GettingYourSaaSBusinessPreparedfortheNewRevenueRecognitionRules(ASC606)

Presentedby:SteveSehy,CaaS forSaaSModerator:ChrisWeber,SaaSOpticsJune20,2017

Welcome– 30secondsaboutus

SaaSOptics providesboth:• SaaSFinancials• SaaSMetricsCustomershavecollectivelyraised~$2BinVCandPEUntoldhoursofduediligenceandauditscrutiny

SteveSehy,CaaS forSaaSProvidingfractionalCFOservicestoSaaScompanies• ImplementingGAAP• PreparingforSeriesA/Professionalfinancing• Upgradingaccountingprocesses/systems• HandlingfinancefortheCEO

StartedcareerinSoftwareDevelopmentMovedtoProductManagementandProductDevelopmentManagementAuditoratRSM(previouslyMcGladrey)Keyclient:ProvidedfinancialleadershipforSaaScompanyHaikuLearningfortwoyearsoffinancialimprovements,endinginacorporateacquisitionbyaPrivateEquityfirm

WhyWe’reHere

SaaSCompanyAccountants/Management:• Tohelpyoutostarttheprocessofconvertingtothenewrevenue

recognitionrules.

Auditors/AccountingServiceproviders:• Tohelpyoutoworkwithyourclientsthroughtheprocessof

convertingtothenewrevenuerecognitionrules.

Agenda

• BackgroundandKeyConceptsforASC606

• KeySaaSrevenuesourcesandhowtotreatthem

• Allocatingtheprice

• ToDoList/CalltoAction

• Q&A

PollingQuestion

Whichtitlebestdescribesyourcurrentrole?(Selectone)

q Auditor/Serviceproviderq CEO/CFOofaSaaSCompanyq ControllerofaSaaSCompanyq AccountantofaSaaSCompanyq Other

NewRevenueRecognition- Background

AccountingName(ASUNo.2014-09,ASCTopic606)–RevenuefromContractswithCustomers:• Affectsallindustries• Attemptingtohaveasingleprocessfordeterminingrevenueinall

situations/industries• Principlesvs.Rules• ConvergencebetweenU.S.GAAPandInternationalGAAP• Fornon-publiccompaniesneedstobeinplaceforCalendaryear

2019.(ForSaaScompaniesthiswillincludeannualandmulti-yearagreementsmadein2018)

NewRevenueRecognition

Disclaimers:• Principlesvs.Rules– “judgement”

• SECrules

• Precedentssetby“firstimplementations”

• U.S.LegalEnvironment

• Auditorconclusions

• 50Minutes

NewRevenueRecognition

WeareNOTcovering:• Collectibility• Publiccompanies• Softwarelicenses(oldschoolsoftware)• Hardware• Usagefees• Contractmodifications*• Disclosures/Footnotesfornon-publiccompanies*

*Youshouldprobablylearnthis,wejustdon’thavetime.

PollingQuestion

Whatisyourmainreasonforattendingthiswebinar?

q Betterreportingofrevenueq Clearerdepictionofcompanyhealthq BecausewehavetoinordertobeincompliancewithGAAP(whichmostSeriesAtypefinancingsourceswillrequire).

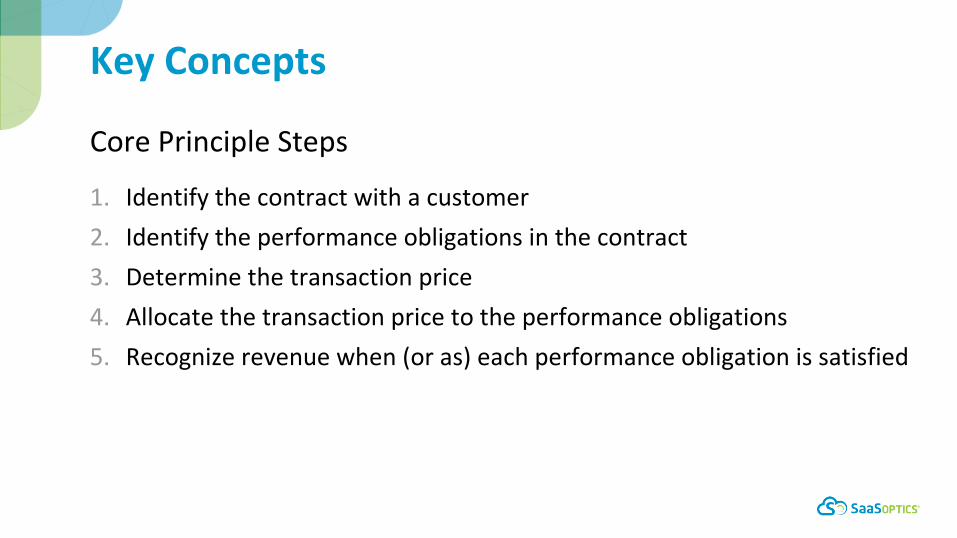

KeyConcepts

CorePrincipleSteps

1. Identifythecontractwithacustomer2. Identifytheperformanceobligationsinthecontract3. Determinethetransactionprice4. Allocatethetransactionpricetotheperformanceobligations5. Recognizerevenuewhen(oras)eachperformanceobligationissatisfied

