Financing housing since the crisis: examples in Europe

Christine M E Whitehead LSE and CCHPR, University of Cambridge

DRAFT – NOT FOR QUOTATION

“Housing finance in Europe in times of crisis” SIEPS

Swedish Institute for European Policy Studies

Stockholm11 April 2013

Introduction: context of the research• Based on ENHR Housing Finance working

group survey together with published data• Number 3 in a series of papers on mortgage

and housing market developments before and after the financial crisis by Scanlon, Lunde and Whitehead (see final slide)

• Covers aspects of the consequences of the crisis

• Credit crunch has turned into a debt crisis and recession in many countries - with impacts back on to mortgage and housing markets

Research question, timing and methodology

• What has happened to housing and mortgage finance markets since 2009?

• How have governments and lenders responded?

• Data gathering mainly early 2011with updates 2012 and 2013

Housing market context

• Upswing in early 2000s: remarkable (but by no means total) synchronisation of markets in developed countries

• Peak not simultaneous: 2006 / 2007/ 2008

• Downswing: initially similar in countries with significant debt, but then variability in trajectories

Three Groups?• Group 1: continuing and sometimes

very large declines in prices and activity – although a subset now stabilising

• Group 2: more limited decline; some recovery; and then often some reversal

• Group 3: continued (although usually much slower) growth

• Another group where relatively little debt finance (mostly Eastern Europe)

Trends in house prices: Initial fall in real house prices from peak and recent price changes

Country % change in real house prices: peak

in 2006/7/8 to 2009:4 (or trough if

earlier)

% change in real house prices: peak in 2006/7/8 to 2012:4 (or 2012:3 for

some countries)

Latest year: nominal house price change to 2012:4 (or

2012:3)

Latest year: real house price change to

2012:4 (or 2012:3)

Group 1: Nominal and real prices fallingUK -15.9 % -17.2 % (2012:3)

+ 1.9 %

(2012:3)

-0.8 %Denmark -19.7 % -28.3 %

(2012:3)

-2.7 %

(2012:3)

-4.7 %Spain -11.3 % -34.2 % (2012:4)

-10.5 %

(2012:4)

-12.0 %Ireland -24.7 % -48.1 % (2012:3)

-6.1 %

(2012:4)

-7.4 %The Netherlands

-4.4 % -21.4 % (2012:4)

-6.9 %

(2012:4)

-9.7 %

Country % change in real house prices: peak

in 2006/7/8 to 2009:4 (or trough

if earlier)

% change in real house prices: peak in 2006/7/8 to 2012:4 (or 2012:3 for

some countries)

Latest year: nominal house price change to 2012:4 (or

2012:3)

Latest year: real house price change to 2012:4

(or 2012:3)

Group 2: Peak in house prices in 2007, then price drop to a 2009 turnaround – and sometimes a new house price drop in 2011-12

US - 18.8 % - 25.8 % (2012:3)

+ 3.0 %

(2012:3)

+ 1.5 %

Finland - 8.8 % + 0.1 % (2012:4)

+ 3.0 %

(2012:4)

+ 1.5 %

France - 9.6 % - 4.0 %

(2012:3)

-1.3 %

(2012:3)

-2.9 %

Sweden - 6.3 % 0.1 % (2012:4)

2.1 %

(2012:3)

0.6 %

Country % change in real house prices: peak

in 2006/7/8 to 2009:4 (or trough

if earlier)

% change in real house prices: peak in

2006/7/8 to 2012:4 (or 2012:3 for some

countries)

Latest year: nominal house price change to 2012:4 (or

2012:3)

Latest year: real house price change to 2012:4

(or 2012:3)

Group 3a: Real prices upNorway For 2007:3 to

trough 2008:4:

-11.6 %

+ 14.4 % (2012:3)

+ 6.6 %

(2012:3)

+ 5.2 %

Belgium For 2008:2 to trough 2009:2:

-1.0 %

+ 3.4 %

(2012:3)

+ 2.0 %

(2012:3)

- 0.5 %

Canada For 2008:3 to trough 2009:2:

-6.6 %

+ 10.1 % (2012:3)

+ 3.3 %

(2012:3)

+ 2.4 %

Group 3b: countries with recently relatively stable real house prices – and with actually increasing housing prices.

Germany -2.4 %

+ 12.9 % (2012:3)

+ 10.2 %

(2012:3)

+ 8.6 %

Switzerland -2.1 %

+ 18.0 % (2012:3)

+ 3.4 %

(2012:3)

+ 4.1 %

Figure 1: Real house prices 1970:1 – 2012:4 - 6 countries with falling prices since the 2006-07 peaks

Source: OECD house price statistics of 28th of January 2013.

