrastructure development plays an important role in supporting society, the

economy and the environment. In Australia, the distribution of essential public

2 Chapter 1: Introduction

services for maintaining human life, especially in dense urban environments, is

heavily dependent on infrastructure systems. According to the Northern Economic

Triangle Infrastructure Plan 2007-2012, the Queensland State Government will

invest over 82 billion Australian dollars in the next 20 years, to fund transportation,

gas delivery and water recycling projects. Some of these projects are quite large,

requiring over a billion dollars each, and will make up almost 20 billion dollars of

the $82 billion as a whole (Queensland Government 2007). Such significant

investment warrants an examination of how infrastructure can become more

sustainable. For this purpose, numerous researchers and industry professionals have

put great effort into the development of criteria, tools, concepts and assessment

systems to improve infrastructure sustainability (Dasgupta and Tam 2005; Sahely,

Kennedy and Adams 2005; Ugwu et al. 2006a, 2006b).

Recently, a significant number of research projects were initiated to investigate

sustainability issues and the built environment in general. At the broader

international level, the issues discussed include environment and industrial ecology,

group decision-making (Seager and Theis 2004; Seager 2004), sustainability

assessment (Ugwu and Haupt 2007), multi-attribute decision analysis (Rogers,

Seager and Gardner 2004; Linkov et al. 2005; Anex and Focht 2002) and

environmental management systems (Gluch and Baumann 2004). Researchers have

investigated social dimensions and partnership (Fisher 2003) and risk analysis in

environmental decision-making (Rogers, Seager and Gardner 2004; Linkov et al.

2005).

Although the application of sustainability in built assets is beneficial, it often

involves major capital investment. Costs always become the impeding factor for

stakeholders when they contemplate sustainability initiatives. Thus, it is crucial to

balance the financial benefits with sustainability deliverables in highway

infrastructure development. The determination of costs is an important aspect of

decision-making and an essential part of the development process. Life-cycle cost

analysis (LCCA) is an economic assessment approach that can predict the costs of a

facility throughout its life span. It takes into account the time, the value of money

and reduces the flow of running costs over a period to a single current value or

present worth. Life-cycle costing is a management tool to be used periodically

Chapter 1: Introduction 3

throughout the economic life of the asset. It is based on the different options

available to determine the alternative with the lowest costs. According to List (2007),

life-cycle cost analysis helps to ensure that these objectives are achieved. Using

LCCA, decision-makers can evaluate competing initiatives and identify the most

sustainable growth path for common infrastructure. LCCA make it possible to deal

with the challenges of competing needs in selecting relevant allocations to spend on

health care, environmental impact mitigation, national defense, transportation, and a

wealth of other programs.

Most of research on life-cycle costing methods on buildings and infrastructure focus

on the economics of a construction project (Aye et al. 2000; List 2007). Little

attention has been paid to the application of the life-cycle costing methods in

evaluating the economic aspects of sustainability in construction projects (List 2007;

Madanu, Li and Abbas 2009; Swaffield and McDonald 2008). LCCA can become a

useful approach to managing the financial aspects of the asset while emphasising

sustainability in its service life. To achieve such a balance, the construction industry

needs to predict financial, social and environmental costs and benefits in the long-

term.

Hence, ideally, the principles of sustainability should be integrated into the LCCA

concept. This is, however, complicated by the difficulties of measuring cost

components related to sustainability and the inconsistencies in measurement

approaches. Previous studies have shown unclear boundaries and ambiguities in

identifying sustainability costs and impacts of highway development (Wilde,

Waalkes and Harrison 2001; List 2007; Kendall, Keoleian and Helfand 2008; Zhang,

Keoleian and Lepech 2008). Understandably, existing LCCA approaches tend to

omit social and environmental costs given that such costs are usually difficult to

measure and the values are often disputed. Worse still, these approaches also show a

large degree of variance in the estimation methods, which has resulted in a lack of

sustainable measures in current LCCA. Figure 1.1 illustrates the variances in

traditional LCCA estimation methods, pointing to the need for a sustainability-based

LCCA model.

