FULL YEAR 2011

RESULTS PRESENTATION

PRESENTERS:

DANNY WALLIS CHIEF EXECUTIVE OFFICER

LACHLAN ARMSTRONG CHIEF FINANCIAL OFFICER

DOUGALL MCBURNIE DIRECTOR – STRATEGIC OPERATIONS

For

per

sona

l use

onl

y

FY11 revenue up 3% to $98.39M

FY11 EBITDA down 8% to $24.81M (in-line with guidance)

FY11 earnings down 6% to $17.39M

Final fully franked dividend of 6.0 cents per share, bringing total payout ratio to 84% (91% incl. special dividends paid)

Balance sheet remains strong with zero debt

Operating cash flow was solid. Q4 cash flow was affected by a slow down in receipts - this has improved in Q1 FY12 with net cash increasing to $15M in July ‘11

Billable consultant numbers up 7% to 540 (FY10: 504) bringing total staff numbers to 594 (FY10: 550)

Financials

Operations during FY11 were affected by Federal and Victorian Elections, natural disasters in QLD and a client close down over the Christmas period

A significant four year strategic transformation program is being delivered - “Improve, Extend, Grow”

Two new specialist business lines added during FY11 (Business Analytics and Information Management, and DWS i-Solutions). Both these practices are contributing to earnings

New regional office opened in Geelong (Victoria) to service growing regional client demand

Added further strategic management and advisory capability to assist in the formulation and execution of the transformation program and various strategic business initiatives

Operations

2

For

per

sona

l use

onl

y

H1 2011 ($’000)

H2 2011 ($’000)

FY11 ($’000)

FY10 ($’000)

Revenue from continuing operations

48,454 49,932 98,386 95,653

EBITDA 12,769 12,041 24,810 26,845

Margin 26% 24% 25% 28%

NPAT 8,969 8,420 17,389 18,516

EPS 6.78 cents 6.36 cents 13 cents 14 cents

Revenue growth driven by a rate increase in the Victorian business & growth in consulting staff numbers

Weighted average revenue per billable consultant in FY11 $196K (FY10: $198K)

Total billable hours in FY11 783,151 (FY10: 800,579)

Average utilisation per billable consultant in FY11 75% (FY10: 78%)

FY11 utilisation was affected by Federal and Vic Government elections, large client Xmas close down and natural disasters in Queensland

Lower utilisation rates dragged on margins, as did initial investment into new business line in H1. Margins have now stabilised and we expect to see the benefit of our new business lines in future periods

Labour market remains competitive and this continues to put pressure on average salary costs

3

For

per

sona

l use

onl

y

JUNE 2011 ($’000)

JUNE 2010 ($’000)

Cash 10,977 13,656

Debtors 23,945 17,742

WIP 1,974 5,156

Total Assets 67,250 66,664

Borrowings NIL NIL

Total Liabilities 9,864 10,453

Net Assets 57,386 56,211

June cash reserves impacted by a slow down in debtor receipts in Q4

Net cash post balance date stronger than PCP at $15M (July ’11)

WIP reduced against PCP with several large projects concluding during Q1 FY11

Continued strengthening of our working capital position

Zero debt position maintained

JUNE 2011 JUNE 2010

Final Dividend 6.0 cents 6.25 cents

Total Dividends 12.0 cents 11.25 cents

Payout Ratio 84% (91% Inc SD) 80%

Franking credits $24.82M $21.54M

Record Date 16 Sept 2011 17 Sept 2010

Dividend payout ratio has been increased due to excess reserves of free cash

Special 1.0 cent fully franked dividend declared during the year to return cash and franking credits

