7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 1/25

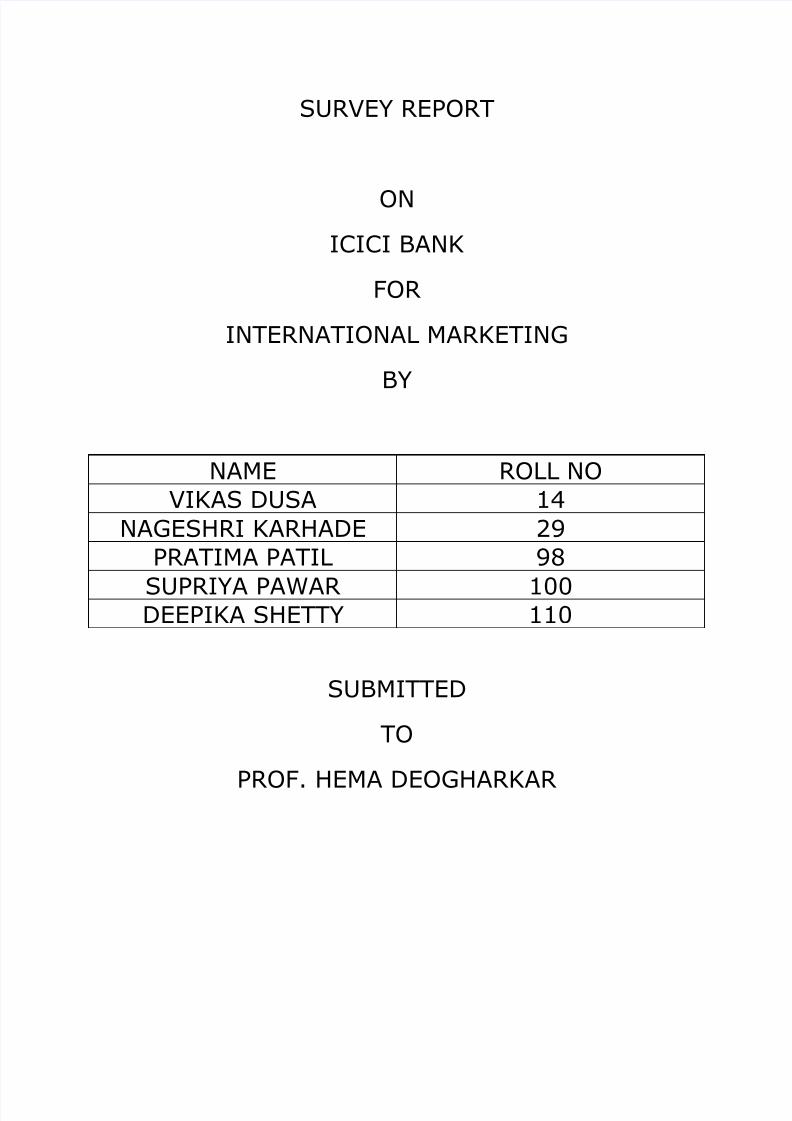

SURVEY REPORT

ON

ICICI BANK

FOR

INTERNATIONAL MARKETING

BY

NAME ROLL NO

VIKAS DUSA 14

NAGESHRI KARHADE 29

PRATIMA PATIL 98

SUPRIYA PAWAR 100DEEPIKA SHETTY 110

SUBMITTED

TO

PROF. HEMA DEOGHARKAR

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 2/25

ICICI BANK SURVEY

ICICI Bank provides vital services to help focus on business and compete in global

markets. Trade services strengthen business relationships by ensuring reliability

and speed in business documentation and payments. Global Trade offersoutstanding opportunities to sell & source products in a complex & fast changing

landscape. Whether you are an exporter or an importer, ICICI Bank has the right

expertise and services to help improve earnings & develop opportunities in the

Global market place. ICICI specialise in forex services & currency risk hedging,

documentary collection & credit, bank guarantee, export & import finance to

provide personalised services through our dedicated & experienced Relationship

Managers

1. What are the steps for getting foreign project finance?

Pre Shipment Finance is issued by a financial institution when the seller wants the

payment of the goods before shipment. The main objectives behind preshipment

finance or pre export finance are to enable exporter to

Procure raw materials.

Carry out manufacturing process.

Provide a secure warehouse for goods and raw materials.

Process and pack the goods.

Ship the goods to the buyers.

Meet other financial cost of the business.

Types of Pre Shipment Finance

1. Packing Credit

2. Advance against Cheques/Draft etc. representing Advance Payments.

Packing Credit - is any loan or advance granted or any other credit provided by a

bank to an exporter for financing the purchase, processing, manufacturing or

packing of goods prior to shipment, on the basis of letter of credit opened in his

favor or in favor of some other person, by an overseas buyer or a confirmed and

irrevocable order for the export of goods from the producing country or any other

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 3/25

evidence of an order for export from that country having been placed on the

exporter or some other person, unless lodgment of export orders or letter of

credit with the bank has been waived.