4 Chapter 1: Introduction

Figure 1.1: Variances leading to a sustainability-based life-cycle cost analysis model

This phenomenon calls for a new decision support model capable of dealing with

sustainability-related cost components and assessing long-term financial

implications. Highway stakeholders need to appreciate such a level of decision

support and act upon sustainability challenges as well as opportunities.

1.2 Research Questions

Based on the background and impetus of the research, the following questions are

posed:

RQ 1. What are the sustainability measures that have cost implications for highway

projects?

It has been argued that the growing problems of monetary turnover among highway

infrastructure investors have become the main hindrance to pursuing sustainability.

To achieve long-term financial viability for highway projects, it is essential to

understand the development of life-cycle cost analysis and how this relates to the

principle of sustainability. Identification of sustainability-related cost components in

a highway project can help to promote critical thinking to fill the gap as shown above

in Figure 1.1.

Traditional LCCA model

Sustainability-based LCCA

model Research Gap

Inconsistent estimation methods in environmental and social costs calculation

Unclear boundaries in considering sustainability impacts

Difficult to quantify sustainability related cost components

Ambiguity in identifying relevant costs for LCCA in highway projects

Chapter 1: Introduction 5

RQ 2. What are the specific cost components relating to sustainability measures

about which highway project stakeholders feel most concerned?

It is recognised that the complex nature of sustainability and highway infrastructure

development often causes challenges in the pursuit of long-term financial viability.

To understand this complex nature, it is important to first understand current

highway industry practice and the development of life-cycle cost analysis. Suitable

actions are needed to cope with these challenges. Identification of cost components

related to sustainable measures provides the basis to assess tangible cost components

in long-term financial decisions at the project level. In this way also, the

understanding of the sustainability foci and the realisation in long-term financial

management for the highway project can be enhanced.

RQ 3. How can long-term financial viability of sustainability measures in highway

projects be assessed?

To facilitate a smooth and practical implementation of sustainability objectives at the

project level, the critical cost components need to be thoroughly dealt with

concerning real-life projects. The solutions to measure these components provide

project stakeholders with concrete actions they can apply in their efforts to pursue

and enhance the sustainability deliverables and financial practicality in highway

infrastructure projects.

1.3 Research Objectives

The aim of this research is to develop a decision support model for evaluating long-

term financial decisions relating to sustainability for highway projects. To achieve

the research aim, the three questions presented in Section 1.2 need to be answered by

the following objectives:

1. To understand the cost implications of pursuing sustainability in highway

projects. This involves:

• Understanding global initiatives on sustainable infrastructure development,

6 Chapter 1: Introduction

• Understanding the context of highway infrastructure development in Australia,

• Reviewing the current LCCA model and programs on highway infrastructure,

and

• Identifying the sustainability-related cost components in highway infrastructure

projects.

2. To identify the critical cost components related to sustainable measures in

highway infrastructure investments. This involves:

• Exploring the different perceptions and expectations of various stakeholders

regardless of the current practice of life-cycle cost analysis in Australian

highway infrastructure,

• Identifying the cost components that are significant in highway infrastructure

investments, and

• Integrating the expectations of the various stakeholders that are suitable for

long-term financial management.

3. To develop a decision support model for the evaluation of long-term financial

decisions regarding sustainability for highway projects. This involves:

• Compiling the industry verified cost components into existing LCCA models

for further development,

• Developing financial decision support model for highway infrastructure

sustainability, and

• Testing and evaluating the decision support model based on the real-life

projects.

1.4 Significance of the Research

As highway infrastructure projects involve large resources and mechanisms,

financial stress is a significant challenge for investors. The concept of sustainability

is gaining popularity in the construction industry and this means achieving

sustainability not only on environmental and social scales, but also through economic

Chapter 1: Introduction 7

responsibility. While the sustainability concept is being emphasised in highway

infrastructure, effective financial management is crucial as highway funding at all

levels of government continues to fall short of infrastructure needs. As a result,

investors’ decisions based on experience are not performing as well, as promised

while managers are under great obligation to optimise society investments as well as

sustainability deliverables at the project level.

