1

Equity Valuation & Analysis of

GUESS INC.

Chris Yelverton

Toan Le

Eric Lundblad

Mike Wallace

Mark Chapman

2

Table of Contents

Executive Summary 4

Industry Analysis 8

Company Overview 8

Industry Overview 10

Five Forces Model 11

Value Chain Analysis 27

Accounting Analysis 33

Financial Analysis 46

Core Sales Manipulation Diagnostics 46

Core Expense Manipulation Diagnostics 49

Forecasting 53

CAPM Estimation 68

WACC Estimation 70

Method of Comparables 71

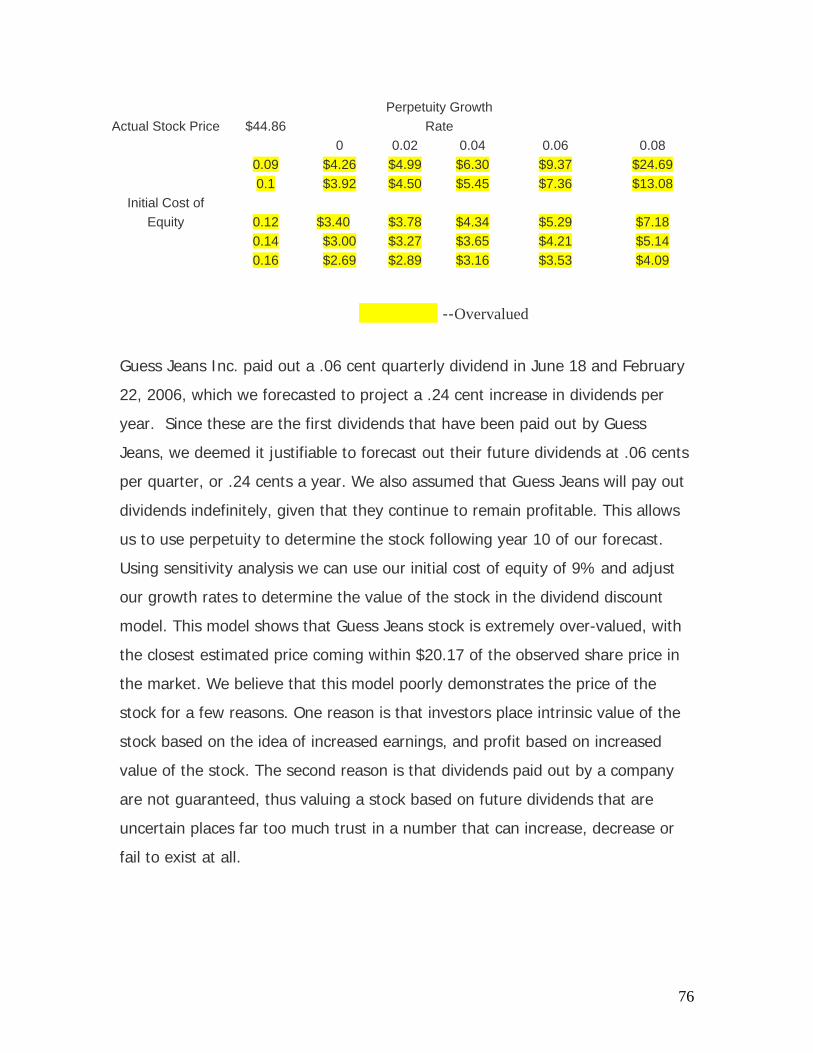

Discount Dividend Model 76

Discounted Free Cash Flows Model 78

AEG 80

Residual Income Valuation Model 83

Long Run ROE Income Model 86

Z Score 88

Appendix

3

Executive Summary

Investment Recommendation: Company Is Slightly Undervalued, Buy

GES – NYSE (06/30/07): $44.86

52 week range: $51.15 - $19.50

Market Capitalization: 4.49B

Shares Outstanding: 93.54M

Avg. Daily Trading Volume: 1.73M

ROE: 30%

ROA: 15%

Cost of Capital Estimate R2 Beta Ke

3-Month .055 .10 5.99

6-Month .045 .10 6.02

2-Year .078 .15 6.40

5-Year .117 .29 7.49

10-Year .163 .48 9.00

Altman Z-Score: 9.41

Ratio Comparison GES AEO GAP

Trailing P/E 28.2 16.8 14.6

Forward P/E 34.8 15.71 30.29

P/B 10.16 4.10 3.06

Valuation Estimates

Actual Price (06/30/2007): $48.04

Ratio Based Valuations

Trailing P/E $10.19

Forward P/E $24.00

P/B $25.78

P/EBIT $28.30

P/FCF $44.80

Intrinsic Valuations Actual Revised

Discounted Dividends $3.40 $73.66

Free Cash Flows $52.13 $71.85

Residual Income $70.92 $103.80

LR ROE $15.53 N/A

AEG $15.53 $137.47

4

Industry Analysis

Guess was founded in 1981 and currently operates as a Delaware corporation.

Guess Inc. (GES) is a component of the specialty retail industry which is a

segment of the overall retail industry. Guess Jeans designs, markets,

distributes, and licenses lifestyle collections of contemporary apparel and

accessories for men, women, and children that reflect American lifestyle and

European fashion sensibilities (Guess Inc. 2006 10-K). Their target customer is a

style-conscious consumer primarily between the ages of 18 and 32 which is a

highly desirable demographic group that is believed to have significant

disposable income. Guess currently operates 336 stores in North America and

386 additional stores internationally. To compete in the specialty retail industry

firms must be conscious of several key success factors.

Guess’ direct competitors include GAP, Abercrombie and Fitch, and American

Eagle Outfitters. These firms were chosen for comparisons because they are

traded publicly and have highly accessible financial data. Firms in the specialty

retail industry compete by differentiating their products from competitors. While

it is important to maintain competitive prices, the main focus in this industry is

not cost leadership. The primary factor that separates firms in the specialty

retail industry is creating a distinguished image that customer’s value. Another

factor that can help gain a competitive advantage is providing a product of

superior quality. Success is also dependent on the variety of products that a firm

provides. Competitors in the industry strive to expand product lines, develop

new product lines, and sell additional accessories.

5

Accounting Analysis

To be able to efficiently analyze a firm, an investor must next do a very

extensive accounting analysis to determine which key accounting strategies a

firm is using to affect their net income. First, key accounting policies are

discussed and then checked to determine if they coincide with the firms key

success factors in the five forces model. Due to GAAP standards and regulations,

firms are allowed a lot of flexibility on how they report on their financials. One of

the areas that firms are allowed a lot of flexibility in the specialty retail industry is

the reporting of inventory. One area that allows a lot of flexibility is the ability to

use off the balance sheet transactions to record operating leases. This allows a

company to understate their liabilities as well as manipulate their cash flows from

operations. By capitalizing the lease an analyst is able to see the true value of

firms’ liabilities and use them to value the firm accordingly.

In the specialty retail industry almost every firm uses operating leases as

opposed to capital leases. The operating lease enables the firm to receive tax

benefits be expensing lease payments as well as allowing them to decrease

liabilities. The capitalization of Guess’s operating leases allows investors to gain a

better understanding of their true financial standing, and that is recognizing

almost 3.5 million in liabilities that did not show up under operating leases.

Guess’s sales and expense ratio diagnostics did not appear to raise any potential

red flags for the company. Guess seems to be operating efficiently in their niche

and is relatively close to the industry average in this area. We believe that this is

a clear red flag. The fact that a company is able to understate its liabilities

significantly distorts its accounting numbers and can portray its company’s

financials in a more appealing manner.

6

Financial Analysis and Forecasting

To compare Guess’ financial performance and gauge their future outlook relative

to competitors we performed a series of liquidity, profitability, and capital

structure ratios for Guess and each of the mentioned competing firms. These

ratios also allow us to calculate an industry average which is useful as a

benchmark measure. The results of the financial analysis are then used to

forecast Guess’ financial statements 10 years out. Next you must estimate a

beta for the firm using the CAPM model, and the cost of equity can be

determined using regression analysis. Ultimately the cost of capital can be

calculated using the weighted cost of capital formula.

