Enlargement of the European Union: Three Years Later

Susan SchadlerEuropean DepartmentInternational Monetary Fund

EU enlargement has succeeded on three fronts

1. Absorption of EU transfers

Rising use of EU Funds helps sustain consumption, investment in new

membersCE4: Gross Inflow of EU Funds 2004-06 (percent of GDP)

Source: National authorities, European Commission, IMF staff estimates.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Czech Rep. Slovenia Slovakia Poland Hungary Estonia Lithuania Latvia

2004 2005 2006

EU enlargement has succeeded on three fronts

1. Rising use of EU funds

2. High and steady trade growth

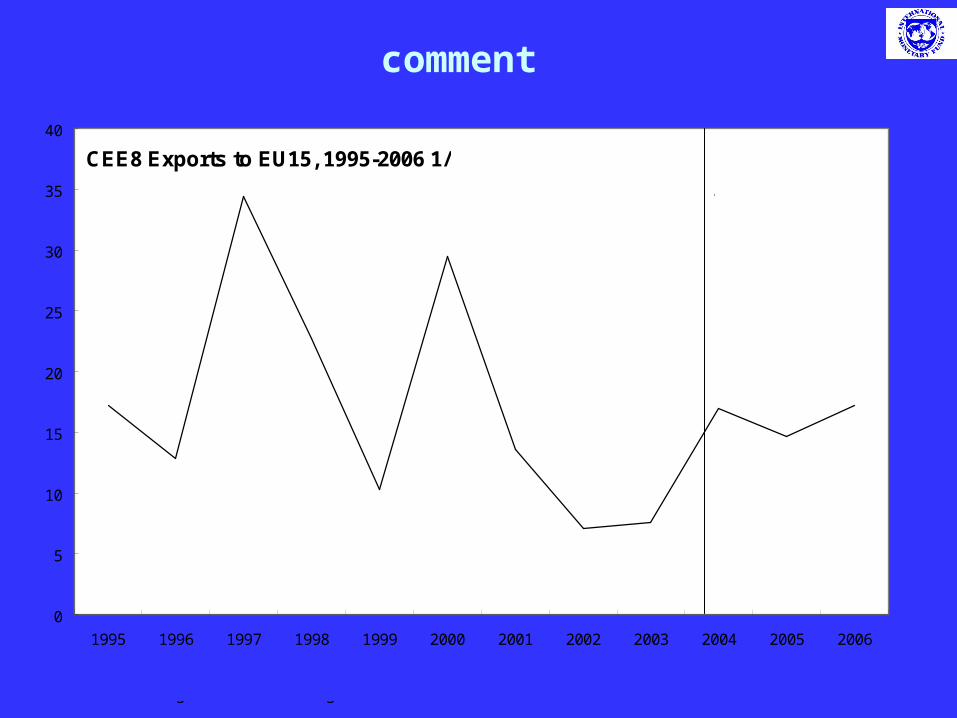

Sustained high export growth from CE8 to EU15

CEE8 Exports to EU15, 1995-2006 1/

0

5

10

15

20

25

30

35

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Excluding Belgium and Luxembourg.

(Annual Percent Change)

pre-enlargement post-enlargement

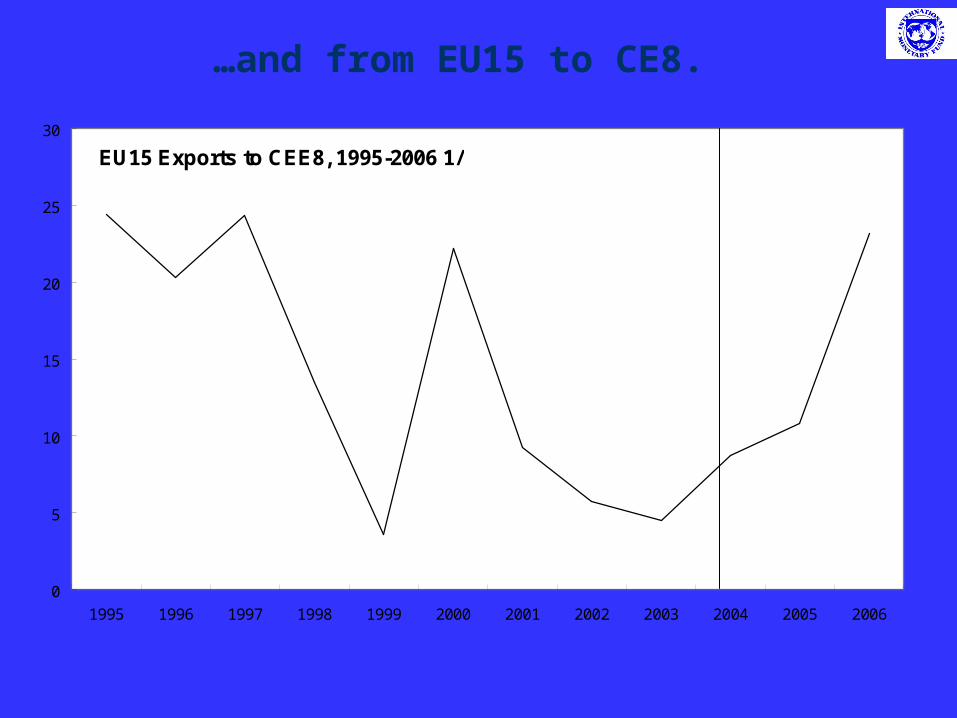

…and from EU15 to CE8.

EU15 Exports to CEE8, 1995-2006 1/

0

5

10

15

20

25

30

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Excluding Belgium and Luxembourg.

(Annual Percent Change)

