Confidential & Proprietary

Automotive Industry in RussiaGoogle Trends & Insights - Q4 2015

Key Q4’15 findings

● Q4’15 search volume in automotive category is 7% down YoY, mostly due to abnormal interest in Q4’2014

● Share of queries from mobile devices is steadily growing and already exceeding share of queries from PCs in all categories - new and used cars, generics, aftersales

● Toyota and Hyundai are fighting in brand interest competition in the Mass segment, while BMW and Audi are consistently leading the Premium segment; Lexus has overtaken 3rd place from Mercedes-Benz

Proprietary + ConfidentialProprietary + Confidential

Industry Overview

‘Universe’ of auto-related queries in Russia created from ~30k keywords. They are split into 4 groups and 10 sample queries from each segment listed below

2006 lexus gs 300

bmw 316i 2013

hyundai i30 2009

porsche cayenne 2013

toyota camry 2012 года

купить машину в тюмени бу

ауди а1 бу

ауди а8 бу

бу машины рязань

купить машину бу в москве

4 4 авто

авто россия

автоновости

внедорожники

кабриолет

как продать авто

какой самый лучший кроссовер

какую машину выбрать

каталог авто

каталог японских машин

двигатель мазда 3

диски land rover

замена масла в акпп пежо 207

замена ремня генератора пежо

замена цепи грм шкода фабия

запчасти на фрилендер

зимние шины мишлен

тормозные диски шкода суперб

рестайлинг рендж ровер

топливный фильтр octavia a5

нисан тюмень

новый fiat ducato

продажа ниссан тиида

рендж ровер спорт 2015

ситроен дс5

киа рио

тойота ленд крузер 200 2014

фольцваген цена

хендай i30

шевроле круз седан

New Cars Used Cars Generic After-sales

Keyword Examples for Segment Analysis,random 10 keywords

Source: Google Internal Data

After a drop in June interest to New Cars has restored by end of 2015 with a slight drop in December. Used Cars segment being in overall decline vs Q4’14

Indexed query growth 2014-2015,100% = number of queries in Jan’14

New

Car

sU

sed

Car

s

Source: Google Internal Data

Search queries in Generics category grew steadily in Q3 resulting in 10% growth in Q4 vs Q3. Aftersales category experience traditional spike in Q4 due to tyres service season

Source: Google Internal Data

Gen

eric

sA

ferr

sale

s

Winter tyres

Indexed query growth 2014-2015,100% = number of queries in Jan’14

Winter tyres

Mobile penetration in both New Cars and Used Cars segment is growing accounting for 60% in new cars and 64% in used cars

Split of Auto-queries on Google.ru by devices,Percent

Split of Auto-queries on Google.ru by devices,Percent

New Cars Used Cars

Source: Google Internal Data

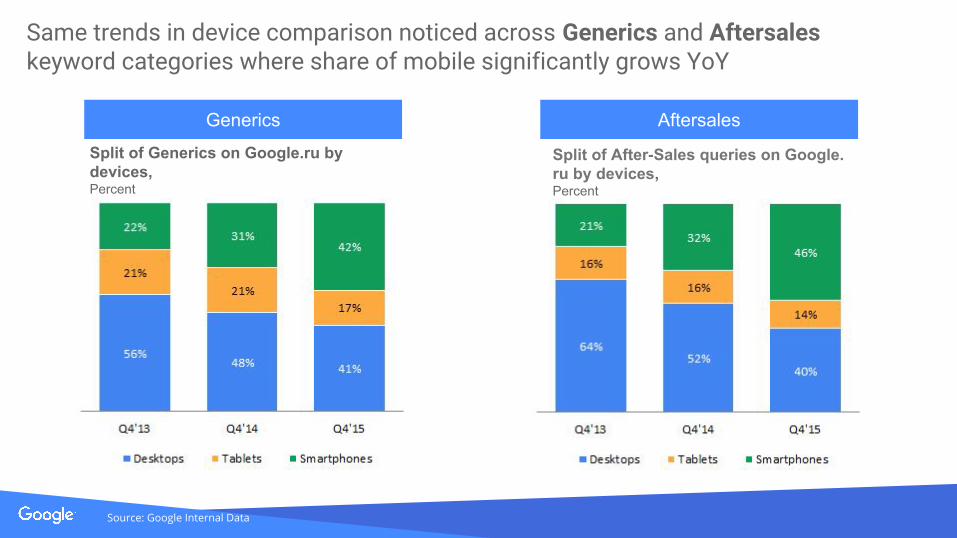

Same trends in device comparison noticed across Generics and Aftersales keyword categories where share of mobile significantly grows YoY

