4

CMP 822.00

Target Price 920.00

ISIN: INE528G01019

JUNE 18th

, 2015

YES BANK LTD. Result Update (PARENT BASIS): Q4 FY15

BUYBUYBUYBUY

Stock Data

Sector Banking

BSE Code 532648

Face Value 10.00

52wk. High / Low (Rs.) 910.00/502.20

Volume (2wk. Avg ) 346000

Market Cap ( Rs in mn ) 343382.28

Annual Estimated Results (A*: Actual / E*: Estimated)

Years FY15A FY16E FY17E

Interest Earned 115720.00 129027.80 141930.58

Total Income 136184.60 152562.09 168288.98

Net Profit 20053.60 21376.16 25247.69

EPS 48.00 54.11 60.44

P/E 17.12 15.19 13.60

Shareholding Pattern (%)

1 Year Comparative Graph

YES BANK LTD. BSE SENSEX

Highlights

YES BANK reported strong 4th quarter results with

Net Interest Income and Net Profit rising by 35.78% and 28.07% respectively.

Net interest Income, core income of the bank rose from Rs. 7195.90 mn to Rs. 9770.70 mn in Q4

FY15.

Net Profit in Q4 FY15 Jumps to Rs. 5509.90 mn

from Rs. 4302.10 mn in corresponding quarter of

previous year.

Total Advances grew by 35.8% to Rs. 755498.00

mn as at March 31, 2015.

Non Interest Income increased by 32.5% y-o-y to

Rs. 5904.00 mn for Q4 FY15.

The Bank has recommended a final dividend @

90% i.e. Rs. 9.00/- per share on face value of Rs. 10.00/- each for the financial year 2015.

Yes Bank Ltd has approved the proposal to seek final approval of Shareholders for increase in the

limit for the FII / FPI of upto 74% of the paid up

share capital of the Bank.

Current and Savings Account (CASA) deposits

grew by 29.0% y-o-y to Rs.210790.00 mn taking the CASA ratio to 23.1% as at March 31, 2015.

Gross NPA as a proportion of Gross Advances was at 0.41%, while Net NPA as a proportion of Net

advances was at 0.12% as at Mar 31, 2015.

Total Deposits grew by 22.9% to Rs.911758.00 mn

as at March 31, 2015.

The Bank’s Balance Sheet grew by 24.9% to Rs.

1361710.00 mn as at March 31, 2015.

YES BANK’s total branch and ATM network stands at 630 branches and 1,190 ATMs as on March 31,

2015.

PEER GROUPS CMP MARKET CAP. EPS P/E (X) P/BV(X) DIVIDEND

Company Name (Rs.) Rs. in mn. (Rs.) Ratio Ratio (%)

YES Bank Ltd. 822.00 343382.28 48.00 17.12 2.94 90.00

ICICI Bank Ltd. 303.05 1760471.20 19.25 15.75 2.40 300.00

Axis Bank Ltd. 549.65 1305373.40 30.98 17.74 3.41 230.00

IndusInd Bank Ltd 823.15 437568.40 33.74 24.40 4.84 40.00

Analysis & Recommendation - BUY

YES BANK reported strong 4th quarter results with Net Interest Income and Net Profit rising by 35.78% and

28.07% respectively. Net interest Income, core income of the bank rose from Rs. 7195.90 mn to Rs. 9770.70 mn

in Q4 FY15. Net Profit Jumps to Rs. 5509.90 mn in Q4 FY15 from Rs. 4302.10 mn in corresponding quarter of

previous year. Non Interest Income increased by 32.5% y-o-y to Rs. 5904.00 mn for Q4 FY15. Both Treasury

operation segment and retail segment have grown by 43.77% and 72.06% YOY.

