Financial globalization

Outline

• Basic facts and figures• Does foreign capital help or hurt growth? • Financial globalization and financial crises• Financial markets and the crash of 2008• An economic interpretation• Lessons and implications for global governance of

financial markets

A large increase in gross flows

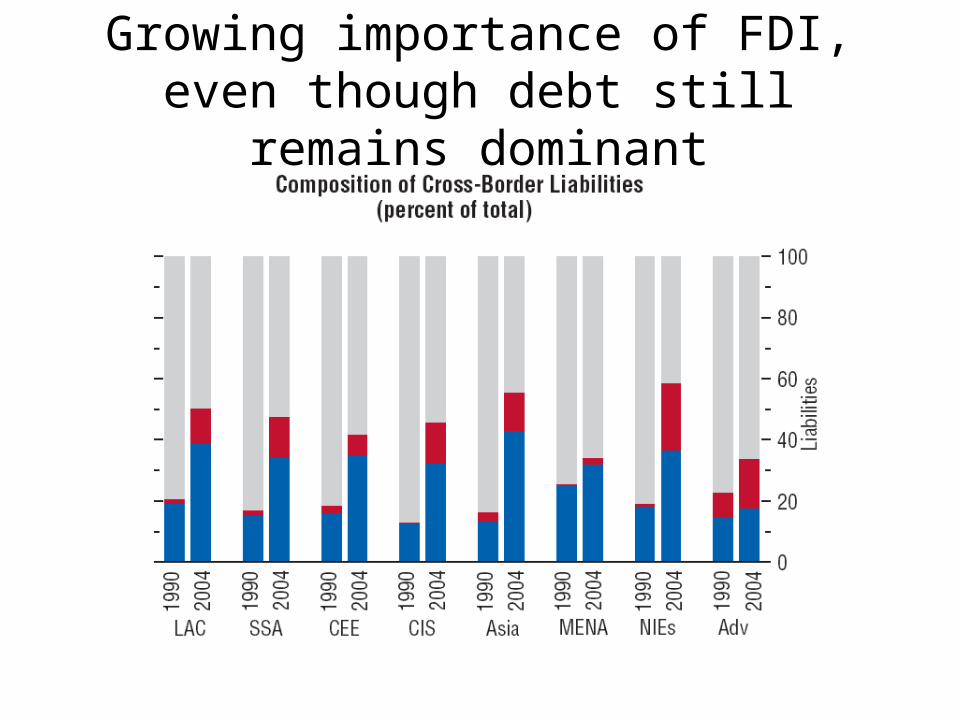

Total cross-border financial assets have more than doubled, from 58 percent of global GDP in 1 990 to 131 percent in 2004.

Growing importance of FDI, even though debt still remains dominant

A more mixed picture in terms of policies

Source: IMF, WEO 2007.

Key developments

• Spread of floating• The creation of the Euro and the Eurozone• Developing nations: from financial repression to

financial liberalization• Series of financial crises

– Latin American debt crisis, Mexico, Asian financial crisis, Russia, Brazil, Argentina, Turkey, …

