FILE

FILE COPYBERNSTEIN LIEBHARD & LIFSHITZ, LLP 05 JUN,Jeffrey M. Haber (JH-1738)Abraham, L Katsman (AK-7306)10 East 40 Street, 22nd Floor U.S, D}sT o COURTNew York, NY 10016Tel: {212} 779-1414

GLANCY BINKOW & GOLDBERG LLPLionel Z . GlancyNeal A. DublinskyAvi N. Wagner1801 Avenue of the Stars, Suite 311Los Angeles, CA 90067Tel: (310) 201-9150

Lead Counsel for Plaintiff s and the Class

UNITED STATES DISTRICT COURTSOUTHERN DISTRICT OF NEW YORK

IN RE: LUMENIS, LTD. ) MASTER FILE NO.: 02-CV- 1989 (DAB)SECURITIES LITIGATION

3

This Document Relates to: )All Actions }

SECOND AMENDED CONSOLIDATED CLASS ACTION COMPLAINT

Lead Plaintiffs, Thomas W. Pruter FBD Stonehedge Securities LLC, Efraiwra Zwecker, and

Jacob Caspi, individually and on behalf of all other persons similarly situated by and through their

attorneys , allege upon the investigation of counsel, which included, inter alma a review of relevant

public filings made by Lumenis Ltd. ("Lumenis" or the "Company"} with the Securities and

Exchange Commission (the "SEC "), as well as teleconferences , press releases , news articles,

analyst reports, and media reports concerning the Company. Plaintiffs ' investigation also included

interviews with former employees ofthe Company and distributors of the Company' s products

and court filings (including a sworn declaration) by Defendant Asif Adil, former Chief Financial

Officer of Lumenis, in his lawsuit, origina lly filed in the federal court in New Jersey , against the

Company. Defendant Adil's complaint against Lurnenis is attached hereto as Exhibit ("Ex.") A,

and the Declaration ofAsifAdil fled in that action is attached as Ex . 13 hereto.

This Complaint is based upon personal knowledge as to the named plaintiffs' own acts,

and upon information and belief as to all other matters, based upon the aforementioned

investigation.

SUMMARY OF ACTION

Lead Plaintiffs bring this action as a class action on behalf of all persons, other than

Defendants, who purchased or otherwise acquired Lumenis securities during the period beginning

October 2, 2000, through May 16, 2002, inclusive (the "Class Period"), to recover damages

caused by Defendants' violations of the federal securities laws.

During the Class Period, Defendants engaged in fraudulent accounting practices,

including, but not limited to. improper revenue recognition, channel stuffing, `Found-tripping,"

improper manipulation of accounts for bad debt and inventory, short shipments, and improper

write-offs. Defendants used these improper accounting practices to inflate Lumenis's financial

results, resulting in the artificial inflation of its stock price The use of these fraudulent practices

rendered the Company's statements of actual and projected financial results materially false and

misleading.

Defendants then sold more than $45 inil lion of Lurnenis stock at artificially inflated

prices; used artificially inflated Lumenis stock as currency in a major acquisition; used the

acquisition to hide financial problems; and discounted and disputed marketplace rumors about

Company operations even as they knew it was being investigated by the SEC and that its

distributors had been contacted by the SEC. For months prior to the investigation, Defendants

were knowingly and/or recklessly engaging in fraudulent accounting practices, as confirmed by

the Company's former Chief Financial Officer, Defendant Asif Adil, and others. Additionally,

even after announcing in a press release that it was subject to an informal inquiry by the SEC, the

Company continued to hide the fact that it had been aware of the SEC inquiry and had been

providing information to the SEC for several weeks.

4. On February 28, 2002, in a conference call, the Company revealed the SEC

investigation. This revelation caused the market to question the propriety ofLumenis's reported

financial results and caused the price of Luznenis stock to fall 30% in one day, and more than 69%

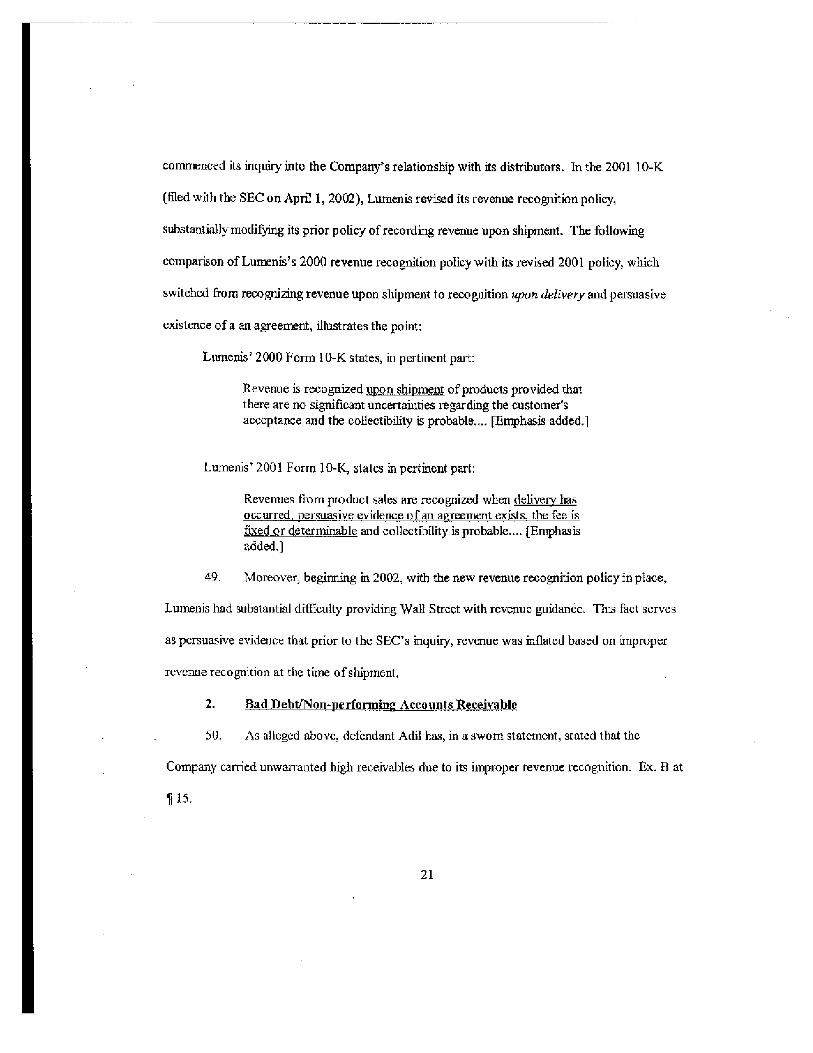

from its Class Period high, damaging plaintiffs thereby. This price decline was a foreseeable result

of the fraudulent conduct complained of herein.

5. Nonetheless, artificial inflation remained in Lumenis's share price, as the full

effects of the SEC's investigation and the impact ofthe accounting machinations complained of

herein had not yet been revealed to the market. Now under the watchful eye of the SEC,

Defendants were not able to engage in the same fraudulent accounting practices as before, and on

which Defendants had relied to create the illusion of financial success. As a result, on May 7,

2002, the Company announced that it would badly miss earnings projections for Q1 2002. The

already depressed stock plunged over 50°% on the news to $3.30 per share, on volume 15 times its

daily average. Defendants responded with false reassurances of expected profitability, which

caused the stock price to temporarily recover. On May 16, 2002, however, the SEC announced

that it was raising the level of its inquiry to a ku-m a! investigation of the Company and its

accounting practices. The stock price dropped 22% on the news.

3

6. The Company's share price has not recovered from Defendants ' fraud, and

currently trades at under $2 per share . This figure stands in marked contrast to the $21431 per

share at which certain Defendants sold their shares . In the aftermath of this collapse, defendants

Sutton and S. Genger were terminated (defendant Adil was tent inated during the Class Period

after complaining ofthe fraud alleged herein).

7. Further, on February 5, 2004 , the Company announced its delisting from the

NASDAQ National Exchange to the pink sheets where it now trades. The fraud complained of

also led to the resignation of Lumenis' Class Period auditors in May 2004. Finally, the Company

announced on February 21, 2005 that it received a notification -- referred to as a "Wells Notice"

-- from the Boston District Office ofthe SEC notifying the Company ofthe SEC's intention to

recommend that a civil proceeding brought against the Company for violations of the antifraud

and other provisions of the U.S. federal securities laws in connection with the Company's 2002

and 2003 financial reporting.

JURISDICTION AND VENUE

8. The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a) of

the Exchange Act [15 U.S.C. §§ 78j(b) and 78t(a)] and Rule lOb-5 promulgated under Section

10(b) by the SEC [17 C.F.R. § 240.lOb-5].

9. This Court has jurisdiction over the subject matter of this action pursuant to 28

U.S.C. §§ 1331 and 1337 and Section 27 of the Exchange Act [15 U.S.C. § 78aaj.

10. Venue is proper in this District pursuant to Section 27 of the Exchange Act, and

28 U_S.C. 1391(b)_ Many of the acts and practices complained of herein occurred in substantial

part in this District. Additionally, Lumenis maintains an office in this District. In connection with

4

the acts alleged in this Complaint, Defendants, directly or indirectly, used the means and

instrumentalities of interstate commerce, including, but not limited to, the mails, interstate

telephone communications and the facilities of the national securities markets.

PARTIES

11. In an Order dated June 17, 2003, this Court consolidated the then-pending related

actions for all purposes, and appointed Thomas W. Pruter FBO Stonehedge Securities LLC,

Efrain Zwecker, and Jacob Caspi as Lead Plaintiffs. Lead Plaintiffs purchased Lumenis securities

as set forth in the certifications submitted with their lead plaintiff motion, and were damaged

thereby.

12. Defendant Lumenis is an Israeli corporation with its principal offices at the

Yokneam Industrial Park, Yokncam 20692, Israel. The Company also maintains a U.S.-based

office located at 375 Park Avenue, 11th Floor, New York, New York 10152. Lumenis,

formerly known as ESC Medical Systems Ltd. ("ESC"), designs, manufactures and markets a

range of pulsed light and laser-based systems for the aesthetic surgical, ophthalmic and medical

communities. The Company also develops, manufactures and markets medical devices utilizing

lasers and proprietary intense pulsed light technology for non-invasive hair removal, treatment of

varicose veins and other benign vascular lesions, as well as other clinical applications such as

ophthalmic and dental.

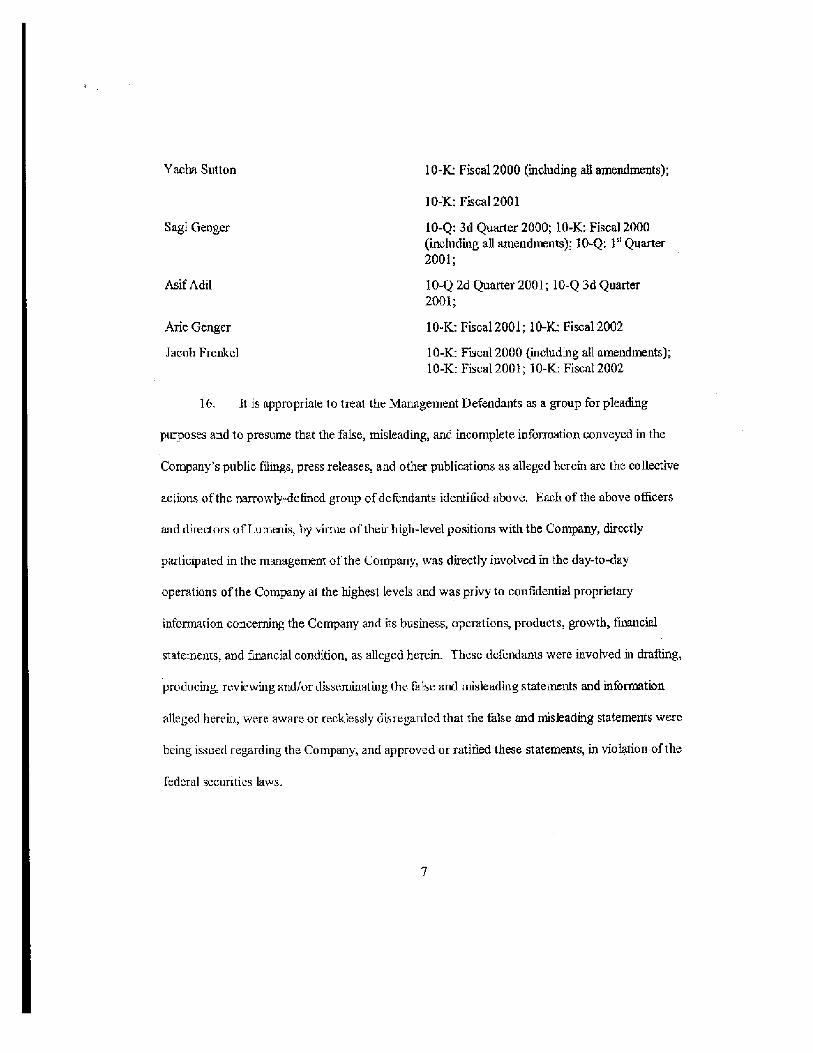

13. Defendants listed below served, at all times relevant to this Complaint, as senior

officers and/or directors of Lumems:

a. Ya.cha Sutton ("Sutton"), President and Chief Executive Officer;

5

b. Sagi Genger ("S. Genger"), Chief Financial Officer and Chief Operating

Officer;

c. Asif Adil ("Adis"), Executive Vice-President for Business Development,

and for part of 2001, Chief Financial Officer,

d. Aria Ganger ("A. Genger"), Director and Vice Chairman of the Board of

Directors since July 16, 2001, Controlling Shareholder of Lumenis and father of S. Genger; and

e. Jacob Frankel {"Frenkel"), Chairman of the Board of Directors.