Figure 2: Real house prices 1970:1 – 2012:4 – 4 countries: upturn, peak in 2007, some house price

drop, a 2009 turn around – and a new house price drop in 2011-12

Source: OECD house price statistics of 28th of January 2013.

Figure 3: Real house prices 1970:1 – 2012:4 - 4 countries with actually increasing real house prices

Source: OECD house price statistics of 28th of January 2013.

Figure 4: Real house prices 1970:1 – 2012:3 - 2 countries with recently relatively stable real house prices – and

with actually slightly increasing real house prices.

Source: OECD house price statistics of 28th of January 2013.

Figure 5: Indices of housing transactions, 2006 – 2010 (2006 = 100) Group 1: price falls

Figure 6: Indices of housing transactions, 2006 – 2010 (2006=100) Group 2: double dip

Figure 7: Indices of housing transactions, 2006 – 2010 (2006=100) Group 3: rising prices

Trends in Mortgage Markets

• Rapid declines in mortgage lending – supply or demand determined?

• Increases in arrears and foreclosures – more complex patterns than expected, partly because of government intervention based on past experience

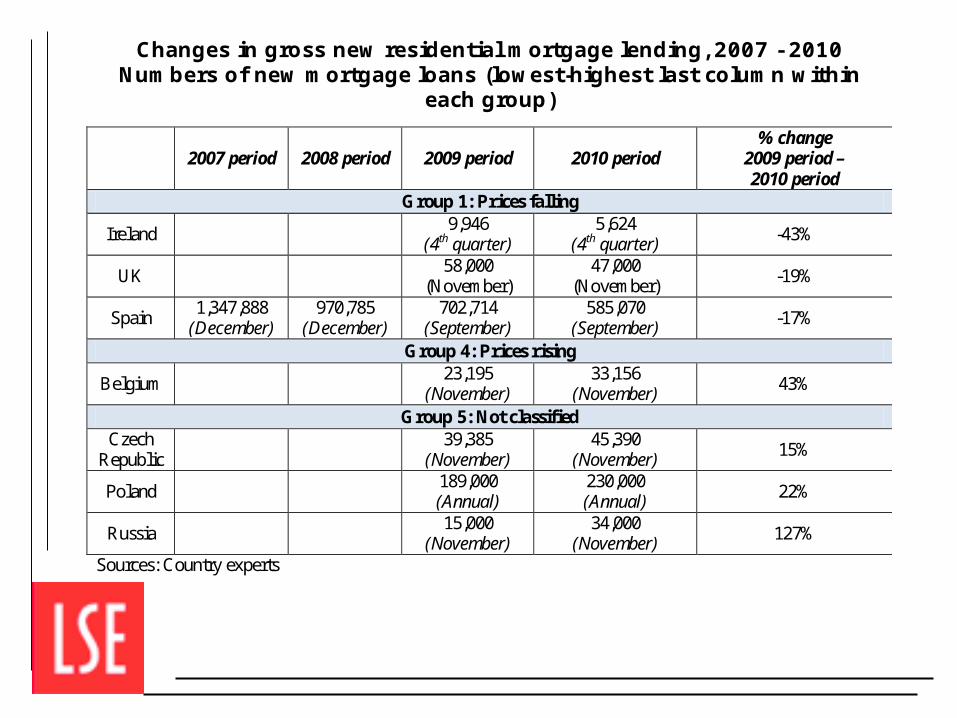

Changes in gross new residential mortgage lending, 2007 - 2010

Numbers of new mortgage loans (lowest-highest last column within each group)

2007 period 2008 period 2009 period 2010 period

% change 2009 period – 2010 period

Group 1: Prices falling

Ireland 9,946

(4th quarter) 5,624

(4th quarter) -43%

UK 58,000

(November) 47,000

(November) -19%

Spain 1,347,888

(December) 970,785

(December) 702,714

(September) 585,070

(September) -17%

Group 4: Prices rising

Belgium 23,195

(November) 33,156

(November) 43%

Group 5: Not classified Czech

Republic 39,385

(November) 45,390

(November) 15%

Poland 189,000

(Annual) 230,000 (Annual)