• Rise of China, as an exporter of capital in the 2000s

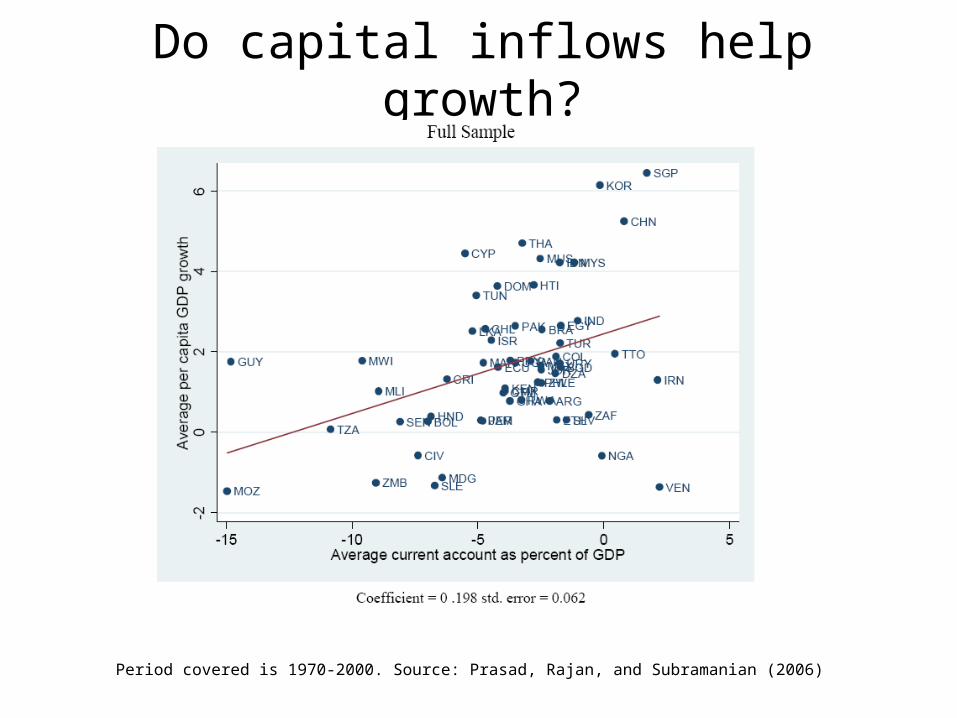

Do capital inflows help growth?

Period covered is 1970-2000. Source: Prasad, Rajan, and Subramanian (2006)

Capital inflows cause overvaluation

MUS

NIC

LKA

PHLSLV

TUNGUY

IDN

BGD

THA

IND

MOZ

ZAFPAK

COL

PRY

MAR

EGY

GTM

ECU

CHN

PER

BOL

URY

MEXZWE

MYSBRA

DZA

TUR

KOR

TTOCHL

CRI

SLE

RWA

DOM

CIV

CYP

ETH

CMR

HTI

ARG

SGP

KEN

PAN

MLI

HND

MWI

VEN

MDG

SENISR

JOR

JAM

IRN

ZMBGHA

TZA

UGA

NGA

-4-2

02

4C

omp

onen

t plu

s re

sidu

al

-100 -50 0 50 100Average Overvaluation (1970-00) from Johnson, Ostry & Subramanian

Partial relationship between a measure of overvaluation of the real exchange rate and net private flows, comprising portfolio equity, debt, and FDI, (controlling for demographics and a

dummy for oil exporting countries. Reproduced from Prasad, Rajan and Subramanian, 2007.

Undervaluation is good for growth: cross section evidence

IRQ

SYR

NGA

MNG

JPN

SURSDN

IRN

COG

BMU

ZAR

TZAGNB

LBR

ZMBANT

UGA

CAF

CHE

SWEFINGHANOR

ISL

ISR

DNKARE

TGO

IRL

BTN

VENPRIAUS

KIR

JAM

HND

MEX

CAN

MRT

TON

USA

TWN

SOMFRA

BEN

GMB

PAN

DEU

KOR

BEL

MDG

NLD

CMR

GRDBHR

CIVFSM

SEN

ARG

BWA

MLI

BHS

PRK

ITA

GBRNZLAUTKWT

SGPKENVUTGAB

KHM

FJI

LCA

JOR

PER

HKG

STPNER

BOL

GRC

LUX

BFAGTM

ETH

TCD

QAT

ESP

MDV

WSM

BLZ

PLWATGTUR

BRA

TTO

RWA

DOM

MWI

DZA

SLV

CRISLB

COL

BDIURY

LAO

SAU

OMN

BRB

MYS

ECU

MOZ

SLE

NAM

EGY

CHL

DJI

CYP

ZAF

CUB

MAC

KNA

BRN

PRYLSO

AFG

CHN

CPV

MLT

COM

VCT

DMAPRT

THA

POLMARZWE

NIC

PAK

TUN

PHL

PNGIDN

BGD

INDROM

NPL

HUN

GIN

LKA

MUS

SWZ

-.05

0.0

5e

( g

row

th80

04 |

X )

-1.5 -1 -.5 0 .5 1e( underval | X )

coef = .01821394, (robust) se = .00360935, t = 5.05

Undervaluation is good for growth: sustained real depreciations as a precondition to growth

China India

Uganda

Mexico

Financial crises over the long run

Source: Reinhart and Rogoff (2008)

Relationship between capital mobility and crises

Source: Reinhart and Rogoff (2008)

Some recent financial crises

Source: Jeanne and Ranciere (2005)