This study seeks to add to the existing body of knowledge by filling the gap between

sustainable development and long-term financial management in the context of

highway infrastructure. The data collected is an asset to knowledge in this area. The

research findings serve as the guidelines to encourage sustainability and long-term

financial management strategies for stakeholders. This result may directly or

indirectly contribute to measurable benefits in the form of cost efficiency, better

product quality and utility.

This study also seeks to develop a decision support model for evaluating long-term

financial management in Australian highway infrastructure. The expected model

aims to serve as a decision-making tool to aid in highway infrastructure investments.

It is also anticipated that the model may assist the stakeholders through increased

understanding of the importance of sustainability concepts and long-term financial

management in highway infrastructure. This understanding can lead to improve

competitiveness in construction markets.

1.5 Scope and Delimitation

This study was delimited to the development of a decision support model aimed at

improving long-term financial decisions in highway investment. “Delimitations” are

within the control of the researcher. The identified delimitations are discussed as

follows:

• The attention of this study is directed at public-sector evaluation in general,

and more especially with respect to highway infrastructure. The data are

collected from industry stakeholders involved in highway infrastructure

projects. The result could be generalised for the highway infrastructure

8 Chapter 1: Introduction

industry, but some of the identified factors may vary and not be relevant for

other infrastructures. Further improvements are necessary for application on

specific types of infrastructure.

• Research data was collected from the Australian highway infrastructure

industry, and the results are applicable to Australia only.

• This study is focused on the highway investment decisions in a financial

perspective. Due to the infrastructure investment involved several stages of

reviewing, this study is concentrating on the business case and budget

committee consideration (Point 3 and 4) as shown in Figure 1.2. The highway

investment decisions need to appropriately meet the needs of the community,

have been appropriately planned and are based on reliable cost estimates.

• The strategic assessment and options analysis as shown in Figure 1.2 includes

several criteria such as risk and sustainability benefits are part of key issues in

strategic assessment. Even though both issues are crucial in considering

project investment decisions, this study focuses purely on the financial

implication for highway infrastructure sustainability. This study aims to

provide the decision makers with a systematic project proposal and identify

the preferred selection for highway investment decisions.

Investment Concept Outline

Strategic Assessment and Option Analysis

Business Case

Budget Committee

Consideration

Interim Project Review

Post Implementation

review

Point 1 Point 2 Point 3 Point 4 Point 5 Point 6

Reason for

project proposal

Relationship to government’s

policy priorities

Benefits/ outcomes

to be achieved

Delivery Alternatives

Project Management

External conditions and critical success

Risk

Stakeholder analysis

Project proposal

cost

Market research

Timeline

Financial Implication

Figure 1.2: Structured infrastructure investment review process (DTF 2011)

Chapter 1: Introduction 9

1.6 Research Framework

A research framework is a systematic structure that helps to coordinate a research

project and ensures the efficient use of resources and to guide the researcher in the

use of suitable research methods through logical stages. It shows a broad picture to

the researchers to help to refine a clear connection between all the stages (King,

Keohane and Verba 1994). The probability of success in a research project is greatly

enhanced when the “beginning” is correctly defined as an accurate statement of goals

and justification. Having accomplished this, it is easier to identify and organise the

sequential steps necessary for writing a research framework and then successfully

executing a research project. This procedure creates a greater understanding of

problems or hypotheses, and makes practical applications through theories,

questioning and reasoning to achieve the research objectives, with the hope to

produce some new knowledge.

For the purpose of this study, the research framework was based on three stages to

answer the research objectives. Each of the stages is described in the following sub-

sections.

1.6.1 Stage 1 - Developing a preliminary model

This stage involves a literature review to explore the scope and issues in

sustainability-related cost components in highway construction. A preliminary model

is developed according to the sustainability-related cost components identified

through previous research and Australian project reports. Imperative aspects of the

cost components are identified and tabulated according to their significance before

incorporating these into the questionnaire for industry verification.

