Global Petrochemical Market OutlookLeveraging Competitive Feedstocks Given Energy Market Uncertainty

Mark EramoGlobal Business DevelopmentIHS Chemical

Presented To:Congreso Argentino de PetroquimicaJune 14, 2016Centro Costa SalgueroBuenos Aires, Argentina

Congreso Argentino de Petroquimica, June 14, 2016

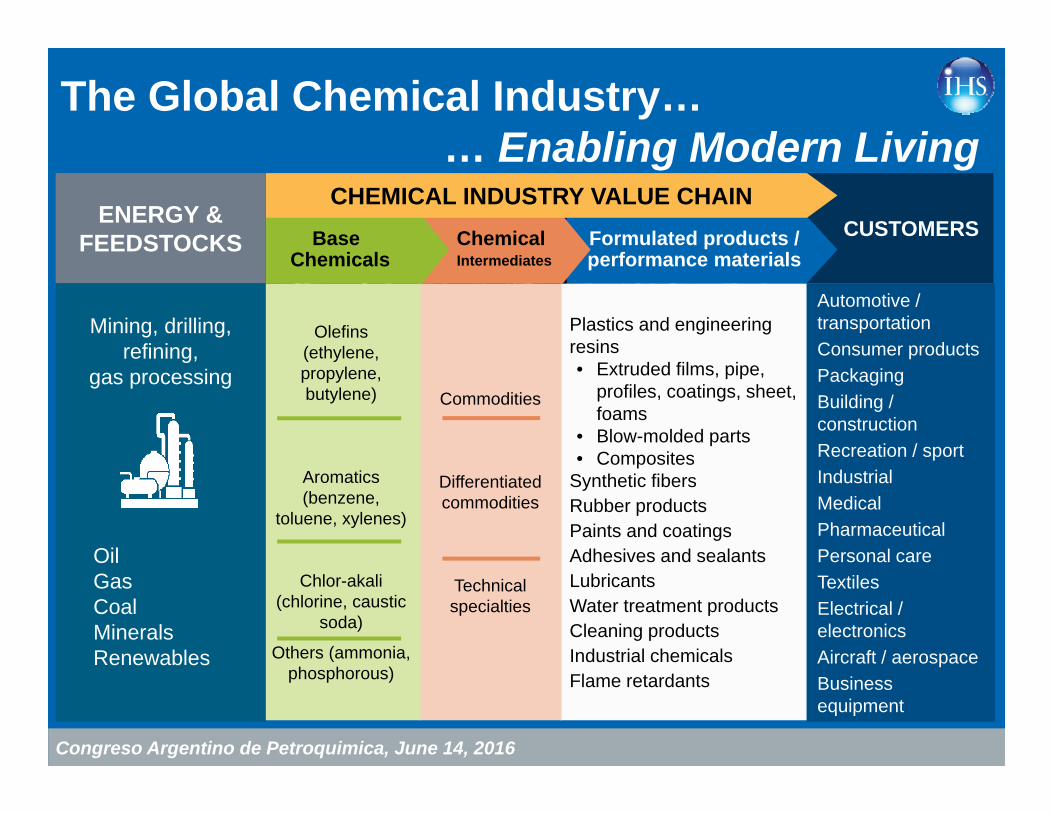

The Global Chemical Industry… … Enabling Modern Living

Automotive / transportationConsumer productsPackagingBuilding / constructionRecreation / sportIndustrialMedicalPharmaceuticalPersonal careTextilesElectrical / electronicsAircraft / aerospaceBusiness equipment

CUSTOMERSFormulated products / performance materials

Plastics and engineering resins• Extruded films, pipe,

profiles, coatings, sheet, foams

• Blow-molded parts• Composites

Synthetic fibersRubber productsPaints and coatingsAdhesives and sealantsLubricantsWater treatment productsCleaning productsIndustrial chemicalsFlame retardants

Commodities

Differentiated commodities

Technical specialties

ChemicalIntermediates

BaseChemicals

Olefins (ethylene, propylene, butylene)

Aromatics (benzene,

toluene, xylenes)

Chlor-akali(chlorine, caustic

soda)

Others (ammonia, phosphorous)

CHEMICAL INDUSTRY VALUE CHAINENERGY & FEEDSTOCKS

Mining, drilling, refining,

gas processing

OilGasCoalMineralsRenewables

ENERGY & FEEDSTOCKS

Congreso Argentino de Petroquimica, June 14, 2016

(right axis )

