Henning Schwabe, Partner, Arendt & Medernach

EMIR – from present to future

ABBL EMIR Conference 20 November 2014

Central clearing, legal obligations, margin requirements

2

© A

rend

t &

Med

erna

ch 2

014

1. Introduction

2. General Overview

3. Clearing

4. EU regulatory framework for securities market infrastructure

Table of Contents

3

1. Introduction

4

© A

rend

t &

Med

erna

ch 2

014

1. Introduction

1.1 A wave of regulatory requirements

1.2 Why EMIR?

1.3 High-level Timeline

Table of Contents

5

1.1 A wave of regulatory requirements

Luxembourg

UCITS IV

UCITS VI

EMIR

UCITS V

Global Reporting /

Disclosure RulesBasel IISolvency IIFATCAetc.

MiFID II & MiFIR

U.S.

Dodd-Frank

AIFMD

Global Distribution Rules Asia (Singapore, Hong Kong) Switzerland (FINMA) etc.

PRIPs

etc.

6

© A

rend

t &

Med

erna

ch 2

014

1.2 Why EMIR?

The financial crisis of 2007/08 was in part due to the lack of transparency in the trading and processing of OTC derivatives It highlighted the need for data standards and management of counterparty risk for OTC instruments

The global impact of this crisis required collective action by governments around the world and hence the issue was taken up by the G-20 leaders at the 2009 summit in Pittsburgh

“All standardized OTC derivatives contracts should be traded on exchanges or electronic trading platforms […] and cleared through central counterparties (CCP) […] OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements.”

The aim is to improve transparency in the derivatives markets, mitigate systemic risk and protect against market abuse

7

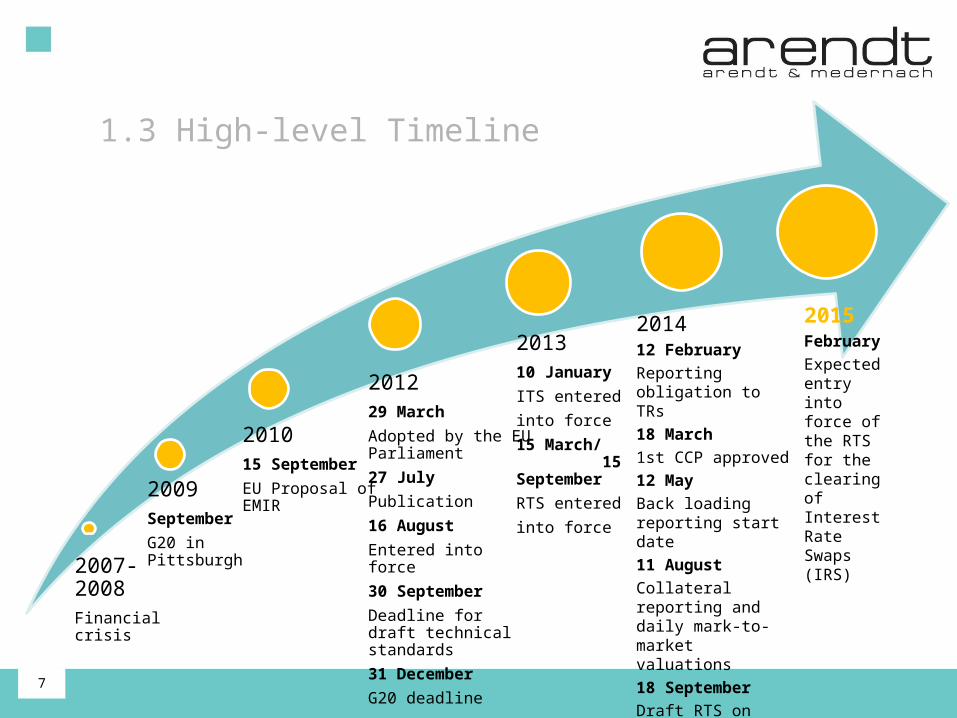

1.3 High-level Timeline

2007-2008Financial crisis

2009September

G20 in Pittsburgh

2010 15 September

EU Proposal of EMIR

2012 29 March

Adopted by the EU Parliament

27 July

Publication

16 August

Entered into force

30 September

Deadline for draft technical standards

31 December

G20 deadline

201412 February

Reporting obligation to TRs

18 March

1st CCP approved

12 May

Back loading reporting start date

11 August

Collateral reporting and daily mark-to-market valuations

18 September

Draft RTS on clearing

2013 10 January

ITS entered

into force

15 March/ 15 September

RTS entered

into force

2015February

Expected entry into force of the RTS for the clearing of Interest Rate Swaps (IRS)

