1

Financing Opportunities and challenges

in the Renewable Energy Sector

Alok Dayal

Senior Director Credit & Environment Risk

IDFC Limited

22nd

November, 2014

2

Power scenario in India

Installed capacity

Capacity addition

Thermal Capacity utilization

Renewable Energy

Renewable snapshot

Edge over thermal projects

Challenges in financing

Opportunities and way forward

2

3

Power Scenario in India

3

4

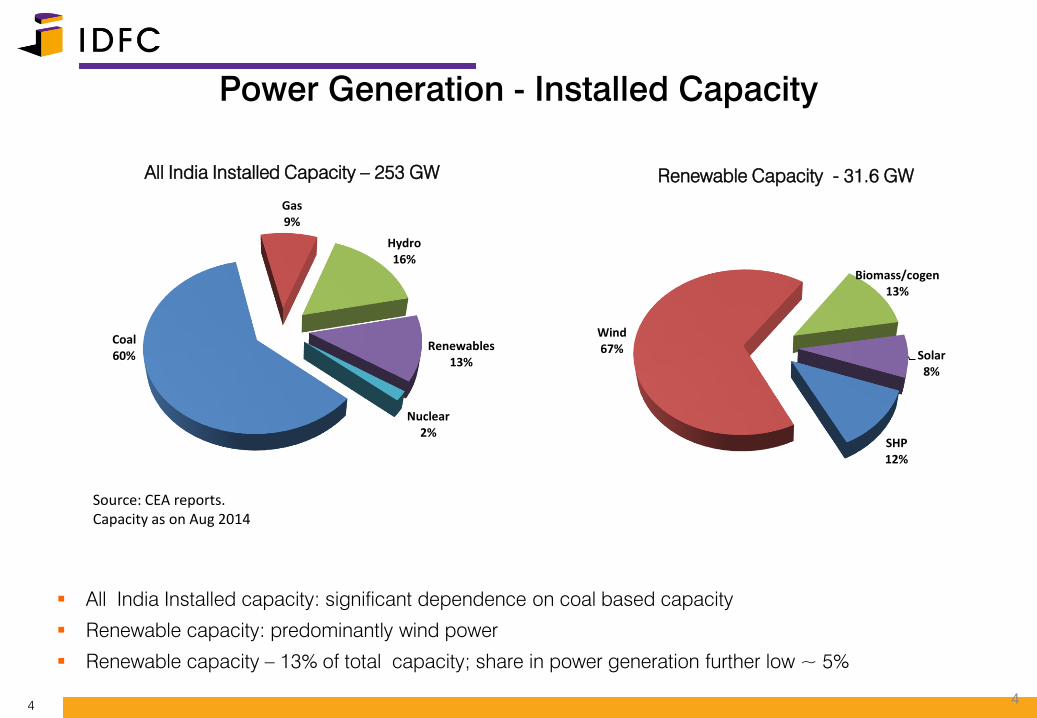

Power Generation - Installed Capacity

4

All India Installed capacity: significant dependence on coal based capacity

Renewable capacity: predominantly wind power

Renewable capacity – 13% of total capacity; share in power generation further low ~ 5%

