1

2

Session 1

Chair: John MairGlobal Technology Manager,

Subsea 7

3

Subsea Technology to Exploit the Potential

Gilles HalleDevelopments and Planning

Manager Business Development,TOTAL E&P UK

TEPUK – Subsea 09 11/02/2009

Subsea technology … To Exploit The Potential

5 - TEPUK – Subsea 09 11/02/2009

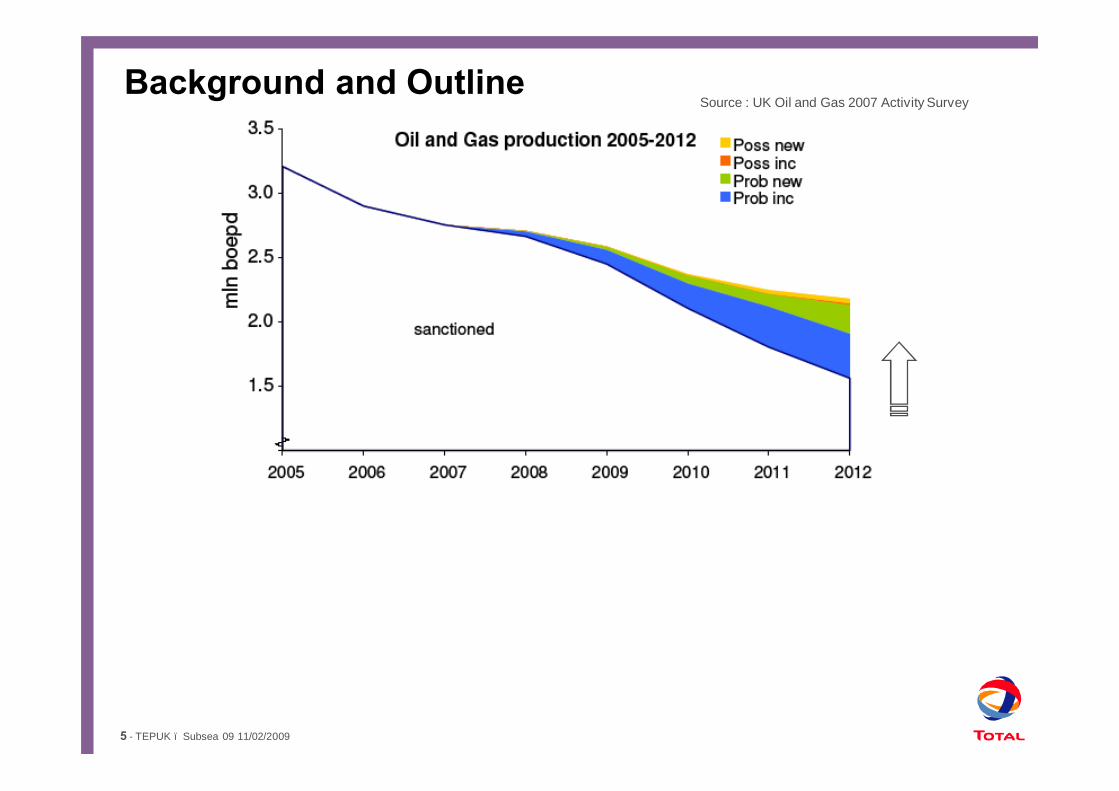

Source : UK Oil and Gas 2007 Activity SurveyBackground and Outline

6 - TEPUK – Subsea 09 11/02/2009

Source : UK Oil and Gas 2007 Activity SurveyBackground and Outline

Subsea 09 Aberdeen: “Exploiting the Potential”§ “What role for subsea technology in an era of declining production,

reducing average size of new discoveries and low oil price/high cost environment?”

§ “Do we need to consider different ways of exploiting these resources?”§ “Can we learn from others’ experiences?”§ “Are emerging technologies developed for other conditions (eg.

deepwater) equally applicable in the UKCS or NCS?”