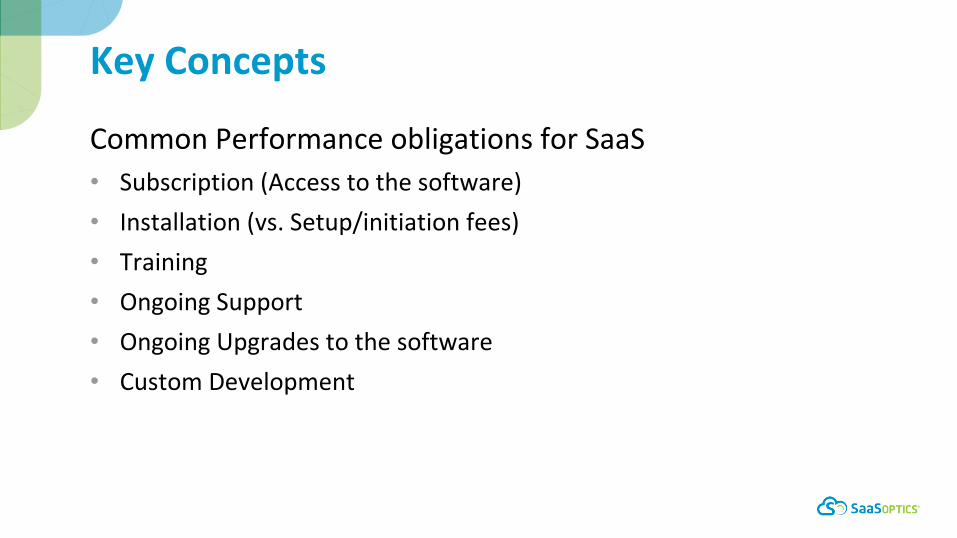

KeyConcepts

CommonPerformanceobligationsforSaaS• Subscription(Accesstothesoftware)• Installation(vs.Setup/initiationfees)• Training• OngoingSupport• OngoingUpgradestothesoftware• CustomDevelopment

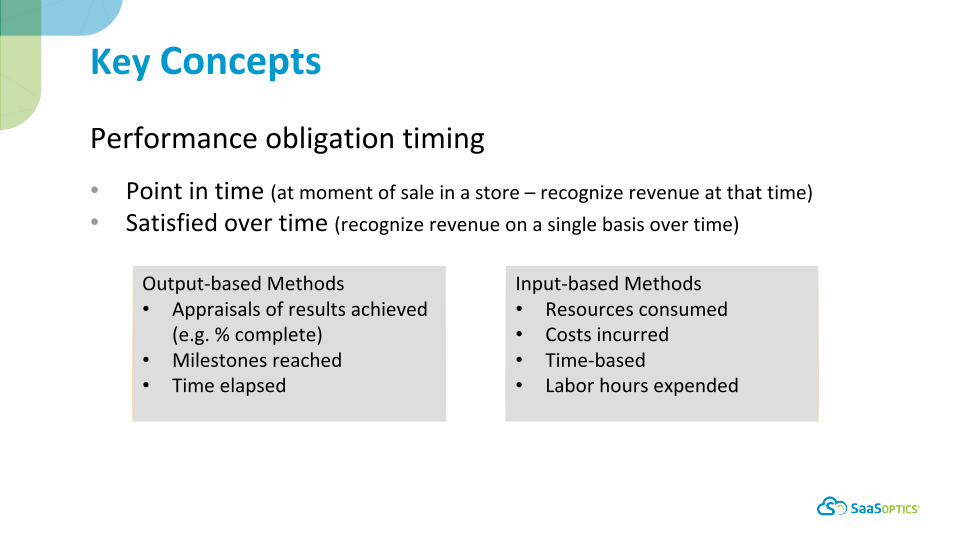

KeyConcepts

Performanceobligationtiming• Pointintime(atmomentofsaleinastore– recognizerevenueatthattime)• Satisfiedovertime(recognizerevenueonasinglebasisovertime)

Output-basedMethods• Appraisalsofresultsachieved

(e.g.%complete)• Milestonesreached• Timeelapsed

Input-basedMethods• Resourcesconsumed• Costsincurred• Time-based• Laborhoursexpended

Revenuebytype

CommonPerformanceobligationsforSaaS• WewillpresenthowtheycanbetreatedunderthenewGAAP• Showingexamplesofvarioussituations

SaaSRevenueRecognition- Subscriptions

Subscriptions• Usuallysatisfiedovertime• CalculatedusingtheTimeElapsed- Outputmethod

SaaSRevenueRecognition- SubscriptionsExamples:CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreement.Customerpays$1,200upfront.• Revenueisrecognizedas$100permonth.

CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreement.Customerpays$100permonth.• Revenueisrecognizedas$100permonth.

CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreement.Customerpays$300perquarter.• Revenueisrecognizedas$100permonth.

