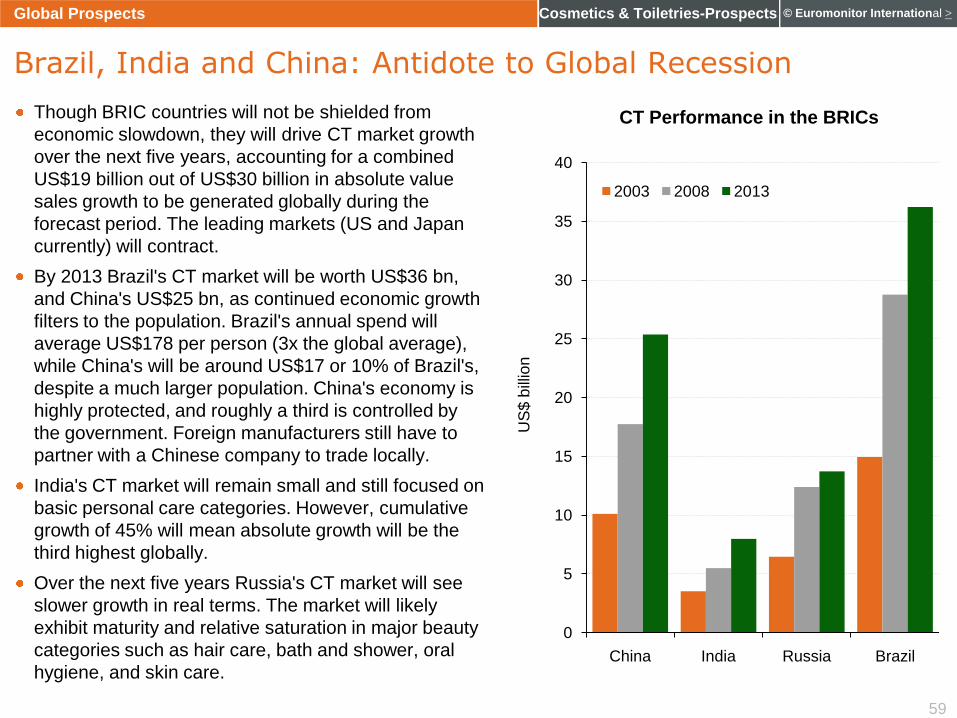

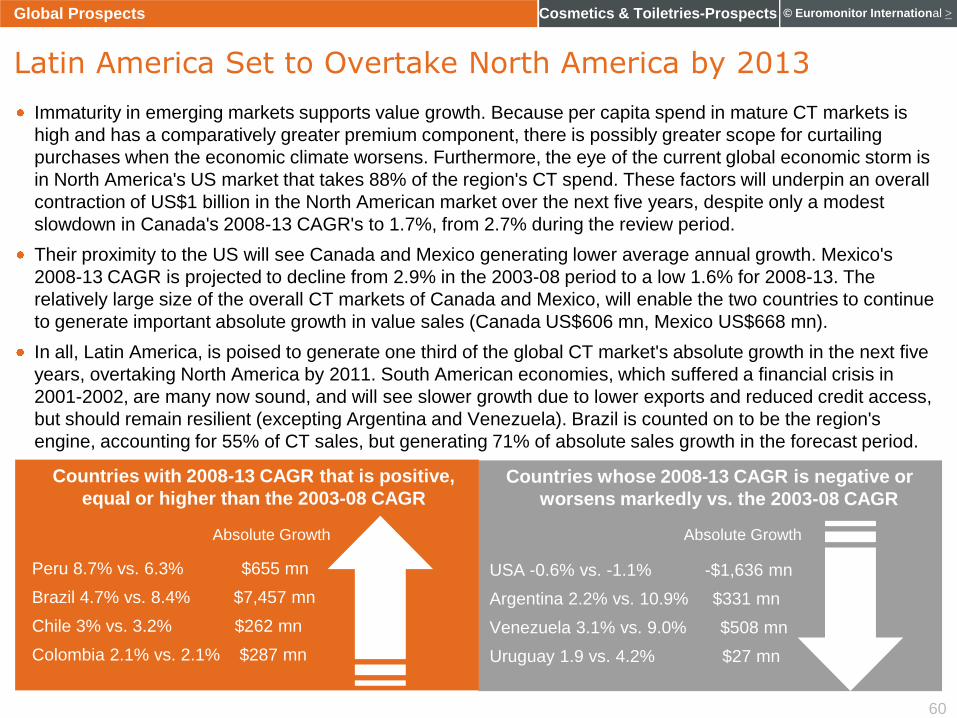

1

© Euromonitor International >Cosmetics & Toiletries-Prospects

Global Cosmetics and Toiletries:

Industry Prospects for 2009 and

Beyond

August 2009

2

© Euromonitor International >Cosmetics & Toiletries-Prospects

Global Snapshot

Regional Overview

Category Review

Channel Analysis

Competitive Environment

Global Prospects

Appendix

3

© Euromonitor International >Cosmetics & Toiletries-Prospects

Buoyed by continued strong growth in emerging markets, the global cosmetics and toiletries market suffered

but a slight slowdown in 2008 despite a full fledged global recession by the end of the year.

The leading markets of the US and Japan saw declines that will persist over the forecast years. Elsewhere,

the effects of the recession on CT spend, will be far more evident in 2009. Growth of only 0.7% in real prices

is forecast for the global CT sector in 2009, driven by skin care and men's grooming products.

Consumers are sacrificing luxury brands for mass or masstige alternatives and premium cosmetics are

bearing the brunt of the economic downturn. In 2009, consumers globally are expected to reduce their

premium CT spend by 1.3%, while hair care will be the only category to see negative growth (-0.3%).

Against the backdrop of tightened consumer purses, resilient and dynamic sectors are being skin care (anti-

agers), men's grooming products (undeveloped sector with untapped opportunities), sun care (education and

rising awareness of anti-ageing benefits), baby care (high population growth and rising incomes in emerging

regions; unwillingness to sacrifice on baby needs by parents in developed markets) and deodorants (as

replacement for fragrances). By 2010, all categories as well as premium, will see renewed expansion.

Despite being less dynamic than other categories, hair care, fragrances and colour cosmetics, will be key

contributors to global absolute value growth over the forecast period, by virtue of sheer size. Skin care, on the

other hand, will be of critical importance, being both amongst both dynamic as well as the largest category.

The Asia Pacific region, excluding Japan, and Latin America are the key growth markets of the future,

particularly, BRIC countries, China, Brazil and India. Success strategies for international manufacturers will

need to incorporate geographic expansion and product share gains in key categories such as skin and hair

care markets and China and Brazil, while laying the seeds in "frontier" markets with highest potential.

The CT consumer base is increasingly sophisticated and global. It is both keen on preventing ageing through

scientific progress, and ethically and environmentally conscious. To succeed, manufacturers thus also need to

invest in efficacious, technologically advanced formulations, as well as be innovative in their

marketing/packaging, addressing consumer concerns and adding clear value/benefits to their purchases.

Global Snapshot

Key Findings

4

© Euromonitor International >Cosmetics & Toiletries-ProspectsGlobal Snapshot

Key Industry Issues

Consumers are increasingly concerned about the safety and purity of products

they consume, as well as their effect on the environment. Products that have

claims of being "natural", "organic" and/or eco-friendly are growing in popularity

across regions, and becoming mainstream. Greatest impact is on baby and

body skin care, and bath and shower. The organics trend is also spreading to

products where efficacy has been a priority, such as facial skin care, hair care

and colour cosmetics.

Consumer perceptions of luxury are changing. Luxury

is an enriching personal experience and no longer a

premium price-tag. Beauty masstige items can now

become affordable luxuries (at "mass prices") in a

tough economic climate. They are positioned across

the whole product spectrum.

Demand is on the rise for technologically advanced

formulations that are positioned on the boundaries of

cosmetics and drugs (cosmeceuticals). These

products are often seen as alternatives to surgery

and include both facial anti-agers as minimally-

invasive treatments such as "Botox."

The economic downturn is making

shoppers more value conscious.

The "at home" beauty care market

is benefitting as a cheaper

substitute to costly out-of home

services such as salons/spas (hair

colorants, perms/relaxants,

depilatories, nail polish), or dentist

visits (teeth whitening and

professional oral hygiene kits).

Beauty is merging with health and

well-being and becoming more

holistic – not just internal

appearance but also physical and

spiritual well-being. CT products

are taking new forms – from jars to

foods. Interest in nutricosmetics

and functional foods is

complementing the traditional

beauty industry.

5

© Euromonitor International >Cosmetics & Toiletries-ProspectsGlobal Snapshot

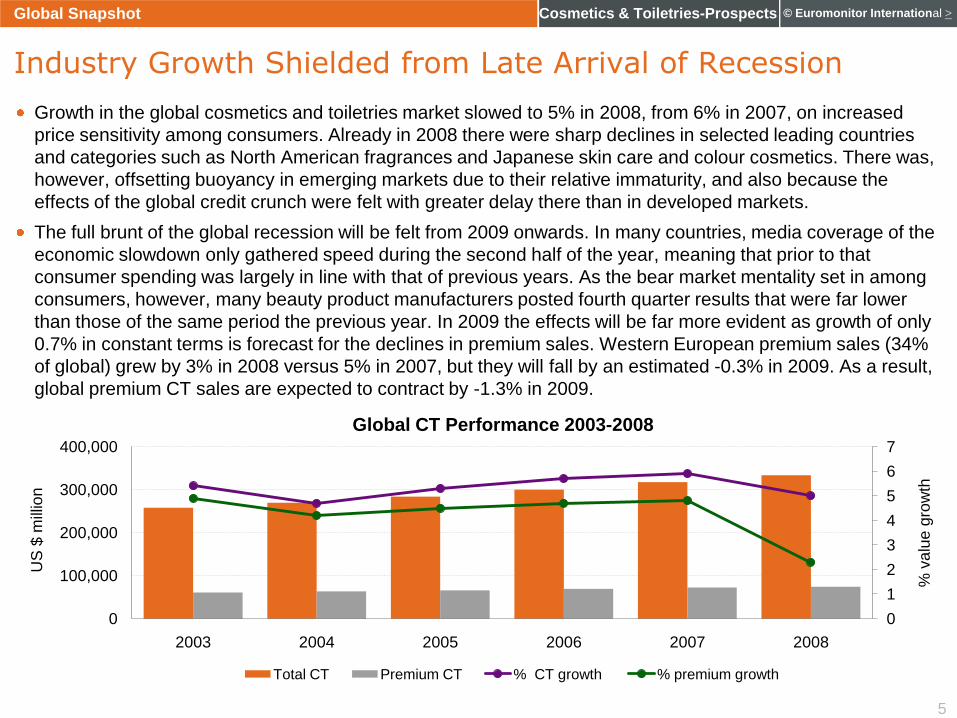

Industry Growth Shielded from Late Arrival of Recession

Growth in the global cosmetics and toiletries market slowed to 5% in 2008, from 6% in 2007, on increased

price sensitivity among consumers. Already in 2008 there were sharp declines in selected leading countries

and categories such as North American fragrances and Japanese skin care and colour cosmetics. There was,

however, offsetting buoyancy in emerging markets due to their relative immaturity, and also because the

effects of the global credit crunch were felt with greater delay there than in developed markets.

The full brunt of the global recession will be felt from 2009 onwards. In many countries, media coverage of the

economic slowdown only gathered speed during the second half of the year, meaning that prior to that

consumer spending was largely in line with that of previous years. As the bear market mentality set in among

consumers, however, many beauty product manufacturers posted fourth quarter results that were far lower

than those of the same period the previous year. In 2009 the effects will be far more evident as growth of only

0.7% in constant terms is forecast for the declines in premium sales. Western European premium sales (34%

of global) grew by 3% in 2008 versus 5% in 2007, but they will fall by an estimated -0.3% in 2009. As a result,

global premium CT sales are expected to contract by -1.3% in 2009.

0

1

2

3

4

5

6

7

0

100,000

200,000

300,000

400,000

2003 2004 2005 2006 2007 2008

% v

alu

e g

row

th

US

$ m

illio

n

Global CT Performance 2003-2008

Total CT Premium CT % CT growth % premium growth

6

© Euromonitor International >Cosmetics & Toiletries-ProspectsGlobal Snapshot

Categories' Resilience Varied Markedly Across Regions

Deodorants and baby care were the best performers globally in 2008 with growth rates of 8% and 7% respectively. These

two sectors, along with bath and shower, were also the only ones to outperform their percentage rise of the previous year.

Latin American's love for scents underpinned strong growth in deodorant roll-ons and sprays. Unwillingness by parents to

give up quality on their children's products together with increased purchases for adult consumption (baby lotion) boosted

baby-care products demand.

Premium cosmetics and toiletries bore the brunt of the impact of decreasing consumer confidence and disposable income

and rising unemployment rates. The category's growth rate more than halved to 2% in 2008, as consumers sacrificed

luxury brands for mass or masstige alternatives.

While global skin care spend slowed to 5.5% growth (7.1% in 2007), nourishers /anti-agers remained star performers,

expanding by 9.7% or only 0.6 percentage points less than in 2007. This adds substance to the belief that most consumers

will sacrifice on many other fmcg's before they will alter their facial care routines.

