THE INVESTOR VOLUME 5 ISSUE 6 June 2012

poor companies - richmultiples, Pg. 18

how do you do infosyspg. 16

Niveshak

FINANCIAL WOES OF INDIA’S RISING SUN

Disclaimer: The views presented are the opinion/work of the individual author and The Finance Club of IIM Shillong bears no responsibility whatsoever.

F R O M E D I T O R ’ S D E S K

NiveshakVolume VISSUE VI

June 2012

Faculty MentorProf. N. Sivasankaran

Editorial TeamAkanksha BehlAkhil Tandon

Chandan GuptaHarshali Damle

Kailash V. MadanNilkesh Patra

Rakesh Agarwal

Creative TeamAnuroop Bhanu

Venkata Abhiram M.

All images, design and artwork are copyright of

IIM Shillong Finance Club

©Finance ClubIndian Institute of Management

Shillong

www.iims-niveshak.com

THE TEAM

Dear Niveshaks,

The month of June has witnessed some major financial events that are likely to shape the future of economic development globally. The fear of a dramatic Grexit that kept the world on edge has finally subsided for some time after Greece election results. The emergence of pro-Europe parties in the Greece’s election should relax fears that a country will leave the euro for the first time and unleash global financial turmoil. How-ever, the slim majority won by pro-bailout parties in Greece elections and worries about the Spain’s fiscal and banking problems kept tensions high.

Another major event this month has been the meeting of the G20 members in Las Cabos, Mexico. The dangers that Europe’s escalating debt crisis would drive the global economy back into recession for the second time in less than four years domi-nated the summit of G20 leaders of industrialized and developing nations, which rep-resent over 80 per cent of world output. European countries showed at the Group of 20 summit that they were considering major steps to integrate their banking sectors so as to break the cycle of highly indebted countries and rescue their banks, which only pushes governments ever deeper into debt.

This year’s meeting of United Nations Conference on Sustainable Development dubbed Rio+20 aimed at setting an agenda for policymakers to act in the coming de-cades, and promote cuts in fossil-fuel subsidies, support for the use of renewable en-ergy and measures to protect oceans. However, as any agreement will have no force as a treaty, the Rio +20 ended with a whimper rather than a bang compared to the legacy of its predecessor, the 1992 Rio Earth Summit, which led to major conventions on climate change and biodiversity.

In India, RBI kept policy rates unchanged in its mid-quarter monetary policy review because of high headline inflation. The market indices reacted negatively to the news. In spite of a sharper than expected rate cut of 50 basis points in April, slowdown in activity, particularly in investment, showed that the role of interest rates is relatively small and a further rate cut could exacerbate inflationary pressures rather than spur growth. The RBI stance had another adverse impact causing rupee to depreciate to 55.83/84 to a dollar on the day of the review and to its all-time low of 57.12 against the dollar days later.

In another major development, Standard & Poor’s warned that India could be-come the first BRIC economy to lose its investment-grade credit rating. In a similar move, Fitch added further insult to injury by revising India’s outlook from stable to negative at BBB-.

This issue brings to you some more interesting and insightful reads. The cover story this month focuses on financial woes of solar power in India. The issue also fea-tures articles on regulations in Insider Trading in India, company valuations and im-plications of regulating propriety trading of financial institutions. The Classroom this month explains the nuances of Leveraged Buyout.

We would also like to thank our readers for their constant support through won-derful articles and appreciation. It is your endless encouragement and enthusiasm that keeps us going.

Kindly send in your suggestions and feedback to [email protected] and as always,

Stay invested.

Team Niveshak

C O N T E N T S

Niveshak Times04 The Month That Was

Article of the month 08 Is India Ready to Fight Insider Trading ?

Cover Story

11 Financial Woes of India’s Rising Sun

Perspective 16 How Do You Do Infosys?

FinGyaan

18 Sir Volcker vs. Prop Trading

Finsight18 Poor Companies - Rich Multiples

CLASSROOM21 Leveraged Buyout (LBO)

May 2012

May WPI inches up to 7.55% and CPI rises to 10.36% Country’s benchmark inflation rate rose to 7.55% in May as a result of elevated food and fuel pric-es. A jump of 0.22% in WPI matched the expec-tations in Reuters Poll. Core inflation, which ex-cludes volatile food and fuel prices, was around 5% in May. Finance Minister talking to reporters on Thursday said “core inflation falling is a silver lining.” He said good monsoon will help ease pressure on inflation and was confident that in-flation will be in the range of 6.5% to 7.5% in FY13.

At the same time Consumer Price Inflation stood at 10.36% up from 10.26% in April, as a result of high vegetable, egg, meat, fish, oil and fat prices. In the urban areas annual inflation based on the CPI stood at 11.52% while in rural areas it remained in single digit at 9.57%. In April in-flation based on the CPI in rural areas stood at 9.67% while in urban areas it was at 11.10%.

Europe crisis: Spanish short-term debt costs reach record levelsSpain, the euro zone’s fourth larg-est economy, had to pay 5.07 percent to sell 12-month Treasury bills and 5.11 percent to sell 18-month paper on June 19 - an increase of about 200 basis points on the last auction for the same maturities a month ago. Spain inched closer to becoming the largest euro zone coun-try to be shut out of credit markets when it had to pay a record price to sell its short-term bor-rowing instruments. The soaring short term bor-rowing yields showed that Europe’s troubles are much bigger and deeper than just Greece and a considerable action is now needed to tame two-and-a-half year old European debt crisis. Span-ish Economy Minister Luis de Guindos, attending G20 summit, told reporters that Madrid’s poli-cies were not to blame for the loss of investor confidence. “We think ... that the way markets

are penalising Spain today does not reflect the efforts we have made or the growth potential of the economy,” he said. “Spain is a solvent coun-try and a country which has a capacity to grow.”

IIP in April was worse than anticipatedReduction in capital goods and shrinkage in man-ufacturing output in April has resulted in a IIP at 0.1% versus -3.5% in March. This is worse than what was expected. The slowdown in growth of factory output was expected to force RBI to cut interest rates but RBI kept the rates unchanged in their quarterly mid-term review on June 18. The unexpected lower IIP and unchanged inter-est rates are expected to put more pressure on Indian Economy which is already suffering from twin problems of lower GDP growth rate and higher inflation.

Indian economy is in stagflation: Moody’sGlobal financial services firm Moody’s, on June 14, said that Indian economy is facing stagfla-tion. “India’s economy is in stagflation, with no-tably weaker growth but inflation still stubborn-ly high,” said Glenn Levine, Senior Economist, Moody’s Analytics. As per Moody, the recent plunge in the rupee is pushing up the price, es-pecially imported goods and commodities priced in US dollar and combined with slower GDP growth, this has led to the situation of stagfla-tion for Indian economy. It further said with the rupee, sitting 15 per cent below its peak of late-February, will ensure that WPI inflation remains in the 7 per cent to 8 per cent range for another six months. “Indeed, with the growth side of the economy slowing, the risks have shifted sharply towards growth and they (the RBI and other pol-icy makers) should just grin and bear the higher inflation numbers,” it added

RBI Governor announces Mid Term re-view, disappoints industry with no rate cuts The Reserve Bank of India (RBI) announced its mid-term credit policy review here on June 18, and against the industry expectations, kept the short term lending rate and the Cash Reserve

The Niveshak Times

www.iims-niveshak.com

IIM, ShillongTeam NIVESHAK

NIVESHAK4T

he

Mon

th T

hat

Was

Ratio (CRR) unchanged at 8 and 4.75 percent re-spectively. Industry expected RBI to bring down the repo rate by at least 0.25-percentage point to 7.75 percent, and the Cash Reserve Ratio (CRR) up by 1 percentage point. “Our assess-ment of the current growth-inflation dynamic is that there are several factors responsible for the slowdown in activity, particularly in investment, with the role of interest rates being relatively small. Consequently, further reduction in the policy interest rate at this juncture, rather than supporting growth, could exacerbate inflationary pressures,” the RBI said in a statement. RBI, tar-geting GOI, also said that government has failed to follow the path of fiscal consolidation while it is trying its best to link monetary policy with fiscal policy. Finance Minister Pranab Mukherjee said high inflation weighed on RBI’s mind but Commerce and Industry Minister Anand Sharma expressed his anguish over RBI choosing a sta-tus quo when the industrial growth was down. Stock market reacted strongly to the announce-ment and tanked, suffering a loss of 244 points at closing.

India’s stand on infrastructure invest-ment sanctioned by G20

The G20 meeting held re-cently in Mexico concluded with an approval of In-dia’s stand on investment in infrastructure by the leaders that included US President Barack Obama, German Vice Chancellor

Angela Morkel, Chinese Prime Minister Wen Jia-bao and Russian President Vladimir Putin. The G20 comprises of the world’s prominent and de-veloping economies. India was of the viewpoint that investment in infrastructure is critical for continued growth, worldwide economic retriev-al, poverty reduction and job creation. India re-quires a minimum of $1 trillion in infrastructure in the coming five years. Manmohan Singh an-nounced that the much needed investment in infrastructure in emerging economies can play a crucial role in firming expansion and stimulat-ing the process of recovery world-wide. A clear

communication was given that growth cannot be overlooked and while austerity is important for countries facing too much debt, surplus nations must counter it with expansion. The affirmation also had other observations which were in line with what was being pushed for by Indian debat-ers at G20 Summits and other forums.

