Imperfect Competition

Economics 101

Imperfect Competition

Imperfect competition refers to those market structures that fall between perfect competition and pure monopoly.

Imperfect competition includes industries in which firms have competitors but do not face so much competition that they are price takers.

Types

Types of Imperfectly Competitive Markets Monopolistic Competition

Many firms selling products that are similar but not identical.

OligopolyOnly a few sellers, each offering a similar or identical

product to the others.

Monopolistic Competition

Definition

Monopolistic CompetitionMany firms selling products that are similar but not

identical.

Markets that have some features of competition and some features of monopoly.

Attributes

Attributes of Monopolistic Competition Many sellers Product differentiation Free entry and exit

Attribute 1

Many Sellers There are many firms competing for the same

group of customers.Product examples include books, CDs, movies,

computer games, restaurants, piano lessons, cookies, furniture, etc.

Attribute 2

Product Differentiation Each firm produces a product that is at least

slightly different from those of other firms. Rather than being a price taker, each firm faces

a downward-sloping demand curve.

Attribute 3

Free Entry or Exit Firms can enter or exit the market without

restriction. The number of firms in the market adjusts

until economic profits are zero.

Short-Run Economic Profits

The Monopolistically Competitive Firm in the Short Run Short-run economic profits encourage new firms to enter

the market. This: Increases the number of products offered. Reduces demand faced by firms already in the market. Incumbent firms’ demand curves shift to the left. Demand for the incumbent firms’ products fall, and their profits

decline.

Copyright©2003 Southwestern/Thomson Learning

Quantity0

Price

Profit-maximizing

quantity

Price

Demand

MR

ATC

(a) Firm Makes Profit

Averagetotal cost

Profit

MC

Short-Run Economic Losses

The Monopolistically Competitive Firm in the Short Run Short-run economic losses encourage firms to exit the

market. This: Decreases the number of products offered. Increases demand faced by the remaining firms. Shifts the remaining firms’ demand curves to the right. Increases the remaining firms’ profits.

Copyright©2003 Southwestern/Thomson Learning

Demand

Quantity0

Price

Price

Loss-minimizing

quantity

Averagetotal cost

(b) Firm Makes Losses

MR

LossesATC

MC

Long-Run Equilibrium

Firms will enter and exit until the firms are making exactly zero economic profits.

Copyright©2003 Southwestern/Thomson Learning

Quantity

Price

0

DemandMR

ATC

MC

Profit-maximizingquantity

P = ATC

Characteristics of Long-Run Equilibrium

Two Characteristics As in a monopoly, price exceeds marginal cost.

Profit maximization requires marginal revenue to equal marginal cost.

The downward-sloping demand curve makes marginal revenue less than price.

As in a competitive market, price equals average total cost.

Free entry and exit drive economic profit to zero.