Generics Aftersales

Split of Generics on Google.ru by devices,Percent

Split of After-Sales queries on Google.ru by devices,Percent

Source: Google Internal Data

Share of mobile search in Russia is 46%, higher than share of search from PCs, which dropped below 50% in majority of the regions

Split of Auto queries on Google.ru by devices and regions,Q4’15, Percent

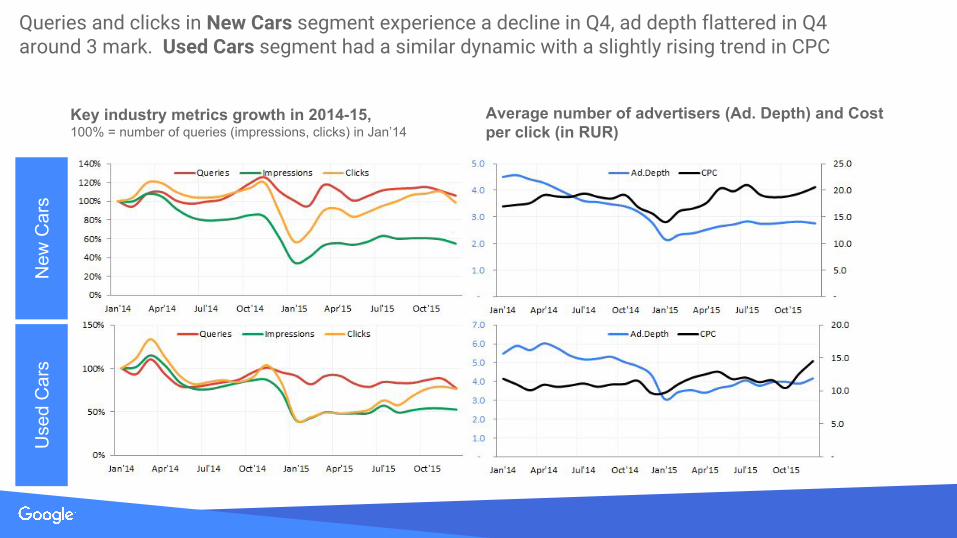

Queries and clicks in New Cars segment experience a decline in Q4, ad depth flattered in Q4 around 3 mark. Used Cars segment had a similar dynamic with a slightly rising trend in CPC

New

Car

sU

sed

Car

s

Average number of advertisers (Ad. Depth) and Cost per click (in RUR)

Key industry metrics growth in 2014-15,100% = number of queries (impressions, clicks) in Jan’14

Auction metrics related to Generics returned to beginning of 2015 positions apart from impressions which dropped. Aftersales experienced traditional spike in Q4.

Average number of advertisers (Ad. Depth) and Cost per click (in RUR)

Key industry metrics growth in 2014-15,100% = number of queries (impressions, clicks) in Jan’14

Gen

eric

sA

fters

ales

Volume & Premium BrandsOverview

Within Volume Brands Toyota lost its position to Hyundai, meanwhile Kia, VW and Nissan have slightly lost in the brand interest rank

Monthly dynamics of branded queries,2014-2015

Tier

1Ti

er 2

Tier

3

Hyundai became a leader. KIA & VW fall dramatically. Nissan stop decline.

SKODA turns to leader in

subcategory. All peers share similar

declining trend

Datsun became a tier leader but interest

started to decrease in Nov-Dec.

BMW is confidently leading the way with Audi following. Lexus has moved to 3d position due to decrease in interest to Mercedes.

Monthly dynamics of branded queries,2014-2015 Interest to Lexus grows

steadily while Mercedes has fallen in Q4 leading to Lexus became #3 brand.

By the end of Q4’15 interest to Infiniti, Porsche

and Volvo were at the same level.

There is a constant competition within Jaguar

Land Rover group of brands

Mini has outgrown Cadillac in Q4

For feedback and questions please reach out to Google Auto team: