Background

● What is algorithmic trading?

● What is the relevance of machine learning?

● Where does the current topic fit in ?

Trading

Traders trade via open outcrying

Close to the conventional notion of “trading”

Slow and inefficient

Manual Algorithmic

People like you and I design algorithms to predict like human traders

Computer algorithms trade with each other

Blazingly fast with high trade volumes

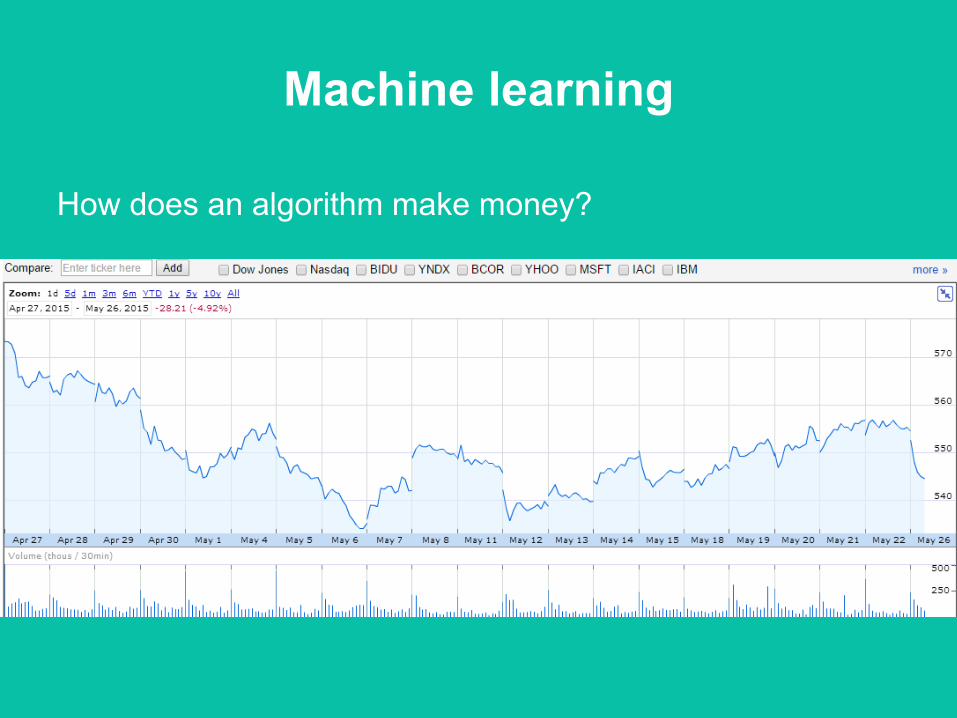

Machine learning

How does an algorithm make money?

Let’s make it more interesting !

Linear regression!

(Why is the relationship linear ?)

(Any more problems ?)

Standard ML technique

How about this graph ?

Trees to the rescue !

Decision trees are very popular in classification

Can do regression as well !

Simple and efficient

Very intuitive

Walk through

Hang on

p

Phew!

Which brings us to the discussion of the day

What is an ensemble method?

How is it relevant to finance?

Two very common ( but remarkably powerful) ensemble methods

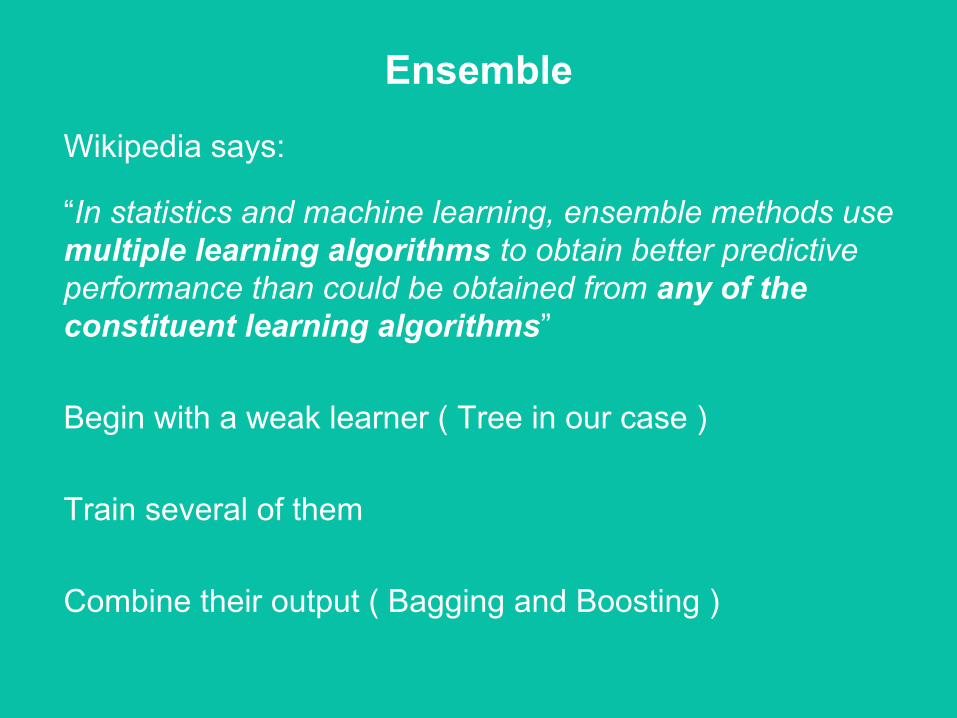

Ensemble

Wikipedia says:

“In statistics and machine learning, ensemble methods use multiple learning algorithms to obtain better predictive performance than could be obtained from any of the constituent learning algorithms”