10 Chapter 1: Introduction

A summary of the Stage 1 is shown in Figure 1.3.

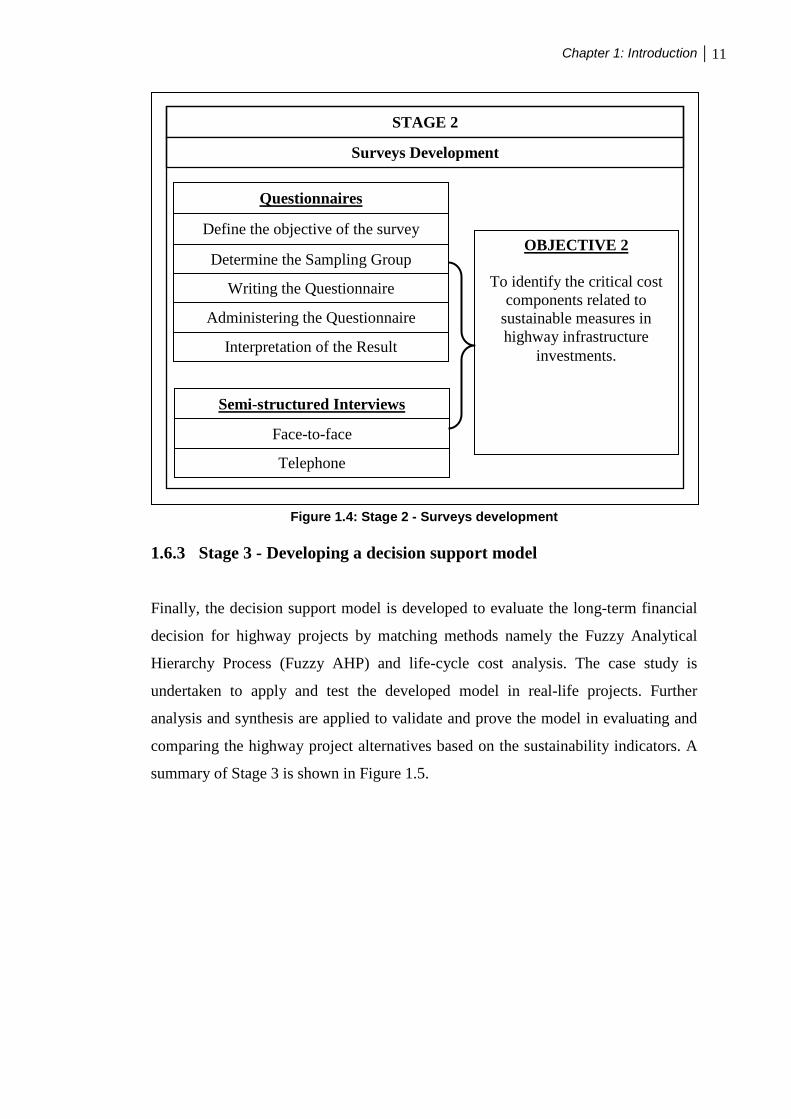

1.6.2 Stage 2 - Developing the survey

The focus of this research is on the stakeholders in highway infrastructure as the

primary respondents in of the surveys. Questionnaire surveys and semi-structured

interviews are conducted with the industry stakeholders. Questionnaire surveys are

administered to identify the cost components related to sustainable measures that are

significant in highway infrastructure investments. Semi-structured interviews are

conducted to have a better understanding of current highway industry practice in

long-term financial management. Both methods reveal the facts for the second

objective, which is to identify the critical cost components related to sustainable

measures in highway infrastructure investments. A summary of Stage 2 is shown in

Figure 1.4.