4

For

per

sona

l use

onl

y

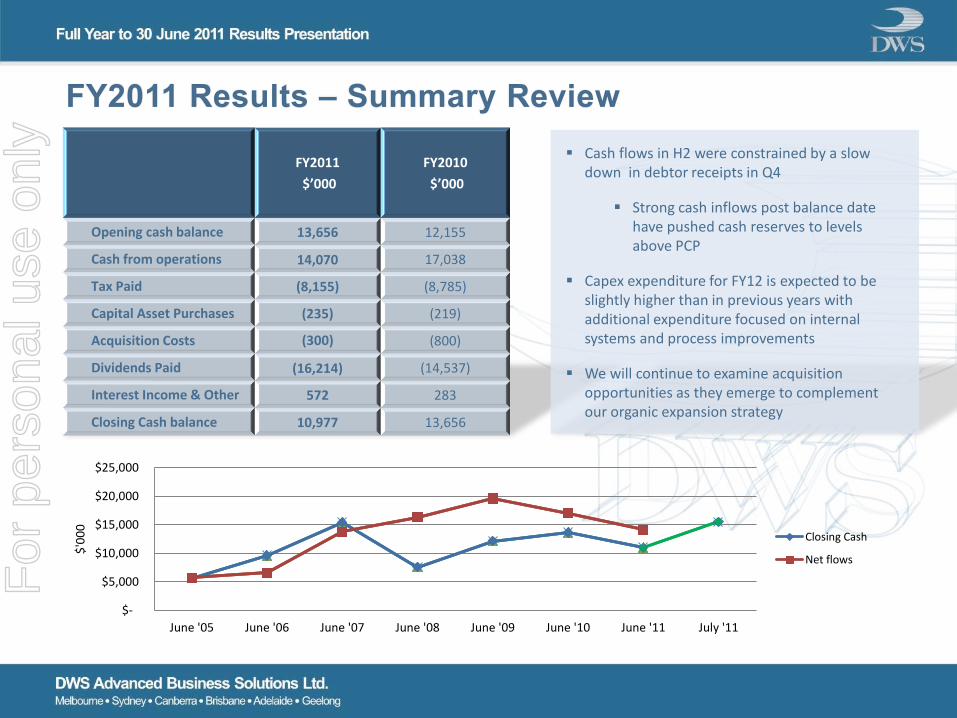

FY2011

$’000

FY2010

$’000

Opening cash balance 13,656 12,155

Cash from operations 14,070 17,038

Tax Paid (8,155) (8,785)

Capital Asset Purchases (235) (219)

Acquisition Costs (300) (800)

Dividends Paid (16,214) (14,537)

Interest Income & Other 572 283

Closing Cash balance 10,977 13,656

Cash flows in H2 were constrained by a slow down in debtor receipts in Q4

Strong cash inflows post balance date have pushed cash reserves to levels above PCP

Capex expenditure for FY12 is expected to be slightly higher than in previous years with additional expenditure focused on internal systems and process improvements

We will continue to examine acquisition opportunities as they emerge to complement our organic expansion strategy

$-

$5,000

$10,000

$15,000

$20,000

$25,000

June '05 June '06 June '07 June '08 June '09 June '10 June '11 July '11

$'0

00

Closing Cash

Net flows

For

per

sona

l use

onl

y

June 2011

Information &

Communications

Technology

24% Utilities

17%

Government

24%

Banking &

Finance

18%

Other

17%

June 2010

Information &

Communications

Technology

33% Utilities

20%

Government

17%

Banking &

Finance

13%

Other

17%

Significant reduction in ICT revenues following the successful delivery of large programs of work in Q1

Although the Federal and Victorian Government elections were disruptive in H1, we have continued to win market share in the Government sector which we view as favourable in the current economic environment

Banking & Finance client portfolio continues to expand and we are confident of further growth in this sector in FY12

We have expanded our national business development capability and we are focussing on winning market share within our existing clients while also increasing our client portfolio

