NYSE:EGY

FirstEnergy Global Energy Conference London, UK

September 16, 2014

2

This presentation includes "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended. All statements included in this presentation that address activities, events or developments that VAALCO

expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements include expected capital expenditures, future

drilling plans, objectives and operations, prospect evaluations, negotiations and relations with governments and third parties, reserve growth, estimated

revenues and losses, and projected costs, timing and amount of future production. These statements are based on assumptions made by VAALCO based on its

experience perception of historical trends, current conditions, expected future developments and other factors it believes are appropriate in the circumstances.

Such statements are subject to a number of assumptions, risks and uncertainties, many of which are beyond VAALCO's control. These risks include, but are not

limited to, inflation, general economic conditions, oil and gas price volatility, the VAALCO's success in discovering, developing and producing reserves, lack of

availability drilling equipment and services, availability of and capital, environmental risks, drilling risks, foreign operational risks, regulatory changes, the

uncertainty inherent in estimating reserves and in projecting future rates of production, cash flow and access to capital, the timing of development expenditures,

and other risks. Additional information on risks and uncertainties that could affect our business prospects and performance are provided in the most recent

reports of VAALCO filed with the Securities and Exchange Commission. These forward-looking statements are based on VAALCO’s current expectations and

assumptions about future events and are based on currently available information as to the outcome and timing of future events. VAALCO cautions you that

forward-looking statements are not guarantees of future performance and that actual results or developments may differ materially from those projected in the

forward-looking statements. VAALCO disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new

information, future events, or otherwise.

The SEC requires oil and gas companies, in their filings with the SEC, to disclose proved reserves that a company has demonstrated by actual production or

conclusive formation tests to be economically and legally producible under existing economic and operating conditions. VAALCO uses the terms “estimated

ultimate recovery,” “EUR,” “probable,” “3P,” “possible,” and “non-proven” reserves, reserve “potential” or “upside,” “unrisked potential” or other descriptions of

volumes of reserves potentially recoverable through additional drilling or recovery techniques that are not classified as proved reserves, may not have been

calculated as defined by SEC regulations and that the SEC’s guidelines may prohibit us from including in any future filings with the SEC. These estimates are by

their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of being actually realized by the

company. VAALCO believes these estimates are reasonable, but such estimates have not been reviewed by independent engineers. Estimates may change

significantly as development provides additional data, and actual quantities that are ultimately recovered may differ substantially from prior estimates. Production

forecasts are dependent upon many assumptions, including estimates of production decline rates from existing wells and the outcome of future drilling activity.

Although VAALCO believes the forecasts are reasonable, VAALCO can give no assurance they will prove to have been correct. They can be affected by

inaccurate assumptions and data or by known or unknown risks and uncertainties.

Market and industry data and forecasts used in this presentation have been obtained from independent industry sources as well as from research reports

prepared for other purposes. Although VAALCO believes these third-party sources to be reliable, VAALCO has not independently verified the data obtained from

these sources and VAALCO cannot assure you of the accuracy or completeness of the data. Forecasts and other forward-looking information obtained from

these sources are subject to the same qualifications and uncertainties as the other forward looking statements in this presentation.

Inquiries:

VAALCO Energy, Inc.

Attn: Gregory R. Hullinger

4600 Post Oak Place, Suite 300

Houston, TX 77027

Ph: 713-623-0801

www.vaalco.com

Safe Harbor Statement

Near Term

Developments

Current West Africa

Exploration Program

Discovered

Undeveloped

Resource Acquisition

Strong Cash Flow

3

Poised for Growth

Strong high margin base business Near term low risk growth opportunities Balanced long term growth strategy

West Africa Focus

4

Block 5 Working Interest 40.0%

1,400,000 gross acres 560,000 net acres

Offshore Exploration

Mutamba Iroru Permit Working Interest 41.0%

270,000 gross acres 111,000 net acres

Onshore Exploration & Development

Etame Marin Permit

Working Interest 28.1% 760,000 gross acres 213,000 net acres

Offshore Production and Exploration

Block P Working Interest 31.0%

57,000 gross acres 18,000 net acres

Offshore Exploration & Development

GABON Port Gentil

Libreville

Luanda

ANGOLA

EQUATORIAL GUINEA

Bata

Company Profile

5

Key Metrics

Share Price(1) $8.67

52-Week Range(1) $5.03 - $9.67

Market Capitalization(1) $494 million

Cash Balance(2) $ 119 million

Revolving Debt Facility(1) $ 65 million

Net Production(1) 4,150 BOPD

2013 EBITDAX $ 118 million

Reserves (2P)(3) 11 MMBOE

% Oil (Brent Based Pricing) 98%

% Operated 100%

Employees(1)