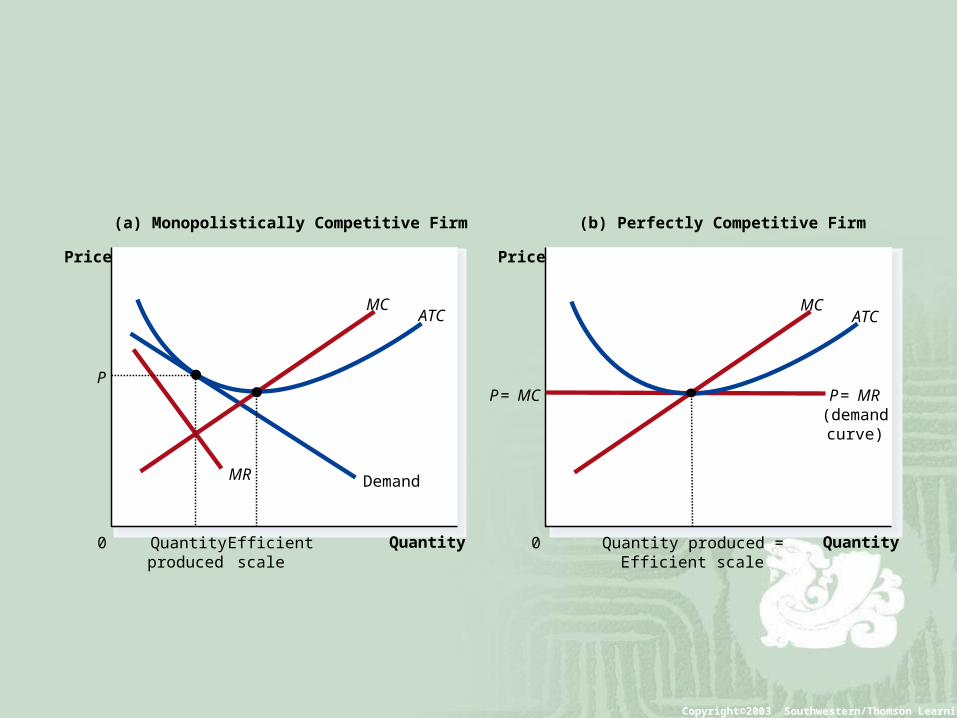

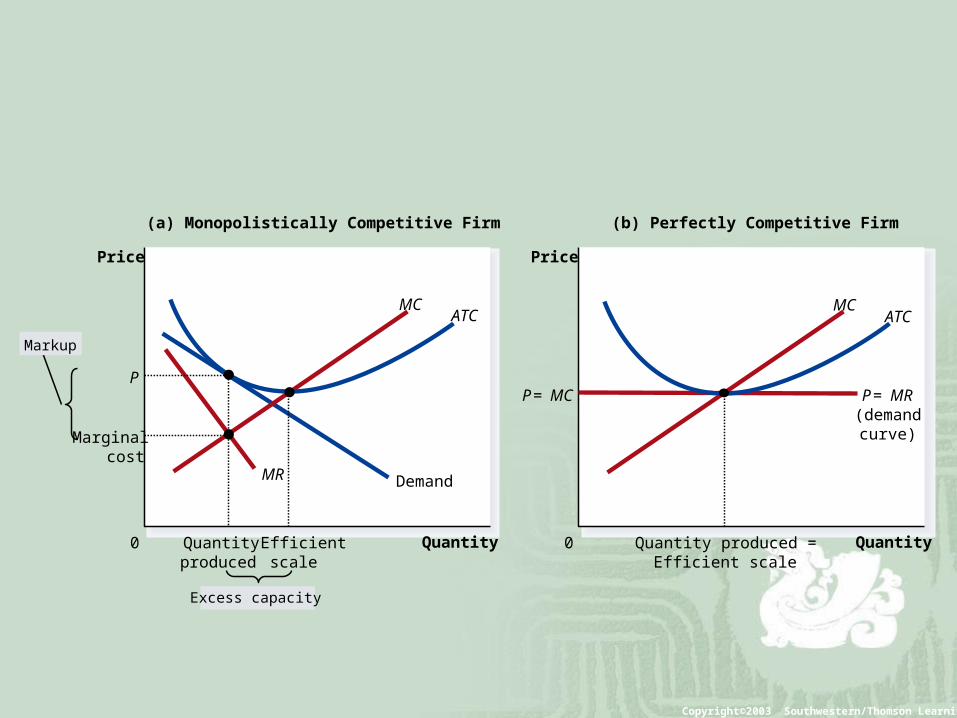

Monopolistic versus Perfect Competition

There are two noteworthy differences between monopolistic and perfect competition—excess capacity and markup.

Excess Capacity

Excess Capacity There is no excess capacity in perfect competition in the

long run. Free entry results in competitive firms producing at the

point where average total cost is minimized, which is the efficient scale of the firm.

There is excess capacity in monopolistic competition in the long run.

In monopolistic competition, output is less than the efficient scale of perfect competition.

