Double-entry System

Process of accounting starts from posting of transactions. Every transaction in accounting has an impact on 2 accounts and double entry system is a system that recognizes and records both the aspects of the transactions,

E.g., on purchase of furniture either the cash balance will be reduced or a liability to the supplier will arise.

Different kind of accounts

1. PERSONAL ACCOUNT – These are accounts of parties with whom the business is carried on. Personal accounts may be:

Accounts of natural or physical persons. Ex: Ram Account, Kris Account

Accounts of artificial or legal persons. Ex: ABC & Co

2. REAL ACCOUNT - These are asset accounts that appear in the Balance Sheet. They are referred to as Real Accounts (or Permanent Accounts) as these are owned by businesses and the balances in these accounts at the end of an accounting period will be carried over to the next period.

Ex, Cash, Land, building etc.

3. NOMINAL ACCOUNT - These are accounts of expenses and losses which a business incurs and income and gains which a business earn in the course of business.

Ex: Rent account, Interest account.

Golden Rules of Accounting

Income Statement The first statement prepared is the Income Statement. The Income Statement reports a business’ performance for the period.

A simple format for an income statement is:

Revenues – Expenses = Net Income

Income Statement

Revenues are earned for the sale of goods or services. Note that revenues occur when the sale is made. The payment may or may not have been received.

Examples of revenues include sales, service revenue and interest revenue.

Income Statement

Expenses are incurred when a business receives goods and services. Like revenues, payment may or may not have been made.

Examples of expenses include salaries expense, utility expense and interest expense.

Income Statement

Most businesses require more information from their businesses than a simple income statement can provide. Therefore, they use a multi-step income statement format.

A format for a multi-step income statement is:

Income Statement

Sales revenue- Cost of goods sold Gross profit- Operating expenses Income from operations+/- Non-operating items Income before taxes- Income taxes Net income

Income Statement

Cost of goods sold represents the expense a business incurred to buy or make a product for resale.

Example - a book store buys a book for $25 and then sells it for $32. The cost of goods sold is $25.

Income Statement

Operating expenses are the usual expenses incurred in operating a business.

Accounts such as salaries expense, utility expense, and depreciation expenses are all shown in this section.

Income Statement

Non-operating items are revenue, expenses, gains and losses that do not relate to the company’s primary operations.

Accounts include interest expense and gains and losses of the sale of equipment and investments.

Balance Sheet

The purpose of the balance sheet is to report the financial position of an accounting entity at a particular point in time.

The basic format for the balance sheet is: Assets = Liabilities + Equity

Balance Sheet

Assets are economic resources owned by a company.

Examples include cash, accounts receivable, supplies, buildings and equipment.

Balance Sheet

Liabilities are the company’s debt or obligations.

Examples are accounts payable, unearned revenues and bonds payable.

Balance Sheet

Equity is the residual balance. Assets – liabilities = equity. Equity is commonly called stockholders’

equity if the business is a corporation as it represents the financing provided by the stockholders along with the earnings from the business not paid out as dividends.

Balance Sheet

There are two different types of assets shown on a balance sheet. These are current assets and non-current assets.

Current assets+ Non-current assets Total assets

Balance Sheet

Current assets are assets that will be used or turned into cash within one year.

Examples include cash, accounts receivable, inventory, short-term investments, supplies and prepaids.

Balance Sheet

Non-current assets comprise the remainder of the assets.

These include accounts such as: long-term investments, land, building, equipment and patents.

Balance Sheet

There are two different types of liabilities shown on a balance sheet – current liabilities and long-term liabilities.

Current liabilities+ Long-term liabilities Total liabilities

Balance Sheet

Current liabilities are obligations that will be paid in cash (or other services) or satisfied by providing service within the coming year.

Examples include accounts payable,, and taxes payable.

Balance Sheet

Long-term liabilities are obligations that will not be paid or satisfied within the year.

Examples include long term loan, debentures etc

Balance Sheet

Stockholders’ Equity is divided into two categories: share capital and retained earnings.

Share capital+ Retained earnings Total stockholders’ equity

Balance Sheet

Share capital is the amount of cash (or other assets) provided by the shareholders.

Retained earnings is the total earnings that have not been distributed to owners as dividends.

The Balance Sheet

Current assets+ Non-current assets Total assets

Current liabilities+ Long-term liabilities+ Stockholders’ equity Total liabilities and stockholders’ equity