Corporate International

106 42 64

(1) As of 9/9/2014 (2) As of 6/30/2014 (3) As of 12/31/2013

Efficient Reserve Development - Etame Marin Permit

6

Cost Metrics (2002-2013)

Development Costs $14 /BBL

Exploration Costs $ 3 /BBL

DD&A $ 9 /BBL

0

5,000

10,000

15,000

20,000

25,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gross Production (BOPD) Etame Original Forecast Etame Base Actual Etame Additional Actual Avouma Ebouri

Exploitation and development

Repeatable performance

New development – Q4 2014

Growth in EUR

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

1P

Re

serv

es

(MM

BO

)

EUR 1P ReservesGross EUR 1P Reserves

$-

$20

$40

$60

$80

$100

$120

$R

ev/B

bl

Realized Oil Price Per BBL Compared to Brent BBL (2013)

Oily and Leveraged to Brent

7

Comparators Anadarko

ENI Harvest

Shell SINOPEC

TOTAL Tullow Oil

0%10%20%30%40%50%60%70%80%90%

100%

Tota

l % o

f P

rod

uct

ion

Oil / Gas Production (2013)

% Gas

% Oil

Development Projects

8

Etame Deck

Etame Jacket Installation

SEENT Deck

SEENT Jacket Installation

Operator with a 28.1% net W.I. Partners: Sinopec (Addax), Sasol, Sojitz , PetroEnergy and Tullow

Oil production averaged - 16,500 gross (4,050 net) BOPD for 1H 2014

Cumulative production through 6/30/2014 – 82.6 million barrels

Installation of two new platforms underway

Proposed the 7th extension to the Etame Marin Exploration Permit

Offshore Gabon – Etame Marin Permit

9

GABON Port Gentil

Libreville

Etame Marin Permit Working Interest 28.1%

Ebouri

SE Etame

Etame

South Tchibala & Avouma

North Tchibala

FPSO “Petroleo Nautipa” Long-term contract with Tinworth through 2020

Capacity: 30,000 bbls of total fluids per day Capacity: 25,000 bbls of oil per day