Copyright©2003 Southwestern/Thomson Learning

Quantity0

Price

Demand

(a) Monopolistically Competitive Firm

Quantity0

Price

P = MC P = MR(demand

curve)

(b) Perfectly Competitive Firm

MCATC

MCATC

MR

Efficientscale

P

Quantityproduced

Quantity produced =Efficient scale

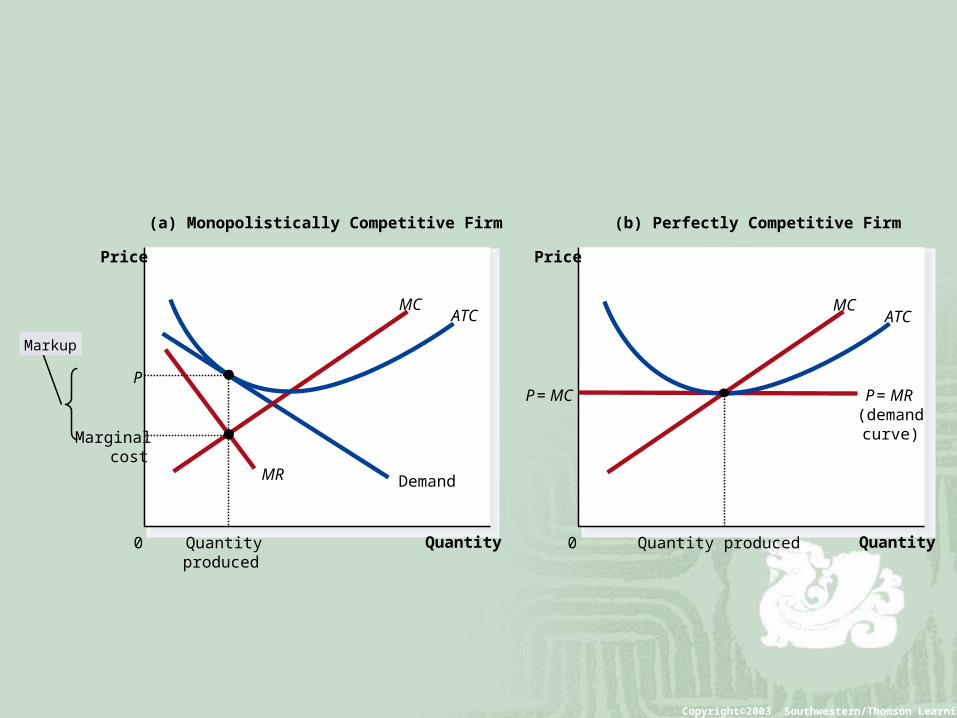

Markup

Markup Over Marginal Cost For a competitive firm, price equals marginal

cost. For a monopolistically competitive firm, price

exceeds marginal cost. Because price exceeds marginal cost, an extra

unit sold at the posted price means more profit for the monopolistically competitive firm.

Copyright©2003 Southwestern/Thomson Learning

Quantity0

Price

Demand

(a) Monopolistically Competitive Firm

Quantity0

Price

P = MC P = MR(demand

curve)

(b) Perfectly Competitive Firm

Markup

MCATC

MCATC

MR

Marginalcost

P

Quantityproduced

Quantity produced

Copyright©2003 Southwestern/Thomson Learning

Quantity0

Price

Demand

(a) Monopolistically Competitive Firm

Quantity0

Price

P = MC P = MR(demand

curve)

(b) Perfectly Competitive Firm

Markup

Excess capacity

MCATC

MCATC

MR

Marginalcost

Efficientscale

P

Quantityproduced

Quantity produced =Efficient scale

Monopolistic Competition and Welfare of Society

Monopolistic competition does not have all the desirable properties of perfect competition.

There is the normal deadweight loss of monopoly pricing in monopolistic competition caused by the markup of price over marginal cost.

Monopolistic Competition and Welfare of Society

However, the administrative burden of regulating the pricing of all firms that produce differentiated products would be overwhelming.

Another way in which monopolistic competition may be socially inefficient is that the number of firms in the market may not be the “ideal” one. There may be too much or too little entry.

Advertising

When firms Sell differentiated products At price above marginal cost

Then, they have incentive to advertise To attract more buyers

25

Oligopoly and Game Theory

Key Feature

Because of the few sellers, the key feature of oligopoly is the tension between cooperation and self-interest.

Characteristics

Characteristics of an Oligopoly Market Few sellers offering similar or identical products Interdependent firms Best off cooperating and acting like a

monopolist by producing a small quantity of output and charging a price above marginal cost

Simple Type: Duopoly

A duopoly is an oligopoly with only two members. It is the simplest type of oligopoly.