pre-enlargement post-enlargement

EU enlargement has succeeded on three fronts

1. Rising use of EU funds

2. High and steady trade growth

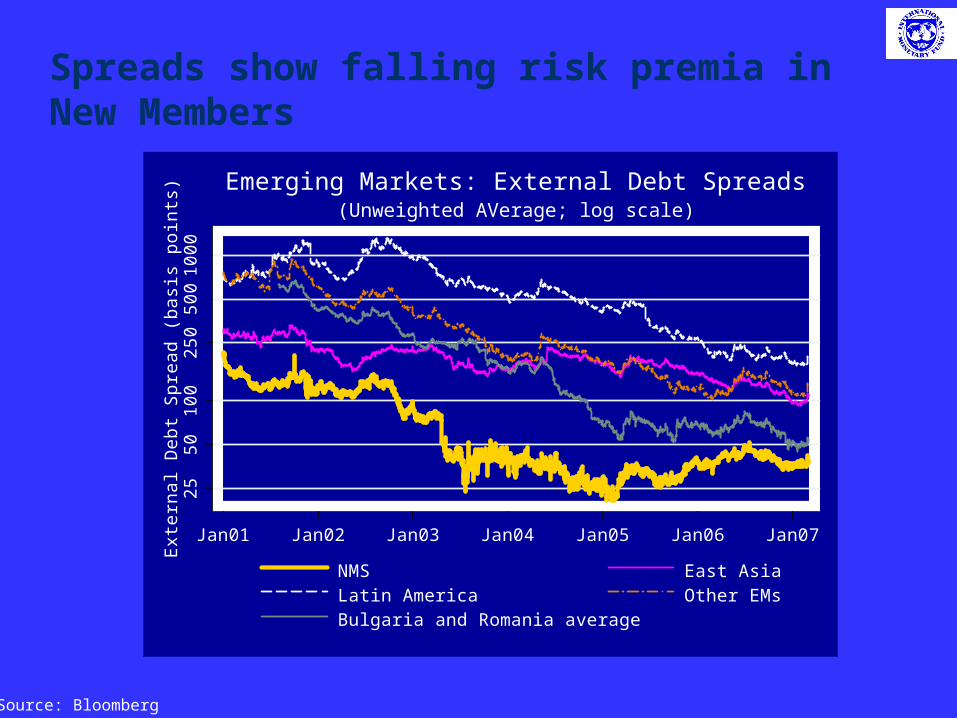

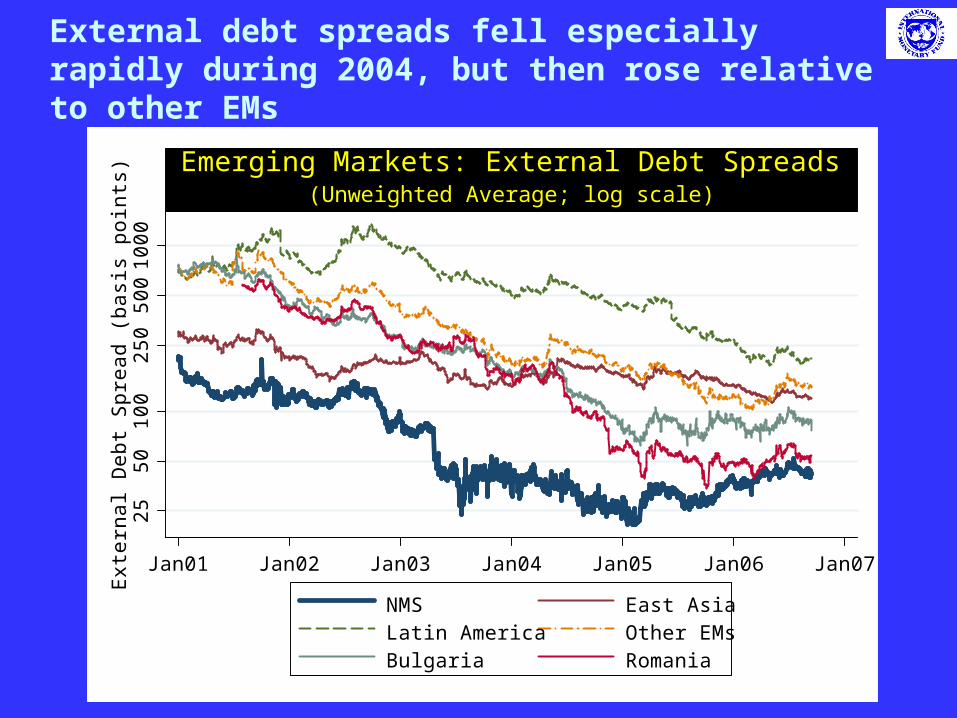

3. Financial market integration

Spreads show falling risk premia in New Members

Source: Bloomberg

2550

100

250

500

1000

Ext

erna

l Deb

t Spr

ead

(bas

is p

oint

s)