Begin with a weak learner ( Tree in our case )

Train several of them

Combine their output ( Bagging and Boosting )

BaggingHow do you naturally expand the idea of a tree? ( Hint : think real world )

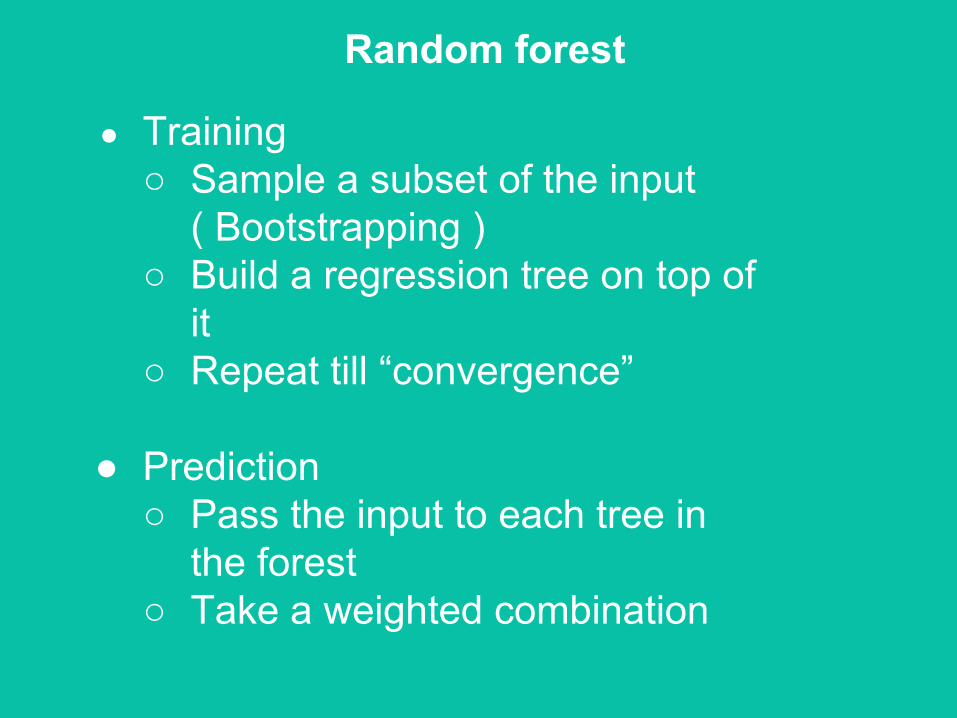

Random forest

● Training○ Sample a subset of the input

( Bootstrapping )○ Build a regression tree on top of

it○ Repeat till “convergence”

● Prediction○ Pass the input to each tree in

the forest○ Take a weighted combination

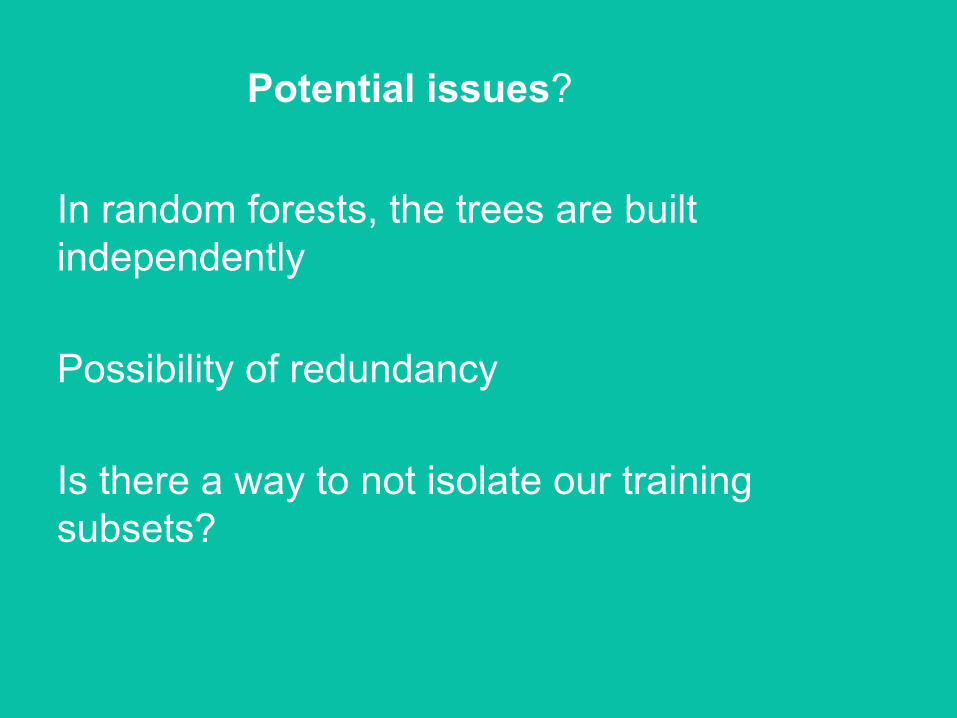

In random forests, the trees are built independently

Possibility of redundancy

Is there a way to not isolate our training subsets?

Potential issues?

Boosting

● Training○ Sample a subset of the input○ Build a tree on top of it○ Obtain an error statistic on the WHOLE

input○ Use this statistic to generate the next

input subset

Median heavy training instead of mean heavy training

Why use this in finance ?

i.i.d assumption goes for a toss

Noise filtering is a challenge

Sophisticated methods often fail ( and are miserably slow)

We need to rely on simple methods and yet guarantee high accuracy