Other resilient sectors included under-developed men's grooming (-0.3 or +6.1% in 2008), and sun care that despite

declining 1.3 percentage points, remained the most dynamic sector over the 2003-08 review period. Though global hair

care spending decelerated by 1.3 percent points and was the slowest growing category, the sheer magnitude of this

relatively mature sector determined it was the second largest contributor to absolute value growth during the review period.

0

4

8

12

16

0

20

40

60

80

% v

alu

e g

row

th

US

$ b

illio

n

Global Sales by Category

Sales (2008, US$bn) % change 2007-08 % change 2006-07

7

© Euromonitor International >Cosmetics & Toiletries-Prospects

Global Snapshot

Regional Overview

Category Review

Channel Analysis

Competitive Environment

Global Prospects

Appendix

8

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

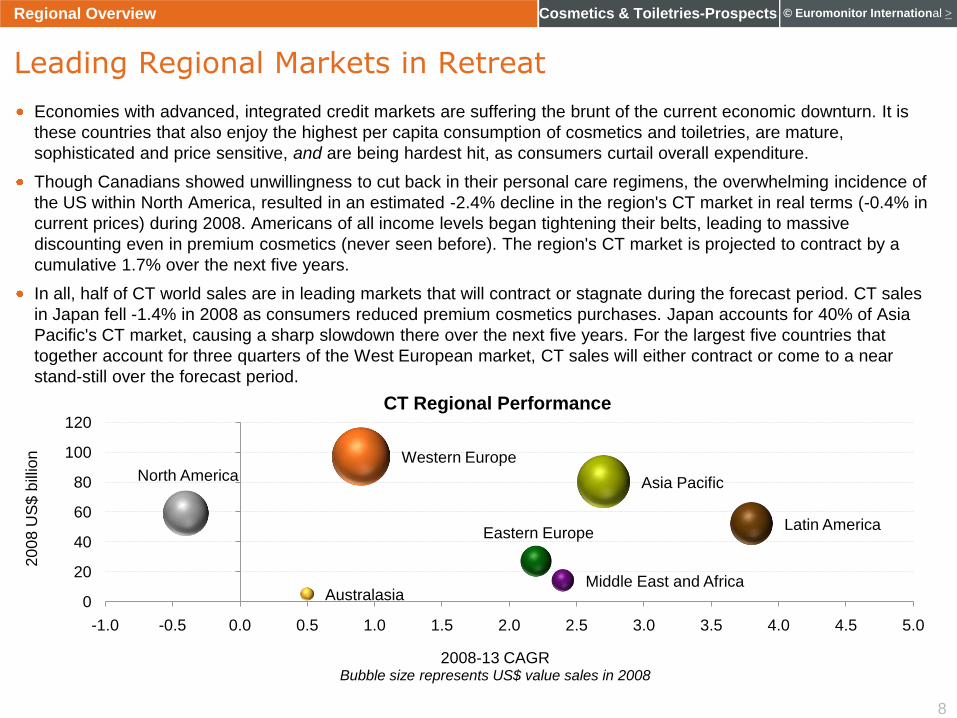

Leading Regional Markets in Retreat

Economies with advanced, integrated credit markets are suffering the brunt of the current economic downturn. It is

these countries that also enjoy the highest per capita consumption of cosmetics and toiletries, are mature,

sophisticated and price sensitive, and are being hardest hit, as consumers curtail overall expenditure.

Though Canadians showed unwillingness to cut back in their personal care regimens, the overwhelming incidence of

the US within North America, resulted in an estimated -2.4% decline in the region's CT market in real terms (-0.4% in

current prices) during 2008. Americans of all income levels began tightening their belts, leading to massive

discounting even in premium cosmetics (never seen before). The region's CT market is projected to contract by a

cumulative 1.7% over the next five years.

In all, half of CT world sales are in leading markets that will contract or stagnate during the forecast period. CT sales

in Japan fell -1.4% in 2008 as consumers reduced premium cosmetics purchases. Japan accounts for 40% of Asia

Pacific's CT market, causing a sharp slowdown there over the next five years. For the largest five countries that

together account for three quarters of the West European market, CT sales will either contract or come to a near

stand-still over the forecast period.

Western Europe

Asia PacificNorth America

Latin AmericaEastern Europe

Middle East and AfricaAustralasia0

20

40

60

80

100

120

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

20

08

US

$ b

illio

n

2008-13 CAGRBubble size represents US$ value sales in 2008

CT Regional Performance

9

© Euromonitor International >Cosmetics & Toiletries-Prospects

Asia Pacific will emerge the global driver of economic recovery. Excluding Japan, annual CT 2008-2013 sales

will grow 5.2% on average, spurred by brisk demand for skin care (and sun care), the largest and most

dynamic category, followed by hair care (2nd largest). CT sales in China and India (55% of AP-ex Japan),

have slowed but projected 5 year CAGRs are above 7%, offsetting weakness in Taiwan, and South Korea.

Latin America was the most dynamic market in the review period, contributing 30% of global absolute growth

in CT spend. Declines in hair care spend in the saturated markets of North America and Western Europe,

were offset by strong growth in Latin America thanks to increased penetration of conditioners and colourants

that are increasingly popular with teens and young adults.

CT value sales in several Eastern European markets should decline in 2009, however, the two largest, Russia

and Poland will expand by slightly over 1%, and the entire region begin recovery in 2010. Spend by category

is fairly spread in Eastern Europe. Skin care (20% of CT spend), hair care (18%), fragrances (17%), and

colour cosmetics (13%) are the key sectors by size and absolute growth. Russians are very designer oriented

in fashion, however, premium cosmetics spend that takes a greater share of CT spend in Eastern Europe than

in other emerging markets (14.9% CAGR 2003-08), is set to slow markedly.

Regional Overview

Emerging Economies Lead Industry Prospects

-202468101214

0

50

100

150

200

250

Asia Pacific Eastern Europe

Latin America Middle East Africa

North America

Western Europe

% g

row

th

US

$

Per Capita Expenditure by Region

Per capita CT spend (2008, US$)

% Change in CT Spend 2007-08

% CAGR in CT spend 2008-13

Note: 2007-08 % change figures are in current prices, whereas projected CAGRs are in real prices that exclude inflation. Eastern Europe, Latin

America and Middle East Africa's 2007-08 % change figures contain significant inflation.

10

© Euromonitor International >Cosmetics & Toiletries-Prospects

Premium cosmetics grew by 2.2% in 2008 as they bore

the brunt of the effect of falling consumer spending. By

product, most growth was in baby care and sun care.

Three product segments make up a huge 84% of

premium cosmetics: skin care, fragrances, colour

cosmetics. By geography, growth focused on Latin

America and Eastern Europe. Two regions make up

65% of premium cosmetics: Western Europe, Asia. In

Asia, baby care grew 35% in 2008, but from a low

base.

Strikingly, sales already fell meaningfully in every single

product category in the US (incl. sun care) in 2008, and

further significant negative growth is likely in 2009/10.

Going forward, sector growth will be pressurised as

reduced disposable income leads consumers to trade

down to varying degrees. This will affect primarily basic

cosmetic and toiletries products, but will also affect the

premium market. Market leaders Estée Lauder and

L'Oréal will face an increasingly fierce competitive

environment across all premium product categories,

though certain lines should hold up better than others.

This is due to the fact that they are easier to market

and 'glamour' helps to justify a premium positioning:

skin care (even high-priced face creams should benefit

as 'eternal youth' is priceless), and sun care (sun

protection, cancer prevention, premature skin-ageing).

Brand loyalty is generally high in premium cosmetics,

though firm separation from the mass market remains

critical in order to preserve product pricing.

Premiumisation will continue to be an important global

trend over the longer term. Premium brand sales

constituted 22% of the global market in 2008. Key sector

drivers include improved wealth in developed and

emerging economies, a growing middle class in BRIC,

further value-adding product enhancements via R&D,

the launch of new and highly priced products (niche

markets, especially in Western Europe), and increased

availability through select mass channels.

Regional Overview

Premium Cosmetics: Time to Buckle Up

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Premium Cosmetics % Growth by Region 2008

11

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

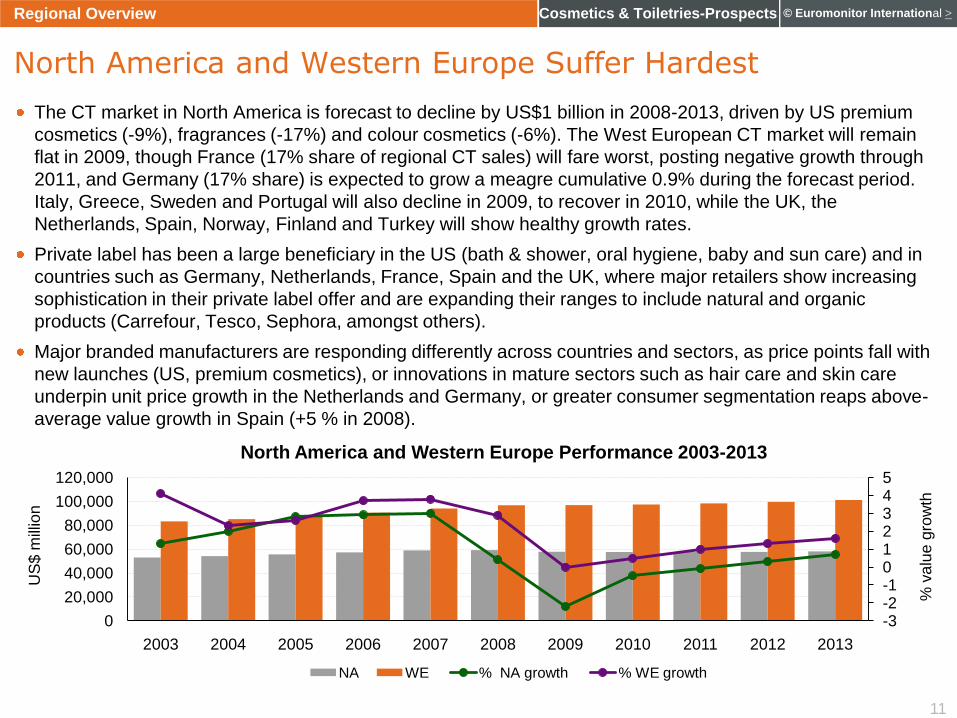

North America and Western Europe Suffer Hardest

The CT market in North America is forecast to decline by US$1 billion in 2008-2013, driven by US premium

cosmetics (-9%), fragrances (-17%) and colour cosmetics (-6%). The West European CT market will remain

flat in 2009, though France (17% share of regional CT sales) will fare worst, posting negative growth through

2011, and Germany (17% share) is expected to grow a meagre cumulative 0.9% during the forecast period.

Italy, Greece, Sweden and Portugal will also decline in 2009, to recover in 2010, while the UK, the

Netherlands, Spain, Norway, Finland and Turkey will show healthy growth rates.

Private label has been a large beneficiary in the US (bath & shower, oral hygiene, baby and sun care) and in

countries such as Germany, Netherlands, France, Spain and the UK, where major retailers show increasing

sophistication in their private label offer and are expanding their ranges to include natural and organic

products (Carrefour, Tesco, Sephora, amongst others).

Major branded manufacturers are responding differently across countries and sectors, as price points fall with

new launches (US, premium cosmetics), or innovations in mature sectors such as hair care and skin care

underpin unit price growth in the Netherlands and Germany, or greater consumer segmentation reaps above-

average value growth in Spain (+5 % in 2008).

-3-2-1012345

0

20,000

40,000

60,000

80,000

100,000

120,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% v

alu

e g

row

th

US

$ m

illio

n

North America and Western Europe Performance 2003-2013

NA WE % NA growth % WE growth

12

© Euromonitor International >Cosmetics & Toiletries-Prospects

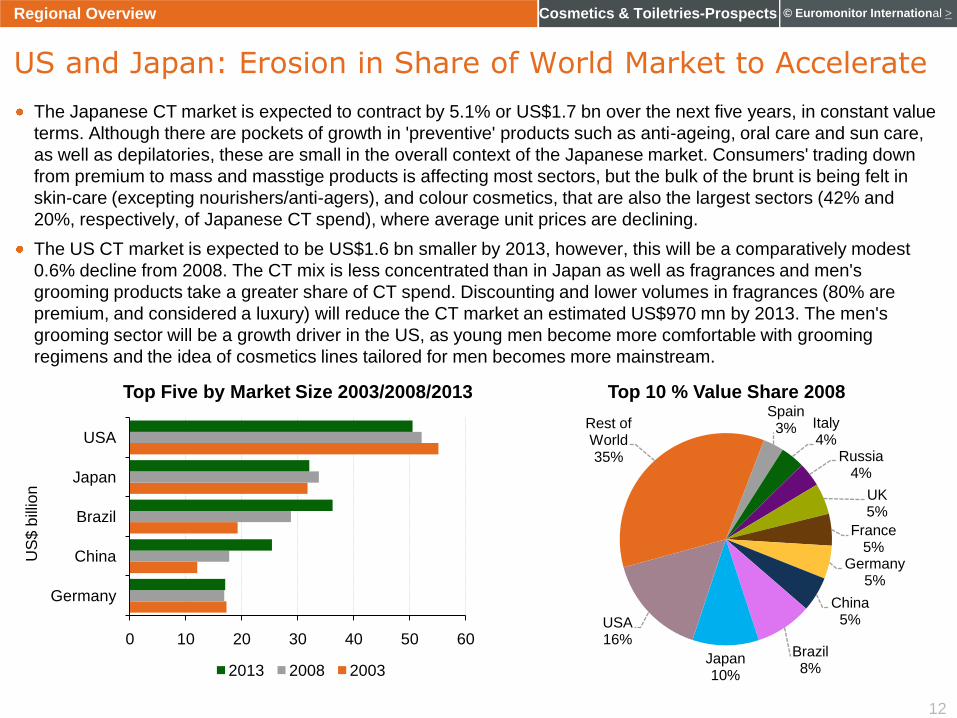

The Japanese CT market is expected to contract by 5.1% or US$1.7 bn over the next five years, in constant value

terms. Although there are pockets of growth in 'preventive' products such as anti-ageing, oral care and sun care,

as well as depilatories, these are small in the overall context of the Japanese market. Consumers' trading down

from premium to mass and masstige products is affecting most sectors, but the bulk of the brunt is being felt in

skin-care (excepting nourishers/anti-agers), and colour cosmetics, that are also the largest sectors (42% and

20%, respectively, of Japanese CT spend), where average unit prices are declining.