As far as the liquidity analysis goes Guess’ had been right at the industry

average. And for the profitability analysis they were among the industry leaders,

which means, they will continue to yield high profits in the future years of

operations. Using the current dividends of 6 cents paid out in 2006, we were

able to successfully forecast dividends out to 2011. We forecasted out other line

items such as earnings on the income statement by using an estimated sales

growth rate of that peaked at 28%. From that point, we gradually reduced the

growth rate and started heading it towards the industry average. This method of

growth is backed up by the very strong sales numbers that Guess has seen in

recent years. We believe that Guess will continue to grow at this strong rate.

Cash flow from investments and operations using the financial analysis derived

from our published statements. This allowed us to get a reasonable estimate on

future earnings that helped us further value the firm until our perpetuity year of

2017.

7

Valuation

Almost all aspects of a company can be analyzed to determine if the company is

over or under valued based upon their share price. Ultimately this is what

investors look at to determine if they would like to invest in the firms stock.

There are various models used to determine the valuation of the stock prices.

The first being the method of comparables, it is the quickest and easiest method

to implement but is not very reliable because the price per share is ultimately

determined upon an industry average. Second, the intrinsic valuation models are

more theory based and take into account the estimated of the companies next

ten years of forecasted financials. There was also a revised section where we

took into account the company’s use of operating leases as opposed to capital

leases. In conclusion, it was determined after running all of the valuation models

that Guess is an extremely overvalued company.

Industry Analysis

Company Overview

Guess Inc. (GES) designs distributes and licenses one of the worlds leading

lifestyle collections of contemporary apparel and accessories for men, women,

and children that reflect the American lifestyle and European fashion sensibilities.

Furthermore, Guess Inc. also grants licenses to manufactures and distribute a

broad range of products that compliment their apparel lines (Guess’s 2006 10-K).

Since Guess’ inception in 1981, Guess has targeted males and females between

the ages of 18 and 32 because they believe that this group is full of style

conscious consumers with enough disposable income to pay for a brand name.

8

Guess is headquartered in Los Angeles, California where it operates its retail,

wholesale, and European Licensing business segments. Guess uses three main

distribution channels to sell their products which includes; using their own stores,

through a network of wholesale accounts, and the Internet. Through these

distribution channels, Guess offers a full apparel line of both denim and cotton

jeans, pants, overalls, skirts, dresses, shorts, blouses, shirts, jackets, and

knitwear. In addition, Guess also offers accessories that promote and

complement its image which includes eyewear, watches, handbags, kids clothing,

footwear, and fragrances that are also distributed through these channels.

Currently, Guess operates 336 stores in the United States and Canada, 24 stores

in Europe and 3 stores in Mexico. Guess is very focused on constantly growing

and expanding their operations in the retail industry. During 2006 they opened a

total of 32 new stores and are planning to open 48 news stores in the year 2007.

Guess’ total revenue for 2006 totaled 1.19 billion dollars and net earnings totaled

123.2 million dollars. The table below demonstrates Guess’ recent success in

growth through sales and the increase in total assets.

2002 2003 2004 2005 2006

Total

Assets

$349,532 $362,765 $424,304 $633,374 $836,925

Sales $583,139 $636,585 $729,262 $936,092 $1,185,184 ** Assets and Sales in thousands**

Total Sales for the 2006 fiscal year was $1,185,184,000.00 which was a 21.02%

increase from the previous year. This increase in sales was nearly 4.2 percentage

points better than their closest competitor (AE 16.9%). This trend seems to be

holding true so far in 2007 with Guess having a sales growth rate of 26.6%

which is 6.3 percentage points better than American Eagle. (20.3%)

(Moneycentral.msn.com)

9

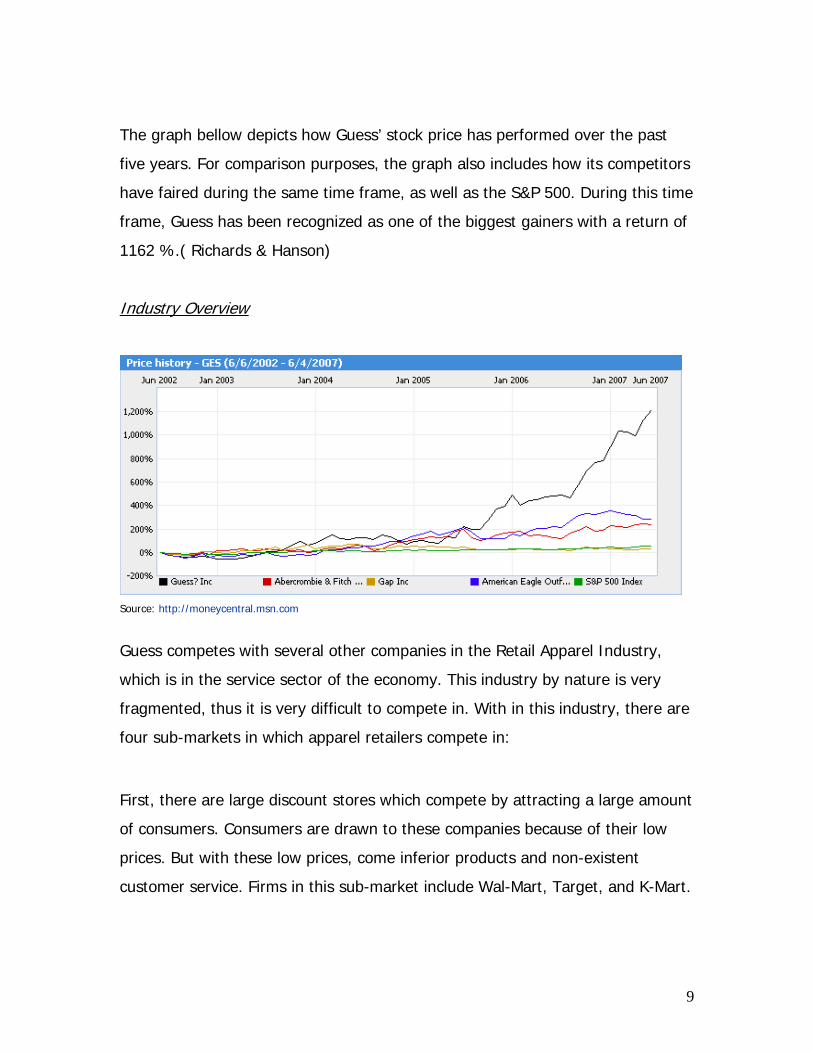

The graph bellow depicts how Guess’ stock price has performed over the past

five years. For comparison purposes, the graph also includes how its competitors

have faired during the same time frame, as well as the S&P 500. During this time

frame, Guess has been recognized as one of the biggest gainers with a return of

1162 %.( Richards & Hanson)

Industry Overview

Source: http://moneycentral.msn.com

Guess competes with several other companies in the Retail Apparel Industry,

which is in the service sector of the economy. This industry by nature is very

fragmented, thus it is very difficult to compete in. With in this industry, there are

four sub-markets in which apparel retailers compete in:

First, there are large discount stores which compete by attracting a large amount

of consumers. Consumers are drawn to these companies because of their low

prices. But with these low prices, come inferior products and non-existent

customer service. Firms in this sub-market include Wal-Mart, Target, and K-Mart.

10

The next sub-market is composed of mass merchandisers. Consumers are drawn

to them because they offer quality products at reasonable prices with fair

customer service. Participants in this market are primarily department stores like

Kohl’s, JC Penney, and Mervyn’s.

Another sub-market in the retail apparel industry is the upscale mass

merchandiser. These companies offer luxurious products and superior customer

service. Consumers of this division are willing to pay a premium for products and

service because of the prestige and status that is associated with shopping at

these companies. Firms associated in this market include Neiman Marcus,

Nordstrom’s, and Sac’s 5th Avenue.

The final sub-market in the retail apparel industry is the specialty retail division.

What makes this division so unique is that the retailers also provide their own

clothing line and accessories to sell. They offer quality differentiated products at

reasonable prices with fair customer service with their own flare. This is the

division in which Guess competes in. Consumers of this division typically range

from male and female teens to adults in their early 30’s. Consumers are attracted

to this division because they are brand image conscious and like the

differentiated products that firms produce. Companies in this division are direct

rivals to Guess and include Abercrombie and Fitch, American Eagle, and Gap.