Advances and deposits grew by 35.8% and 22.9% at Rs. 755498.00 mn and Rs. 911758.00 mn respectively as

at 31 March, 2015. YES Bank has delivered another steady quarter with healthy growth in Net Profit of 28.07%

driven by sustained increase in NII, expanding NIMs and stable asset quality. Further, the Bank continued its

focus on building granularity in deposits demonstrated by Retail deposit contribution of 72.06% as on March

31, 2015. YES BANK has signs up MoU with OPIC, Us Governments Development finance Institution, and Wells

Fargo for financing Small Businesses for up to US$ 220.00 mn. The bank has approved a capital raising fund of

upto US$ 1 billion by way of QIP or any other international offering such as ADR/GDR. Yes bank has approved

setting up an IBU in the GIFT City, as per regulatory approvals, which will allow the bank to establish

operations to cater to global requirements of Indian companies and also allow the bank to access international

funding competitive rates. The bank has satisfied with the trust and faith shown by the institutional and retail

shareholders on the Board of Directors, Bank’s performance, growth plans and decisions to maintain the

highest professional standards of the Bank’s management team. Further, with the enabling approvals in place,

YES BANK is fully geared up to capitalize on the renewed economic momentum and achieve its Vision of

emerging the finest large bank in India by 2020. Thus we recommend ‘BUY’ for the scrip with the target

price of Rs. 920.00 for medium and long term.

Company Profile

YES BANK, India’s fifth largest private sector Bank, is a state-of-the-art high quality, customer-centric, service-

driven Bank catering to the “Future Businesses of India”. The bank provides services in Corporate and

Institutional Banking, Financial Markets, Investment Banking, Corporate Finance, Branch Banking, Business and

Transaction Banking, and Wealth Management business lines across the country, and is well equipped to offer a

range of products and services to corporate and retail customers.

YES BANK has adopted international best practices, the highest standards of service quality and operational

excellence, and offers comprehensive banking and financial solutions to all its valued customers. The Bank has

received numerous recognitions for its world-class IT infrastructure, and payments solutions, as well as

excellence in Human Capital. YES BANK’s total branch’s and ATM network now stands at 630 branches and 1,190

ATMs as on March 31, 2015. BSE has signed a first of its kind Memorandum of Understanding (MoU) with YES

BANK.

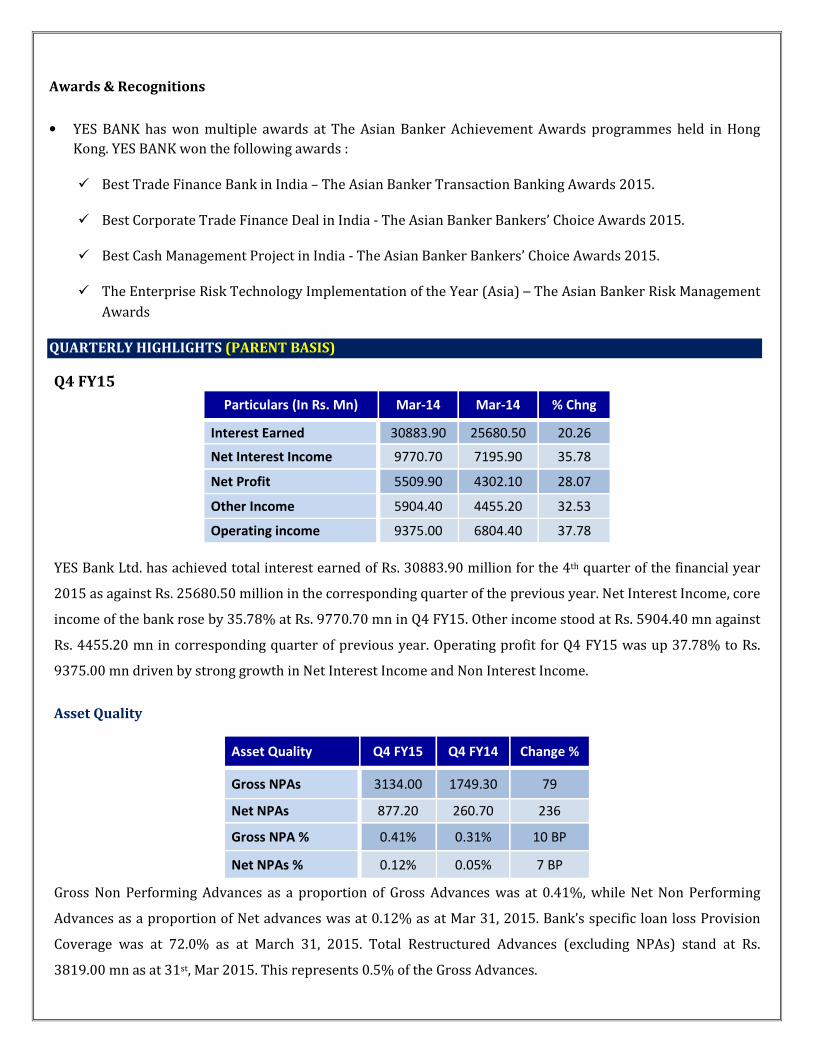

Awards & Recognitions

• YES BANK has won multiple awards at The Asian Banker Achievement Awards programmes held in Hong

Kong. YES BANK won the following awards :

� Best Trade Finance Bank in India – The Asian Banker Transaction Banking Awards 2015.