STAGE 1

Preliminary Model

Reviewing the Literature

Defining the Topic

Identify Source of Information

Keeping Records

Reading and Taking Notes

OBJECTIVE 1

To understand the costs implication of pursuing

sustainability in highway projects

Figure 1.3: Stage 1 - Developing a preliminary model

Chapter 1: Introduction 11

1.6.3 Stage 3 - Developing a decision support model

Finally, the decision support model is developed to evaluate the long-term financial

decision for highway projects by matching methods namely the Fuzzy Analytical

Hierarchy Process (Fuzzy AHP) and life-cycle cost analysis. The case study is

undertaken to apply and test the developed model in real-life projects. Further

analysis and synthesis are applied to validate and prove the model in evaluating and

comparing the highway project alternatives based on the sustainability indicators. A

summary of Stage 3 is shown in Figure 1.5.

STAGE 2

Surveys Development

Define the objective of the survey

Writing the Questionnaire

Interpretation of the Result

Determine the Sampling Group

Administering the Questionnaire

Questionnaires

Face-to-face

Telephone

Semi-structured Interviews

OBJECTIVE 2

To identify the critical cost components related to

sustainable measures in highway infrastructure

investments.

Figure 1.4: Stage 2 - Surveys development

12 Chapter 1: Introduction

Generally, a research framework follows certain structural stages and processes.

Each stage represents different methodologies to achieve the research objectives. In

this research, all possible methods and strategies were carefully considered before

choosing the most appropriate one. The quantitative and qualitative data is processed

and analysed using computer-assisted tools to derive meaningful results. The

implementation of the key research methodologies assists in defining appropriate

processes to answer the research questions as well as the aim. The research

framework shows the overall research design procedure, and is illustrated in Figure

1.6.

STAGE 3

Matching Methods

OBJECTIVE 3

To develop a decision support model for the evaluation of long-term financial decision for highway projects.

Case Study

Decision Support Model

Fuzzy Analytical Hierarchy Process (Fuzzy AHP)

Life-Cycle Cost Analysis (LCCA)

Figure 1.5: Stage 3 - Developing a decision support model

Chapter 1: Introduction 13

Figure 1.6: Research plan chart

Dat

a C

olle

ctio

n A

naly

sis

Res

ult

Lite

ratu

re R

evie

w

Industrial Feedback

Literature Review

Research Problems

Methodological Approach

Consultation with academics

Research Objectives

Industrial Feedback

Conclusions, Recommendations and Further Studies

Survey • Questionnaire-based survey based on the

literature review and preliminary model building

• Identify the cost components in LCCA that emphasise sustainability

• Semi-structured interviews undertaken to identify current industry practice of LCCA in highway infrastructure

Case Study • Apply and test the developed model in real-life

projects • Evaluate and validate the model

Research Analysis and Findings

Literature Review & Preliminary Model Development

• Refine traditional life-cycle cost analysis model.

• Identify sustainability-related cost components

Research Question Hypotheses Statements

Quantitative Method Quantitative Method

Model Development • Develop decision support model that

emphasise the sustainability context.

Stage 1

Stage 2

Stage 3

14 Chapter 1: Introduction

1.7 Thesis Organisation

This dissertation consists of nine chapters. A brief summary of each is outlined as

follows.

Chapter 1 comprises the introductory section that develops the direction of this

investigation. It also states the research background, problems and objectives; and

provides a brief discussion of the methodology and the thesis organisation.

Chapter 2 summarises the current state of knowledge by addressing the relevant

literature. Areas covered in this chapter include sustainable development principles

and the evolution of highway infrastructure development in Australia. The literature

review also covers the long-term financial management in highway development

which includes the principles of long-term financial management, application of

LCCA in highway projects, development of the LCCA models and programs, and the

limitation of existing LCCA studies regarding sustainability. Literature on the

responses to the sustainability challenge and cost implication in highway

infrastructure is also surveyed. Overall, this chapter identifies the research gap,

which justifies the need for this study.

Chapter 3 describes the research methodology in detail including: the research

methodology; data collection methods (namely questionnaire, interview, model

development and case studies); research information; selection of participants and

case projects; research instrumentation; data analysis and validation of results; and,

finally, guideline formulation.