Revenue by Sector Analysis

6

For

per

sona

l use

onl

y

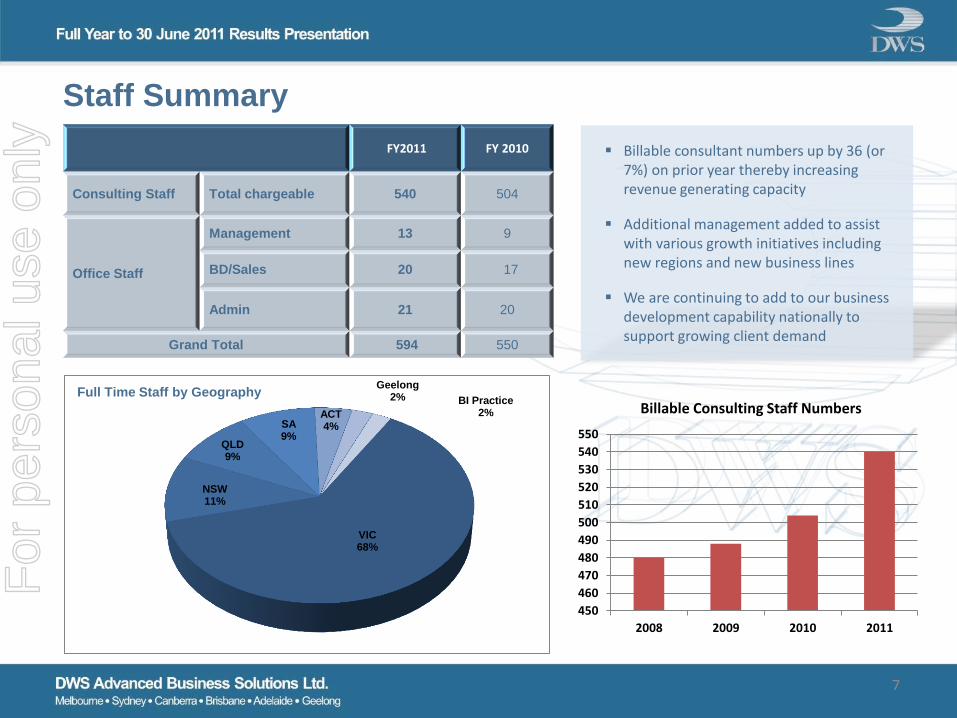

FY2011 FY 2010

Consulting Staff Total chargeable 540 504

Office Staff

Management 13 9

BD/Sales 20 17

Admin 21 20

Grand Total 594 550

VIC 68%

NSW 11%

QLD 9%

SA 9%

ACT 4%

Geelong 2% BI Practice

2%

Full Time Staff by Geography

Billable consultant numbers up by 36 (or 7%) on prior year thereby increasing revenue generating capacity

Additional management added to assist with various growth initiatives including new regions and new business lines

We are continuing to add to our business development capability nationally to support growing client demand

Staff Summary

450

460

470

480

490

500

510

520

530

540

550

2008 2009 2010 2011

Billable Consulting Staff Numbers

7

For

per

sona

l use

onl

y

EVP research undertaken by internationally recognised consultancy

Robust training and development framework implemented for all consulting staff

Leading branding and marketing consultant engaged to assist with the development of the brand strategy

Implementation of new performance management platform

Launch of new and enhanced DWS brand (including logo, website and marketing materials)

Enhance and expand our recruitment strategy (which includes our 457 visa program)

FY12 INITIATIVES

Enhance our overall Employee Value Proposition (EVP)

