1

Market Dynamics : India, Asia and World The LBMA/LPPM Precious Metals Conference 2013, Rome The London Bullion Market Association September 30, 2013

Shekhar Bhandari Executive Vice President

Kotak Mahindra Bank email: [email protected]

2

India

3

Trade :: 500 - 300 Equation

Source: CEIC, Kotak Mahindra Bank

CAD without gold imports within the comfort zone

(80)

(60)

(40)

(20)

0

20

40

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

CAD CAD ex gold imports$bn

Policy makers needed to take

cognizance of a steadily widening

CAD in these years

Source: CEIC, Kotak Mahindra Bank

Consumption oriented growth has led to jumps in import items

Major imports ($bn)

9 7 8

2129

87

10 7 10

27

41

106

1711 13

33

56

155

158 11

31

54

125

0

20

40

60

80

100

120

140

160

180

Coal Fertiliser Metal scrap Electronics Gold Oil

2010 2011 2012 2013

Source: Bloomberg, Kotak Mahindra Bank

Oil prices drop in $ terms…..beneficial to CAD but not in terms of other economic variables

20

40

60

80

100

120

140

160

2005 2006 2007 2008 2009 2010 2011 2012 2013

1800

2300

2800

3300

3800

4300

4800

5300

5800

6300

6800Brent ($/bbl) Brent (Rs/bbl), RHS

CAD sensitivity to oil and gold

1150 1200 1250 1300 1350 1400 145090 (56.6) (57.7) (58.7) (59.8) (60.9) (62.0) (63.1)95 (61.6) (62.7) (63.8) (64.9) (65.9) (67.0) (68.1)

100 (66.6) (67.7) (68.8) (69.9) (71.0) (72.0) (73.1)105 (71.7) (72.7) (73.8) (74.9) (76.0) (77.1) (78.2)110 (76.7) (77.8) (78.8) (79.9) (81.0) (82.1) (83.2)115 (81.7) (82.8) (83.9) (85.0) (86.0) (87.1) (88.2)120 (86.7) (87.8) (88.9) (90.0) (91.1) (92.1) (93.2)

Gold price (US$/oz)

Cru

de

pri

ce

(US$

/bb

l)

$/` 43.30 $/` 68.85

Source: Bloomberg, Kotak Mahindra Bank

The non-trade portion of CAD is also under stress

(12)

(2)

8

18

28

38

48

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Private transfers Software services%yoy, 4QMA

(22)

(12)

(2)

8

18

28

38

48

58

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Software services Transfers Income$ bn

0

100

200

300

400

500

600

700

800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

(25)

(20)

(15)

(10)

(5)

0

IIP asset ($bn)

IIP Liabilities ($bn)

Net investment income ($bn, reverse scale, RHS)

Stress on the BoP due to (1) wide CAD (2) volatile capital flows

Source: CEIC, Kotak Mahindra Bank Estimates

8

(US$bn) 2014E

2011 2012 2013 Oil@100 Oil@105 Oil@110

Current account (45.9) (78.2) (88.2) (70.6) (76.3) (82.0)GDP 1,708 1,871 1,842 1,927 1,927 1,927CAD/GDP (%) (2.7) (4.2) (4.8) (3.7) (4.0) (4.3)Trade balance (130.6) (189.8) (195.7) (182.2) (187.9) (193.6)Trade balance/GDP (%) (7.7) (10.3) (10.6) (9.5) (9.7) (10.0) - Exports 250 310 307 308 310 312 - Imports 381 500 502 490 498 505 - oil imports 105 155 170 154 162 169 - non-oil imports 276 345 332 336 336 336Invisibles (net) 85 112 107 112 112 112 - Services 49 64 65 71 71 71 - software 53 61 64 69 69 69 - non-software (4.4) 3.1 1.4 2.0 2.0 2.0 - Transfers 53 63 64 65 65 65 - Income (net) (17.3) (16.0) (21.5) (24.0) (24.0) (24.0)Capital account 62.1 67.8 89.4 77.0 77.0 77.0Percentage of GDP 3.7 3.7 4.9 4.0 4.0 4.0Foreign investment 39.7 39.2 46.7 35.0 35.0 35.0 - FDI 9.4 22.1 19.8 20.0 20.0 20.0