8

2. General Overview

9

© A

rend

t &

Med

erna

ch 2

014

2. General overview

2.1 Legal framework

2.2 Some legal texts regarding clearing

2.3 Recap

2.4 Scope

Table of Contents

10

2.1 Legal framework (1/2)

Penalties

Development of ITS and RTS

EMIR Regulation

11

2.1 Legal framework (2/2)

12

© A

rend

t &

Med

erna

ch 2

014

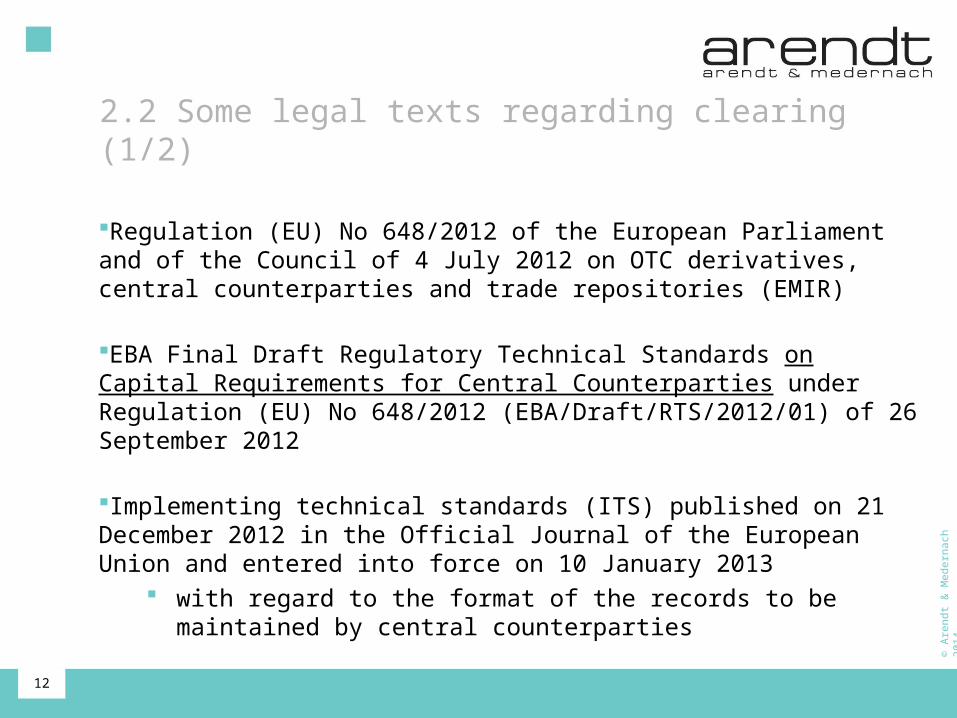

2.2 Some legal texts regarding clearing (1/2)

Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories (EMIR)

EBA Final Draft Regulatory Technical Standards on Capital Requirements for Central Counterparties under Regulation (EU) No 648/2012 (EBA/Draft/RTS/2012/01) of 26 September 2012

Implementing technical standards (ITS) published on 21 December 2012 in the Official Journal of the European Union and entered into force on 10 January 2013

with regard to the format of the records to be maintained by central counterparties