� Best Corporate Trade Finance Deal in India - The Asian Banker Bankers’ Choice Awards 2015.

� Best Cash Management Project in India - The Asian Banker Bankers’ Choice Awards 2015.

� The Enterprise Risk Technology Implementation of the Year (Asia) – The Asian Banker Risk Management

Awards

QUARTERLY HIGHLIGHTS (PARENT BASIS)

Q4 FY15

YES Bank Ltd. has achieved total interest earned of Rs. 30883.90 million for the 4th quarter of the financial year

2015 as against Rs. 25680.50 million in the corresponding quarter of the previous year. Net Interest Income, core

income of the bank rose by 35.78% at Rs. 9770.70 mn in Q4 FY15. Other income stood at Rs. 5904.40 mn against

Rs. 4455.20 mn in corresponding quarter of previous year. Operating profit for Q4 FY15 was up 37.78% to Rs.

9375.00 mn driven by strong growth in Net Interest Income and Non Interest Income.

Asset Quality

Gross Non Performing Advances as a proportion of Gross Advances was at 0.41%, while Net Non Performing

Advances as a proportion of Net advances was at 0.12% as at Mar 31, 2015. Bank’s specific loan loss Provision

Coverage was at 72.0% as at March 31, 2015. Total Restructured Advances (excluding NPAs) stand at Rs.

3819.00 mn as at 31st, Mar 2015. This represents 0.5% of the Gross Advances.

Particulars (In Rs. Mn) Mar-14 Mar-14 % Chng

Interest Earned 30883.90 25680.50 20.26

Net Interest Income 9770.70 7195.90 35.78

Net Profit 5509.90 4302.10 28.07

Other Income 5904.40 4455.20 32.53

Operating income 9375.00 6804.40 37.78

Asset Quality Q4 FY15 Q4 FY14 Change %

Gross NPAs 3134.00 1749.30 79

Net NPAs 877.20 260.70 236

Gross NPA % 0.41% 0.31% 10 BP

Net NPAs % 0.12% 0.05% 7 BP

Capital Funds:

As per Basel III, Tier I Capital stood at 11.5% and total CRAR stood at 15.6% as at March 31, 2015. Total Capital

funds stood at Rs. 161513.00 million as at March 31, 2015.

Segment-wise Revenue

Particulars (Rs.mn.) Q4 FY15 Q4 FY14 Chng %

Corporate 23659.60 19591.70 20.76%

Treasury 9563.50 6652.00 43.77%

Retail 2739.60 1592.20 72.06%

Other Operations 290.10 180.40 60.81%

Latest Updates

• Yes Bank Ltd has approved the proposal to seek final approval of Shareholders for increase in the limit for

the FII / FPI of upto 74% of the paid up share capital of the Bank from the existing limit of 49% of the paid up

share capital.

• YES BANK, has successfully completed ISO 14001 certification for 79 of its locations including all major

branches and 3 corporate offices. In 2014, it became the first bank in India to qualify for ISO 14001:2004

Certification. Bank reported that its international foray by launching its first International representative

office in Abu Dhabi, U.A.E.

• For Q4 FY15, Net Interest Income grew by 35.78% y-o-y to Rs. 9770.70 mn on account of robust growth in

advances.

• Current and Savings Account (CASA) deposits grew by 29.0% y-o-y to Rs.210790.00 mn taking the CASA ratio

to 23.1% as at March 31, 2015 up from 22.0% as at March 31, 2014.

• Total Deposits grew by 22.9% to Rs.911758.00 mn as at March 31, 2015. The Bank’s Balance Sheet grew by

24.9% to Rs. 1361710.00 mn as at March 31, 2015.