- FII 30.3 17.2 26.9 15.0 15.0 15.0

Banking capital 5.0 16.2 16.6 17.0 17.0 17.0 - NRI deposits 3.2 11.9 14.8 12.0 12.0 12.0

Short-term credit 11.0 6.7 21.7 20.0 20.0 20.0

ECBs 12.5 10.3 8.5 8.0 8.0 8.0External assistance 4.9 2.3 1.0 2.0 2.0 2.0Other capital account items (11.0) (6.9) (5.0) (5.0) (5.0) (5.0)

E&O (3.0) (2.4) 2.7 0.0 0.0 0.0

Overall balance 13.1 (12.8) 3.9 6.4 0.7 (5.0)Memo items

Average USD/INR 45.63 47.96 54.41 57.56 57.56 57.56Average crude (US$/bbl) 85.1 111.7 108.2 100.0 105.0 110.0

Need to fund CAD makes India heavily reliant on global capital flows

§ CAD in FY2013 at US$ 88 bn, implies India would need ~US$ 7-8 bn / month of capital inflows to bridge this gap

§ Global capital flows to EM economies face uncertainty with the ongoing debate of Fed QE withdrawal

§ With CAD correction proving to be difficult, reliance on capital flows are higher, thereby leading to INR volatility

Trade Trade Trade Trade Trade

Fresh RBI Circular

Trade Trade Trade Trade Trade

• Import of gold in the form of coins and medallions is now prohibited.

• It shall be incumbent on all nominated banks/nominated agencies and other entities to ensure

that at least one fifth, i.e., 20%, of every lot of import of gold imported to the country is exclusively

made available for the purpose of exports and the balance for domestic use. A working example of

the operations of the 20/80 scheme envisaged in terms of the present instructions is given in

the Annex. This shall be monitored by customs authorities, and will be implemented port-wise only.

• Further, nominated banks/ nominated agencies and other entities shall make available gold for

domestic use only to the entities engaged in jewellery business/bullion dealers and to banks

authorised to administer the Gold Deposit Scheme against full upfront payment. In other words,

supply of gold in any form to the domestic users other than against full payment upfront shall not

be permitted.

• The nominated banks/agencies/refineries and other entities shall ensure that there is no front

loading of imports, particularly in the first and second lots of imports. Such imports shall be linked

to normal quantities of gold supplied to the exporters by the nominated banks/agencies and shall

not exceed the highest quantity supplied during any one year out of last three years. The quantity

thus arrived at, however, will not be imported in one or two lots only. As a thumb rule, imports of

more than maximum of two months of requirements of the exporters in a lot would be considered

unusual. Illustratively, if the gold supplied to exporters by a bank during the last three years is say,

30 tonnes, 40 tonnes and 60 tonnes respectively, imports in terms of this circular shall be based on

highest of three i.e. 60 tonnes. Further, import of 50 tonnes( two months export of 10 tonnes for

exports and 4 times the amount for domestic use, totalling 50 tonnes) will be considered unusual.

In case of nominated banks not having a previous record of having supplied gold to the exporters

they would need to seek prior approval from RBI before placing orders for import of gold for the

first lot under the 20/80 scheme.

Fresh RBI Circular…contd

Trade Trade Trade Trade Trade

• The 20/80 principle would also apply for the henceforth import of gold in any form/purity including

gold dore, whereby 20 per cent of the gold imported shall be provided to the exporters. This will be

administered and monitored at the refinery level for each consignment at the time of such imports.

This will also be monitored by the customs authorities. The refinery shall make available for

domestic use only to the entities engaged in jewellery business/bullion dealers and to the banks

authorised to administer the Gold Deposit Scheme against full upfront payment and sale of gold

against any other form of payment shall not be permitted. Further, the import of gold dore is

permitted only against a licence issued by DGFT.

• Any authorisation such as Advance Authorisation/Duty Free Import Authorization (DFIA) is to be

utilised for import of gold meant for export purposes only and no diversion for domestic use shall

be permitted.

3. Entities/units in the SEZ and EoUs, Premier and Star trading houses are permitted to import gold

exclusively for the purpose of exports only.