22%

Russia 15,000

(November) 34,000

(November) 127%

Sources: Country experts

WS-01: Housing Finance and Regulation

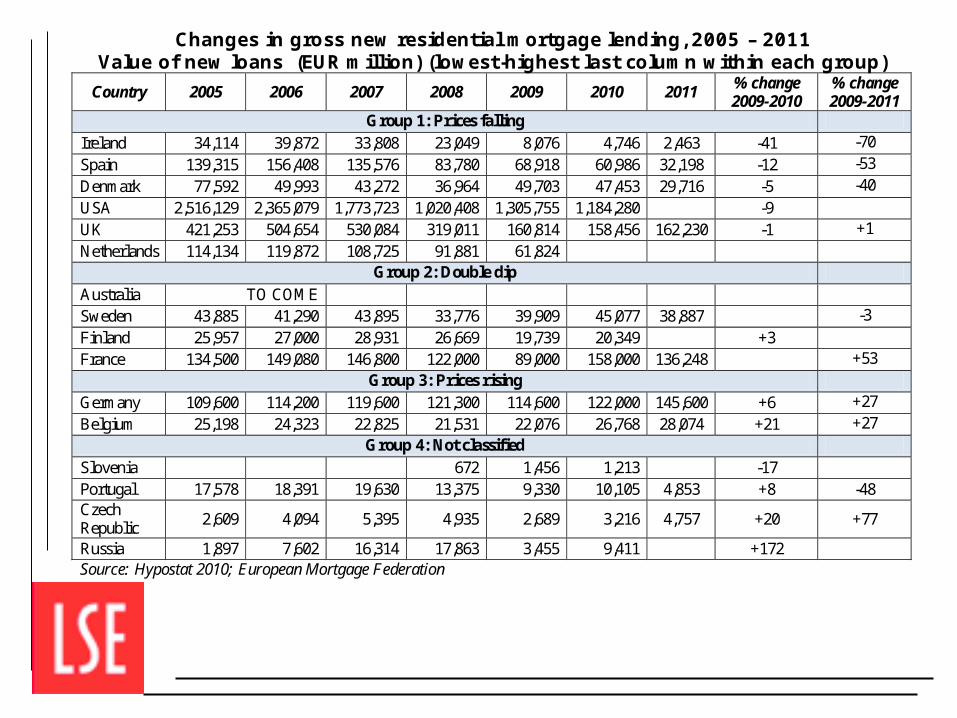

Changes in gross new residential mortgage lending, 2005 – 2011 Value of new loans (EUR million) (lowest-highest last column within each group)

Country 2005 2006 2007 2008 2009 2010 2011 % change 2009-2010

% change 2009-2011

Group 1: Prices falling Ireland 34,114 39,872 33,808 23,049 8,076 4,746 2,463 -41 -70

Spain 139,315 156,408 135,576 83,780 68,918 60,986 32,198 -12 -53

Denmark 77,592 49,993 43,272 36,964 49,703 47,453 29,716 -5 -40

USA 2,516,129 2,365,079 1,773,723 1,020,408 1,305,755 1,184,280 -9

UK 421,253 504,654 530,084 319,011 160,814 158,456 162,230 -1 +1

Netherlands 114,134 119,872 108,725 91,881 61,824 Group 2: Double dip

Australia TO COME

Sweden 43,885 41,290 43,895 33,776 39,909 45,077 38,887 -3

Finland 25,957 27,000 28,931 26,669 19,739 20,349 +3

France 134,500 149,080 146,800 122,000 89,000 158,000 136,248 +53 Group 3: Prices rising

Germany 109,600 114,200 119,600 121,300 114,600 122,000 145,600 +6 +27

Belgium 25,198 24,323 22,825 21,531 22,076 26,768 28,074 +21 +27 Group 4: Not classified

Slovenia 672 1,456 1,213 -17

Portugal 17,578 18,391 19,630 13,375 9,330 10,105 4,853 +8 -48 Czech Republic

2,609 4,094 5,395 4,935 2,689 3,216 4,757 +20 +77

Russia 1,897 7,602 16,314 17,863 3,455 9,411 +172 Source: Hypostat 2010; European Mortgage Federation

WS-01: Housing Finance and Regulation

Percentage of residential mortgages over three months in arrears, late 2007- late 2010 (highest-lowest last column within each group)

2007 period 2008 period 2009 period 2010 period Group 1: Prices falling

Ireland 1.21

(December 06) 1.44

(June) 3.6

(4th quarter) 5.7

(4th quarter)

Spain 0.95

(December) 2.40

(December) 3.0

(September) 2.58

(September)

UK 1.08

(2nd half) 1.88

(4th quarter) 2.42

(3rd quarter) 2.13

(3rd quarter)

USA 0.85

(December) 1.88

(December) TO COME

Denmark 0.14

(December) 0.32

(December) 0.57

(November) 0.42

(November) Group 2: Double dip

Sweden 3.5

(November) 1.5

(November)

Australia < 1

November < 1

(November) 0.7

(November) 0.7

(November) Group 3: Prices rising

Belgium* 2.1

(November) 2.1

(November)

Norway 0.7

(November) 0.7

(November) 1.6

(November) 1.7

(November) Group 4: Unclassified

Russia 3.5

(December) 5.4

(December) 6.9

(November) 7.0

(November)

Portugal 1.3

(November) 1.5

(November) 5.2

(November) 5.2

(November)

Czech 2.2

(December) 2.9

(November) Source: Scanlon et al. (2011) and questionnaires * Borrowers with at least one overdue payment

Reasons for Differential Arrears• Careful lending – eg France; Germany• Variable interest rates/lower rates of

unemployment than expected – UK; Denmark; Netherlands?