Indian money has risen after five years in Swiss BanksAt the end of 2011, the amount of money held by Indians in Swiss banks totalled 2.18 billion Swiss francs. This figure has risen for the first time in the last five years. The latest data by the Swiss National Bank has revealed that the total fund is inclusive of 2.025 billion Swiss francs held direct-ly by the Indian individuals and 158 million held through fiduciaries or wealth managers. This fig-ure does not indicate the much-debated alleged black money held by Indians in safe tax havens of Switzerland. Also, the figure is exclusive of money held by Indians in the names of others. The quantum of funds by Indians in Swiss banks has last increased in 2006 by over 1 billion Swiss francs but fell to less than one third by the end of year 2010.

SBI does not agree to RBI’s move to pre-vent Rupee from falling

RBI has directed the oil companies to purchase half of their dollar requirements directly from a selected group of PSU banks as they believe that this move would prevent the Rupee from falling. It maintains that this would help check volatility and seize the free-fall of the rupee. However, State Bank of India stated that it doesn’t think that such a move would increase the overall availability of dollar or en-hance the rupee-dollar prices and considers the move to be a step by the RBI to keep away the criticism that RBI is not doing enough.

The Niveshak Times

www.iims-niveshak.com 5NIVESHAKT

he M

onth

Th

at Was

© FINANCE CLUB, INDIAN INSTITUTE OF MANAGEMENT SHILLONG

June 2012

6C

over

Sto

ryNIVESHAK6

Art

icle

of t

he M

onth

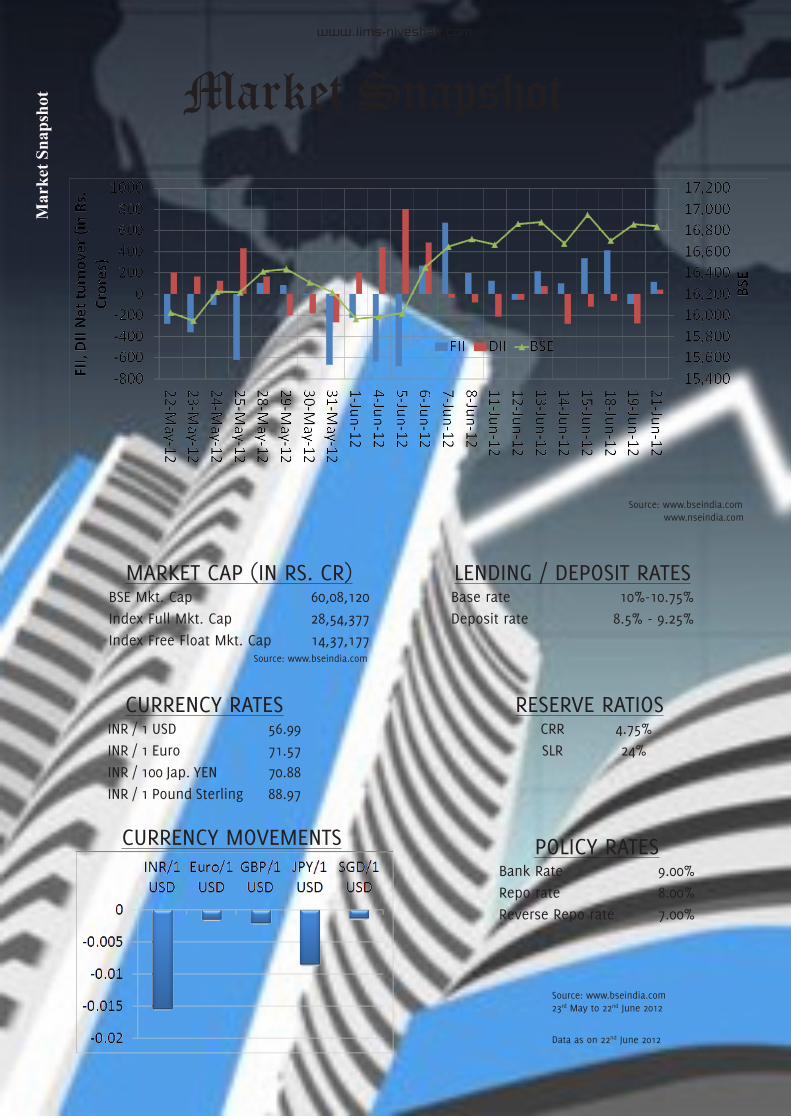

MARKET CAP (IN RS. CR)BSE Mkt. Cap 60,08,120Index Full Mkt. Cap 28,54,377Index Free Float Mkt. Cap 14,37,177

CURRENCY RATESINR / 1 USD 56.99INR / 1 Euro 71.57INR / 100 Jap. YEN 70.88INR / 1 Pound Sterling 88.97

POLICY RATESBank Rate 9.00%Repo rate 8.00%Reverse Repo rate 7.00%

Market Snapshotwww.iims-niveshak.com

RESERVE RATIOSCRR 4.75%SLR 24%

LENDING / DEPOSIT RATESBase rate 10%-10.75%Deposit rate 8.5% - 9.25%

Source: www.bseindia.com www.nseindia.com

Source: www.bseindia.com

Source: www.bseindia.com23rd May to 22nd June 2012

Data as on 22nd June 2012

Mar

ket S

naps

hot

CURRENCY MOVEMENTS

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

7C

over Story

NIVESHAK 7A

rticle of the Month

7C

over Story

NIVESHAK 7M

arket Snapshot

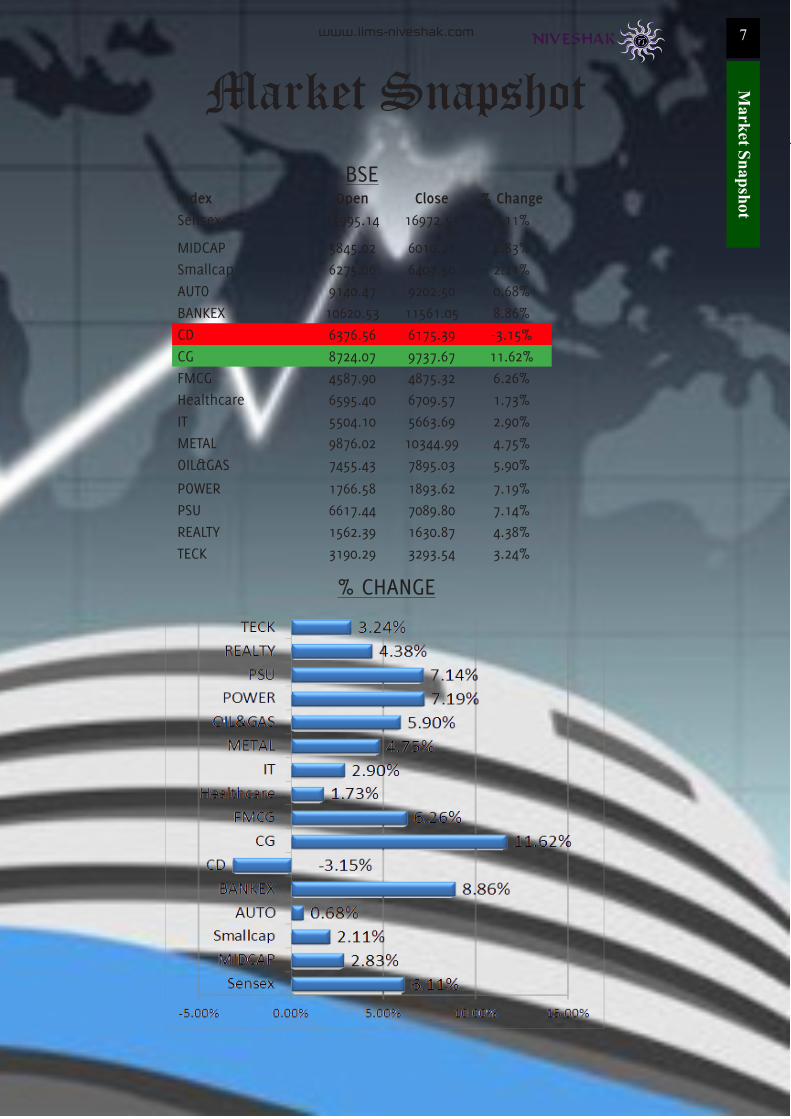

BSEIndex Open Close % ChangeSensex 15995.14 16972.51 6.11%

MIDCAP 5845.02 6010.21 2.83%Smallcap 6275.06 6407.50 2.11%AUTO 9140.47 9202.50 0.68%BANKEX 10620.53 11561.05 8.86%CD 6376.56 6175.39 -3.15%CG 8724.07 9737.67 11.62%FMCG 4587.90 4875.32 6.26%Healthcare 6595.40 6709.57 1.73%IT 5504.10 5663.69 2.90%METAL 9876.02 10344.99 4.75%OIL&GAS 7455.43 7895.03 5.90%

POWER 1766.58 1893.62 7.19%PSU 6617.44 7089.80 7.14%REALTY 1562.39 1630.87 4.38%TECK 3190.29 3293.54 3.24%

www.iims-niveshak.com

Market Snapshot

% CHANGE

June 2012

8C

over

Sto

ryNIVESHAK8

Art

icle

of t

he M

onth

8C

over

Sto

ry

All of us, as investors seek the best avenues to invest our hard earned money. As a prerequisite to this, we expect the equity markets we invest in to be free of any manipulation or bias. How-ever, there have been an increasing number of cases where board members or top executives of companies have manipulated the markets purely on the basis of certain information privy to them. Such acts of insider trading are growing in number and if not acted upon swiftly could deprive regular investors of a clean and an ef-ficient market.

