Amateur Hour is Over-- Using GPS and Wireless to Manage Field Service Workers --

Jeanine Sterling, Senior Industry Analyst

Mobile and Wireless

September 17, 2008

2

Focus Points

• Next-Gen MRM: Changing the Business Model

• MRM Evolution: Stage III

• Evolving Trends and Issues

• Market Consolidation Scenarios

• Stakeholder Challenges: Preparing for the Shake-Out

3

Typical Field Scenario: Minimal Visibility

• Management team is working in the dark – no/low visibility into field employee activity

• Worker tethered by periodic cell phone calls or text messaging

• Self-reporting on location, breaks, etc.

4

MRM’s Changing Business Model

TRADITIONAL

• Truck tracking

• In-vehicle, hard-mounted devices

• Satellite tracking

• Dedicated servers

• Per-seat licensing

• High upfront investment

NEXT-GENERATION

• Focus on individual worker and task

• GPS-enabled mobile handhelds

• Web-based tracking systems

• Hosted, per-user per-month pricing

• Lower entry cost

Mobile Resource Management

Business solutions that use wireless and location technologies to maximize the productivity of mobile workforces – by more effectively locating, tracking, and managing mobile workers, mobile tasks, and

mobile assets

5

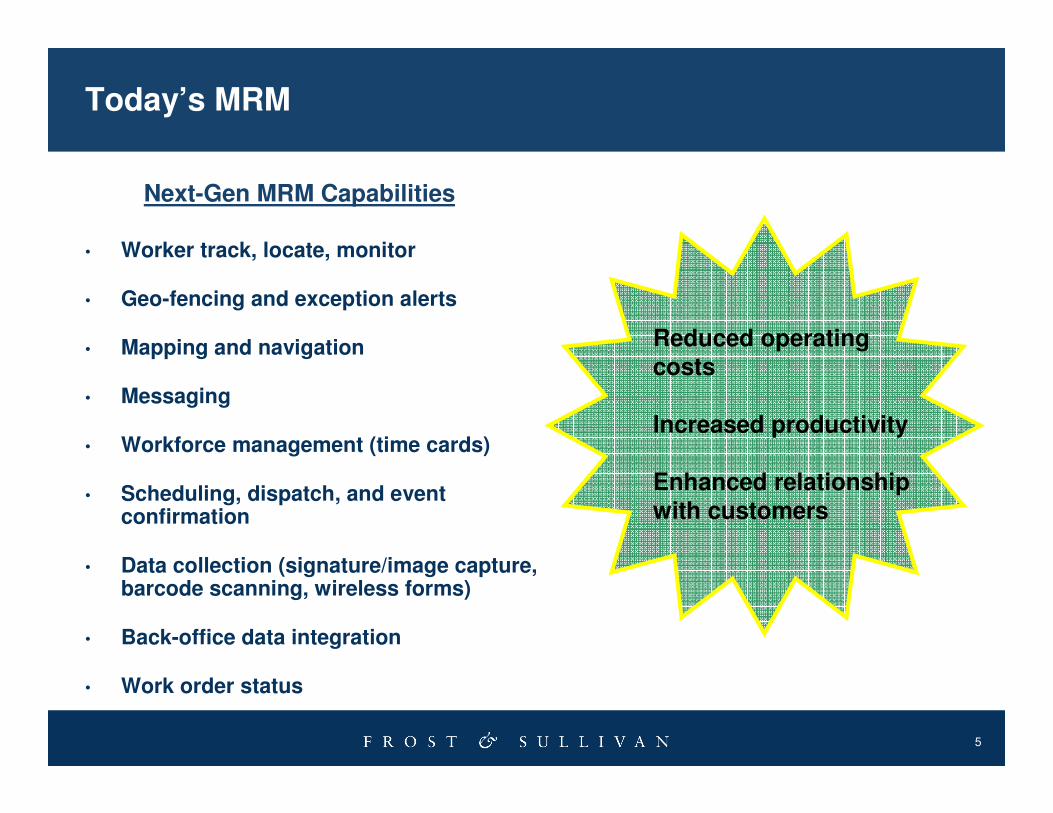

Today’s MRM

• Worker track, locate, monitor

• Geo-fencing and exception alerts

• Mapping and navigation

• Messaging

• Workforce management (time cards)