13

© A

rend

t &

Med

erna

ch 2

014

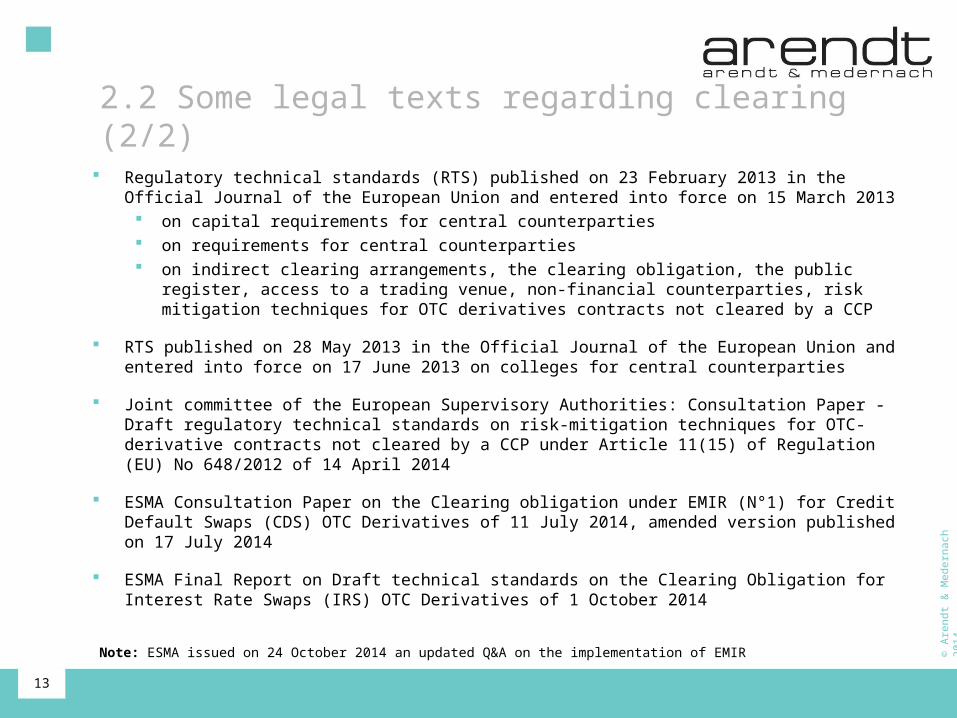

2.2 Some legal texts regarding clearing (2/2)

Regulatory technical standards (RTS) published on 23 February 2013 in the Official Journal of the European Union and entered into force on 15 March 2013 on capital requirements for central counterparties on requirements for central counterparties on indirect clearing arrangements, the clearing obligation, the public register, access to a

trading venue, non-financial counterparties, risk mitigation techniques for OTC derivatives contracts not cleared by a CCP

RTS published on 28 May 2013 in the Official Journal of the European Union and entered into force on 17 June 2013 on colleges for central counterparties

Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 of 14 April 2014

ESMA Consultation Paper on the Clearing obligation under EMIR (N°1) for Credit Default Swaps (CDS) OTC Derivatives of 11 July 2014, amended version published on 17 July 2014

ESMA Final Report on Draft technical standards on the Clearing Obligation for Interest Rate Swaps (IRS) OTC Derivatives of 1 October 2014

Note: ESMA issued on 24 October 2014 an updated Q&A on the implementation of EMIR

14

© A

rend

t &

Med

erna

ch 2

014

2.3 Recap

Trade repositoryTrade repository

Derivative contractsDerivative contracts

Clearing / risk-mitigation obligation

Clearing / risk-mitigation obligation

Reporting obligationretrospective

Reporting obligationretrospective

ESMAESMA

Clearing member

ClearingClearingRisk mitigationRisk mitigation

All derivative contracts

OTC derivative contracts

CCPCCP

Client

Systemic risk monitoring Systemic risk reduction

Increase of market and price transparency

Mitigation of counterparty and operational risk

15

2.4 Scope

Non EU Entities

Financial Counterparty

FCBanks, Insurances,

investment firms, UCITS, pension funds, AIFs

Financial Counterparty

FCBanks, Insurances,

investment firms, UCITS, pension funds, AIFs

Non Financial CounterpartyNon Financial Counterparty

NFC +“Systemically

important” Non-Financial

Counterparty entering into “non-

hedging” activities in derivatives above

the clearing threshold

NFC +“Systemically

important” Non-Financial

Counterparty entering into “non-

hedging” activities in derivatives above

the clearing threshold

EU Entities

NFC -Not “systemically important” Non-

Financial Counterparty entering into

derivatives positions for “hedging” activities only

NFC -Not “systemically important” Non-

Financial Counterparty entering into

derivatives positions for “hedging” activities only

Exemptions: - Bank of International Settlements, member of ESCB and other entities involved with the management of public debt

- Pension scheme arrangements (until 5/08/15)

- Intragroup transactions (on a permanent basis)

Exemptions: - Bank of International Settlements, member of ESCB and other entities involved with the management of public debt

- Pension scheme arrangements (until 5/08/15)

- Intragroup transactions (on a permanent basis)

Non EU counterparties that would be subject to the

clearing obligation if they were established in the Union will have to clear

relevant OTC transactions via CCPs if the contract has

a direct, substantial and foreseeable effect within the

Union

16

3. Clearing

17

© A

rend

t &

Med

erna

ch 2

014

3. Clearing

3.1 Simple example

3.2 General overview

3.3 Client clearing structure chart

3.4 Simple contractual overview

3.5 OTC derivatives subject to clearing

3.5.1 Who decides which OTC derivatives must be

cleared?