Insider trading is the buying, selling or dealing in the securities of a listed company by a di-rector, member of the management, employee of the company, or by any other person such as internal auditor, advisor, consultant, analyst etc., who has material and non-public informa-tion. One of the most common indications of insider trading is the spike in stock prices ahead of some important corporate announcement, especially mergers and acquisitions.

To put the entire scenario in perspective, we can consider the case of the United States.

The Indian born Managing Director of McKinsey & Co, Rajat Gupta, was recently found guilty on three cases of securities fraud and one case of

conspiracy. He, along with his business partner Anil Kumar and close friend Raj Rajaratnam, the Sri Lankan born head of the Galleon group are believed to have indulged in insider trading and are now held guilty by the law. Mr. Gupta could face up to 20 years in prison, proving that no corporate honcho is above the law in the US.

As much as it’s against the law for company ex-ecutives to profit from inside information, these laws seldom apply to the Congress.

They call their Congress members “representa-tives,” but they are far wealthier and live far different lives than those they are supposed to represent. Election to the House or Senate puts members in esteemed company, replete with respect and perks most of their constituents can barely imagine. And since wealth accompanies power, that means they are often surrounded by wealthy people, who invite them to restaurants, golf clubs and resorts frequented by the very rich.

The wealth gap and disparity between Congress members and their constituents appears to be growing. A recent New York Times analysis of public records found that nearly half of the members of the House and Senate are now mil-lionaires. And while many Americans have lost

8A

rtic

le o

f th

e M

onth

NIVESHAK

IIM ShIllongKailash V. Madan

Is Indiaready to fight

Insider

Trading ?

One of the most common indications of insider trading is the spike in stock prices ahead of some important corporate announcement, especially mergers and acquisitions.

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

9C

over Story

NIVESHAK 9A

rticle of the Month

9C

over Story

9A

rticle of the Month

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

9

ground in the last few years, Congress members have gotten wealthier.

There have been several cases where speakers and other politicians have been invited on the ground floor when private companies went pub-lic through their IPO’s. It is not a rare sight to see politicians and bureaucrats make millions from stock market killings.

If the goal is to root out corruption and ensure an information-efficient market, and raise the public’s low opinion of the Congress, the House should ensure that the Senate Bill is applied for everyone in the same effect.

Closer home, in India, any broker, dealer, ana-lyst, securities lawyer or even someone in the

stock market will accept that insider trading is not only rampant on Dalal Street, but also inter-linked with stock trading.

Insider trading was branded as illegal only about two decades ago after the regulator SEBI (Securi-ties and Exchange Board of India) enacted the Prohibition of Insider Trading Regulations, 1992. Earlier, phone calls, emails and internet chats were the preferred mode of communication for sharing information. Nowadays, messages through Blackberry, which make tracking at the source and recipient after deletion impossible in India, has emerged as the preferred medium among market players.

Because of such loopholes, there have been

NIVESHAK 9A

rticle of the M

onth

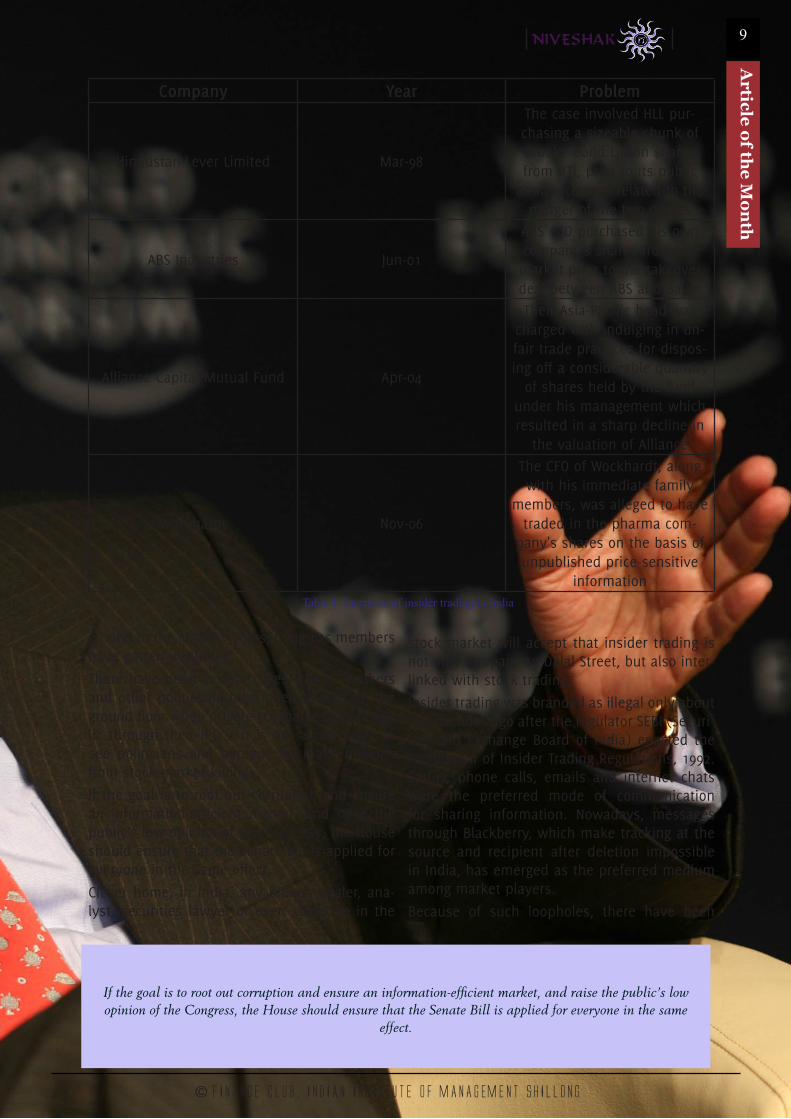

Company Year Problem

Hindustan Lever Limited Mar-98

The case involved HLL pur-chasing a sizeable chunk of Brooke Bond Lipton shares from UTI, prior to its public

announcement related to the merger of the two outfits

ABS Industries Jun-01

ABS' MD purchased his own company's shares from the market prior to the takeover deal between ABS and Bayer

Alliance Capital Mutual Fund Apr-04

Their Asia-Pacific head was charged with indulging in un-fair trade practices for dispos-ing off a considerable quantity

of shares held by the fund under his management which resulted in a sharp decline in

the valuation of Alliance

Wockhardt Nov-06

The CFO of Wockhardt, along with his immediate family

members, was alleged to have traded in the pharma com-

pany's shares on the basis of unpublished price-sensitive

information Table 1: Instances of insider trading in India

If the goal is to root out corruption and ensure an information-efficient market, and raise the public’s low opinion of the Congress, the House should ensure that the Senate Bill is applied for everyone in the same

effect.

June 2012

10C

over

Sto

ryNIVESHAK10

Art

icle

of t

he M

onth

10C

over

Sto

ry10

many instances of stock price manipulation and insider trading on Indian bourses. The most famous example is Hindustan Lever Limited’s purchase of 8 lakh shares of Brooke Bond Lip-ton India days before the announcement of the merger between the two companies. SEBI had initiated criminal action against HLL but the quantum of punishment was mainly monetary and prohibitive in nature.

The more recent case is that of the founder of erstwhile Satyam Computers, Ramalinga Raju, who committed a heinous fraud of nearly 8,000 crore on his shareholders and even admitted to manipulating the company’s accounts. White collar criminals in our country usually go scot-free as there is one set of laws for the rich and powerful and another set for the poor.

Our regulatory bodies, like the SEBI, or even the CBI, are reportedly understaffed. In the case of SEBI, the surveillance system is not as ef-ficient as it should be, making the enforcement against insider trading less effective. However, lately, SEBI has been using market data analyt-ics tools and is also taking vital cues from the Income Tax department, CBI and the Intelligence Bureau to crack down on market manipulators. The market regulator has set up an integrated market surveillance system (IMSS) and a data warehousing and business intelligence system both together capable of generating and recog-nizing patterns from stock prices and volumes to detect crimes like insider trading.