14. Defendants Sutton, S. Genger, Adil, and Frenkel are sometimes herein referred to

as the "Management Defendants." By reason of their management positions and responsibilities

and/or stock holdings during the time relevant to this Complaint, the Managerneni Defendants

were "controlling persons" of Lumens within the meaning ofSection 20 ofthe Exchange Act,

and had the power and influence to control Lumenis and exercised such control to cause the

Company to engage in the violations and improper practices complained of herein. The

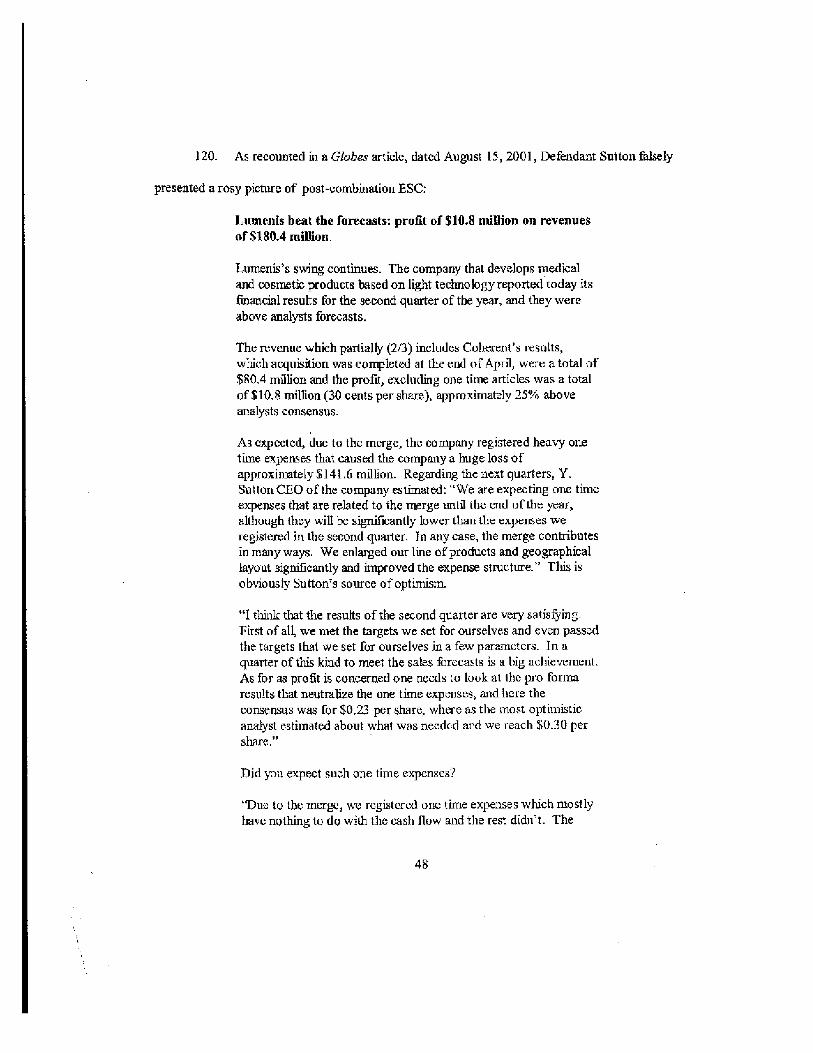

Management Defendants, due to their positions as officers and/or directors of f.u nis, had

access to adverse, non-public information about Lumenis and acted to conceal and misrepresent

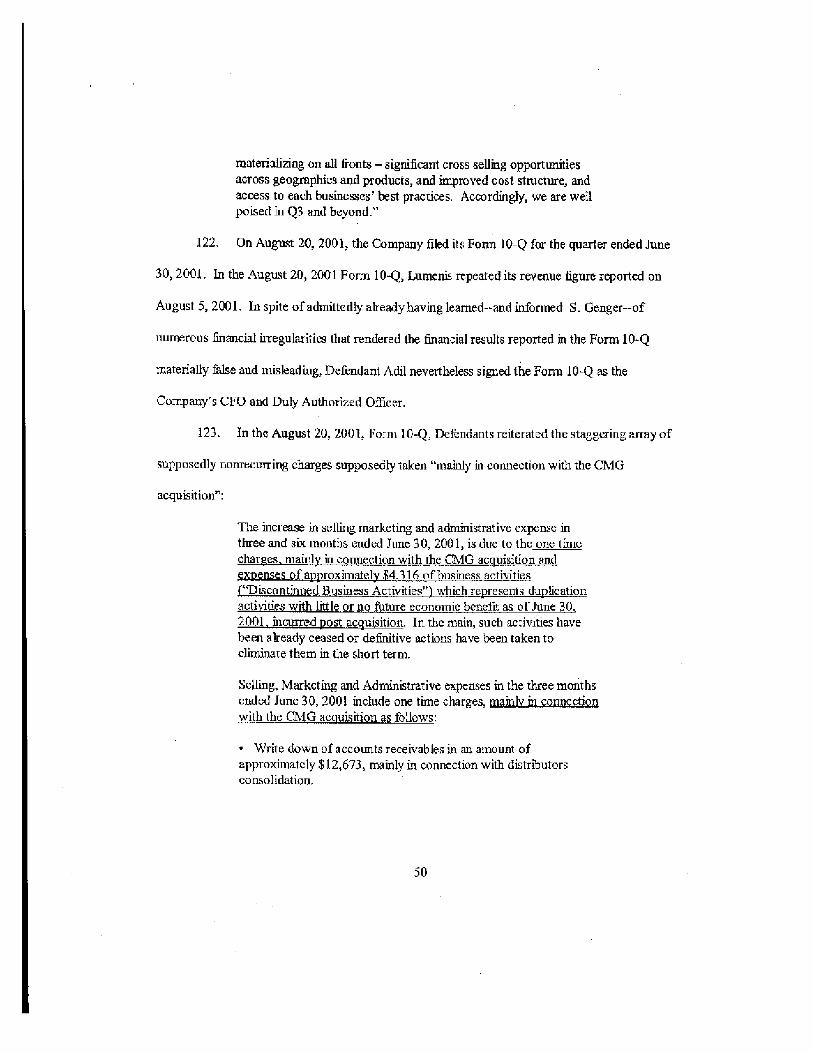

such material informnation in violation of their duties and responsibilities under the federal

securities laws.

15. The Management Defendants signed various SEC filings made by Lumenis as

follows:

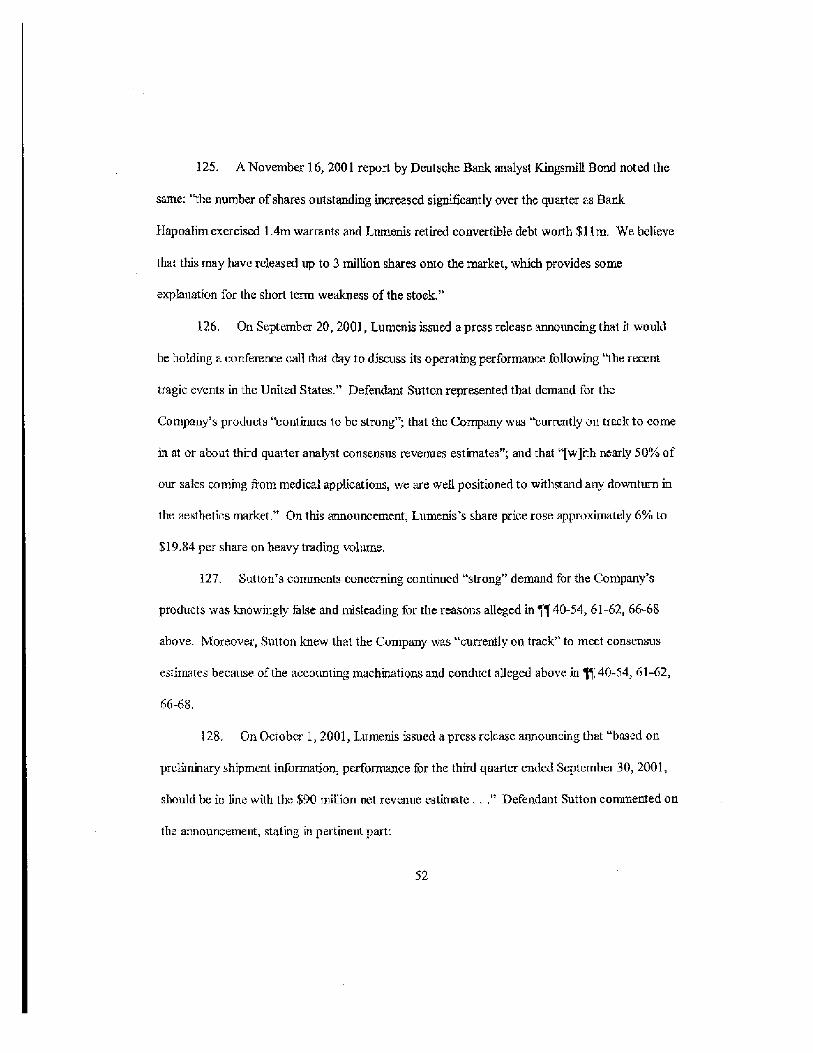

Defendant Lumenis Quarterly and Annual FilingsSigped

6

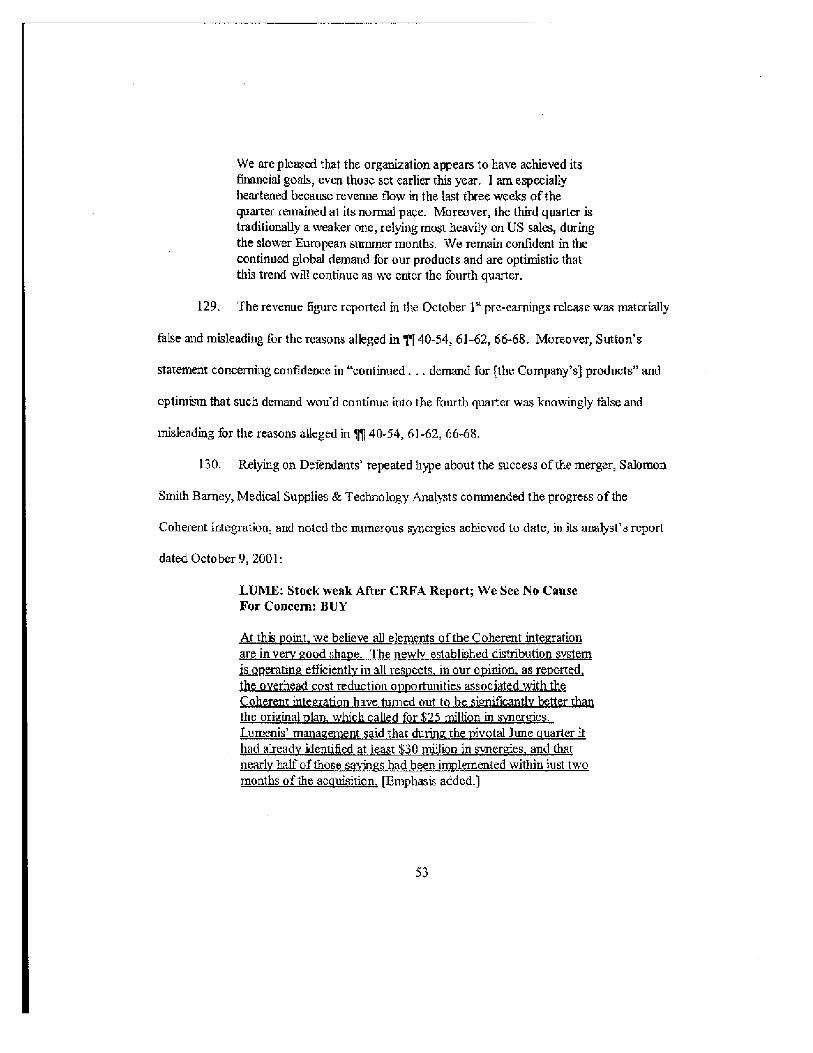

Yacha Sutton 10-K: Fiscal 2000 (including all amendments);

l0-K: Fiscal 2001

Sagi Genger 10-Q: 3d Quarter 2000; 10-K: Fiscal 2000(including all amendments); 10-Q: 18` Quarter2001;