7 - TEPUK – Subsea 09 11/02/2009

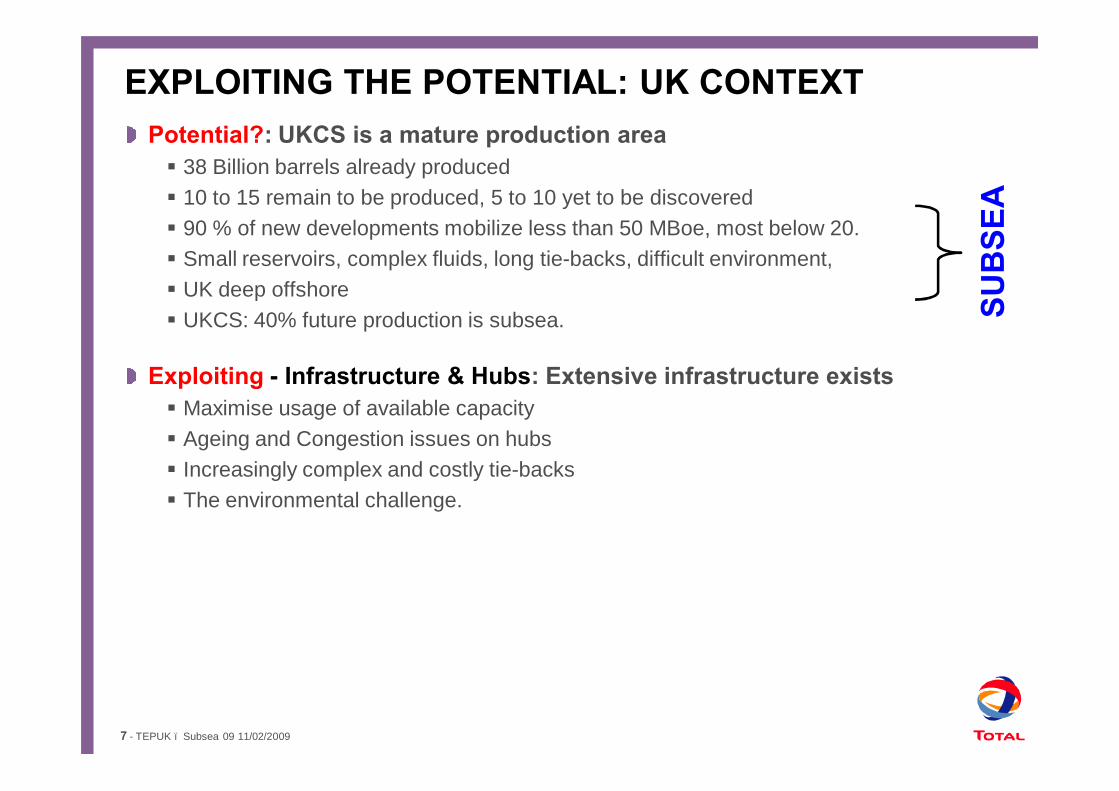

EXPLOITING THE POTENTIAL: UK CONTEXTPotential?: UKCS is a mature production area§ 38 Billion barrels already produced§ 10 to 15 remain to be produced, 5 to 10 yet to be discovered § 90 % of new developments mobilize less than 50 MBoe, most below 20.§ Small reservoirs, complex fluids, long tie-backs, difficult environment, § UK deep offshore§ UKCS: 40% future production is subsea.

Exploiting - Infrastructure & Hubs: Extensive infrastructure exists§ Maximise usage of available capacity§ Ageing and Congestion issues on hubs§ Increasingly complex and costly tie-backs§ The environmental challenge.