Packing Credit is extended in the following forms:

Packing Credit in Indian Rupee

Packing Credit in Foreign Currency (PCFC)

Requirements for Getting Packing Credit

This facility is provided to an exporter who satisfies the following criteria

A ten digit Importer - Exporter Code (IE Code ) number allotted by DGFT.

Exporter should not be in the caution list of RBI. If the goods to be exported are

not under OGL (Open General License), the exporter should have the required

license /quota permit to export the goods.

Packing credit facility can be provided to an exporter on production of the

following evidences to the bank:

Formal application for releasing the packing credit with undertaking to the effectthat the exporter would be ship the goods within stipulated due time and submit

the relevant shipping documents to the banks within prescribed time limit.

Firm order or irrevocable L/C or original cable / fax / telex message exchange

between the exporter and the buyer.

License issued by DGFT if the goods to be exported fall under the restricted or

canalized category. If the item falls under quota system, proper quota allotment

proof needs to be submitted.

The confirmed order received from the overseas buyer should reveal theinformation about the full name and address of the overseas buyer, description

quantity and value of goods (FOB or CIF), destination port and the last date of

payment.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 4/25

Different Stages of Packing Credit

I. Appraisal and Sanction of Limits - Before making any an allowance for Credit

facilities, banks need to check the different aspects like product profile, political

and economic details about country. Apart from these things, the bank also looks

in to the status report of the prospective buyer, with whom the exporterproposes to do the business.

The Bank extended the packing credit facilities after ensuring the following :-

The exporter is a regular customer, a bona fide exporter and has a goods standing

in the market.

Whether the exporter has the necessary license and quota permit (as mentioned

earlier) or not.

Whether the country with which the exporter wants to deal is under the list of

Restricted Cover Countries (RCC) or not.

II. Disbursement of Packing Credit Advance - Once the proper sanctioning of the

documents is done, bank ensures whether exporter has executed the list of

documents mentioned earlier or not. Disbursement is normally allowed when all

the documents are properly executed.

Sometimes an exporter is not able to produce the export order at time of availing

packing credit. So, in these cases, the bank provides a special packing credit

facility and is known as Running Account Packing.

Before disbursing the bank specifically check for the following particulars in thesubmitted documents"

Name of buyer

Commodity to be exported

Quantity

Value (either CIF or FOB)

Last date of shipment / negotiation.

Any other terms to be complied with

The quantum of finance is fixed depending on the FOB value of contract /LC or the

domestic values of goods, whichever is found to be lower. Normally insurance and

freight charged are considered at a later stage, when the goods are ready to be

shipped.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 5/25

In this case disbursals are made only in stages and if possible not in cash. The

payments are made directly to the supplier by drafts/bankers/cheques.

The bank decides the duration of packing credit depending upon the time

required by the exporter for processing of goods.

The maximum duration of packing credit period is 180 days; however bank mayprovide a further 90 days extension on its own discretion, without referring to

RBI.

III. Follow up of Packing Credit Advance - Exporter needs to submit stock

statement giving all the necessary information about the stocks. It is then used by

the banks as a guarantee for securing the packing credit in advance. Bank also

decides the rate of submission of these stocks.

IV. Liquidation of Packing Credit Advance - Packing Credit Advance needs be

liquidated out of as the export proceeds of the relevant shipment, thereby

converting pre- shipment credit into post shipment credit. In case if the exportdoes not take place then the entire advance can also be recovered at a certain

interest rate. RBI has allowed some flexibility in to this regulation under which

substitution of commodity or buyer can be allowed by a bank without any

reference to RBI. Hence in effect the packing credit advance may be repaid by

proceeds from export of the same or another commodity to the same or another

buyer. However, bank need to ensure that the substitution is commercially

necessary and unavoidable.

V. Overdue Packing - Bank considers a packing credit as an overdue, if the

borrower fails to liquidate the packing credit on the due date. And, if thecondition persists then the bank takes the necessary step to recover its dues as

per normal recovery procedure.

Packing Credit in Foreign Currency (PCFC)

Authorized dealers are permitted to extend Pre-shipment Credit in Foreign

Currency (PCFC) with an objective of making the credit available to the exporters

at internationally competitive price. This is considered as an added advantage

under which credit is provided in foreign currency in order to facilitate the

purchase of raw material after fulfilling the basic export orders. The rate of interest on PCFC is linked to London Inter-bank Offered Rate (LIBOR). The

exporter has freedom to avail PCFC in convertible currencies like USD, Pound,

Sterling, Euro, Yen etc. However, the risk associated with the cross currency

truncation is that of the exporter.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 6/25

The sources of funds for the banks for extending PCFC facility include the Foreign

Currency balances available with the Bank in Exchange, Earner Foreign Currency

Account (EEFC), Resident Foreign Currency Accounts RFC(D) and Foreign

Currency(Non Resident) Accounts.