3.5.2 OTC derivatives subject to clearing

Table of Contents

18

© A

rend

t &

Med

erna

ch 2

014

3.5.3 Market participants for whom central clearing will become mandatory based on ESMA’s Final Report

3.5.4 Frontloading

3.5.5 Further outlook

3.6 Non-financial counterparties and clearing

3.6.1 When do non-financial counterparties have to comply with the clearing obligation?

3.6.2 Non-financial counterparties: obligation and threshold

3.7 Central counterparties (CCPs)

3.7.1 Central counterparties (CCPs) – Overview

3.7.2 List of CCP’s authorised to offer services and activities in the Union

Table of Contents

19

© A

rend

t &

Med

erna

ch 2

014

3.8 Margin requirements

3.8.1 Margin requirements for non-centrally cleared OTC derivatives

3.8.2 Margin requirements for centrally cleared OTC derivatives

Table of Contents

20

© A

rend

t &

Med

erna

ch 2

014

3.1 Simple example

A and B might be a FC and / or a NFC

Central counterparty (CCP) means a legal person that interposes itself between the counterparties to the contracts traded on one or more financial markets, becoming the buyer to every seller and the seller to every buyer

Clearing means the process of establishing positions including the calculation of net obligations, and ensuring that financial instruments, cash, or both, are available to secure the exposures arising from those positions

Financial counterparty (FC) means investment funds, credit institutions, insurance/reinsurance undertakings, UCITS, AIFs and pension funds

Non-financial counterparty (NFC) means an undertaking established in the Union other than FCs

Simple bilateral trade:Simple bilateral trade: Cleared trade:Cleared trade:

21

© A

rend

t &

Med

erna

ch 2

014

Party B (Indirect Client)

Client

Clearing Member

CCP

Party A

(Clearing Member)

Party A

(Clearing Member)

CCP

Party B

(Client of Clearing Member)

Clearing Member

Client clearing:Client clearing: Indirect client clearing:Indirect client clearing:

3.2 General overview

22

3.3 Client clearing structure chart (1/3)

Party A

(Clearing Member)

CCP

Party B

(Client of Clearing Member)

Clearing Member

Party B’s Clearing Member is Party A

So in fact there is only 1 Clearing Member i.e. Party A

Party A holds its own account separate from the account held for Party B

So there is, at Clearing Member level, an internal segregation between Party A’s and Party B’s Account

23

3.3 Client clearing structure chart (2/3)

CCP

Party B

(Client of Clearing Member)

Clearing Member

Clearing Member

Party A

(Client of Clearing Member)

Party A and Party B are clearing their transcation via the same Clearing Member

Of course the Clearing Member needs to apply the segregation rules and therefore needs to keep a separate account on behalf of Party A and one on behalf of Party B

24

3.3 Client clearing structure chart (3/3)

CCP

Party B

(Client of Clearing Member)

Clearing Member

Party A

(Client of Clearing Member)

Clearing Member

Party A and Party B are clearing their transaction via different Clearing Members.

25

3.4 Simple contractual overview (1/3)

General Agreement

Appendix for centrally

cleared OTC derivatives

Appendix for non-centrally cleared OTC derivatives

Terms and conditions for business of the individual

CM and CCP

Individual Appendices re. specific CM & Client

26

3.4 Simple contractual overview: ISDA (2/3)

ISDA Master Agreement

ISDA/FOA Client Cleared OTC Derivatives Addendum

ISDA EMIR Protocols

Terms and conditions for business of the individual

CM and CCP

Individual Appendices re. specific CM & Client

27

3.4 Simple contractual overview: BdB DRV* (3/3)

*Bankenverband deutscher Banken (Deutscher) Rahmenvertrag / German Bank Association Master Agreement

*Bankenverband deutscher Banken (Deutscher) Rahmenvertrag / German Bank Association Master Agreement

German Master Agreement for financial Derivative Transactions

(DRV)

Annex to the DRV for transactions to

be cleared by a central

counterparty

EMIR Appendix to the above-

referenced DRV

Terms and conditions for business of the individual

CM and CCP

Individual Appendices re. specific CM & Client

28

3.5.1 Who decides which OTC derivatives must be cleared?

Approach Approach

ESMAESMA

CCP? CCP?

ESMA’s role: Identification of classes of OTC derivatives which should be subject to the clearing obligation but for which no CCP has yet received authorisation.

Top down

Notification that a CCP was authorised to clear a certain class of OTC derivatives

Assessment of the suitability of the notified classes to the clearing obligation

Endorsement of ESMA RTS for those classes of OTC derivatives that should be subject to the clearing obligation

Bottom up

ESMA

Public Register

ESMA

Public Register

Classes of OTC derivatives to be cleared

CCPs authorised to clear or recognised for the purpose of clearing

Date by which clearing obligation takes effect and phase in implementation

Classes of OTC for which CCPs have been authorised to clear

Minimum Remaining maturity

CCPs notified to ESMA by NCAs

NCA NCA CCPCCP

ESMAESMA

EU CommissionEU Commission

Info provider

3.5 OTC derivatives subject to clearing

29

© A

rend

t &

Med

erna

ch 2

014

ESMA published on 1st October 2014 its final report of the draft RTS on the clearing obligation for Interest Rate OTC Derivatives that will be submitted to the European Commission for endorsement.