Moral– timingofpaymentsdoesnotimpactrevenuerecognition.

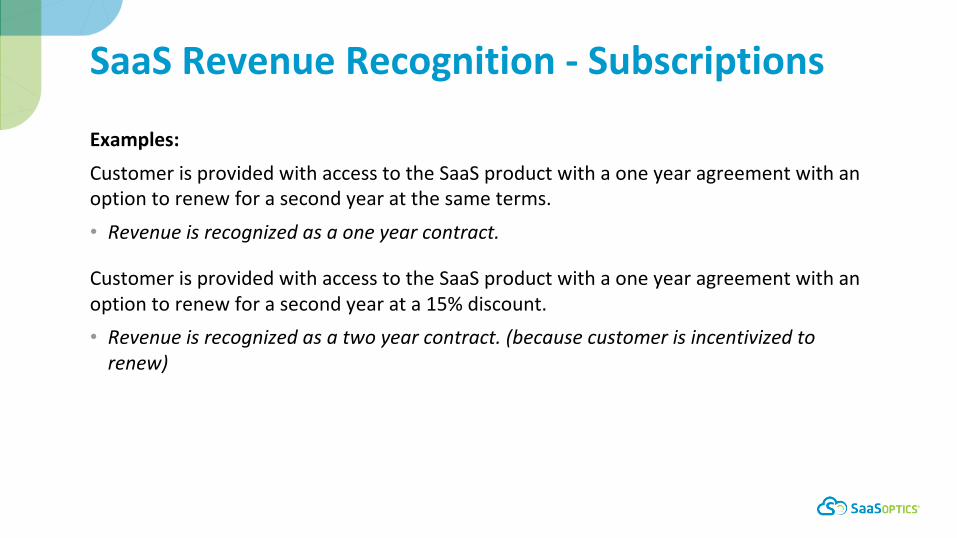

SaaSRevenueRecognition- Subscriptions

Examples:CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreementwithanoptiontorenewforasecondyearatthesameterms.• Revenueisrecognizedasaoneyearcontract.

CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreementwithanoptiontorenewforasecondyearata15%discount.• Revenueisrecognizedasatwoyearcontract.(becausecustomerisincentivizedtorenew)

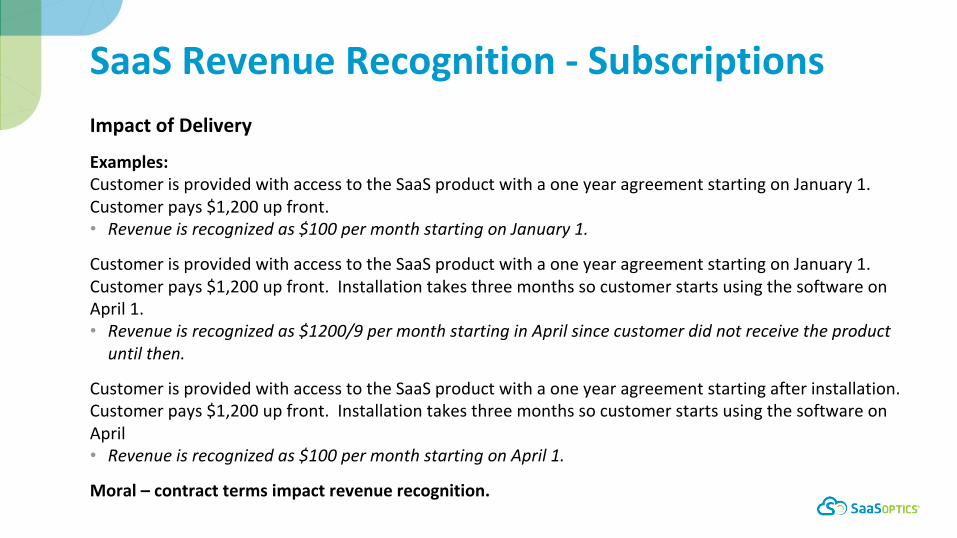

SaaSRevenueRecognition- SubscriptionsImpactofDelivery

Examples:CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreementstartingonJanuary1.Customerpays$1,200upfront.• Revenueisrecognizedas$100permonthstartingonJanuary1.

CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreementstartingonJanuary1.Customerpays$1,200upfront.InstallationtakesthreemonthssocustomerstartsusingthesoftwareonApril1.• Revenueisrecognizedas$1200/9permonthstartinginAprilsincecustomerdidnotreceivetheproductuntilthen.

CustomerisprovidedwithaccesstotheSaaSproductwithaoneyearagreementstartingafterinstallation.Customerpays$1,200upfront.InstallationtakesthreemonthssocustomerstartsusingthesoftwareonApril• Revenueisrecognizedas$100permonthstartingonApril1.

Moral– contracttermsimpactrevenuerecognition.