Jan01 Jan02 Jan03 Jan04 Jan05 Jan06 Jan07

NMS East AsiaLatin America Other EMsBulgaria and Romania average

(Unweighted AVerage; log scale)Emerging Markets: External Debt Spreads

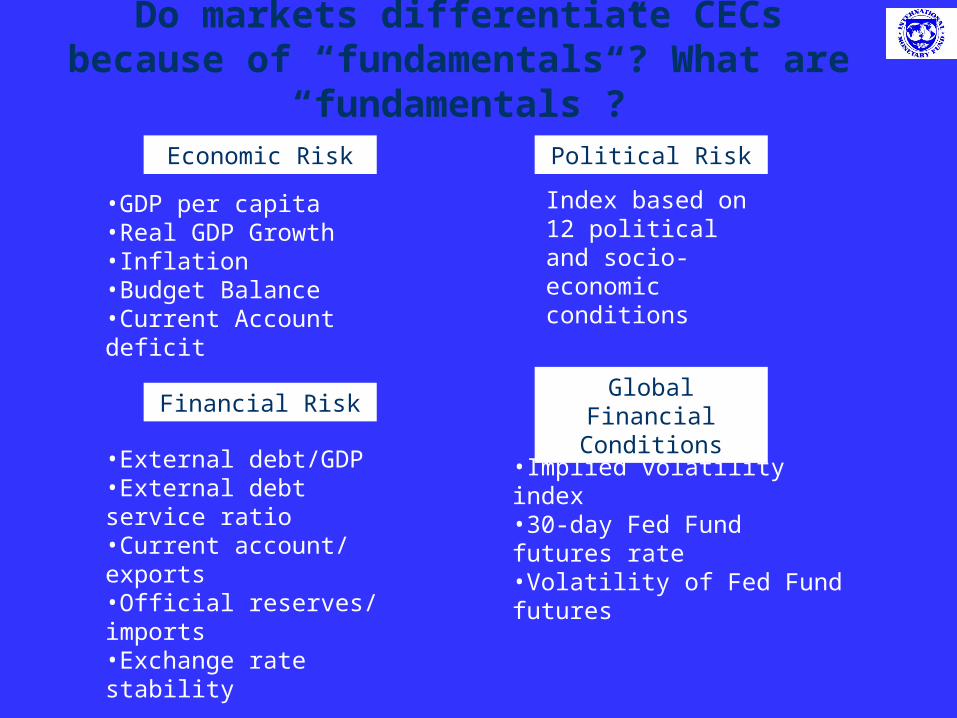

Do markets differentiate CECs because of “fundamentals”? What are

“fundamentals”?Economic Risk

•GDP per capita•Real GDP Growth•Inflation•Budget Balance•Current Account deficit

Political Risk

Index based on 12 political and socio-economic conditions

Financial Risk

•External debt/GDP•External debt service ratio•Current account/ exports•Official reserves/ imports•Exchange rate stability

Global Financial Conditions

•Implied volatility index•30-day Fed Fund futures rate•Volatility of Fed Fund futures

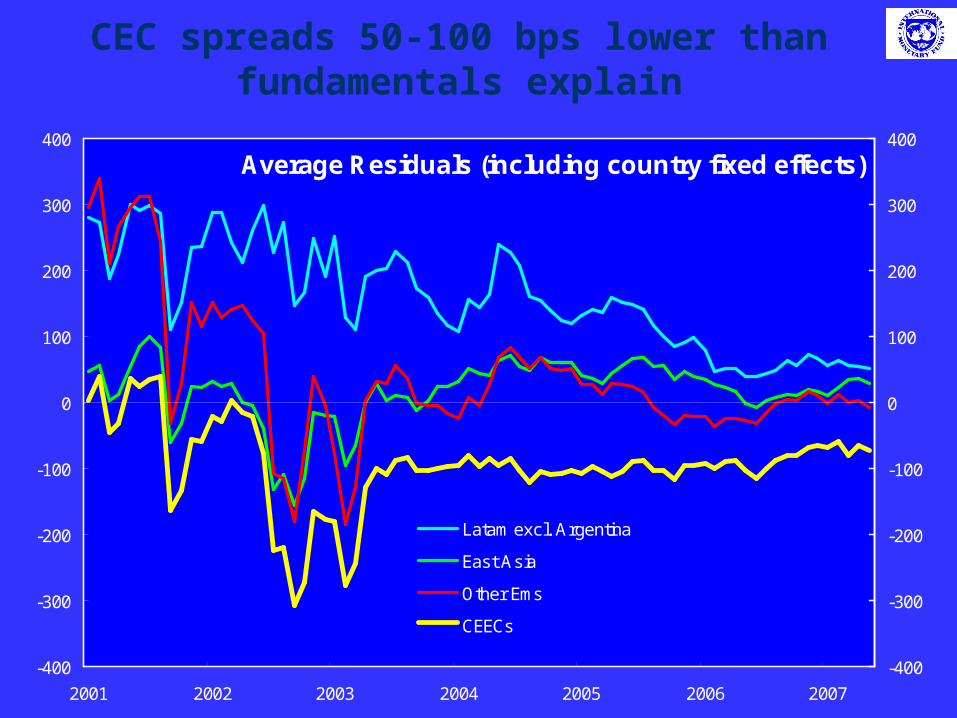

CEC spreads 50-100 bps lower than fundamentals explain

Average Residuals (including country fixed effects)

-400

-300

-200

-100

0

100

200

300

400

2001 2002 2003 2004 2005 2006 2007

-400

-300

-200

-100

0

100

200

300

400

Latam excl. Argentina

East Asia

Other Ems

CEECs(in basis points)