The third section of the Draft RTS covers the determination of the following interest rate derivatives classes which should be subject to mandatory clearing: Basis swaps denominated in EUR, GBP, JPY, USD; Fixed-to-float swaps denominated in EUR, GBP, JPY, USD; Forward rate agreements denominated in EUR, GBP, USD;

and Overnight index swaps denominated in EUR, GBP, USD.

3.5.2 OTC derivatives subject to clearing

30

© A

rend

t &

Med

erna

ch 2

014

Category 1: Clearing Members of a recognised or authorised CCP listed on the Public Register – 6 months after the RTS enter into force.

Category 2: FC and AIFs that are non-financial counterparties above the clearing threshold (NFCs+), which are not included in Category 1 and which belong to a group for which the aggregate month-end average notional amount of non-centrally cleared derivatives over a certain 3 month period (i.e. the 3 months preceding the entry into force of the RTS, excluding the month of entry into force) is above €8 billions – 12 months after RTS enter into force.

Category 3: FCs and other NFC+ AIFs that have a low level of activity in uncleared derivatives and which are not included in Category 1 or 2 – 18 months after the RTS enter into force.

Category 4: NFCs that are not included in Category 1, 2 or 3 – 36 months after the RTS enter into force.

3.5.3 Market participants for whom central clearing will become mandatory based on ESMA’s Final Report* (1/2)

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

31

© A

rend

t &

Med

erna

ch 2

014

N.B.: Where a contract is entered into between two counterparties included in different categories of counterparties, the date from which the clearing obligation takes effect for that contract shall be the later of the two.

3.5.3 Market participants for whom central clearing will become mandatory based on ESMA’s Final Report* (2/2)

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

32

© A

rend

t &

Med

erna

ch 2

014

The minimum remaining maturity for Categories 1 and 2 counterparties are the same for contracts entered into or novated before the date of publication of the RTS in the Official Journal, 49.5 years for basis swaps and fixed-to-float IRS contracts and 2.5 years for foward rate agreements and overnight index swaps. Contracts entered into or novated on or after the publication of the RTS are subject to a 6 month minimum remaining maturity.

For Category 3 the minimum remaining maturity is 50 years for basis swaps and fixed-to-float IRS classes and 3 years for forward rate agreements and overnight index swaps.

Counterparties falling within Category 4 are not subject to frontloading, e.g. frontloading is not applicable where at least one of the counterparties is a non-financial counterparty (NFC+ or NFC-).

3.5.4 Frontloading*

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

*Source: ESMA Final Report: Draft technical standards on the Clearing Obligation – Interest Rate OTC Derivatives (01/10/2014)

33

© A

rend

t &

Med

erna

ch 2

014

ESMA also published on 1 October a consultation paper on draft RTS it has developed under EMIR for the clearing of foreign-exchange non-deliverable forwards (“ESMA/2014/1185”). This paper provides explanations on the draft regulatory technical standards establishing a clearing obligation on a class of foreign-exchange non-deliverable forward (FX NDF) OTC derivatives.

ESMA is currently also developing regulatory technical standards (RTS) for credit default swaps (CDS) following the same logic as for the interest rate swaps (IRS). These new RTS which will probably be submitted to the European Commission for endorsement in the near future.

3.5.5 Further outlook

34

© A

rend

t &

Med

erna

ch 2

014

3.6.1 When do non-financial counterparties have to comply with the clearing obligation?

Clearing thresholds values for the purpose of the clearing obligation:

Breach of threshold in one product class entails breach in all classes

derivative contracts threshold

credit derivative EUR 1 billion in gross notional value

OTC equity derivative EUR 1 billion in gross notional value

OTC interest rate derivative EUR 3 billion in gross notional value

OTC foreign exchange derivative EUR 3 billion in gross notional value

OTC commodity derivative and all other OTC derivatives

EUR 3 billion in gross notional value

3.6 Non-financial counterparties and clearing

35

© A

rend

t &

Med

erna

ch 2

014

3.6.2 Non-financial counterparties: obligation and threshold

Qualified as Financial Counterparty

(Investment firm; credit institution; insurance undertaking; assurance undertaking; reinsurance undertaking; UCITS; AIF)?

Qualified as Financial Counterparty

(Investment firm; credit institution; insurance undertaking; assurance undertaking; reinsurance undertaking; UCITS; AIF)?

Has the OTC derivative class been defined by ESMA to be subject to the clearing obligation?

Do the positions in OTC derivative contracts exceed the thresholds?