Art

icle

of

the

Mon

thNIVESHAK

FIN-Q SolutionsMay 2012

1. Black Scholes Model

2. JM Hurst, Father of Modern Cyclical Theory

3. VaR

4. Facebook

5. Printed on its coins

6. Payment Float

7. Joint Float

8. Both have indi-ces named after them: Big Mac Index and Hot Waitress Index

9. Bridge Loan

10. Golden Boot

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

11C

over Story

NIVESHAK 11A

rticle of the Month

11NIVESHAK 11

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

11NIVESHAK 11

sive bids, it is a no brainer to assume solar power to be a solution the panacea to India’s “Carbon-ized” power sector.

Though solar power seems to be a lucrative option, a question worth pondering upon is why solar pow-er fuels only 0.48% of India’s electricity demand?

One of the major reasons behind this is the “Bank-ability” of solar power plants. As these projects require a heavy upfront capital investment, the de-velopers rely on banks for funding. However, the bankers are apprehensive about the same, which leaves the cash crunched developers in a difficult situation. Even the successful bidders under JNNSM have faced problems to achieve financial closure within the stipulated time. The particular risks that make solar power project financing a concern for banks are as follows:

• Technology

Given the fact that solar technologies are relatively a new concept in India, there exists numerous risks with respect to execution of the projects. Crystal-line cells and modules are comparatively easier to execute and come with a guarantee of more than 20 years, rendering them to be less risky both for developers as well as banks. However, in the last couple of years, novel technologies like thin-film modules have emerged which involve a lower up-front investment, but are unproven and therefore considered more risky.

• Power Purchase Agreements

The current draft of the JNNSM provides for a “Trader PPA” with Nation Vidyut Vyapar Nigam Ltd. (NVVN), under which the developers will receive the pre-defined tariff for supplying solar power to the state utilities. This may appear a sure shot money mak-ing project on paper, but the financial health of the

Cover Story

TeaM nIveShak

Akhil Tandon

Introduction

India is located in the equatorial sun belt of the earth, thereby receiving abundant radiant energy from the sun. As per the data published by The In-dia Meteorological Department (IMD), in most parts of India, clear sunny weather is experienced 300 to 330 days a year. The annual global radiation varies from 1600 to 2200 kWh/sq. m. which is comparable with radiation received in the tropical and sub-tropical regions. The equivalent energy potential is about 6,000 million GWh of energy per year, which qualifies solar to be one of the most lucrative op-tions for fuelling India’s power requirement in the near future.

In an effort to provide impetus to the adoption of solar power, the government has taken numer-ous initiatives, notably setting up of Ministry of new and renewable energy(MNRE), introduction of Renewable Purchase Obligations(RPOs) and Re-newable energy certificates(RECs). However, the most significant effort has been the launch of the Jawaharlal Nehru National Solar Mission (JNNSM) in 2010. Under JNNSM, the government adopted a unique mechanism of inviting bids from develop-ers at which they were to supply solar power to the state utilities. The tariff was to last a period of 25 years.

Till date, two round of bidding have successfully taken place, which saw the participation from both national and international behemoths. The two rounds of bidding saw the average bids to decline from Rs 12.16 per Kwh to Rs 8.77 per kWh. Solaire Direct SA, a French company, surprised the entire globe by offering an ultra-low bid of Rs 7.49 per kWh, which was more than 50% lower than the benchmark tariff quoted by the Central Electricity Regulatory Commission (CERC). With such aggres-

FINANCIAL WOES OF INDIA'SRISING SUN

June 2012

12C

over

Sto

ryNIVESHAK12

Art

icle

of t

he M

onth

Cov

er S

tory

There exist primarily two routes by which developers can raise finance:

• Balance-sheet based financing

This option can be effectively tapped by large con-glomerates having a healthy balance sheet, which would interest the bankers. The companies can use their liaison with their banks to provide debt at a cheaper rate. Also, the large asset base of these com-panies provides them with the necessary armour to support large projects, which helps in lowering the cost of operations and operating efficiently. However this would put the company balance sheets at risk and the entire burden of the project failing or under-performing falls on the developers. In India, com-panies like GAIL, IOCL, Punj Lloyd have successfully availed of this option to fund their projects.

• Non-recourse project financing

Non-recourse financing refers to a loan where the lending bank is only entitled to repayment from the profits of the project the loan is funding, not from other assets of the borrower. This is the preferred financing structure where the lending financial insti-tution funds a special purpose vehicle (SPV) set-up especially for the project or for a group of projects. In such a framework, the financial institution has a lien on the project’s cash-flows. However as this structure does not provide recourse to the developer’s balance sheet, lending institutions require rock-solid agree-ments for revenues from the projects. Given the un-certainty of cash flows, the spread for non-recourse financing is typically higher than what banks are will-ing to accept for balance sheet financing. In India, many conglomerates such as Mahindra & Mahindra, Reliance Industries, Jindal Group, etc. have under-taken this route to fund their projects.

While entering into a negotiation with the banks, the developers also need to ensure that the following are in place to make the lending institutions comfort-able:

1. Performance – The viability of a solar power plant is contingent on the Capacity Utilization factor (CUF)

state utilities puts a question mark on the assumed to be ‘assured’ return. Many state discoms are no-torious about delaying and even defaulting on pay-ments which results in financial institutions refusing to consider these PPAs bankable.

• Estimation of Solar Radiation

The output of a solar power plant is contingent upon the Direct Normal Irradiance (DNI) at the plant site. High quality solar radiation data is a pre-requisite for determining the viability of a plant. Given the sensi-tivity of the generation capacity to the solar radiation received, solar radiation assessment is deemed to be a very important activity and typically requires several months for ground measurement of solar ra-diations. Any error in solar resource estimation adds an uncertainty to expected future returns. As of now, on-ground solar radiation data is sketchy and the simulation models are at a preliminary stage.

• Evacuation Infrastructure

In India, the interiors of states of Rajasthan, Gujarat, Maharashtra and Tamil Nadu are considered to be the best sites for installing solar power plants. Evacua-tion of the electricity generated from power plants located in these isolated areas is a challenging task. Extending the grid to these sites requires develop-ment of new transmission lines which are often con-troversial, both because of their expense and the po-tential of damage to property and environment.

Given the above factors, it is highly unlikely for the banks to consider Solar Projects as bankable in the near future, which makes recourse based lending a distant dream.

In wake of such circumstances, let us examine the possible options which can help reviving India’s ‘Set-ting Sun’.

Options for debt financing

Solar power is at a nascent stage in India. However, nations like Germany, Italy and France have been successful in arranging for finance for solar projects. This provides a ray of hope for Indian developers.

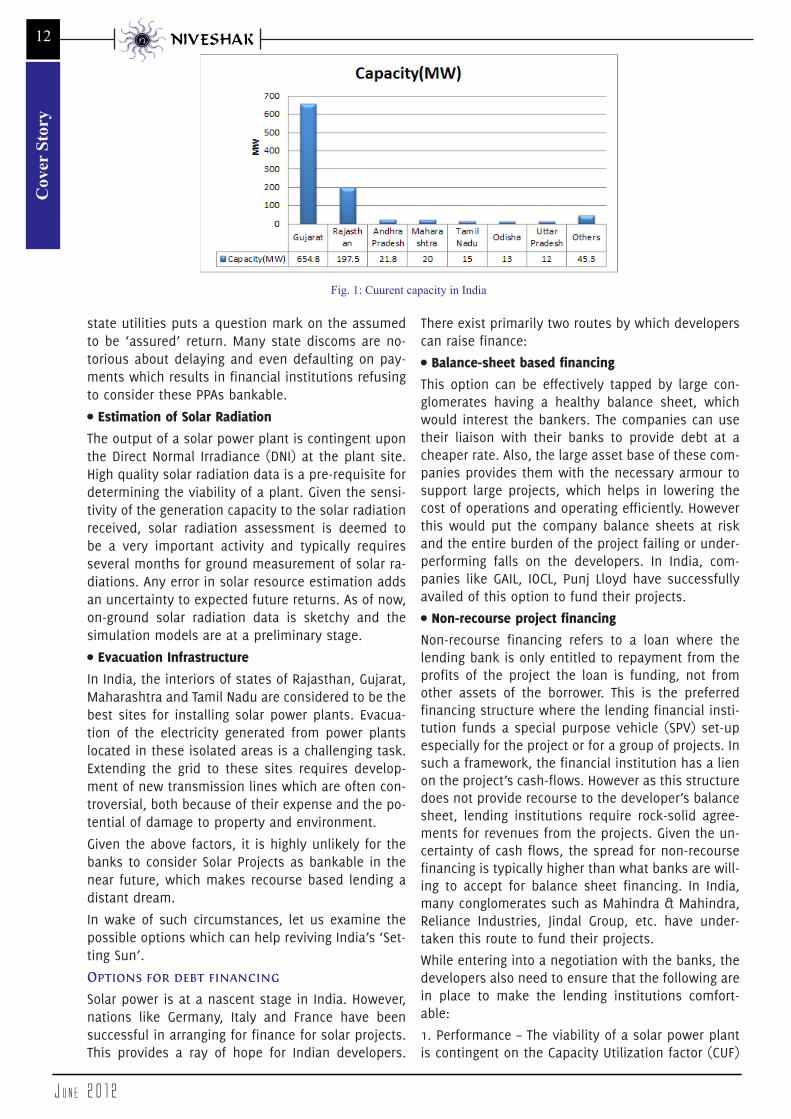

Fig. 1: Cuurent capacity in India

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

13C

over Story

NIVESHAK 13A

rticle of the Month

13C

over Story

NIVESHAK 13A

rticle of the Month

13C

over Story

NIVESHAK 13

lier this month, Azure power announced long-term financing of $70.35 million by Export Import Bank of the United States for its solar power plant at Nagaur in Rajasthan. Indian behemoths like Reliance Power have also availed of these concessional loans.