SUB

SEA

8 - TEPUK – Subsea 09 11/02/2009

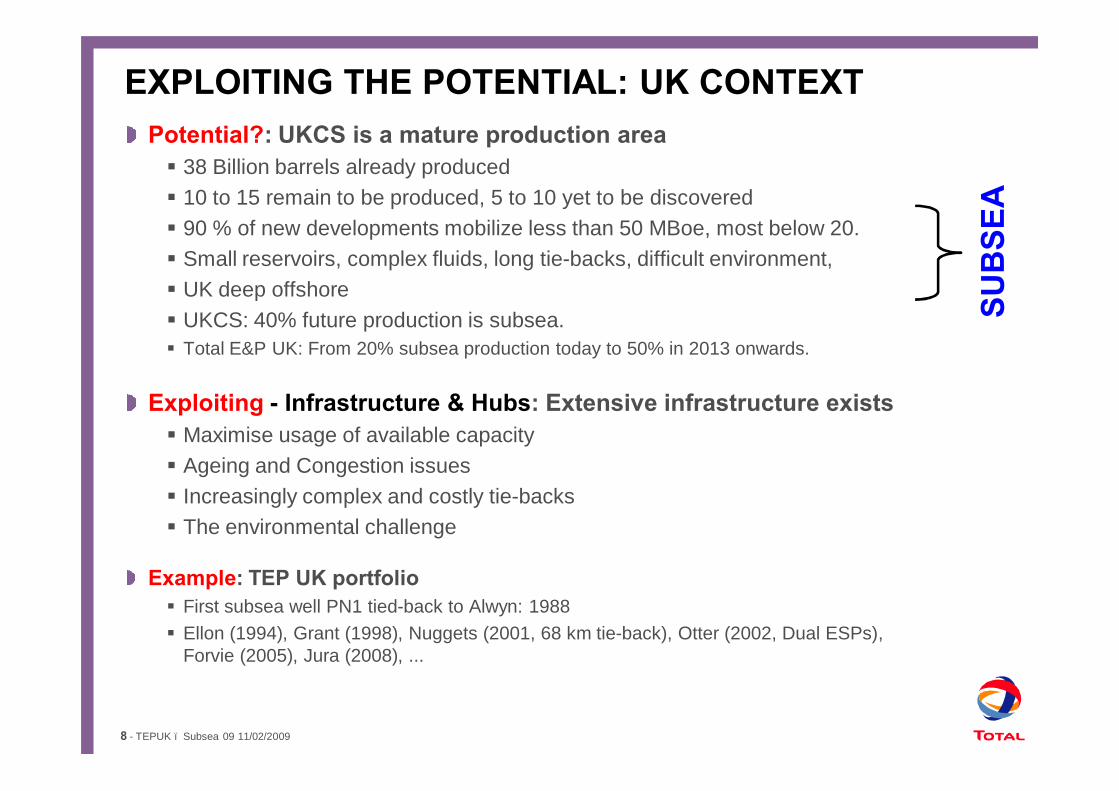

EXPLOITING THE POTENTIAL: UK CONTEXTPotential?: UKCS is a mature production area§ 38 Billion barrels already produced§ 10 to 15 remain to be produced, 5 to 10 yet to be discovered § 90 % of new developments mobilize less than 50 MBoe, most below 20.§ Small reservoirs, complex fluids, long tie-backs, difficult environment, § UK deep offshore§ UKCS: 40% future production is subsea.§ Total E&P UK: From 20% subsea production today to 50% in 2013 onwards.

Exploiting - Infrastructure & Hubs: Extensive infrastructure exists§ Maximise usage of available capacity§ Ageing and Congestion issues§ Increasingly complex and costly tie-backs§ The environmental challenge

Example: TEP UK portfolio§ First subsea well PN1 tied-back to Alwyn: 1988§ Ellon (1994), Grant (1998), Nuggets (2001, 68 km tie-back), Otter (2002, Dual ESPs),

Forvie (2005), Jura (2008), ...