Clearing by a CCPClearing by a CCP

Has the OTC derivative class been defined by ESMA to be subject to the clearing obligation?

Risk MitigationRisk Mitigation

Yes No

NoYes

NoYes

No

Yes

36

© A

rend

t &

Med

erna

ch 2

014

Conduct of Business Participation requirements Transparency Segregation and portability

Prudential requirements Exposure management Margin requirements Default fund Liquidity risk controls Default waterfall Collateral requirements Investment policy Default procedures Review models, stress testing and back testing Settlement

3.7.1 Central counterparties (CCPs) - Overview

3.7 Central counterparties (CCPs)

37

© A

rend

t &

Med

erna

ch 2

014

No

Name of the CCP Identification Code of CCP (LEI)

Established in the Union or in a Third Country

Country of establishment

Competent authority (if established in the Union)

Date of authorisation

1

Nasdaq OMX Clearing AB 54930002A8LR1AA UCU78

In the Union

Sweden

Finansinspektionen

18 March 2014

2 European CentralCounterparty N.V.

724500937F740MH CX307

In the Union

Netherlands

De NederlandscheBank (DNB)

1 April 2014

3

KDPW_CCP 2594000K576D5CQ XI987

In the Union

Poland

Komisja NadzoruFinansowego (KNF)

8 April 2014

4

Eurex Clearing AG

529900LN3S50JPU47S06

In the Union

Germany

Bundesanstalt für Finanzdienstleistungs aufsicht

(Bafin)

10 April 2014

5

Cassa di Compensazione eGaranzia S.p.A. (CCG)

8156006407E264D

In the Union

Italy

Banca d’Italia

20 May 2014

6

LCH.Clearnet SA

R1IO4YJ0O79SMW VCHB58

In the Union

France

Autorité de Contrôle Prudentiel et de Résolution

(ACPR)

22 May 2014

7

European CommodityClearing

529900M6JY6PUZ9

In the Union

Germany

Bundesanstalt für Finanzdienstleistungs aufsicht

(Bafin)

11 June 2014

8

LCH.Clearnet Ltd

F226TOH6YD6XJB17KS62

In the Union UnitedKingdom

Bank of England

12 June 2014

3.7.2 List of CCP’s authorised to offer services and activities in the Union (1/2)

Source: ESMA List of Central Counterparties authorised to offer services and activities in the Union (03/11/2014)

Source: ESMA List of Central Counterparties authorised to offer services and activities in the Union (03/11/2014)

38

© A

rend

t &

Med

erna

ch 2

014

9

Keler CCP

529900MHIW6Z8O TOAH28

In the Union

Hungary Central Bank ofHungary (MNB)

4 July 2014

10

CME Clearing Europe Ltd 6SI7IOVECKBHVY BTB459

In the Union UnitedKingdom

Bank of England

4 August 2014

11CCP Austria

Abwicklungsstelle für Börsengeschäfte GmbH

(CCP.A)

529900QF6QY66Q

In the Union

Austria

Austrian Financial Market Authority (FMA)

14 August 2014

12

LME Clear Ltd

213800L8AQD59D3JRW81

In the Union UnitedKingdom

Bank of England

3 September 2014

13

BME Clearing

5299009QA8BBE2OOB349

In the Union

Spain

Comisión Nacional del Mercado de Valores

(CNMV)

16 September 2014

14

OMIClear - C.C., S.A.

5299001PSXO7X2J X4W10

In the Union

PortugalComissão do Mercado de Valores Mobiliários

(CMVM)

31 October 2014

3.7.2 List of CCP’s authorised to offer services and activities in the Union (2/2)

Source: ESMA List of Central Counterparties authorised to offer services and activities in the Union (03/11/2014)

Source: ESMA List of Central Counterparties authorised to offer services and activities in the Union (03/11/2014)

39

© A

rend

t &

Med

erna

ch 2

014

This concerns FCs and NFCs+, hereafter referred to as ‘Counterparties’.

Counterparties requirement to exchange variation margin (VM) on a daily basis and in full should apply from 1 December 2015 (in line with international standards, i.e. BCSBS-IOSCO framework).

Counterparties may agree that where the total initial margin (IM) calculated to be exchanged for all non-centrally cleared OTC derivatives between counterparties at group level is equal to or lower than € 50 million, they may agree that no initial margin will be exchanged and that they will hold capital against their exposure to their counterparties.

Counterparties may agree not to post IM or VM where the total collateral to be exchanged between them is less than or equal to € 500.000.

IM will be posted gross on a counterparty potfolio (in contrast to net for cleared trades).