Advance against Cheque/Drafts received as advance payment - Where exportersreceive direct payments from abroad by means of cheques/drafts etc. the bank

may grant export credit at concessional rate to the exporters of goods track

record, till the time of realization of the proceeds of the cheques or draft etc. The

Banks however, must satisfy themselves that the proceeds are against an export

order.

Post Shipment Finance is a kind of loan provided by a financial institution to an

exporter or seller against a shipment that has already been made. This type of

export finance is granted from the date of extending the credit after shipment of the goods to the realization date of the exporter proceeds. Exporters don’t wait

for the importer to deposit the funds.

Basic Features

The features of post-shipment finance are:

Post-shipment finance is meant to finance export sales receivable after the date

of shipment of goods to the date of realization of exports proceeds. In cases of

deemed exports, it is extended to finance receivable against supplies made to

designated agencies.A post-shipment finance is provided against evidence of shipment of goods or

supplies made to the importer or seller or any other designated agency.

Post -shipment finance can be secured or unsecured. Since the finance is

extended against evidence of export shipment and bank obtains the documents

of title of goods, the finance is normally self liquidating.

As a quantum of finance, post-shipment finance can be extended up to 100% of

the invoice value of goods. In special cases, where the domestic value of the

goods increases the value of the exporter order, finance for a price difference can

also be extended and the price difference is covered by the government.Post-shipment finance can be of short terms or long term, depending on the

payment terms offered by the exporter to the overseas importer. In case of cash

exports, the maximum period allowed for realization of exports proceeds is six

months from the date of shipment. Concessive rate of interest is available for a

highest period of 180 days, opening from the date of surrender of documents.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 7/25

Usually, the documents need to be submitted within 21days from the date of

shipment.

Financing For Various Types of Export Buyer's Credit

Post-shipment finance can be provided for three types of export:

Physical exports: Finance is provided to the actual exporter or to the exporter in

whose name the trade documents are transferred.

Deemed export: Finance is provided to the supplier of the goods which are

supplied to the designated agencies.

Capital goods and project exports: Finance is sometimes extended in the name of

overseas buyer. The disbursal of money is directly made to the domestic exporter.

Types of Post Shipment Finance:-The post shipment finance can be classified as :

Export Bills purchased/discounted.

Export Bills negotiated

Advance against export bills sent on collection basis.

Advance against export on consignment basis

Advance against undrawn balance on exports

Advance against claims of Duty Drawback.

Export Bills Purchased/ Discounted. (DP & DA Bills) - Export bills (Non L/C

Bills) is used in terms of sale contract/ order may be discounted or purchased by

the banks. It is used in indisputable international trade transactions and the

proper limit has to be sanctioned to the exporter for purchase of export bill

facility.

Export Bills Negotiated (Bill under L/C) - The risk of payment is less under the LC,

as the issuing bank makes sure the payment. The risk is further reduced, if a bank

guarantees the payments by confirming the LC. Because of the inborn securityavailable in this method, banks often become ready to extend the finance against

bills under LC.

However, this arises two major risk factors for the banks:

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 8/25

The risk of nonperformance by the exporter, when he is unable to meet his terms

and conditions. In this case, the issuing banks do not honor the letter of credit.

The bank also faces the documentary risk where the issuing bank refuses to

honour its commitment. So, it is important for the for the negotiating bank, and

the lending bank to properly check all the necessary documents beforesubmission.

Advance against Export Bills Sent on Collection Basis - Bills can only be sent on

collection basis, if the bills drawn under LC have some discrepancies. Sometimes

exporter requests the bill to be sent on the collection basis, anticipating the

strengthening of foreign currency. Banks may allow advance against these

collection bills to an exporter with a concessional rates of interest depending

upon the transit period in case of DP Bills and transit period plus usance period in

case of usance bill.The transit period is from the date of acceptance of the export documents at the

banks branch for collection and not from the date of advance.

Advance against Export on Consignments Basis - Bank may choose to finance

when the goods are exported on consignment basis at the risk of the exporter for

sale and eventual payment of sale proceeds to him by the consignee.

However, in this case bank instructs the overseas bank to deliver the document

only against trust receipt /undertaking to deliver the sale proceeds by specified

date, which should be within the prescribed date even if according to the practice

in certain trades a bill for part of the estimated value is drawn in advance againstthe exports.

Advance against Undrawn Balance - It is a very common practice in export to

leave small part undrawn for payment after adjustment due to difference in rates,

weight, quality etc. Banks do finance against the undrawn balance, if undrawn

balance is in conformity with the normal level of balance left undrawn in the

particular line of export, subject to a maximum of 10 percent of the export value.