Asif Adil IQ-Q 2d Quarter 2001; 10-Q 3d Quarter2001;

Arie Genger 10-K: Fiscal 2001; 10-K: Fiscal 2002

Jacob Frenkel 10-K: Fiscal 2000 (including all amendments);

10-K: Fiscal 2001; 10-K: Fiscal 2002

16. It is appropriate to treat the Management Defendants as a group for pleading

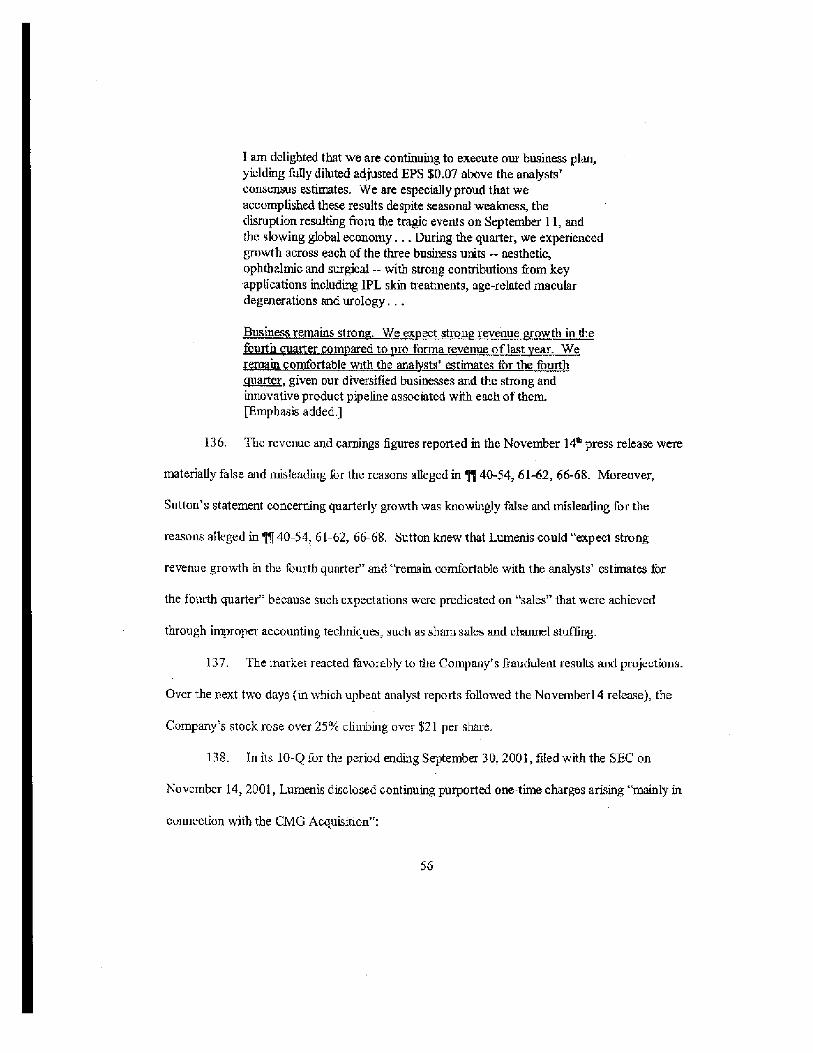

purposes and to presume that the false, misleading, and incomplete information conveyed in the

Company's public filings, press releases, and other publications as alleged herein are the collective

actions ofthe narrowly-dcfincd group ofdefendants identified above. Each of the above officers

and directors ofLunrenis, by virtue of their high-level positions with the Company, directly

participated in the management of the Company, was directly involved in the day-to-day

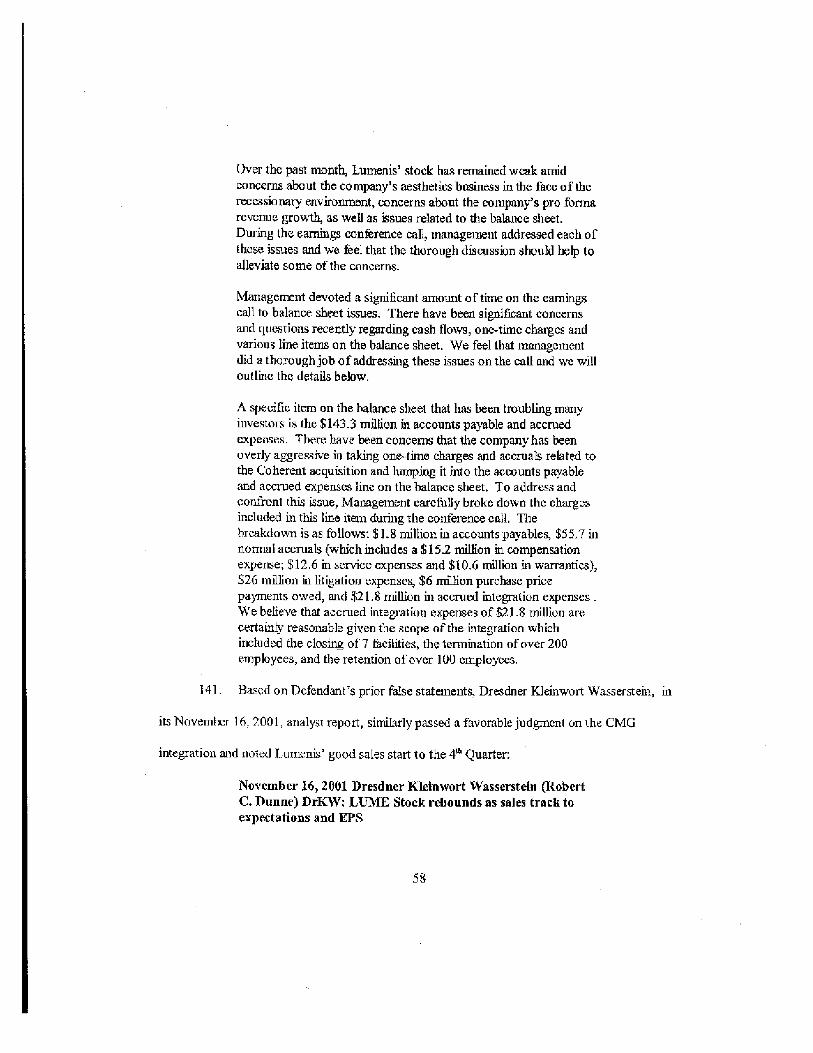

operations of the Company at the highest levels and was privy to confidential proprietary

information concerning the Company and its business, operations, products, growth, financial

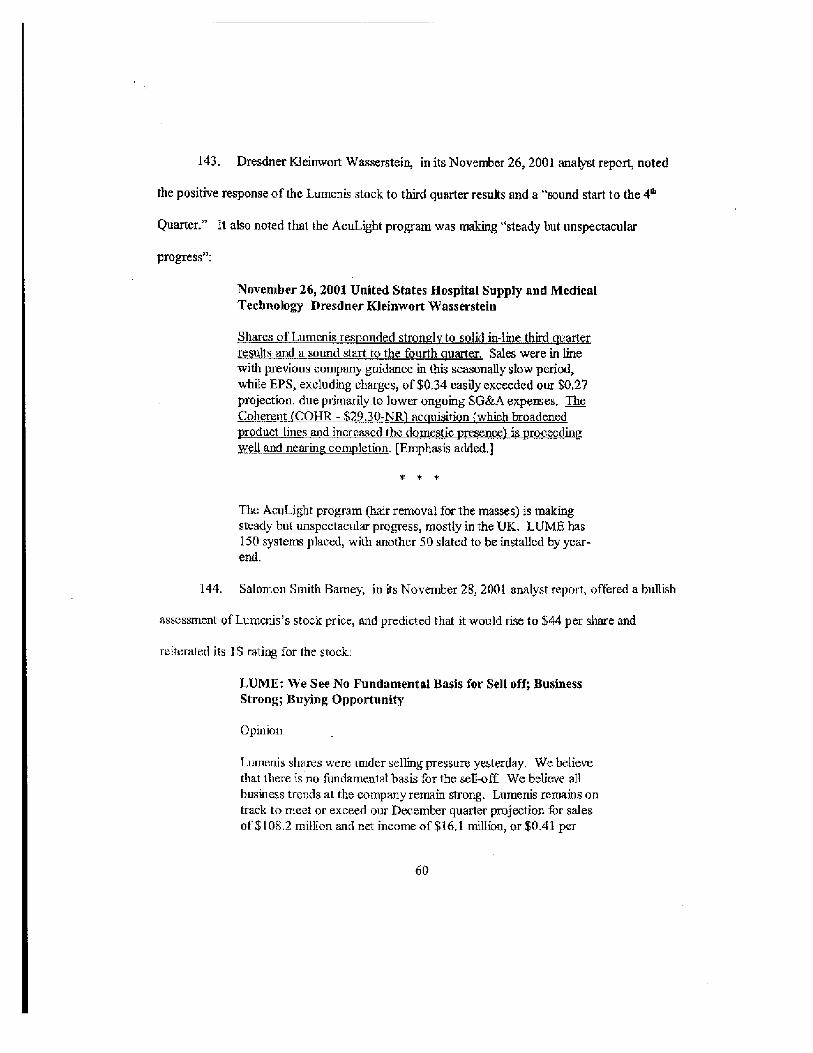

statements, and financial condition, as alleged herein. These defendants were involved in drafting,

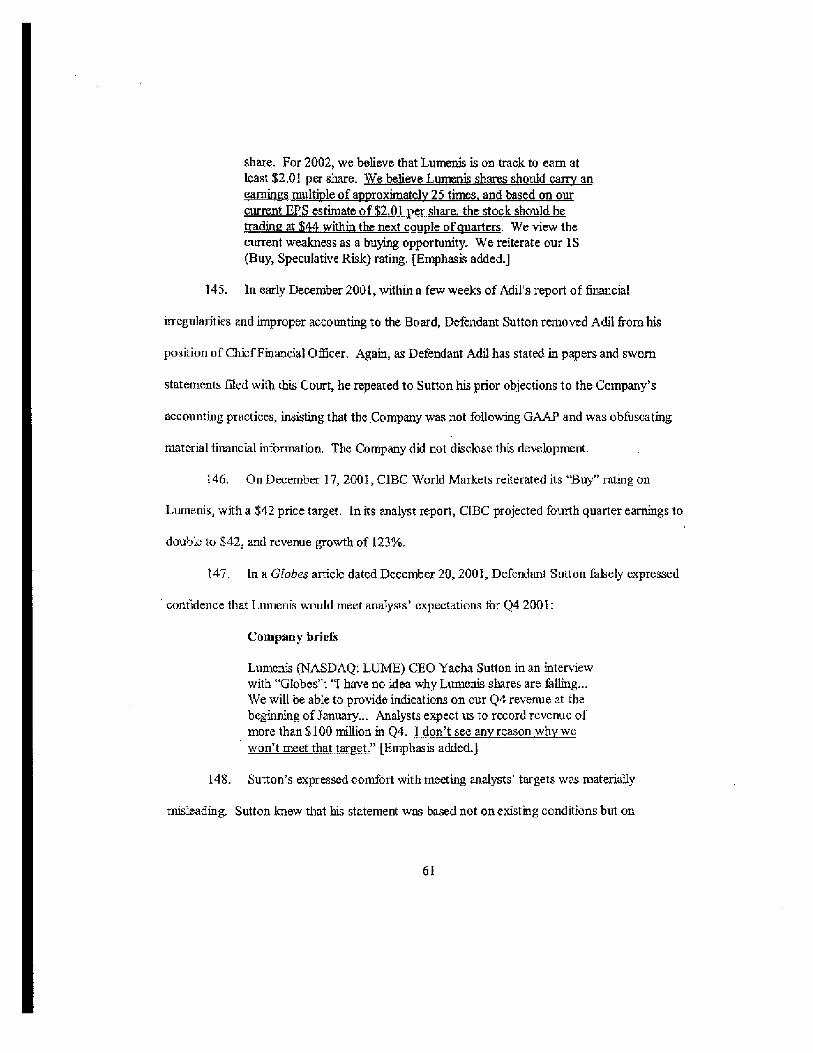

producing, reviewing End/or disseminating the false and misleading statements and information

alleged herehi, were aware or recklessly disregarded that the false and misleading statements were

being issued regarding the Company, and approved or ratified these statements, in violation of the

federal securities laws.

7

17. As officers, directors, and controlling persons of a publicly-held company, whose

common stock was, and is, registered with the SEC pursuant to the Exchange Act, traded on the

NASDAQ National Market System (the "NASDAQ"), and governed by the provisions of the

federal securities laws, Defendants had a duty to disseminate promptly, accurate and truthful

information with respect to the Company's financial condition and performance, growth,

operations, financial statements, business, products, markets, management, earnings and present

and future business prospects, and to correct any previously-issued statements that had become

materially misleading or untrue, so that the market price of the Company's publicly-traded

securities would be based upon truthful and accurate information. Defendants' misrepresentations

and omissions during the Class Period violated these specific requirements and obligations.