SUB

SEA

9 - TEPUK – Subsea 09 11/02/2009

140

TEP UK SUBSEAPORTFOLIO

140

TEP UK SUBSEAPORTFOLIO

10 - TEPUK – Subsea 09 11/02/2009

Numerous Technological Challenges§ New architectural concepts§ Extended tie-backs for paraffinic and non-paraffinic fluids§ Subsea boosting and compression§ Subsea processing, decanter wells§ Umbilicals

EXPLOITING THE POTENTIAL: TECHNOLOGY

11 - TEPUK – Subsea 09 11/02/2009

Numerous Technological Challenges§ New architectural concepts§ Extended tie-backs for paraffinic and non-paraffinic fluids§ Subsea boosting and compression§ Subsea processing, decanter wells§ Umbilicals

Technology Transfer: Worldwide Market§Worldwide examples (Total)§ Deep offshore: Girassol – Angola – 240,000 bopd:

Project sanction July 1998 – Start-up December 2001§ Long distance tie-backs: Canyon Express – GOM –

100 km: Start-up September 2002§ Subsea processing and boosting: Pazflor – Angola:

3 subsea separation / multiphase boosting units. Project sanction Jan. 2008; Start-up 2011.

§… in the North Sea also§ HP/HT Subsea Christmas Tree: Kristin, Rhum,

Kessog (15 000 psi, 185 DegC. Installed Automn 2008).§ Subsea HP/HT HIPPS SIL3: Rhum, Kristin, Jura (May

2008)§ Subsea processing and boosting: Tordis

EXPLOITING THE POTENTIAL: TECHNOLOGY

12 - TEPUK – Subsea 09 11/02/2009

DALIA – ANGOLATotal Operator

13 - TEPUK – Subsea 09 11/02/2009

CONCLUSIONSSupply Chain Joint Effort§ Joint effort between operators & contractors/suppliers à Bridge the gap§ Oil and Gas Prices vs Costs vs Size of discoveries.§ Short Term Target: Applying “best-in-class” technology as made available.§ Reliability and Long Term operability of subsea systems, Standardization.

Hosts Platforms and Infrastructure: § Safety and Environment.§ Tie-backs to hosts: Detailed integration Studies.

Mid to Long term Target: Prepare in advance 10 – 20 years (R & D)§ Integration of Reservoir management and Subsea R&D / Technology§ Maximise late recovery of subsea developments § CO2 capture, transportation, injection: Role for Subsea?§ Bridges between Operators / Suppliers / Academy (NSRI)

Integrated Plannings – Integrated Teams Beyond Companies individual perimeters

14

Operator/Contractor Rapport – The Key to Creating Mutual Success

Eric KiltieProject Manager UK Engineering

CoordinatorPetro-Canada UK

* Marque de commerce de Petro-Canada - Trademark

Reference, date, place 15

Operator Contractor RapportThe Key to Creating Mutual Success

Operator Contractor RapportThe Key to Creating Mutual Success

Subsea 09 – AECC 11/02/09

2006 Petro-CanadaReference, date, place 16

Triton development area – Guillemot West

2006 Petro-CanadaReference, date, place 17

Triton development area – Guillemot West Western Extension

2006 Petro-CanadaReference, date, place 18

Triton development area – Clapham

2006 Petro-CanadaReference, date, place 19

Triton development area – Pict

2006 Petro-CanadaReference, date, place 20

Triton development area – Saxon

2006 Petro-CanadaReference, date, place 21

2006 Petro-CanadaReference, date, place 22

Clapham Manifold Installation

2006 Petro-CanadaReference, date, place 23

Pict Umbilical Cross-haul

2006 Petro-CanadaReference, date, place 24

Pict Manifold

2006 Petro-CanadaReference, date, place 25

Flexible Over-boarding

2006 Petro-CanadaReference, date, place 26

Pict Pipelay

2006 Petro-CanadaReference, date, place 27

Survey support

2006 Petro-CanadaReference, date, place 28

Triton FPSO

29

Working in Partnership has Never Been More Important

Mel FitzgeraldCEO, Subsea 7

www.subsea7.com subsea partner of choice11.02.2009

www.subsea7.com subsea partner of choice11.02.2009

Subsea UK Annual Conference

February 11th

Aberdeen Exhibition and Conference Centre

Mel Fitzgerald

Chief Executive OfficerSubsea 7

www.subsea7.com subsea partner of choice11.02.2009

www.subsea7.com subsea partner of choice11.02.2009

Subsea 7 Financial performance 2004 – 2008 (USDm)