The US CT market is expected to be US$1.6 bn smaller by 2013, however, this will be a comparatively modest

0.6% decline from 2008. The CT mix is less concentrated than in Japan as well as fragrances and men's

grooming products take a greater share of CT spend. Discounting and lower volumes in fragrances (80% are

premium, and considered a luxury) will reduce the CT market an estimated US$970 mn by 2013. The men's

grooming sector will be a growth driver in the US, as young men become more comfortable with grooming

regimens and the idea of cosmetics lines tailored for men becomes more mainstream.

Regional Overview

US and Japan: Erosion in Share of World Market to Accelerate

0 10 20 30 40 50 60

Germany

China

Brazil

Japan

USA

US

$ b

illio

n

Top Five by Market Size 2003/2008/2013

2013 2008 2003

Spain3% Italy

4%Russia

4%

UK5%

France5%

Germany5%

China5%

Brazil8%

Japan10%

USA16%

Rest of World35%

Top 10 % Value Share 2008

13

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

A Diverse Environment in Asia Pacific

0

20

40

60

80

100

120

140

160

180

0

1

2

3

4

5

6

7

South Korea Taiwan HK, China Singapore

Pe

r ca

pita

CT

(U

S$

)

Ma

rket siz

e (

US

$ b

illio

n)

Developed Markets 2008

Market Size (US$ bn) Per capita C&T (US$)

In 2009, Asian economies (ex-Japan) will grow their lowest since 2001, nevertheless, above 5%. Public debt

has been reduced (excepting India) and foreign reserves are mostly ample. A more rapid recovery than in

other parts of the world, should thus be possible as governments are better able to cope with recession

through increased spending. The region remains dependent on and vulnerable to foreign investment flows.

Skin care is the key sector taking up 37% of CT spend, and the share is higher in mature markets. Catering to

Asian women's traditional preference for clear and pale skin, majors P&G, Amway, and L'Oréal launched

several new whitening skin care products during 2008. Products with whitening function are penetrating into

nearly every area of facial skin care - moisturisers, cleansers, toners, face masks, and even nourishers/anti-

agers - as manufacturers seek to add extra benefits to basic functionality. Sales will slow sharply but the high

importance of facial skin beauty will continue to make skin care the star performer of the Asia Pacific CT

market (37% of projected five-year absolute growth), followed by hair care (20% of absolute growth).

14

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

China Sees Highest Absolute Growth Potential

0

5

10

15

20

25

30

35

40

45

50

0

2

4

6

8

10

12

14

16

18

20

China India Thailand Philippines Indonesia Malaysia

Pe

r ca

pita

CT

(U

S$

)

Ma

rket siz

e (

US

$ b

illio

n)

Developing Asian Markets 2008

Market Size (US$ bn) Per capita C&T (US$)

Around half of CT purchases in developed Asia Pacific markets (per-capita CT spend above US$120) are

premium products, that will do poorly such as in Japan (US$252 CT per-capita spend) and Taiwan.

In contrast, countries such as China and India, where premium product penetration is low, will see premium

products outperforming mass even in the economic downturn. Broadly speaking, developing countries whose

CT markets are very large yet per capita CT spend remains low, will see the greatest absolute growth.

15

© Euromonitor International >Cosmetics & Toiletries-Prospects

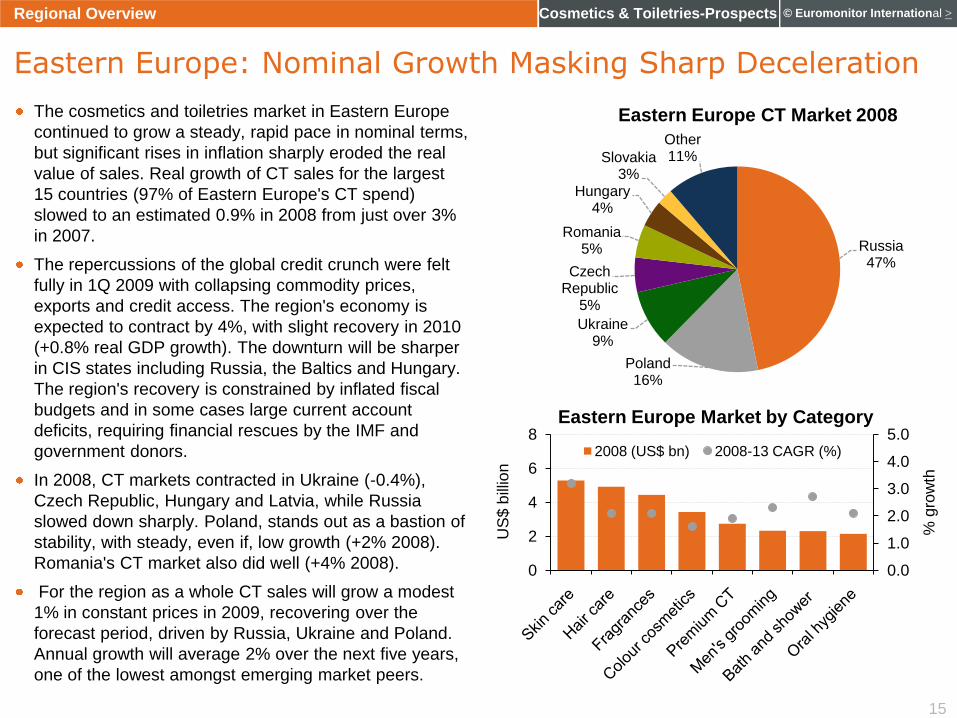

The cosmetics and toiletries market in Eastern Europe

continued to grow a steady, rapid pace in nominal terms,

but significant rises in inflation sharply eroded the real

value of sales. Real growth of CT sales for the largest

15 countries (97% of Eastern Europe's CT spend)

slowed to an estimated 0.9% in 2008 from just over 3%

in 2007.

The repercussions of the global credit crunch were felt

fully in 1Q 2009 with collapsing commodity prices,

exports and credit access. The region's economy is

expected to contract by 4%, with slight recovery in 2010

(+0.8% real GDP growth). The downturn will be sharper

in CIS states including Russia, the Baltics and Hungary.

The region's recovery is constrained by inflated fiscal

budgets and in some cases large current account

deficits, requiring financial rescues by the IMF and

government donors.

In 2008, CT markets contracted in Ukraine (-0.4%),

Czech Republic, Hungary and Latvia, while Russia

slowed down sharply. Poland, stands out as a bastion of

stability, with steady, even if, low growth (+2% 2008).

Romania's CT market also did well (+4% 2008).

For the region as a whole CT sales will grow a modest

1% in constant prices in 2009, recovering over the

forecast period, driven by Russia, Ukraine and Poland.

Annual growth will average 2% over the next five years,

one of the lowest amongst emerging market peers.

Russia47%

Poland16%

Ukraine9%

Czech Republic

5%

Romania5%

Hungary4%

Slovakia3%

Other11%

Eastern Europe CT Market 2008

Regional Overview

Eastern Europe: Nominal Growth Masking Sharp Deceleration

0.0

1.0

2.0

3.0

4.0

5.0

0

2

4

6

8

% g

row

th

US

$ b

illio

n

Eastern Europe Market by Category

2008 (US$ bn) 2008-13 CAGR (%)

16

© Euromonitor International >Cosmetics & Toiletries-Prospects

Skin care20%

Fragrances18%

Hair care17%

Colour cosmetics

14%

Men's grooming

9%

Oral hygiene

9%

Bath & shower

8%

Other5%

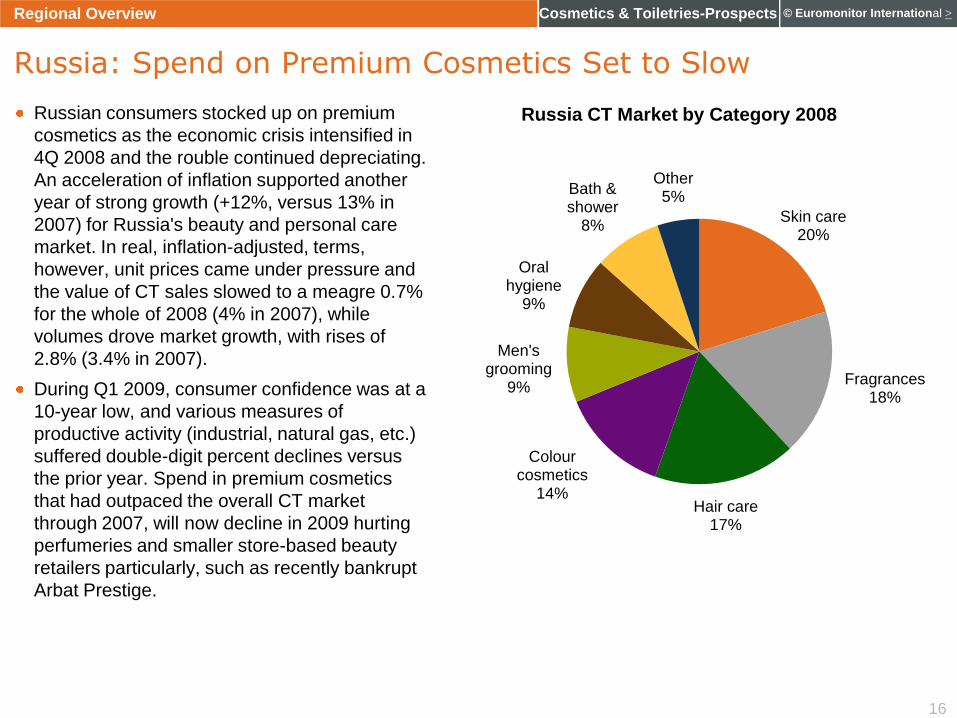

Russia CT Market by Category 2008Russian consumers stocked up on premium

cosmetics as the economic crisis intensified in

4Q 2008 and the rouble continued depreciating.

An acceleration of inflation supported another

year of strong growth (+12%, versus 13% in

2007) for Russia's beauty and personal care

market. In real, inflation-adjusted, terms,

however, unit prices came under pressure and

the value of CT sales slowed to a meagre 0.7%

for the whole of 2008 (4% in 2007), while

volumes drove market growth, with rises of

2.8% (3.4% in 2007).

During Q1 2009, consumer confidence was at a

10-year low, and various measures of

productive activity (industrial, natural gas, etc.)

suffered double-digit percent declines versus

the prior year. Spend in premium cosmetics

that had outpaced the overall CT market

through 2007, will now decline in 2009 hurting

perfumeries and smaller store-based beauty

retailers particularly, such as recently bankrupt

Arbat Prestige.

Regional Overview

Russia: Spend on Premium Cosmetics Set to Slow

17

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

Russia: Direct Sellers Thrive in Recessionary Market

-4

-2

0

2

4

6

8

10

12

0

2

4

6

8

10

12

14

16

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% g

row

th

US

$ b

illio

n

Russia: CT Sales Evolution (Real Prices) 2004-2013

Total CT Premium Total % y-o-y growth Premium % y-o-y growth

With strong long-standing reputations, value-for-money images, and innovative marketing, direct sellers

flourished during 2008. Oriflame saw sales grow by 25% and staff by 50%. Amway saw another year of record

sales, up 32%. Avon launched Bond Girl 007 fragrance to coincide with the Quantum of Solace's movie

premiere, with a curvy, feminine-shaped bottle and high-tech metal top, even distributed at film screenings.

Active TV advertising—highly effective in Russian consumer choice—played a key role for direct sellers. It is

likely that buyers of premium cosmetics will look to direct sellers' masstige product ranges to reduce outlays.

18

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

Japan: Pockets of Growth Overshadowed by General Declines

In Q1 2009, Japan's real GDP contracted by 4% quarter-on-quarter, the fastest decline since the 1974 oil crisis.