• Formal forbearance procedures – Ireland; UK

• Legal/cultural attitudes to foreclosure – at one extreme Spain – at the other France

WS-01: Housing Finance and Regulation

Foreclosures late 2009 – late 2010 (alphabetical within each group)

2009 period 2010 period Group 1: Prices falling

Denmark 417

(November) 426

(November)

Ireland 0.01 %

(November) 0.01 %

(November)

Netherlands 550

(November) n.a.

Spain 92,632

(Annual) 118,000 (Annual)

UK 12,200 – 0.11 %

(3rd quarter) 8,900–0.08% (3rd quarter)

USA

TO COME

Group 2: Double dip

Australia App 0

(November) App 0

(November)

Sweden 1%

(November) < 1 %

(November) Group 3: Prices rising

Belgium 1335

(November) 1478

(November)

Norway 486

(November) 704

(November)

Mortgage Products

• Credit assessments tightened• Increasing limitations on range of mortgage

products – demand? Institutional response? Increased regulation?

• Interest –only down being treated like annuity mortgages (UK) and special tax provisions (Netherlands)

• Limitations on maximum LTV - Sweden• But evidence does not suggest that

products themselves were are major source of arrears/foreclosures

WS-01: Housing Finance and Regulation

Changes in availability of mortgage products January 2009 – May 2011 (alphabetical by country in each group)

Interest-only High LTV Long terms High loan-to-income

Reverse Other

Group 1: Prices falling

Denmark Up No change No change Credit evaluation tightened

Not common Fees increased by some banks

Ireland Down Down No data No data No data Netherlands Down Up Down Spain Not available Down Down Down Up

UK Down Down Credit evaluation tightened

Little change

Group 2: Double dip

Australia Up Down Little change in equivalent metric

Little used

Finland No change No change No change No change No change No change Group 3: Prices rising

Belgium Down Not legal Germany No change Down No change Down Up

Norway Down Down Down ‘Frame loans’ limited

Group 4: Unclassified

Austria Down Down Max 20 yrs Limited availability

Little demand

Foreign currency loans down.

Czech Down but not much used

Down No change Down Not legal Self-certification down

Poland Not available Not available Portugal Down Down Down Not available Source: Country experts

WS-01: Housing Finance and Regulation

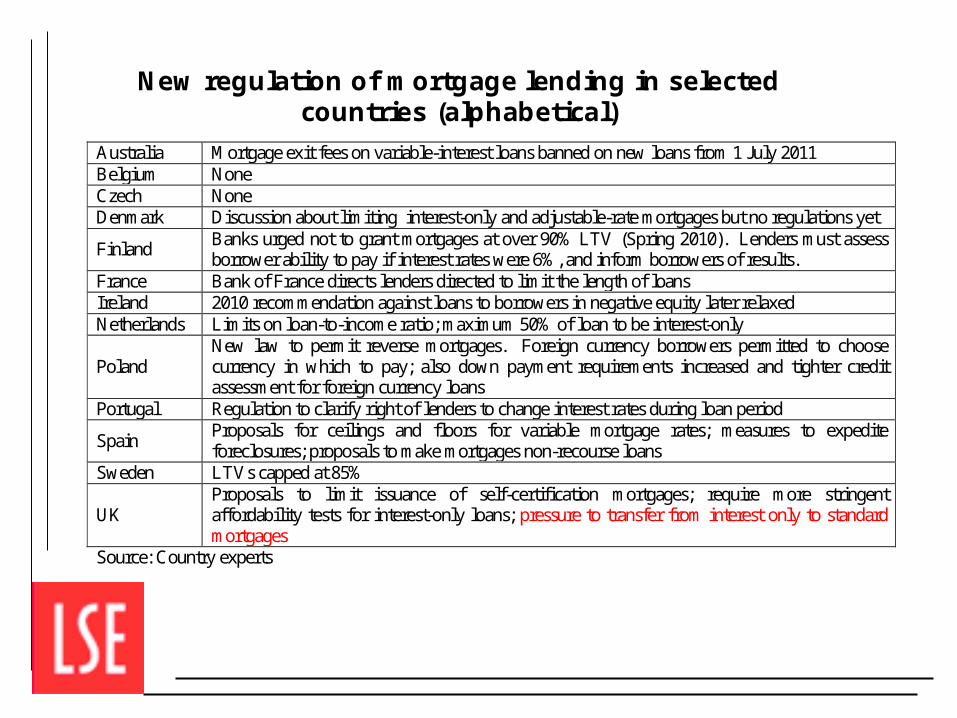

New regulation of mortgage lending in selected countries (alphabetical)