An undertaking is also obtained from the exporter that he will, within stipulated

time from due date of payment or the date of shipment of the goods, whichever

is earlier surrender balance proceeds of the shipment.Advance Against Claims of Duty Drawback - Duty Drawback is a type of discount

given to the exporter in his own country. This discount is given only, if the in-

house cost of production is higher in relation to international price. This type of

financial support helps the exporter to fight successfully in the international

markets.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 9/25

In such a situation, banks grants advances to exporters at lower rate of interest

for a maximum period of 90 days. These are granted only if other types of export

finance are also extended to the exporter by the same bank.

After the shipment, the exporters lodge their claims, supported by the relevant

documents to the relevant government authorities. These claims are processedand eligible amount is disbursed after making sure that the bank is authorized to

receive the claim amount directly from the concerned government authorities.

2. Finance in Rs or $

Export Finance

Avail ICICI Banks Export Finance services to facilitate cash flow in your business.

Our Export Finance is available in Indian rupees and foreign currency, tailor-madeto support your export requirements. ICICI Banks Export Finance services include

both pre-shipment and post-shipment credit.

Obtain pre-shipment finance in the form of Export Packing Credit to finance

purchase or import of raw materials and processing and packing of goods for

export. Our pre-shipment credit is based on actual trading cycles.

Post-shipment credit finances export sales receivables after you have shipped the

goods until the export proceeds are realized. ICICI Bank offers post-shipmentcredit in the form of Export Bill Negotiation.

The ICICI Bank Edge

Competitive rate of interest

Negotiation, payment or acceptance of export documents under letter of credit

Document scrutiny services to ensure compliance with LC terms and conditions

Arranging forfeiting of your export bills drawn under LC at very competitive rates,

without recourse to you

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 10/25

3. What do you mean by fund based and non fund based finance?

Fund-based working capital products include cash credit, overdraft, bill

discounting, short-term loans, and export financing (pre-shipment as well as post-

shipment). Non fund based facilities include letters of credit and bank guarantees.

Non Fund Based

Letter of Credit

With ICICI Banks Letter of Credit, you can be assured of timely and correct

payments from your buyers. Now, interact with ease even with companies with

whom you have had limited experience or are unsure of their credit history.

ICICI Bank offers inland and foreign LCs of two types Sight LC and Usance LC. Sight

LC commands immediate payment on presentation of the necessary documents.

In case of a Usance LC, payment is set for a specified future date only after

acceptance of presented documents.

The ICICI Bank Edge

Sanctioned and issued quickly

Competitively priced

Usance period of up to 180 days Assessment based on a parameterized model.

ICICI Bank LCs can also be availed against 100% cash margin in the form of Fixed

Deposits

ICICI Bank LCs are available against 25%-35% cash margin and 100% collateral

security in the form of residential property or liquid securities. ICICI Bank holds

first charge on current assets.

Bank GuaranteeICICI Banks Bank Guarantees are available to you against minimal requirements

and in the shortest possible time. ICICI Banks Bank Guarantees are also available

in foreign currency for approved purposes as defined under FEMA.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 11/25

The ICICI Bank Edge

Maximum tenor of guarantee 18 months

Valid for a maximum of 10 years

Competitively priced

ICICI Bank also issues Bank Guarantees against 25% cash margin and 100%

collateral security in the form of residential property or liquid securities. Bank

guarantees in foreign currency are available against credit limits or 100% cash

margin.

Fund based

Exports Pre-shipment Finance We provide pre-shipment finance in the form of Export Packing Credit (EPC) to

help you to meet your working capital needs while manufacturing your goods for

export. We provide Export Packing Credit both in rupee as well as foreign

currency at competitive rates.

Export Letter of Credit Advising

Exporters can insist that their export Letters of Credit are advised through ICICI

Bank to ensure timely delivery.

Export Letter of Credit Confirmation

Benefit from the credit strength of ICICI Bank for confirmation of export Letters of

Credit received from other foreign banks. With ICICI Bank's confirmation services,

you can eliminate the foreign bank and country risks from your export collections.

Once we add our confirmation to the Letter of Credit, you are assured of

payment, subject to non-discrepant documents, irrespective of non-payment by

LC opening bank.

Purchase /Discounting of Export Bills

Do not worry when your exports are not covered under Letter of credit. Against

sanctioned credit limits, we can pay you the discounted value of your invoice,

immediately on shipment. The proceeds will be credited to your account if the

export documents are presented before cut off time at your ICICI Bank branch.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 12/25

We offer this at competitive rates both in rupee as well as foreign currency and

with world-class service standards.