Five Forces Model

The five forces model is a strategic market analyzing tool that enables firms to

analyze their specific industry and use its knowledge to create a competitive

edge over competing firms in the industry. The five forces model uses five

competitive forces to determine attractiveness to the industry, and the ability to

generate a profit. The five forces is composed of the threat of substitute

products, the threat of new entrants, rivalry among existing firms, and the

11

competitive bargaining power of both buyers and suppliers. The apparel industry

is a highly competitive industry, divided into smaller sub-markets such as men’s

and women’s clothing, and accessory apparel.

Rivalry Among Existing Firms

Rivalry among existing firms is one of the biggest sources of competition in an

industry, with firms all competing for the available profits created in the market.

The analysis of the existing firms allows a company to evaluate the level of

competition between the major players with in an industry and come to a

decision on how to create a competitive advantage. “In being a specialty retail

entity, we compete with numerous apparel manufacturers and distributors, both

domestically and internationally, as well as several well-known designers,

including some that have recently entered or re-entered the designer denim

market” (GUESS?, INC. 10k).

Guess Jeans Inc. competes on several different platforms in the retail industry,

allowing them to be very versatile in tapping into the fashion market. Guess

retail and outlet stores compete with a wide variety of other specialty retailers,

such as Gap, Abercrombie & Fitch, and American Eagle. Among these firms,

there are several factors that determine the degree of competition between

existing players in this industry.

Industry Growth

Industry growth helps a corporation determine the available share of the market,

as well as the level of competition with in the industry. If an industry is steadily

growing, companies do not have to compete for each others market share. The

apparel industry is a constantly growing market, with new fashions and styles

12

leading the way to new, evolving product markets. In 2006, GUESS opened a

total of 32 new stores in the United States and Canada alone, as well as

increasing their average retail outlet square footage by 5.3%. This shows that

the demand in the market is still high enough to satisfy their needs for growth

and increasing profits.

As a multi-national corporation, Guess is also continuing growth in countries

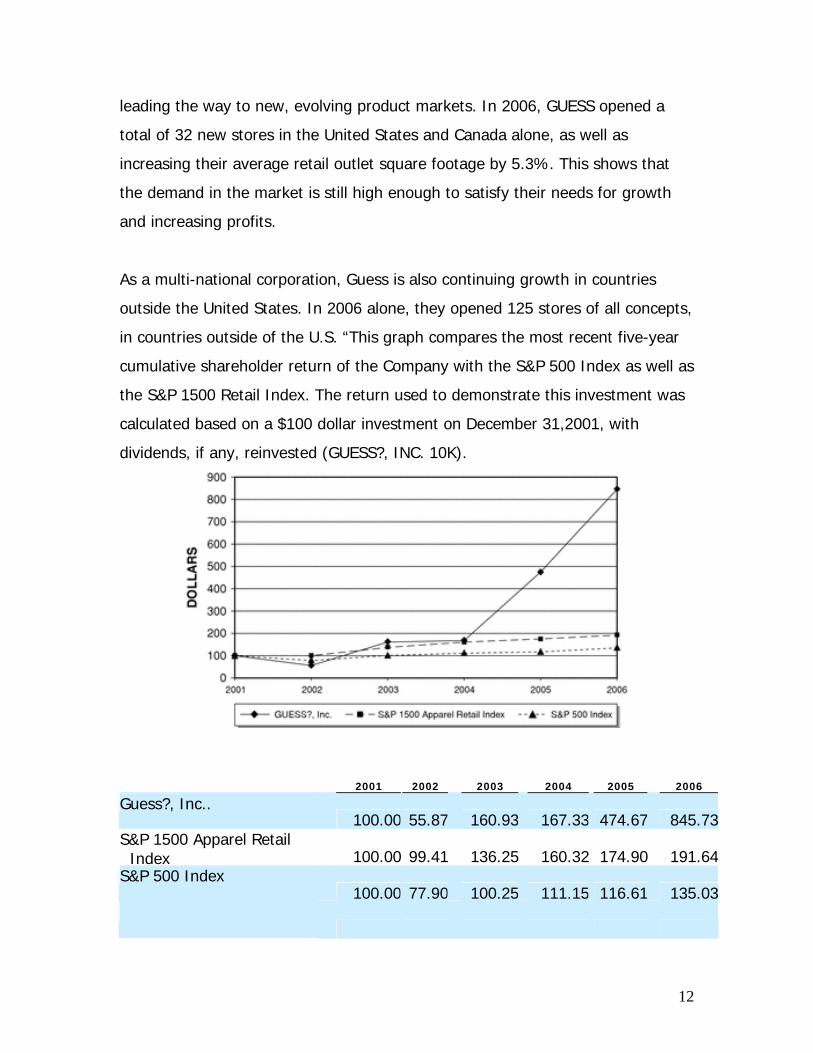

outside the United States. In 2006 alone, they opened 125 stores of all concepts,

in countries outside of the U.S. “This graph compares the most recent five-year

cumulative shareholder return of the Company with the S&P 500 Index as well as

the S&P 1500 Retail Index. The return used to demonstrate this investment was

calculated based on a $100 dollar investment on December 31,2001, with

dividends, if any, reinvested (GUESS?, INC. 10K).

2001

2002

2003

2004

2005

2006

Guess?, Inc..

100.00

55.87

160.93

167.33

474.67

845.73S&P 1500 Apparel Retail

Index

100.00

99.41

136.25

160.32

174.90

191.64S&P 500 Index

100.00

77.90

100.25

111.15

116.61

135.03

13

As you can see, the S&P Apparel Retail Index has been steadily increasing since

2001, with Guess significantly outperforming the index in the recent years. This

demonstrates to us that the Apparel industry is growing, allowing firms not to

engage in price competition.

The following graph shows the sales growth for the industry with in the past five

years. Based on the information, the industry is still experiencing growth from

year to year.

Percentage Sales Grwoth

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

Years

Perc

ent

Series1

Series1 8.65% 8.98% 6.49% 5.54% 5.32%

2002 2003 2004 2005 2006

We can also see that the industry is growing by assessing the assets of the

companies. By doing this, you can analyze the changes in total assets which

equates to growth or decay for firms in an industry. The graph bellow shows that

most of the firms within this industry are growing. However, Gap assets have

been decreasing for the past three years.

14

Total Assets

02000000400000060000008000000

1000000012000000

2002 2003 2004 2005 2006

Year

Tota

l A

sset

s(th

ousa

nds

ofdo

llars

)

Gap American EagleAbercrombie & Fitch Guess

Sources: www.gap.com, www.ae.com, www.abercrombie.com, www.guess.com

Gap’s diminishing assets correlates with the loss of market share that Gap has

also experienced over the past few years. This can also explain the very strong

growth that Guess and its other competitors have experienced over this five year

span. To help illustrate this situation, we used total sales to see how much of

their market share has been relinquished to its competitors over the past five

years. The graphs bellow illustrates the situation.

Market Share 2002

80%

8%

9%3%

Market Share 2006

69%

12%

14%5%

Sources: www.gap.com, www.ae.com, www.abercrombie.com, www.guess.com

15

In 2002, Gap held 80% of the market share, while American Eagle held 8%,

Abercrombie & Fitch held 9%, and Guess occupied 3% of the market share. Four

years later, Gap had relinquished 11% of its market share to its rivals. American

Eagle has increased its market share to 12%, while Abercrombie & Fitch

increased to 14%, and Guess saw an increase to 5%.

In 2007 we saw a significant slowdown in the retail/apparel industry. Many

economists argue that the downturn in the housing market as well as rising gas

prices has affected consumer spending, decreasing sales on non-commodity

items. “April was rough also for mall-based specialty stores. Gap Inc. reported a

16% same-store sales decline. Abercrombie & Fitch Co. said results will fall

below analysts' forecasts. American Eagle missed Wall Street expectations, with

a 10% decline in same-store sales, but it reaffirmed its first-quarter earnings

outlook of 34 to 35 cents a share (James Covert, WSJ, May 11, 2007).”