Japan's recovery will be slower than in its 1997-98 recession reflecting the more severe global economic downturn

currently, and Japan's reliance on exports to deliver economic growth.

Consumers' move away from premium to mass/masstige is the over-riding trend in Japan. Nourishers/anti-agers, sun

care, men's grooming, oral hygiene and organics should perform better than other sectors.

A distinctive feature of the Japanese market versus its AP developed peers, is the leadership of national champions

(Kao, Shiseido), though foreigners are making inroads with products that target untapped sub-sectors—such as Veet's

hair removers that helped Reckitt Benckiser make a 29% sales gain in depilatories in 2008—or by successfully

adapting top brands to local peculiarities such as L'Oréal (+17% sales gain in 2008) that successfully reformulated

Revitalift to suit the Japanese skin type.

With an ageing population and highly sophisticated Japanese consumer, new scientifically-based age-defying

products with increased efficacy, are the way forward for manufacturers. Segmentation and targeted marketing can

also bear fruit as the case with Shiseido's Elixir Prior that caters to the growing 60+ female group, with packaging for

easy handling, large labelling and easy-to-follow steps.

-3

-2

-1

0

1

2

3

4

0

2

4

6

8

10

12

14

16

Hair care Colour cosmetics

Men's grooming

Oral hygiene Skin care Anti-agers Premium CT

% g

row

th

US

$ b

illio

n

Japan CT Market by Category

2008

2013

% CAGR 2003-08

% CAGR 2008-13

19

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

China and India Growth Engines of Asia Pacific

China's booming skin care market grew an average 18% pa over the review period, yet per capita spend on

skin care was a low US$5 in 2008 versus Taiwan's US$63 and HK China's US$76. The top five players,

foreign, had combined market share of 50%, and fueled value growth with diverse marketing campaigns and

introductions of high potency anti-ageing products, as well as through greater segmentation of the 25-to-35s.

Brands grounded in local traditions are capturing market dynamism: Shanghai Jahwa's new Herborist range of

TCM-based skin care products saw 67% growth in 2008. Three of the top five brands are from direct sellers

that gained share in 2008 as the economic slowdown increased jobless women-turned-direct sellers.

As wealth and infrastructure investment gradually reaches the highly rural Indian population, and incomes rise

in urban areas, much of the absolute growth in the Indian CT market has come from sectors that represent

basic necessities (bath & shower, hair care and oral hygiene) where consumers are switching from loose,

unbranded products to branded goods. The most dynamic sectors in the forecast period are forecast to be

fragrances (+17% CAGR) and colour cosmetics (+20% CAGR) as more young women join the work force.

China and India will account for 66% and 22%, respectively, of Asia Pacific's absolute value sales growth

between 2008 and 2013, thanks to projected CAGRs above 7%. Thailand, however, with similar consumption

patterns to China, will also be an important generator of CT absolute market growth (+US$820 mn).

0

10

20

30

40

China India Thailand Philippines Indonesia Malaysia

% s

ha

re

Category Share of Total CT Market 2008

Bath & shower Hair care Colour cosmetics Oral hygiene Skin care Premium CT

20

© Euromonitor International >Cosmetics & Toiletries-Prospects

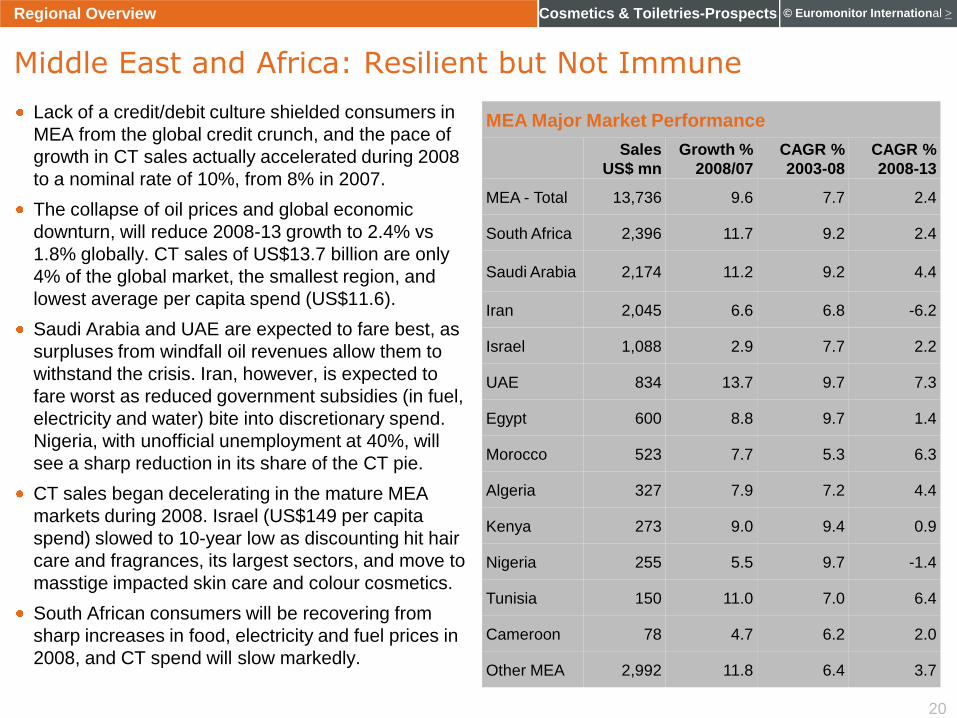

Lack of a credit/debit culture shielded consumers in

MEA from the global credit crunch, and the pace of

growth in CT sales actually accelerated during 2008

to a nominal rate of 10%, from 8% in 2007.

The collapse of oil prices and global economic

downturn, will reduce 2008-13 growth to 2.4% vs

1.8% globally. CT sales of US$13.7 billion are only

4% of the global market, the smallest region, and

lowest average per capita spend (US$11.6).

Saudi Arabia and UAE are expected to fare best, as

surpluses from windfall oil revenues allow them to

withstand the crisis. Iran, however, is expected to

fare worst as reduced government subsidies (in fuel,

electricity and water) bite into discretionary spend.

Nigeria, with unofficial unemployment at 40%, will

see a sharp reduction in its share of the CT pie.

CT sales began decelerating in the mature MEA

markets during 2008. Israel (US$149 per capita

spend) slowed to 10-year low as discounting hit hair

care and fragrances, its largest sectors, and move to

masstige impacted skin care and colour cosmetics.

South African consumers will be recovering from

sharp increases in food, electricity and fuel prices in

2008, and CT spend will slow markedly.

MEA Major Market Performance

Sales

US$ mn

Growth %

2008/07

CAGR %

2003-08

CAGR %

2008-13

MEA - Total 13,736 9.6 7.7 2.4

South Africa 2,396 11.7 9.2 2.4

Saudi Arabia 2,174 11.2 9.2 4.4

Iran 2,045 6.6 6.8 -6.2

Israel 1,088 2.9 7.7 2.2

UAE 834 13.7 9.7 7.3

Egypt 600 8.8 9.7 1.4

Morocco 523 7.7 5.3 6.3

Algeria 327 7.9 7.2 4.4

Kenya 273 9.0 9.4 0.9

Nigeria 255 5.5 9.7 -1.4

Tunisia 150 11.0 7.0 6.4

Cameroon 78 4.7 6.2 2.0

Other MEA 2,992 11.8 6.4 3.7

Regional Overview

Middle East and Africa: Resilient but Not Immune

21

© Euromonitor International >Cosmetics & Toiletries-Prospects

Fragrances (66% of which premium) was the most dynamic sector in MEA during 2003-08, accounting for

20% of the absolute increase in sales. The region benefits from a deeply-rooted fragrance culture that favours

premium and oriental products. Fragrances will be the largest contributor to regional sales growth during

2008-2013, followed by skin care (23% premium) and colour cosmetics (35% premium). Given tougher

economic climate, well-positioned and advertised masstige products show significant potential.

Iran's stellar growth of 76% in colour cosmetics in 2003-2008 masks a mixed reality of high inflation and poor

border control. Smuggled and counterfeits account for 80% of the CT market. Rapid expansion of satellite TV

and outreach to small cities has brought Farsi channel advertising to Iran's growing youthful population,

spurring CT purchases. Colour cosmetics will continue to drive positive CT sales growth in current prices.

As the UAE struggles with oil price and property market collapses, it will see 7% average forecast growth

underpinned by high per capita income, a cosmopolitan population with over 60% under 25, and an expanding

retail landscape. Hair care is the largest and most dynamic sector, with climate and ethnic factors supporting

strong growth (+12% 08/13 CAGR) across most products.

Regional Overview

Middle East and Africa: A Region With Diverse Markets

Baby care

Bath and shower products

DeodorantsDepilatories

Hair careMen's

grooming products

Colour cosmetics

Fragrances

Skin care

Oral hygiene

Sun care

0%

2%

4%

6%

8%

10%

12%

-1% 0% 1% 2% 3% 4% 5%

CA

GR

% 2

00

3-0

8, cu

rre

nt,

U

S$

bill

ion

CAGR % 2008-2013, constant, US$ billion

CT MEA Growth by Category

Bubble size shows sector's share of cosmetics & toiletries market, ranged displayed: 1.20-19.3%

22

© Euromonitor International >Cosmetics & Toiletries-ProspectsRegional Overview

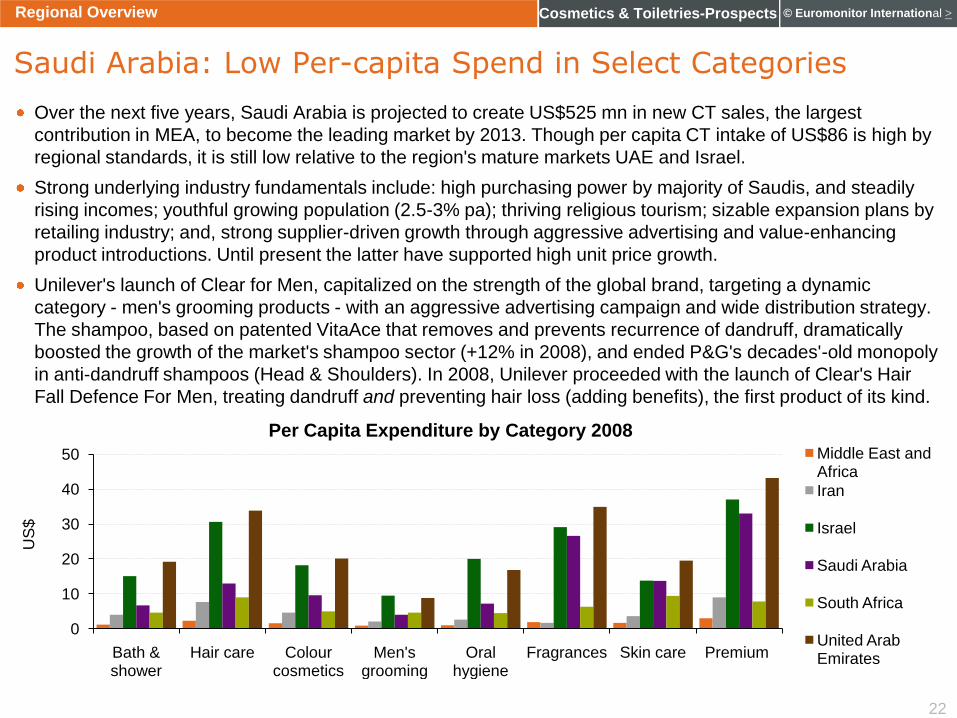

Saudi Arabia: Low Per-capita Spend in Select Categories

Over the next five years, Saudi Arabia is projected to create US$525 mn in new CT sales, the largest

contribution in MEA, to become the leading market by 2013. Though per capita CT intake of US$86 is high by

regional standards, it is still low relative to the region's mature markets UAE and Israel.

Strong underlying industry fundamentals include: high purchasing power by majority of Saudis, and steadily

rising incomes; youthful growing population (2.5-3% pa); thriving religious tourism; sizable expansion plans by

retailing industry; and, strong supplier-driven growth through aggressive advertising and value-enhancing

product introductions. Until present the latter have supported high unit price growth.

Unilever's launch of Clear for Men, capitalized on the strength of the global brand, targeting a dynamic

category - men's grooming products - with an aggressive advertising campaign and wide distribution strategy.

The shampoo, based on patented VitaAce that removes and prevents recurrence of dandruff, dramatically

boosted the growth of the market's shampoo sector (+12% in 2008), and ended P&G's decades'-old monopoly

in anti-dandruff shampoos (Head & Shoulders). In 2008, Unilever proceeded with the launch of Clear's Hair

Fall Defence For Men, treating dandruff and preventing hair loss (adding benefits), the first product of its kind.