All India Installed Capacity – 253 GW Renewable Capacity - 31.6 GW

Coal60%

Gas9%

Hydro16%

Renewables13%

Nuclear2%

SHP12%

Wind67%

Biomass/cogen13%

Solar8%

Source: CEA reports. Capacity as on Aug 2014

5

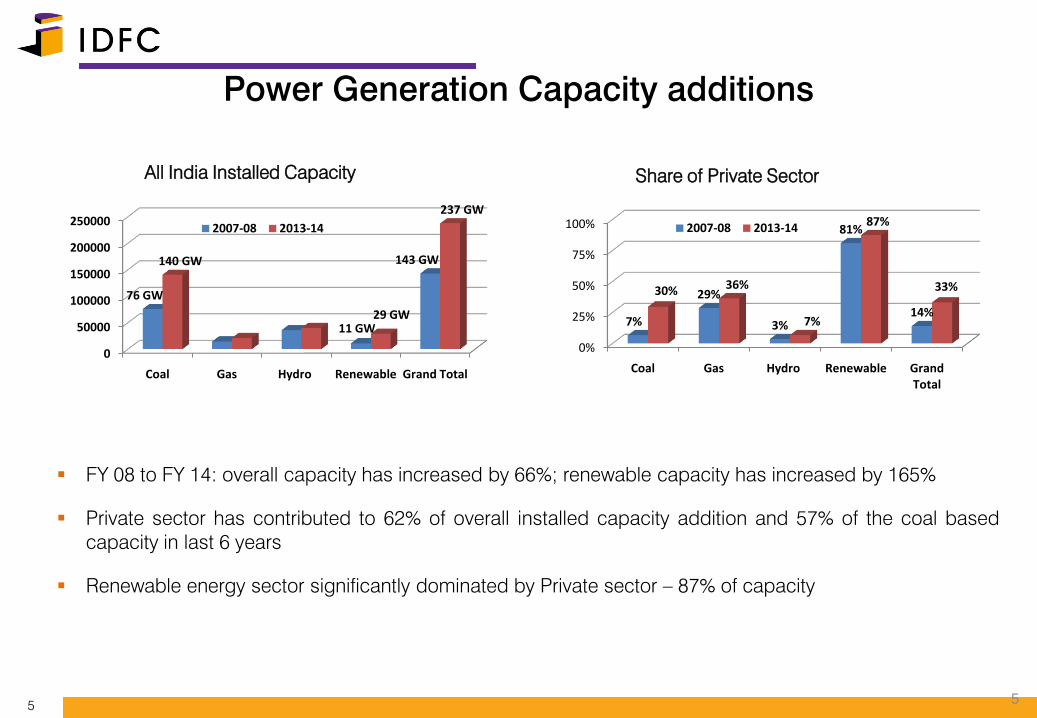

Power Generation Capacity additions

5

FY 08 to FY 14: overall capacity has increased by 66%; renewable capacity has increased by 165%

Private sector has contributed to 62% of overall installed capacity addition and 57% of the coal based

capacity in last 6 years

Renewable energy sector significantly dominated by Private sector – 87% of capacity