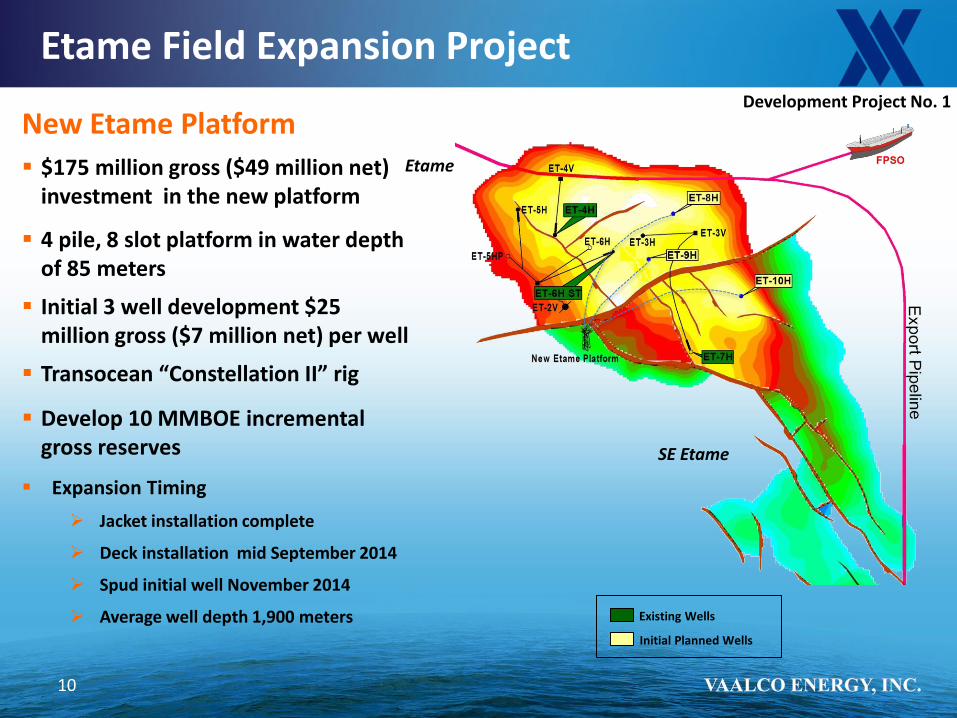

Etame Field Expansion Project

10

New Etame Platform

$175 million gross ($49 million net) investment in the new platform

4 pile, 8 slot platform in water depth of 85 meters

Initial 3 well development $25 million gross ($7 million net) per well

Transocean “Constellation II” rig

Develop 10 MMBOE incremental gross reserves

Expansion Timing

Jacket installation complete

Deck installation mid September 2014

Spud initial well November 2014

Average well depth 1,900 meters Existing Wells

Initial Planned Wells

Etame

SE Etame

Development Project No. 1

SE Etame & North Tchibala Fields Project

11

New SEENT Platform

$150 million gross ($42 million net) investment in the new platform

4 pile, 8 slot platform in water depth of 85 meters

Initial 3 well development $25 million gross ($7 million net) per well

Develop 7 MMBO gross reserves

Gross in place resource potential of over 100 MMBO

Expansion Timing

Jacket installation nearing completion

Deck installation mid September 2014

Spud initial well 2Q 2015

Gamba well depth ~1,900 meters

Dentale well depth ~2,750 meters Initial Planned Wells

SE Etame

North Tchibala

Development Project No. 2

Existing Wells

Initial Planned Wells

Ebouri Redevelopment Project

New Crude Sweetening Platform

$200 - $250 million gross ($56 - $70 million net) investment in the new platform to remove H2S

1 new Ebouri development well at $27 million gross ($7.5 million net)

Reentry of existing Ebouri wells bores at $11 million gross ($3 million net) per well

Develop 9 MMBOE incremental gross reserves at Ebouri

Crude Sweetening Platform

12

Ebouri

Etame

SE Etame

Expansion Timing

Front End Engineering + Design 2H 2014

Final Investment Decision 1H 2015

Installation expected early 2017

Development Project No. 3

13

Onshore Gabon- Mutamba Iroru Permit

VAALCO operated with 41% working interest

N’Gongui discovery well drilled in Q4 2012

Encountered 49 feet of oil pay in the Gamba Formation

Revised production sharing contract term sheet was signed in 3Q 2014

Final PSC negotiations underway

Plan of Development underway for submittal to Gabon Government

Potential first oil production - 2016

Shell Rabi Kounga Field Cum: 840 MMBO EUR 900 MMBO

TOTAL Atora Field

Cum: 38 MMBO

VAALCO N’Gongui Discovery

Shell Bende Field

Shell Gamba-Ivinga Field

Cum: 286 MMBO & 568 BCF EUR 350 MMBO Discoveries

Rabi Kounga Pipeline

VAALCO Permit

Development Project No. 4

14

Offshore Equatorial Guinea - Block P

VAALCO joint operatorship model with 31% working interest

VAALCO has proposed the development of the Venus discovery occurring prior to the drilling of exploration wells

Subsea development

Leased FPSO

2 production wells

1 water injection well

17-21 million BOE gross EUR

Potential first oil production - 2017

Marathon 1,100 mmboe

Exxon 1,300 mmboe

Hess 600 mmboe

VAALCO Block P

PDA

Noble 210 mmboe

Oil Blocks

VAALCO Block

Atlantic

Atlantic Ocean

Block P PDA

A’

A

Venus

Europa

SW Grande

Marte

Development Project No. 5

Tentative Sequence of Milestones

15

Gabon Activity

Set Etame / SEENT Platforms

Central Crude Sweetening Project

FEED

Development

Drill Development Wells at Etame

3 Etame Wells

3 SEENT Wells

Ebouri Wells

Mutamba Development (Onshore Gabon)

EG Activity

Venus Development

Drill Block P Exploration Wells

1st Well

2nd Well

Angola Activity

Process Angola Seismic

Drill Block 5 Exploration Wells

1st Well - Post Salt (Kindele)