• YES BANK’s total branch and ATM network stands at 630 branches and 1,190 ATMs as on March 31, 2015.

• Total Advances grew by 35.8% to Rs. 755498.00 mn as at March 31, 2015.

• The Bank’s RoA expanded to 1.7% for from 1.6% in Bank’s RoE stood at 19.0% for Q4 FY15.

Financial Statements & Estimations (PARENT BASIS) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as on March 31st, 2014 to 2017E

YES BANK LTD FY14A FY15A FY16E FY17E

CAPITAL AND LIABILITIES

Capital 3606.30 4177.40 4177.40 4177.40

Reserves and Surplus 67611.10 112622.50 133998.66 158118.42

Deposits 741920.20 911758.50 1075875.03 1242635.66

Borrowings 213142.90 262204.00 301534.60 337718.75

Other Liabilities and Provisions 63877.40 70941.70 78035.87 84278.74

Total Liabilities 1090157.90 1361704.10 1593621.56 1826928.97

ASSETS

Cash and Balances with Reserve Bank of India 45415.70 52406.50 59219.35 65733.47

Balances with Banks and Money at Call and Short notice 13501.00 23165.00 30577.80 38528.03

Investments 409503.60 466052.40 517318.16 569049.98

Advances 556329.60 755498.20 918845.03 1083146.48

Fixed Assets 2934.70 3189.70 3444.88 3686.02

Other Assets 62473.30 61392.30 64216.35 66785.00

Total Assets 1090157.90 1361704.10 1593621.56 1826928.98

Annual Profit & Loss Statement for the period from 2014 to 2017E

Value(Rs. mn) FY14A FY15A FY16E FY 17E

Description 12m 12m 12m 12m

Interest Earned 99813.50 115720.00 129027.80 141930.58

Other Income 17215.80 20464.60 23534.29 26358.40

Total income 117029.30 136184.60 152562.09 168288.98

Interest Expended -72650.90 -80841.70 -89584.00 -97932.10

Gross Interest Income 44378.40 55342.90 62978.09 70356.88

Operating Expenses -17498.70 -22847.10 -25676.53 -28528.05

Operating Profit 26879.70 32495.80 37301.56 41828.84

Provisions and Contingencies -3616.90 -3394.70 -4252.38 -4852.15

Profit Before Tax 23262.80 29101.10 33049.18 36976.69

Tax -7085.00 -9047.50 -10443.54 -11729.01

Profit After Tax 16177.80 20053.60 22605.64 25247.69

Equity Capital 3606.30 4177.40 4177.40 4177.40

Reserves 67611.10 112622.50 133998.66 158118.42

Face Value (Rs.) 10.00 10.00 10.00 10.00

EPS 44.86 48.00 54.11 60.44

Quarterly Profit & Loss Statement for the period from 30th Sept 2014 to 30th June 2015E

Value(Rs. mn) 30-Sep-14 31-Dec-14 31-Mar-15 30-Jun-15E

Description 3m 3m 3m 3m

Interest Earned 28323.50 29716.60 30883.90 31671.44

Other Income 5056.20 5368.10 5904.40 6057.91

Total income 33379.70 35084.70 36788.30 37729.35

Interest Expended -19759.50 -20626.40 -21113.20 -22138.34

Gross Interest Income 13620.20 14458.30 15675.10 15591.02

Operating Expenses -5448.80 -5831.00 -6300.10 -6429.30

Operating Profit 8171.40 8627.30 9375.00 9161.72

Provisions and Contingencies -1195.10 -698.60 -1263.60 -907.01

Profit Before Tax 6976.30 7928.70 8111.40 8254.71

Tax -2150.90 -2525.80 -2601.50 -2616.74

Profit After Tax 4825.40 5402.90 5509.90 5637.96

Equity Capital 4161.00 4172.60 4177.40 4177.40

Face Value (Rs.) 10.00 10.00 10.00 10.00

EPS 11.60 12.95 13.19 13.50

Ratio Analysis

Particulars FY14A FY15A FY16E FY17E

EPS (Rs.) 44.86 48.00 54.11 60.44

Operating Profit Margin (%) 26.93% 28.08% 28.91% 29.47%

PAT Margin (%) 16.21% 17.33% 16.57% 17.79%

P/E Ratio (x) 18.32 17.12 15.19 13.60

ROE (%) 22.72% 17.17% 15.47% 15.56%

ROCE (%) 2.62% 2.52% 2.46% 2.40%

Debt-Equity Ratio 13.41 10.05 9.97 9.74

Book Value (Rs.) 197.48 279.60 330.77 388.51

P/BV (x) 4.16 2.94 2.49 2.12

Charts

Industry Overview

According to the Reserve Bank of India (RBI), the banking sector in India is sound, adequately capitalised and