Negotiation of Export Bills under Letter of Credit

Against sanctioned credit limits, we negotiate your export bills drawn underLetter of Credit, if the documents are found to be strictly in terms with the Letter

of Credit conditions. We offer this at competitive rates both in rupee as well as

foreign currency and with world-class service standards.

Forfaiting:

Forfaiting means discounting of receivables, under a Letter of Credit or Co-

accepted Bills of Exchange, 'without recourse' on a fixed rate basis. Generally,

Forfaiting is often applied where the exporter is selling goods on credit terms and

the export receivables are guaranteed by the importer's bank. This service

enables you to fund your working capital requirements and allows you to secure

deals that might otherwise not have been possible.

Export Bill Collection

Concentrating your Documentary Collection activities with ICICI Bank, you can

eliminate many of your exporting hassles. Not only will your international banking

become much more uniform, you can experience fewer delays in receiving

payment, effortlessly access collection information details, gain increased controlover export receivables and have an efficient cash flow management.

Advances against exports on Consignment basis

ICICI Bank can provide financing for export on consignment basis, wherein goods

are exported at the risk of the exporter for sale and eventual payment of sale

proceeds to him by the consignee.

Factoring

It is a service that covers the financing and collection of account receivables in

domestic and international trade. It is an ongoing arrangement between the

client and Factor (ICICI Bank), where client assigns the receivables to the Factor.

By obtaining payment of the invoices immediately from the factor, the company's

cash flow is improved. At the same time due to the involvement of Factor, your

credit risk on the buyer is also minimized.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 13/25

4. Importance of bank guarantee

What is Bank Guarantee?

A Bank Guarantee is a guarantee issued by a banker that, in case of an occurrence

or non-occurrence of a particular event, the bank guarantees to make good the

loss of money as stipulated in the contract.

Bank analyses the creditworthiness or the business capacity of its clients and then

issues various types of bank guarantees like Financial Guarantees, Performance

Bank Guarantees, Deferred Payment Guarantees. Bank guarantees can be issued

against Cash Margin and Mortgage of Immovable Properties.

5. How is LC used

What is Letter of Credit?

When a buyer want to purchase goods or importer wants to import goods from

an unknown seller or exporter, he can take assistance of banks in such buying or

importing transactions.

On the basis of creditworthiness, a Bank issues a Letter of Credit addressed to the

supplier or exporter who, on the strength of Letter of Credit issued by a reputed

bank, will not hesitate to supply or export goods to such unknown buyer/

importer. After the goods are supplied, A Signed Invoice with a Letter of Credit is

presented to the banker of buyer / importer and the payment is made to the

seller/exporter directly by the bank.

Step-by-step process:

Buyer and seller agree to conduct business. The seller wants a letter of

credit to guarantee payment.

Buyer applies to his bank for a letter of credit in favor of the seller.

Buyer's bank approves the credit risk of the buyer, issues and forwards the

credit to its correspondent bank (advising or confirming). The

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 14/25

correspondent bank is usually located in the same geographical location as

the seller (beneficiary).

Advising bank will authenticate the credit and forward the original credit to

the seller (beneficiary).

Seller (beneficiary) ships the goods, then verifies and develops thedocumentary requirements to support the letter of credit. Documentary

requirements may vary greatly depending on the perceived risk involved in

dealing with a particular company.

Seller presents the required documents to the advising or confirming bank

to be processed for payment.

Advising or confirming bank examines the documents for compliance with

the terms and conditions of the letter of credit.

If the documents are correct, the advising or confirming bank will claim the

funds by:o Debiting the account of the issuing bank.

o Waiting until the issuing bank remits, after receiving the documents.

o Reimburse on another bank as required in the credit.

Advising or confirming bank will forward the documents to the issuing

bank.

Issuing bank will examine the documents for compliance. If they are in

order, the issuing bank will debit the buyer's account.

Issuing bank then forwards the documents to the buyer.

6. What is an EEFC Account and what are its benefits?

Ans. Exchange Earners' Foreign Currency Account (EEFC) is an account maintained

in foreign currency with an Authorised Dealer i.e. a bank dealing in foreign

exchange. It is a facility provided to the foreign exchange earners, including

exporters, to credit 100 per cent of their foreign exchange earnings to the

account, so that the account holders do not have to convert foreign exchange intoRupees and vice versa, thereby minimizing the transaction costs.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 15/25

EEFC Account

Indian exports have surged over the last decade owing to an unprecedented

boom in sectors like software, biotechnology, gems, jewellery, textiles etc. As a

result of this, the volume of inward remittances has also increased significantly.

To shield the firms engaged in regular export and import from the exchange ratefluctuations RBI has allowed parking of foreign currency by exporters in an

account designated as Exchange Earners Foreign Currency Account (EEFC). EEFC

accounts are Current Accounts held in foreign currency with authorized dealers of

foreign exchange in the country.

