Richard Woods, Georgia’s School Superintendent“Educating Georgia’s Future”

gadoe.org

GASBO 2016GaDOE

RESA Indirect Costs, Funding, and Other IssuesNovember 10, 2016

Amy Rowell – Financial Review

11/7/2016 1

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

AGENDA

• Indirect Costs Purpose and Definition• Indirect Cost Rate Calculation• RESA QBE Funding Formula• Other Grants Awarded to RESAs• Fiscal Reporting Requirements

11/7/2016 2

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent“Educating Georgia’s Future”

gadoe.org

Indirect Cost

11/7/2016 3

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost

An indirect cost rate is a means of determining, in a reasonable manner, the percentage of allowable general management costs that benefit each federal program or activity.

Indirect costs are generally administrative costs such as the salaries and expenses for staff engaged in organization‐wide activities.

11/7/2016 4

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect CostIndirect costs are recovered only to the extent of direct costs incurred. The indirect cost rate is applied to the direct cost amount expended, not to the grant award.The source of information utilized to determine indirect cost rates are the LEA's official FIN003 Financial Analysis Reports (DE 46).

11/7/2016 5

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost• Direct Costs ‐ those that can be identified specifically with a particular cost objective. These costs may be charged directly to grants, contracts, or to other programs against which costs are finally assigned. Typical direct costs chargeable to a grant include, but are not limited to:

• Compensation of employees for the time devoted and identified specifically to the performance of those programs;

• Cost of materials acquired, consumed, or expended specifically for the purpose of those programs;

• Travel expenses incurred specifically to carry out the program; etc.

11/7/2016 6

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost• Indirect Costs ‐ Incurred for a common or joint purpose benefiting more than one cost objective.

• Not readily assignable to the cost objectives specifically benefitted, without effort that is disproportionate to the results achieved.

• Typical examples: procurement, payroll, personnel functions, maintenance and operations of space, data processing, accounting, auditing, budgeting, communications (telephone, postage), etc.

11/7/2016 7

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost

A cost may not be allocated to a federal program as an indirect cost if any other cost incurred for the same purpose, in like circumstances, has been assigned to a federal program as a direct cost.

11/7/2016 8

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect CostRestricted Rates – applied to those federal programs with supplement versus supplant rules.

This means that the funds are for support in addition to state and local funding.

Non Restricted Rates – applied to those federal programs not subject to the supplement versus supplant legislative regulations.

For LEAs, most common grant is Child Nutrition Cluster.

11/7/2016 9

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect CostRestricted Rate Versus Non Restricted RateRestricted Rate ‐ Indirect cost rate pool (numerator) includes only expenditures of general management costs and fixed charges.

Non Restricted Rate ‐ Expenditures for the Superintendent and operations and maintenance of plant are classified as indirect costs when calculating an unrestricted rate. All other costs are classified the same as the restricted rate calculations.

11/7/2016 10

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 11

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 12

• FY 2016 Rate Calculated.• Using FY 2014 DE 46 Actual Financials.• Compares Amount of Indirect Costs calculated by Indirect Costs Reported.

• Determines the amount that is over or under the amount recovered and carries forward the effect of the difference.

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 13

Total Expenditures Identified as Indirect Costs +/‐ Indirect Costs RecoveredTotal Expenditures Identified as Direct Costs PLUS Non Allowable Costs Indirect Cost Rate

470,851.87 + 77,262.939,208,167.61 + 808,578.20 5.47%

=

=

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 14

• How is the Indirect Cost Amount Over or Under the Calculated Amount Determined?

• Comparing Indirect Costs Calculated to the Amount of Actual Costs Recovered (i.e. Charged)

• We are using the FY 2014 Actual Expenditures to calculate the FY 16 Indirect Costs Rate. So using the rate that was calculated for FY 2014, we determine the amount of indirect costs that would have been expected based on the direct and unallowable expenditures reported for FY 2014. We then compare the amount calculated to the Indirect Costs Recorded Plus the Carry‐forward adjustment utilized in FY 2014.

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 15

• How is the Indirect Cost Amount Over or Under the Calculated Amount Determined?