American Eagle credits their late increase due to the coming summer months, a

time when new fashions and styles are released into the market. These numbers

demonstrate the cyclical nature of the retail market. Increases and decreases in

net sales can be affected industry wide by availability of consumer spending as

well as other fashion related issues such as weather.

This graph shows the Net Sales (in Millions) of some of the leading competitors

in the retail industry today. With all but one of the companies reporting a loss, it

16

is easy for us to analyze and foresee events in the economy that would lead to

slowdowns in the retail industry.

Concentration and Balance of Competitors

The number of firms that compete in an industry and their relative sizes

determine the degree of concentration in an industry (Palepu 2-3). The amount

of concentration that is present in an industry influences whether competing

firms will co-ordinate their pricing to avoid price competition between firms.

Retailers are commonly positioned close to each other, either in shopping malls

or large strip centers. This highly concentrates the industry, with individual

retailers each competing for customers in a similar area. When an industry is

highly concentrated, it is dominated by a few key players, allowing them to

influence the market and help prices to remain fairly stable. When the market is

in low concentration, there is no large firm to establish pricing standards, and

firms will begin to compete on a “lowest cost” basis.

As previously mentioned, there are many different sub-markets in the apparel

market. Guess as well as their competitors try to differentiate themselves from

that type of genre, and focus more on the high end side of the clothing

spectrum. This “specialty” clothing sector of the market is less concentrated. This

allows them to focus on a client basis that relies more on brand name value, and

the quality and style associated with this sector.

Degree of Differentiation and Switching Costs

The degree of differentiation between products refers to the similarities those

different items in the same market share. If a product line can differentiate itself

17

from the other items in its genre, it can separate itself and not allow themselves

to become a common substitute for other items in its industry.

When Guess focuses on its customer base, individuals range in age from 18-32.

They also target both males and female consumer. In addition, Guess targets a

style-conscious customer that they believe to posses a significant disposable

income. By focusing on superior quality and features that can help a customer

focus on brand recognition, their product is able differentiate itself from other

products and avoid price competition. Guess accomplishes this by encompassing

business wear as well as the latest styles appealing to a slightly older customer

base.

This marketing strategy helps differentiate themselves from their most common

competitors Abercrombie & Fitch and American Eagle. These companies seem to

focus on a slightly younger, more laid back genre ranging from the ages of 15-25

(americaneagle.com; abercrombie.com). These companies do not do a good job

at differentiating themselves from one another. The lack of differentiation is

evident because it is difficult to distinguish products from Abercrombie & Fitch,

American Eagle, and Aeropostle. Abercrombie also faces additional problems

because it has not been successful at differentiating itself from the other apparel

lines that they offer such as Hollister and RUEHL. This has caused lower than

expected sales for the first quarter of 2007(MacNeally).

Switching costs relate to the cost the consumer will undertake in switching

between different items in the same market. Because of the nature of this

industry, switching costs for customers is generally low. In a market where

success is dominated by new and evolving fashion trends, a company is forced to

remain competitive by introducing new fashions and clothing styles. Consumers

of this market tend to switch between competitors in an industry quite

frequently; this forces competition for the target market to remain high. Since

18

the beginning, Guess has focused on superior product quality and style. They

believe the customer views a slightly higher price as a sign of quality, tending to

focus more on innovations in style and quality then to compete on a price basis.

Fixed-Variable Costs/Scale Economies

The methods a firm uses in its production and sales operations determines the

amount of money a company invests in developing its products, which is directly

related to consumer prices paid. In the specialty retail industry, fixed costs tend

to be low, with variable costs remaining high. This remains true at Guess for

many reasons.

Because of the cyclical nature of the business, certain times of the year can

remain stagnant while others can significantly increase in sales. Guess handles

this by striving to keep fixed costs relatively low. They do this by choosing not to

purchase land sites for stores, but to instead engage in operating leases.

Outsourcing is also a significant part of this strategy. Together, these methods

allow them to retain a reasonably low fixed to variable cost ratio. According to

Guess’ 10-K, they were able to lower their Selling, General, and Administrative

cost down 230 basis points. They credited this improvement because of better

leveraging of fixed cost in all areas.

By outsourcing product manufacturing and leasing retail sites, they keep their

fixed costs low at times when the apparel market is down, allowing them to pick

up production and increase spending only at times when the market demands it.

These measures are common in the retail industry, with Abercrombie & Fitch,

Gap, and American Eagle all leasing their retail sites, with most commonly being

located in shopping malls and large retail centers. By utilizing these strategies

19

retailers significantly reduce the markets competitive pressures as well as price

competition in the market.

Excess Capacity and Exit Barriers

Exit Barriers exist in an industry when companies have specific merchandise and

machinery that is difficult to liquidate, making it more costly to exit the industry

than to remain in and accept a loss. Because of the constant changing of fashion

styles accompanied with the different styles of clothing associated with the

seasons, liquidating inventory is a common practice of retail stores. This problem

is solved by large sales and discount promotions, usually 4 times a year. This

gives a company the chance to halt production, not replenishing inventory, and

to exit the industry. The increased competition affects negatively the other

incumbents. Incumbents’ profits are potentially lower than in a true competitive

market. These frequent opportunities for turnover accompanied by the common

practice of outsourcing production make the barriers of exit relatively low.

Excess Capacity deals with the notion that when supply grows in excess of

demand, companies must reduce prices and compete amongst each other for

market shares. This also leads the problem of unsold merchandise, resulting in a

loss of profit. Inventory liquidation, via large sales and discount promotions, are

also used to combat this problem. When the market seems slow, for instance at

a period in between seasons, retail companies will simply liquidate inventory for

a lower cost, generating less profits or sometimes breaking even. In the clothing

specialty retailer industry is a great amount of competition because every

clothing company is constantly changing their image and clothing styles to reflect

the current trends of seasonality or ever day wear. For instance, if you into an

typical clothing company in the spring time, they might have a sales rack selling

jackets, sweaters, etc. from the previous fall season on sale for considerably less

20

then what you could have bought it for in the actual fall season. Companies in

this industry must rely on inventory management to produce a profit. If they

don’t sell enough of their products then they will have to use an excess capacity

strategy by selling their products for less then what originally predicted. If you

find your company constantly having to use excess capacity in selling your

products then you will find that you will have to close down your store or

relocate. In this industry you see a lot of store closure or relocation in places like

malls, shopping centers, etc. mostly due to this excess capacity concept.

In conclusion, the degree among the competition of existing firms in the

specialty retail industry is very high. Close competitors are marketing to similar

customer bases, in close proximity to each other. This forces them to create

profits by differentiating themselves through style and image. These firms are

also competing among each other regarding price, yet in the specialty retail

subsidiary of the apparel market, price competition is not as highly focused on in

relation to cost competitive retailers such as Wal-Mart and Target.

Threat of New Entrants

The threat of new entrants deals with the idea that large profits in an industry

will attract new firms into the industry, shaving away profits from the existing

players in the market. There are several factors that decipher the level of

competition an industry has in regards to new entrants entering a market and

reducing a company’s market share.

Economies of Scale/Learning Economies

Companies that enter into a new market must compete with the smaller

manufacturers as well as the large staple companies in the industry. This could

21

be difficult on many levels for a company that is trying to generate a profit early

on in its company life.

Economies of scale deals with the idea that as a company begins to produce

more and more of a product, the price per unit of each item will effectively drop

as a result of a mass scale production operation. As we know, decreasing the

price of production for an item allows a company to reduce its prices more,

competing on a cost basis and forcing companies to lower their prices as well to

stay competitive.

This situation could be very difficult for a start up company to overcome because

they will have to possess a large amount of initial equity to be able to enter into

the market a competitive force. A company could try to enter the market with

less than optimum capacity, but this will force them to compete on a level of

product quality and consumer knowledge.

This is a difficult task in an industry where gaining a successful customer base

requires knowledge of customer styles, expectations, and the nature of the

business. The graph bellow shows total assets for Guess and its competitors over

the past five years. Based on this information, a start up company would have to

possess a large amount of assets to compete with existing firms. Based on these

numbers, it would probably be unrealistic for a start up firm to possess that

much in assets.

22

Total Assets

02000000400000060000008000000

1000000012000000

2002 2003 2004 2005 2006

Year

Tota

l A

sset

s(th

ousa

nds

ofdo

llars

)

Gap American EagleAbercrombie & Fitch Guess

Guess was formed in 1981 and possess 26 years of experience. This experience

has given them valuable knowledge of their customers, information regarding

business and manufacturing prices, and learning what works and what does not.

Seasoned firms use their knowledge of cyclical demands as well as new and

upcoming fashions to create and maintain a strong customer base resulting in

profit. New entrants into a market will struggle to adapt to find the right

customer base and learn what it takes to be successful in the specialty-retail

industry.

First-Mover Advantage

Since its conception in 1981, Guess Jeans has been a well recognized retailer in

the apparel industry. In the fashion industry brand recognition is a prevailing

factor that leads to the success of a company. This will inherently lead to a first-

mover advantage among companies in the industry. As a retailer becomes

seasoned in the market, it will gather a customer base that identifies the brand

name as being cool, stylish and as having exceptional quality. All of these factors

23

will result in brand loyalty and a strong customer base. It will be very difficult for

a start up company that has just entered into the market to compete with

retailers such as Guess, Abercrombie & Fitch, American Eagle, and Gap who are

recognized by consumers by their brand name and trademark style.

Access to Channel Distributions and Relationships

Since many retailers in the industry today outsource their manufacturing

responsibilities, it is very important that a company have access to these

distribution channels and obtain a positive professional relationship with them.

When outsourcing a product, quality will obviously become an issue a firm has to

deal with because even though they are not directly behind the creation of their

product, it is ultimately the retailers’ responsibility to produce a quality product

that is in line with the companies’ brand name, and that will be attractive to the

consumer. Without positive relationships with suppliers, a company can fail to

put out a quality product that is necessary to generate product in the specialty

market. Shipments must be timely and correct to compete with the cyclical

changes in fashion as well as the constantly changing clothing lines of similar

competitors. A new entrant into the industry will have to correctly identify a

reliable supplier and maintain a relationship with them that will allow them to

market a quality product and to remain efficient.

New entrants face this dilemma because there are limited suppliers in the market

place. So when there is a new entrant in the market, they are competing with

bigger firms who have bigger accounts with these suppliers. Suppliers will want

to please their bigger clients first. As a result, new entrants will find it harder to

get their products in a timely manner. In addition, their quality of product might

suffer because suppliers will rush to get their products to them in a timely

manner.

24

Legal Barriers

The retail industry has almost no legal barriers to entry. Trademarks of

companies tend to be the most restrictive barriers to new entrants. These

trademarks do not allow a company to mimic or reproduce products that are

directly related to a companies’ trademarked logo. This allows a company to

remain new and innovative in the industry, and not to be threatened by

competitors attempting recreate another retailers clothing line.

In conclusion, the threat of new entrants into the specialty-retail sector of the

apparel market is relatively low. New entrants into the market will have to deal

with the difficult issues of economies of scale, a large first-mover advantage, as

well as attaining efficient and reliable distribution channels.

The Threat of Substitute Products

Obviously in an industry such as clothing, substitute products will be very evident

in the market. Retailers in the specialty-retailing sector of the apparel market will

have to differentiate themselves from the rest of the pack, and look at factors

such as relative price and performance, as well as a buyers’ willingness to switch

from one product to another. Guess focuses on differentiated product designs

and styles they believe will separate themselves from the rest of the retail

industry. Because consumers tend to relate a higher product cost to a higher

product quality, Guess focuses more on exceptional product quality rather than

creating a lower cost.

Another factor that might influence a customer purchasing substitute products is

the manner in which they shop for their products. Guess not only sells its

25

products in a traditional retail locations, but also offer their products via the

internet. This new selling channel will become more prevalent in future years as

the general population begins to trust the internet more and becomes more

computer savvy. This idea is supported by the fact that online sales have

continued to increase from year to year.

This is different from our competitors in the industry such as American Eagle and

Abercrombie. Although they are categorized as specialty-retailers, they focus

more on relaxed, leisure clothing, which can sometimes be associated with a

slightly lesser cost. Guess chooses to focus on a customer base that is willing to

spend a higher price for the latest designs in fashion and the highest clothing

quality.

In conclusion, the threat of substitute products in the clothing industry is high

because of the extreme variety a consumer can choose when purchasing

clothing. For an industry to be successful in retailing, they must focus on brand

image and quality to gather and retain a customer base and create a profit.

Bargaining Power of Buyers

Bargaining power of buyers is determined by two things in the Specialty Retail

industry, price sensitivity and relative bargaining power. In the Specialty retail

industry companies suck as Guess customers or buyers are very price sensitive

because they can easily switch over to competitors apparel if they offer they

same item at a lower price. So price wars among the retail industry can get very

severe at times. Due to the fact that one single buyer in a retail industry does

not consumer a significant amount of the companies apparel, losing a couple of

customers due to price changes will not harm the company. Basically companies

in the retail industry need to constantly make an effort to keep up with changing

26

trends in fashion and preferences among certain age groups to ensure that they

can compete on a competitive level and maintain a significant amount of market

share in their industry. Furthermore, since one single buyer does not consume

massive amounts of inventory they have little to none relative bargaining power

over the suppliers. This is also true because the switching cost is very low for the

buyer. In essence, in the specialty retail industry the customer has very low

bargaining power because the individual suppliers i.e. the stores are forced to

compete on cost due to low switching cost.

Bargaining Power of Suppliers

In the specialty retail industry firms attempt to buy their goods at the lowest

price possible, and this gives suppliers very little bargaining power over the

buyers because the buyers can opt to change suppliers very easily due to the

large volume of suppliers willing to offer the goods at a lower price. There are so

many different retail suppliers that buyers can have produce their product that

might offer a lower price that the supplier has relatively low bargaining power

over the buyer. Because Guess is a widely recognized brand name they do not

have to compete on quality but more so on cost and trying to differentiate

themselves from their competitors. The suppliers want to offer the lowest price

they can due to the easy with witch the buyer can switch suppliers. So the

suppliers are very price sensitive and this gives bargaining power to the buyer

because they don’t have to rely on one single supplier. Overall, the specialty

retail industry has to compete on price most of all due to all the reasons stated

above.

Value Chain Analysis

Firms in the specialty retail industry compete on differentiation. To be successful

while following a differentiation strategy the firm must accomplish three things.

27

First, it needs to identify one or more attributes of a product that customer’s

value. It must then position itself to meet these customer needs in a unique

way. Finally, firms must achieve differentiation while maintaining a cost below

the price premium that customers are willing to pay. Because the industry is

highly competitive firms must also take into account some cost leadership

strategies to maximize their potential advantage. There are several key success

factors which are vital to achieving and sustaining a competitive advantage in the

specialty retail industry.

Key Success Factors

Differentiation

The primary factor that separates firms in the specialty retail industry is a

distinguished image that customer’s value. Firms are able to accomplish this by

investing resources in their brand image. By creating a reputable image and

distinct design, firms are able to capture and retain a certain customer base.

Because firms in this industry are not competing solely on cost leadership it is

imperative that they invest in developing a unique product image to differentiate

themselves from competitors.

Another factor is the ability to produce a product of superior quality. The

products created must have a high perceived quality to gain any kind of

competitive advantage in the specialty retail industry. There are general market

expectations for a certain level of quality within the industry. Without meeting or

exceeding these standards a firm cannot expect to compete.

The ability to develop a superior product variety is another important success

factor. There is an opportunity to achieve further competitive advantage by

28

offering a larger variety of products. Firms accomplish this through the

expansion of current product lines, creation of new product lines, and selling

additional accessories. Engaging in such a strategy allows firms to expand their

customer base and further serve their current customer base.

Cost Leadership

Because the specialty retail industry is highly competitive and fragmented, firms

that follow a differentiation strategy cannot ignore the cost leadership dimension.

There is a price premium that will turn customers away from firms in the

industry, so it is important to find ways to reduce production costs where

possible. Areas that firms can focus on are low-cost distribution and efficient

production. This can allow a firm to reduce production costs without sacrificing

the product quality or brand equity that is necessary in a differentiation strategy.