• Foreign funding

Large project developers can tap international banks to get lower rates of finance. Financing of Solar proj-ects is not a new prospect for banks abroad, which makes the spread relatively lower than that offered by their Indian counterparts. However, hedging can put a substantial dent in the rate differential and only someone ready to take the currency risk should resort to this option. Given the current macro-eco-nomic scenario, it will be a bold move to discount currency fluctuations while taking a call on foreign funding.

• Joint Ventures

Many companies have also entered into JVs with foreign companies for technical as well as financial assistance. Companies like Tata group have taken a lead here, and have tied up with BP Solar to set up Tata BP Solar Ltd.

• Green Energy funds

There are many green energy funds currently in the market and these can provide equity, quasi-equity and mezzanine financing.

Conclusion

In view of the policy support and the abundant solar radiation available in India, solar projects are an at-tractive investment option and can provide equity re-turns in the 15%-20% range. However until the banks get comfortable with the proposed solar PPA, devel-opers rely on non-conventional sources of financing; and support from the government, in terms of final-izing the PPA,REC and RPO structures, can go a long way in getting the projects financed in a nonrecourse manner.

of the equipment, which is a measure of the abil-ity of the equipment to convert solar radiations into electricity. Contractual guarantees from technology providers for the long-term performance of the plant is one possible way out which can assure the bank-ers that the plant will be able to sustain the prom-ised performance.

2. Revenues – As discussed above, the PPAs provide assured revenues only on paper. With the current structure of the JNNSM, PPA may not be bankable due to the credibility of many states. There has been a buzz around that government has been contemplat-ing a tri-partite agreement between the developer, state discom and the Reserve Bank of India to ensure the PPAs bankability, however this is not confirmed yet. Another source of revenue for the projects can be the Renewable Energy Certificate (REC). The devel-opers can forego the preferential tariff and trade the RECs on the energy exchange. In India, the trading of RECs has started in two exchanges – Indian Energy Exchange (IEX) and Power Exchange India Limited (PXIL). However, the market is in its nascent stage and depends on the state’s renewable purchase ob-ligations.

3. Project viability – In addition to the above, develop-ers must be able to take the lenders into confidence that projects are viable and have the capability of repaying debt without outside assistance. This could mean that the project has to fund a Debt-Service-Reserve-Account in addition to having healthy Debt Service Coverage Ratios.

Other options for financing

Other non-conventional options for obtaining funding that can be considered by developers are:

• EXIM financing

The United States export-import bank provides fund-ing for projects which import a significant chunk of their equipment from the United States. This is a good option in case the main technology provider is from the US and has relations with the EXIM bank. US EXIM bank has committed $7 billion to India. Ear-

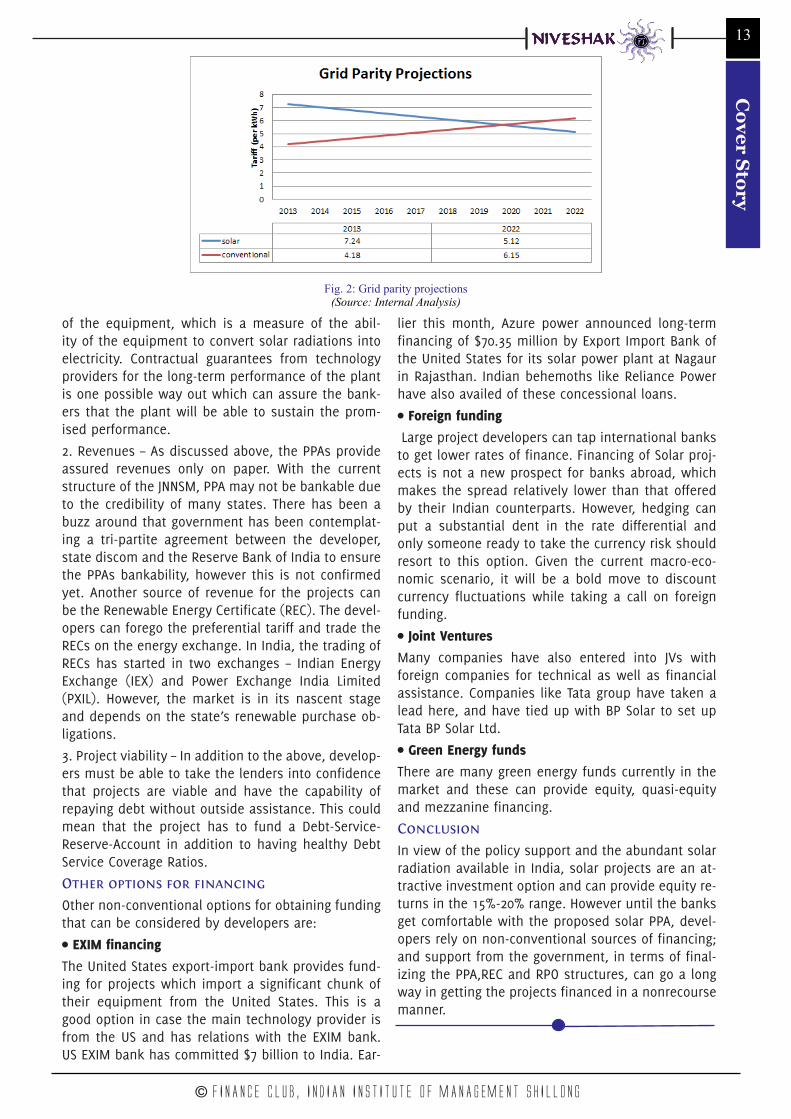

Fig. 2: Grid parity projections(Source: Internal Analysis)

....

June 2012

14 NIVESHAKC

over

Sto

ry14

Art

icle

of t

he M

onth

14 NIVESHAKC

over

Sto

ry14

Art

icle

of t

he M

onth

14 NIVESHAKC

over

Sto

ry14

Art

icle

of t

he M

onth

14 NIVESHAKC

over

Sto

ry14

Fins

ight

Taking the example of two energy firms Apache Corp (APA) and Anadarko Petroleum (APC), each

with an EV/EBITDA multiple of just over 5 in the year 2010, the average EV/EBITDA multiple in their peer group being just under 7. This seems to in-dicate APA and APC were relatively undervalued. However, looking at these companies strictly on a P/E basis, one would wonder why shares in these companies hold any appeal when they are trading at P/E multiple of nearly 30x.

There are more detailed valuation models available in the market that incorporates not only the past performance but also forecast future ones. However, these models are complex for the general investing public and they seldom make the headline. This is generally a cause of concern for senior executives as their claim that their company has great growth prospects and many investments projects in hand are not properly valued in their company’s stock price. Actually, they are not necessarily wrong. Even financial theories suggest that companies which have higher growth prospects should have higher earnings ratios and hence better market value.

But the problem with the P/E ratio is that it’s a retroactive metric. It pits a company’s current mar-ket cap against its trailing-12-month (TTM) profit. But when you buy shares of a company, you are

A premium earning multiple is hard to come to a company and even harder to maintain.In recent times when everybody seems to be in a hurry, investors too have discovered a quick short hand for their investment – P/E ratio.

Countless investors, individuals and professionals alike, spend their time seeking out cheap stocks with very low P/E ratios. Sometimes the stocks are cheap for negative reasons like uncomplimentary industries or poor fundamentals hidden within. And as a result, the stock prices stay stagnant... sometimes for years. But sometimes investors do not pay attention to this fact and companies take undue advantage and modify the P/E ratio by var-ious means – the most common being inclusions of debt in the capital structure.

When companies are financially leveraged then the company with higher debt in the capital struc-ture has lower P/E ratio and is more preferable among its peers.

Company with debt

Company with only equity

Earnings (EBITA) 50 50

Interest -20 0

Net Income 30 50

Enterprise Value (EV)

1,000 1,000

Debt -500 0

Market Capitaliza-tion

500 1000

EV/EBITA 20.0x 20.0x

Debt/Interest 25.0x N/A

P/E Ratio 16.7x 20.0x

Table 1: Leverage distorts the P/E ratio (Hypothetical case)

Table 1 clearly shows that though both the com-pany has same EV value, their P/E ratios have changed substantially due to inclusion of debt.