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

(40.0)

(20.0)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

Revenue Net Income2005 2006 2007 2008*

2,000.0

2,200.0

2,400.0

180.0

200.0

220.0

(31)

138

2142189

813

1670

240.0

260.0

280.0264

2373

*2008 unaudited

1287

45

2004

Average NetIncome 8%

www.subsea7.com subsea partner of choice11.02.2009

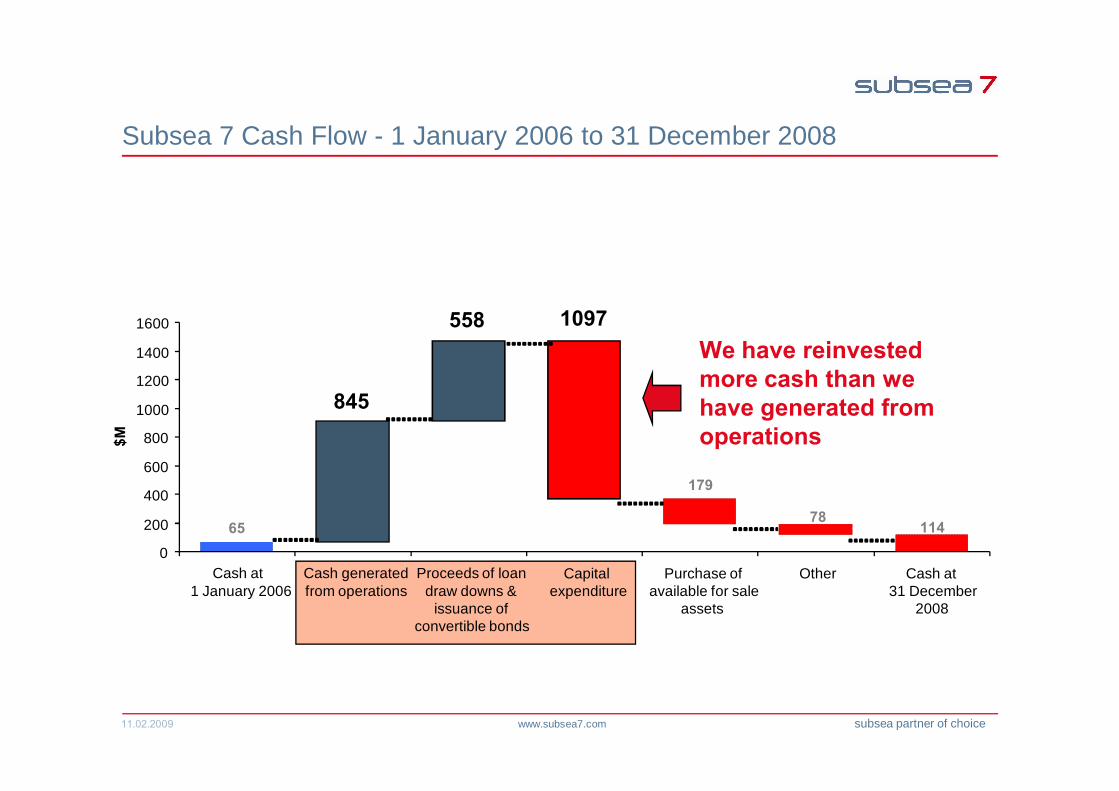

Subsea 7 Cash Flow - 1 January 2006 to 31 December 2008

We have reinvested more cash than we have generated from operations

65

845

558 1097

179

78114

0

200

400

600

800

1000

1200

1400

1600

Cash at 1 January 2006

Cash generatedfrom operations

Proceeds of loandraw downs &

issuance ofconvertible bonds

Capitalexpenditure

Purchase ofavailable for sale

assets

Other Cash at 31 December

2008

$M

www.subsea7.com subsea partner of choice11.02.2009

Industry cost escalation was becoming unsustainable

Actual project cost2004 2008

60-80% growth

40% increase in ‘staff’ costs.