0

10

20

30

40

50

Bath & shower

Hair care Colour cosmetics

Men's grooming

Oral hygiene

Fragrances Skin care Premium

US

$

Per Capita Expenditure by Category 2008

Middle East and Africa

Iran

Israel

Saudi Arabia

South Africa

United Arab Emirates

23

© Euromonitor International >Cosmetics & Toiletries-Prospects

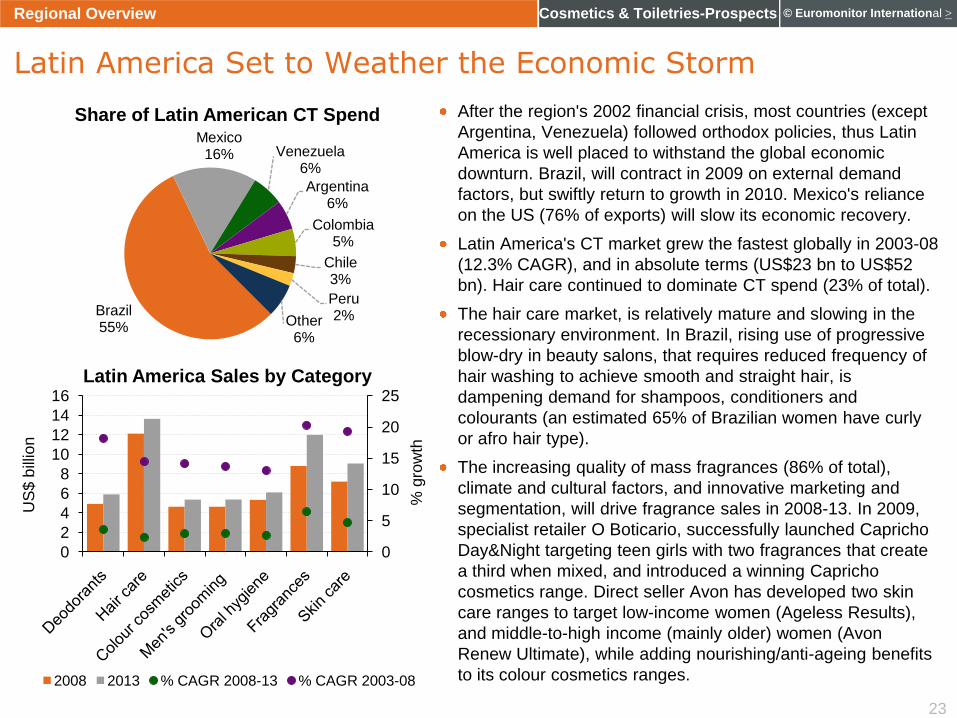

After the region's 2002 financial crisis, most countries (except

Argentina, Venezuela) followed orthodox policies, thus Latin

America is well placed to withstand the global economic

downturn. Brazil, will contract in 2009 on external demand

factors, but swiftly return to growth in 2010. Mexico's reliance

on the US (76% of exports) will slow its economic recovery.

Latin America's CT market grew the fastest globally in 2003-08

(12.3% CAGR), and in absolute terms (US$23 bn to US$52

bn). Hair care continued to dominate CT spend (23% of total).

The hair care market, is relatively mature and slowing in the

recessionary environment. In Brazil, rising use of progressive

blow-dry in beauty salons, that requires reduced frequency of

hair washing to achieve smooth and straight hair, is

dampening demand for shampoos, conditioners and

colourants (an estimated 65% of Brazilian women have curly

or afro hair type).

The increasing quality of mass fragrances (86% of total),

climate and cultural factors, and innovative marketing and

segmentation, will drive fragrance sales in 2008-13. In 2009,

specialist retailer O Boticario, successfully launched Capricho

Day&Night targeting teen girls with two fragrances that create

a third when mixed, and introduced a winning Capricho

cosmetics range. Direct seller Avon has developed two skin

care ranges to target low-income women (Ageless Results),

and middle-to-high income (mainly older) women (Avon

Renew Ultimate), while adding nourishing/anti-ageing benefits

to its colour cosmetics ranges.

Regional Overview

Latin America Set to Weather the Economic Storm

Brazil55%

Mexico16% Venezuela

6%

Argentina6%

Colombia5%

Chile3%

Peru2%Other

6%

Share of Latin American CT Spend

0

5

10

15

20

25

0

2

4

6

8

10

12

14

16

% g

row

th

US

$ b

illio

n

Latin America Sales by Category

2008 2013 % CAGR 2008-13 % CAGR 2003-08

24

© Euromonitor International >Cosmetics & Toiletries-Prospects

Global Snapshot

Regional Overview

Category Review

Channel Analysis

Competitive Environment

Global Prospects

Appendix

25

© Euromonitor International >Cosmetics & Toiletries-Prospects

Consumers are far more willing to economise on toiletries than they are on cosmetics such as skin care and colour

cosmetics, however, in mature markets, the slowdown in toiletries' consumption has been moderate, and less intense

than that seen in value sales of cosmetics. Globally, cosmetics sectors outgrew their toiletries counterparts in 2008, as

they did throughout the review period 2003-08 across all regions. In 2008, however, there was a notable major

exception: Japan's cosmetics market took a sudden sharp turn, and both skin care and colour cosmetics spend

declined sharply. As Japan accounts for 51% of the Asian Pacific cosmetics sector, that region's overall toiletries

market outperformed that of cosmetics (5.2% vs. 3.8%). This is likely to continue as Japanese consumers are

expected to restrain their consumption of skin care and colour cosmetics products and continue switching down from

premium to mass and masstige alternatives.

World spending on fragrances accelerated over the past five years, outpacing both toiletries and cosmetics in 2007

and in 2008, but consumer spending patterns varied across regions. Latin America, Eastern Europe, and Middle East

Africa (a combined 40% of global spending on fragrances) saw double-digit growth in both mass and premium

products. Mass fragrances in Latin America (20% of the global fragrances market) rose by nearly 15% in 2008. At the

other end, North America (16% of world fragrance sales) saw a 4% decline, that region's worst performing sector due

to record discounting across both mass and premium fragrances.

Category Review

Cosmetics Surpass Toiletries, Fragrances Post Varied Results

0% 25% 50% 75% 100%

Fragrances

Cosmetics

Toiletries

Regional Shares of Major Category Groups 2008

AP AU EE LA MEA NA WE

-202468

10121416

World AP AU EE LA MEA NA WE

% C

AG

R

Regional 2003-08 CAGR (%)

Toiletries Cosmetics Fragrances

26

© Euromonitor International >Cosmetics & Toiletries-Prospects

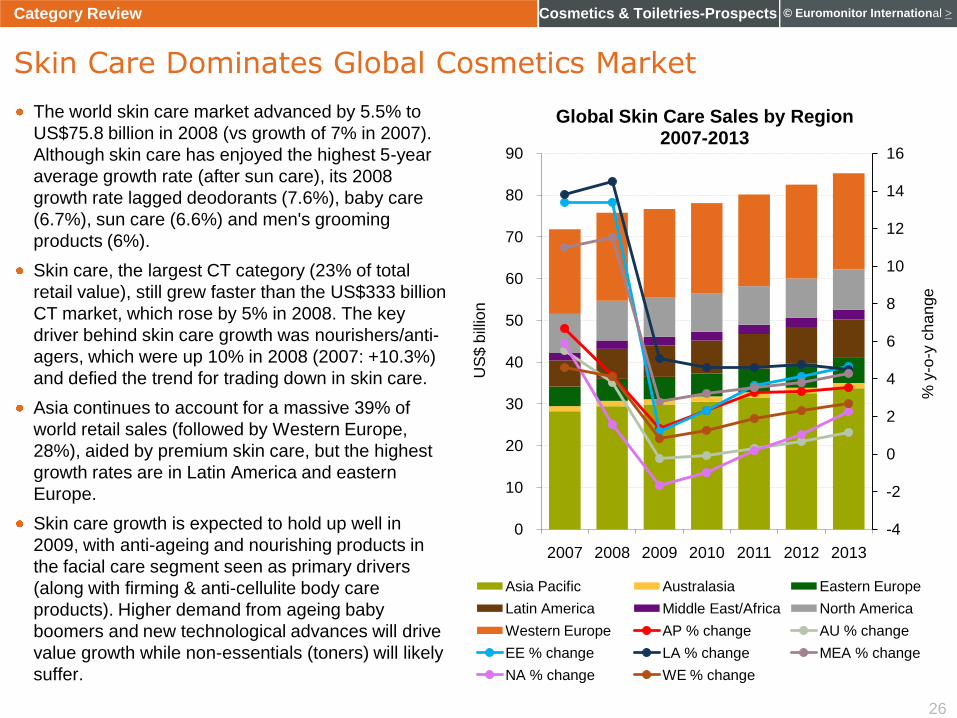

The world skin care market advanced by 5.5% to

US$75.8 billion in 2008 (vs growth of 7% in 2007).

Although skin care has enjoyed the highest 5-year

average growth rate (after sun care), its 2008

growth rate lagged deodorants (7.6%), baby care

(6.7%), sun care (6.6%) and men's grooming

products (6%).

Skin care, the largest CT category (23% of total

retail value), still grew faster than the US$333 billion

CT market, which rose by 5% in 2008. The key

driver behind skin care growth was nourishers/anti-

agers, which were up 10% in 2008 (2007: +10.3%)

and defied the trend for trading down in skin care.

Asia continues to account for a massive 39% of

world retail sales (followed by Western Europe,

28%), aided by premium skin care, but the highest

growth rates are in Latin America and eastern

Europe.

Skin care growth is expected to hold up well in

2009, with anti-ageing and nourishing products in

the facial care segment seen as primary drivers

(along with firming & anti-cellulite body care

products). Higher demand from ageing baby

boomers and new technological advances will drive

value growth while non-essentials (toners) will likely

suffer.

Category Review

Skin Care Dominates Global Cosmetics Market

-4

-2

0

2

4

6

8

10

12

14

16

0

10

20

30

40

50

60

70

80

90

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

US

$ b

illio

n

Global Skin Care Sales by Region 2007-2013

Asia Pacific Australasia Eastern Europe

Latin America Middle East/Africa North America

Western Europe AP % change AU % change

EE % change LA % change MEA % change

NA % change WE % change

27

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Skin Care: Anti-agers Surpass Other Category Performance

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% y

-o-y

va

lue

gro

wth

Skin Care Growth by Category 2004-2013

Skin care Facial care Nourishers/anti-agers Body care Hand care

Anti-ageing products continue to become increasingly specialised and segmented by age group, gender,

combination products, as well as targeting different parts of the body – eye, neck, face, chest, the whole body.

L'Oréal for example has developed different anti-ageing products for each generation of women, and its

website advises on which product to choose for their age group.

Nourishers/anti-agers will be the growth stars of skin care as consumers clearly prioritise age prevention. To

succeed, manufacturers will need to bring to bare technological advances and innovative marketing to tap into

consumer interest in scientifically-proven age prevention methods, together with holistic approaches to beauty

that stress inner health and wellbeing and the use of natural ingredients.

Turning masstige items into affordable luxuries in a tough economic climate characterized recent new

products by Beisdorf and Procter and Gamble. Age-defying cosmeceuticals with high-tech formulations at

affordable prices were: 1) Beiersdorf's Nivea Expert Lift, which comes in a novel and more mature purple

colour packaging, is formulated with Bioxilift ingredients, shown to increase the connective activity of collagen;

and 2) Procter & Gamble‟s Olay Regenerist promises 'dramatic results without drastic measures'.

28

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Skin Care: Merger Between "Inner Beauty" and Science

Some scepticism remains over the efficacy of both cosmeceuticals and nutricosmetics, however supplements

alongside topical products (such as Nivea GoodBye Cellulite) are gaining appeal. Ferrosan's orally taken

Imedeen supplement that is patented with biomarine complex to optimise skin health, has clearly succeeded

in Western Europe. Q10 is both popular as a supplement and contained in skin care products. Natural

ingredients of sea kelp and red ginseng for example are being added to some premium cosmetic brands.

Given tighter consumer purses, it is likely the threshold for success of cosmeceuticals will be raised, and only

products that deliver the promised benefits will succeed. Cosmeceuticals contain biologically active

ingredients such as retinoids and hydroxy acids, or have trans-dermal properties that for example infuse

collagen into the skin, or use nanotechnology. Cosmetic-savvy women that recognise these scientific

properties have driven demand, despite some uncertainty as to their benefits, but they are increasingly

sophisticated and broadly speaking all consumers are more discerning and informed.

USA, 53%

Russia, 2%

Norway, 2%

South Korea, 2%

Japan, 34%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0 100 200 300 400 500

CA

GR

20

08

-20

13

Size 2008 (US$ million)

Top Five Co-enzyme Q10 Countries

Bubble size shows country share of the global CoQ10 sales in 2008

29

© Euromonitor International >Cosmetics & Toiletries-Prospects

Depilatories, the smallest category in the CT sector,

grew by 5% to US$3.8 billion in 2008 (Western

Europe 39%, North America 33%). Women's razors

and blades is the biggest market, constituting 53%

of sector sales.

The strongest growth impulse was seen in women's

razors & blades, where there was buoyant demand

growth across all regions (especially Middle East

and Africa), followed by hair removers/bleaches,

where growth was firmly propelled by Latin America

and Eastern Europe, which showed very strong

growth across all product segments.