Firm Competitive Advantage Analysis

Since its founding in 1981 as a small California jeans company, Guess has

developed into one the most familiar brand names in the fashion industry. The

specialty retail clothing and apparel industry has been classified as one of the

most highly competitive industries due to many swift variations of consumer

wants and interests. “Guess believes that its success depends in large part upon

its ability to anticipate, gauge and respond to changing consumer demands and

fashion trends in a timely manner and upon the continued appeal to consumers

of the Guess image.” (GUESS?, Inc. 2007 10-K)

29

Brand Image

The best way of achieving competitive advantage in this industry is to possess a

strong attribute in differentiating your products from your competitors. They

have achieved this by continually leveraging what they want their brand image to

represent. With their headquarters in Los Angeles, CA, they are constantly

visiting dominant fashion locations where their marketing teams can see what

the new styles are and get a glimpse of where they think the industry is headed.

Guess puts most of its effort into new product innovation and differentiation.

They have done this by utilizing a retail strategy that focuses on opening more

retail stores, while at the same time, constantly improving the quality of the

stores that already exist. The constant improvement of stores will keep the brand

image consist with the current trends of the period. This is a very simple, but

effective strategy of maintaining, capturing, and retaining a susceptible customer

base.

Guess has also correlated their brand image into an expansion and growth plan.

This expansion plan can be a way of building brand awareness and executing

market penetration. “During 2006, we opened a total of 32 new stores in the

U.S. and Canada consisting of eight new full-price retail stores, seven factory

outlet stores, 11 MARCIANO stores and six Guess Accessories stores, while

closing 11 stores. Guess expects to open approximately 48 new stores in 2007,

consisting of 15 full-price retail, four factory outlet, 13 MARCIANO stores, three

Guess Accessories and 13 G by Guess stores.”(GUESS?, Inc. 10-K)

Internationally, Guess acquires licensees and distributors in Europe, South

America, Asia, Africa and the Middle East. If Guess can effectively establish itself

as a defiant manufacturer and distributor, it can take advantage of economies of

scale and further expand its operations abroad. Guess needs to be competitive

with constant expansion and growth. The more exposure in the market, the

more consumers will want to buy your products.

30

Superior Product Quality

Guess strives to offer products that are superior in quality. To ensure that

products meet the desired standards Guess has implemented a quality control

program. This program allows them to monitor the quality of the fabrics being

used prior to the production of a final product, and inspect prototypes of each

product before initiating production runs. Another aspect of the program is

random quality control checks during and after production before garments leave

the contractor. There are also final random quality checks after the products

have been received by the distribution centers. Guess believes that this policy of

inspection is important in maintaining quality and consistency in its products.

The quality control program allows Guess to produce a product of superior

quality which conforms to their strategy of differentiation.

Superior Product Variety

To achieve product variety Guess is placing additional emphasis on their

Accessories line and their MARCIANO line. Guess plans to direct greater

attention to these lines in existing stores as well as open additional stores that

exclusively feature these products. This strategy targets current Guess

customers while also aiming to capture new customers. By focusing on

developing superior product variety, Guess has enabled them to significantly

expand. In 2006 there were six Guess Accessories and 11 MARCIANO stores

opened. The previous year there were six Guess Accessories and nine

MARCIANO stores opened.

Another way that Guess is expanding their product variety is introducing a new

mid-tier brand concept. G by Guess targets a more price conscious

demographic. In early 2007 Guess will open the first G by Guess store in North

America. By the end of the year the expectation is to have approximately 32 G

31

by Guess locations. The product variety that Guess has pursued is essential to

the differentiation strategy that is necessary to gain a competitive advantage in

the specialty retail industry.

Efficient Production

To increase efficiency Guess has made improvements in their product sourcing.

In the past year, changes streamlined processes, provide calendar alignment,

and increase the timeliness of delivery. “This globalization of operations will

enable us to begin integrating our European, North American and Asian-based

supply chains. This, in turn, supports our long term strategy of developing a

global core product assortment, through collaboration between our U. S. and

Italy based design teams.” (GUESS?, Inc. 10-K) To assist the design process,

Guess has formed a Product Development team that dictates calendar deadlines,

assortment plans, and financial goals. These steps have allowed Guess to

increase the efficiency and lower the cost of production.

Low-Cost Distribution

Guess’ primary distribution center is located in Louisville, Kentucky. The site is

near the United Parcel Service’s national transit hub. (GUESS?, Inc. 10-K) This

had allowed the company to reduce shipping time and costs of distributing goods

to the Eastern part of the United States. Guess projects that it will continue to

reduce operating cost by reducing handling costs in this facility. The company

has also updated software systems in the Montreal and Los Angeles distribution

facilities to align with the systems used in the primary facility. This has resulted

in further operating efficiencies. The goal of these actions is to reduce future

processing and freight costs. (GUESS?, Inc. 10-K)

32

Looking Forward

Guess has been successful at creating a distinguished brand and valued product

lines within the specialty retail industry. By differentiating themselves from

competitors and maintaining competitive prices they have achieved a competitive

advantage. This has allowed Guess to expand domestically and internationally.

In 2006 Guess increased retail average square footage by 5.3%. Sales in 2006

were up 12.8% from the previous year. They plan to open 108 new stores in

2007 and further expand through international acquisitions. They are regularly

implementing new strategy and innovation to increase and sustain their

competitive advantage in this highly competitive industry.

Accounting Analysis

To thoroughly and properly analyze a firm and be able to value it with a high

degree of certainty, one must perform an accounting analysis to understand the

true underlying meaning of the numbers and ratios present in the financial

statements. The process of accounting analysis involves six key steps.

First, you need to identify the Key accounting policies which entails

understanding the policies and estimates the firm uses to implement their key

success factors to their business. A firm’s industry characteristics and competitive

advantage strategy both determine what makes up their key success factors and

risks. One of the goals of a company should be to evaluate their key success

factors and risks and how they plan to take advantage of success factors and to

avoid risks. As for a company like Guess in the Retail Sector Inventory

Management is a major key success factor.

33

Second, the degree of accounting flexibility needs to be assessed and this

directly relates to the amount of flexibility allowed through (GAAP) standards. A

company with a high degree of flexibility might be able to present their financial

statements in a more clear way in relation to their key success factors, and vice

versa if there is not a sufficient amount of flexibility.

The third step involved is evaluating the actual accounting strategy that the

managers of the firm use. From the previous step we know that managers have

the ability to manipulate financial figures. For this reason we must carefully

examine the accounting strategy that the firm implements. The fourth step is to

evaluate the quality of disclosure because the extent to which managers can

disclose their information can vary greatly across companies making financials

either transparent or very difficult to use in assessment of the firm.

The fifth step is to identify potential red flags such as unexplained increases or

decreases on the financial statements. This is done bye looking at the 10-Q’s for

a company. Many companies will defer expenses in the fourth quarter to the first

quarter of the following year. By doing this, companies incomes will be

overstated. Last, as an analyst if distortions are discovered they need to attempt

to undo the red flags to enhance the credibility and true underlying meaning of

the companies financials.

Key Accounting Policies

In determining a company’s key accounting policies it is imperative the

companies’ key success factors match up with the key accounting policies that

they company uses. As previous discussed in our companies five forces model a

company in the specialty retail industry like Guess has to create value through

tight cost control or cost leadership. There are many ways that a company can

manipulate their financials to make it seem as if costs are being lowered, which

looks pretty to investors, but as an analyst it must be explored to find the actual

34

reason for cost being lowered. Flexibility in (GAAP) enables this type of problem

to occur.

There are four distinctive qualities that are used in valuating a firms accounting

policy, each one bring more light to how the firms accounting is effecting their

overall performance. These qualities include reporting for Inventory methods,

Depreciation methods, Goodwill treatments, and Property, plant, and equipment

(PPE) valuations.

For evaluating inventory methods, you want to find out which method for

accounting for inventory the company actually used. Decipher whether the

company decided to use FIFO, LIFO, Weighted Average, etc. for their inventory

analysis. Out of these methods, you need to decide under which method the

company has the most flexibility to make their company look the best to an

investor. If they used one method over the other determined what the company

is really worth by working another method to compare it to the company’s

desired method.