Chapter 4 describes the data analysis and results of the questionnaire and semi-

structured interview. Questionnaire feedback is presented and the results tabulated in

order to answer the research questions. Sustainability-related cost components are

identified and conclusions are drawn. The data analysis and findings of the interview

results illustrate the understanding on the current industry practise of long-term

financial management in highway infrastructure. In addition, potential issues

hindering the integration of sustainability into LCCA are identified. Their conceptual

solutions are also recognised.

Chapter 1: Introduction 15

Chapter 5 discusses the development of a decision support model to aid stakeholders

in highway investment. This section explains the development of the model by using

one of the multi-criteria decision support approaches, Fuzzy analytical hierarchy

process (Fuzzy AHP) and integration with the traditional LCCA concept. The model

will then be tested and evaluated by industry stakeholders in real-life highway

infrastructure projects.

Chapter 6 introduces the case projects, their significance to the research, and the

profile of interviewees, before case studies are undertaken to demonstrate the model

application and justify the specific cost components in long-term financial

management towards sustainable highway infrastructure.

Chapter 7 discusses the results of the questionnaire and the interview. Subsequently,

based on the case studies, the ultimate research findings are presented in the form of

a model.

Chapter 8 reviews the research objectives and development processes; and offers

conclusions with regard to the research outcomes based on the respective research

questions, the contributions to the body of knowledge and its implications for both

the research community and the highway infrastructure industry. Finally,

recommendations for future research are proposed.

1.8 Chapter Summary

This chapter lays the foundation for the thesis. It first introduces the research

background and points to the current crux of the issue in sustainability and long-term

financial management in highway infrastructure development before presenting the

research problems and its objectives. Next, the research significance is identified

before the research scope and delimitation are drawn. Finally, the research

framework is briefly discussed, and the thesis organisation is also outlined. On this

basis, the study proceeds with a detailed description of the research and development

processes.

Chapter 2: Literature Review 17

CHAPTER 2: LITERATURE REVIEW

2.1 Introduction

This chapter presents the current state of knowledge by reviewing the literature

relevant to the research objectives set out in Section 1.3. Apart from establishing the

depth and breadth of the existing body of knowledge in the area of sustainability and

highway infrastructure development, the literature review serves to understand the

cost implications of pursuing sustainability in highway projects, thus paving the way

for questionnaires and interviews in a subsequent stage.

To begin with, the following sections present the sustainable development principles

before discussing the dynamics and application of sustainability in highway

infrastructure development generally. This is followed with an overview of the

current Australian construction industry and highway infrastructure practice. Long-

term financial management in highway infrastructure development is highlighted.

Principle of long-term financial management in highway development and the

application of life-cycle cost analysis (LCCA) in highway projects are specifically

discussed. A thorough review of current life-cycle cost analysis models and

programs in highway development, the limitation of existing LCCA studies in

adopting sustainability and the types of cost components related to sustainability

measures in the project was undertaken. Premised on these discussions, the research

gap in this research is identified, which leads to the formation of the research

questions.

2.2 Sustainability and Transport

There is an increasing demand for transport and mobility in our society. At the same

time, a desire for a clean environment, preservation of nature and concern for the

welfare of future generations is also progressively salient. Policymakers must

18 Chapter 2: Literature Review

accommodate these conflicting desires in order to balance the positive and negative

impacts of transport infrastructure.

Several research projects have been carried out to investigate a variety of topics

related to sustainability and transport. Jonsson (2008) implemented an appraisal

framework in the transportation system where the main elements of sustainability are

taken into account. In Jonsson’s study, an appraisal framework was developed to

analyse and measure the achievement of sustainability in the transport sector.

Gudmundsson (1999) found that sustainability indicators are “selected, targeted, and

compressed variables that reflect public concerns and are of use to decision-makers”.

These indicators are based on a selection of literature on social, environmental,

health and sustainability factors.