Eligibility

A person resident in India may open, hold and maintain theEEFC Account, subject

to terms and conditions as may be specified by RBI from time to time includingthe FEMA Regulations 2000 governing EEFC Account and the Foreign Exchange

Management Act, 1999.

Documentation

All the account opening for EEFC accounts will be done at COPS only. The forms

have to be stored in the branch itself. All the documents would be scanned

through Omnidocs to COPS.

The documents required for opening an EEFC account is the same as that required

for opening an RCA, wherever an existing RCA account reference is given.

Additionally, the proof of status of the client is required.

Common Documents Check list for Account Opening

The documents / information required to be scanned / couriered to COPS are as

below:

Completely filled-in & signed EEFC Account Opening form.

Constitution Document like the board resolution, partnership letter,

propreitorship letter etc authorising the EEFC account opening. The Board

Resolution / Partnership letter / propreitorship letter should mention the

currency in which the account is to be opened.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 16/25

The proof of status (i.e. whether the unit is located in SEZ, STP or EHTP etc.)

should accompany the AOF and other documents being sent to COPS.

Importer- Exporter Code if applicable.

Nomination form, if the customer has given the consent for the same,

Nomination form is applicable only to Individual and Sole Proprietors Proof of PAN/ Form 60.

NOC from the Lending Bank(s) extending credit facility to the entity / firm, if

applicable.

Exchange Earner's Foreign Currency (EEFC) Account

Attention of Authorised Dealer Category - I (AD Category - I) banks is invited to

A.P. (DIR Series) Circular No.15 dated November 30, 2006 in terms of which all

foreign exchange earners were permitted to retain 100% of their forex earnings in

EEFC account with any AD in India.

2. On a review of the Scheme, it has been decided as under :-

a) 50% of the balances in the EEFC accounts should be converted forthwith into

rupee balances and credited to the rupee accounts as per the directions of the

account holder. This process may be completed within a fortnight from the date

of the circular and compliance reported to the Chief General Manager, ForeignExchange Department, Central Office, Trade Division, Amar Building, Sir P.M.

Road, Fort, Mumbai 400 001

b) In respect of all future forex earnings, an exchange earner is eligible to retain

50% (as against the previous limit of 100%) in non-interest bearing EEFC

accounts. The balance 50% shall be surrendered for conversion to rupee

balances.

c) The facility of EEFC scheme is intended to enable exchange earners to save onconversion/transaction costs while undertaking forex transactions in future. This

facility is not intended to enable exchange earners to maintain assets in foreign

currency, as India is still not fully convertible on Capital Account. Accordingly,

EEFC account holders henceforth will be permitted to access the forex market for

purchasing foreign exchange only after utilising fully the available balances in the

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 17/25

EEFC accounts. ADs may, accordingly, obtain a declaration while selling foreign

exchange to their constituents.

3. It may be noted that the provisions at paragraph 2(b) and 2(c) above will apply,

mutatis mutandis, also to holder of either a Resident Foreign Currency Account(RFC) or a Diamond Dollar Account (DDA).

4. AD Category - I banks may bring the contents of this circular to the notice of

their constituents and customers concerned.

5. The directions contained in this circular have been issued under Sections 10(4)

and 11(1) of the Foreign Exchange Management Act, 1999 (42 of 1999) and are

without prejudice to permissions / approvals, if any, required under any other

law.

7. What is a foreign exchange contract?

Every foreign exchange transaction involves exchange of two currencies by the

counter parties to the transaction. The date on which the exchange is to take

place is the value date of the transaction. The standard nomenclatures for value

dates are:

Ready or cash – value todayTomorrow "tom" – value tomorrow, or next working day

Spot – value two business days after the trading date

Forwards – any value date beyond spot.

Forward exchange contract

What is it?

A forward exchange contract—also called a forward currency contract—is anagreement between you and your bank in which the bank agrees to buy or sell a

certain amount in a foreign currency at a fixed rate of exchange on, or during a

period up to, a particular date.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 18/25

As an exporter entering an export contract in a foreign currency, a forward

exchange contract allows you to determine at the time you sign the contract the

exchange rate which will apply to future payments from your buyer.

Elimination of exchange risk due to movement in the exchange rate can beavoided by the following options:

By invoicing in Indian Rupees.

By fixing the Foreign Exchange Contract.

First alternative is possible only when the buyer agrees to it. He may have his own

reasons for not agreeing to invoice in Indian rupees. The second alternative is

commonly resorted to. This alternative involves booking of forward exchangecontract with your bank.

This means that pending submission of documents to the bank for

purchase/negotiation, you have made firm commitment with the bank under

which you agree to sell to the bank foreign exchange at a future date/period and

the bank agrees to purchase at the firm rate the foreign exchange to be tendered

by you on that date / during the agreed period.