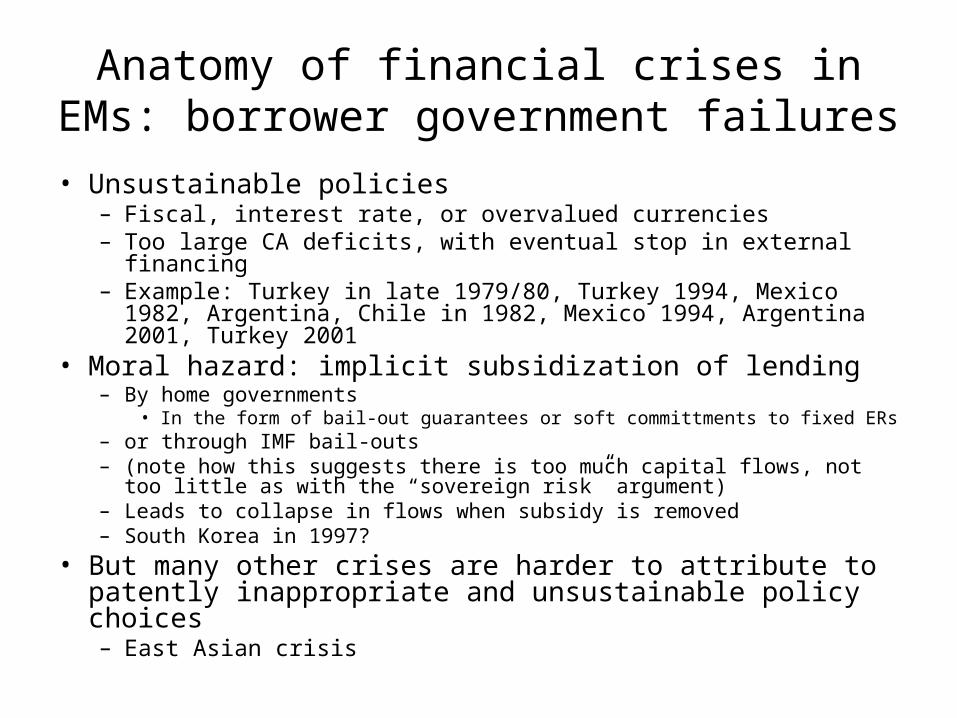

Anatomy of financial crises in EMs: borrower government failures

• Unsustainable policies– Fiscal, interest rate, or overvalued currencies– Too large CA deficits, with eventual stop in external financing– Example: Turkey in late 1979/80, Turkey 1994, Mexico 1982,

Argentina, Chile in 1982, Mexico 1994, Argentina 2001, Turkey 2001

• Moral hazard: implicit subsidization of lending– By home governments

• In the form of bail-out guarantees or soft committments to fixed ERs– or through IMF bail-outs– (note how this suggests there is too much capital flows, not too little as

with the “sovereign risk” argument)– Leads to collapse in flows when subsidy is removed– South Korea in 1997?

• But many other crises are harder to attribute to patently inappropriate and unsustainable policy choices– East Asian crisis

Anatomy of financial crises in EMs: international financial market pathologies

• Financial panic– self-fulfilling liquidity shortages (“bank runs”) provoked by the

absence of a true international lender of last resort– East Asia in 1997?

How financial panics work

• Suppose a country faces a temporary shock and needs resources in the amount K in order not to default. Each of two lenders has up to K/2 to lend. Will they make the loan? Not necessarily, unless they can coordinate their actions.

• There are two stable equilibria in the above game, one where each bank gives a loan, and one where neither does. As the number of lenders increase, it may become more difficult to coordinate on the good equilibrium. In the domestic economy, a national lender of last resort and orderly bankruptcy proceedings limit such panics and creditor grab races.

Lender B give loan don’t give loan

give loan (1+r)K/2, (1+r)K/2 -K/2, 0 Lender A don’t give

loan 0, -K/2 0, 0

Financial crises occur under all types of ER arrangements

• Turkey (2000-2001): an ERBS• Argentina (2001-2002): a GS-type experiment• U.S.: floating

The financial crash of 2008

• A housing bubble• Fed by financial innovation (securitization)• … large capital inflows into U.S. (the “saving glut”)• … and poor regulation and supervision of risk-taking by

financial intermediaries• When it bursts, it spreads globally through

– Flight to safety in financial markets– De-leveraging and reduced credit flows– Sharp fall in private-sector wealth– And the induced effects of the above on aggregate demand and

activity

A tale of financial innovationWho wouldn’t want credit markets to serve the cause of home ownership? So:

• introduce some real competition into the mortgage lending business by allowing non-banks to make home loans

• let them offer creative, more affordable mortgages to prospective homeowners not well served by conventional lenders.