Using the depreciation method of a company is also another way to determine

where there is flexibility for a company to make themselves look good. Whether

a company used straight-line method, declining balance method, or sum-of-years

digits method can make a big difference in determining how a company is really

performing. Once you determine which one they used, I would as beginning

investor would find out why the company picked that method, compare it all the

other methods and see how the company is performing.

Goodwill is the difference between the purchase price and the book value of an

acquired company’s assets. All U.S. firms are required to capitalize and amortize

goodwill against income for financial statements and deny them any tax

deductions for the amortization. Some companies get around this policy by

35

conducting a comprehensive estimation to determine assets being acquired by

both tangible and intangible. Then a depreciation deduction can be rationalized

with an established individual value and a limited life. Some company’s use this

method and some of them use the GAAP standard for accounting for goodwill,

the only way to determine whether the company is doing this or not is to look at

their journal entries on the financial statements.

Property, Plant, and Equipment (PPE) are the physical assets the company owns

but can't quickly convert to cash. Depending on the type of business, this may

make up a large portion of total assets. Whether it does or not depends on how

the company allocates for its PPE. Identify, whether it possesses a lot of land

and separate assets used in agricultural activity or if its productive assets held by

entities in the other industries. These qualities are very important in evaluating a

company. Using these methods will shine light on how a company makes itself

look to investors and what characteristics it does not want you know about.

Another key accounting policy is how a company reports on its building assets,

which can be either of the two options, capital or operating leases. Capital leases

will increase a company’s asset which directly increases owner’s equity on the

balance sheet. The use of operating leases is a more aggressive approach

because it attempts to decrease liabilities. In guess’s case they use both

operating and capital leases. Their operating leases only recognize the current

years rent as a liability rather than the life of the asset, so for the next five years

using a discount rate of 8.5% investors are seeing that liabilities are understated

by 4million making the company look like it is in better financial condition than it

really is. In other words this should be the true present value of the future

payments.

Another key accounting policy is how a company reports on its building assets,

which can be either of the two options, capital or operating leases. Capital leases

36

will increase a company’s asset which directly increases owner’s equity on the

balance sheet. The use of operating leases is a more aggressive approach

because it attempts to decrease liabilities. In guess’s case they use both

operating and capital leases. The use of operating leases has a major influence

on how companies financial appear to investors. By capitalizing all of Guess’s

operating leases we have determined that Guess must make an adjustment of

$388,532 to their liability section of the balance sheet. The discount factor that

we used was 3.8% which is not stated in the companies 10-K. This is probably

because the number observed is even lower than the risk-free rate which would

never feasibly happen. This forecast will give investors a more honest picture of

Guess’s true financial standing in the future.

Year Operating Lease PMT PV

Factor PV 2007 77,515 0.963 74677.262008 72,251 0.928 67057.782009 66,752 0.894 59685.972010 56,164 0.861 48380.312011 46,762 0.830 38806.662012 22,820 0.799 18244.482013 22,820 0.770 17576.572014 22,820 0.742 16933.112015 22,820 0.715 16313.212016 22,820 0.689 15716 2017 22,820 0.663 15140.66

TOTAL 388,532 Areas of Accounting Flexibility

All companies are required to prepare their consolidated financial statements in

conformity with Generally Accepted Accounting Principles. This requires

management to make estimates and assumptions which affects the amounts of

assets, liabilities, revenues and expenses during the reporting period.

Accounting rules allow flexibility because it is difficult to restrict management

37

discretion without reducing the information content of accounting data. For this

reason it is possible for corporate managers to introduce noise and bias into data

through their accounting decisions. Managers have a variety of incentives to

exercise their discretion to achieve certain objectives. Guess has disclosed

significant accounting polices which they believe involve a higher degree of

judgment and complexity. These disclosed policies are those for which GAAP has

left room for accounting flexibility and managers have choices in the way that

they disclose financial information. In the following areas Guess’ is less

constrained by accounting standards and conventions.

Guess recognizes retail operations at the point of sale and wholesale operations

revenue from the sale of merchandise when products are shipped. There is

room for accounting flexibility within GAAP standards when it comes to the way

that management recognizes sales returns. Guess accrues for estimated sales

returns and other allowances in the period in which the related revenue is

recognized. To recognize the impact of returns, Guess estimates the amount of

goods that will be returned based on historical experience and reduces sales and

cost of sales accordingly based on historical return experience. The change in

sales returns accruals decreased gross profit by $3.3 million at December 31,

2006 (Guess 2006 10-K). Management can manipulate the amount of allowance

for returns to affect the net income. An understated allowance for returns

results in overstated sales and thus overstated net income.

Guess leases their showrooms, advertising, licensing, sales and merchandising

offices, remote distribution and warehousing facilities and retail and factory

outlet store locations under non-cancelable operating lease agreements expiring

on various dates through January 2018 (GUESS? Inc. 10-K). Guess reports both

operating leases and capital leases however capital leases only account for 4.4%

of their total lease agreements. When a lease is capitalized the building is

booked as an asset and the firm can recognize depreciation and amortization

38

benefits. The benefit of having a large percentage of lease agreements remain

operating leases is that the expenses incurred are not fully recognized. This

understatement of expenses leads to an overstated net income and more

appealing financial outlook for the firm. The decision not to capitalize leases

allows the firm to understate liabilities, receive tax benefits, and overstate

equity. This aggressive accounting strategy allows managers to distort balance

sheet entries to make a companies financials look more appealing to investors.

Guess assesses the impairment of its long-lived assets such as goodwill,

intangible assets, and property and equipment which requires the company to

make assumptions and judgments regarding the carrying value of these assets

on an annual basis, or more frequently if events or changes in circumstances

indicate that the assets might be impaired (GUESS? Inc. 10-K). If the assets are

considered to be impaired, the impairment is recognized as the amount by which

the carrying value of the assets exceeds the fair value of those assets. There is

a great deal of flexibility in this policy because managers have discretion in

assigning carrying value to impaired assets. As of December 2006 Guess

reported goodwill of approximately $28 million and gross intangible assets as of

December 2006 were $24.8 million. Assessing the value of goodwill is highly

subjective because the company determines the fair value to be reported and

compares it to its carrying amount. Management is capable of overstating assets

or understating expenses which both result in overstatement of net income and

equity.

Since there is a certain degree of flexibility allowed in GAAP standards, these

policy choices provide managers with an opportunity to significantly impact the

numbers reported on the performance of a firm. Without this flexibility however,

accounting data are likely to be less informative for understanding the firm’s

economics. For these reasons we must critically evaluate the firm’s actual

accounting strategy to accurately evaluate their financial outlook.

39

Accounting Strategy Using the methods demonstrated in the key accounting policies, the accounting

strategy focuses on accounting flexibility and how they use this flexibility to

either communicate their firm’s economic situation or to hide their true

performance. Because of GAAP, managers have flexibility in their accounting

methods. They can use various accounting methods to help communicate the

company’s financial health, or they can use it to distort true performance. The

methods in which they use are conservative, moderate, or aggressive by nature.

A firm that uses a conservative accounting approach will not have as high a net

income as a firm with an aggressive approach. This is because firms that have an

aggressive accounting approach will manipulate anything to get their income as

high as they can. The approach that Guess uses is a combination of aggressive

and conservative accounting methods which correlate into their accounting

strategy.

When reporting their inventory, most companies use the First In – First Out

Method (FIFO). This means as a business purchases its inventory, holds the

inventory, and finally sells the inventory the first group of purchases will be

taken off the books first. (Mangan 2000) This method is considered to be

aggressive because it artificially inflates net income in an inflationary economy.

On the other hand, American Eagle uses the retail method. In this method,

“markdowns are fully accounted for in the month in which they have been taken.

It assumes most of the markdowns apply to good sold and therefore that few of

those goods are a part of the ending inventory.” (www.cfpsa.com) This method

is considered moderate by nature.