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 16

• Now Compare the Expected FY 2014 Indirect Costs to the Actual Amount +/‐ Carryforward

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

11/7/2016 17

• The Amount Recovered OVER the calculated amount will reduce the FY 2018 Rate calculation (which the FY 2016 expenditures will be used to calculate)

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation – Excluded Costs

• On Behalf Payments• Payments to Charter Schools

• Payments to Residential Treatment Centers

• Subcontracts in Excess of $25K

• Capital Outlay Costs

• RESA Fees• Interest Payments• Redemption of Bond Principal

• Amortization of Bond Issuance

• Transfers Out• Special Items• Extraordinary Items

11/7/2016 18

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation – Not Allowable

• School Board Salaries• Superintendent Salaries• Assistant Superintendent Salaries• General Administration Assistants Salaries• Related benefits, travel costs for employees listed above• School Administration Expenditures (excluding depreciation expense – which is Direct)

11/7/2016 19

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation – Types of Indirect Costs

• Terminated Leave Payments• Retirement Incentive Payments• Various costs charged to General Administration, Business Administration, Central Office, and Other Support Services

11/7/2016 20

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Indirect Cost Calculation

• How do you utilize the Indirect Cost rate?• Indirect costs are normally charged to Federal awards by the use of an indirect cost rate.

• Monthly, consider total costs charged to the Federal program, excluding payments to charters, RTCs, capital outlay costs, and terminated leave pay.

• Apply the percentage to those direct and unallowable expenditures incurred by the Federal program to allocate certain amount to General Fund.

• The indirect cost rate applied can be less than approved rate, but not more than approved rate.

11/7/2016 21

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent“Educating Georgia’s Future”

gadoe.org

RESA State Funding

11/7/2016 22

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA FundingO.C.G.A. §20‐2‐274“….state board shall be authorized to provide each [RESA] with a uniform state‐wide needs program grant and a documented local needs program grant, subject to appropriation by the General Assembly.”

“…shall consist of two components: the same fixed amount for each [RESA]; and an amount which reflects the number of local school systems, the number of schools, the number of students, and the number of square miles contained collectively within its member local school systems.”

11/7/2016 23

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA FundingWhat is considered in State QBE Allocation?

1. Number of School Systems Served in EXCESS of 62. Number of School Systems Served with FTEs LESS

than 3,3003. Number of Schools Served in EXCESS of 304. Number of FTEs Served in EXCESS of 18,0005. Number of Miles Served in EXCESS of 2,500