• Scheduling, dispatch, and event confirmation

• Data collection (signature/image capture, barcode scanning, wireless forms)

• Back-office data integration

• Work order status

Next-Gen MRM Capabilities

Reduced operating costs

Increased productivity

Enhanced relationship with customers

6

Evolution of North American Location-Aware Services (U.S.), 2002-2010+

Stage IPre-2006

E911 Priority

Long Term Technology Planning

Trial of Early Adopters

Entry of Competitors

Few Commercially Deployed Location-

based Services

Enterprise Applications (iDEN)

Stage II2006-08

Leverage E911 Investments

More Aggressive Marketing of

Commercial Services

Handsets Gain Critical Mass with A-GPS

Enterprise and Consumer

Applications (CDMA)

Stage III2008-10

Growing Traction

Increased Location Accuracy

Shakeout of Weakest Competitors

Competitive Advantage Drives

Enterprise Adoption

Enterprise and Consumer

Applications (GSM)

Stage IV2010+

Platforms Replace “Silo” Apps

End-to-End Offerings

Sophisticated, Integrated

Deployments

Mobile Advertising + Location

Location Interoperability

between Networks

LocationLocationLocationLocation----based Customer Adoption Over Timebased Customer Adoption Over Timebased Customer Adoption Over Timebased Customer Adoption Over Time

Source: Frost & Sullivan

MRM Evolution: Growing Traction

7

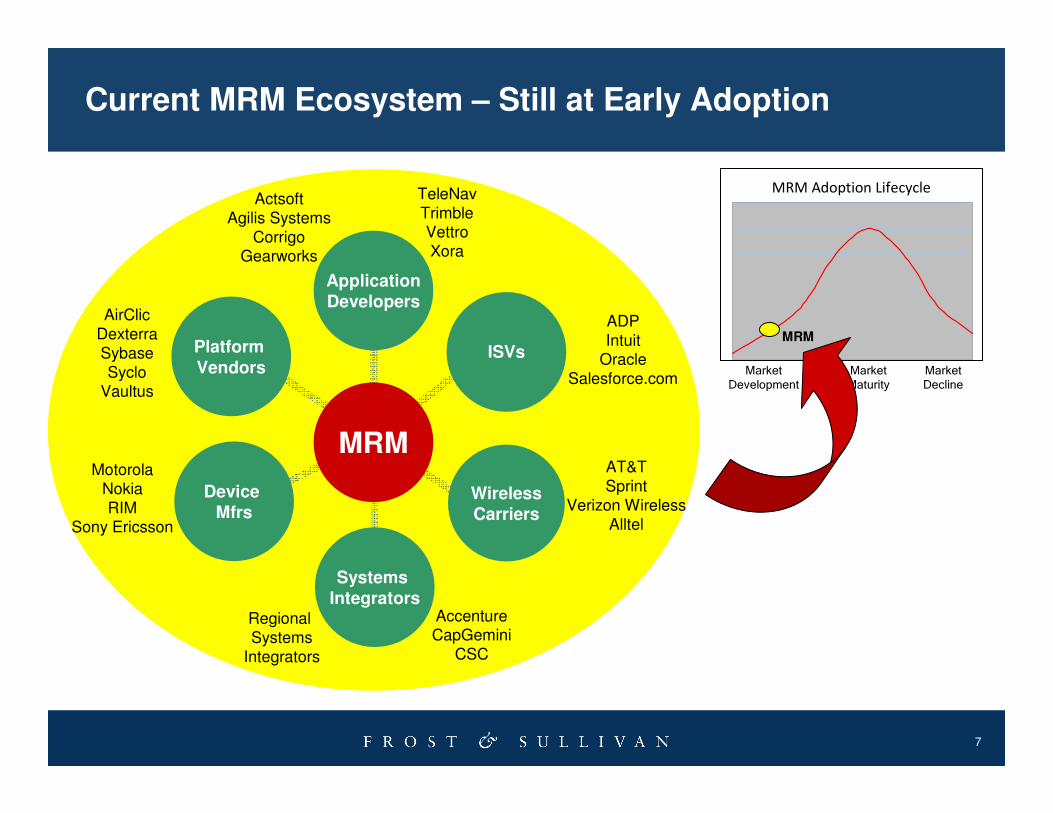

Current MRM Ecosystem – Still at Early Adoption

Device Mfrs

WirelessCarriers

ISVsPlatform Vendors

Systems Integrators

MotorolaNokiaRIM

Sony Ericsson

AirClicDexterraSybaseSyclo

Vaultus

ActsoftAgilis Systems

CorrigoGearworks

ADPIntuit

OracleSalesforce.com

AccentureCapGemini

CSC

AT&TSprint

Verizon WirelessAlltel

Market Development

Market Maturity

Market Decline

MRM Adoption Lifecycle

MRM

MRM

TeleNavTrimbleVettroXora

Regional Systems

Integrators

ApplicationDevelopers

8

Market Drivers (2008 - 2013)