4. AD Category I banks are advised to strictly ensure that foreign exchange transactions effected by /

for their constituents are compliant with the above instructions. Head Offices of nominated agencies /

International Banking Divisions of banks would be responsible for monitoring operations of the revised

scheme taking into account transactions put through different centres. In respect of gold released

for the purpose of exports, AD Category I banks will also put in place a special mechanism to

monitor realization of export proceeds as per the extant regulations and any contraventions/

unusual developments in this regard should be reported forthwith to the concerned Regional

Office of the Reserve Bank of India.

5. Government of India will be issuing separate instructions, if any, to the customs authorities/DGFT to

operationalise and monitor the above requirements for import of gold.

6. The above instructions will come into force with immediate effect. Authorised dealers may please

bring the contents of this circular to the notice of their constituents and customers concerned.

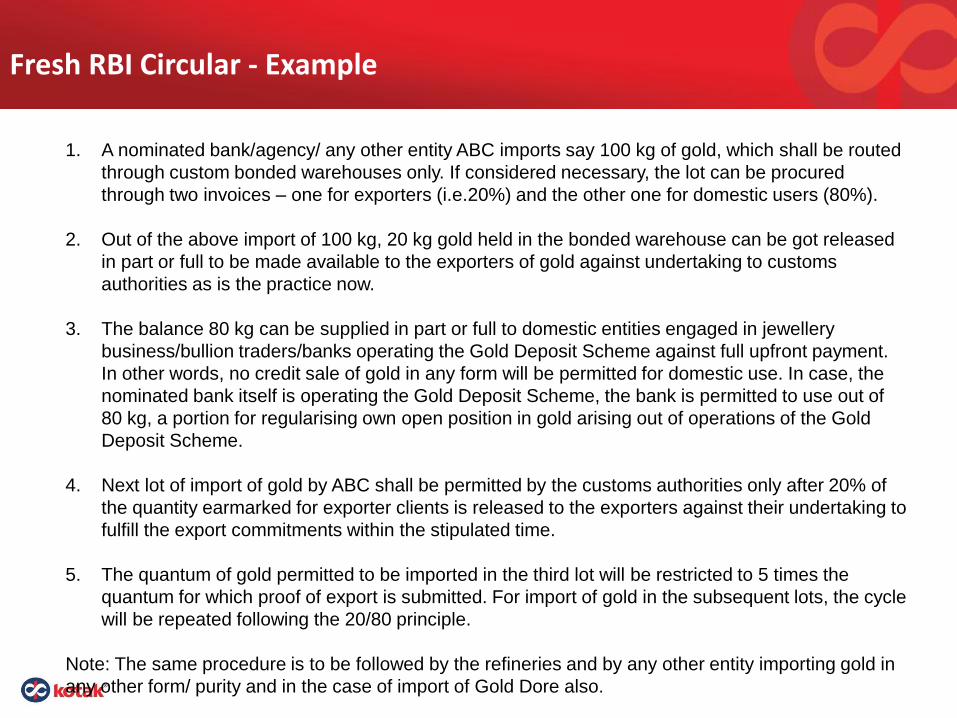

Fresh RBI Circular - Example

Trade Trade Trade Trade Trade

1. A nominated bank/agency/ any other entity ABC imports say 100 kg of gold, which shall be routed

through custom bonded warehouses only. If considered necessary, the lot can be procured

through two invoices – one for exporters (i.e.20%) and the other one for domestic users (80%).

2. Out of the above import of 100 kg, 20 kg gold held in the bonded warehouse can be got released

in part or full to be made available to the exporters of gold against undertaking to customs

authorities as is the practice now.

3. The balance 80 kg can be supplied in part or full to domestic entities engaged in jewellery

business/bullion traders/banks operating the Gold Deposit Scheme against full upfront payment.

In other words, no credit sale of gold in any form will be permitted for domestic use. In case, the

nominated bank itself is operating the Gold Deposit Scheme, the bank is permitted to use out of

80 kg, a portion for regularising own open position in gold arising out of operations of the Gold

Deposit Scheme.