0

50000

100000

150000

200000

250000

Coal Gas Hydro Renewable Grand Total

76 GW

11 GW

143 GW140 GW

29 GW

237 GW

2007-08 2013-14

0%

25%

50%

75%

100%

Coal Gas Hydro Renewable Grand Total

7%

29%

3%

81%

14%

30% 36%

7%

87%

33%

2007-08 2013-14

All India Installed Capacity Share of Private Sector

6

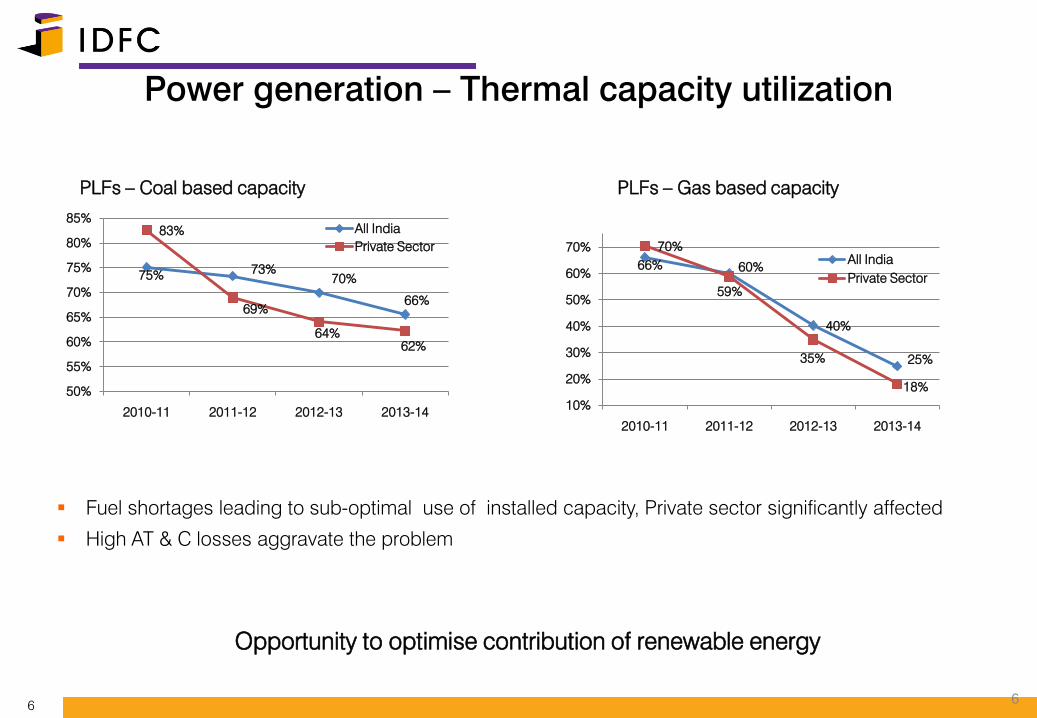

Power generation – Thermal capacity utilization

6

Fuel shortages leading to sub-optimal use of installed capacity, Private sector significantly affected

High AT & C losses aggravate the problem

Opportunity to optimise contribution of renewable energy

PLFs – Coal based capacity

75%73%

70%

66%

83%

69%

64%

62%

50%

55%

60%

65%

70%

75%

80%

85%

2010-11 2011-12 2012-13 2013-14

All India

Private Sector

66% 60%

40%

25%

70%

59%

35%

18%

10%

20%

30%

40%

50%

60%

70%

2010-11 2011-12 2012-13 2013-14

All India

Private Sector

PLFs – Gas based capacity

7

Renewable Energy

7

8

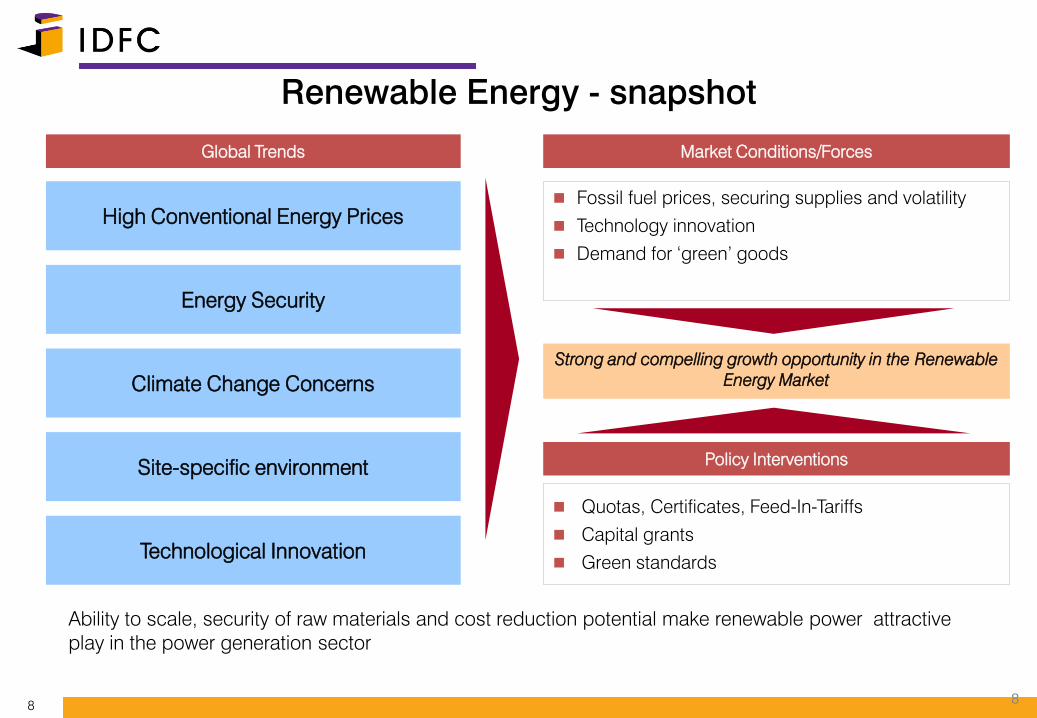

Renewable Energy - snapshot

8

Ability to scale, security of raw materials and cost reduction potential make renewable power attractive