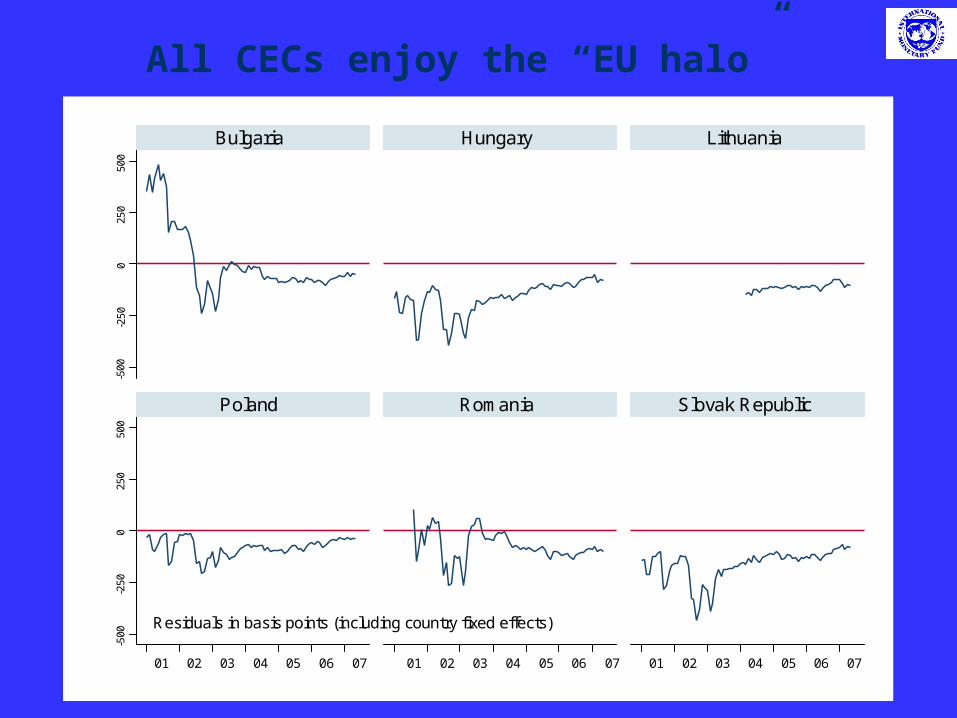

All CECs enjoy the “EU halo”-5

00-2

500

250

500

-500

-250

025

050

0

01 02 03 04 05 06 07 01 02 03 04 05 06 07 01 02 03 04 05 06 07

Bulgaria Hungary Lithuania

Poland Romania Slovak Republic

Residuals in basis points (including country fixed effects)

-500

-250

025

050

0-5

00-2

500

250

500

01 02 03 04 05 06 07 01 02 03 04 05 06 07 01 02 03 04 05 06 07

Bulgaria Hungary Lithuania

Poland Romania Slovak Republic

-500

-250

025

050

0-5

00-2

500

250

500

01 02 03 04 05 06 07 01 02 03 04 05 06 07 01 02 03 04 05 06 07

Bulgaria Hungary Lithuania

Poland Romania Slovak Republic

Residuals in basis points (including country fixed effects)

Real convergence is picking up

Yearly Growth of GDP per capita

0

2

4

6

8

10

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007projection

Source: WEO, IMF.

(In percent)