4. Next lot of import of gold by ABC shall be permitted by the customs authorities only after 20% of

the quantity earmarked for exporter clients is released to the exporters against their undertaking to

fulfill the export commitments within the stipulated time.

5. The quantum of gold permitted to be imported in the third lot will be restricted to 5 times the

quantum for which proof of export is submitted. For import of gold in the subsequent lots, the cycle

will be repeated following the 20/80 principle.

Note: The same procedure is to be followed by the refineries and by any other entity importing gold in

any other form/ purity and in the case of import of Gold Dore also.

India : : Monetising Gold Reserves

§ Recycling

§ Processing

§ Temple Gold

§ Gold imports in 2016 …. Will it be required at all !!

Trade Trade

14

China ….Asia …..World

15

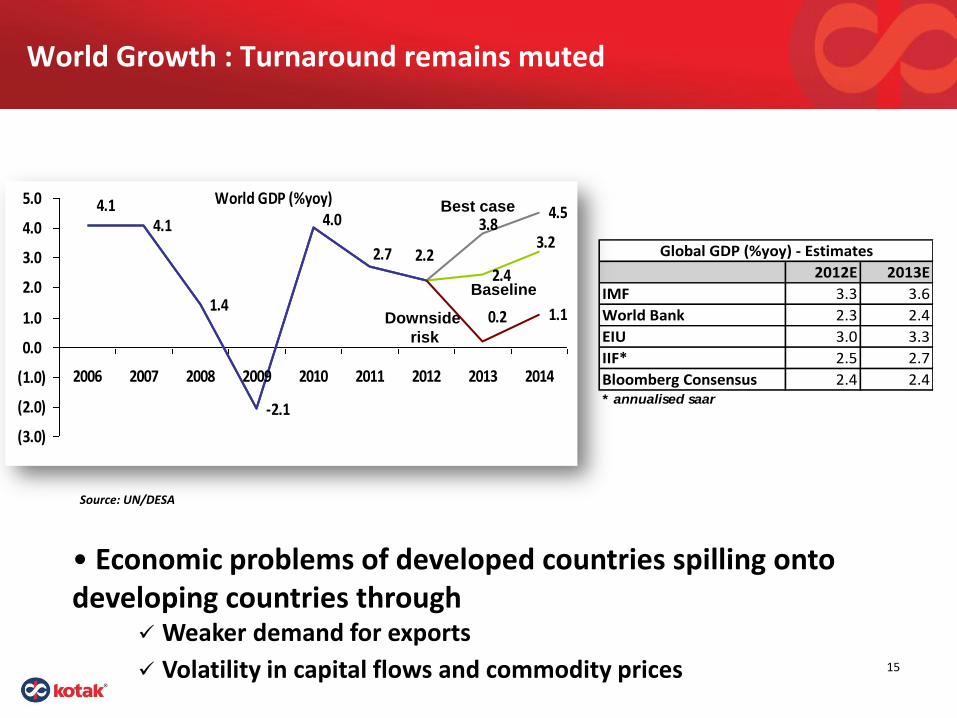

World Growth : Turnaround remains muted

• Economic problems of developed countries spilling onto developing countries through

Weaker demand for exports

Volatility in capital flows and commodity prices

2012E 2013E

IMF 3.3 3.6

World Bank 2.3 2.4

EIU 3.0 3.3

IIF* 2.5 2.7

Bloomberg Consensus 2.4 2.4* annualised saar

Global GDP (%yoy) - Estimates

Source: UN/DESA

World GDP (%yoy)

4.1

1.4

-2.1

1.1

2.4

3.2

4.53.8

2.7

4.0

0.2

2.2

4.1

(3.0)

(2.0)

(1.0)