Duopoly Oligopoly with only two members Decide quantity to sell Price – determined on the market

By demand

30

The Demand Schedule for Water

Production Decisions

For a perfectly competitive firm Price = marginal cost Quantity = efficient

For a monopoly Price > marginal cost Quantity < efficient quantity

31

Markets with a few Sellers

Duopoly Collude and form a cartel

Act as a monopoly Total level of production Quantity produced by each member

Don’t collude – self-interestDifficult to agree; Antitrust lawsHigher quantity; lower price; lower profit

Not competitive allocation

Nash equilibrium

32

Collusion and Cartel

The duopolists may agree on a monopoly outcome. Collusion

An agreement among firms in a market about quantities to produce or prices to charge.

CartelA group of firms acting in unison.

Is Cartel Possible?

Although oligopolists would like to form cartels and earn monopoly profits, often that is not possible. Antitrust laws prohibit explicit agreements among oligopolists as a matter of public policy.

The Equilibrium for an Oligopoly

A Nash equilibrium is a situation in which economic actors interacting with one another each choose their best strategy given the strategies that all the others have chosen.

The equilibrium for an Oligopoly

When firms in an oligopoly individually choose production to maximize profit, they produce quantity of output greater than the level produced by monopoly and less than the level produced by competition.

The oligopoly price is less than the monopoly price but greater than the competitive price (which equals marginal cost).

Size of an Oligopoly

How increasing the number of sellers affects the price and quantity: The output effect: Because price is above

marginal cost, selling more at the going price raises profits.

The price effect: Raising production will increase the amount sold, which will lower the price and the profit per unit on all units sold.

Size of an Oligopoly

As the number of sellers in an oligopoly grows larger, an oligopolistic market looks more and more like a competitive market.

The price approaches marginal cost, and the quantity produced approaches the socially efficient level.

Strategic Action

Because the number of firms in an oligopolistic market is small, each firm must act strategically.

Each firm knows that its profit depends not only on how much it produces but also on how much the other firms produce.

Game Theory

Game theory is the study of how people behave in strategic situations.

Strategic decisions are those in which each person, in deciding what actions to take, must consider how others might respond to that action.

Prisoners’ Dilemma

The prisoners’ dilemma provides insight into the difficulty in maintaining cooperation.

Often people (firms) fail to cooperate with one another even when cooperation would make them better off.

The prisoners’ dilemma is a particular “game” between two captured prisoners that illustrates why cooperation is difficult to maintain even when it is mutually beneficial.

Copyright©2003 Southwestern/Thomson Learning

Bonnie’ s Decision

Confess

Confess

Bonnie gets 8 years

Clyde gets 8 years

Bonnie gets 20 years

Clyde goes free

Bonnie goes free

Clyde gets 20 years

gets 1 yearBonnie

Clyde gets 1 year

Remain Silent

RemainSilent

Clyde’sDecision

Dominant Strategy

The dominant strategy is the best strategy for a player to follow regardless of the strategies chosen by the other players.

Dominant strategies in Prisoners’ dilemma:

_ Clyde: Confess

_ Bonnie: Confess

Nash Equilibrium & Best Outcome

Nash Equilibrium (self-interest): _ Clyde: Confess & Bonnie: Confess Best Outcome (cooperation): _ Clyde: Silent & Bonnie: Silent

Cooperation is difficult to maintain, because cooperation is not in the best interest of the individual player.

Game Example: OPEC

Iraq and Iran: Members of OPEC Their decisions on oil production. Decisions: High Production or Low

Production

Copyright©2003 Southwestern/Thomson Learning

Iraq’s Decision

High Production

High Production

Iraq gets $40 billion

Iran gets $40 billion

Iraq gets $30 billion

Iran gets $60 billion

Iraq gets $60 billion

Iran gets $30 billion

Iraq gets $50 billion

Iran gets $50 billion

Low Production

LowProduction

Iran’sDecision

Nash Equilibrium

Dominant strategies: _ Iran: High Production _ Iraq: High Production

Nash Equilibrium (self-interest): _ Iran: High Production & Iraq: High Production

Best Outcome (cooperation): _ Iran: low production & Iraq: low production

Game Example: Where to Advertise?