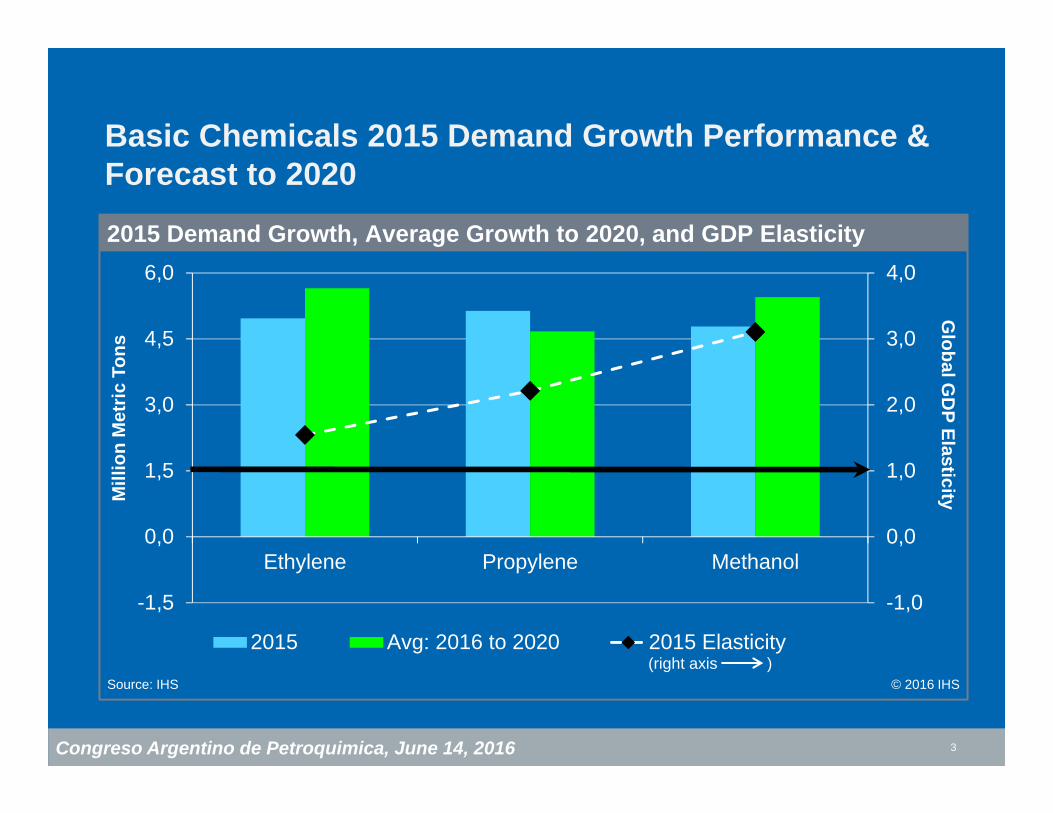

Basic Chemicals 2015 Demand Growth Performance & Forecast to 2020

3

-1,0

0,0

1,0

2,0

3,0

4,0

-1,5

0,0

1,5

3,0

4,5

6,0

Ethylene Propylene Methanol

2015 Avg: 2016 to 2020 2015 Elasticity

2015 Demand Growth, Average Growth to 2020, and GDP Elasticity

© 2016 IHS

Mill

ion

Met

ric T

ons

Source: IHS

Global G

DP Elasticity

Congreso Argentino de Petroquimica, June 14, 2016

Global Energy & Economic Fundamentals Have Changed…Impacting Investment Decisions

4

• Crude oil price trends impact regional competitiveness, cash margins, project returns and future investment decisions.

• Global economic growth patterns are shifting as developing countries adjust to lower energy and changes inside China evolve.

• Key decisions of location, feedstock, technology, scale, growth, cost position: are much less “obvious”