play in the power generation sector

Global Trends Market Conditions/Forces

High Conventional Energy Prices

Energy Security

Climate Change Concerns

Site-specific environment

Technological Innovation

Fossil fuel prices, securing supplies and volatility

Technology innovation

Demand for ‘green’ goods

Strong and compelling growth opportunity in the Renewable

Energy Market

Policy Interventions

Quotas, Certificates, Feed-In-Tariffs

Capital grants

Green standards

9

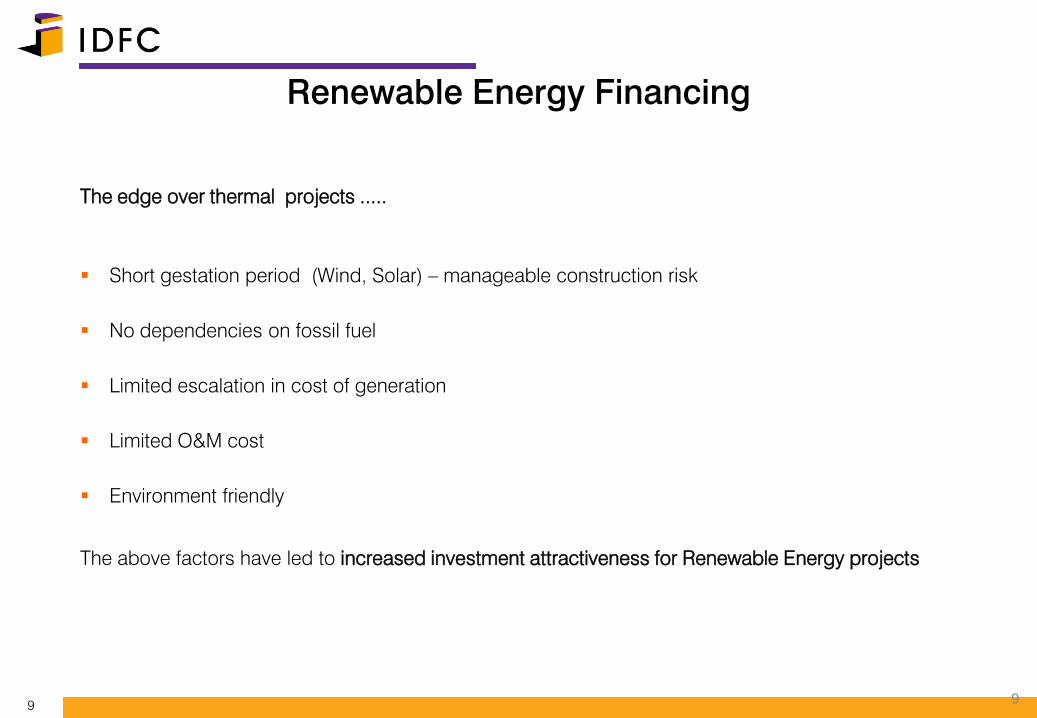

Renewable Energy Financing

9

The edge over thermal projects .....