In Latin America, growth was driven by Brazil, which

expanded by 13%. Extensive advertising campaigns

and improved product positioning on shelves

stimulated hair removers sales. Hair removers

/bleaches posted robust value growth of 24% in

2008. Procter & Gamble remains market leader with

48% market share, though this slipped 100 bp, while

Church & Dwight strengthened its #2 position after

gaining 220 bp to 17.5% after investing in hair

removers products. Latin America is expected to

show the strongest regional growth pace in 2009-13,

driven by Brazil, and especially in the hair

removers/bleaches category.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Depilatories by Category and Region 2008

Western Europe

North America

Middle East and Africa

Latin America

Eastern Europe

Australasia

Asia Pacific

Category Review

Depilatories Dominated by Razors and Blades

30

© Euromonitor International >Cosmetics & Toiletries-Prospects

In Russia, sales grew 16% in value terms in 2008

(48% of Eastern Europe sales), with pre-shave

growing fastest (21%). Key drivers are a vastly

(supermarkets, pharmacies), growing advertising

under-developed market, expanding retail

infrastructure and consumer education on the

benefits of using depilatories, and rising

popularity of electrical epilators. Russian growth

rates will likely diminish – and Procter & Gamble's

47% market share feel pressure -- going forward

given a challenging economy, new competitors

entering the market and a growing number of

clinics and salons offering laser treatment. Note

that the bulk of annual sales occur during 3-4

months of the year.

Category Review

Depilatories: Buoyant Growth in Russia

-5

5

15

25

35

45

2004 2005 2006 2007 2008 2009

% g

row

th

Depilatories Performance 2004-2009

World Eastern Europe Russia

-5

5

15

25

35

45

2004 2005 2006 2007 2008

% g

row

th

Russia Depilatories by Category 2004-2008

Depilatories Pre-shave

Razors and blades Hair removers/bleaches

31

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

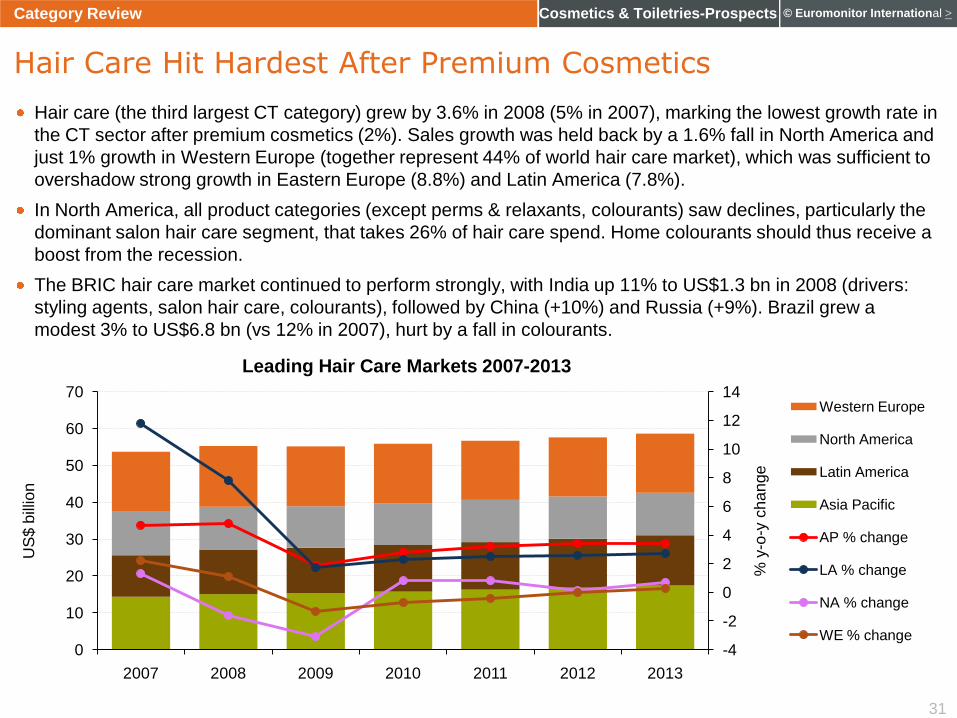

Hair Care Hit Hardest After Premium Cosmetics

Hair care (the third largest CT category) grew by 3.6% in 2008 (5% in 2007), marking the lowest growth rate in

the CT sector after premium cosmetics (2%). Sales growth was held back by a 1.6% fall in North America and

just 1% growth in Western Europe (together represent 44% of world hair care market), which was sufficient to

overshadow strong growth in Eastern Europe (8.8%) and Latin America (7.8%).

In North America, all product categories (except perms & relaxants, colourants) saw declines, particularly the

dominant salon hair care segment, that takes 26% of hair care spend. Home colourants should thus receive a

boost from the recession.

The BRIC hair care market continued to perform strongly, with India up 11% to US$1.3 bn in 2008 (drivers:

styling agents, salon hair care, colourants), followed by China (+10%) and Russia (+9%). Brazil grew a

modest 3% to US$6.8 bn (vs 12% in 2007), hurt by a fall in colourants.

-4

-2

0

2

4

6

8

10

12

14

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

US

$ b

illio

n

Leading Hair Care Markets 2007-2013

Western Europe

North America

Latin America

Asia Pacific

AP % change

LA % change

NA % change

WE % change

32

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Further Innovation to Sustain Growth Levels

Hair care sales are expected to cool further in 2009 driven by discounting, promotions and weak demand in

the US as consumers trade down from premium-priced salon hair care products to cheaper brands and private

label products.

Better insulated segments include naturally positioned hair care products, while added benefits such as anti-

ageing, doctor brands or UV protection may help maintain average unit prices.

-10

-8

-6

-4

-2

0

2

4

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

US Hair Care Market by Value (Real Prices) 2007-2013

Shampoo 2-in-1 products Conditioners Styling agents

Perms and relaxants Colourants Salon hair care US hair care market

33

© Euromonitor International >Cosmetics & Toiletries-Prospects

Oral hygiene is amongst the most commoditised

segments of the CT market. Segmentation,

consumer education and rapid product development

are supporting the global oral care market in the

short term, but price pressure, mass market

imitators and a lack of room for innovation are

making market development ever more exhausting

for producers.

The key to sustained growth will be consumer

education. This could drive consumption of floss and

mouthwashes, for example, but private label and

new entrants will present stiff competition.

In toothpaste, there is still significant room for further

development of natural ingredients and organics.

Category Review

Oral Hygiene: Multinationals Well Placed in Growth Markets

Oral hygiene grew by 4 % to US$34 billion in 2008 (vs 5.5% in 2007), consistently growing slightly slower than the

cosmetics and toiletries market over the past five years. Toothpaste rose by 4% to US$17 billion, now

representing a massive 51% of the oral hygiene market. The most dynamic segment with the fastest growth for a

third consecutive year was mouthwashes/dental rinses, expanding by 7% to US$3.5 billion (vs 10.5% in 2007)

and growing across all regions (low world consumption rates of such products and growing professional

recommendations for increased oral hygiene continues to unlock new growth potential, especially in Latin America

and Europe). In contrast, despite a bounce in 2007, tooth whiteners fell by 3% (competition from whitening

toothpaste) while mouth fresheners fell by 4 %, marking a fifth year of market decline.

Manual toothbrush sales accounted for 69% of segment sales and expanded by 4% whereas power toothbrushes

grew by 5.3%. Overall, the US$9.3 billion toothbrush market grew by 4.6% in 2008, and there was positive growth

across all regions. Western Europe kept its market share leadership with sales up by 3.5% to US$2.6 billion,

followed by Asia Pacific where sales came to US$2.2 billion (+3.9% in 2008).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2013

Oral Care by Category 2003/2013

Toothbrushes

Tooth whiteners

Dental floss

Mouth fresheners

Denture care

Mouthwashes/dental rinses

Toothpaste

34

© Euromonitor International >Cosmetics & Toiletries-Prospects

Colour cosmetics, worth US$43.5 billion,

slowed their growth to 4.4% in 2008 (vs. 5.8%

in 2007). A growth thrust from Latin America

(10.9%) and Eastern Europe (10.1%) was

offset by weak sales of just 1.1% in North

America (lip products, facial make-up) and

2.7% in Asia (mainly facial make-up).

Emerging markets mostly maintained their

rapid pace of expansion, substantially better

than developed regions. Latin America saw

double-digit growth in all sub-sectors except

nail products (-2.8%). China (+12%) and

India (+29% from low base) saw the highest

growth amongst BRIC countries. Brazil

remained the largest BRIC market with a

value of US$2.2 bn, however saw lower

though respectable growth of 9.4% in 2008.

The long-held 'lipstick effect' theory is not

holding up quite as well as in past recessions,

with both high-end and mass products being

affected. Colour cosmetics will grow below

the overall CT market; Asia Pacific (mainly

China) and West Europe will produce the bulk

of absolute growth and Latin America will

come in a close third value creation.

Category Review

Colour Cosmetics: Strong Growth Dynamics in India and China

-4

-2

0

2

4

6

8

10

12

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

US

$ b

illio

n

Global Colour Cosmetics by Region 2007-2013

Asia Pacific Eastern EuropeLatin America Middle East and AfricaNorth America Western EuropeAP % change EE % changeLA % change MEA % changeNA % change WE % change

35

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Colour Cosmetics: Product Innovation Critical

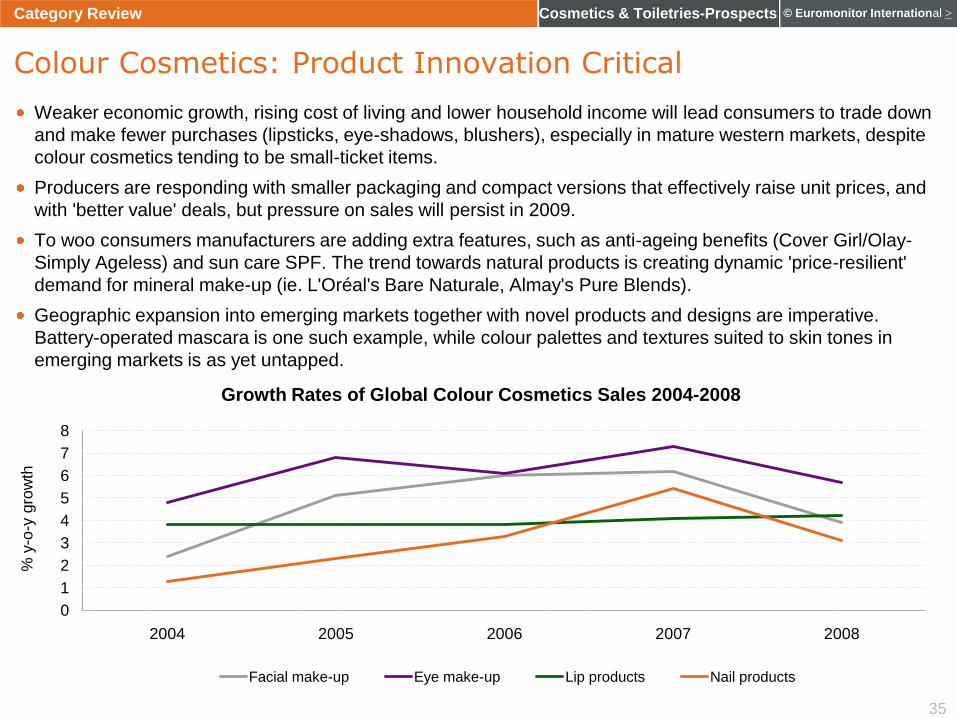

Weaker economic growth, rising cost of living and lower household income will lead consumers to trade down

and make fewer purchases (lipsticks, eye-shadows, blushers), especially in mature western markets, despite

colour cosmetics tending to be small-ticket items.

Producers are responding with smaller packaging and compact versions that effectively raise unit prices, and

with 'better value' deals, but pressure on sales will persist in 2009.

To woo consumers manufacturers are adding extra features, such as anti-ageing benefits (Cover Girl/Olay-

Simply Ageless) and sun care SPF. The trend towards natural products is creating dynamic 'price-resilient'

demand for mineral make-up (ie. L'Oréal's Bare Naturale, Almay's Pure Blends).

Geographic expansion into emerging markets together with novel products and designs are imperative.

Battery-operated mascara is one such example, while colour palettes and textures suited to skin tones in

emerging markets is as yet untapped.