The End

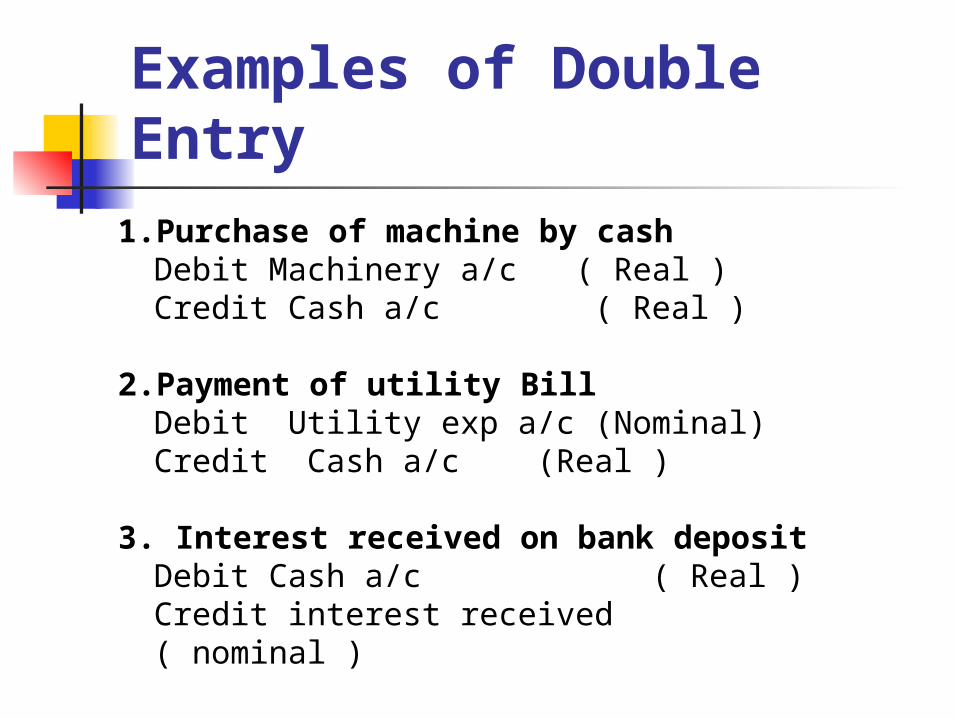

Examples of Double Entry

1. Purchase of machine by cashDebit Machinery a/c ( Real )Credit Cash a/c ( Real )

2.Payment of utility BillDebit Utility exp a/c (Nominal)Credit Cash a/c (Real )

3. Interest received on bank depositDebit Cash a/c ( Real )Credit interest received ( nominal )

Example Problem

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Common Stock 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Step One

Classify the accounts as assets, liabilities, equity, revenue or expenses.

Assets

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Common Stock 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Assets, Liabilities,

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Common Stock 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Assets, Liabilities, Equity

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Share capital 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Assets, Liabilities, Equity, Revenues

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Share capital 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Assets, Liabilities, Equity, Revenues, Expenses

Cash 5,000 Sales 100,000

Utility Expense 8,000 Buildings 65,000

Share capital 45,000 Accounts Payable 12,000

Supplies 4,000 Cost of Goods Sold 58,000

Interest Expense 5,000 Additional Paid in Capital

20,000

Bonds Payable 40,000 Supplies Expense 3,000

Salaries Expense 16,000 Accounts Receivable

10,000

Inventories 45,000 Retained Earnings 5,000 (beg. bal.)

Income Tax Rate 30%

Step Two

Prepare the Income Statement. Sales revenue- Cost of goods sold Gross profit- Operating expenses Income from operations+/- Non-operating items Income before taxes- Income taxes Net income

Income Statement

Sales 100,000

- Cost of Goods Sold

-58,000

Gross Margin 42,000

- Operating Expenses

-27,000

Income from Operations

15,000

- Non-operating Items

-5,000

Income before Taxes

10,000

- Income Taxes -3,000

Net Income 7,000

Income Statement

Sales 100,000

- Cost of Goods Sold

-58,000

Gross Margin 42,000

- Operating Expenses

-27,000

Income from Operations

15,000

- Non-operating Items

-5,000

Income before Taxes

10,000

- Income Taxes -3,000

Net Income 7,000

Operating expenses include:

Utility expense 8,000Salaries expense 16,000Supplies expense 3,000

Income Statement

Sales 100,000

- Cost of Goods Sold

-58,000

Gross Margin 42,000

- Operating Expenses

-27,000

Income from Operations

15,000

- Non-operating Items

-5,000

Income before Taxes

10,000

- Income Taxes -3,000

Net Income 7,000

Non-operating items include:

Interest expense 5,000

Income Statement

Sales 100,000

- Cost of Goods Sold

-58,000

Gross Margin 42,000

- Operating Expenses

-27,000

Income from Operations

15,000

- Non-operating Items

-5,000

Income before Taxes

10,000

- Income Taxes -3,000

Net Income 7,000

Income taxes = Income before taxes * Income tax rate

10,000 * 30% = 3,000

Step Three

Prepare the Statement of Retained Earnings.

Beg. balance, retained earnings+ Net income- Dividends End. balance, retained earnings

Statement of Retained Earnings

Beginning Balance, Retained Earnings

5,000

+ Net Income +7,000

- Dividends -0

Ending Balance, Retained Earnings

12,000

Net Income is brought forward from the Income Statement.

Step Four

Prepare the Balance Sheet.

Current assets+ Non-current assets Total assets

Current liabilities+ Long-term liabilities+ Stockholders’ equity Total liabilities and stockholders’ equity

Balance SheetCurrent Assets: Current

Liabilities:

Cash 5,000 Accounts Payable 12,000

Accounts Receivable

10,000 Long-term liabilities:

Inventories 45,000 Bonds Payable 40,000

Supplies 4,000 Stockholders’ Equity:

Non-Current Assets:

Share capital 45,000

Buildings 65,000 Additional Paid in Capital

20,000

Retained Earnings 12,000

Total Assets 129,000 Total Liabilities and Equity

129,000

Balance SheetCurrent Assets: Current

Liabilities:

Cash 5,000 Accounts Payable 12,000

Accounts Receivable

10,000 Long-term liabilities:

Inventories 45,000 Bonds Payable 40,000

Supplies 4,000 Stockholders’ Equity:

Non-Current Assets:

Share capital 45,000

Buildings 65,000 Additional Paid in Capital

20,000

Retained Earnings 12,000

Total Assets 129,000 Total Liabilities and Equity

129,000

End. Bal. is brought forward from the Statement of Retained Earnings

The End