• Result is a slowdown in approving new investments for 2020+

Congreso Argentino de Petroquimica, June 14, 2016

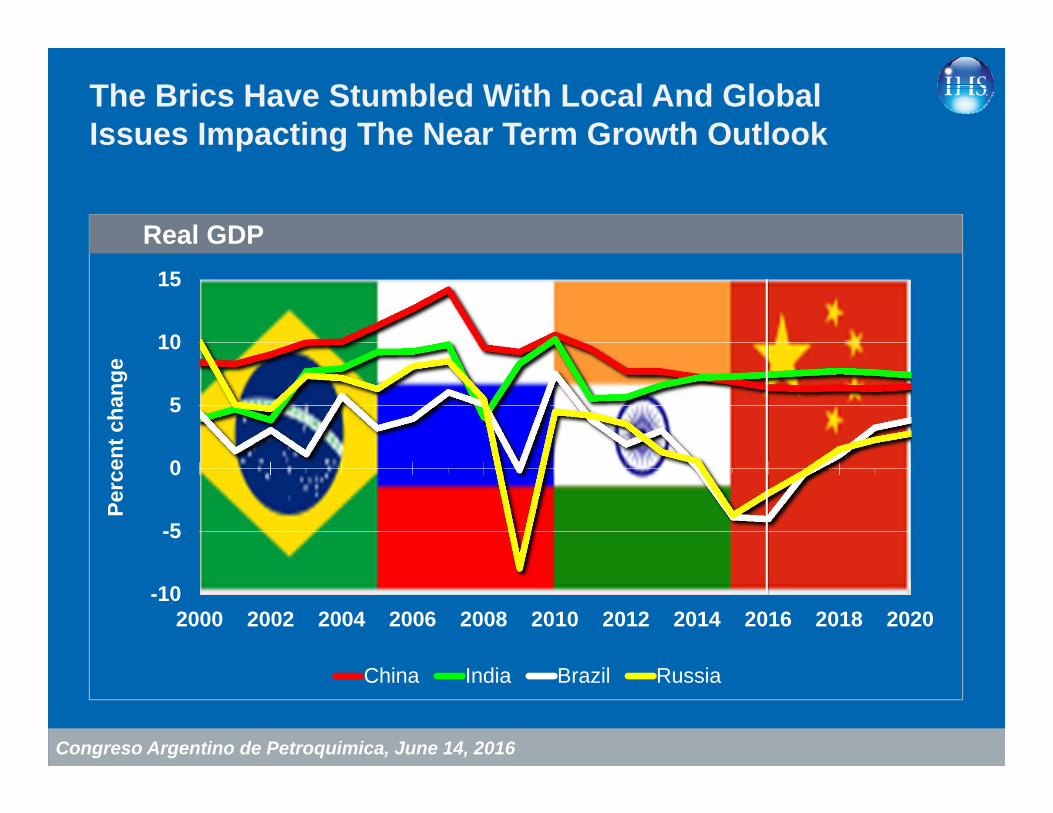

The Brics Have Stumbled With Local And Global Issues Impacting The Near Term Growth Outlook

-10

-5

0

5

10

15

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Perc

ent c

hang

e

China India Brazil Russia

Real GDP

Congreso Argentino de Petroquimica, June 14, 2016

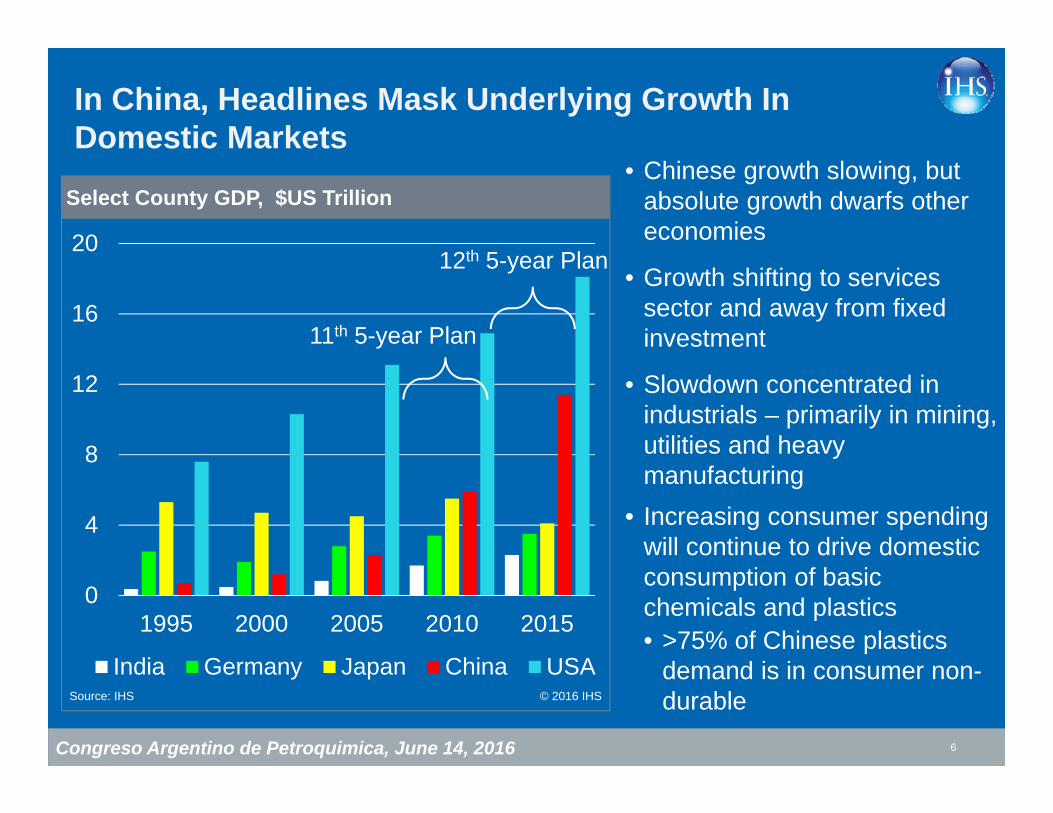

In China, Headlines Mask Underlying Growth In Domestic Markets

6

0

4

8

12

16

20

1995 2000 2005 2010 2015

India Germany Japan China USA

Select County GDP, $US Trillion

Source: IHS © 2016 IHS

• Chinese growth slowing, but absolute growth dwarfs other economies

• Growth shifting to services sector and away from fixed investment

• Slowdown concentrated in industrials – primarily in mining, utilities and heavy manufacturing