3.8.1 Margin requirements for non-centrally cleared OTC derivatives* (1/3)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

3.8 Margin requirements

40

© A

rend

t &

Med

erna

ch 2

014

IM requirements don’t apply to transactions where at least one of the counterparties aggregate month-end average notional amounts of non-centrally cleared derivatives for June, July and August in a given year is below € 8 billion.

Physically settled FX fowards and swaps including those associated with the exchange of principal in currency swaps are to be exempt from IM requirements. VM is still applicable to such contracts.

Covered bonds issues and covered pools don’t need to post IM or VM in case certain conditions are satisfied.

The IM requirements apply to all new contracts entered into from 1 December 2015. No mandatory retrospective application.

Re-hypothecation of IM should not be permitted.

Eligible collaterall which meets the IM and VM requirements includes cash, high quality government and corporate bonds, shares in major stock indices and gold.

3.8.1 Margin requirements for non-centrally cleared OTC derivatives* (2/3)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

41

© A

rend

t &

Med

erna

ch 2

014

IM requirements to be phased in as follows:

From 01/12/15 to 30/11/16: any counterparty belonging to a group whose aggregate month-end average notional amount of non-centrally cleared derivatives for June, July and August 2015 exceeds € 3 trillion.

From 01/12/16 to 30/11/17: any (…) August 2016 exceeds € 2.25 trillion.

From 01/12/17 to 30/11/18: any (…) August 2017 exceeds € 1.5 trillion.

From 01/12/18 to 30/11/19: any (…) August 2017 exceeds € 0.75 trillion.

From 01/12/19 on: any (…) August 2017 exceeds € 8 billion.

3.8.1 Margin requirements for non-centrally cleared OTC derivatives* (3/3)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

42

© A

rend

t &

Med

erna

ch 2

014

Eligible collaterall which meets the IM and VM requirements includes cash, high quality government and corporate bonds, shares in major stock indices and gold.

The amount which has to be transferred as IM is being determined by the concerned CCP. It should however be enough to collateralise the underlying transaction.

The amount which has to be transferred as VM is being determined by the concerned CCP. It should however be enough to collateralise the underlying transaction.

3.8.2 Margin requirements for centrally cleared OTC derivatives*

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

*Source: Joint committee of the European Supervisory Authorities: Consultation Paper -Draft regulatory technical standards on risk-mitigation techniques for OTC-derivative contracts not cleared by a CCP under Article 11(15) of Regulation (EU) No 648/2012 (14/04/2014)

43

4. EU regulatory framework for securities market infrastructure

44

© A

rend

t &

Med

erna

ch 2

014

4. EU regulatory framework for securities market infrastructure

4.1 EU regulatory framework for securities market infrastructure

4.2 EMIR & MiFID II – the overlap

Table of Contents

45

© A

rend

t &

Med

erna

ch 2

014

EMIR together with MiFID II (& CSDR) are anticipated to enhance the safety and soundness of the financial system.

They will form the framework in which systematically important securities infrastructures are subject to common rules on a European level.

4.1 EU regulatory framework for securities market infrastructure (1/2)

46

© A

rend

t &

Med

erna

ch 2

014

Step 1: MiFID II & MiFIR regulate trading venues, i.e. MTFs*, OTFs**, where trading takes place;

Step 2: EMIR regulates central counterparties; and

Step 3: CSDR regulates central securities depositories, who are responsible for settlement of securities transactions.

4.1 EU regulatory framework for securities market infrastructure (2/2)

*Multilateral trading facilities

** Organised trading facilities

*Multilateral trading facilities

** Organised trading facilities

47

© A

rend

t &

Med

erna

ch 2

014

G20 agreed that trading in standardised OTC derivatives: (i) should move to exchanges or electronic trading platforms,

where appropriate (MiFID II) and (ii) should be cleared through central counterparties (EMIR). The provisions in MiFID II require trading in suitably developed

derivatives to occur only on eligible platforms, that is, RMs*, MTFs, or OTFs**. This requirement is consistent with the requirement to central clearing OTC derivatives under EMIR.

Article 29 (1) MiFIR requires the operator of a regulated market to ensure that all transactions in derivatives that are concluded on that regulated market to be cleared by a CCP.