• High, hard-dollar ROI

• More affordable hardware, software, network services

• Supports Wireless Carrier focus on long-term value creation

• Major ISVs see value in mobilizing their traditional business software

• A major avenue for carriers to recoup E911 investment

9

Market Restraints (2008 – 2013)

• Limited customer awareness

• Wireless carriers’ ability to sell MRM is uneven

• Challenges with back-office integration

• Limited GSM device options

• High TCO – Hardware and integration expense can be prohibitive

10

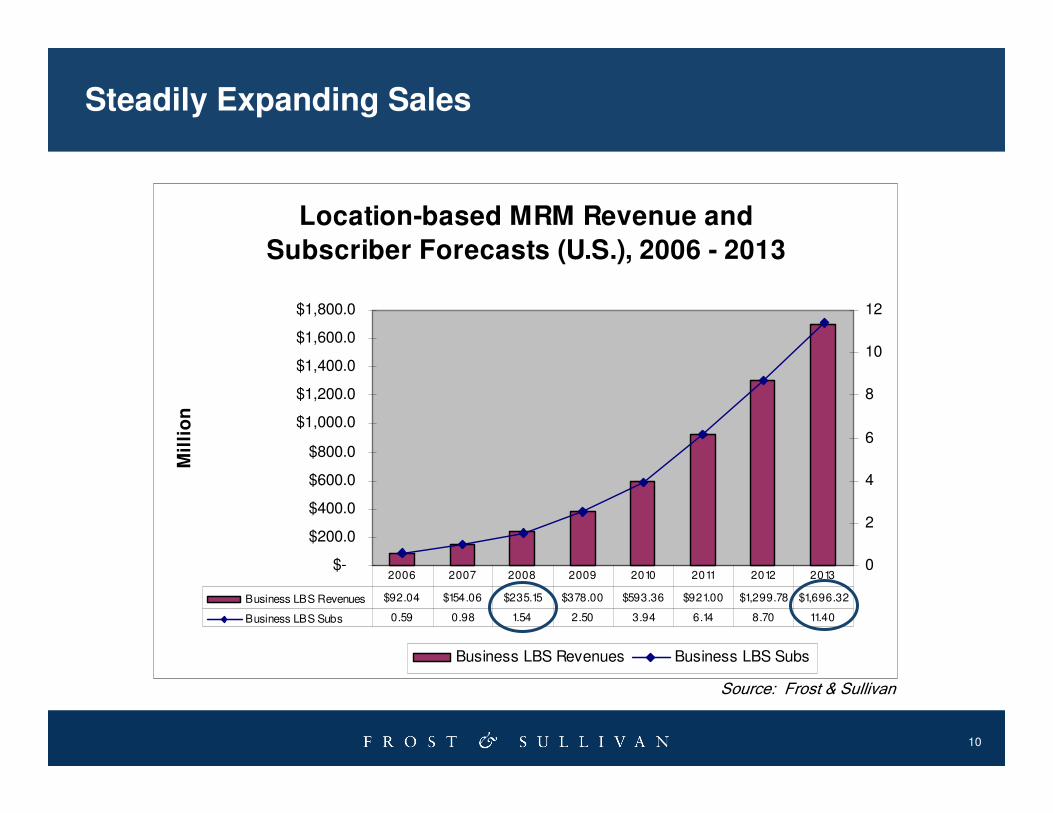

Steadily Expanding Sales

Location-based MRM Revenue and

Subscriber Forecasts (U.S.), 2006 - 2013

$-

$200.0

$400.0

$600.0

$800.0

$1,000.0

$1,200.0

$1,400.0

$1,600.0

$1,800.0

Mil

lio

n

0

2

4

6

8

10

12

Business LBS Revenues Business LBS Subs

Business LBS Revenues $92.04 $154.06 $235.15 $378.00 $593.36 $921.00 $1,299.78 $1,696.32