• Increasing consumer spending will continue to drive domestic consumption of basic chemicals and plastics• >75% of Chinese plastics

demand is in consumer non-durable

11th 5-year Plan

12th 5-year Plan

Congreso Argentino de Petroquimica, June 14, 2016

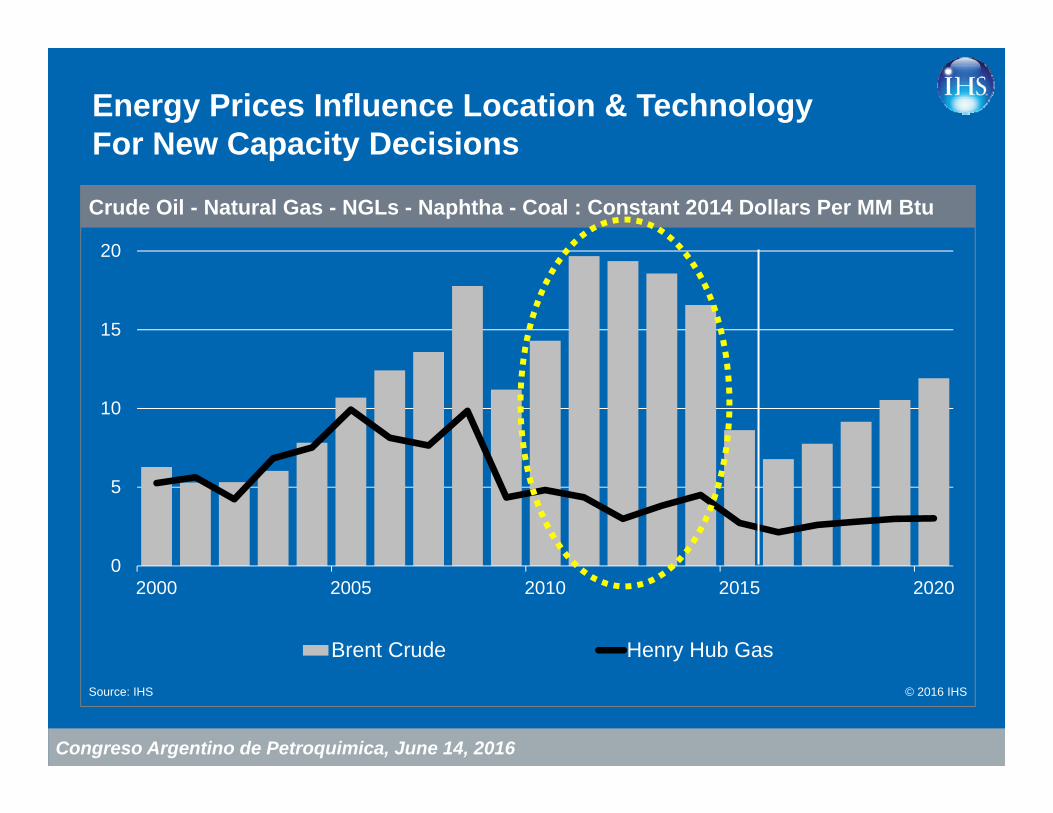

Energy Prices Influence Location & Technology For New Capacity Decisions

0

5

10

15

20

2000 2005 2010 2015 2020

Brent Crude Henry Hub Gas

Crude Oil - Natural Gas - NGLs - Naphtha - Coal : Constant 2014 Dollars Per MM Btu