well-regulated. Indian financial and economic conditions are much better than in many other countries of the

world. Credit, market and liquidity risk studies show that Indian banks are generally resilient and have

withstood the global downturn well.

With a sense of optimism slowly creeping in, the banking industry expects that 2015 will bring better growth

prospects. This optimism stems from factors such as the Government working hard to revitalise the industrial

growth in the country and the RBI initiating a number of measures that would go a long way in helping the banks

to restructure. The recent announcements of RBI, it is felt, are a clear pointer to the future of the restructured

domestic banking industry.

Market Size

The Indian banking sector is fragmented, with 46 commercial banks jostling for business with dozens of foreign

banks as well as rural and co-operative lenders. State banks control 80 percent of the market, leaving relatively

small shares for private rivals.

At the end of February, 13.7 crore accounts had been opened under Pradhanmantri Jan Dhan Yojna (PMJDY) and

12.2 crore RuPay debit cards were issued. These new accounts have mobilised deposits of Rs 12,694 crore (US$

2.01 billion).

Standard & Poor’s estimates that credit growth in India’s banking sector would improve to 12-13 per cent in

FY16 from less than 10% in the second half of CY14.

Investments/developments

There have been many investments and developments in the Indian banking sector in the past few months.

• The United Economic Forum (UEF), an organisation that works to improve socio-economic status of the

minority community in India has signed a memorandum of understanding (MoU) with Indian Overseas Bank

(IOB) for financing entrepreneurs from backward communities to set up businesses in Tamil Nadu.

• The RBI has allowed third-party white label automated teller machines (ATM) to accept international cards,

including international prepaid cards, and said white label ATMs can now tie up with any commercial bank

for cash supply.

• In a major boost for the infrastructure sector, as well as for banks financing long gestation projects, the RBI

has extended its flexible refinancing and repayment option for long-term infrastructure projects to existing

ones where the total exposure of lenders is more than Rs 5000.00 mn (US$ 78.98 million).

• With the objective of increasing investment opportunities for Indian alternative investment funds (AIFs), the

RBI has allowed these funds to invest overseas.

• Syndicate Bank is planning to open 300-500 branches in the next financial year

• RBI governor and European Central Bank President has signed an MoU on cooperation in central banking.

“The memorandum of understanding provides a framework for regular exchange of information, policy

dialogue and technical cooperation between the two institutions.

• RBL Bank has announced that it would be the anchor investor in Trifecta Capital’s Venture Debt Fund, the

first alternative investment fund (AIF) of its kind in India with a commitment of Rs 500.00 mn (US$ 7.89

million). This move provides RBL Bank the opportunity to support the emerging venture debt market in

India.

• The RBI has allowed banks to become insurance brokers, permitting them to sell policies of different

insurance firms subject to certain conditions.

• Bandhan Financial Services Pvt. Ltd has raised Rs 16000.00 mn (US$ 252.69 million) from two international

institutional investors to help convert its microfinance business into a full service bank. Bandhan was one of

the two entities to get a banking licence in April 2014 along with infrastructure finance company IDFC Ltd.

• Yes Bank Ltd has signed an MoU with the US government’s development finance institution Overseas Private

Investment Corp (OPIC) to explore US$ 220 million of financing to lend to micro, small and medium

enterprises (MSMEs) in India.

• Reliance Industries Limited (RIL) has said that it has applied for a Payments Bank licence, where the

company will be the promoter and State Bank of India will be its joint venture partner with an equity

investment of up to 30 per cent.

• The RBI has allowed bonds issued by multilateral financial institutions like World Bank Group, the Asian

Development Bank and the African Development Bank in India as eligible securities for interbank borrowing.

The move will further develop the corporate bonds market, RBI said in a notification.