Business LBS Subs 0.59 0.98 1.54 2.50 3.94 6.14 8.70 11.40

2006 2007 2008 2009 2010 2011 2012 2013

Source: Frost & Sullivan

11

Application Trends

• More robust capabilities, as handsets become more powerful and user-friendly

• SaaS approach vs. per-seat licensing

• Must have: Integration and customization capability

• 24/7 support + SLAs

• Increased assistance with managing “data spigot”

• Intensifying focus on verticals

• Standardization of Packaging/Pricing

12

Increasing Offer Standardization

GPS location trackingMappingGeo-fencingException alertsStandard reports

Timecard reportingText messaging Mileage trackingBasic dispatch/schedulingData captureWork order statusBasic back-office integrationWireless formsText navigationGPS location trackingMappingGeo-fencingException alertsStandard reports

Richer dispatchRicher integration optionsEvent confirmation/notificationAudible navigationTimecard reportingText messaging Mileage trackingBasic dispatch/schedulingData captureWork order statusBasic back-office integrationWireless formsText navigationGPS location trackingMappingGeo-fencingException alertsStandard reports

Entry-Level~$10/user/month

Mid-Tier Package~$15/user/month

Top-Tier Package~$20/user/month

Good-Better-Best Packaging

13

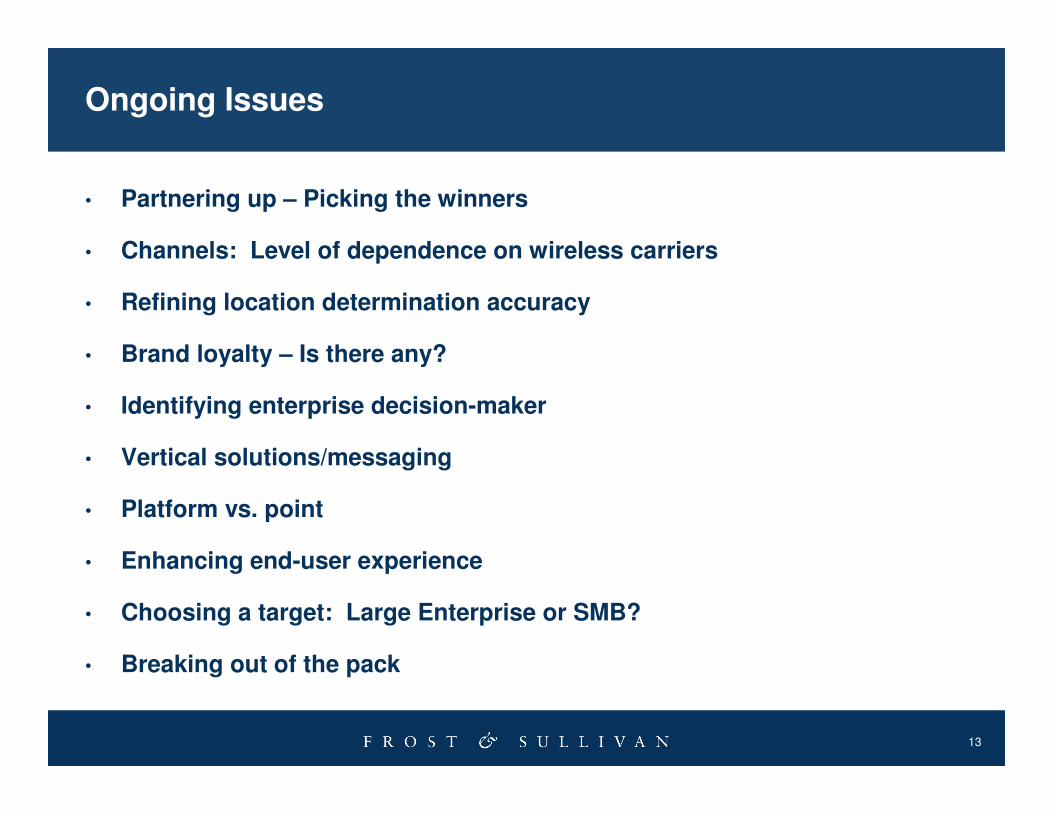

Ongoing Issues

• Partnering up – Picking the winners

• Channels: Level of dependence on wireless carriers

• Refining location determination accuracy

• Brand loyalty – Is there any?