Source: IHS © 2016 IHS

Congreso Argentino de Petroquimica, June 14, 2016

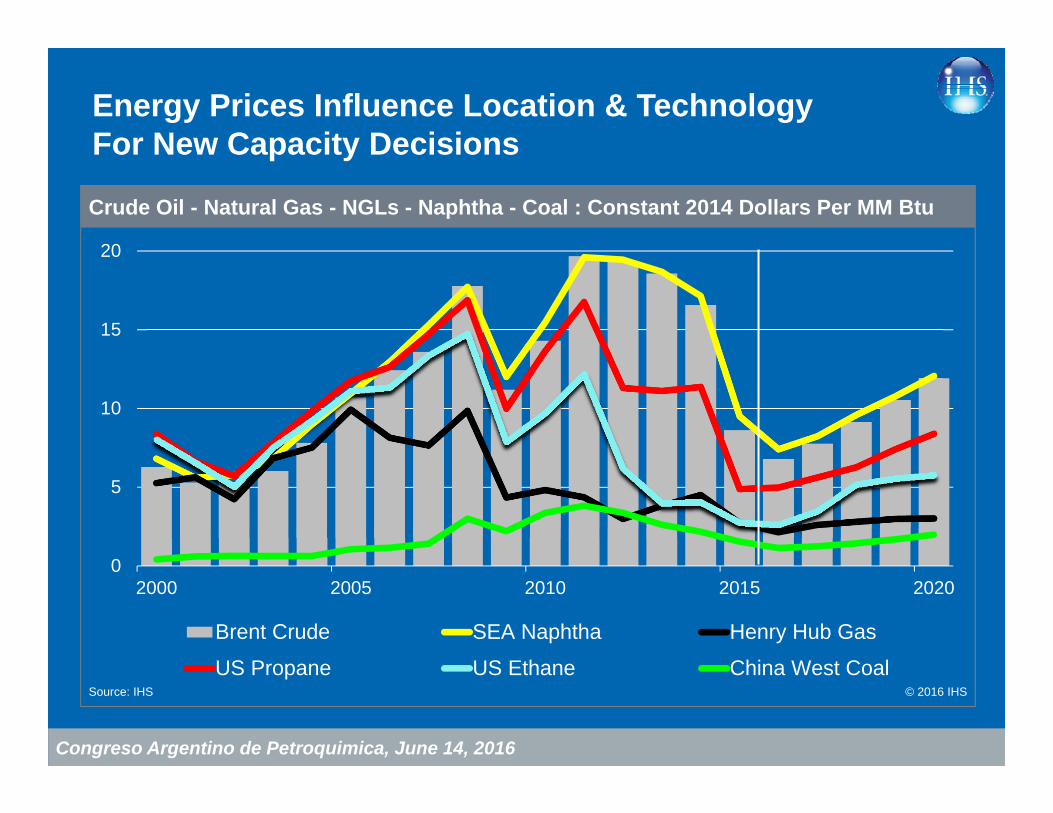

Energy Prices Influence Location & Technology For New Capacity Decisions

0

5

10

15

20

2000 2005 2010 2015 2020

Brent Crude SEA Naphtha Henry Hub Gas

US Propane US Ethane China West Coal

Crude Oil - Natural Gas - NGLs - Naphtha - Coal : Constant 2014 Dollars Per MM Btu

Source: IHS © 2016 IHS

Congreso Argentino de Petroquimica, June 14, 2016

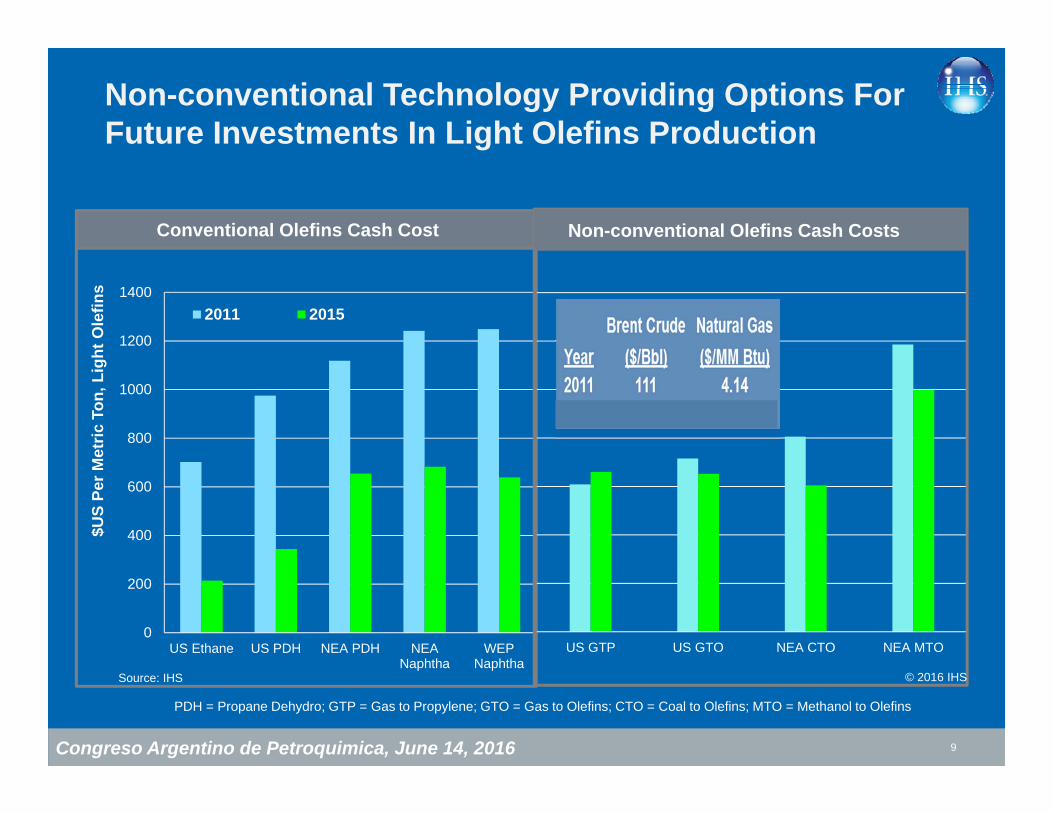

Non-conventional Technology Providing Options For Future Investments In Light Olefins Production

9

0

200

400

600

800

1000

1200

1400

US Ethane US PDH NEA PDH NEANaphtha

WEPNaphtha

2011 2015

Conventional Olefins Cash Cost

US GTP US GTO NEA CTO NEA MTO

Non-conventional Olefins Cash Costs

PDH = Propane Dehydro; GTP = Gas to Propylene; GTO = Gas to Olefins; CTO = Coal to Olefins; MTO = Methanol to Olefins

Source: IHS © 2016 IHS

$US

Per M

etric

Ton

, Lig

ht O

lefin

s

Congreso Argentino de Petroquimica, June 14, 2016

Key Assumptions Regarding Future Investments Are No Longer “Obvious”

10

Investment Key Assumptions:• Global crude oil price scenarios• Global economic growth outlook• North American energy market• China structural changes• Non-conventional technology • Current state of the profit cycle• Project Financing• Sustainability (GHG emissions)• Levels of integration• Logistics investments• Geo-political considerationsPhoto courtesy of Braskem Idesa