11/7/2016 24

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA State Wide Funding

11/7/2016 25

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

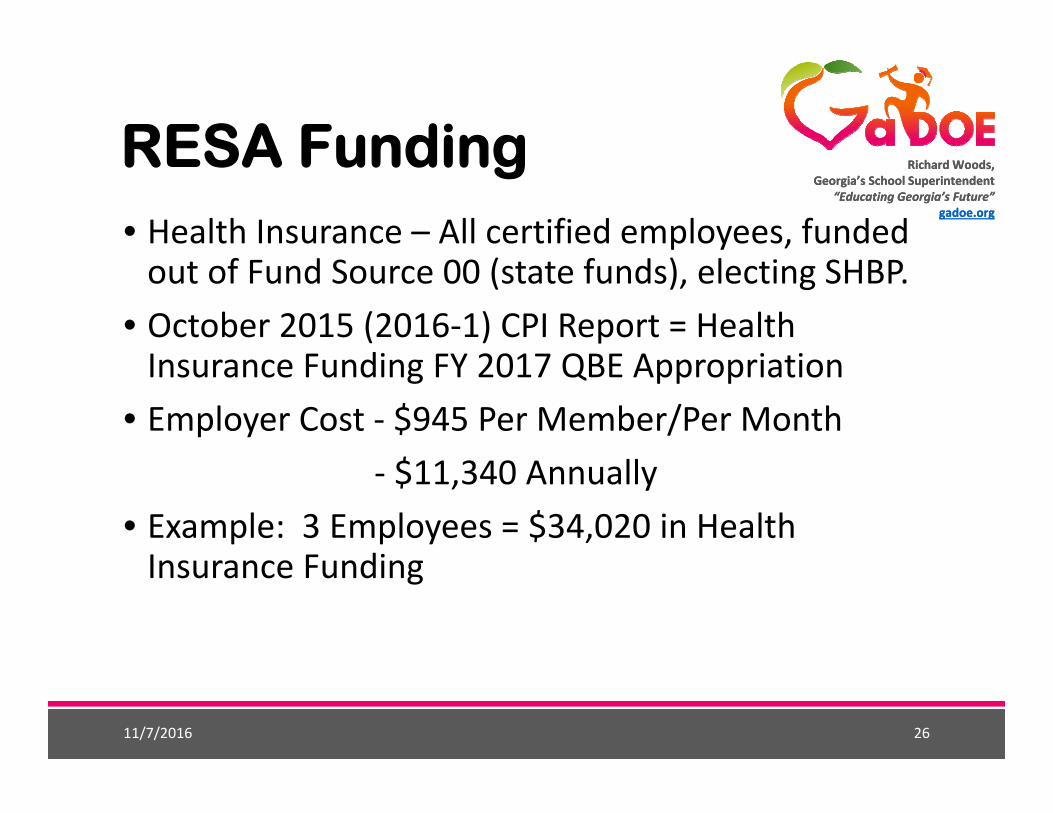

RESA Funding• Health Insurance – All certified employees, funded out of Fund Source 00 (state funds), electing SHBP.

• October 2015 (2016‐1) CPI Report = Health Insurance Funding FY 2017 QBE Appropriation

• Employer Cost ‐ $945 Per Member/Per Month‐ $11,340 Annually

• Example: 3 Employees = $34,020 in Health Insurance Funding

11/7/2016 26

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA Funding

11/7/2016 27

This RESA reported 3 certified employees, participating in SHBP, funded by the State funds (Fund Source 00).

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA Local Needs Funding

11/7/2016 28

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA Local Needs Funding

11/7/2016 29

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA FundingRESA Base Cost

+ Systems Served in Excess of 6 + Systems Served with FTEs less than 3,300

+Schools Served in Excess of 30+FTEs Served in Excess of 18,000+ Miles Served in Excess of 2,500= Total RESA QBE Basic Allocation

Local = 20% State = 80%

11/7/2016 30

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA FundingTotal RESA QBE Basic AllocationLocal = 20% State = 80%What about Austerity?

FY 2017 = Austerity 55.262% of State Earnings

Example: State Earnings of $1,044,373Austerity = $577,138Total State Grant as Reported in GAORS = $467,235

11/7/2016 31

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA FundingOther State GrantsEducation Technology Centers (ETC) Services Grant = $97,186 per RESAMath Mentor Grant = $105,854.13 per RESASchool Climate Specialist = Varies based on percentage of PBIS participating districts in the RESA. Ranges from $59,000 to $105,195ELA Professional Learning Specialist = $36,050

11/7/2016 32

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent“Educating Georgia’s Future”

gadoe.org

RESA Fiscal Reporting Requirements

11/7/2016 33

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

RESA Fiscal Reporting Requirements• Submit Financial Data as of June 30th to GaDOE• Financial Data is submitted to the State Accounting Office

• Financial Information is reported in State CAFR one year in arrears

• FY 2016 Financial Data provided to SAO in January 2017

• Worksheets for converting information needed for CAFR (including notes) updated and maintained by GaDOE

• Collection Process Administered by SAO

11/7/2016 34

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent“Educating Georgia’s Future”

gadoe.org

Questions?

11/7/2016 35

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Contact Information• Atlanta

• Hotline – 404‐656‐2447• Viola Darrington (404‐651‐8176) – [email protected]• Steve Lyle (404‐656‐6769) – [email protected]• Debara Montgomery (404‐656‐2344) –[email protected]

• Russ Swindle (404‐463‐0513) – [email protected]• Naylor (229‐241‐9915)

• Rhonda Metts – [email protected]

11/7/2016 36

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Richard Woods, Georgia’s School Superintendent

“Educating Georgia’s Future”gadoe.org

Contact Information

• Amy Rowell• [email protected]• Georgia Department of Education• 1652 Twin Towers East• 205 Jesse Hill Jr Drive• Atlanta, GA 30334• 404‐656‐6754

11/7/2016 37