0

1

2

3

4

5

6

7

8

2004 2005 2006 2007 2008

% y

-o-y

gro

wth

Growth Rates of Global Colour Cosmetics Sales 2004-2008

Facial make-up Eye make-up Lip products Nail products

36

© Euromonitor International >Cosmetics & Toiletries-Prospects

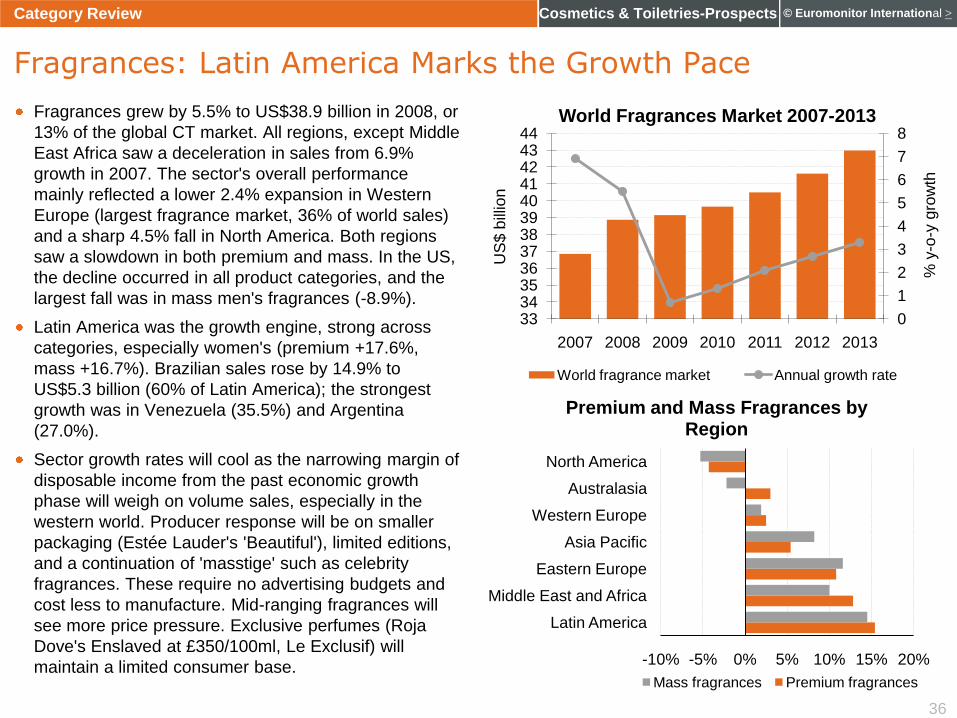

Fragrances grew by 5.5% to US$38.9 billion in 2008, or

13% of the global CT market. All regions, except Middle

East Africa saw a deceleration in sales from 6.9%

growth in 2007. The sector's overall performance

mainly reflected a lower 2.4% expansion in Western

Europe (largest fragrance market, 36% of world sales)

and a sharp 4.5% fall in North America. Both regions

saw a slowdown in both premium and mass. In the US,

the decline occurred in all product categories, and the

largest fall was in mass men's fragrances (-8.9%).

Latin America was the growth engine, strong across

categories, especially women's (premium +17.6%,

mass +16.7%). Brazilian sales rose by 14.9% to

US$5.3 billion (60% of Latin America); the strongest

growth was in Venezuela (35.5%) and Argentina

(27.0%).

Sector growth rates will cool as the narrowing margin of

disposable income from the past economic growth

phase will weigh on volume sales, especially in the

western world. Producer response will be on smaller

packaging (Estée Lauder's 'Beautiful'), limited editions,

and a continuation of 'masstige' such as celebrity

fragrances. These require no advertising budgets and

cost less to manufacture. Mid-ranging fragrances will

see more price pressure. Exclusive perfumes (Roja

Dove's Enslaved at £350/100ml, Le Exclusif) will

maintain a limited consumer base.

Fragrances: Latin America Marks the Growth Pace

-10% -5% 0% 5% 10% 15% 20%

Latin America

Middle East and Africa

Eastern Europe

Asia Pacific

Western Europe

Australasia

North America

Premium and Mass Fragrances by Region

Mass fragrances Premium fragrances

Category Review

0

1

2

3

4

5

6

7

8

333435363738394041424344

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

gro

wth

US

$ b

illio

n

World Fragrances Market 2007-2013

World fragrance market Annual growth rate

37

© Euromonitor International >Cosmetics & Toiletries-Prospects

In 2008, the global bath & shower products market grew by

5% as consumers were more willing to trade up for basic

hygiene products. Bar soap is the single most valuable

product, with sales of US$11.8 billion (41% of sector value),

followed by body wash/shower gel (32%.)

Bar soap grew by 7% and was the fastest growing category

given rising disposable income in emerging markets and

despite falling sales in Western Europe (fifth year in a row).

Liquid soap was second fastest and rose by 6% (11% of bath

& shower sales), aided by bubble gel in individual capsules

and gel in sachets.

Asia is the largest market in value terms with a 27% share

(US$7.7 bn). The highest growth was in shower gel and liquid

soap. Latin America and Eastern Europe grew double-digit

and faster than the global average.

Latin American middle and high-income consumers traded up

to more sophisticated products, causing a sharp growth rate

of 14% in 2008. Shower gel is seeing strong growth as the

category is still very small. A trend to shower more often and

with more value-added features (eg. moisturising, anti-

bacterial properties) are the two main factors that buoyed

sales of bar soap.

Bath & shower sales are to grow on average 1.5% over

2009-13. Firmly rising growth rates in China/India stand in

sharp contrast to mature Japan, and Asia could further

expand its share of global bath & shower spend to 28% by

2013.

Category Review

Bath & Shower Products: Emerging Regions Steer Growth

-4

-2

0

2

4

6

8

02468

101214

% C

AG

R

US

$ b

illio

n

Global Bath & Shower Sales by Category

2008 2003-08 CAGR % 2008-13 CAGR %

Sector Growth: Mature vs Dynamic

DYNAMIC

Bar soap

Liquid soap

Body wash/

shower gel

Latin America

Eastern Europe

MATURE

Bath additives

Talcum powder

North America

Western Europe

38

© Euromonitor International >Cosmetics & Toiletries-Prospects

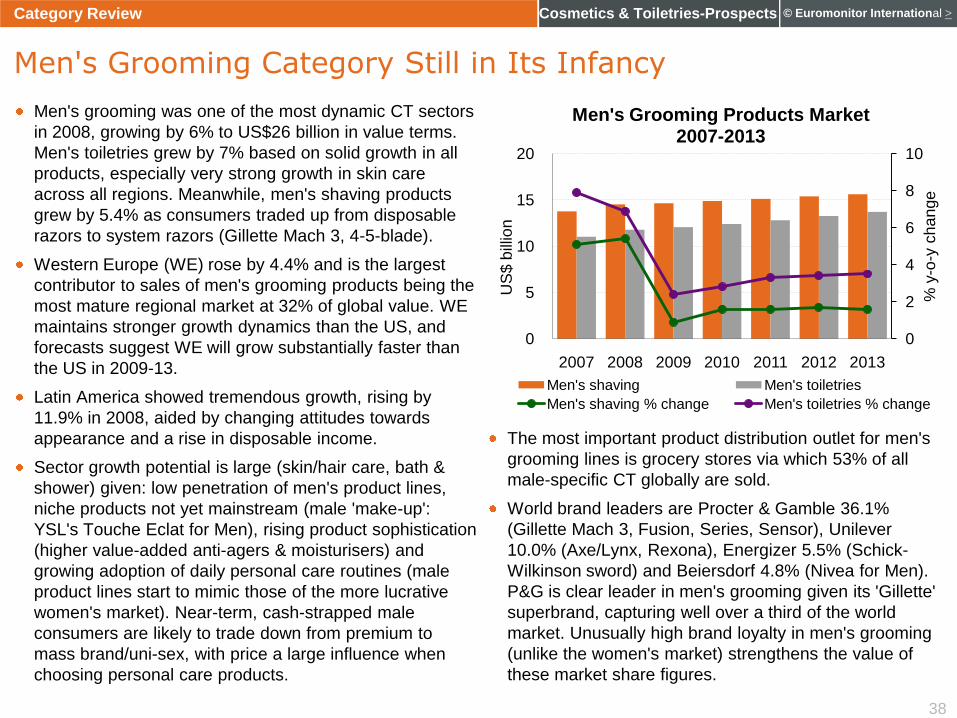

Men's grooming was one of the most dynamic CT sectors

in 2008, growing by 6% to US$26 billion in value terms.

Men's toiletries grew by 7% based on solid growth in all

products, especially very strong growth in skin care

across all regions. Meanwhile, men's shaving products

grew by 5.4% as consumers traded up from disposable

razors to system razors (Gillette Mach 3, 4-5-blade).

Western Europe (WE) rose by 4.4% and is the largest

contributor to sales of men's grooming products being the

most mature regional market at 32% of global value. WE

maintains stronger growth dynamics than the US, and

forecasts suggest WE will grow substantially faster than

the US in 2009-13.

Latin America showed tremendous growth, rising by

11.9% in 2008, aided by changing attitudes towards

appearance and a rise in disposable income.

Sector growth potential is large (skin/hair care, bath &

shower) given: low penetration of men's product lines,

niche products not yet mainstream (male 'make-up':

YSL's Touche Eclat for Men), rising product sophistication

(higher value-added anti-agers & moisturisers) and

growing adoption of daily personal care routines (male

product lines start to mimic those of the more lucrative

women's market). Near-term, cash-strapped male

consumers are likely to trade down from premium to

mass brand/uni-sex, with price a large influence when

choosing personal care products.

The most important product distribution outlet for men's

grooming lines is grocery stores via which 53% of all

male-specific CT globally are sold.

World brand leaders are Procter & Gamble 36.1%

(Gillette Mach 3, Fusion, Series, Sensor), Unilever

10.0% (Axe/Lynx, Rexona), Energizer 5.5% (Schick-

Wilkinson sword) and Beiersdorf 4.8% (Nivea for Men).

P&G is clear leader in men's grooming given its 'Gillette'

superbrand, capturing well over a third of the world

market. Unusually high brand loyalty in men's grooming

(unlike the women's market) strengthens the value of

these market share figures.

Category Review

Men's Grooming Category Still in Its Infancy

0

2

4

6

8

10

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

US

$ b

illio

n

Men's Grooming Products Market 2007-2013

Men's shaving Men's toiletries

Men's shaving % change Men's toiletries % change

39

© Euromonitor International >Cosmetics & Toiletries-Prospects

The global deodorants market grew by 7.6% in

value terms in 2008, despite the economic

slowdown. Much of this industry-beating growth

was due, in large part, to strong growth in sprays

and roll-ons in Latin America (Brazil +18%,

Argentina +28%) and Middle East/Africa (South

Africa, UAE/Saudi Arabia). Latin Americans' liking

of scents makes the region the world's second

largest for deodorants after Western Europe, which

grew by 2.7% aided by manufacturers' value-

adding efforts (enhanced efficacy, 24h/48h

protection, Old Spice Red Zone's anti-bacterial

properties).

Globally, the share of premium vs mass products

remained almost unchanged at 3%.

Sprays sales rose by 9%, driven by consumers in

emerging markets trading up from pumps to sprays

(growth engine Latin America up a massive 35%),

and the gaining popularity of sprays vs pumps and

new products with natural qualities (Natura): aloe,

cucumber, green tea appeal to consumers looking

for more natural, gentle and moisturizing products.

Many consumers with sensitive skin search for

gentle products without added fragrances or

irritants, especially given frequent use of

deodorants. Growth in Western Europe was a more

moderate 4%.

Unilever is undisputed global market leader with 31% share

(brands: Rexona, Axe/Lynx, Dove), and is the #1 player in

Western Europe and Latin America (combined 62% of world

market); the #2 player is Procter & Gamble with 10% market

share.

New product launches ('hair-minimising' formula for Dove:

24h anti-perspirant, skin care benefits, slower rate of under-

arm hair growth) could boost sales for the group, though its

response to price hikes by competitors to offset higher

production costs could challenge market share.

Category Review

Deodorants Fastest Growing in 2008

-5

-4

-3

-2

-1

0

1

2

3

4

0

1

2

3

4

5

6

7

8

Sprays (+9.2%)

Roll-ons (+9.5%)

Sticks (+5.0%)

Pumps (+4.7%)

Creams (+0.0%)

Wipes (+0.1%)

% C

AG

R

US

$ b

illio

n

Global Deodorants by Category

Market Size - US$bn 2008-13 % CAGR

Note: Brackets indicate % y-o-y growth for 2008

40

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Sun Care Maintains Growth Dynamics

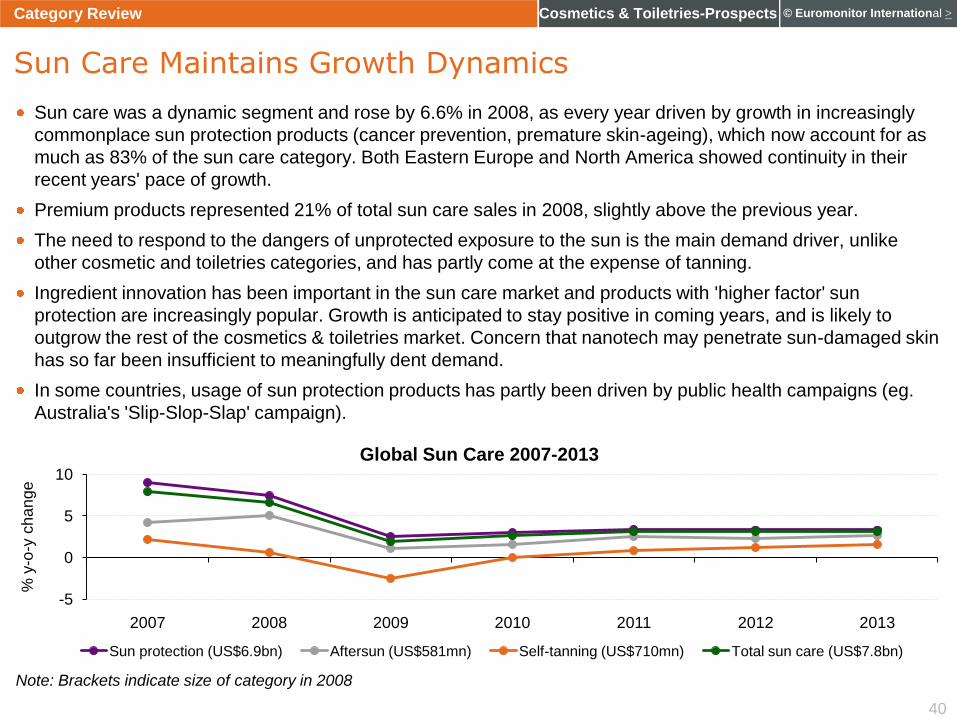

Sun care was a dynamic segment and rose by 6.6% in 2008, as every year driven by growth in increasingly

commonplace sun protection products (cancer prevention, premature skin-ageing), which now account for as

much as 83% of the sun care category. Both Eastern Europe and North America showed continuity in their

recent years' pace of growth.