Short gestation period (Wind, Solar) – manageable construction risk

No dependencies on fossil fuel

Limited escalation in cost of generation

Limited O&M cost

Environment friendly

The above factors have led to increased investment attractiveness for Renewable Energy projects

10

1

0

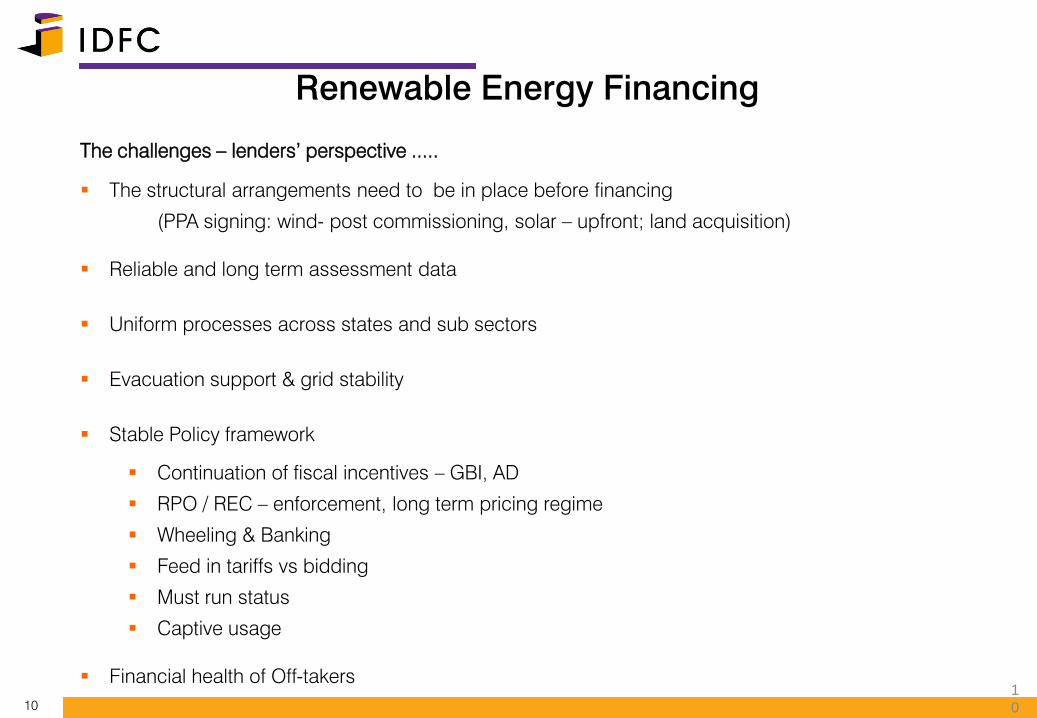

The challenges – lenders’ perspective .....

The structural arrangements need to be in place before financing

(PPA signing: wind- post commissioning, solar – upfront; land acquisition)