Defendants participated in the drafting, preparation, and/or approval of the various public

shareholder and investor reports and other communications complained of herein and were aware

of, or recklessly disregarded, the misstatements contained therein and omissions therefrom, and

were aware of their materially false and misleading nature. Because of their directorship and/or

executive and managerial positions with Lumenis, each of the Defendants had access to the

adverse, undisclosed information about Lumenis's business prospects and financial condition and

performance as particularized herein and knew (or recklessly disregarded) that these adverse facts

rendered the positive representations made by or about Lumenis and its business issued or

adopted by the Company materially false and misleading.

18. Defendants, because of their positions of control and authority as officers and/or

directors of the Company, were able to and did control the content of the various SEC filings,

press releases and other public statements pertaining to the Company during the Class Period.

Each Defendant was provided with copies of the documents alleged herein to be misleading prior

to or shortly after their issuance and/or had the ability and/or opportunity to prevent their issuance

or cause them to be corrected. Accordingly, each Defendant is responsible for the accuracy of the

public reports and releases detailed herein and is, therefore, primarily and/or secondarily liable for

the representations contained therein.

19. Each of the Management f}efendants is liable as a participant in a fraudulent

scheme and course of business that operated as a fraud or deceit on purchasers of Lumenis

common stock by disseminating materially false and misleading statements and/or concealing

material adverse facts. The scheme: (i) deceived the investing public regarding Lumenis's

business, finances, financial statements and the intrinsic value of Lumenis common stock, and (ii)

caused plaintiffs and other members of the Class to purchase or otherwise acquire Lumens

securities at artificially inflated prices.

CLASS ACTION ALLEGATIONS

20. Lead Plaintiffs bring this action as a class action pursuant to Federal Rule of Civil

Procedure 23(a) and (b)(3) on behalf of all those who purchased or otherwise acquired the

securities of Lumens during the Class Period, and who suffered damages thereby (the "Class").

Excluded from the Class are Defendants, members of the immediate families of the Individual

Defendants, officers and directors of the Company, any affiliate or subsidiary of the Company and

the senior officers and directors of the affiliate or subsidiary, or any entity in which any excluded

person has a controlling interest, and the legal representatives, heirs, successors, and assigns of

any excluded person.

21. The members of the Class are so numerous that joinder of all members is

impracticable. During the Class Period, Lumenis had in excess of27 million shares of common

stock outstanding and approximately 270 shareholders of record. While the exact number of

Class members is unknown to Lead Plaintiffs at this time and can only be ascertained through

appropriate discovery, Lead Plaintiffs believe that there are hundreds, if not thousands, of

members in the proposed Class. Record owners and other members of the Class may be identified

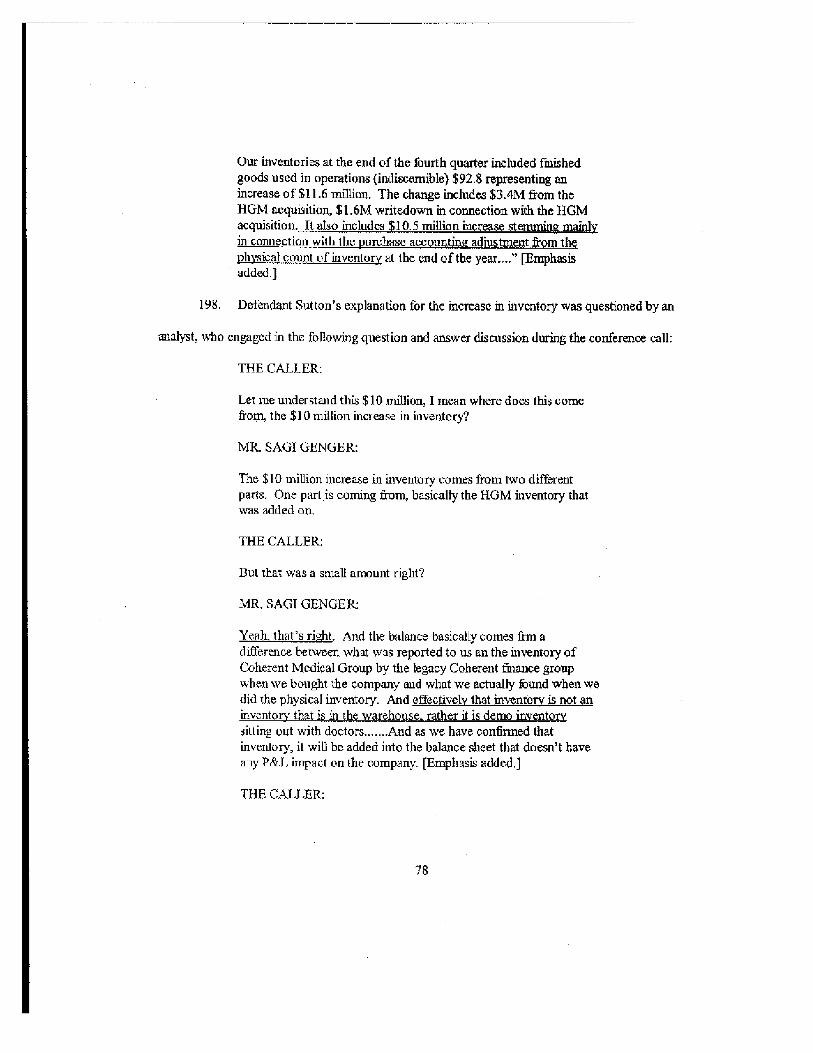

from records maintained by Lumens or its transfer agent and may be notified of the pendency of

this action by mail, using the form of notice similar to that customarily used in securities class

actions.

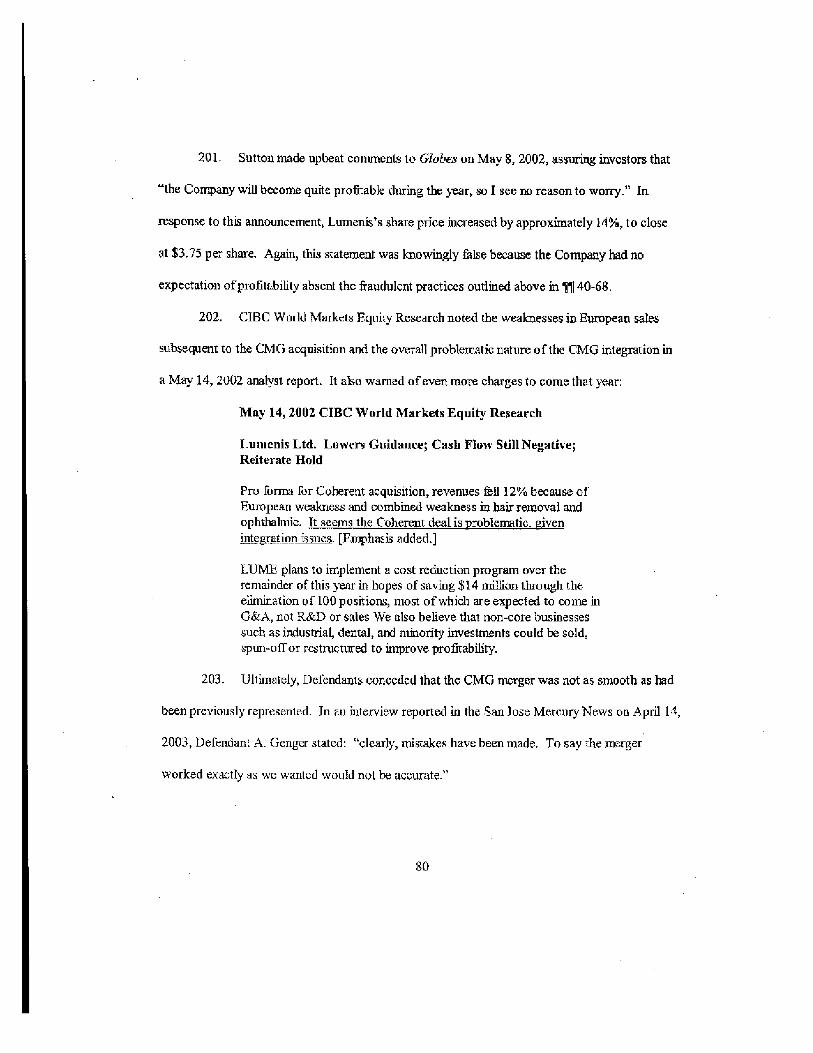

22. Lead Plaintiffs' claims are typical of the claims of the members of the Class as all

members of the Class are similarly affected by Defendants' wrongful conduct in violation of the

federal law that is complained of herein.

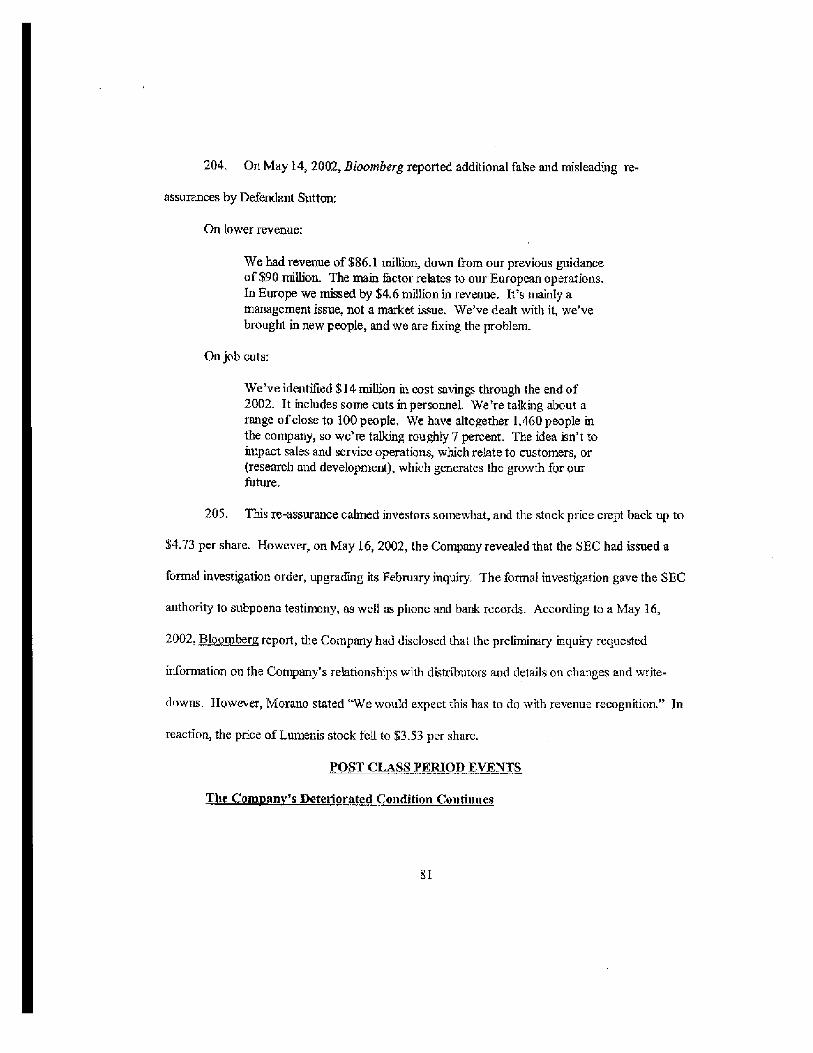

23. Lead Plaintiffs will fairly and adequately protect the interests of the members of the

Class and have retained counsel competent and experienced in class and securities litigation.

24. Common questions of law and fact exist as to all members ofthe Class and

predominate over any questions solely affecting individual members of the Class. Among the

questions of law and fact common to the Class arc:

a. whether the federal securities laws were violated by Defendants' acts as

alleged herein;

b. whether statements made by Defendants to the investing public during the

Class Period misrepresented material facts about the business, operations, and financial statements

of Lumenis; and

10

c. to what extent the members of the Class have sustained damages and the

proper measure of damages.