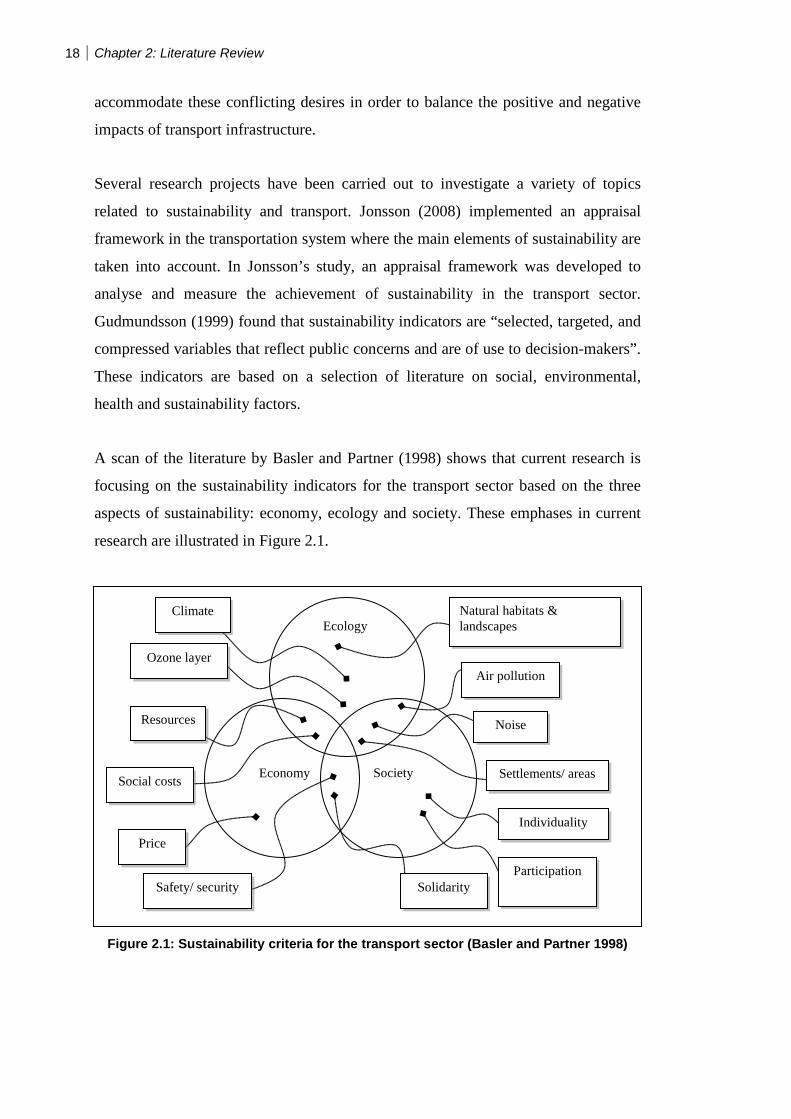

A scan of the literature by Basler and Partner (1998) shows that current research is

focusing on the sustainability indicators for the transport sector based on the three

aspects of sustainability: economy, ecology and society. These emphases in current

research are illustrated in Figure 2.1.

Figure 2.1: Sustainability criteria for the transport sector (Basler and Partner 1998)

Natural habitats & landscapes

Air pollution

Noise

Settlements/ areas Society

Individuality

Participation

Ecology

Economy

Solidarity Safety/ security

Price

Social costs

Ozone layer

Climate

Resources

Chapter 2: Literature Review 19

Furthermore, a set of transport indicators developed by Bickel et al. (2003) provides

an overview of key sustainable development issues at the UK level as shown in

Figure 2.2.

Figure 2.2: UK sustainable development indicators (Bickel et al. 2003)

The International Council for Local Environmental Initiatives - Australia/New

Zealand has collaborated with the Australian Greenhouse Office and the Victorian

Health Promotion Foundation to deliver a resource package of tools, case studies and

financial assistance to local governments that are Cities for Climate Protection™

(CCP™) participants around Australia through the Sustainable Transport initiative.