• The Competition Commission of India (CCI) has cleared the merger of ING Vysya Bank with Kotak Mahindra

Bank, which would create the country's fourth largest private sector lender. The proposed Rs 150000.00 mn

(US$ 2.36 billion) deal is not likely to have any appreciable adverse effect on competition in India.

• Tata Consultancy Services Ltd (TCS), India’s largest software services exporter, has announced that it has

expanded its presence in Singapore with the opening of a new 1,000-seat TCS Singapore banking and

financial services (BFS) centre. The new centre replaces a 500-seat centre opened in 2011 and will offer a

broader range of services to global banks in the Asia-Pacific region, with a major focus on digital offerings.

Government Initiatives

There have been a lot of developments in the Indian banking sector.

� The Government has announced a capital infusion of Rs 69900.00 mn (US$ 1.1 billion) in nine state run

banks, including State Bank of India (SBI) and Punjab National Bank (PNB), but based on new efficiency

parameters such as return on assets and return on equity. In a statement, the finance ministry said, “This

year, the Government of India has adopted new criteria in which the banks which are more efficient would

only be rewarded with extra capital for their equity so that they can further strengthen their position."

� The Union cabinet has approved the establishment of the US$ 100 billion New Development Bank (NDB)

envisaged by the five-member BRICS group as well as the BRICS “contingent reserve arrangement” (CRA).

� The RBI has decided to allow nominated banks to import gold, including coins, on a consignment basis,

extending its clarification issued in November 2014, which had eased certain categories of gold imports.

� To help Micro Small and Medium Enterprises (MSME), RBI has permitted setting up of an exchange-based

trading platform to facilitate financing of bills raised by such small entities to corporate and other buyers,

including government departments and PSUs.

Road Ahead

The Indian economy is now on the threshold of a major transformation, with expectations of policy initiatives

being implemented. Positive business sentiments, improved consumer confidence and more controlled inflation

should help boost the economic growth. Higher spending on infrastructure, speedy implementation of projects

and continuation of reforms will provide further impetus to growth. All this translates into a strong growth for

the banking sector too, as rapidly growing business turn to banks for their credit needs, thus helping them grow.

Also, with the advancements in technology, mobile and internet banking services have come to the fore. Banks in

India are focusing more and more to provide better services to their clients and have also started upgrading their

technology infrastructure, which can help improve customer experience as well as give banks a competitive edge.

Many banks, including HDFC, ICICI and AXIS are exploring the option to launch contact-less credit and debit

cards in the market soon. The cards, which use near field communication (NFC) mechanism, will allow customers

to transact without having to insert or swipe.

Outlook and Conclusion

� At the current market price of Rs. 822.00 the stock P/E ratio is at 15.19 x FY16E and 13.60 x FY17E

respectively.

� Earning per share (EPS) of the company for the earnings for FY16E and FY17E is seen at Rs. 54.11 and

Rs.60.44 respectively.

� Net Income and PAT of the company is expected to grow at a CAGR of 12% & 16% over 2014 to 2017E

respectively.

� Price to Book Value of the stock is expected to be at 2.49 x and 2.12 x for FY16E and FY17E respectively.

� We recommend ‘BUY’ in this particular scrip with a target price of Rs. 920.00 for Medium to Long term

investment.

Disclaimer:

This document is prepared by our research analysts and it does not constitute an offer or solicitation for the

purchase or sale of any financial instrument or as an official confirmation of any transaction. The information

contained herein is from publicly available data or other sources believed to be reliable but we do not represent that

it is accurate or complete and it should not be relied on as such. Firstcall Research or any of its affiliates shall not be

in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the

information contained in this report. Firstcall Research and/ or its affiliates and/or employees will not be liable for

the recipients’ investment decision based on this document.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma & Diversified

U. Janaki Rao Capital Goods

B. Anil Kumar Auto, IT & FMCG

M. Vinayak Rao Diversified

G. Amarender Diversified

Firstcall Research Provides

Industry Research on all the Sectors and Equity Research on Major Companies

forming part of Listed and Unlisted Segments

For Further Details Contact:

Tel.: 022-2527 2510/2527 6077 / 25276089 Telefax: 022-25276089

040-20000235 /20000233

E-mail: [email protected]

www.firstcallresearch.com