Thus you are in a position to know in advance the exchange rate you are going toget on submission of your export documents. Thus, though you have to pay some

charge for booking a forward contract, you are certain about the rupee amount of

the bill on conversion of foreign currency at a future date. For booking a forward

contract, you should approach your bank with whom you are enjoying a credit

limit.

The bank will book a forward contract only against a firm export order showing

description and quantity of the goods to be supplied, aggregate price and

approximate date of shipment. The bank can accept telex, cable order/fax in thisregard, provided you give an undertaking to produce the original one. Where

shipment has already been completed, forward contract will be booked on the

basis of export bill tendered by you. It can also be booked against an irrevocable

Letter of Credit provided L/C is complete in all respects and you give a declaration

to the bank that you have not booked any forward contract against the underlying

sale contract covering shipments under the L/C. You must ensure delivery of the

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 19/25

related documents within the agreed period of the contract. In case you fail to

deliver the documents within the specified period, the forward contract needs to

be cancelled and fresh contract booked for which your bank will levy cancellation

charges as per the FEDAI Rules.

In case the documents are delivered before the stipulated period, it will involve

early delivery and bank will levy charges for the early delivery, as per FEDAI Rules.

Where the documents are not delivered at all, contract has to be cancelled either

at your request or by the bank itself under certain circumstances, and this will

entail cancellation charges as per the FEDAI Rules.

It therefore becomes extremely important that the period of delivery of the

export documents is carefully chosen and strictly adhered to, so as to avoid

unnecessary charges on account of early delivery or cancellation of forward

contracts. However, facility for substitution of export order is permitted by RBI on

specific request if the unfulfilled export order and the substituted order is for the

same commodity.

8. Difference between BRC and FIRC

Bank Realization Certificate and Foreign Inward Remittance certificate. FIRC is

issued against any receipt of amount from foreign countries by a bank to their

customers. It can be an advance payment against export proceeds, ocean or

airfreight, or remuneration or wages under consultancy charges or for any other

reasons.

BRC means Bank Realization Certificate issued by bank to their customers against

any specific documents. Normally BRC is issued by a bank to their customer who

has been in to export business on each shipment of export proceeds. Various

export promotion agencies provide incentives, import duty exemptions and other

financial assistance to the exporters. These agencies requires to be submitted

export proof by exporters to claim such benefits. One of the proof of exports

other than export promotion copy of shipping bill (EP copy of shipping bill), MateReceipt issued by the carrier and/or customs authorized ARE-1 (for goods under

central excise only) is Bank Realization Certificate BRC issued by the respective

bank who received foreign amount for exporters.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 20/25

So once after receiving the amount under each shipment, the exporter

approaches their bank and submits the proof of exports and FIRC details (Foreign

Inward Remittance Certificate) to obtain a BRC under each shipment. This Bank

Realization Certificate BRC is submitted with the various authorities as proof of

shipment or proof of exports along with customs legal document of EP copy of shipping Bill, Mate receipt issued by carrier of goods and central excise document

of ARE – 1 where ever applicable.

Here you need to observe that an FIRC can be obtained whenever you receives

amount from foreign country. It can be an advance amount against exports or

services.

Before introducing EDI system (Electronic Data Interchange), a GR form has to be

filed by exporters along with shipping bill to customs for completion of export

procedures and formalities. The copy of shipping bill is impressed on GR form. GR

form is a document of export to be submitted with RBI to regulate foreign inward

remittance. In order to get BRC, exporter has to submit a copy of GR form to

prove the account under which they had received foreign amount.

At present, there is no FIRC or BRC required for government export promotion

agencies like DGFT or Customs department where in EDI facility available, as the

said foreign receipt is directly linked electronically with customs and DGFT

through the authorized dealer bank of exporters.

So, the exporters need not obtain FIRC (foreign inward remittance certificate) or

BRC (Bank realization certificate) from their bank to claim any export benefits

from DGFT or customs department.

9. What is ECGC?

Export Credit Guarantee Corporation of India Limited, was established in the year

1957 by the Government of India to strengthen the export promotion drive by

covering the risk of exporting on credit.

Being essentially an export promotion organization, it functions under the

administrative control of the Ministry of Commerce & Industry, Department of

Commerce, Government of India. It is managed by a Board of Directors

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 21/25

comprising representatives of the Government, Reserve Bank of India, banking,

insurance and exporting community.

ECGC is the fifth largest credit insurer of the world in terms of coverage of

national exports. The present paid-up capital of the company is Rs.800 crores andauthorized capital Rs.1000 crores.

What does ECGC do?

Provides a range of credit risk insurance covers to exporters against loss in

export of goods and services

Offers guarantees to banks and financial institutions to enable exporters to

obtain better facilities from them

Provides Overseas Investment Insurance to Indian companies investing in

joint ventures abroad in the form of equity or loan

How does ECGC help exporters?