Poor Companies - Rich Multiples

WelIngkar InSTITuTe of ManageMenT

Preetam Mittal

Countless investors, individuals and professionals alike, spend their time seeking out cheap

stocks with very low P/E ratios

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

..

15C

over Story

NIVESHAK 15A

rticle of the Month

15C

over Story

NIVESHAK 15Finsight

not purchasing its history – you are purchas-ing its future cash flows. What matters is what the company is going to do and not what it has done.

Another very common form of manipulation used by companies is called the “big bath,” and this can make stocks seem undervalued to in-vestors. This happens when the company incurs a big loss to their bottom line. In this method the company takes the complete loss in a single accounting period, instead of spreading these losses over years. This will cause the earnings per share to drop significantly for the time pe-riod involved due to the large losses posted and move earnings from the present to the future. The intention of the company is to foster the idea among investors that this charge is a once only deal, and that the stock will rise consider-ably after the loss has been absorbed. This will cause investors to see the stock as underval-ued and an attractive investment and thus will cause the demand and price for the stock to rise artificially.

One must always keep in mind that using only P/E ratios on a relative basis means that the analysis can be skewed by the benchmark be-ing used. After all, there are periods when in-dustries in entire market become overvalued. In 2000, an Internet stock with a P/E of 75 might have looked cheap when the rest of its peers had an average P/E of 200. In hindsight, neither the price of the stock nor the benchmark made sense. This shows that being less expensive than a benchmark does not mean that the stock is cheap because the benchmark itself may be vastly overpriced.

Also, these ratios are completely ineffective for cyclical firms that go through boom and bust cy-cles--semiconductor companies and auto manu-facturers are good examples and these requires a bit more investigation. Although one would typically think of a firm with a very low trailing P/E as cheap, for a cyclical industry it would be the wrong time to buy because it means that earnings have been very high in the recent past and are likely to fall off soon.

Other things that can distort the P/E ratio include

Even financial theories suggest that companies which have

higher growth prospects should have higher earnings ratios and

hence better market value

inclusion of gains from recently sold businesses to produce an artificially inflated earnings and a lower P/E as a result. The denominator of the ratio can also be manipulated by changing the revenue recognition, depreciation and capital-izing cost. In late 2000, software-maker Oracle ORCL had a very low P/E based on its prior four quarters’ earnings giving the impression that it is a good investment opportunity until a deeper investigation into the numbers revealed that the company had booked a $7 billion gain by selling its stake in Oracle Japan. Based on operating earnings, the stock was not cheap at all.So what’s the solution?The solution is to account for the growth rate of the company or expected growth rate if it can be calculated. Thus, it gives birth to a new and better ratio - PEG ratio computed as:

PEG Ratio = Price-to-Earnings (P/E) Ratio / An-nual Earnings per Share GrowthA crude analysis suggests that companies with PEG values between 0 to 1 may provide higher returns (the closer to 0 the more undervalued a company).In fact, if one goes back a decade then one may find that Apple’s P/E ratio at the time was 297. So, anyone making investment on the basis of P/E ratios would not have considered it a very profitable investment then based on its high P/E value. However investors who had bought shares of the company then have made whoop-ing returns of 7,300% today. But if someone calculated the PEG ratio, it would be something close to 1 indicating that PEG can better guide investors in their investments.Finally, as an investor, it is important to continu-ally sharpen your skills and put new tools in the toolbox. It makes sense to go through and calculate different multiples such as EV multiple (EV/EBITDA, EV/EBIT, EV/NPAT, EV/Invested Capi-tal etc.), PEG and Dividend yield ratio etc. for all current holdings and for future investments to reduce the likelihood of making poor bets.

June 2012

16C

over

Sto

ryNIVESHAK16

Art

icle

of t

he M

onth

Pers

pect

ive

With Infosys witnessing steep falls in stock price, with stagnant salaries to continue for one more year and with attrition rates to blow up, the headwind of squatty guidances has hit the bellwether company badly from all sides. In the wake of these develop-ments, this article is an analysis of a few aspects of Infosys’ financials and policies. Using concepts of leverage, cost of equity, human-resource accounting and balanced scorecard, the analysis tries to explore the possibilities which the management, particularly finance department, might have partially or fully missed to attend; overlooking which can be hazard-ous to Infy’s health.

Why didn’t CFO Mr. Balakrishnan deem it es-sential to burn up….?

Any company would and should take pride in maxi-mizing profits through leverage. By leverage, I mean that you step up your revenue by x%, but your net and operating profits jump by (x+ ∆)% where ∆ >0. But this happens only when you incur a “Fixed Cost” for your operations.

In absence of fixed costs, ∆revenue = ∆profits. It’s because of fixed costs that a 50% rise in revenue results in 80% rise in profits. Now, had the fixed cost been 4000 instead of 3000, the leveraging effect would have been better. A 50% ∆revenue could have led to 100% ∆profits, bringing leverage multiple to 2 from 1.6.

Thus, more the fixed cost, the better leverage your firm enjoys. In other words, to bring your company in a better condition, so that it enjoys better lever-age, you “need” to expend some “additional” fixed cost. The moment I say “fixed” cost, it has abso-lutely no proportionate relation with revenues.

One such fixed cost is “Salaries”. Coming to Infosys, where the mantra to be harped upon in FY 2012-13 is to maximize profits,with financial leverage almost absent, to capitalize on operating leverage, why didn’t CFO Mr. Balakrishnan deem it essential to burn up some money on salary increments and so incur the additional fixed cost?

With this decision not at all favoring a rise in profits in any which way, what good has been cited in slashing variable….?

Let’s try to understand the aspect of distribution of costs between fixed and variable on leverage effect. A higher leverage multiple also means a higher risk of losing profits substantially on a relatively smaller fall in revenues. So, if a company senses a slow-down in future, it ought to “divert” its spending un-der fixed costs to variable costs. As a manifestation of this idea, the company may decrease fixed salary component and increase the performance-based in-centives. On the other hand, if the company senses a brighter market ahead, it diverts the salary com-ponents in the reverse manner to make the leverage multiple higher.

Surprisingly, what Infosys has done is that it has made steep cuts to variable pay of their employees with no diversion of the same to the fixed compo-nent of the salary. Oops..! This falls in neither of the two categories of decisions…

Check table 1 for a few numbers to get a clearer picture.

The only difference between the three cases in table 1 is of the variable cost. Relative to case1, the de-crease in variable costs in case 3 is more than that of case 2. Observe that lesser the variable costs, lesser is the increase in net profits for the same 50% rise in the revenues of the company from Rs. 10000 to Rs. 15000. Even though one may say that more than the percent increase in profits, the rise in absolute profits due to variable cost cut makes more sense for a firm, what I wish to say is, this is possible only when two things are ensured. One, if the variable cost cut is in salaries, it should not result in a fall in top-line (revenues), as a salary cut is enough to cause exodus of top talent. If revenues fall, profits are destined to plummet. Second, to still maintain a fair result compared to case 1, the firm needs to at least ensure the same 50% rise in revenues for growth. Practically speaking; how is it possible for any company to “enhance” its sales by “reducing” variable costs and by keeping the fixed costs “the same”?

With respect to Infosys, the departure of a few peo-ple from top management is already an event of re-cent past. The blow of this verdict has fallen harder on the 300 top executives whose variable salaries shall be cut by 70%, and the already existing lever-age has been substantially tarnished due to this.

SCMhrD,Pune

Vibhu Gangal How do you do ?

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

17C

over Story

NIVESHAK 17A

rticle of the Month

17C

over Story

NIVESHAK 17Perspective

With this decision, not at all favoring a rise in profits in any which way, what good has been sighted in slashing variable salaries heftily and giving a null hike in fixed component of salaries by Infosys to its employees?

Has Infosys also succumbed to the trap of……?

Any company aims to earn substantially more than its cost of capital. Thus, if a firm has missed to learn its true cost of capital, the target set for earnings and revenues is also virtual. This eventually leads to disappointing “actual earnings” and leaves the man-agement puzzled.

Equity is often considered as a “less expensive” source of capital.

Let’s give a second thought to this. Owners carry the maximum risk, which gets accentuated by the fact that they have zero security of assets to fall back in case the company drowns tomorrow unlike the lenders which have the first preference during liquidation of company assets. More the risk more should be the returns. Following this, company is obliged to consider the “true” cost of equity much more than the rest of the sources. If the firm fal-ters here, it gets into the trap of setting false tar-gets and landing in trouble as mentioned above.

Infosys has been the legacy for being a zero-debt company in its sector and functioning purely based on stockholders’ money. So, the question is, has Infosys also succumbed to the trap of under-estimating cost of equity, setting stumpy guidances, pursuing and achieving them and causing shares ul-timately to plummet?

One may contest this with the stand that Infosys has declared a massive 940% dividend per share this year and so has taken due care of its owners. To this, let’s understand that that the activity of maxi-mizing shareholders’ interests is based on two legs: Paying considerable dividends and performing such that share price in secondary market keeps on rising. What Infy has chosen to do could strengthen the first leg, but will badly knock and punch the second. And that’s what seems to be happening- the worst fall of stock in the last 3 years.