Congreso Argentino de Petroquimica, June 14, 2016

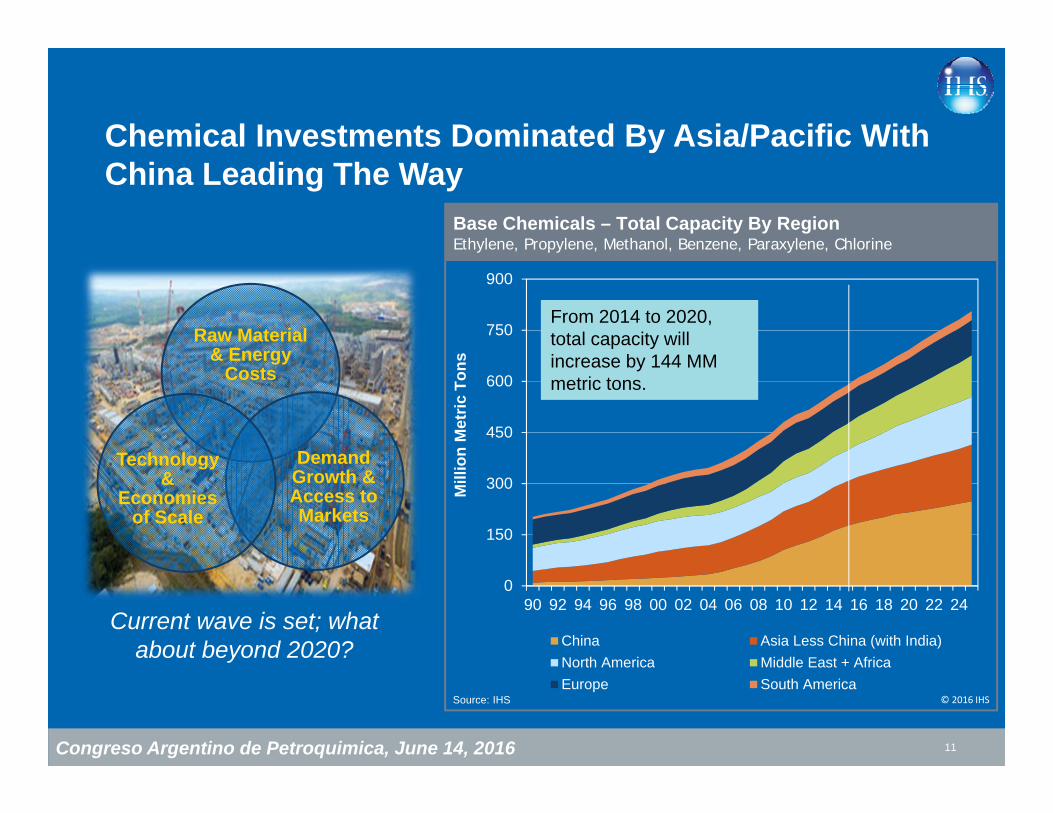

Chemical Investments Dominated By Asia/Pacific With China Leading The Way

11

Raw Material & Energy

Costs

Demand Growth & Access to Markets

Technology &

Economies of Scale

0

150

300

450

600

750

900

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

China Asia Less China (with India)North America Middle East + AfricaEurope South America

Base Chemicals – Total Capacity By Region Ethylene, Propylene, Methanol, Benzene, Paraxylene, Chlorine

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

Current wave is set; what about beyond 2020?

From 2014 to 2020, total capacity will increase by 144 MM metric tons.

Congreso Argentino de Petroquimica, June 14, 2016 12

Benzene

Chlorine

Ethylene

Methanol

Paraxylene

Propylene PG

Where To Invest The Next Wave Beyond 2020?

CERI 2016 Petrochemical Conference: June 5-7, 2016Congreso Argentino de Petroquimica, June 14, 2016