• Identifying enterprise decision-maker

• Vertical solutions/messaging

• Platform vs. point

• Enhancing end-user experience

• Choosing a target: Large Enterprise or SMB?

• Breaking out of the pack

14

Future Industry Consolidation: A Possible Template

Market Leader

IntellisyncIntellisyncIntellisyncIntellisync

NOKIA

Acquired by:

Good TechnologyGood TechnologyGood TechnologyGood Technology Acquired by

Large Enterprise Play Hosted SMB-Carrier Play

Remains

Autonomous

Remains

Autonomous

Large Enterprise = 1,000+ EmployeesSMB = <1,000 Employees

(Medium, Small, SOHO)

Mobile Business Application: Mobile Office Email/PIM

15

Future Industry Consolidation: The Navigation Angle

• The Navigation piece is critical to MRM success.

• A Possible Merger/Acquisition: MRM + Navigation Partner

Navigation

capability is

in-house

+ +

OROROROR

16

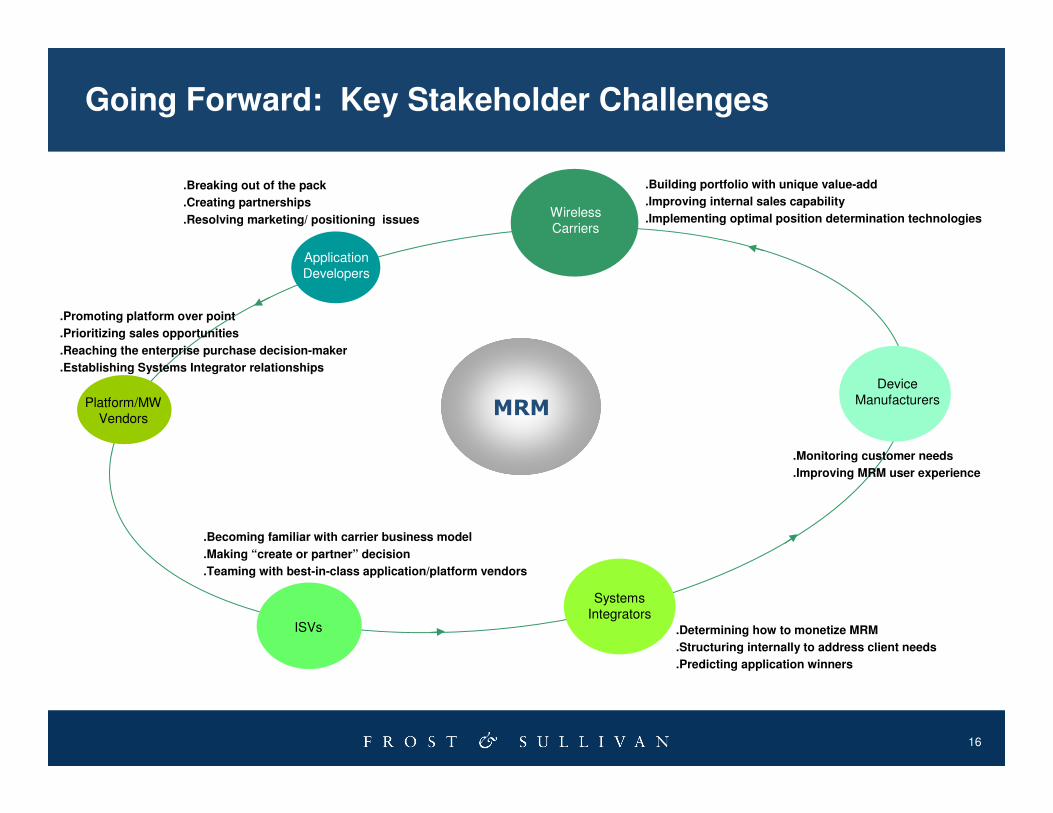

MRM

.Building portfolio with unique value-add

.Improving internal sales capability

.Implementing optimal position determination technologiesWireless Carriers

Application Developers

.Breaking out of the pack

.Creating partnerships

.Resolving marketing/ positioning issues

.Promoting platform over point

.Prioritizing sales opportunities

.Reaching the enterprise purchase decision-maker

.Establishing Systems Integrator relationships

Platform/MW Vendors

ISVs

.Becoming familiar with carrier business model

.Making “create or partner” decision

.Teaming with best-in-class application/platform vendors