Euro area

CEE8

pre-enlargement post-enlargement

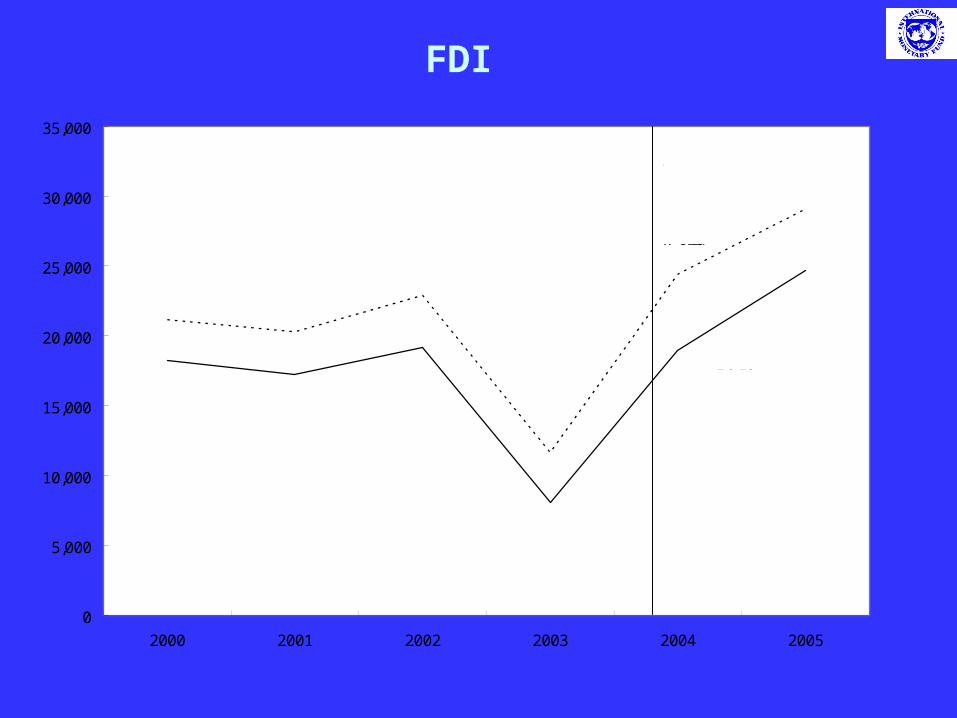

FDI

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2000 2001 2002 2003 2004 2005

Source: Eurostat.

(Millions of euros)

EU15

World

pre-enlargement post-enlargement

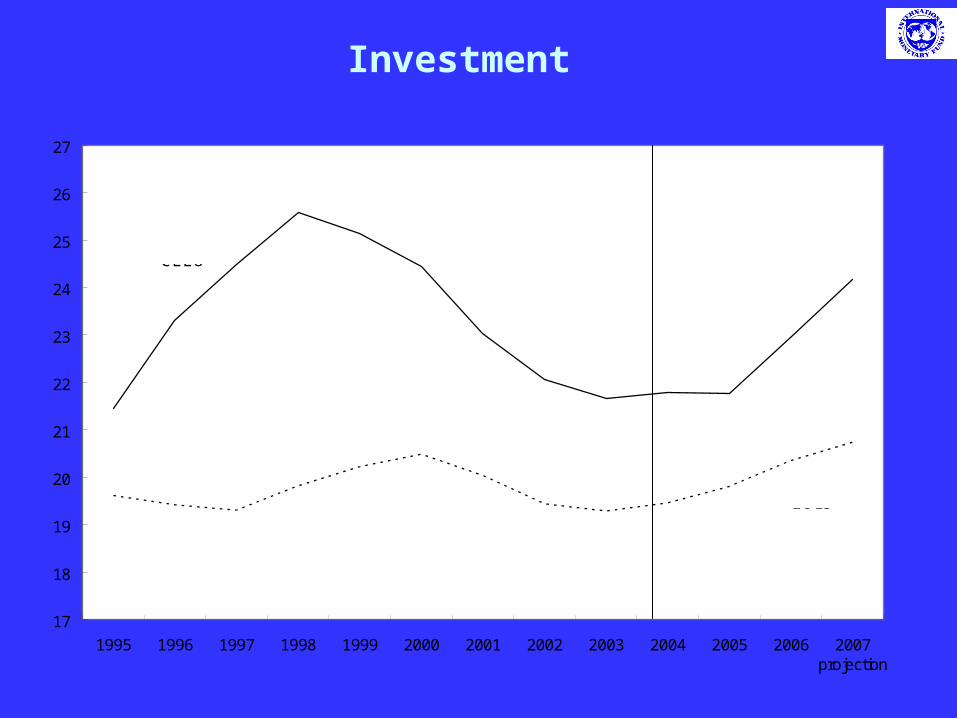

Investment

17

18

19

20

21

22

23

24

25

26

27

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007projection

Source: WEO, IMF.

(In percent of GDP)

EU15

CEE8

pre-enlargement post-enlargementFixed Investment

Title

Czech Rep.

Actual

Predicted

-8

-6

-4

-2

0

2

1997 1999 2001 2003 2005 2007

-8

-6

-4

-2

0

2Hungary

Actual

Predicted

-10

-8

-6

-4

-2

0

2

4

1997 1999 2001 2003 2005 2007

-10

-8

-6

-4

-2

0

2

4

Poland

Actual

Predicted

-10

-8

-6

-4

-2

0

2

1997 1999 2001 2003 2005 2007

-10

-8

-6

-4

-2

0

2

Slovak Rep.