Brand refresh and launch to raise DWS’ industry awareness

Internal platforms and process improvements

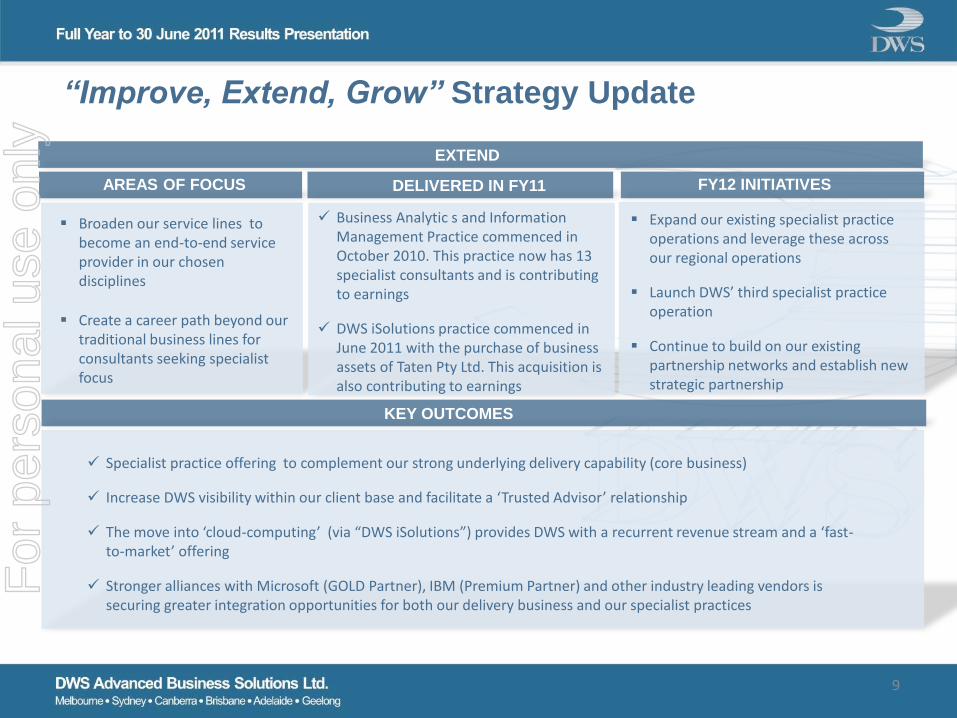

“Improve, Extend, Grow” Strategy Update

AREAS OF FOCUS DELIVERED IN FY11

Lower consultant attrition rates through enhanced consultant career development

Attraction of industry recognised technical and solution specialists to underpin our delivery capability

Improvement to core operations by driving operational efficiency with the use of technology platforms

Raise the profile of DWS at Executive and Board levels of existing and potential clients

IMPROVE

KEY OUTCOMES

8

For

per

sona

l use

onl

y

Business Analytic s and Information Management Practice commenced in October 2010. This practice now has 13 specialist consultants and is contributing to earnings

DWS iSolutions practice commenced in June 2011 with the purchase of business assets of Taten Pty Ltd. This acquisition is also contributing to earnings

Expand our existing specialist practice operations and leverage these across our regional operations

Launch DWS’ third specialist practice operation

Continue to build on our existing partnership networks and establish new strategic partnership

FY12 INITIATIVES

Broaden our service lines to become an end-to-end service provider in our chosen disciplines

Create a career path beyond our traditional business lines for consultants seeking specialist focus

“Improve, Extend, Grow” Strategy Update

AREAS OF FOCUS DELIVERED IN FY11

Specialist practice offering to complement our strong underlying delivery capability (core business)

Increase DWS visibility within our client base and facilitate a ‘Trusted Advisor’ relationship

The move into ‘cloud-computing’ (via “DWS iSolutions”) provides DWS with a recurrent revenue stream and a ‘fast-to-market’ offering

Stronger alliances with Microsoft (GOLD Partner), IBM (Premium Partner) and other industry leading vendors is securing greater integration opportunities for both our delivery business and our specialist practices