Offers insurance protection to exporters against payment risks

Provides guidance in export-related activities

Makes available information on different countries with its own

credit ratings

Makes it easy to obtain export finance from banks/financial

institutions

Assists exporters in recovering bad debts

Provides information on credit-worthiness of overseas buyers

Need for export credit insurance

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 22/25

Payments for exports are open to risks even at the best of times. The risks have

assumed large proportions today due to the far-reaching political and economic

changes that are sweeping the world. An outbreak of war or civil war may block

or delay payment for goods exported. A coup or an insurrection may also bring

about the same result. Economic difficulties or balance of payment problems may

lead a country to impose restrictions on either import of certain goods or on

transfer of payments for goods imported. In addition, the exporters have to face

commercial risks of insolvency or protracted default of buyers. The commercial

risks of a foreign buyer going bankrupt or losing his capacity to pay are aggravated

due to the political and economic uncertainties. Export credit insurance is

designed to protect exporters from the consequences of the payment risks, both

political and commercial, and to enable them to expand their overseas business

without fear of loss.

10. RBI guidelines for getting funds from the final customers.

Write off of unrealised Export Bills

(i) In cases where the exporter has not been able to realise the outstanding

export dues despite his best efforts, he may approach the authorised dealer, whohad handled the relevant shipping documents, with appropriate supporting

documentary evidence with a request for write off of the unrealised portion.

Authorised dealers may accede to such requests (the branch concerned should

obtain the approval of its controlling office) subject to the undernoted conditions:

(a) The relevant amount has remained outstanding for 360 days or more.

(b) The aggregate amount of write off allowed by the authorised dealer (at all

branches put together) during a calendar year should not exceed 10% of the total

export proceeds realised by the exporter through the concerned authorised

dealer during the previous calendar year.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 23/25

(c) Satisfactory documentary evidence has been furnished in support of the

exporter having made all efforts to realise the dues but has been unsuccessful

due to reasons beyond his control.

(d) The case falls under any of the undernoted categories:

(i) The overseas buyer has been declared insolvent and a

certificate from the official liquidator indicating that there is no possibility of

recovery of export proceeds has been produced. (Names, addresses and other

relevant particulars of the overseas buyers who have been declared insolvent may

be intimated to ECGC for updating their files on buyers).

(ii) The overseas buyer has not been traceable over a

reasonably long period of time and suitable supporting documentary evidence to

that effect has been produced. (His name, original address and other relevant

particulars may be reported to ECGC, for updating their files).

(iii) The goods exported have been auctioned or destroyed

by the Port/Customs/Health authorities in the importing country and a certificate

issued by the said authorities or the Indian Mission or Chamber of Commerce in

the country of destination indicating that the goods have been auctioned or

destroyed has been produced.

(iv) The unrealised amount represents the balance due in a

case settled through the intervention of the Indian Embassy, Foreign Chamber of

Commerce or similar Organisation.

(v) The unrealised amount represents the undrawn balance of

an export bill (not exceeding 10 per cent of the invoice value) and has remained

outstanding and turned out to be unrealisable despite all efforts made by the

exporter. The authorised dealer should take into consideration the track record of the exporter, documentary evidence/correspondence showing that there is no

possibility of recovery of the undrawn balance, frequency of similar cases

considered in the past and the antecedents of the overseas buyer, if available,

before allowing the closure.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 24/25

(vi) The cost of resorting to legal action would be

disproportionate to the unrealised amount of the export bill or where the

exporter even after winning the Court case against the overseas buyer could not

execute the Court decree due to reasons beyond his control and sufficient

documentary evidence is produced to fully satisfy the authorised dealer.

(vii) Bills were drawn for the difference between the letter of

credit value and actual export value or between the provisional and the actual

freight charges but the amount has remained unrealised consequent on

dishonour of the bills by the overseas buyer and documentary evidence is

produced to show that there are no prospects of realisation.

(e) The case is not the subject matter of any civil or criminal suit which is

pending.

(f) The exporter has not come to the adverse notice of the Enforcement

Directorate or the Central Bureau of Investigation or such other law enforcement

agency.

(g) The exporter has surrendered proportionate export incentives, if any,

availed in respect of the relative shipments.

(ii) The documentary evidence received by the authorised dealer should be

kept for a period of two years or till their verification by the Reserve Bank's

Inspectors, whichever is earlier. A half yearly statement, as on June 30 and

December 31, showing particulars of export bills allowed to be written off should

be furnished to Reserve Bank in form EBW. The statement should be submitted

within fifteen days from the close of the relative half year. Where there is nofurther amount to be realised against the GR / PP form covered by the write off,

authorised dealer should submit the duplicate thereof to Reserve Bank along with

'R' return, duly certified.

7/27/2019 IM Marketing

http://slidepdf.com/reader/full/im-marketing 25/25