SaaSRevenueRecognition- Installation

InstallationFees• Usuallysatisfiedovertime• Dependingonyourcontract,thiscouldbecalculatedusingthe:1. TimeElapsed- Outputmethod,2. AppraisalsofResultsAchieved– Outputmethod3. Laborhoursexpended– InputMethod4. PointinTimemethod

SaaSRevenueRecognition- Installation

Examples:Customerisprovidedwithinstallationservicesforthefirst60days.Thisprocessispredictableandconsistentforallcustomers.Customerpays$1,200upfront.• Revenueisrecognizedas$600permonthfor2months.

Customerisprovidedwithinstallationservicesuntiltheinstallationiscomplete.Thisprocessistrackableandpredictable.Customerpays$1,200upfront.Attheendofthefirstmonththeprojectisestimatedtobe33%complete.• Revenueisrecognizedas$400forthefirstmonth.

Customerisprovidedwithinstallationservicesasabundleofhours.Customerpays$1,200upfrontfor12hours.Attheendofthefirstmonththeprojecthasconsumed8hours.• Revenueisrecognizedas$800forthefirstmonth.

SaaSRevenueRecognition- Installation

Examples(cont.):

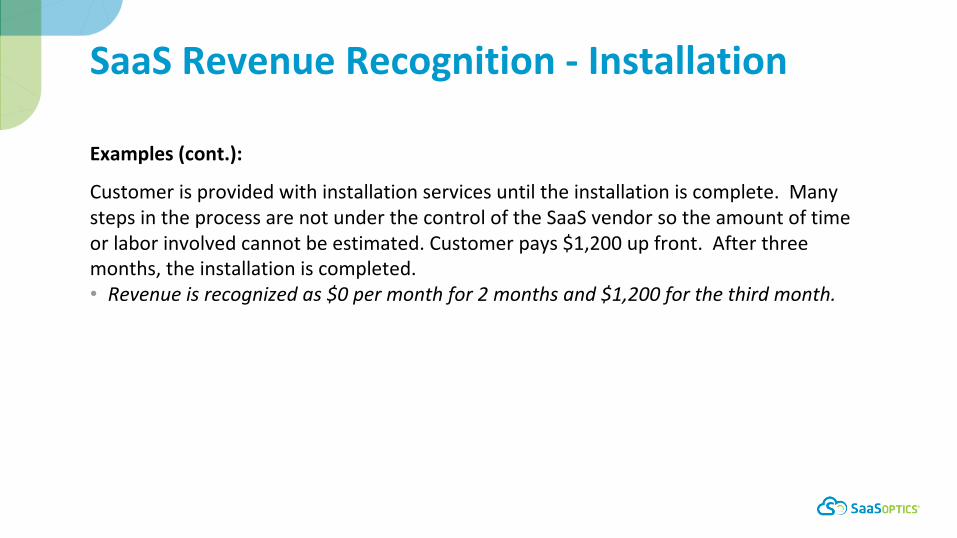

Customerisprovidedwithinstallationservicesuntiltheinstallationiscomplete.ManystepsintheprocessarenotunderthecontroloftheSaaSvendorsotheamountoftimeorlaborinvolvedcannotbeestimated.Customerpays$1,200upfront.Afterthreemonths,theinstallationiscompleted.• Revenueisrecognizedas$0permonthfor2monthsand$1,200forthethirdmonth.

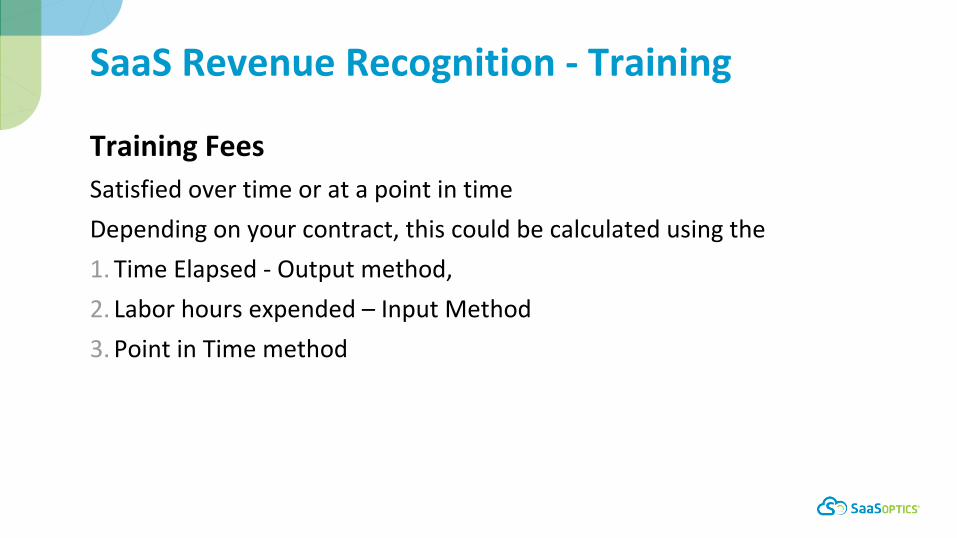

SaaSRevenueRecognition- Training

TrainingFeesSatisfiedovertimeoratapointintimeDependingonyourcontract,thiscouldbecalculatedusingthe1. TimeElapsed- Outputmethod,2. Laborhoursexpended– InputMethod3. PointinTimemethod