25. A class action is superior to all other available methods for the fair and efficient

adjudication of this controversy since joinder of all members is impracticable. Furthermore, as the

damages suffered by individual Class members maybe relatively small, the expense and burden of

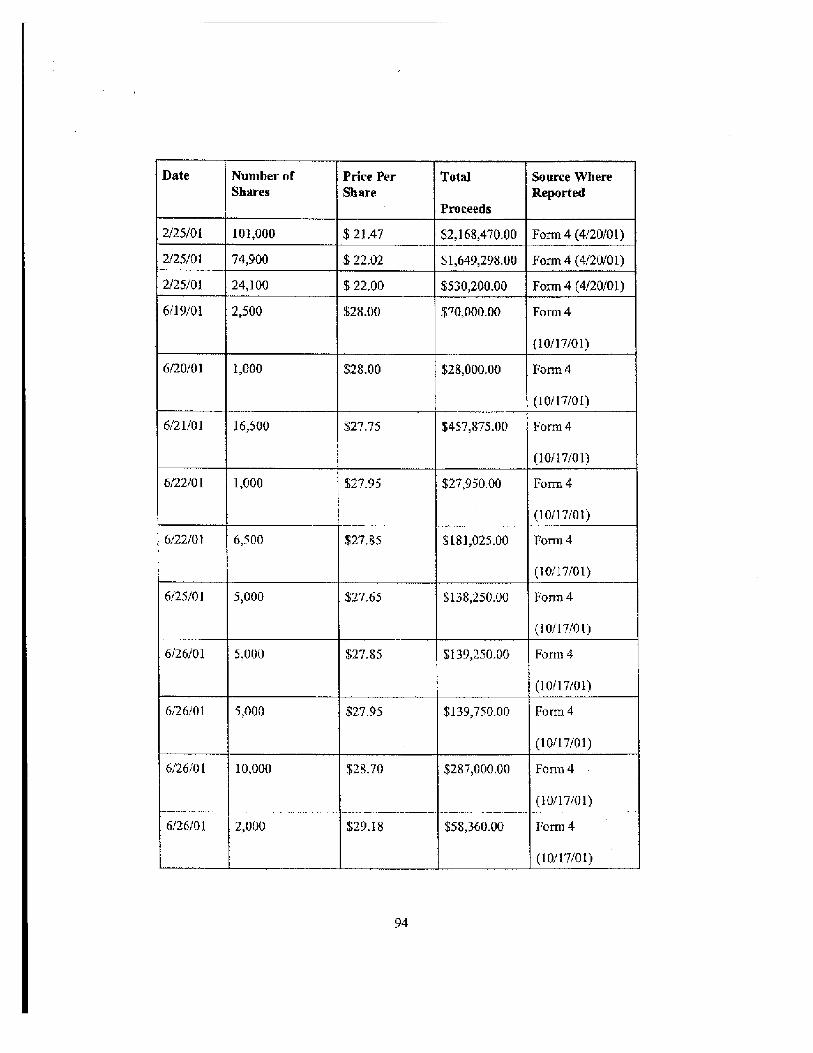

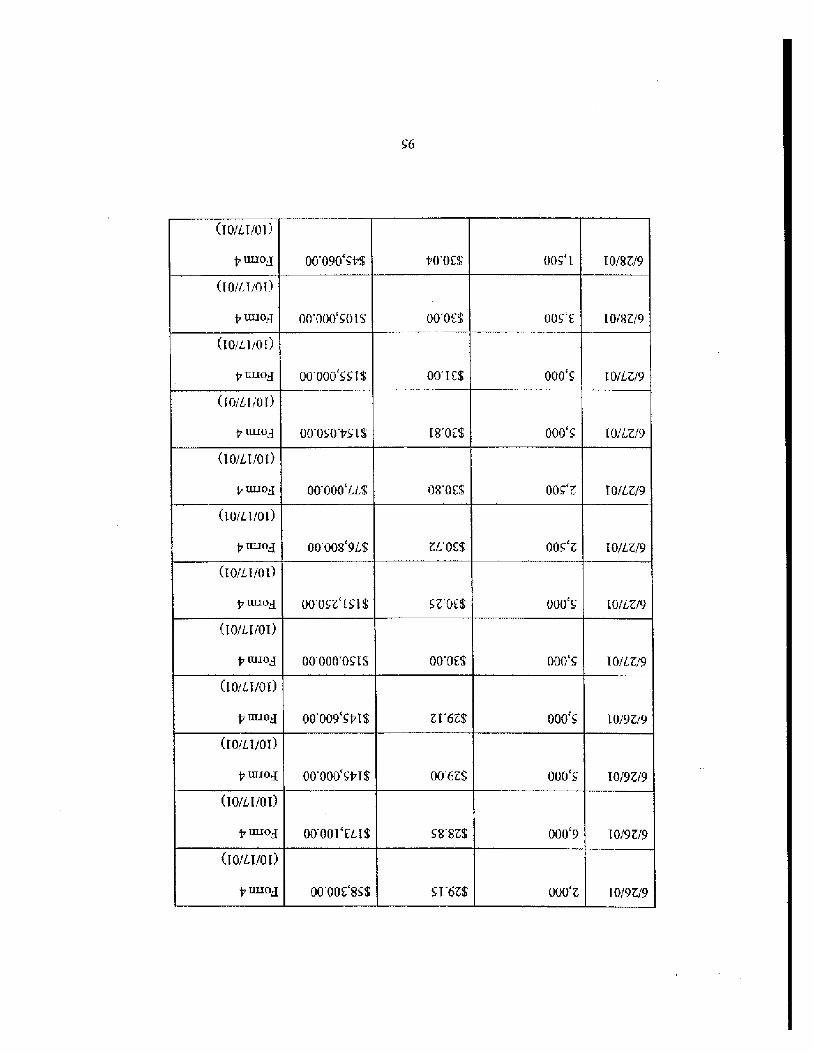

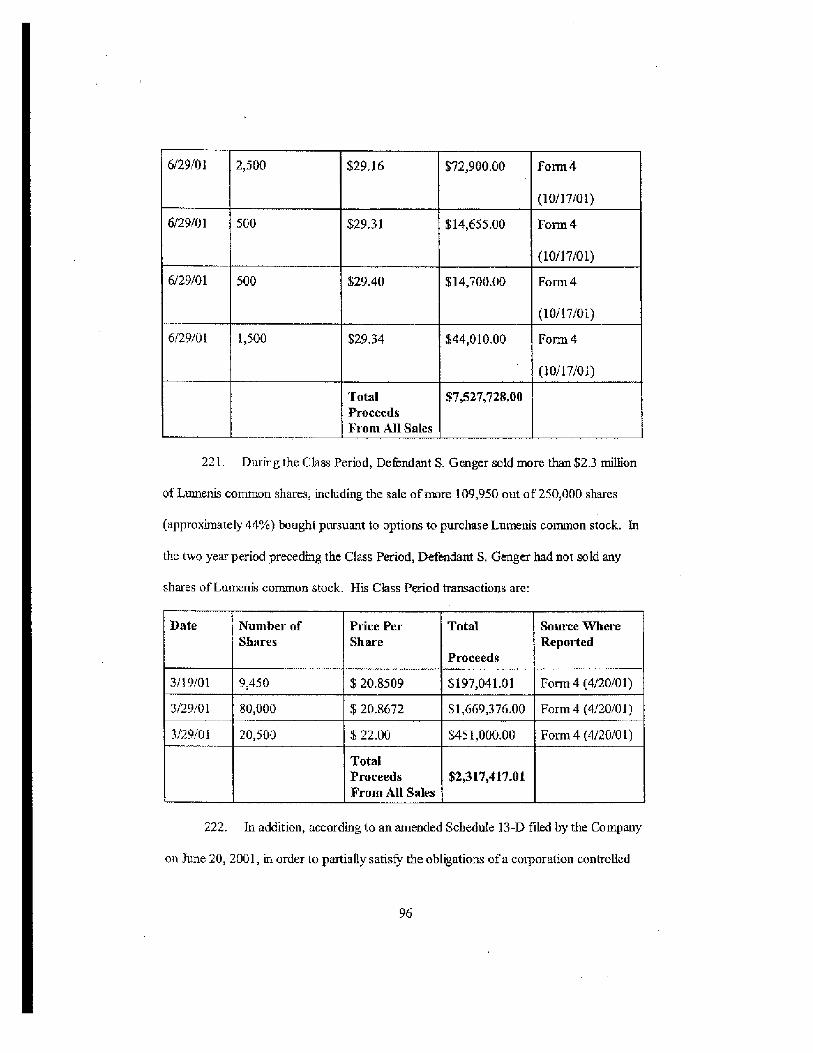

individual litigation make it impossible for members of the Class to individually redress the

wrongs done to I here There will be no difficulty in the management of this action as a class

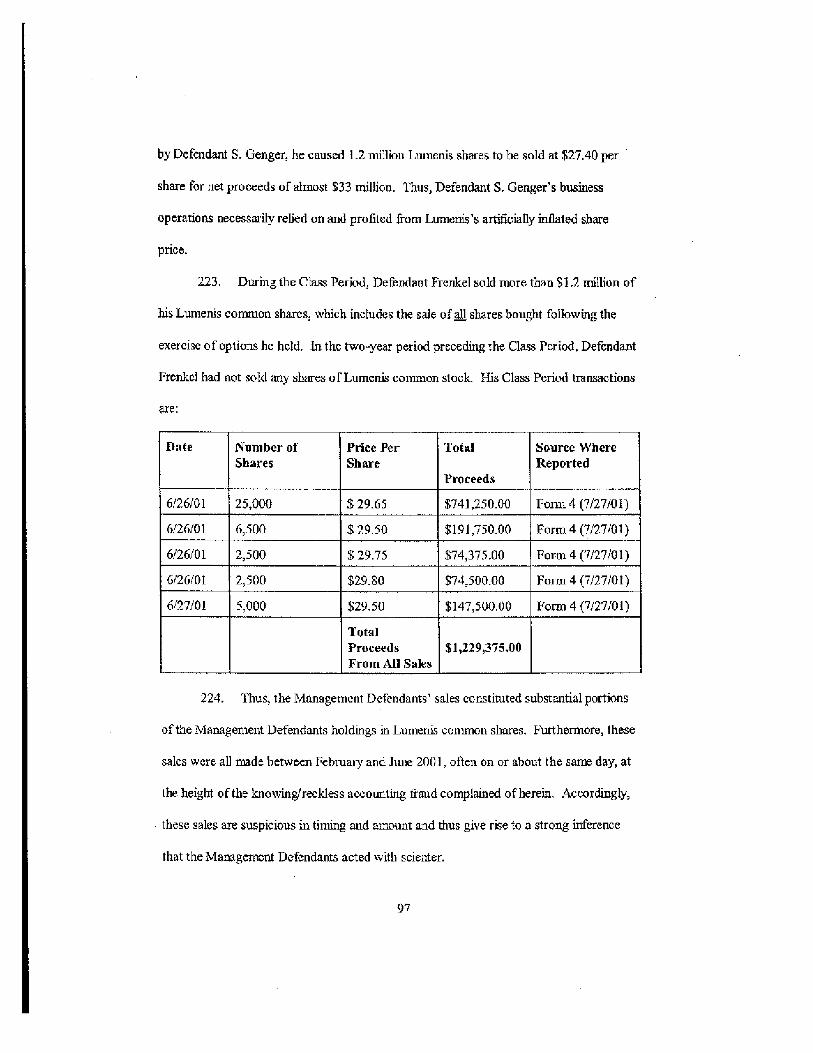

action.

SUMMARY OF TUUE ALLEGATIONS

Defendant A . Gen er Takes Over FSC Improper Practices and Accounting Mani irtilaonsEnsue

26. In May, 1999, Defendant Arie Genger engineered a hostile takeover of ESC_ He

promptly installed his 27-year old son as Chief Financial Officer, hired Defendant Sutton as Chief

Executive Officer, stacked the Board of Directors with his associates, and granted hundreds of

thousands of options to himself, his son, and his newly-installed officers and directors.

27. ESC had been a company fraught with problems, including , among other things

poor product reliability, a raft of product liability and physician lawsuits, increasing inventories,

and poor collections on accounts receivable. Its stock traded undramatically in the $4-$6 per

share range for most of 1999,

28 Begin iinig at the end of 1999, under A. Genger's now consolidated contra I, the

Company began to show dramatically improved financial results, launching the stock price on a

steady climb. However, as described below, these results were more the product of improper

11

practices and accounting manipulations than actual business success. The Company showed

improved (albeit illusory) earnings by, inter alia, recognizing revenues on sham sales, and

"channei-staffing" by loading distributors with product, but having undisclosed side agreements

with the distributors granting unlimited return rights and not requiring payment until - if ever ---

the distributors "sold-through" the products to customers.

29. Defendants were well-aware of their financial misrepresentations. Defendant Asif

Adil has filed a complaint and a sworn declaration in his action for wrongful termination against

the Company, in which he states that he learned of several ofthese illegal and improper

accounting practices shortly after his hiring as Executive Vice President in July, 2000. His

repeated protests about Lumenis's improper accounting practices to defendants Sutton, S. Genger

and Frenkel fell on deaf ears, however. In fact, Adil states that he learned that S. Genger was

misrepresenting the financial information he was providing to the Company's auditors, with the

knowledge of Defendant CEO Sutton.

30. The Company's illusory revenues and earnings could not be totally hidden forever;

ESC's accounts receivable began to rise and to age, as the company was not being paid for its

charnel-stuffed product or sham sales. Yet, the Company was not adequately reserving for

doubtful accounts or writing off bad debt. In addition, the Company continued to Garryun its

books excess inventory and other items that should have been written off.