Actual

Predicted

-12

-8

-4

0

4

1997 1999 2001 2003 2005 2007

-12

-8

-4

0

4

(Percent of GDP)

Title

Estonia

Actual

Predicted

-16

-12

-8

-4

0

4

8

1997 1999 2001 2003 2005 2007

-16

-12

-8

-4

0

4

8

Latvia

Actual

Predicted

-25

-20

-15

-10

-5

0

5

1997 1999 2001 2003 2005 2007

-25

-20

-15

-10

-5

0

5Lithuania

Actual

Predicted

-16

-12

-8

-4

0

4

1997 1999 2001 2003 2005 2007

-16

-12

-8

-4

0

4

(Percent of GDP)

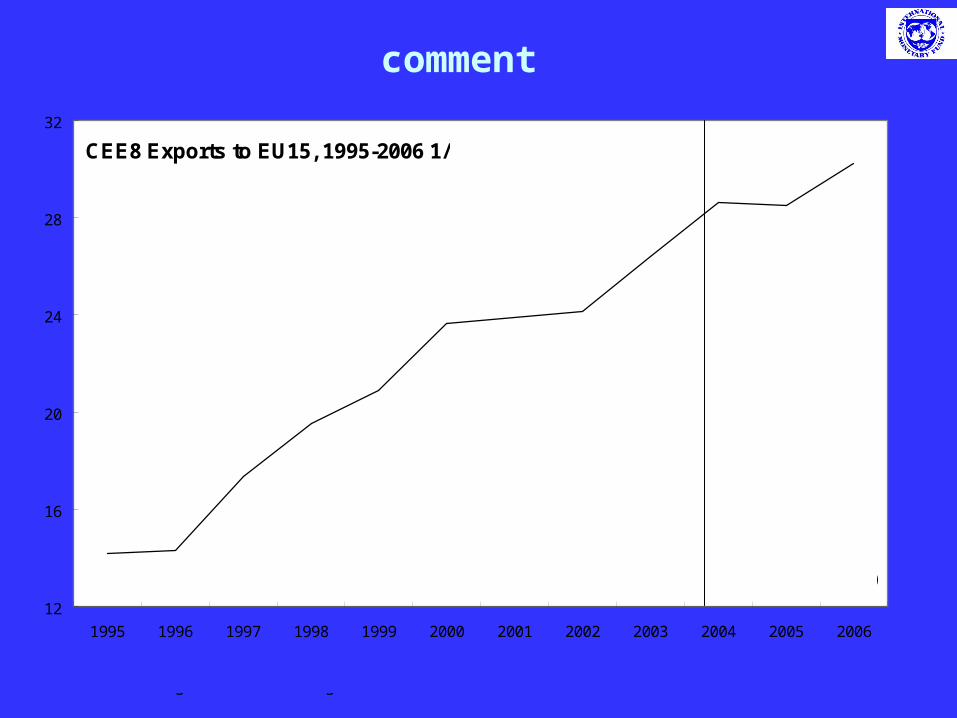

comment

CEE8 Exports to EU15, 1995-2006 1/

0

5

10

15

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Data for Belgium and Luxembourg start in 1997.

(Annual Percent Change)