The aim of the initiative is to accelerate the implementation of sustainable transport

systems and to demonstrate the strong and multiple benefits that arise from

implementing these actions (CCP-PLUS 2005). These indicators show that

sustainability plays an important role in the development of a transport project. In the

following sub-sections, the evolution of sustainable development principles and the

practice of highway infrastructure development in Australia are introduced, before

A SUSTAINABLE ECONOMY - Social investment as a percentage of GDP - Consumer expenditure - Energy efficiency of road passenger travel - Average fuel consumption of new cars - Sustainable tourism - Leisure trips by mode of transport - Overseas travel - Freight transport by mode - Heavy goods vehicle mileage intensity BUILDING SUSTAINABLE COMMUNITIES - Road traffic (headline) - Passenger travel by mode - How children get to school - Average journey length by purpose - Traffic congestion - Distance travelled relative to income - People finding access difficult - Access to services in rural areas - Access for disabled people - New retail floor space in town centres and

out of town - Noise levels

MANAGING THE ENVIRONMENT AND RESOURCES - Carbon dioxide emissions by end

user • Transport • Non-transport

- Concentrations of selected air pollutants • NO2, SO2, CC, Particulates • Ozone

- Emissions of selected air pollutants • CO • NOx • Particulates

- Sulphur dioxide and nitrogen oxides emissions

SENDING THE RIGHT SIGNALS - Prices of key resources fuel

• Petrol/diesel • Industrial/domestic

- Real changes in the cost of transport - Public understanding and awareness

Individual action for sustainable development

20 Chapter 2: Literature Review

integrating both to set the scene to show the importance of sustainability in highway

infrastructure development.

2.2.1 Sustainable development principles and evolution

In the construction context, a definition of sustainability is suggested in the following

exposition:

The built environment provides a synthesis of environmental, economic and

social issues. It provides shelter for the individual, physical infrastructure for

communities and is a significant part of the economy. Its design sets the pattern

for resource consumption over its relatively long lifetime. (Prasad and Hall

2004)

Such an approach relates to the concept of sustainability to the concept of sustainable

development. These two terms are often used interchangeably, and it is worthwhile

to clarify the relationship of these two terms.

“Sustainable development is defined as “a development that meets the needs of the

present without compromising the ability of future generations to meet their own

needs” (WCED 1987). According to this definition from the World Commission on

Environment and Development, the underlying philosophy of sustainable

development is restraining the use of natural resources and materials to keep enough

for future generations to fulfill their own ambitions of living standards. In fact, the

main concerns of the contemporary construction industry are ecological impact,

economic development, and societal equity when considering sustainable

development.

Even though this definition leaves much to argue about, it is the basis for most work

on sustainable development. Koo et al. (2007) demonstrate the general concept of

sustainable development in three major aspects, namely, economic, environmental,

and social aspects. These aspects need to be considered, incorporated, and improved

to achieve a desired level of sustainable development. These aspects are illustrated as

the three pillars of sustainable development in Figure 2.3.

Chapter 2: Literature Review 21

On the other hand, the built environment represents one of the main supports

(infrastructure, buildings) of economic development, and its construction has

significant impacts on resources (land, materials, energy, water, human and social

capital) and on the living and working environment.

Hence, the current established concept of sustainable development gives rise to many

issues regarding the physical resources required for human existence and overall

quality of life for both present and future generations. A comprehensive plan of

action, including sustainable development in the construction area, is set out in

Agenda 21, which was an outcome of the 1992 United Nations Conference on

Environment and Development. The Johannesburg Plan of Implementation, agreed at

the Earth Summit 2002, affirmed UN commitment to ‘full implementation’ of

Agenda 21. It functions as a fundamental guideline to define sustainability in many

areas, including the construction industry.

To appropriately define sustainability in the construction industry, the term

`sustainable construction’ was proposed to describe the responsibility of the

construction industry in attaining sustainability. Kibert (1994) explained that a major

FUTURE/ PRESENT GENERATION

ENHANCEMENT OF SUSTAINABILITY BY CONSIDERING THREE PILARS

ECO

NO

MY

ENV

IRO

NM

ENT

SOC

IETY

ENHANCEMENT OF SUSTAINABILITY BY CONSIDERING THREE PILARS

ECO

NO

MY

ENV

IRO

NM

ENT

SOC

IETY