• enable these loans to be pooled and packaged into securities that can be sold to investors

– reducing risk in the process. • divvy up the stream of payments on these home loans further into tranches

of varying risk– compensating holders of the riskier kind with higher interest rates

• call on credit rating agencies to certify that the less risky of these mortgage-backed securities are safe enough for pension funds and insurance companies to invest in

• just in case anyone is still nervous, create derivatives that allow investors to purchase insurance against default by issuers of those securities.

Who or what is the culprit? (1)

• unscrupulous mortgage lenders who devised credit terms?– such as “teaser” interest rates and prepayment penalties– perhaps, but these strategies would not have made sense for lenders

unless they believed house prices would keep on rising • a housing bubble that developed in the late 1990s?

– and the reluctance of Alan Greenspan’s Fed to burst it?– even so, the explosion in collateralized debt obligations (CDOs) and

other securities went far beyond what was needed to sustain mortgage lending

– especially true of credit default swaps, which became an instrument of speculation instead of insurance and reached an astounding $62 trillion in volume.

• Irresponsible financial institutions of all types leveraging themselves to the hilt in pursuit of higher returns?

• credit rating agencies that fell asleep on the job?

• high-saving Asian households and dollar-hoarding foreign central banks that produced a global savings “glut”?

– which pushed real interest rates into negative territory, in turn stoking the U.S. housing bubble while sending financiers on ever-riskier ventures

• macroeconomic policy makers who failed to get their act together and move in time to unwind large and unsustainable current-account imbalances?

• the U.S. Treasury, which played its hand poorly as the crisis unfolded?– bad as things were, what caused credit markets to seize up was Paulson’s

decision to make an example of Lehman Brothers by refusing to bail it out. – might it have been better to do with Lehman what he had already done with Bear

Stearns and would have had to do in a few days with AIG: save them with taxpayer money.

• all (or none) of the above?

We can be certain that no future regulation will prevent similar occurrences unless leverage (i.e., borrowing) itself is directly restrained

Who or what is the culprit? (2)

An economic interpretation

The theory of second-best:

“… in an economy with some unavoidable market failure in one sector, there can actually be a decrease in efficiency due to a move toward greater market perfection in another sector…. Thus, it may be optimal for the government to intervene in a way that is contrary to laissez faire policy. This suggests that economists need to study the details of the situation before jumping to the theory-based conclusion that an improvement in market perfection in one area implies a global improvement in efficiency.”

-- from Wikipedia

An economic interpretation

Financial markets operate in a highly second-best environment (1)a) Inherent market imperfections

• information asymmetries• agency problems• systemic externalities• … that can be targeted only imperfectly by

supervision and regulation• … and therefore cannot be fully neutralized even

under the best of circumstances– As the financial crash of 2008 has made painfully clear

An economic interpretation

Financial markets operate in a highly second-best environment (2)b) … augmented by the political fragmentation

of the world economy• sovereign risk• absence of a global regulator• absence of an ILLR• resulting in:

– small net flows– incomplete risk sharing– inability to prevent import of “toxic” assets (cf. trade in

damaged goods”)– EMs as innocent victims of the subprime crisis

An economic interpretation

Financial markets operate in a highly second-best environment (3)

c) … exacerbated by market failures associated with the structural transformation process in developing nations