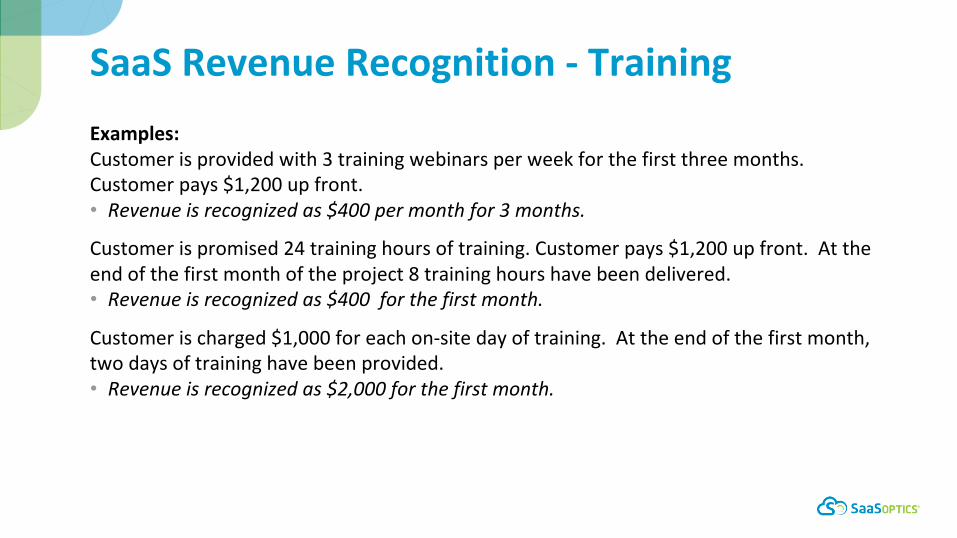

SaaSRevenueRecognition- TrainingExamples:Customerisprovidedwith3trainingwebinarsperweekforthefirstthreemonths.Customerpays$1,200upfront.• Revenueisrecognizedas$400permonthfor3months.

Customerispromised24traininghoursoftraining.Customerpays$1,200upfront.Attheendofthefirstmonthoftheproject8traininghourshavebeendelivered.• Revenueisrecognizedas$400forthefirstmonth.

Customerischarged$1,000foreachon-sitedayoftraining.Attheendofthefirstmonth,twodaysoftraininghavebeenprovided.• Revenueisrecognizedas$2,000forthefirstmonth.

SaaSRevenueRecognition- Support

SupportFeesSatisfiedovertimeoratapointintimeDependingonyourcontract,thiscouldbecalculatedusingthe1. TimeElapsed- Outputmethod,2. Laborhoursexpended– InputMethod3. PointinTimemethod

SaaSRevenueRecognition- SupportExamples:Customerisprovidedwithongoingphoneandothersupportduringaoneyearagreement.Customerpays$1,200upfront.• Revenueisrecognizedas$100permonth.

Customerispromised24hoursofsupport.Customerpays$1,200upfront.Attheendofthefirstmonthoftheproject8supporthourshavebeendelivered.• Revenueisrecognizedas$400forthefirstmonth.

Customerischarged$100foreachhourofsupport.Attheendofthefirstmonth,6hoursofsupporthavebeenprovided.• Revenueisrecognizedas$600forthefirstmonth.

SaaSRevenueRecognition- Upgrades

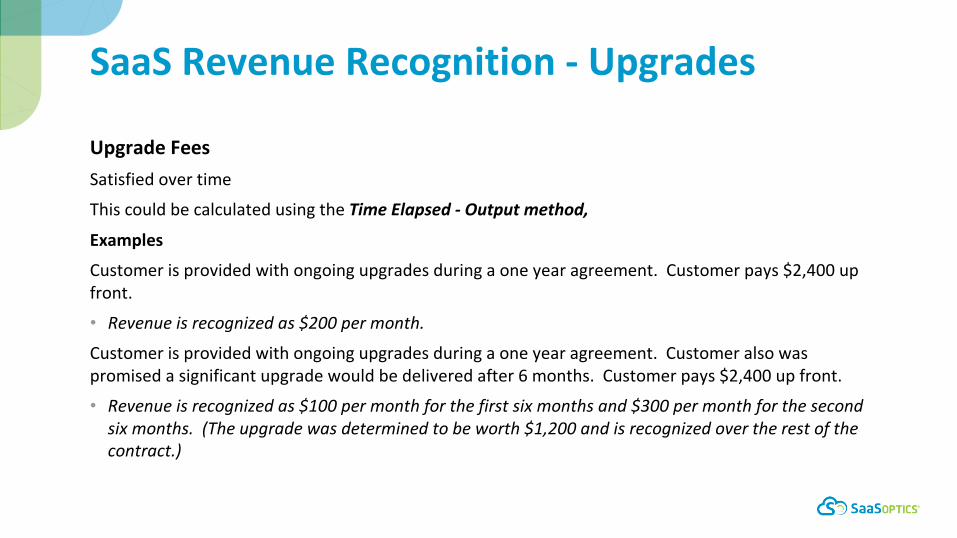

UpgradeFeesSatisfiedovertime

ThiscouldbecalculatedusingtheTimeElapsed- Outputmethod,

Examples

Customerisprovidedwithongoingupgradesduringaoneyearagreement.Customerpays$2,400upfront.