Without “directly” spending more, how can this massive asset be churned to.….?

Say a firm targets to earn 25% based on its Cost of

capital calculations and has an asset size of 1000, which currently is earning 20%. To get this additional 5%, the firm may increase the asset size, but be-fore that a wiser decision would be to check if the capabilities of these assets have been exploited to maximum. If yes, then the firm shall incur cost to acquire more assets. If not, the firm shall spend to augment productivity of existing assets. In the latter case, the firm shall prudently choose to spend mon-ey more on those assets which directly contribute to the revenue rather than spending on ancillary activi-ties and non-performing assets which just facilitate the performing assets to perform (like furniture and transport).

Let’s understand that with the presence of NPAs, even if the asset size stands tall, the actual pres-sure on each unit of PA to earn 25% profit is much

more (its 50% if PAs are half of total assets) than it appears and so, firm’s responsibil-ity to keep these PAs pepped-up to per-form is indispensable. For this analysis, employees are considered as assets; with reference to concept of human resource

accounting.

Coming to Infosys, where an employee-base of 1.5 lacs a huge performing asset, how can

this massive asset be churned to contribute more to earn revenue without “directly”

spending more on them? In other words, how could a “zero” salary hike enable these PAs to be more productive? Even though HR accounting is not followed commercially in India, has Infosys missed to understand that employees are its significant “Performing” Assets?

Infosys was the one which kept its promise to ab-sorb recruited candidates when the industry was gripped with job crunch in 2009, which paid salary hikes of 10% even during recession, which rolled out ESOPs in 2010, and which was uniquely efficient with excellent cash management practices.

With due credits and acknowledgement for all this to you, CFO Mr. Balakrishnan, the present speaks of a totally different picture. I am really curious to know what’s going on in your mind. Looks like either you have a big surprise to throw or you’ve faltered badly….

Table 1: Three cases with different variable costs

June 2012

18C

over

Sto

ryNIVESHAK18

Art

icle

of t

he M

onth

18 NIVESHAKC

over

Sto

ry18

FinG

yaan

The Volcker Rule coming to effect from July 2012 is an effort by the US to restrict the propriety trading done by financial institutions. The article also reflects the trading scenario in India. This is an important step in the light of the recent trad-ing losses seen by JP Morgan. The regulation currently seeks to re-strict the trading and the FDI in the institutions carrying on such trading.

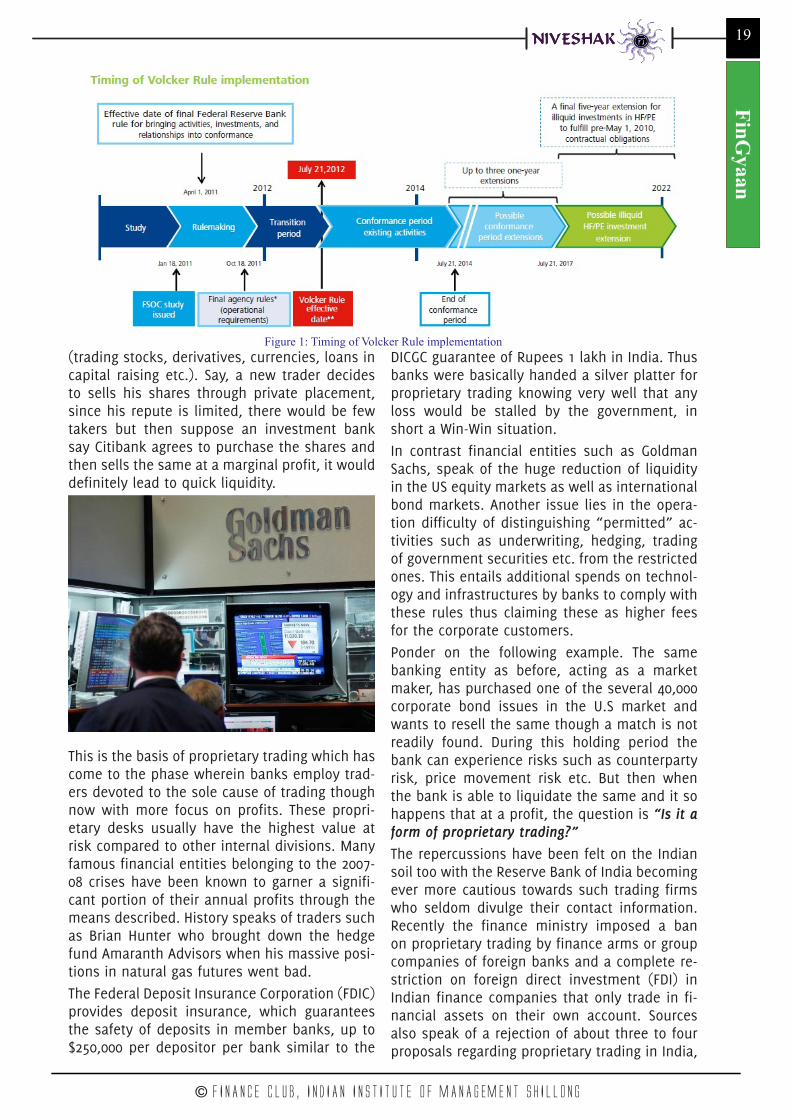

nicipal, Treasury and federal agency securities. The rule’s provisions are scheduled to be implemented as a part of Dodd–Frank Wall Street Reform and Consumer Protection Act on July 21, 2012 and were publicly endorsed by President Obama on January 21, 2010. (Refer Fig 1).There has been a constant tussle be-tween the Regional Bond Dealers As-sociation being supportive of the rule while the Securities Industry and Fi-nancial Markets Associations oppose the provision. “The Volcker rule re-mains highly problematic and is likely to have the unintended consequence of constricting market liquidity, as evidenced by the fact that Treasuries, agencies and munis are exempted,” said Michael Decker, managing direc-tor and co-head of municipal securi-ties at SIFMA. Let’s delve deeper into the various provisions and technicali-ties of the rule and leave such deci-sions to the avid readers.The financial industries started off with the banking industry and invest-ment banking being at bipolar ends but as time passed these were brought under a common umbrella holding for e.g. Citibank has retail banking as well as an investment arm though the line has blurred being under the same cap. Let us rather use the term investment banks to generalize the commonality between the bank and the investment arm. The main motive of such banks is to make a market for themselves (market-maker) to sur-vive in terms of the services offered

Everybody “Rest Assured Sir, Just wish us Luck” says the big banker to his customer. If the deal turns sweet, it’s the bankers to praise and if it doesn’t well they are “Too Big to fall”. This very stance of power and autonomy achieved by these institutions is what Paul Volcker is adamant about ending but then who is Paul Volcker and how is he planning to do so?Paul Volcker is an economist and former head of the Federal Reserve who currently heads President Barack Obama’s Economic Recovery Advisory Board and is credited with ending the high periods of inflation during the 1970’s and 1980’s. But then he is more famous among the biggies of the financial markets because of the Volcker rule established by him.

Wiki states the rule as “a ban on proprietary trading by commercial banks, whereby deposits are used to trade on the bank’s personal ac-counts, although a number of excep-tions to this ban were included in the Dodd-Frank law”, such as the mu-

goa InSTITuTe of ManageMenT

Savio Fernandes

Sir Volcker

Prop Tradingvs.

© FINANCE CLUB, INDIAN INSTITUTE Of MANAGEMENT SHILLONG

19C

over Story

NIVESHAK 19A

rticle of the Month

19C

over Story

NIVESHAK 19FinG

yaan

(trading stocks, derivatives, currencies, loans in capital raising etc.). Say, a new trader decides to sells his shares through private placement, since his repute is limited, there would be few takers but then suppose an investment bank say Citibank agrees to purchase the shares and then sells the same at a marginal profit, it would definitely lead to quick liquidity.

This is the basis of proprietary trading which has come to the phase wherein banks employ trad-ers devoted to the sole cause of trading though now with more focus on profits. These propri-etary desks usually have the highest value at risk compared to other internal divisions. Many famous financial entities belonging to the 2007-08 crises have been known to garner a signifi-cant portion of their annual profits through the means described. History speaks of traders such as Brian Hunter who brought down the hedge fund Amaranth Advisors when his massive posi-tions in natural gas futures went bad.The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance, which guarantees the safety of deposits in member banks, up to $250,000 per depositor per bank similar to the

DICGC guarantee of Rupees 1 lakh in India. Thus banks were basically handed a silver platter for proprietary trading knowing very well that any loss would be stalled by the government, in short a Win-Win situation.