EXTEND

KEY OUTCOMES

9

For

per

sona

l use

onl

y

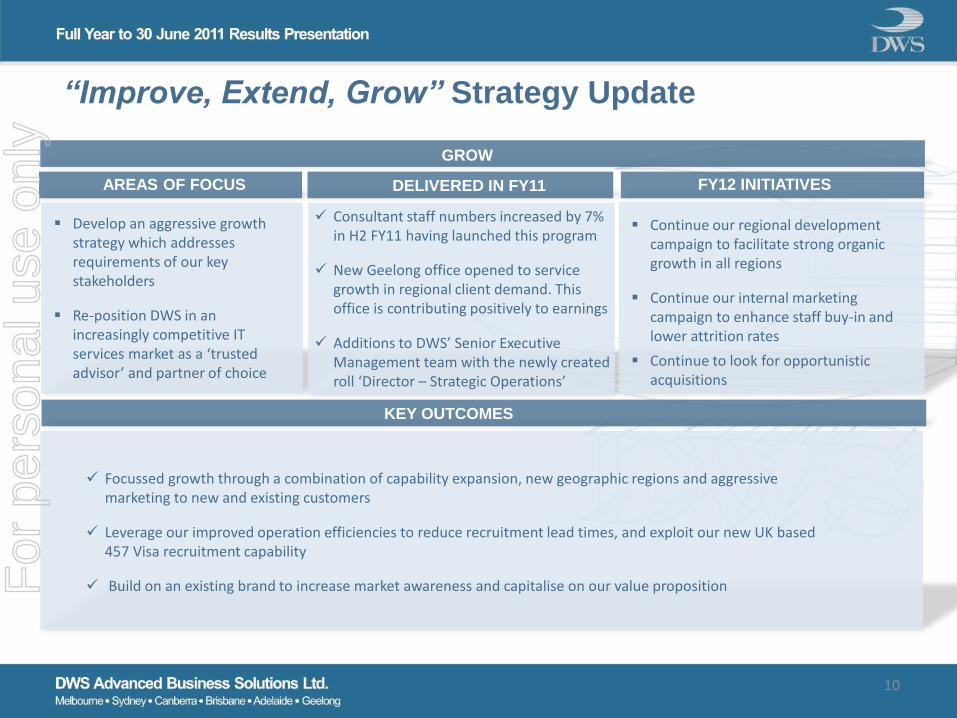

Consultant staff numbers increased by 7% in H2 FY11 having launched this program

New Geelong office opened to service growth in regional client demand. This office is contributing positively to earnings

Additions to DWS’ Senior Executive Management team with the newly created roll ‘Director – Strategic Operations’

Continue our regional development campaign to facilitate strong organic growth in all regions

Continue our internal marketing campaign to enhance staff buy-in and lower attrition rates

Continue to look for opportunistic acquisitions

FY12 INITIATIVES

Develop an aggressive growth strategy which addresses requirements of our key stakeholders

Re-position DWS in an increasingly competitive IT services market as a ‘trusted advisor’ and partner of choice

“Improve, Extend, Grow” Strategy Update

AREAS OF FOCUS DELIVERED IN FY11

Focussed growth through a combination of capability expansion, new geographic regions and aggressive marketing to new and existing customers

Leverage our improved operation efficiencies to reduce recruitment lead times, and exploit our new UK based 457 Visa recruitment capability

Build on an existing brand to increase market awareness and capitalise on our value proposition

GROW

KEY OUTCOMES

10

For

per

sona

l use

onl

y

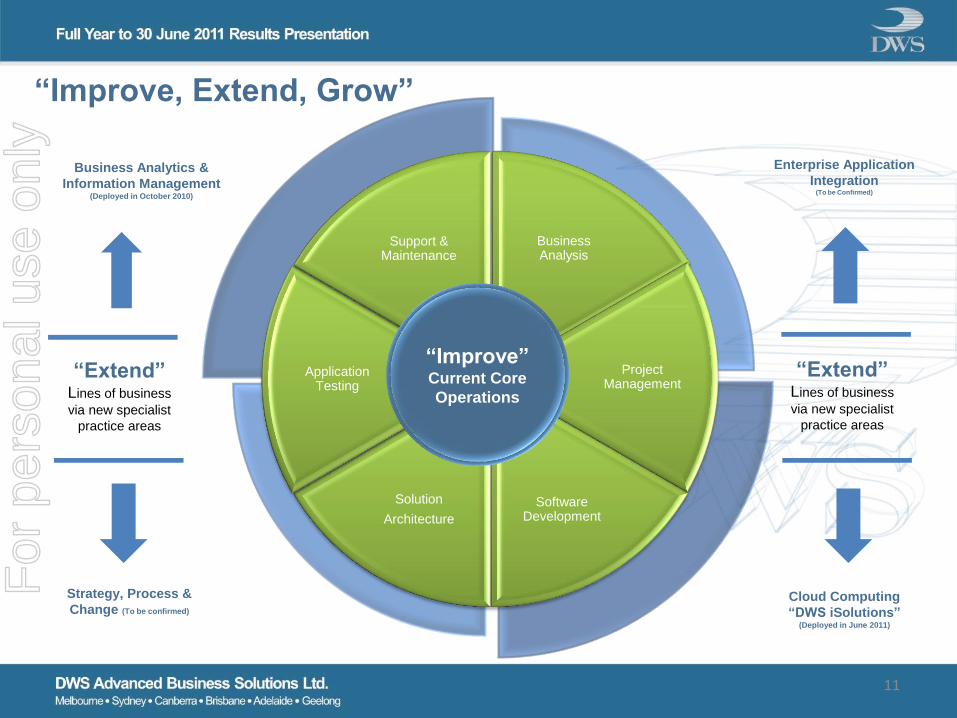

Business Analysis

Project Management

Software Development

Solution

Architecture

Application Testing

Support & Maintenance

Business Analytics &

Information Management (Deployed in October 2010)