• Revenueisrecognizedas$200permonth.

Customerisprovidedwithongoingupgradesduringaoneyearagreement.Customeralsowaspromisedasignificantupgradewouldbedeliveredafter6months.Customerpays$2,400upfront.

• Revenueisrecognizedas$100permonthforthefirstsixmonthsand$300permonthforthesecondsixmonths.(Theupgradewasdeterminedtobeworth$1,200andisrecognizedovertherestofthecontract.)

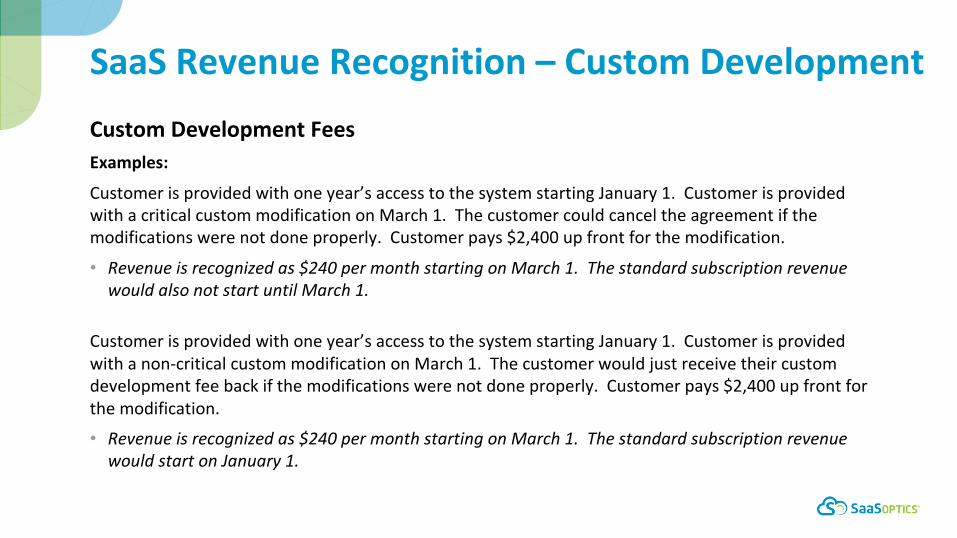

SaaSRevenueRecognition– CustomDevelopment

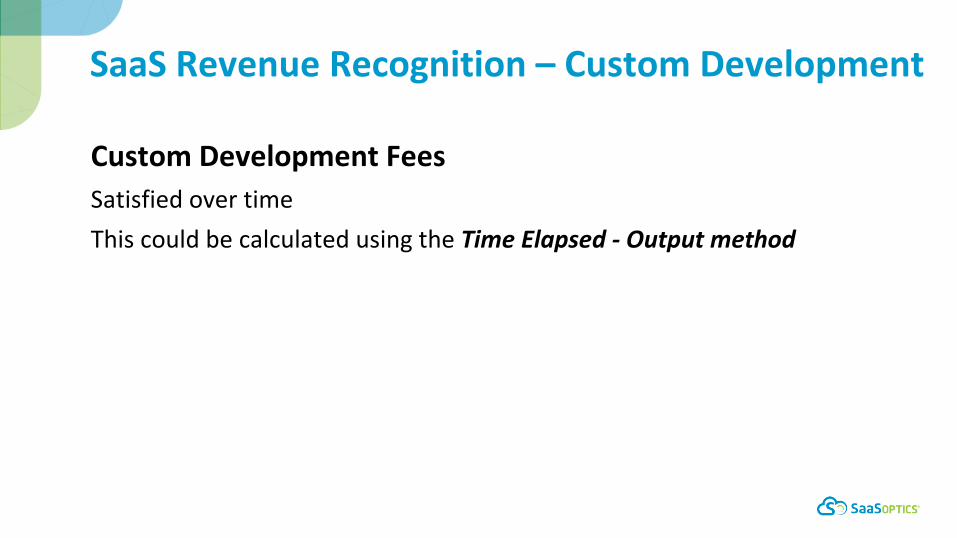

CustomDevelopmentFeesSatisfiedovertimeThiscouldbecalculatedusingtheTimeElapsed- Outputmethod

CustomDevelopmentFeesExamples:

Customerisprovidedwithoneyear’saccesstothesystemstartingJanuary1.CustomerisprovidedwithacriticalcustommodificationonMarch1.Thecustomercouldcanceltheagreementifthemodificationswerenotdoneproperly.Customerpays$2,400upfrontforthemodification.

• Revenueisrecognizedas$240permonthstartingonMarch1.ThestandardsubscriptionrevenuewouldalsonotstartuntilMarch1.