Players: Competitor.com or We.com Decisions: NBA and NHL

No Nash equilibrium in pure strategies

Competitor.com

NBA NHL

NBA W: 4, C: 3

W: 3, C: 4

We.com NHL W: 3,

C: 4 W: 4, C: 3

Where to advertise?

No Nash Equilibrium

Dominant strategies: _ We.com: none _ Competitor.com: none Nash Equilibrium (self-interest): _ We.com: none _ Competitor.com: none

Game Example: Evening News

Players: ATV and TVB Decisions: 7:30 pm or 8:00 pm

Evening News:

TVB

7:30pm 8:0pm

7:30pm A: 1, B: 1

A: 3, B: 4

ATV 8:0pm A: 4, B: 3

A: 2.5, B: 2.5

Nash Equilibrium

Dominant strategies: _ ATV: none _ TVB: none Two Nash Equilibria (self-interest):

_ ATV: 7:30pm & TVB: 8:00pmor _ ATV: 8:00pm & TVB: 7:30pm

Why People Sometimes Cooperate

Firms that care about future profits will cooperate in repeated games rather than cheating in a single game to achieve a one-time gain.

Repeated prisoners’ dilemma Encourage cooperation

Penalty for not cooperating

Better strategyReturn to cooperative outcome after a period of

noncooperation

Best strategy: tit-for-tatPlayer - start by cooperating

Then do whatever the other player did last time

Starts out friendlyPenalizes unfriendly playersForgives them if warranted

55

Public Policy Toward Oligopolies

Controversies over antitrust policies Most commentators agree that price-fixing

agreements among firms should be illegal. Yet the antitrust laws have been used to condemn some business practices whose effects are not obvious. There are three examples of controversial business practice:Resale price maintenancePredatory pricingTying

Resale price maintenance

Resale price maintenance (fair trade) Require retailers to charge customers a given

price Might seem anticompetitive

Prevents the retailers from competing on price

Defenders:Not aimed at reducing competitionLegitimate goal: Prevent from free rider problem

Example

Superduper sells disc players to retailers for $100. Require retailers to charge customers a given price, say

$150. Might seem anticompetitive

Prevents the retailers from charging less than $150 Defenders:

Superduper would be worse off if its retailers were a cartel, so it is not aimed at reducing competition.

Legitimate goal of resale price maintenance Without resale price maintenance, some customers

would take advantage of one store’s service, and then buy the item at a discount retailer. Resale price maintenance prevents from free rider problem.

Public Policy Toward Oligopolies

Predatory pricing Charge prices that are too low

AnticompetitivePrice cuts may be intended to drive other firms out of

the market

SkepticsPredatory pricing – not a profitable strategyPrice war - to drive out a rival

Prices - driven below cost

Example

Coyote Air has a monopoly on some route. Roadrunner Express enters and takes 20% of the market.

Coyote’s anticompetitive move: slashing its fare. The price cut (predatory pricing) of Coyote intends to drive

Roadrunner out of the market. Prices have to be driven below cost.

Coyote sells cheap tickets at a loss, and low fares attract more customers. Therefore, Coyote had better be ready to fly more planes. Meanwhile, Roadrunner can respond to Coyote’s predatory pricing by cutting back on flights. As a result, Coyote ends up bearing more losses.

The predator suffers more than the prey.

Public Policy Toward Oligopolies

Tying Offer two goods together at a single price

Expand market power

SkepticsCannot increase market power by binding two goods

together

Form of price discriminationTying may increase profit

Example Makemoney Movie produces two films. It offers theaters the two films

(Film A is a blockbuster, and Film B is art film) together at a single price. Makemoney uses tying as a mechanism for expanding its market power. Skeptical: forcing a theater to accept a worthless movie as part of the

deal does not increase the theater’s willingness to pay. Makemoney cannot increase its market power simply by using tying.

Tying exists because it is a form of price discrimination. Suppose there are two theaters. Theater 1 is willing to pay $15000 for film A and $5000 for film B. Theater 2 is willing to pay $5000 for film A and $15000 for film B.

Pricing strategy for each film: $15000; Tying strategy for two films :$20000

Tying allows Makemoney to increase profit by charging a combined price.