pre-enlargement post-enlargement

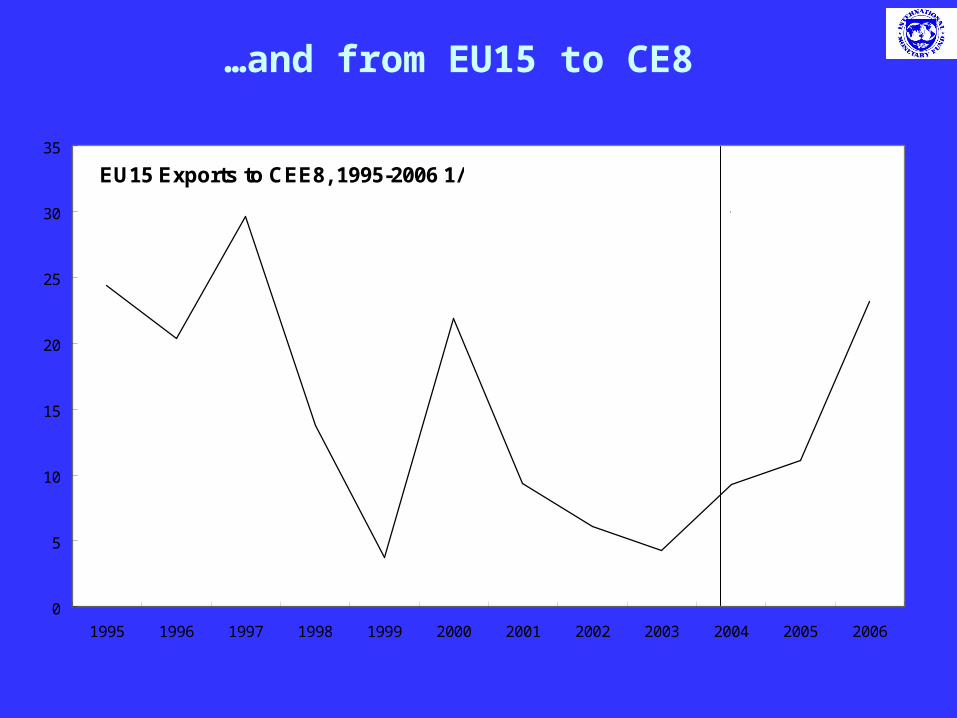

…and from EU15 to CE8

EU15 Exports to CEE8, 1995-2006 1/

0

5

10

15

20

25

30

35

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Data for Belgium and Luxembourg start in 1997.

(Annual Percent Change)

pre-enlargement post-enlargement

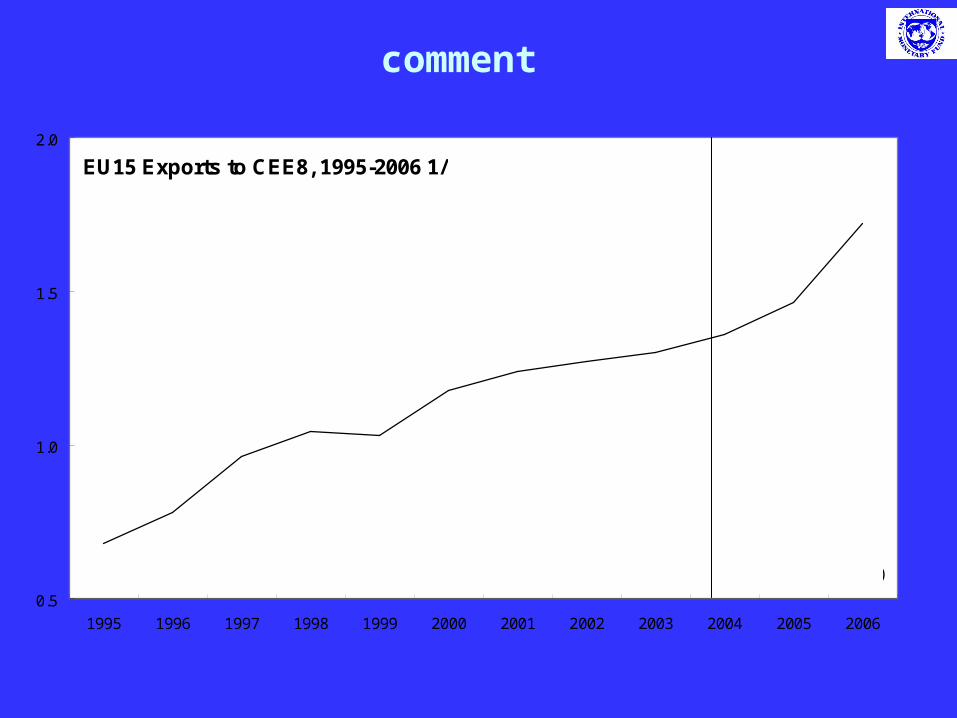

comment

CEE8 Exports to EU15, 1995-2006 1/

12

16

20

24

28

32

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Data for Belgium and Luxembourg start in 1997.

(Percent of GDP)

pre-enlargement post-enlargement

comment

EU15 Exports to CEE8, 1995-2006 1/

0.5

1.0

1.5

2.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: Direction of Trade Statistics, IMF.1/ Data for Belgium and Luxembourg start in 1997.

(Percent of GDP)

pre-enlargement post-enlargement

External debt spreads fell especially rapidly during 2004, but then rose relative to other EMs

2550

100

250

500

1000

Ext

erna

l Deb

t Spr

ead

(bas

is p

oint

s)

Jan01 Jan02 Jan03 Jan04 Jan05 Jan06 Jan07

NMS East AsiaLatin America Other EMsBulgaria Romania

(Unweighted Average; log scale)Emerging Markets: External Debt Spreads

Source: Bloomberg