2nd Well - Pre Salt

Exploration Projects

16

17

Angola Block 5 - Prospects and Leads

Mubafo Discovery NE

NE SW

SW

Kindele Prospect (Post Salt) WD=101m : 20-49 MMbls*

Ombundi Lead (Pre Salt) WD=500m+ : 100-760 MMbls*

Jack Prospect (Post Salt) WD= 75m : 22-55 MMbls*

VAALCO Loengo Prospect (Post Salt and Pre Salt)

WD= 108m : 70-250 MMbls*

Prospects

Oil Discoveries

Gas Discoveries

A

A’

Maersk AZUL-1

Cobalt Mavinga-1

Cobalt CAMEIA-1 & CAMEIA-2

Cobalt Lontra-1

VAALCO Block 5

Mobil Baleia-1A

Prospects

Oil Discoveries

Cobalt Bicuar-1A

KWANZA BASIN

Gas Discoveries

Cobalt Orca-1

NE SW

NE SW

* Gross Unrisked Recoverable Resources

Angola Block 5 – Kindele Post Salt Prospect

18

Kindele Prospect

$38 million gross ($19 million net ) - DHC

Expected spud 4Q 2014

Mucanzo sand target

Water depth 101 meters

Planned total depth 2,250 meters

Transocean “Celtic Sea” rig

20-49 million gross unrisked recoverable resources

Kindele-1

Mubafo-1 1988 Conoco

Discovery Tested 1100

BOPD

Mubafo Discovery Kindele Prospect Discovery

Prospects

A’

A

A’ A

A

Block 5 Block 20

Possible Oil Zone

Confirmed Oil Zone

Angola Block 5 – Pre Salt Prospects

Confirmed Gas Zone

Large presalt structures in the Kwanza Basin

VAALCO operated with 40% WI (Sonangol P&P 40% WI)

Currently processing 3D seismic in advance of first presalt prospect late 2015/early 2016

Prospects

Oil Discoveries

Gas Discoveries

A

A’

Loengo

A’ Ombundi

VAALCO Prospect

VAALCO Lead

Cobalt Discovery

Orca -1

Mobil Discovery Baleia -1A

Cobalt Discovery

Lontra -1

~15 miles ~65 miles

Cobalt Discovery

Cobalt Discovery

Cobalt Discovery

Mavinga-1 Bicuar -1A Cameia -1

Cameia-2

Maersk AZUL-1

Cobalt Mavinga-1

Cobalt CAMEIA-1 & CAMEIA-2

Cobalt Lontra-1

VAALCO Loengo Prospect

VAALCO Ombundi Lead

Mobil Baleia-1A

VAALCO Block 5

Prospects

Oil Discoveries

Cobalt Bicuar-1A

KWANZA BASIN

Gas Discoveries

Cobalt Orca-1

19

Block 21

SW Grande:Tertiary Channels

Albian/Aptian Structures

Marte:Late Cretacous

Turbidites

Upper Cretaceous Sands

A’A

Venus Field

EuropaDiscovery

20

Block P - Prospects and Leads

20

Atlantic

Atlantic Ocean

VAALCO

PDA

Boundary

57,000 acres

Block P PDA

Discoveries

Prospects

SW Grande 10-180 MMBO*

Europa Discovery

Venus Field 17 - 21 MMBO*

Marte 16-70 MMBO*

A’

A

SW Grande Marte

Exploration Play Types

Proposed exploratory drilling post Venus Development (2017+) Water Depth 250 – 425m Well Depths 1,500 – 2,000m

* Gross Unrisked Recoverable Resources

2014 – Estimated Capital Expenditures

21

Gross $millions

VAALCO

$millions

Development

Etame

Facilities $ 201 $ 57

Drilling 47 13

Exploration

Angola

3-D Seismic 7 3

Kindele 38 19

Gabon

Dimba 30 13

Total $ 323 $ 105

2014 Components (Net) $millions

Construction of platforms $ 57

Development wells 13

Exploration wells 32

Seismic 3

Total $ 105

55%

12%

30%

3%

2014 CAPEX

Construction of platforms

Development wells

Exploration

Seismic

22

Why Invest in VAALCO Now?