In contrast financial entities such as Goldman Sachs, speak of the huge reduction of liquidity in the US equity markets as well as international bond markets. Another issue lies in the opera-tion difficulty of distinguishing “permitted” ac-tivities such as underwriting, hedging, trading of government securities etc. from the restricted ones. This entails additional spends on technol-ogy and infrastructures by banks to comply with these rules thus claiming these as higher fees for the corporate customers.Ponder on the following example. The same banking entity as before, acting as a market maker, has purchased one of the several 40,000 corporate bond issues in the U.S market and wants to resell the same though a match is not readily found. During this holding period the bank can experience risks such as counterparty risk, price movement risk etc. But then when the bank is able to liquidate the same and it so happens that at a profit, the question is “Is it a form of proprietary trading?”The repercussions have been felt on the Indian soil too with the Reserve Bank of India becoming ever more cautious towards such trading firms who seldom divulge their contact information. Recently the finance ministry imposed a ban on proprietary trading by finance arms or group companies of foreign banks and a complete re-striction on foreign direct investment (FDI) in Indian finance companies that only trade in fi-nancial assets on their own account. Sources also speak of a rejection of about three to four proposals regarding proprietary trading in India,

Figure 1: Timing of Volcker Rule implementation

June 2012

20C

over

Sto

ryNIVESHAK20

Art

icle

of t

he M

onth

NIVESHAK

from firms such as Morgan Stanley India Com-pany Pvt Ltd and UBS Securities India Pvt Ltd. Domestic banks are not allowed proprietary trading as a standalone activity but are allowed to do so through separate subsidiary or a joint venture though the maximum market exposure cap stands at 40%. Cur-rently, FDI is regulated through foreign invest-ment promotion board (FIPB) in India. However, in 18 NBFC activities, 100% FDI is permitted through the automatic route. This has been viewed by the RBI as a “clear possibility of regulatory arbitrage by foreign investors for then can directly pump in their money into these firms without having themselves subject to the regu-lations of SEBI. This uniform amount of higher capital inflow can subsequently weaken the In-dian rupee thus harming the nation. Rough es-timates during the April-June 2010 period state that nearly 24% of total trading on the stock market was a part of proprietary trading.On a different perspective, we are limiting a huge chuck of the bank’s assets which could be used for the trading activities benefiting not only the bank but also the customers through lower transaction charges. True we already have Capital adequacy ratio based on the BASEL norms which restrict reserves in bank but a ban on proprietary trading may actually increase the systemic risk by accumulating assets into the banking system thus only fuelling the too big to fail scenario. The new norms release by RBI for banking licenses states that a minimum capital of 500 crore needs to be held hence the banks will lose a significant amount of returns which could be passed on to customers.Overall, calling for a sudden closure of such trades may lead to a huge increase in the bank’s administrative costs such as costs of regulatory compliance, which would be passed on to con-sumers thus making capital investments costs much higher in turn affecting the GDP negative-ly. Studies state this as an additional 6.6 million work hours coupled with 1.8 million hours per year for enforcement. It would also entail an ad-ditional 3000 employees per bank along with a cost increase of around $350 million.The effect may also make foreign interest rates

20C

over

Sto

ry20

FinG

yaan

attractive thus affecting trade and devaluation of the domestic currency. Small time firms and start-ups would also be left devoid of funds due to these high fees and interest rates.In conclusion it can be said that these regulation don’t merely remove risk but simply transfer it.

Say a company that would be protected by hedging strategies used by a bank may now undergo curren-cy risk, operational risks, currency risks etc. Of course the end customer seems to be at a loss but then frequent finan-cial crisis such as the collapse of MF Global Holdings Ltd, attrib-

uted to proprietary trading, left the authority no other option but to tighten the regulatory cords which come into effect post July 21, 2012.

© FINANCE CLUB, INDIAN INSTITUTE OF MANAGEMENT SHILLONG

21C

over Story

NIVESHAK 21A

rticle of the Month

© FINANCE CLUB, INDIAN INSTITUTE OF MANAGEMENT SHILLONG

21C

over Story

NIVESHAK 21A

rticle of the Month

© FINANCE CLUB, INDIAN INSTITUTE OF MANAGEMENT SHILLONG

21C

over Story

Sir, I recently read about Leveraged Buyout, what is a Leveraged Buyout?

In a leveraged buyout, the Investor / Private Equity fund acquires controlling in-terest in another company through substan-tial proportion of debt. Apart from very high proportion of debt, what distinguishes LBO

from a normal acquisition is that the assets of the ac-quired company are used as collateral for the debt, which is usually non-recourse to the investor. Also cash flows of the acquired company are used to make inter-est and principal payments.

Sir, it all looks very confusing. Can you please explain the concept with the help of an example?

It is similar to buying a rental house through mortgage. As in a rental house, mortgage is secured by the house; in LBO the assets of the target company are used

to secure the mortgage. Rental income generates cash flows for servicing debt, while in a LBO target com-pany’s earnings are used for paying the mortgage. Nor-mally institutional investors and private equity funds use LBO to acquire large companies without contribut-ing much capital of their own.

But sir, as we have read in our fi-nance course, high debt also increases the risk. Isn’t LBO a risky acquisition strategy considering the high degree of leverage involved?

Correct, high debt involves both high gain and high risk. A very high proportion of debt sometimes results in downfall of the company, if the cash flow projections of the

company do not go the predicted way. Company in such cases, therefore, is unable to service high debt obligations and goes bankrupt.

Which companies are the likely tar-gets to be acquired through a LBO?

Some features like low debt, high assets (useful for collateral), stable cash flows, and synergies make a company highly attractive and more vulnerable to

takeovers. Also the acquiring firms look for compa-nies with viable exit options. LBO funds or investors typically try to exit within three to five years through an outright sale, IPO or recapitalisation i.e. replacing equity with more debt.

If suppose, the company manage-ment wants to avoid this takeover, what should they do?

A number of strategies are adopted by companies to avoid hostile takeovers. A company may adopt ‘Poison Pill’ strat-egy, i.e. making the company less attrac-tive to the investor by strategies like load-

ing the company with debt, selling its priced assets etc. Another strategy used is ‘White knight’, where the company approaches another party for a friendly takeover, to counter the hostile takeover.

When did the LBOs originate, and are they actually practiced?

LBOs started around the post-world war period and were hugely successful during the 1980’s. However, its popular-ity has faded since due to stricter lend-ing norms and sceptical perception of the

company’s management. Tata’s acquisitions of Tet-ley, Corus and Jaguar, Hindalco’s acquisition of Nov-elis, and Suzlon’s acquisition of Re-power are some of the examples of LBOs.

Sir, thank you for explaining Lever-aged Buyout to us.

CLASSROOMFinFunda

of the Month

Leveraged Buyout (LBO)

NIVESHAK 21C

lassroomIIM Shillong Shirish jain

June 2012

2222

F I N - Q1. Established in 1998 “X” does the work of 17 national banks. What is “X”?

2. Find the next and state the link: Real- Sol- ?? - ??

3. Established in 1929, “X” is the 3rd largest Bourse of Africa. Name “X”.

4. “X” owns “Delaire Sunrise”, “The Magnificence”, “Letseng Legacy”, etc. What was “X” recently in news for?

5. Developed by Lars Kestner, this ratio which helps measure the performance of an equity. Which ratio is this?

6. Find Odd man out: Economic Affairs, Financial Services, Disinvestment, Grants.

7. Identify the country:

8. Name the country which will host the next G20 Summit.

9. “X” is the financial regulator of the banks where India is reported to be the 55th biggest client. Identify “X”.

10. “X” is a term in bond valuation which represents the value of a bond, exclusive of any commissions or fees mostly used in European Markets. What is “X”?

All entries should be mailed at [email protected] by 7th July, 2012 23:59 hrs One lucky winner will receive cash prize of Rs. 500/-

Article of the MonthPrize - INR 1000/-Kailash V. Madan

IIM Shillong

W I N N E R S

A N N O U N C E M E N T SALL ARE INVITED

Team Niveshak invite articles from B-Schools all across India. We are looking for original articles related to finance & economics. Students can also contribute puz-zles and jokes related to finance & economics. References should be cited wherever necessary. The best article will be featured as the “Article of the Month” and would be awarded cash prize of Rs.1000/-

Instructions » Please email your article with the file name and the subject as <Title of the

Article>_<Institute Name>_<Author’s name/Group’s name> by 7 July 2012. » Article must be sent in Microsoft Word Document (doc/docx), Font: Times New

Roman, Font Size: 12, Line spacing: 1.5 » Please ensure that the entire document has a wordcount between 1200 - 1500 » The cover page of the article should only contain the Title of the Article, the Au-

thor’s Name and the Institute’s Name » Mention your e-mail id/ blog if you want the readers to contact you for further

discussion » Also certain entries which could not make the cut to the Niveshak will get figured

on our Blog in the ‘Specials’ section

SUBSCRIBE!!Get your OWN COPY delivered to inbox

Drop a mail at [email protected]

ThanksTeam Niveshakwww.iims-niveshak.com

23

© FINANCE CLUB, INDIAN INSTITUTE OF MANAGEMENT SHILLONG

FIN - QPrize - INR 500/-

Chhavi SalujaNMIMS, Mumbai

COMMENTS/FEEDBACK MAIL TO [email protected]://iims-niveshak.comALL RIGHTS RESERVED

Finance ClubIndian Institute of Management, Shillong

Mayurbhanj Complex,NongthymmaiShillong- 793014