Customerisprovidedwithoneyear’saccesstothesystemstartingJanuary1.Customerisprovidedwithanon-criticalcustommodificationonMarch1.Thecustomerwouldjustreceivetheircustomdevelopmentfeebackifthemodificationswerenotdoneproperly.Customerpays$2,400upfrontforthemodification.

• Revenueisrecognizedas$240permonthstartingonMarch1.ThestandardsubscriptionrevenuewouldstartonJanuary1.

SaaSRevenueRecognition– CustomDevelopment

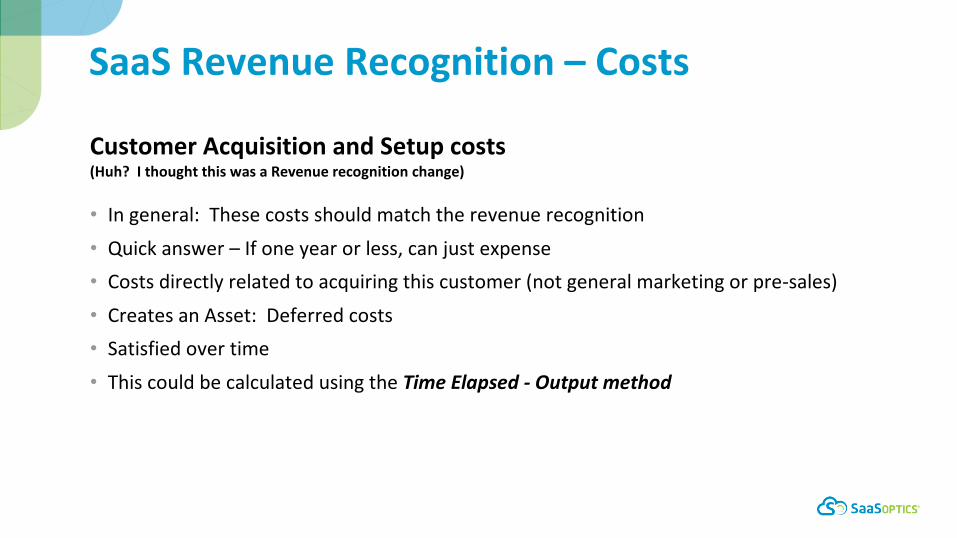

SaaSRevenueRecognition– Costs

CustomerAcquisitionandSetupcosts(Huh?IthoughtthiswasaRevenuerecognitionchange)

• Ingeneral:Thesecostsshouldmatchtherevenuerecognition• Quickanswer– Ifoneyearorless,canjustexpense• Costsdirectlyrelatedtoacquiringthiscustomer(notgeneralmarketingorpre-sales)• CreatesanAsset:Deferredcosts• Satisfiedovertime• ThiscouldbecalculatedusingtheTimeElapsed- Outputmethod

SaaSRevenueRecognition– Costs

CustomerAcquisitionandSetupCosts

Examples:

Customerisprovidedwithtwoyear’saccesstothesystemstartingJanuary1.Salescommissionforthetwoyearagreementis$2,400.• Salescommissioniscapitalizedasanasset.Costisrecordedas$100permonthstartingonJan1.

Customerisprovidedwithoneyear’saccesstothesystemstartingJanuary1.Directcostsofcustomersetupis$3,600.Customerisexpectedtorenewforatleasttwomoreyears.• Customercostiscapitalizedasanasset.Costisrecordedas$100permonthstartingonJanuary1.Spreadoverthethreeyearexpectedlifeoftheasset.

AllocatingthePrice

The“deal”doesnotmatterforallocatingtheprice

Customer1GoldPlanincludessubscription,hosting,supportandupgradesforoneyear.Customercharged$4,800.

Customer2Customerchargedbyitem:subscription$2,000,hosting$800,support$1,000,upgrades$1,000.Totalof$4,800.

Customer3Customerchargedforsomeitems,Othersare“free”:subscription$2,800,hostingfree,supportfree,upgrades$2,000.Totalof$4,800.