ESC Merges. With C oherent Group to Mask ESL's Improper Machinations and Allow

Defendants to Take Advantage of ES Artificially Inflated Stock Pric

31. Defendants, however, had a plan for "cleansing" their books of these looming

liabilities: Defendants continued to release fraudulent financial information in order to keep the

12

stock price rising, and then leveraged the artificially-inflated stock by using it as currency in an

acquisition. In early 2001, the Company bought Coherent Medical Group ('CMG" or

"Coherent"), using cash and over $100 million of inflated stock (then trading at approximately

$21 per share). The Management Defendants promptly sold millions ofdollars of artificially

inflated stock. Although claiming - but vastly exaggerating - that synergies would ensue from the

acquisition, Defendants had additional motives for the acquisition: to camouflage the Company's

wide assortment of long-needed write-offs as acquisition-related expenses in a single "Big Bath,"

cleansing ESC's books ofthese expenses and liabilities; and to create other "cookiejar" accruals

and provisions which could be reversed in later quarters to help the Company meet its financial

projections-

32. Of course, Defendants had an additional motive: The announcement of the CMG

acquisition and its accompanying hype about (never-to-materialize) synergies sent ESC (now

named Lurnenis) stock to levels over S30 per share, making Defendants' options to purchase

Lumenis stock worth tens of millions of dollars. Defendant A. Genger, in fact, promptly sold off

$33 million of his stock. With the high stock price, the Company could raise substantial, much-

needed cash through options exercises, and prepare for a future secondary offering.

33. After the merger, in July, 2001, the Company appointed Adil Chief Financial

Officer. In this role, he learned the extent of the fraudulent activity behind the Company's

apparent financial success, Over the fbllowing weeks, he reported his finding to Defendants

Sutton and S. Genger_ When they refused to heed his protests, he reported his findings to

Defendant Frenkel and the Lumens Board. The Company reacted by stripping him of his CFO

and management positions, and dispatching him to India,

13

34. Defendants continued their illegal accounting practices , even adding new

fraudulent transactions to their repertoire, such as a self-dealing "sale" to a subsidiary in order to

meet continued public projections of record revenues, reversing accruals, and reversing

allowances forbad debt - even though there had been no improvement in collections.

35. Ultimately, these practices drew the attention of the SEC. The Company disclosed

that it was the subject of an informal inquiry in January 2002, news which dropped the stock price

50% in one day. Now under regulatory scrutiny, Defendants could no longer engage in rampant

accounting misconduct, the secret to Lumenis's illusion of success and high-fying stock price. In

May 2002 when the Company disclosed that the SEC inquiry had been raised to a formal SEC

investigation, the stock dropped another 30°%a. Lumenis stock dropped from its $30-plus level in

the summer of 2001 to approximately $3.50, scarcely nine months later, in May of 2002.

36. Lead Plaintiffs, and other class members who purchased Lumenis stock at those

lofty, fraudulently- inflated prices, have been injured by Defendants' conduct.

CONFIDENTIAL WITNESSES

37. Numerous former employees of Lumenis and/or its distributors have informed

Plaintiffs that Defendants caused the Company to report false financial results during the Class

Period through various improper accounting techniques. These witnesses spoke to Lead

Plaintiffs' counsel on a confidential basis and are referred to herein as confidential witnesses 1-11

("CW "). These persons include:

a. CW 1 is a former executive who worked at Lumenis from May 2001

through the end of the Class period and beyond. CW I has personal knowledge of: the SEC

inquiry and investigation, various accounting improprieties including improper revenue

14

recognition, the problematic integration of CMG into Lumens, and other matters relevant to the

allegations alleged in this Complaint.

b. CW2 is a former sales coordinator who worked at Sun Medical, a former

distributor of ISC/Lumenis, from June 1998 through April 2003. In that position, CW2 was

responsible for providing support to Greg Sellards, the CEO of Sun Medical, and Doug Archer,

Sun Medical's President, and assisting the sales representatives that sold ESC/Lumenis medical

lasers. CW2 has personal knowledge of Lumenis's sales practices - e g., quotas and channel

stuffing.

c. CW3 is a fernier senior executive who worked at Premier Medical, a

former distributor of Lumens and its predecessors. Premier Medical acted as a distributor for

ESC/Lumenis prior to the Class Period and throughout 2000 and early 2001. CW3 was

responsible for, Lntex alia the distribution ofmerchandise and the negotiation ofdistrbution

agreements, including those with Lumenis. CW3 has personal knowledge of Lumenis's sales

practices - e.&,, quotas and channel stuffing.

ci. CW4 is a former sales representative who worked at Eclipse Medical, a

distributor of Lumenis, from prior to the start of the Class Period through May 2001. In that

position, CW4 was responsible for selling Lumerus products such as the Epil.ighi, Vasculight,

C02 Lasers, and the Urbium Lasers. CW4 has personal knowledge of Lurnenis's sales practices -

e.g chaimel stuffing.

e. CW5 is a former director of sales for Eclipse Medical, from prior to the

start of the Class Period through July 2000. In that position, CW5 was responsible for selling

15

Lumens products. CW5 has personal knowledge of Lumenis's sales practices - M, channel

stuffing.

f. CW6 is a former support manager at Eclipse Medical, from prior to the

start of the Class Period through December 2001. In that position, CW6 was responsible for

quality control testing and shipment of Lumcnis products to the end user. CW6 has personal

knowledge of Lumcnis's sales practices - e g , channel stuffing,

g. CW7 is a former credit and collections analyst for Lumenis from November

2001 through March 2002, In that position, CW7 was responsible for the review of delinquent

accounts, investigation of complaints, verification of charges, and preparation of reports. CW7

has personal knowledge of many of the matters alleged in this Complaint, such as the SEC inquiry

and investigation and accounting improprieties.

h. CW8 is a former materials manager, who worked for Lumenis from March

2000 through January 2002. In that position, CW8 managed parts inventory of 4000 sku's valued

at $6.9 million and system level inventory of $12 million- CW9 has personal knowledge of many

matters alleged in the Complaint, such as the integration of CMG into Lumens, and accounting

techniques related to Lumenis's accounts receivable and inventory tracking.

i. CW9 worked as a controller for Lumenis during the year 2001. By virtue

of this position, CW9 had access to Lumenis's MSG-PRO accounting system which CW9 said

produced a document that tracked weekly sales calls and gave a clear picture as to the level of

sales. CW9 indicated that this document was provided to all senior management in the US and

Israel.

16

J. CW 10 worked as Senior Manufacturing Engineer at Lurnenis before, after

and throughout the entire Class Period. In this capacity, CWIO traveled extensively to the

Company's various facilities and is familiar with the manufacture, quality, and sales practices

involving Lumenis products.

k. CWI I is a former administrative assistant for Lumenis. In that position,

CW1 I was responsible for pulling documents and making copies for the "Lumens SEC Project."

FACTUAL BACKGROUND

38. Lumenis is an Israeli company that develops, manufactures and markets medical

devices utilizing lasers and proprietary intense pulsed light technology fornon-invasive treatment

of varicose veins and other benign vascular lesions, as well as other clinical applications. The

Company was formerly known as ESC.

39. As described in detail below, the Company engaged in systematic manipulation of

its financials in order to artificially inflate its stock price. This manipulation utilized several forms

of improper revenue recognition and accounting involving bad debts, write-offs, nun-performing

accounts receivables, "channel stuffing," and "sales" to related parties.

Improper Revenue Recognition

1. "Channel Stuffing"

40. Anwng the methods used by the Company to inflate reported revenue was

"channel stuffing." Although Lumenis emphasized that its marketing and distribution practice was

"based upon the manufacture and delivery of products to customers based upon specific orders

received from its customers," this representation , repeated in each ofthe Company's Class Period

10-Ks was materially false and misleading . In reality, the Company would ship excessive

17

quantities ofproduet to distr ibutors, and recognize revenue upon shipment-especially at the end

of each quarter. Moreover, the Company would not have any real expectation for receiving

timely payment for any of those "sales," or even that the distributor would be able to sell that

excess product in the foreseeable future. The Cornpanywould not demand timely payment from

the distributors, and/or would allow, without conditions, return privileges. These methods have

been the subject of the SEC's investigation into the Company publicly reported revenues.

41. The practice of"channel stuffing" was rampant. Lurnenis employed similar

agreements with distributors all across the United States and abroad. For example, CWI heard

that the Company's channel stuffed distributors included, among others, Eclipse, Aculight, its

Spanish distributor (Guissepe), and Canadian distributor, Coherent-AMT. Other distributors

whose channels Defendants' stuffed included Premier Medical and Sun Medical.

42. Defendant Adil has admitted that the Company engaged in such practices, noting

that while employed at Lumenis he learned that the Company was "inflating earnings by [, inter

alia,] booking sales to distributors with the understanding that the product could be returned, by

giving recourse financing to increase apparent sales when such sales were actually contingent and

not bona fide, and by charging ongoing expenses to a reserve account, rather than against sales,

so that the net sales numbers would not be reduced." Ex. B at 115.

43. According to CW3, Lurnenis loaded Premier Medical, an Ohio-based distributor of

Lurnenis surgical laser systems for hospitals, with excessive inventory on a regular basis at the end

of each quarter, especially during 2000-2001. CW3 said that there was a verbal agreement

between Premier Medical and Lumenis wherein the former was never required to pay for the

excess inventory--especially not within the 30-day period listed on the "purchase orders," which

18

CW3 personally reviewed. Although the purchase orders on these units ostensibly required

payment within 30 days, there was effectively a "sell through" arrangement whereby no payment

was required for any units until Premier Medical sold them to an end user. CW3 referred to this

as "a look the other way arrangement, it wasn't written down., it was verbal" According to CW3,

Lumens would pressure Premier Medical at the end ofevery quarter to take one or two extra

units, even though both sides knew that Premier Medical had more inventory than it needed. As

an incentive for Premier Medical to agree to the arrangement, Liunenis would offer discounts of

5.10%, and would never press for payment for the units, instead offering extended payment terms

on its inventory. As additional "incentive," CW3 was told on several occasions that if Premier

Medical did not "help them out," Lumenis would strip Premier Medical of its distributorship.

Moreover, according to CW3, Lumens granted Premier Medical the right to return unsold units

for felt credit. CW3 estimates that by early 2002, Premier Medical was holding approximately

$800,000 of Lumenis inventory beyond that which it could sell, and all ofwhich was ultimately

returned to the Company.

44. CW5 also stated that Lumenis would ship excess product to Eclipse Medical--

many times during periods with no orders--without requiring payment. CW4 confirmed that

Lumens stuffed the channels for Eclipse Medical: "We always had a bunch of equipment in the

warehouse with no purchase orders. We weren't supposed to be a stocking distributor but we

were, and we would always have to get rid of i.e„ sell] the inventory that we weren't suppose to

have. Tom O'Brien [Eclipse's President] would tell us that they received special pricing for the

equipment and so we got extra." On several occasions, CW4 heard both Paul O'Brien [Eclipse's

19

comptroller] and Tom O'Brien state "Let's get the equipment from ESCiLumenis, it is not like we

have to pay for the stuff."

45. Lumenis's stuffing of Eclipse Medical's distribution channels is also evident from

the fact that following the Class Period, when Eclipse Medical's distribution agreement with

Lumenis terminated, the Company contended, in a November 24, 2004 press release, that Eclipse

Medical owed it $1.2 million in outstanding loans. Lumenis ultimately forgave these loans in

connection with its settlement of other disagreements with Eclipse MedicaL

46. CW2 said that during 2000 and 2001, Sun Medical routinely took in excess lasers

from ESC/Lunienis at the end of every quarter, and at the end ofthe year. According to CW2,

the majority of time there were no actual customers. There was an understanding between the

two companies that Sun Medical did not have to pay for the machines until it could make a sale.

Doug Archer, Sun Medical's President, would determine which excess equipment to order so that

Sun Medical could meet the fnancial quota per the distribution agreement that Sun Medical was

expected to make. According to CW2, it was a very aggressive number, and the result was that

Sun Medical would "demo" all of the excess lasers for doctors and hospitals in a desperate

attempt to sell lasers and meet the quota. CW2 said that ESC promised to buy back any unsold

equipment. By 2001, there was $400.000.00 worth of such ESC lasers in Sun Medical's

warehouse.

47. CW7 also confirmed that following the merger with Coherent, Lumenis customers

were receiving incorrect invoices that failed to reflect unwritten sales discount agreements.

48. The channel stuffing described by these confidential witnesses is further evidenced

by a comparison ofl.,urnenis's stated revenue recognition policy before and after the SEC

20

commenced its inquiry into the Company's relationship with its distributors. In the 2001 10-K

(filed with the SEC on April 1, 2002), Lumenis revised its revenue recognition policy,

substantially modifying its prior policy of recording revenue upon shipment. The following

comparison ofLumenis's 2000 revenue recognition policy with its revised 2001 policy, which

switched from recognizing revenue upon shipment to recognition upon delivery and persuasive

existence ofa an agreement, illustrates the point:

Lumenis' 2000 Form 10-K states, in pertinent part:

Revenue is recognized np_on shipment of products provided thatthere are no significant uncertainties regarding the customer'sacceptance and the collectbility is probable.... [Emphasis added.]