4.2 EMIR & MiFID II – the overlap

* Regulated markets

** Article 28 MiFID II

* Regulated markets

** Article 28 MiFID II

49

APPENDIX

50

© A

rend

t &

Med

erna

ch 2

014

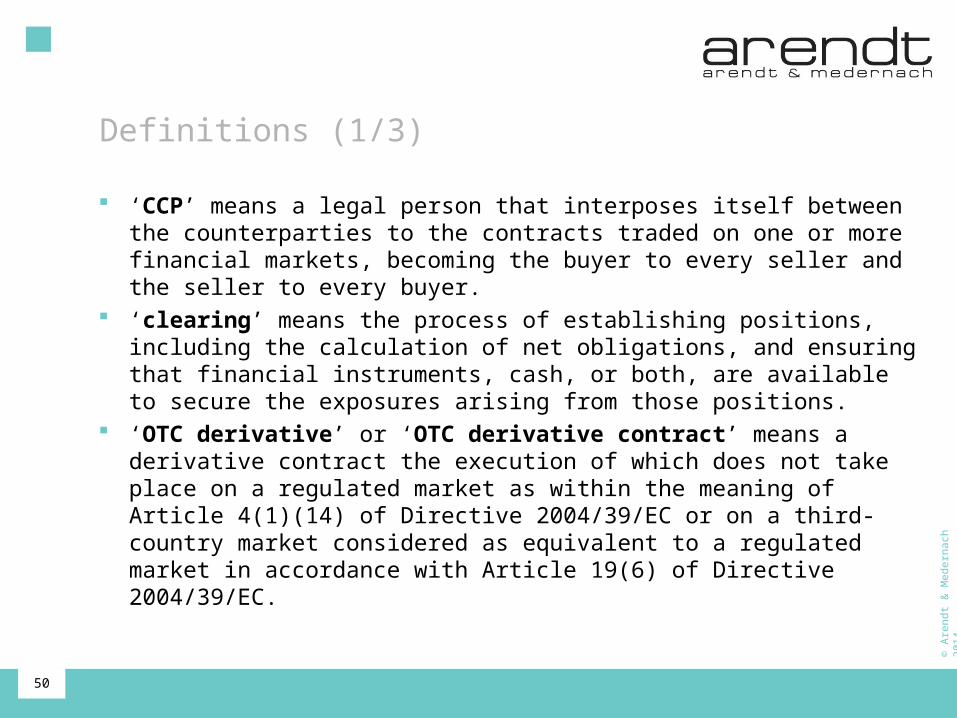

‘CCP’ means a legal person that interposes itself between the counterparties to the contracts traded on one or more financial markets, becoming the buyer to every seller and the seller to every buyer.

‘clearing’ means the process of establishing positions, including the calculation of net obligations, and ensuring that financial instruments, cash, or both, are available to secure the exposures arising from those positions.

‘OTC derivative’ or ‘OTC derivative contract’ means a derivative contract the execution of which does not take place on a regulated market as within the meaning of Article 4(1)(14) of Directive 2004/39/EC or on a third- country market considered as equivalent to a regulated market in accordance with Article 19(6) of Directive 2004/39/EC.

Definitions (1/3)

51

© A

rend

t &

Med

erna

ch 2

014

‘financial counterparty’ means an investment firm authorised in accordance with Directive 2004/39/EC, a credit institution authorised in accordance with Directive 2006/48/EC, an insurance undertaking authorised in accordance with Directive 73/239/EEC, an assurance undertaking authorised in accordance with Directive 2002/83/EC, a reinsurance undertaking authorised in accordance with Directive 2005/68/EC, a UCITS and, where relevant, its management company, authorised in accordance with Directive 2009/65/EC, an institution for occupational retirement provision within the meaning of Article 6(a) of Directive 2003/41/EC and an alternative investment fund managed by AIFMs authorised or registered in accordance with Directive 2011/61/EU.

‘non-financial counterparty’ means an undertaking established in the Union other than ‘CCP’ and ‘FC’.

Definitions (2/3)

52

© A

rend

t &

Med

erna

ch 2

014

‘clearing member’ means an undertaking which participates in a CCP and which is responsible for discharging the financial obligations arising from that participation.

‘MiFID II’ means Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (recast).

‘MiFIR’ means Regulation (EU) No 600/2014 of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Regulation (EU) No 648/2012.

‘CSDR’ means Regulation (EU) No 909/2014 of the European Parliament and of the Council of 23 July 2014 on improving securities settlement in the European Union and on central securities depositories and amending Directives 98/26/EC and 2014/65/EU and Regulation (EU) No 236/2012

Definitions (3/3)

53

© A

rend

t &

Med

erna

ch 2

014

Thank you for your attention

Thank you for your attention!

The information provided in this presentation shall give you an overview of the legal and regulatory requirements in Luxembourg and the European Union without being claimed to be exhaustive or being considered as legal advice. Arendt & Medernach has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied.

No part of this presentation may be published, reproduced, transmitted or otherwise distributed in any form or by any means, e.g. electronic or mechanical, without the written permission of the author.

Contact us

Henning Schwabe Partner Investment Management Tel : (+352) 4078 78 525 Email : [email protected]