Like many retailers in our industry, Guess offers its customers the opportunity to

purchase gift cards for friends, family, and loved ones. In 2005, Guess accounted

40

for 8,460 of store credits and gift certificates. In 2006, Guess accounted for

10,705 of store credits and gift certificates which means there was a 2,245

increase in store credits and gift certificates in the year of 2005. The Company

defers all revenues related to gift certificates “cards” and store credits until they

are redeemed for merchandise. Based on prior redemption experience, the

Company does not recognize unredeemed balances prior to two years from the

date of issuance. The breakage income is subsequently recognized ratably into

operating income over a four-year period. Once this benchmark is met, the

unused portions are recognized into the operating income over a four year

period. This is considered a conservative method of accounting because

revenues are not recorded until they can be matched with their expenses.

One of Guess’ buildings is tied down to a capital lease and the remaining of their

facilities are tied down into operating leases. A capital lease is where the value of

the building is booked as an asset and the asset is depreciated over the lifetime

of the building. The lease payments are booked as a liability and decrease over

the life of the asset. Capital leases give more information on the financial

statements because it books all future lease payments for the asset as a liability.

If Guess had all of their facilities on a capital lease, it would paint a much more

accurate picture of how the company is doing financially. Capital leases recognize

expenses sooner than equivalent operating leases. In an operating lease, the

owner transfers only the right to use the property to the lessee. At the end of

the lease period, the lessee returns the property to the owner. Since the lessee

does not assume the risk of ownership, the lease expense is treated as an

operating expense in the income statement and the lease does not affect the

balance sheet. In a capital lease, the lessee assumes some of the risks of

ownership and enjoys some of the benefits. Consequently, the lease, when

signed, is recognized both as an asset and as a liability (for the lease payments)

on the balance sheet. The firm gets to claim depreciation each year on the asset

and also deducts the interest expense component of the lease payment each

41

year. In general, capital leases recognize expenses sooner than equivalent

operating leases ( pages.stern.nyu.edu).

However, Guess chooses to put the majority of their facilities into operating

leases. By using the operating leases, Guess only has to recognize the current

years rent as a liability. Guess has the future contractual rights to the properties

for at least 15 years thus these expenses should be classified as a liability. By

choosing operating leases over capital leases, Guess is allowed to keep a present

value amount of about $338 million of liability off of its balance sheet. This

practice of using operating leases is not just isolated to one firm in this industry.

As a matter of fact, Gap, Abercrombie & Fitch, and American Eagle all use

operating leases for their respected facilities. In operating leases, the lease

expense is treated as operating expense in the income statement, so it stays off

of the balance sheet. This is very significant to the effect that it is not reported

on the balance sheet and ultimately does not affect any value on it. The value

stated on the balance sheet is larger with the lease not stated on it then it would

be stated if the lease was to be added onto it. This accounting method is

considered to be very aggressive in nature, and is used by retailers in this

industry because it makes the companies in this industry much more attractive to

lenders and investors.

As you can see, the accounting methods in which a company uses can have a

substantial impact on the financial statements. Just by choosing to use operating

leases over a capital leases for their facilities, Guess was able to understate their

liabilities by over $338 million dollars. In addition, the FIFO method in which

Guess employs with its inventory produces a net income that is overstated.

Overall the various accounting methods Guess deploys make their accounting

strategy aggressive because of activities in reporting their inventory methods,

gift certificates, depreciation methods, goodwill treatment, property, plant, and

equipment, and their operating and capital leases.

42

Quality of Disclosure

Guess is a publicly traded company which means it must report its financial

standings to the SEC yearly in a document called the 10-K. The 10-K is a

collection of all the companies’ financial statements and management’s

discussion and analysis which is audited before being handed over to the SEC.

Managers determine how easy or hard it is for anyone to assess the firm’s

accounting quality. They possess considerable power over what they determine

should be disclosed and what should not be disclosed on the financial

statements. The quality of disclosure is very important because accounting rules

require a certain amount of information to disclose, but the information that the

mangers of the company discloses is exactly what you want to see. You must

determine whether this information is biased or not.

Qualitative

Qualitative information is individual narrative reports of experiences. Qualitative

information is gathered with methods that are personal, direct, and open-ended,

with very few constraints on what the answers to the questions may be. These

methods include formal research methods. It was found that Guess does a very

good job of presenting their information in their 10-K through their financials and

management discussion and analysis in a very clear manner. Most companies in

the retail industry use operating leases. Guess does a good job of disclosing

clearly whether they function using operating or capital leases. Most companies if

they do use both will attempt to only make the operating leases clear so that

liabilities do not look as high, but Guess was very credible in this area of

disclosure.

43

Furthermore, the quality of disclosure regarding how they account for sales

return reserves, pension benefit plan, and valuation of goodwill, everything is

clearly disclosed and supported with more than enough information for an

investor to gain a fair and true understanding of the business and its operations.

Another item that increases Guess’s credibility when it comes to reporting their

financial statements is they paint a very clear understanding of why there were

increases or decreases in different line items on the financials due to changes in

(GAAP), or changes in the operations of the company.

The only item that might seem slightly sketchy is they method they use to

account for inventory, which is, first in first out. This is considered an aggressive

approach as opposed to last in last out if there is inflation over the previous fiscal

year. And there is inflation of around 3.5% with almost every year that passes.

So the use of the FIFO method we assume is being used to increase revenues.

On the contrary, FIFO is acceptable to use under (GAAP) due to the flexibility, so

the company cannot be looked down upon for using this method in its entirety.

Quantitative

Quantitative information is very important to look at when evaluating a firm. This

type of information usually falls under a few categories in a company’s activities.

Social security, personal retirement accounts, payroll taxes, pensions, stock

trends, and bonds all fall under being analyzed as quantitative information.

Quantitative data and analysis is assessed using pure form data and numbers to

draw conclusions on the quality and disclosure of a company’s financials. The

conclusions drawn are more accurate because the decisions are based upon

factual numbers. The ratios on the graphs below will help to gain a better

understanding of core sales manipulation and core expense manipulation to

better understand the business and its competitors.

44

Potential “Red Flags”

From the information provided by Gap’s quarterly’s, it can be established that

Guess is making large fourth-quarterly adjustments on their books. When Guess

filed their 10-Q on 11/09/05, they reported an increase to selling, general, and

administrative expenses of $23.5 million, or 46.9%, equaling $79.0 million in the

three months ended October 1, 2005, from $53.7 million in the comparable 2004

period, primarily attributable to the increase in European operations. On their

05/11/06 10-Q filing, they reported another increase of $10.5 million, or 15.7%,

to $77.6 million in the first quarter ended April 1, 2006, from $67.1 million in the

comparable 2005 period, primarily due to increased costs in the European

operations, the incremental costs to run an average of 25 net new stores in

North America and additional compensation expenses, including the impact of

expensing options in accordance with the new accounting rules. This also

suggests that Guess could have been forced to make adjustments to their end of

the year results due to increased pressure from their external auditors. If Guess

is consistently making drastic fourth-quarter adjustments to their financial

statements, this means their accountants are operating under an aggressive

accounting management of interim reporting.

Undoing Accounting Distortions

When an analyst sorts through all of the financial statements, they will normal

find errors in reporting or aggressive accounting practices that affect the balance

sheet, income statement, or statement of cash flows. Once the analysis is done,

the analyst must make changes as they see fit to get a more accurate

assessment of the company.

45

As stated above, the only main issue that needed to be adjusted was converting

the operating leases to a capital lease. In conclusion Guess Jeans Inc. remains

competitive in regards to this ratio, and reveals to us that it is consistent with the

industry in regards to relating its cash flow from operations to its net operating

assets, and investing in operating assets wisely. This would not be considered a

“red flag” in their accounting policies.

Financial Analysis

Core Sales Manipulation Diagnostics

Sales manipulations diagnostics are a series of ratios designed to let you know if

you can believe a companies net income. More specifically, it enables you to

compare net sales to various revenue related accounts, such as, cash from sales,

net account receivables, and inventory. The following ratios were used to analyze

Guess and their competitors over the past five years. The tables provide an

industry average and compare Guess against their competitors in the industry.

This can help to identify potential red flags and help to gain a clearer

understanding of the current accounting policies in place.

Most of the companies in this industry do a good job of collecting cash from their

sales. In the specialty retail industry most of revenue over the past five years

analyzed comes from cash over those same years. For Guess a third party takes

on the responsibility of guess’s accounts receivables and Guess, is compared with