Lumens' 2001 Form 10-K, states in pertinent part:

Revenues from product sales are recognized when delivery hasoccurred, persuasive evidence of an agreement exists, the fee isfixed or determinable and collectibility is probable.... [Emphasisadded.]

49. Moreover, beginning in 2002, with the new revenue recognition policy in place,

Lumenis had substantial difficulty providing Wall Street with revenue guidance. This fact serves

as persuasive evidence that prior to the SEC's inquiry, revenue was inflated based on improper

revenue recognition at the time ofshipment.

2. Bad Debt/Non=perfurming_Accounts Receiva ble

50. As alleged above, defendant Adil has, in a sworn statement , stated that the

Company carried unwarranted high receivables due to its improper revenue recognition- Ex. B at

T, 15.

21

51. According to CW 7, management at the Company indicated that part of the SEC's

inquiry "seemed to focus on the fact that there were nonperforming accounts receivables which

had been carried on the Coherent/Lumenis books," and were not being written off as bad debt,

CW7 noted that the Company was not promptly recording credit memos, instead holding them

back, thereby not properly recording a write-off of bad debt. Hy not properly recording a write-

offofbad debt, Defendants were able to overstate the Company's accounts receivable. This

falsely conveyed the message to investors that the receivable would be convertible to cash flow.

CW7 stated that the Company's management did not want to write off the bad debt because it

would have decreased Lumens' profitability. CW7 reported having encountered resistance from

the Company's management in writing off any accounts receivable that was non-performing and

should more accurately be categorized as bad debt. CW7 stated that following the merger with

Coherent, Lumenis's accounts receivable increased by approximately $12.4 million, as a result of

these practices-not due to the "processing difficulties" that Defendants claimed led to in reased

accounts receivables.

52. CW7 said that the Company's senior management knew first-hand about the bad

debt/aging accounts receivable problem because spread sheets were customarily and ordinarily

prepared and provided to management detailing the extent of the problem.

53. CW8 also stated that the Company's accounts receivables increased following the

merger of the accounting systems from Coherent and ESC. CWS described it as "a mess"

brought on as a by-product of the integration of operations to the West Coast, but was told by a

supervisor, "don't worry about it."

22

54. CW9 confirmed that there were massive accounts receivables , which the Company

had inherited along with certain acquisitions. According to CW9, a printout of these receivables

was over 2 inches thick . CW9 said that attempts to collect on them failed due to lack of attention

from management in dealing with outstanding receivables, which had been on the books beyond

the time when they should have been written off as bad debt.

3. Manipulation of Allowance for Doubtful Accounts

55. Another source of "income" for the Company was receiving parts of an accrual

allowance into income. Creating accruals and later reversing them into income is sometimes

referred to as "cookie jar" accruals. The company maintains the "cookie jar" of loss accruals.

Then, in subsequent periods, when the company needs additional gains/income to offset a shortfall

in income, it reaches into the cookie jar and reverses the accrual, taking it back into income.

Based on data from the Company's SEC filings, the Company shrunk its allowance--even while

there was no improvement in collections, and total receivables continued to mount--as illustrated

below:

Allowance For Doubtful Q2 2001 Q3 2001 Q4 2001 Q1 2002Accounts

Trade Receivables 117,254 121,696 120,567 131,184

Allowance (25,281) (26,315) (19,744) (17,296)

Net Trade Receivables 91,873 95,381 100,823 113,888

Allowance Percent 21.6% 21 .6% 16.3% 13.2%

56. As the foregoing chart demonstrates , by 4Q 2001, Defendants began reversing the

Allowance accrual into income. In the fourth quarter 2001 , earrings conference call, Defendant

23

S. Genger admitted that the prior Allowance (merely from the prior two quarters) was now

"creating" gains for Lumenis:

There was a $3.8 million gain for reversal - - a provision for

receivables from discontinued distributors-related to the Coherent

acquisition.

57. In the first quarter 2002 conference call, Defeiidan(s admitted that the Company

benefitted from reversing 2Q 2001 accruals into income. Kevin Morano ("Moran"), Lnmenis's

new CFO, stated the following:

This was offset by $3.3 million in reductions in previously providedaccruals for items associated with the CMG acquisition.

Although Morano did not specifically state that this additional reduction in "previously provided

accruals" was a reversal of the Allowance, the foregoing chart shows that the Allowance was

inexplicably reduced again in IQ 2002, to a level approximately 40% lower than two quarters

prior--all at a time when net receivables had increased by over 15%.

4. Related Party " sales"--Aculight Ltd.

58. In order to meet the Company's reassurances of the 4Q 2001 financial projections

(Lumenis had reiterated its expectation of "record fourth quarter" results of EPS of $0.41 as late

as December 31, 2001), Defendants also manipulated the Company 's revenues by counting as a

" sale" existing leases of equipment to its own hair removal products affiliate, Aculight Ltd.

("Aculight') ( in addition to the "channel-stuffing" of Aculight discussed above).

59. Lumenis recognized $4.8 million in revenue, based on a transaction with Aculight,

a related party, in violation ofCAAP_ (It was later revealed by Defendants that the $6.4 million

account receivable had to be restructured with extended payment terms)

24

60. Based on Defendants' glowing reports ofthe Company's hair removal business, on

October 22, 2001, CIBC World Markets issued an Equity Research report that estimated Lumenis

hair removal revenue in 4Q 2001 would be $29 million. In reality, however, demand was far from

strong and 4Q 2001 hair removal revenue - without the $4.8 million revenue from Aculight -

would only have been $8.2 million, -well-below the $29 million estimated by analysts-

5. Bookinnt of Sham "Sales"

61. CWI recalls being privy during most of the Class Period to multiple and repeated

end-of-quarter sales conference calls which were headed by Defendant S. Genger in New York.

Other senior executives participated in these marathon calls. CWl recalled how Defendant S.

Genger, in many of these conference calls, would approve open credit terms for deals with very

little to no assurance of payment in the future. Thus, the likely conversion into a bona fide

payment was not readily apparent during these end-of-quarter calls. CW l explained that although

the standard operational procedure was to withhold approval until receipt of the prerequisite

backup items (e.g., signed purchase orders, lease approvals, bank deposits, confirmed checks), on

numerous occasions, S. Genger would freely allow exceptions on these calls and approve sales for

shipment. Gouger freely granted approval this way in order to book sales, increasing the

recognized revenue levels for the quarter. These tactics figured prominently in the Company's

reported quarterly sales figures since greater than 50% of the sales volume was approved, booked

and recorded during the last two weeks of any given quarter. Lumenis's SEC filings acknowledge

this fact. See, e.g. Fiscal 2001, 10-K, filed with the SEC on April 1, 2002 ("a substantial portion

of the Company's sales are completed in the last few weeks of each calendar quarter").

25

62. CW I also stated, on the problem of sales that were improperly booked, that there

was an email from the Controller in Europe, dated May 23, 2002, in which two dubious deals

were detailed, both relating to QI 2002. The Controller referred to them as "potential for sale

reversal" sales, The first was for a $400,000 "sale" to a Saudi Arabian company, Alainoudi in

which the purchase order specified "hold delivery", but the sale was booked and recognized. The

second was for the 240,000 Euros sale to the Company's Russian distributor, Rosslyn Medical

Ltd., in which payment was not assured, product was held, and the sale should not have been

booked.

6. Short Shipments/"Headless" Sales

63. Concerning improperly recognized sales, CW1 stated that, in each ofthe first two

quarters of 2002, about $5 million of lasers were sent without their "heads." "Heads" is a

technical term for a vital component on the machine, and if it was missing, then the machine

would not be functional for the customers, CW1 stated, "fit was like shipping a car without its

wheels." The Company did this because, although there were quality problems with the heads,

Defendants, regardless, wanted to ship and book the sales. When doctors complained that no

heads were included in their shipments, the Company would explain the omission away as a mere

accident. CW1, however, stated that this happened numerous times, and was deliberately done by

Lunienis.

64. CW10 recounted how amazed employees at the Bothell, Washington location were

when systems started to be shipped out without their accompanying "heads." CW10 also

explained that absent a head, the equipment was missing a major portion of its full value. CW 10

said that these employees were forced to sell things that were not sales worthy.

26

7. Mani u lation of Aecountin For Invento

65. Defendants violated GAAP (SFAC No. ¶1 120-121), by classifying demonstration

equipment acquired from CMG as inventory on Lurnenis's balance sheet rather than as finished

goods used in operations ("F'.G.s"), the balance sheet classification used by Lurnenis for

demonstration equipment. This was materially fake and misleading because inventory is an asset

held for sale, whereas F.G. is a wasting asset being depreciated over 3 years as described in the

Company's 2001 10-K see page F-12). The following chart (derived from the Company's 2001

Form IO-K and 3Q 2001 Form l0-Q, filed November 14, 2001) illustrates that the year end $9

million adjustment was added to the inventory balance sheet account and not the F.G. balance

sheet account.

9130101 12/31/01 Change

Inventory 71,381 83,614 12,233

F.G. 9,860 9,180 (680)

Total 81.241 92,794 11,553

Allegations Against Lumenis by former CFO

66. As described herein, Defendant Adil, former CFO of Lumenis, has confirmed the

accounting allegations of this Complaint in the sworn declaration he filed in an employment-

related lawsuit against the Company filed in the United States District Court fbr the District of

New Jersey and later transferred to the United States District Court for the District of

Massachusetts. See Ex. B at ¶J¶15-16.

67. Adil joined Lumens as an Executive Vice President ("EVP") on July 5, 2000.

Shortly thereafter, he discovered rnumernns accounting irregularities , including carrying

27

unwarranted high receivables, underfunding accruals, booking write-offs as revenue, and handling

excessive product returns. He first reported his findings to S. Genger, then the Company's CFO,

but S. Genger ignored his findings. See Ex. A hereto at X10-11.

68. Subsequently, Adil learned that the Company was engaging in these improper

accounting practices at the direction of S. Genger, who, with Defendant Sutton's knowledge, had

concealed material information from the Company's outside auditors. Id. at ¶12.

69. AN then informed Sutton of his findings, requesting that the practices be

corrected. According to Adis, Sutton declined to act on this request . Id, at 113.

70. On July 20, 2001, Adil was appointed acting CFO, while continuing to serve as

PVP.

71. Once serving as CFO, Adil learned of additional financial misconduct, including

lack of full disclosure to investors regarding undisclosed insider transactions, undisclosed side

agreements between the Company and its primary lender, mischaracterizations of sales to make up

for earnings shortfalls, and the booking ofapparently non-existent sales. Id. at ¶15.

72. Add reported these irregularities to the Lurnenis Board in November 2001 due to

his belief that these practices violated the securities laws. Id . at 1116-17

73. Within a few weeks, Sutton removed Adil from his CFO position. Add repeated

his concerns to Sutton regarding Lumenis's GAAP violations. On January 3, 2002, Adil was also

relieved of his EVP position and dispatched to India to work as a sales representative. According

to Adil, Defendant S_ C;enger threatened to fire him and to ruin his reputation in the business

world if be continued to object to Lumenis's financial practices.

28

The Coherent Merger

74. On February 2, 2000, and on February 29, 2000, Lumens issued press releases

announcing FDA approval of its new intense Pulsed Light (IPLTM) technology for hair removal

treatment, touting the "multi-billion" dollar market potential for hair removal in the U.S. alone,

and announcing that hair removal treatment was the "cornerstone" ofthe Company's growth

strategy. As Defendants later learned, this growth strategy would fail, leading Lumenis to seek

growth and new markets through its merger with Coherent the following year.

75. Following the February 2000 announcements, Lumenis began to tout its hair

removal line ofproducts, Thus, for example, on March 13, 2000, Lumenis issued the following

release:

"ESC Medical continues to improve on the superiority of lPLtechnology," said Yacha Sutton, President and CEO of ESCMedical Systems. "In the p ast, our customers have benefitted fromthe, h' h efficacy an excellent safe erfannance of ourtechnology . Now we have demonstrated that these products can bemade compact and affordable, without cornprornisng any of thefactors that gave IPL the largest number of light-based aestheticprocedure devices in the world." [Emphasis added.]

76. At the same time as Lumenis was promoting its hair removal products as the

"cornerstone" of its growth strategy, the Company was getting sued for product liability and

misrepresentation involving its hair removal equipment and other products. The following

excerpts froin ESC's 1999 Form 10-K, filed with the SEC on March 30, 2000 mentions two such

litigations.

Note 12 - COMMITMENTS AND CONTINGENT LIABILITIES

C. (2) On September 20, 1999, Dr. Richard Urso filed whatpurports to he a class action lawsuit against the Company in the

29

State District Court in Harris County, Texas. Dr, Urso alleges anumber of causes of action including, breach of contract, breach ofwarranty, product liability, misrepresentation and violations of theTexas Deceptive Trade Practices Act. The complaint purports tobe filed on behalf ofa national class. The Company has taken stepst.o remove the case to Federal court and intends to vigorously denyall allegations and challenge plaintiffs class certification motionwhen it is filed, No accrual has been recorded in the financialstatements for this matter.