AllarethesameforGAAP– totalpriceof$4,800

AllocatingthePrice

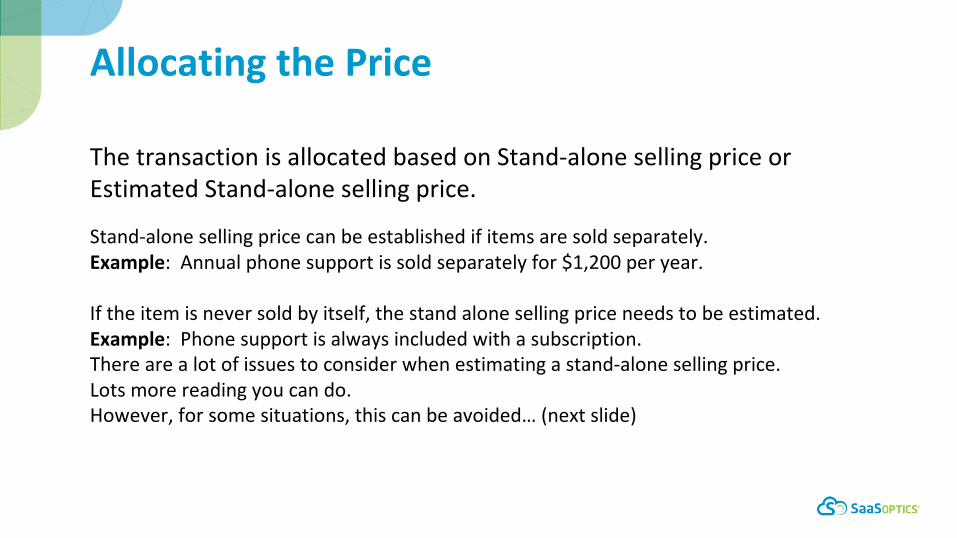

ThetransactionisallocatedbasedonStand-alonesellingpriceorEstimatedStand-alonesellingprice.

Stand-alonesellingpricecanbeestablishedifitemsaresoldseparately.Example:Annualphonesupportissoldseparatelyfor$1,200peryear.

Iftheitemisneversoldbyitself,thestandalonesellingpriceneedstobeestimated.Example:Phonesupportisalwaysincludedwithasubscription.Therearealotofissuestoconsiderwhenestimatingastand-alonesellingprice.Lotsmorereadingyoucando.However,forsomesituations,thiscanbeavoided…(nextslide)

AllocatingthePrice

Simpleoption:IfallofthePerformanceObligationswillbetreatedthesame,thenyoudon’tneedtoallocate.Example#1:AnnualSubscription,phonesupportandupgradesarealwayssoldtogetherandwillallbeallocatedovertheyear.Theycanbetreatedasoneitemforpriceallocation.• Subscription,phonesupportandupgradesaresoldfor$3,600forayear.Theseitemswouldnotneedtobeallocated.

Example#2:AnnualSubscription,phonesupportandupgradesarealwayssoldtogether,howeverphonesupportisbasedonhourswhiletheotheritemswillallbeallocatedovertheyear.Theycannotbetreatedasoneitemforpriceallocation.• Subscription,phonesupportandupgradesaresoldfor$3,600forayear.Theseitemswouldneedtobeallocatedbetweenthesubscription/upgradesandphonesupport.

AllocatingthePrice- Discounting

Ifthetransactionislessthanthesumofthestand-alonesellingprices,itshouldgenerallybespreadacrosstheitemsevenly.(Notethereareexceptionswhereyouwouldnot.)

Example:AnagreementwithInstallation,AnnualSubscription,phonesupportandupgradesissoldfor$4,800.Thesumofthestand-alonesellingpricesis$6,000.• The$1,200discountwouldbeevenlyspreadacrosstheitems.

Example:AnagreementwithInstallation,AnnualSubscription,phonesupportandupgradesissoldfor$4,800.Thesumofthestand-alonesellingpricesis$3,600.• Thisisnotexpectedtohappen,butifitoccursthe$1,200extrawouldbeevenlyspreadacrosstheitems.(Itmighthappenwithacustomerthatissmallerthanwhatisexpectedinthestand-aloneprice.)

CalltoAction/ToDoList

Whatyouneedtodoby12/31/17:• IdentifyallofyourPerformanceObligationsandhowyouwillrecognizetherevenue–includinghowyouwillgroupthem

• Determinehowyouwillallocatetheprice• Reviewyourstandardcontracts/TermsofServiceandmakesurethecontractisconsistentwithhowyouwanttotreattherevenue.

• Implementaprocessofpre-approvalorreviewofanycontractmodifications.• Contactyourauditor(oraconsultant)andreviewconclusions• Determinehowyouwillimplementthenewstandard,(starting1/1/18or1/1/19)usingfullretrospectiveormodifiedretrospectivemethod

PollingQuestion

ForSaaScompanyemployees,whatrevenuerecognitionchangepreparationstepshaveyoualreadycompleted?(Selectallthatapply)

q IdentifiedPerformanceObligationsq Determinedpriceallocationprocessq ReviewedcurrentcontractsandTermsofServiceq Determinedimplementationplanq Noneoftheabove/OrnotaSaaSCompany

SelectedFurtherReading

1.FASBCodificationASC6062.RSMRevenueRecognition:AWholeNewWorld– Jan2017,43pages

http://rsmus.com/what-we-do/services/assurance/revenue-recognition-a-whole-new-world.html

3.RSMChangestorevenuerecognitioninthetechnologyindustry– Jan2017,18pageshttp://rsmus.com/what-we-do/services/assurance/financial-reporting-resource-center/financial-reporting-resource-center-revenue-recognition/changes-to-revenue-recognition-in-the-technology-industry.html

4.KPMGRevenueforSoftwareandSaaS– March2017,648pageshttps://frv.kpmg.us/reference-library/2017/03/revenue-for-software-and-saas.html

5.EarlyAdopter:Workday– Form10-QdatedApril30,2017

NewRevenueRecognitionRules

Q&A

SteveSehyCaaS forSaaSCFOConsulting

www.linkedin.com/in/stevesehy

ChrisWeberSaaSOptics

Thankyouforjoiningus!