Australia Mortgage exit fees on variable-interest loans banned on new loans from 1 July 2011 Belgium None Czech None Denmark Discussion about limiting interest-only and adjustable-rate mortgages but no regulations yet

Finland Banks urged not to grant mortgages at over 90% LTV (Spring 2010). Lenders must assess borrower ability to pay if interest rates were 6%, and inform borrowers of results.

France Bank of France directs lenders directed to limit the length of loans Ireland 2010 recommendation against loans to borrowers in negative equity later relaxed Netherlands Limits on loan-to-income ratio; maximum 50% of loan to be interest-only

Poland New law to permit reverse mortgages. Foreign currency borrowers permitted to choose currency in which to pay; also down payment requirements increased and tighter credit assessment for foreign currency loans

Portugal Regulation to clarify right of lenders to change interest rates during loan period

Spain Proposals for ceilings and floors for variable mortgage rates; measures to expedite foreclosures; proposals to make mortgages non-recourse loans

Sweden LTVs capped at 85%

UK Proposals to limit issuance of self-certification mortgages; require more stringent affordability tests for interest-only loans; pressure to transfer from interest only to standard mortgages

Source: Country experts

Impact on Investment• Much less variation in supply response

across countries – impact of lack of confidence, Euro recession and unemployment as well as credit crunch

• Some countries still suffering constraints on availability of funds – for developers as well as purchasers

• Initial stimulus packages mainly replaced by public expenditure cutbacks

• Impact of shifting tenure structures

Change in residential building permits 2007-2011

Countries Percentage (%)

EU27 -44

Spain -89

Ireland -86

Greece -75

Portugal -71

Hungary -68

Cyprus -60

Denmark -43

United Kingdom -42

Netherlands -35

Norway -33

Poland -28

Sweden -18

France -13

Germany -7

Switzerland 36

Source: RICS Research – European Housing Review 2012

Outlook: prices and activity

• Have prices bottomed out? – some signs of stabilisation except in worst affected countries

• Equally there are concerns in countries where price increases are occurring notably Norway, Sweden and against past trends, Germany and Switzerland.

• Some countries with strong austerity packages beginning to use housing as a means of expansion – but as yet no significant impact – exception France?

• But low levels of activity in mortgage markets expected to be maintained as much because of lack of demand than funding constraints

Outlook: Mortgage Regulation

• Numbers of mortgage products have declined and generally become more traditional to the country

• Greater access constraints for first time buyers – but also lack of demand

• Changes in regulatory processes and potential impact of Basle III

• So far, long term regulatory change more rhetoric than reality in part because of low levels of activity – some evidence of reversal of strong constraints

• Macro-stability issues seen as increasingly important – both with respect to mortgage markets and funding for developers

Outlook: housing market adjustment

• Levels of development activity remains low in most countries

• Owner-occupation declining in some countries • Capacities to transfer stock to private renting

varies between countries• Concern that real economic growth potential

limited at least for some years

Conclusions• Trajectories with respect to house prices have

varied greatly since the financial crisis • More commonality in mortgage market

behaviour with lower levels of activity and some constraints on mortgage products-. Those that were more flexible have tightened controls – so now more in line with traditionally more regulated countries

• But little agreement with respect to mortgage products on what is risky

• Currently the real economy constraining activity as much as regulators – but if and when there is significant improvement what then?

Sources and ContactsThis presentation is based on research by KJ Scanlon, J

Lunde and CME Whitehead and the ENHR Housing Finance Working Group.

It is a draft and not for quotation.

Earlier papers are published in the International Journal of Housing Finance:

Scanlon, K, Lunde, J and Whitehead, C (2008) ‘Mortgage product innovation in advanced economies: more choice, more risk’ International Journal of Housing Policy 8:2, 109-131

Scanlon, K, Lunde, J and Whitehead, C (2011) ‘Responding to the housing and financial crises:

mortgage lending, mortgage products and government policies’ International Journal of Housing Policy 11:1, 23-49

Contact: [email protected]