Strategy, Process &

Change (To be confirmed)

Cloud Computing

“DWS iSolutions” (Deployed in June 2011)

Enterprise Application

Integration (To be Confirmed)

“Improve, Extend, Grow”

“Improve” Current Core

Operations

“Extend” Lines of business

via new specialist

practice areas

“Extend” Lines of business

via new specialist

practice areas

11

For

per

sona

l use

onl

y

New Practice - “DWS iSolutions”

Established through the acquisition of the Taten business assets

Industry leading Internet technologies delivered through a Cloud Computing model

Revenue based on ‘per click’ basis

Strong existing client base in Financial Services industry

Introduces this client base to DWS

Represents significant opportunity to deploy this technology across existing DWS clients

Gain important exposure to Cloud Computing paradigm

Opportunity to ‘Extend’ DWS iSolutions service offering with additional Cloud Solutions

12

For

per

sona

l use

onl

y

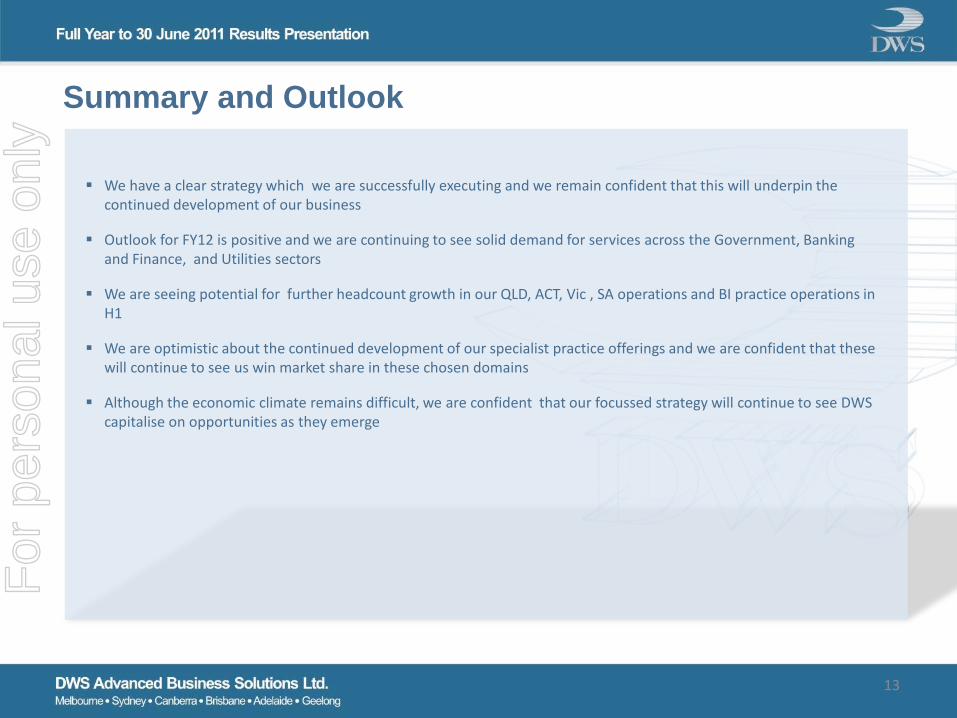

Summary and Outlook

We have a clear strategy which we are successfully executing and we remain confident that this will underpin the continued development of our business

Outlook for FY12 is positive and we are continuing to see solid demand for services across the Government, Banking and Finance, and Utilities sectors

We are seeing potential for further headcount growth in our QLD, ACT, Vic , SA operations and BI practice operations in H1

We are optimistic about the continued development of our specialist practice offerings and we are confident that these will continue to see us win market share in these chosen domains

Although the economic climate remains difficult, we are confident that our focussed strategy will continue to see DWS capitalise on opportunities as they emerge

13

For

per

sona

l use

onl

y