0.0

1.0

2.0

3.0

4.0

5.0

2006 2007 2008 2009 2010 2011 2012 2013 2014

Baseline

Downside

risk

Best case

16

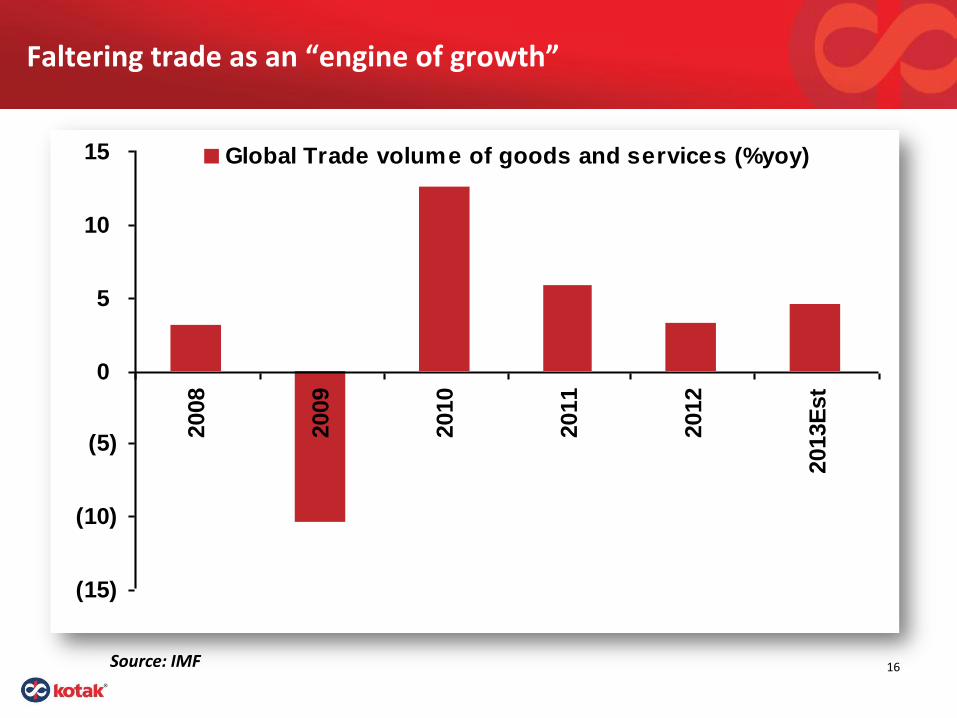

Faltering trade as an “engine of growth”

(15)

(10)

(5)

0

5

10

15

2008

2009

2010

2011

2012

2013E

st

Global Trade volume of goods and services (%yoy)

Source: IMF

17

Unwinding not easy

Disclaimer

• In the preparation of the material contained in this document, Kotak Mahindra Bank Ltd. (Kotak Bank), has used information that is publicly available, including information developed inhouse. Some of the material used in the document may have been obtained from members/persons other than the Kotak Bank and/or its affiliates and which may have been made available to Kotak Bank and/or its affiliates. Information gathered & material used in this document is believed to be from reliable sources. Kotak Bank however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material no such party will assume any liability for the same. Kotak Bank and/or any affiliate of Kotak Bank does not in any way through this material solicit any offer for purchase, sale or any financial transaction/commodities/products of any financial instrument dealt in this material. All recipients of this material should before dealing and or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice.

• We have included statements/opinions/recommendations in this document which contain words or phrases such as "will", "expect" "should" and similar expressions or variations of such expressions, that are "forward looking statements". Actual results may differ materially from those suggested by the forward looking statements due to risks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated.

• Kotak Bank (including its affiliates) and any of its officers directors, personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/ are liable for any decision taken on the basis of this material. The investments discussed in this material may not be suitable for all investors. Any person subscribing to or investing in any product/financial instruments should do so on the basis of and after verifying the terms attached to such product/financial instrument. Financial products and instruments are subject to market risks and yields may fluctuate depending on various factors affecting capital/debt markets. Please note that past performance of the financial products and instruments does not necessarily indicate the future prospects and performance thereof.

• Such past performance mayor may not be sustained in future. Kotak Bank (including its affiliates) or its officers, directors, personnel and employees, including persons involved in the preparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation in the financial instruments/products/commodities discussed herein or act as advisor or lender/borrower in respect of such securities/financial instruments/products/commodities or have other potential conflict of interest with respect to any recommendation and related information and opinions. The said persons may have acted upon and/or in a manner contradictory with the information contained here. No part of this material may be duplicated in whole or in part in any form and or redistributed without the prior written consent of Kotak Bank. This material is strictly confidential to the recipient and should not be reproduced or disseminated to anyone else.

Thank You

www.kotak.com