Reliable and long term assessment data

Uniform processes across states and sub sectors

Evacuation support & grid stability

Stable Policy framework

Continuation of fiscal incentives – GBI, AD

RPO / REC – enforcement, long term pricing regime

Wheeling & Banking

Feed in tariffs vs bidding

Must run status

Captive usage

Financial health of Off-takers

Renewable Energy Financing

11

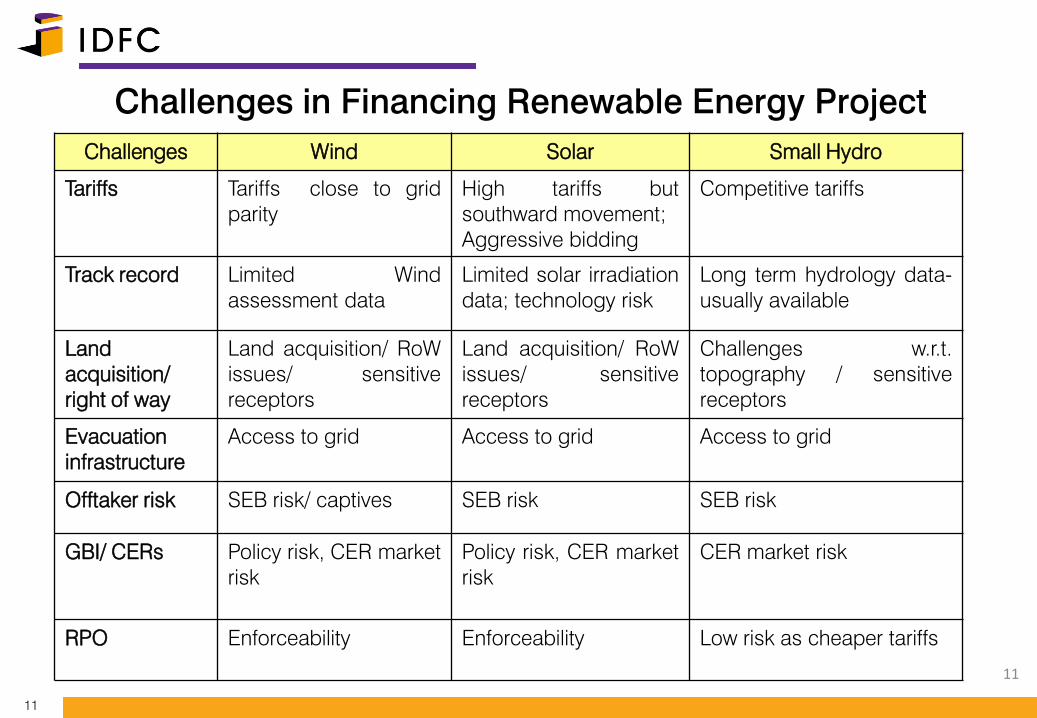

Challenges in Financing Renewable Energy Project

11

Challenges Wind Solar Small Hydro

Tariffs Tariffs close to grid

parity

High tariffs but

southward movement;

Aggressive bidding

Competitive tariffs

Track record Limited Wind

assessment data

Limited solar irradiation

data; technology risk

Long term hydrology data-

usually available

Land

acquisition/

right of way

Land acquisition/ RoW

issues/ sensitive

receptors

Land acquisition/ RoW

issues/ sensitive

receptors

Challenges w.r.t.