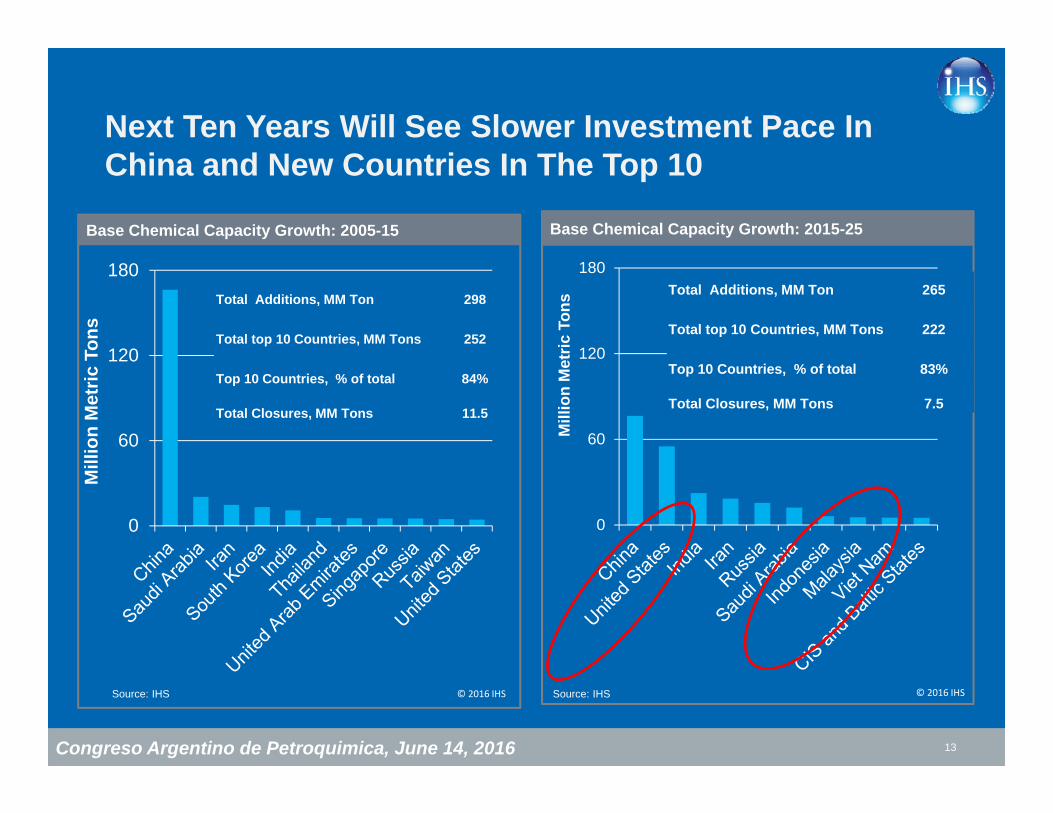

Next Ten Years Will See Slower Investment Pace In China and New Countries In The Top 10

13

0

60

120

180

Mill

ion

Met

ric T

ons

Base Chemical Capacity Growth: 2015-25

Source: IHS © 2016 IHS

0

60

120

180

Mill

ion

Met

ric T

ons

Base Chemical Capacity Growth: 2005-15

Total Additions, MM Ton 298

Total top 10 Countries, MM Tons 252

Top 10 Countries, % of total 84%

Total Closures, MM Tons 11.5

Source: IHS © 2016 IHS

Total Additions, MM Ton 265

Total top 10 Countries, MM Tons 222

Top 10 Countries, % of total 83%

Total Closures, MM Tons 7.5

CERI 2016 Petrochemical Conference: June 5-7, 2016Congreso Argentino de Petroquimica, June 14, 2016

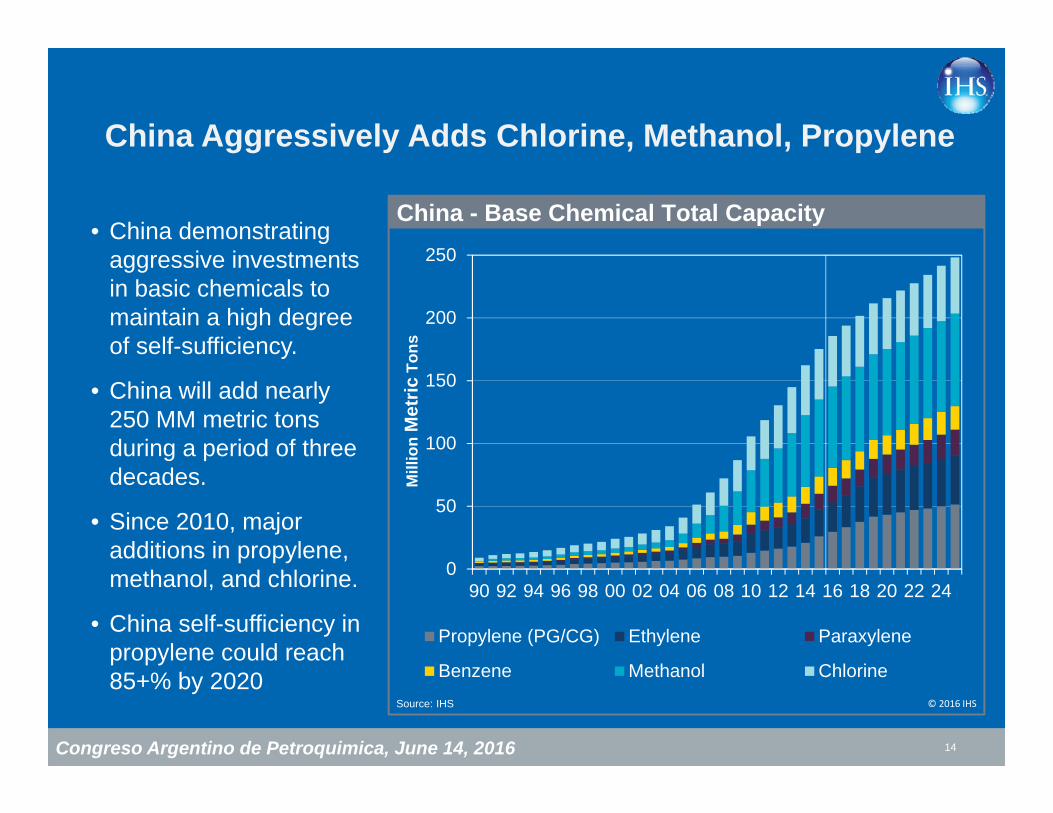

China Aggressively Adds Chlorine, Methanol, Propylene

14

0

50

100

150

200

250

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Propylene (PG/CG) Ethylene Paraxylene

Benzene Methanol Chlorine

China - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Mill

ion

Met

ricTo

ns

• China demonstrating aggressive investments in basic chemicals to maintain a high degree of self-sufficiency.