Outstanding Near Term Development Projects Etame/SEENT expansion projects Ebouri redevelopment Mutamba Iroru development Venus Field development

Proven International Low Cost Operator 100% operated In 3 out of top 4 West Africa producing countries Projects on time, on budget

Solid Financial Position Growing Cash Flow - increasing production profile in 2015 Unrestricted Cash Position + Borrowing Base Financing development and exploration activities with cash flow

High Impact Exploration Prospects Exposure in excess of 1.9 BBOE net unrisked resources

Identifying Potential Discovered Resource Acquisition Acquisition would balance development / exploration portfolio

23

Questions?

24

APPENDIX

Consolidated Balance Sheets

25

6/30/2014 12/31/2013

Assets Cash & cash equivalents $ 130,529 $

Restricted cash 13,131 13,196

Accounts receivables 28,569 21,714

Other current assets 3,336 2,855

PP&E, net 167,452 138,524

Other non-current assets 3,262 1,349

Total assets 334,317 $ 308,167 $

Liabilities & Owners' Equity

Current liabilities 51,358 $ 45,829 $

Asset Retirement Obligation & Other 11,732 11,464

Shareholders' equity 271,227 250,874

Total liabilities & owners equity (Amounts in thousands)

334,317 $ 308,167 $

118,567

Income Statements

26

6 months

ended

6/30/2014

12 months

ended

12/31/2013

Revenues $ 169,277 $

Operating costs and expenses (46,991) (92,052)

Operating income 33,181 $ 77,225 $

Other expense, net (370) (38)

Income tax expense (15,135) (34,115)

Net income 17,676 $ 43,072 $

(Amounts in thousands)

80,172

EBITDAX Reconciliation

27

6 months

ended

6/30/2014

12 months

ended

12/31/2013

Revenues $ 169,277 $

Operating costs and expenses (46,991) (92,052)

Operating income 33,181 $ 77,225 $

Depreciation, depletion and amortization 11,155 16,929

Exploration expenses 14,616 23,928

Total add backs 25,771 $ 40,857 $

EBITDAX (Amounts in thousands)

58,952 $ 118,082 $

80,172

Reserves - Etame Marin Permit

28

Reserves Summary(1) (As of 12/31/2013)

Proved 7.2 MMBO

Probable 3.4 MMBO

Possible 3.8 MMBO

Total Reserves 14.4 MMBO

(1) Fully Engineered by Netherland Sewell & Associates, Incorporated

50%

24%

26%

3P Reserves

Proved Probable Possible

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$14

$16

$4 $6

$19

$10

$39

Net Cash Flow Summary ($/bbl) 2013

Margin

DD&A

Taxes (Profit Oil)

G&A

Workovers

OPEX

Royalty

13%

15%

4%

6%

17% 9%

36%

Net Cash Flow Summary (%/bbl) 2013

Royalty OPEX Workovers G&A Taxes (Profit Oil) DD&A Margin

Margin per Barrel - Etame Marin Permit

29

$ 108

Attributes of Exploration Opportunities

30

Attributes

Angola Block 5

EG Block P

Etame Marin

Blocks have existing hydrocarbon (oil) discoveries

Prospects are liquids prone

Shallower water (75m – 500m)

Normally pressured regime

Shallower targeted structures

Lower commerciality threshold

State of the art 3D processing and imaging

Development schemes replicates experience

Total unrisked mean net recoverable resource potential ~ 700 MMBOE

31

VAALCO Strong Financial Position for Growth

Asset

Financed by Cash Flow +

Current Cash Position +

IFC Loan

Financed by Capital Markets Transaction

Etame /SEENT Developments

Central Crude Sweetening Project

Mutamba Development

Venus Development

Angola Exploration Wells

EG Exploration Wells

Discovered Undeveloped Resource “Acquisition Costs”

Discovered Undeveloped Resource “Development Costs”

32

Strong Financial Position

($’s in millions)

Financial Position 6/30/2014

Cash Balance (Includes Restricted) $ 132

Working Capital 111

Net PP&E 167

Retained Earnings 271

Financial Performance (1H 2014)

Revenues 80

Operating Income 33

Tax Expense 15

Net Income 18

EBITDAX 59

Funds Available for Growth

Working Capital 111

Revolving Credit Facility (IFC Loan) 65

Total Funds Available for Growth $ 176

Shares Outstanding 6/30/2014 (in millions) 56.9

Earnings Per Share (1H 2014) $ .31