Systems Integrators

.Determining how to monetize MRM

.Structuring internally to address client needs

.Predicting application winners

Device Manufacturers

.Monitoring customer needs

.Improving MRM user experience

Going Forward: Key Stakeholder Challenges

17

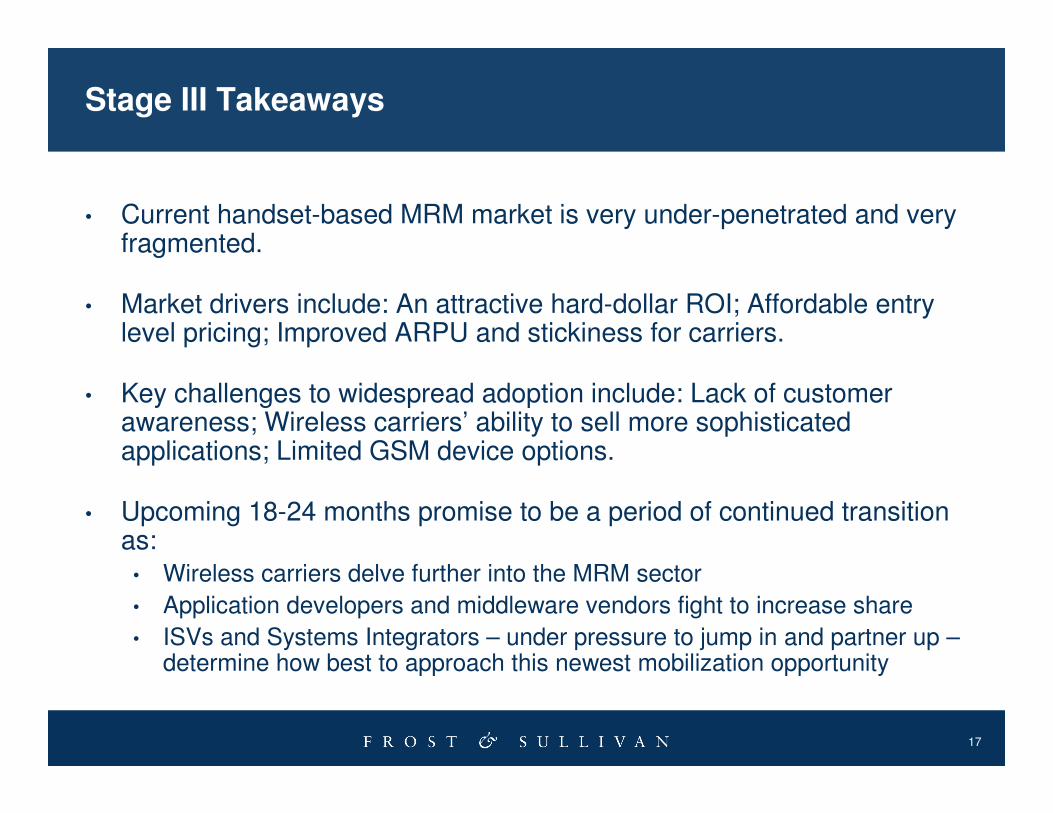

Stage III Takeaways

• Current handset-based MRM market is very under-penetrated and very fragmented.

• Market drivers include: An attractive hard-dollar ROI; Affordable entry level pricing; Improved ARPU and stickiness for carriers.

• Key challenges to widespread adoption include: Lack of customer awareness; Wireless carriers’ ability to sell more sophisticated applications; Limited GSM device options.

• Upcoming 18-24 months promise to be a period of continued transition as:

• Wireless carriers delve further into the MRM sector

• Application developers and middleware vendors fight to increase share

• ISVs and Systems Integrators – under pressure to jump in and partner up –determine how best to approach this newest mobilization opportunity

18

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by taking our survey.

What would you like to see from Frost & Sullivan?

19

For Additional Information

• To leave a comment, ask the analyst a question, or receive the free audio segment that accompanies this presentation, please contact Stephanie Ochoa, Social Media Manager at (210) 247-2421, via email, [email protected], or on Twitter at http://twitter.com/stephanieochoa.