• China will add nearly 250 MM metric tons during a period of three decades.

• Since 2010, major additions in propylene, methanol, and chlorine.

• China self-sufficiency in propylene could reach 85+% by 2020

CERI 2016 Petrochemical Conference: June 5-7, 2016Congreso Argentino de Petroquimica, June 14, 2016

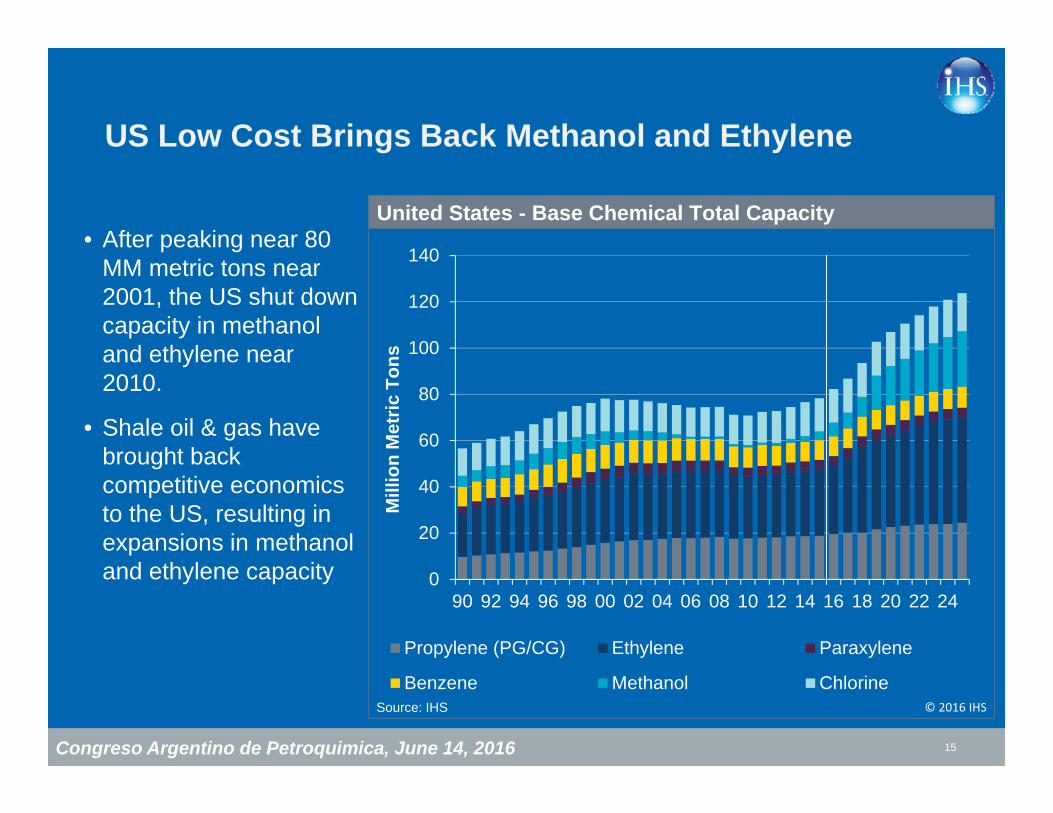

US Low Cost Brings Back Methanol and Ethylene

15

• After peaking near 80 MM metric tons near 2001, the US shut down capacity in methanol and ethylene near 2010.

• Shale oil & gas have brought back competitive economics to the US, resulting in expansions in methanol and ethylene capacity 0

20

40

60

80

100

120

140

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24

Propylene (PG/CG) Ethylene Paraxylene

Benzene Methanol Chlorine

United States - Base Chemical Total Capacity

Source: IHS © 2016 IHS

Mill

ion

Met

ric T

ons

Congreso Argentino de Petroquimica, June 14, 2016

Planning Future Investments In Petrochemicals

Strategic Implications

16

• High level of uncertainty in energy and economic fundamentals present difficult scenarios for future project evaluations.

• The investment landscape is changing with shifting demand growth and non-conventional options on technology and feedstocks.

• Board rooms likely to require higher returns; approvals deferred until conditions signal more predicable outcomes.

• Investment decisions for 2016 placed “on hold” could lead to supply limitations in the 2020+ time-period.

Global Petrochemical Market Outlook

Thank You

Mark EramoGlobal Business DevelopmentIHS Chemical

Presented To:Congreso Argentino de PetroquimicaJune 14, 2016Centro Costa SalgueroBuenos Aires, Argentina