topography / sensitive

receptors

Evacuation

infrastructure

Access to grid Access to grid Access to grid

Offtaker risk SEB risk/ captives SEB risk SEB risk

GBI/ CERs Policy risk, CER market

risk

Policy risk, CER market

risk

CER market risk

RPO Enforceability Enforceability Low risk as cheaper tariffs

12

1

2

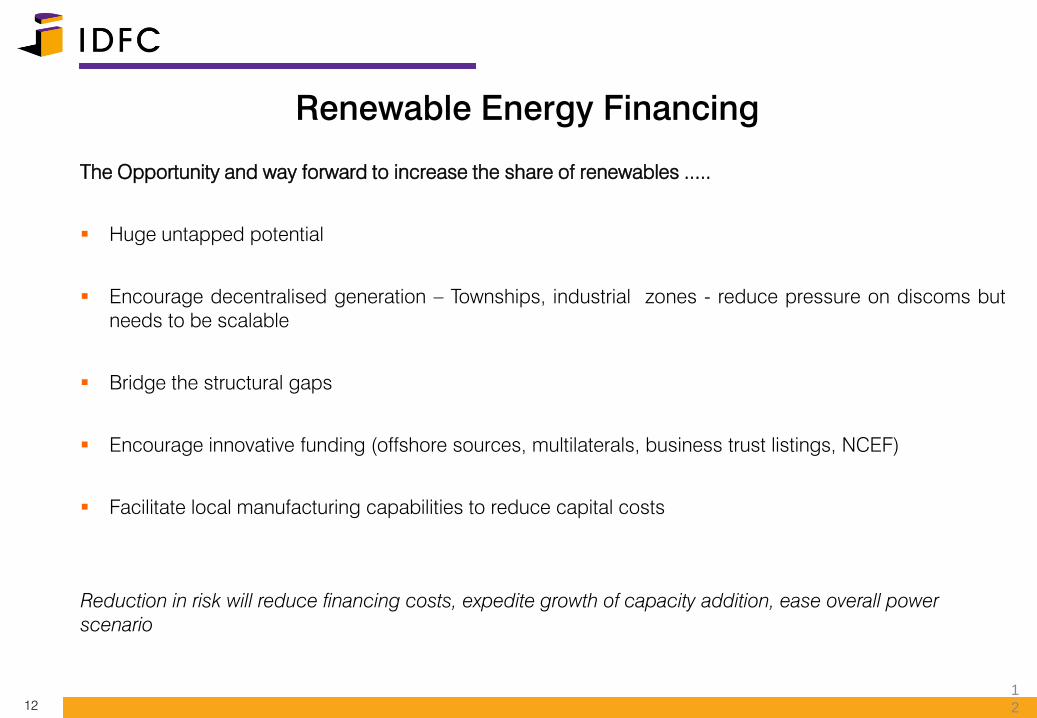

The Opportunity and way forward to increase the share of renewables .....

Huge untapped potential

Encourage decentralised generation – Townships, industrial zones - reduce pressure on discoms but

needs to be scalable

Bridge the structural gaps

Encourage innovative funding (offshore sources, multilaterals, business trust listings, NCEF)

Facilitate local manufacturing capabilities to reduce capital costs

Reduction in risk will reduce financing costs, expedite growth of capacity addition, ease overall power

scenario

Renewable Energy Financing

13

1

3

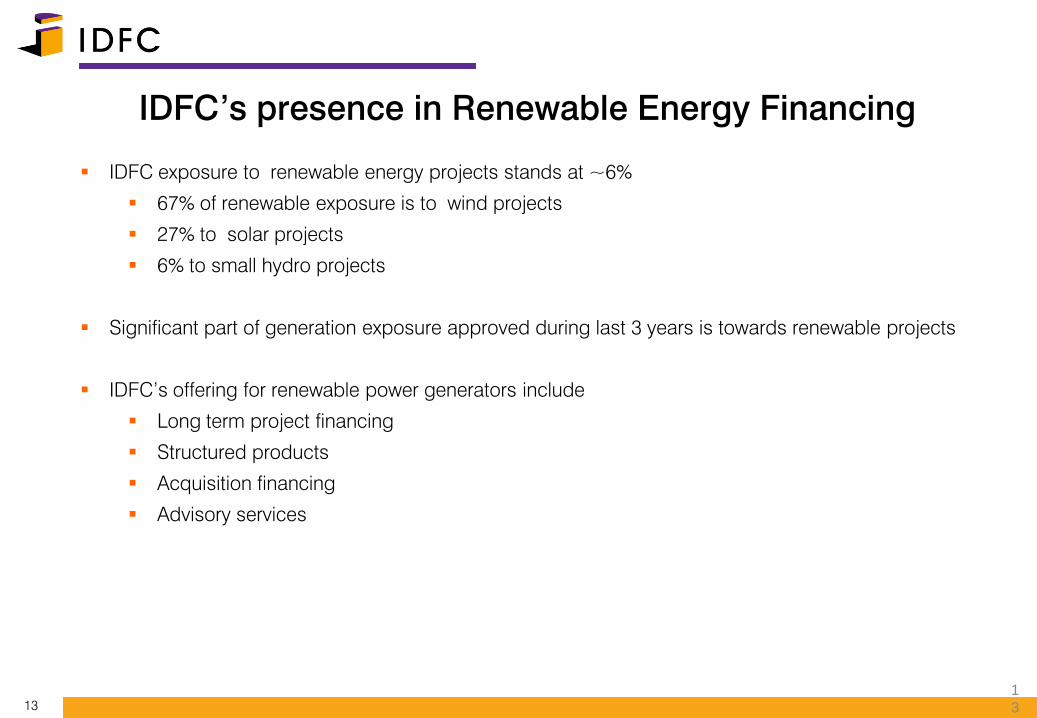

IDFC exposure to renewable energy projects stands at ~6%

67% of renewable exposure is to wind projects

27% to solar projects

6% to small hydro projects

Significant part of generation exposure approved during last 3 years is towards renewable projects

IDFC’s offering for renewable power generators include

Long term project financing

Structured products

Acquisition financing

Advisory services

IDFC’s presence in Renewable Energy Financing

14

Thank You

1

4