• Non-traditional tradable economic activities as the dynamic source of economic growth – The challenge of economic development is to shift resources

from traditional to modern (tradable) activities

• Key role of the RER in supporting such activities– The RER determines the relative profitability of investment in

tradables

– Capital inflows cause overvaluation, and move the RER in the wrong direction

Consequences: financial globalization syndromes

• Absence of international risk diversification• Foreign finance is least available when most

needed (and vice versa)• Financial crises• Capital inflows are often bad news for economic

growth

An economic interpretation

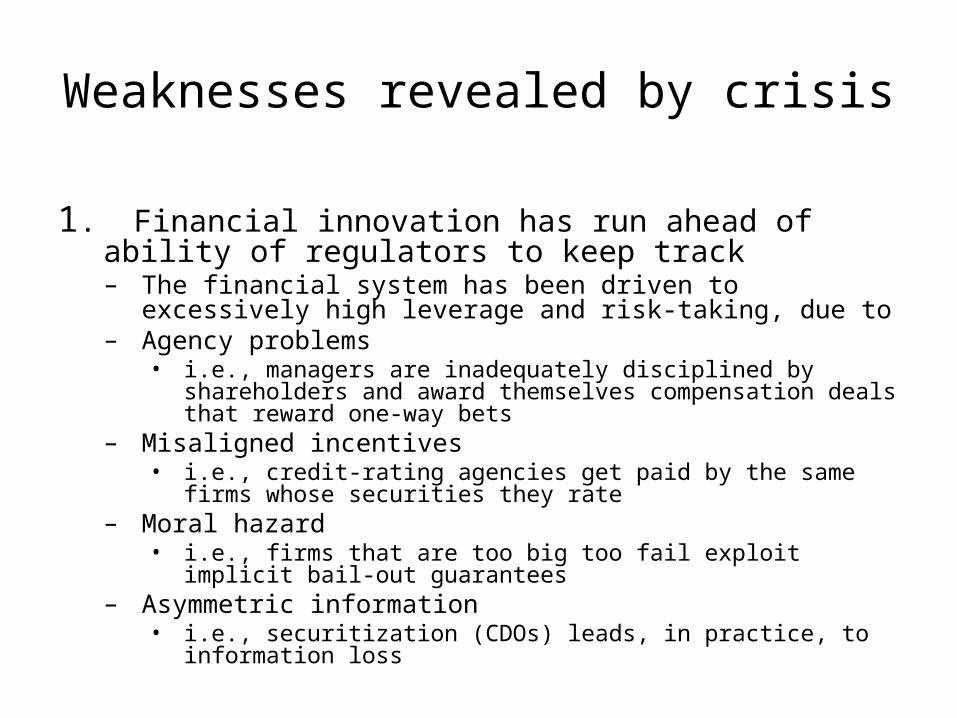

Weaknesses revealed by crisis

1. Financial innovation has run ahead of ability of regulators to keep track– The financial system has been driven to excessively high

leverage and risk-taking, due to – Agency problems

• i.e., managers are inadequately disciplined by shareholders and award themselves compensation deals that reward one-way bets

– Misaligned incentives• i.e., credit-rating agencies get paid by the same firms whose

securities they rate– Moral hazard

• i.e., firms that are too big too fail exploit implicit bail-out guarantees– Asymmetric information

• i.e., securitization (CDOs) leads, in practice, to information loss

Weaknesses revealed by crisis

2. Global macro imbalances are a source of instability– Epitomized by the U.S-China trade relationship

• China’s growth model has come to rely increasingly on its trade surplus with the U.S.

• Which, however, was unsustainable both for economic and political reasons

• Note contrast between liberal and mercantile models of the economy and the fragility created by the interaction of the two

– And by huge build-up of reserves in EMEs• Motivated by self-insurance against financial whiplash

– Result is a “liquidity glut”• Leading to bubble in asset prices

• And search for high-yield, but riskier investments

Weaknesses revealed by crisis

3. There are no adequate mechanisms to respond to financial crises at the global level

– Regulatory response fragmented, despite clear spillovers– Fiscal stimulus not coordinated, despite clear spillovers– No lender-of-last resort to counter the “sudden stop”

experienced by emerging and developing countries, which were innocent by-standers