30% increase in vessel related costs.

100% increase in some 3rd party costs, commodities and equipment.

www.subsea7.com subsea partner of choice11.02.2009

Softer market has been driving cost down

Actualproject cost

??

2008 2009Potential

project cost

January 2009 spot steel $300 / t (from $1300 / t in June 2008).

Vessel fuel and charter rates down –may go further.

Some realism has come back into wage demands.

These reductions are not immediate.

www.subsea7.com subsea partner of choice11.02.2009

Costs were increasing but……. now coming backThe high costs were driven by the global market demand for energy and scarce

resources.

Higher oil prices encouraged faster development which put even more pressures on scarce resources.

Yes margins have increased but realistic margins are required to sustain investment.

Focus on efficiency has helped Subsea 7 to drive better performance.

A willingness to look for and embrace new business models has helped Subsea 7 create shared value for clients and suppliers eg Venture Production plc, Block 31 and Merwede / Huisman.

The industry has the opportunity to get back to more sustainable cost levels.

Operators and the supply chain must work at this together; look at creating shared value, not put pressure on skilled, scarce resources and drive profit from the supply chain.

www.subsea7.com subsea partner of choice11.02.2009

The Venture Production / Subsea 7 Partnership

Subsea 7 was selected by Venture Production in 2005 to be their partner of choice for the supply of subsea services in the North Sea.

Venture were actively seeking a new type of contracting arrangement.

Partnership now executing over $100m of work each year for Venture.

Venture has saved over $300m to date; from a variety of areas such as bringing in engineering expertise earlier and by having access to vessels when they need them.

Partnership becoming attractive as a model by other operators.

Uni

t cos

ts $

/boe

2004 - 2007

Overall UKCS Development Costs

Venture Production5

20

Source: UK Oil &Gas and Venture Production

www.subsea7.com subsea partner of choice11.02.2009

BP - Block 31, Offshore Angola

• BP placed considerable emphasis on selecting a contractor that they believed would work in partnership to deliver the Programme.

• BP’s innovative contracting model offers enhanced commercial opportunities for both parties through a day rate contract and KPI driven margin targets.

• The KPI model recognises both hard and soft deliverables eg performing work in a safe and timely manner.

This programme for BP Angola includes up to four (4) developments.

The first of these - PSVM – has an awarded value of $460m.

www.subsea7.com subsea partner of choice11.02.2009

Working with the supply chain – Merwede and Huisman

A novel contracting model ensures that all parties, including the pipelay equipment supplier, are rewarded for the value created..

• Smooth (planned) process

• Helps manage their risk

• Leads to shorter building period

• Helps control cost levels

Supplier benefits: Subsea 7 benefits:

• Integrated planning process

• Lower design / build costs

• Reduced management costs

• Optimised technical solution

• Improved risk management

Low operational costsRepeat business

On budgetOn time delivery

www.subsea7.com subsea partner of choice11.02.2009

Key messages to take away

Cost growth is not sustainable.

Work together / focus on efficiency to take unnecessary costs out.

Contractors should not be asked to take on unmanageable risk.

The supply chain needs to remain profitable to survive.

We can not afford to lose the skill sets that we have developed in recent years.

Innovative contracting model’s can create value between operators and contractors - and contractors and their supply chain.

It’s all about creating and recognising shared value.

www.subsea7.com subsea partner of choice11.02.2009

Or do you really want to go back to the old ways?

Drive down contractors margins?

Create adversarial relations?

Have contractors take on unmanageable risks?

Have no ongoing investment in the assets and equipment required for a sustainable future?

See graduate programmes disappear?

See no investment in skills development?

See contractors go to the wall / merge?

www.subsea7.com subsea partner of choice11.02.2009

subsea partner of choice

44

Lower Oil Prices and the Subsea Sector

Colin WelshCEO, Simmons & Company

International

Low Oil Prices And The Financial Crisis:Impact On The Subsea Sector

11 February 2009