Premium products represented 21% of total sun care sales in 2008, slightly above the previous year.

The need to respond to the dangers of unprotected exposure to the sun is the main demand driver, unlike

other cosmetic and toiletries categories, and has partly come at the expense of tanning.

Ingredient innovation has been important in the sun care market and products with 'higher factor' sun

protection are increasingly popular. Growth is anticipated to stay positive in coming years, and is likely to

outgrow the rest of the cosmetics & toiletries market. Concern that nanotech may penetrate sun-damaged skin

has so far been insufficient to meaningfully dent demand.

In some countries, usage of sun protection products has partly been driven by public health campaigns (eg.

Australia's 'Slip-Slop-Slap' campaign).

-5

0

5

10

2007 2008 2009 2010 2011 2012 2013

% y

-o-y

ch

an

ge

Global Sun Care 2007-2013

Sun protection (US$6.9bn) Aftersun (US$581mn) Self-tanning (US$710mn) Total sun care (US$7.8bn)

Note: Brackets indicate size of category in 2008

41

© Euromonitor International >Cosmetics & Toiletries-ProspectsCategory Review

Sun Care: Leaders Differ Across Regions

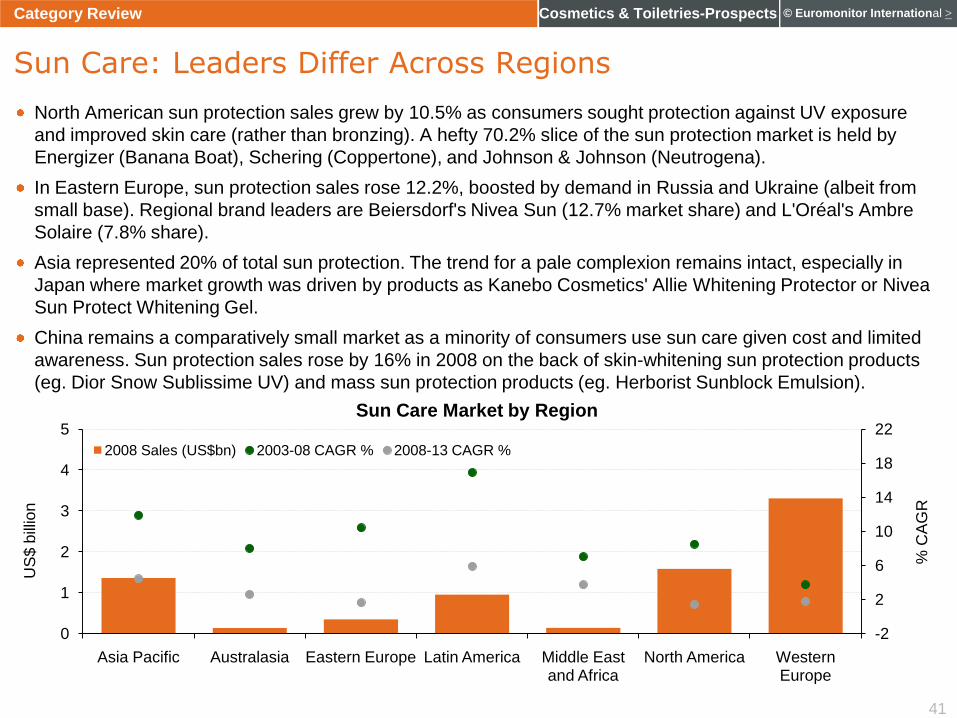

North American sun protection sales grew by 10.5% as consumers sought protection against UV exposure

and improved skin care (rather than bronzing). A hefty 70.2% slice of the sun protection market is held by

Energizer (Banana Boat), Schering (Coppertone), and Johnson & Johnson (Neutrogena).

In Eastern Europe, sun protection sales rose 12.2%, boosted by demand in Russia and Ukraine (albeit from

small base). Regional brand leaders are Beiersdorf's Nivea Sun (12.7% market share) and L'Oréal's Ambre

Solaire (7.8% share).

Asia represented 20% of total sun protection. The trend for a pale complexion remains intact, especially in

Japan where market growth was driven by products as Kanebo Cosmetics' Allie Whitening Protector or Nivea

Sun Protect Whitening Gel.

China remains a comparatively small market as a minority of consumers use sun care given cost and limited

awareness. Sun protection sales rose by 16% in 2008 on the back of skin-whitening sun protection products

(eg. Dior Snow Sublissime UV) and mass sun protection products (eg. Herborist Sunblock Emulsion).

-2

2

6

10

14

18

22

0

1

2

3

4

5

Asia Pacific Australasia Eastern Europe Latin America Middle East and Africa

North America Western Europe

% C

AG

R

US

$ b

illio

n

Sun Care Market by Region

2008 Sales (US$bn) 2003-08 CAGR % 2008-13 CAGR %

42

© Euromonitor International >Cosmetics & Toiletries-Prospects

The baby care market rose by 6.7% in 2008 to

US$6.7 bn or 2% of global CT spend. Sales

withstood economic pressures comparatively well

as parents were generally unwilling to sacrifice

product quality for their children (despite media

cover on potentially dangerous chemicals in baby

products).

Demand growth also benefited from increased

purchases of baby care products for adult

consumption (female consumers trade down to

cheaper baby body care, such as baby lotion).

Premium products represented 5.6% of sector

sales.

The move towards natural and environmentally

friendly products showed resilience in this category.

Baby toiletries remain the largest product type, with

sales of US$2.2 billion (38% of sector value),

followed by baby skin care with 31%. Baby toiletries

and baby hair care were the two fastest growing

products in 2008, rising by 7.3%/6.8% respectively.

Growing competition, especially from local

companies in emerging markets, will increasingly

place pressure on Johnson & Johnson's dominant

market share. This is the case across all BRIC

markets, and strong growth projected for China

suggest increasingly fierce competition from Tianjin

Yumeijing, Henkel and Pigeon Corp going forward.

Category Review

Baby Care: Small but Robust

Baby toiletries

38%

Baby hair care22%

Baby skin care31%

Baby sun care9%

Baby Care by Category 2008

02468101214

0

400

800

1,200

1,600

% C

AG

R

US

$ m

illio

n

Baby Care Market by Region

2008 Sales (US$mn) 2003-08 CAGR % 2008-13 CAGR %

43

© Euromonitor International >Cosmetics & Toiletries-Prospects

Global Snapshot

Regional Overview

Category Review

Channel Analysis

Competitive Environment

Global Prospects

Appendix

44

© Euromonitor International >Cosmetics & Toiletries-ProspectsChannel Analysis

Winners and Losers by Channel Type

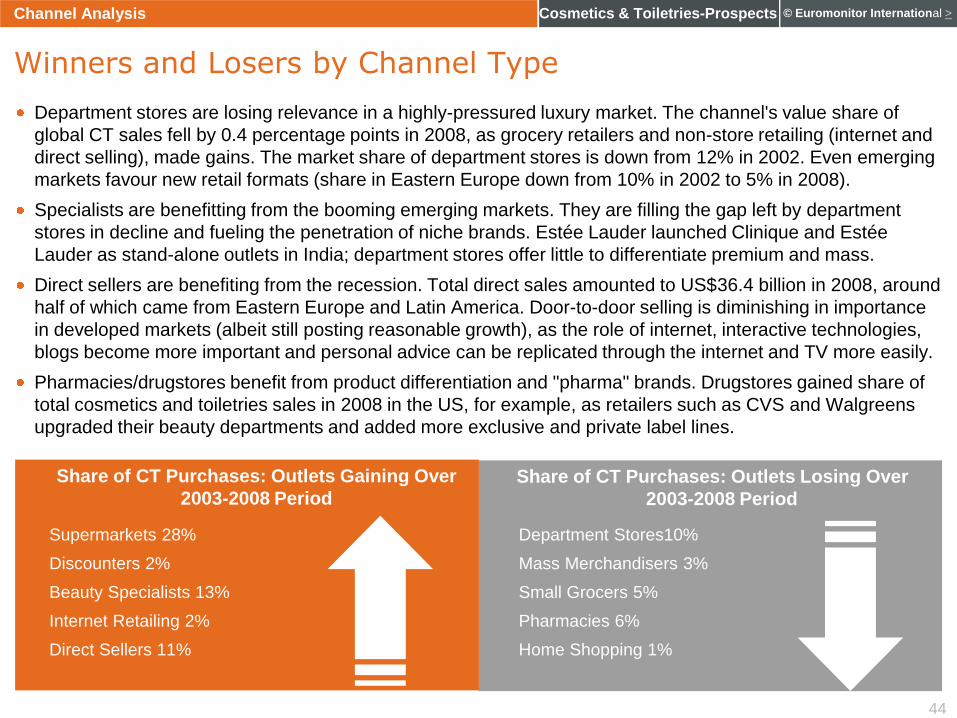

Department stores are losing relevance in a highly-pressured luxury market. The channel's value share of

global CT sales fell by 0.4 percentage points in 2008, as grocery retailers and non-store retailing (internet and

direct selling), made gains. The market share of department stores is down from 12% in 2002. Even emerging

markets favour new retail formats (share in Eastern Europe down from 10% in 2002 to 5% in 2008).

Specialists are benefitting from the booming emerging markets. They are filling the gap left by department

stores in decline and fueling the penetration of niche brands. Estée Lauder launched Clinique and Estée

Lauder as stand-alone outlets in India; department stores offer little to differentiate premium and mass.

Direct sellers are benefiting from the recession. Total direct sales amounted to US$36.4 billion in 2008, around

half of which came from Eastern Europe and Latin America. Door-to-door selling is diminishing in importance

in developed markets (albeit still posting reasonable growth), as the role of internet, interactive technologies,

blogs become more important and personal advice can be replicated through the internet and TV more easily.

Pharmacies/drugstores benefit from product differentiation and "pharma" brands. Drugstores gained share of

total cosmetics and toiletries sales in 2008 in the US, for example, as retailers such as CVS and Walgreens

upgraded their beauty departments and added more exclusive and private label lines.

Share of CT Purchases: Outlets Gaining Over

2003-2008 PeriodShare of CT Purchases: Outlets Losing Over

2003-2008 Period

Supermarkets 28%

Discounters 2%

Beauty Specialists 13%

Internet Retailing 2%

Direct Sellers 11%

Department Stores10%

Mass Merchandisers 3%

Small Grocers 5%

Pharmacies 6%

Home Shopping 1%

45

© Euromonitor International >Cosmetics & Toiletries-ProspectsChannel Analysis

Intensive Retail Expansion in Russia

Price and convenience continued to place supermarkets in the lead of CT retailing, and the format gained

share across most regions, except in Latin America and Australasia, where supermarkets nevertheless

distribute the highest shares of regional CT sales in the world (39% and 44%, respectively). Geographic

expansion continued with intensive focus on Russia where Auchan and Carrefour made commitments to

expand their networks in 2009, and Wal-Mart looked set to take a controlling stake in local hypermarket Lenta.

As the Eastern European economic landscape continues its transformation, the falls in small grocery retailers

and department stores have been dramatic, with consumers being attracted to the ease of supermarkets and

the better product differentiation and service of beauty retailers (perfumeries). The latter are the 3rd most

important channel in this region, where fashion and appearance are taking increasing importance and growth

of the channel has been exceptional. LVMH was seen taking a 50% stake in Ile de Beaute in Russia in 2008,

indicative of the company's commitment to this fast developing market.

Beauty retailers also made great inroads in Western Europe, and Middle East Africa. However, focussing on

small speciality retailers as opposed to department stores has also become a focus in Japan. Shiseido has

released its first major brand for speciality shops in 10 years.

0

10

20

30

40

World Asia Pacific Eastern Europe Latin America Middle East Africa

North America Western Europe

% v

alu

e s

ha

re

Share of Regional Market

Supermarkets & Discounters Department Stores & Mass Merchandisers Drugstores & Pharmacies

Beauty Specialists Non-store Retailers Others

46

© Euromonitor International >Cosmetics & Toiletries-Prospects

0

5

10

15

Internet Homeshopping Direct Selling

% v

alu

e s

ha

re

Non-store Retail 2003/2008