• Large build-up of reserves has provided at best partial cushion

Weaknesses revealed by crisis

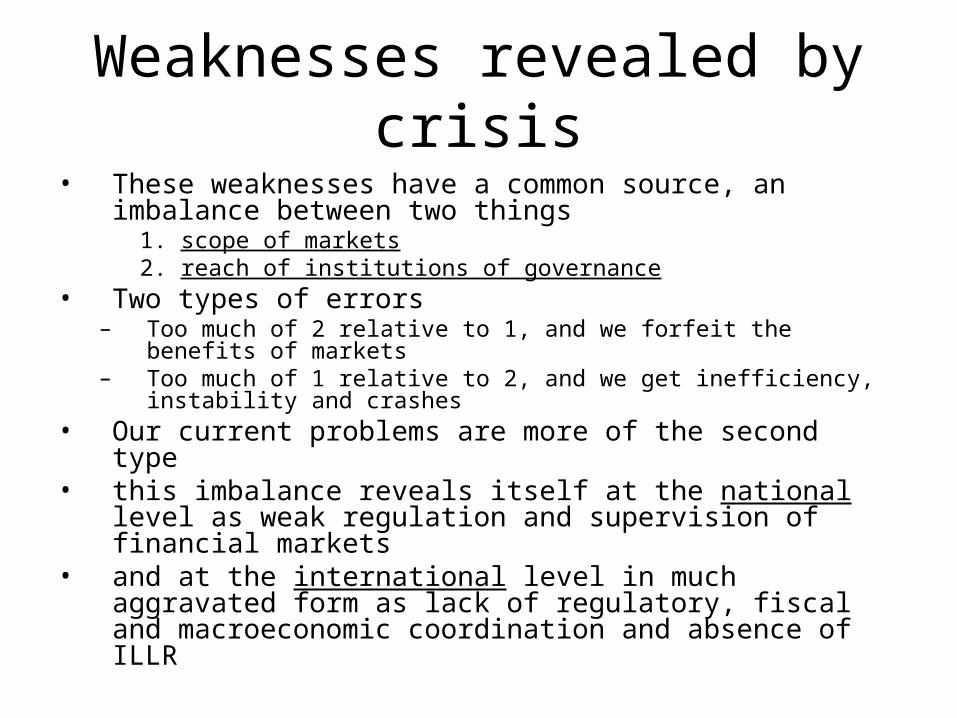

• These weaknesses have a common source, an imbalance between two things

1. scope of markets 2. reach of institutions of governance

• Two types of errors– Too much of 2 relative to 1, and we forfeit the benefits of

markets– Too much of 1 relative to 2, and we get inefficiency, instability

and crashes • Our current problems are more of the second type• this imbalance reveals itself at the national level as

weak regulation and supervision of financial markets• and at the international level in much aggravated form

as lack of regulatory, fiscal and macroeconomic coordination and absence of ILLR

Responses

• As a matter of logic, the imbalance can be corrected in one of two ways– Restrict the scope of markets

• “throw sand in the wheels of finance”– Broaden and deepen the scope of regulatory and governance

arrangements• Current approach focuses largely on second strategy

– Regulatory reforms at home– Institution-building at the international level

• Financial Stability Board (the old FSF, with enlarged membership and responsibilities)

• A revamped IMF with larger resources• Greater international oversight over currency practices and trade

imbalances

Problems with the global strategy

• Does (can) it go far enough?– What’s on the agenda so far is quite limited– Analogy with domestic markets

• Financial markets require extensive institutional infrastructure to function well (including corporate governance, bankruptcy, regulation, supervision, deposit insurance, LLR)

– In a world that is politically divided, could we ever create the global institutional infrastructure to underpin a truly global financial system

Problems with the global strategy

• Does it recognize the need for national diversity?– Preferences for risk (financial innovation) versus stability may

differ across countries– Implementation capacity differs as well, requiring different

approaches– In developing countries, there may be scope for “development

finance” under different rules – So convergence towards common set of “best practices” in

regulating finance may not even be desirable

Problems with the global strategy

• Does it provide a solution to the Chinese growth conundrum?– Stimulating domestic aggregate demand in China reduces global

imbalances but only at the expense of lower economic growth in the longer run

• That is because what China (and other developing countries) need to grow is demand for tradables, not demand across the board

– Economically ideal solution is to let China target industrial policies on structural transformation while the currency is allowed to appreciate to eliminate spillovers on the trade balance

– Which would run against WTO prohibitions on subsidies– And in any case, not clear if Chinese leadership have thought

their way out of this conundrum

Problems with the global strategy

• Does it not rely too much on willingness and ability of major countries to provide leadership and surrender sovereignty?– Political constituency for globalization will remain (at best) weak

in the advanced countries – There will be no “hegemon” to impose (or pay for) global rules

• U.S. and EU weakened; China not strong or dominant enough

– So global leadership will be in short supply

– And the baseline trend will be towards some degree of de-

globalization in the medium-term