C (3) On May 10, 1999, the Company and a former director andofficer were named as Defendants in an action filed in Tel-AvivCourt by H.K. Hashalom Ltd. in connection with the sale of theCompany's EpiLight systems. H.K. Hashalom is seeking monetarydamages in the amount of $2,500 but has reserved the right toincrease such amount as well as a declaratory judgment that, interalas, the Company indemnify it for certain costs and expensesarising out of the transaction between the parties. On July 15,1999, the Defendants filed a Statement of Defense. The case hasnot yet been set for a first hearing. No accrual has been recorded inthe financial statements fur this matter.

77. By the time Lu'tnenis announced the impending acquisition ofCMG , its litigation

troubles were significant . Defendants were desperate to quickly acquire another company with a

respected industry name, significant revenue generating capabilities , and better technology.

CMG, with its thirty years of industry experience and annual revenue of $205,287,000 for year

ended September 30, 2000, made an attractive target.

78. On July 25, 2000, i umenis announced the creation of Aculight, a new business

enterprise intended to place Lumenis hair removal machines into beauty shops, salons, and spas.

The Company's revenue model was based on customers paying a down payment on the machines,

and commissions from each use. The customers would receive frill training, marketing support,

and medical supervision. Defendant Adil was recruited to lead the Aculight project.

30

79. On July 26, 2000, ESC issued a press release in which it announced the launch of

the Acufight Program to sell lair removal equipment to non-physician customers . In the release,

Defendant Sutton discussed the purported growth opportunities this program provided the

Company:

We are expanding into new markets with our. proven technologies

to take advantage of new growth opportunities. Just yesterday, we

announced the launch of a major new market expansion initiative tocommercialize our proprietary Intense Pulsed Light (1PL)

technology and market it ,as theAcuL ' T' PhotooosmeticProgram to beauty salons, cpsmeticians, edectrologists and other

professionals who provide hair removal services. We arecontinuing to invest in the future through our ongoing R&D effortand through a variety ofinvestments in start-up ventures includingour dental unit. [Emphasis added.]

80. As revealed in the ESC's 3Q 2000 Form 10-Q, filed an November 15, 2000 launch

of the Aculight Program caused ESC to invest heavily in its hair removal inventory:

OPERATING ACTIVITIES

The increase of inventories is due to preparation for a sienifcant

increase in sales in the fourth auarter and the manufacture of hairremoval machines for the Aculihht prog^ann . Under the Aculightprogram, machines owned by the Company are placed withoperators who are charged per usage fees. [Emphasis added.]

81, The Company changed its name to Lumens after the early 2001 acquisition of

CMO for 5.4 million ESC shares (artificially inflated in value to approximately $21 per share due

to Defendants' financial misrepresentations as confirmed by Defendant Adil in sworn papers filed

in this Court) and approximately $112 million in cash and subordinated notes. The acquisition,

which was announced on February 26, 2001, closed on April 30. 2001. According to the February

26, 2001 issue of Globes, the acquisition was made possible by "up to $242 million in financing to

31

consist of a$ 100million six-year term loan to fund the cash portion of the transaction, a $50

million revolver to fund ongoing working capital needs , and draw down rights of up to $92

million to refinance the outstanding subordinated convertible notes upon maturity . The draw

down rights are subject to certain operational and indebtedness milestones,"

82. On February 26, 2001, in a company press release , ESC announced its acquisition

of Coherent Medical Group and the intent to change its name to Lumenis. The press release

stated, in pertinent part:

ESC Medical Systems (NASDAQ: ESCM) announced today this ishas signed a definitive purchase agreement with Coherent, Inc.(NASDAQ: COHR) to acquire the operations of Coherent MedicalGroup (CMG), its medical products division , for case, notes andstock plus an earnout ofup $25 million . The total consideration,excluding the eam- out, is valued at approximately $203 million,

Following closing of the transaction and subject to shareholderapproval, ESC will change its name to Lumenis, derived fromlumen, Latin for light. Post transaction, ESC will be a global leaderin the design, manufacture and marketing of light-based medicalsolutions. Combined sales for the two businesses in year 2000 wereapproximately $360 million with a focus on aesthetics (approx.$180 million), ophthalmic (approx. $70 million), surgical (approx.$60 million), and service (approx. $50 million). On a pro forma

basis (assuming the transaction had been consummated on January1, 2002 and assuming fall synergies had been achieved), ESCestimates that the transaction would be over $0.60 accretive to caseEPS in 2001

83. Although the CMG transaction crealed integral ion problems from the start, as

confirmed by CW I, the February 26' press release reflected how Lumenis's top officials vied with

each other to heap praises for the deal and camou flage the fact that Defendants were relying on

CMG's acquired assets and product lines to bail ESC out of the looming drop-offs in its sales and

excessive .inventory problems:

32

"We are pleased to join forces with CMG with its stellar reputationin the medical community. We believe that combining its highquality products and unparalleled customer service with ESC'sstrong record of product innovation will accelerate the profitablegrowth of the new company and delight our customers,," said Prof.Jacob A. Frenkel , Chairman of ESC.

"We are excited about the opportunities that this transaction withcreate for our customers , shareholders and employees ," said YachaSutton , President and CEO of ESC. "CMG's products anddistribution assets are highly complementary to ESC. Incombination with our own, they will create critical mass across ourvarious markets to better enable us to maximize our innovativeR&D pipeline quickly on a global basis," Mr. Sutton concluded.[Emphasis added-]

84. CWI recalled that CMG's average days outstanding on accounts receivable prior

to the merger was approximately 70 days, compared to ESC's approximately 110 days. CWI

stated that the Company's management was not overly concerned about its own accounts

receivable aging, as several potentially questionable sales remained in the `past due' category on

the accounts receivable list for extended periods. CWI stated that CMG product lines were state

of the art and of higher quality than ESC's aesthetic lines. CW I stated that pre-merger, CMG's

annual revenues were approximately $200 million and ESCs annual revenues were around $165

milliau. The tide shifted radically post-merger so that the precursor ESC product lines accounted

for only about $90 million of Lumenis' annual revenues while the precursor CMG lines accounted

for the balance. CW I stated that CMG's Light Sheer product line was a strong one that was well

accepted in the marketplace and quickly replaced the inferior hair removal line that ESC had been

marketing. So, rather than providing synergies as promised and represented by Defendants, the

Coherent products instead replaced and made redundant the less competitive ESC hair removal

product lines. CWI observed that, in particular, the merger did not provide the SG&A cost

33

savings promised by the Defendants to investors. For example, cost savings were not realized in

the combined companies' marketing, legal or sales expenses.

FALSE AND MISLEADING STATEMENTS AND MATERIAL OMISSIONS

85. On October 2, 2000, the Company pre-announced its financial results for the third

quarter of2000. In the press release, Lumens stated that "based on shipments to date, it expects

to report third quarter revenues of approximately $37 million, 23% more than the same quarter

last year." Commenting on the expected results, Sutton stated: "I am pleased that our sales have

continued to grow through our traditionally weak third quarter. We continue to experience

strong demand for our products and are optimistic about results."

86. On October 24, 2000, the Company announced its operating results for the quarter

ending September 30, 2000. Lumenis reported the following results in the October 24"' press

release:

Net revenue for the third quarter 2000 was 537.1 million, 23%

more than the same quarter last year. Operating income was $5.3

million, or 14.3% of revenues, net income was $4.0 million, and net

earnings per basic and fully diluted share were $0.16 and $0.14

respectively. Excluding a one-time charge of $0.4 million in

litigation settlement expenses and ESC's dental unit's loss of about

$0.6 million, the Company's earnings per basic and fully diluted

share were about $0.20 and $0.17 respectively

87. The revenue figure reported in the two October earnings releases were materially

false and misled ng for the reasons alleged in 1140 -54, 61-62, 66-73.

88. Sutton ' s statement concerning " strong demand" for the Company' s products was

materially false and misleading for the reasons alleged in ¶ 40-54, 61-62, 66-73.

34

89. On January 2, 2001, the Company pre-announced its financial results for the fourth

quarter of 2000. In the press release, Lumenis stated that "based on shipments to date, it expects

to report fourth quarter revenues ofapproximately $46 million, consistent with major Wall Street

analyst forecasts," representing "an increase of about 15% over the same quarter last year."

Commenting on the expected results, Sutton stated: "We are delighted that ESC has completed a

full year of double digit growth and profitability, Continued growth in sales of our core high

margin proprietary IPL technology continued to accelerate our momentum through the quarter.

We intend to report full results for the fiscal year in February and are optimistic that they will

meet or exceed analyst expectations."

90. The revenue figure reported in the January pre-announcement was materially false

and misleading for the reasons alleged in ¶¶ 40-54, 61-62, 66-73.

91. Sutton's statement concerning "[c]ontinued growth in sales" for the Company's

IPL technology products was materially false and misleading for the reasons alleged in 1140-54,

61-62, 66-73. As the expected revenue figures were based on "sales" achieved through improper

accounting techniques, such as channel stuffing, Sutton knew that the Company would not "meet

or exceed analyst expectations."

92. On February 26, 2001, the Company armounced the acquisition of CMG, as

described above. The February 26th press release emphasized the purported synergigs that were

supposed to result from the CMG deal:

Integration teams arc being created to capture the best practices of

both organizations to maximize custofner benefits and achieve the

acquisition synergy objectives.... The overall objective is to

create a rapid and smooth transition that achieves the acquisition

goals of strengthening customer relationships, opening new

35

opportunities for employees, and generating superior returns forshareholders.

93. Even CMG's CEO, Dr. Bernard Couillaud, was taken in by the hoopla. The same

press release quoted his reassuring comments:

"We are very pleased to enter into this agreement with ESCMedical. I have been impressed with the actions of ESC'smanagement team over the past eighteen months. The creation of astrong and independent medical business benefits Coherent'semployees, customers and stockholders. This combination enablesour medical group to grow and prosper, while providing us with anopportunity to participate in its future growth. As a result of thistransaction, our customers will have a greater choice ofproductsand services and our employees better job opportunities."

94. Financhig for the acquisition was provided by Bank Hapoalirn. The loans and lines

of credit required ESC to maintain certain financial covenants, including maintaining certain

EBITDA ratios. As part of the financing, ESC granted Bank Hapoalim options to purchase

2,500,000 shares of ESC stock at $20.25 per share. The market reacted favorably to the news.

Lumenis stock jumped 24% on heavy trading volume to close at $20.44 per share.

95. On March 12, 2001, the Company announced its operating results for the fourth

quarter and year ended December 31, 2000. Lurnenis reported the following results in a March

12th press release:

Net revenue for the fourth quarter 2000 was $46.0 millioncompared to $40 . 1 million in the same quarter Last year. Operatingincoine was $7.1 million , or 15% of revenues, net income was $5.7million , and earnings per basic and fully diluted share were $0.22and $0 .20 respectively. In the fourth quarter of 1999, ESCreported a net loss.

Excluding a $1.0 million loss from ESC's start-up dental unit,OpusDent, and $0.7 loss from the new acolight program, ESC'sfully diluted EPS was $0.26 per share.

36

For fiscal year 2000, net revenue was $161.6 million compared to$142.2 million in 1999. Operating income was $22.3 million, or14% of revenues, net income was $17.3 million, and net earnings

per basic and fully diluted share were $0.68 and $0.61 respectively.For full year 1999, ESC reported an operating and net loss of$140.2 million and $140.8 million respectively.

96. Commenting on the reported results, Defendant Sutton stated: "We are delighted

that ESC is rounding out a full year of growth and profitability. Strength in our key target

markets has accelerated our momentum and we expect it to continue in the first quarter and

moving forward."

97. The revenue figures reported in the March 12, 2001 earnings release were

materially false and misleading tar the reasons alleged in 1140--54, 61-62, 66-73.

98. Sutton's statement concerning growth and profitability were knowingly false and

misleading for the reasons alleged in IN 40-54, 61-62, 66-73. Moreover, because reported

revenue figures were based on `sales" achieved through improper accounting techniques, Sutton

knew that the Company would continue the growth spawned by the purported "strength in [the

Company's] key target markets" in the first quarter and beyond.

99. On March 30, 2001, the Company filed its Forrin 10-K, for the fiscal year ended

December 31, 2000. The 2000 10-K repeated the same reported revenue for the fourth quarter of

2000. The Company's share price increased by approximately $2 per share or 9% following this

announcement. As alleged above in 111140-54, 61-62, 66-73, the reported revenue was materially

false and misleading.

100. The Company also used its Form 14-K to provide assurance on its quality control

measures by touting its ISO 9001 Quality System Certification Award, It would later be revealed

37

in ESC's 2001 Form I O-K that the ISO 9001 award was received back in 1997, with no mention

of any recertification after that period. The 2000 Form 10-K included the following excerpt under

the section entitled "GOVERNMENT REGULATION":

The Company received a Quality System Certification Award for

being in compliance with ISO 9001. ISO 9001 is a globally

recognized standard established by the international Standard

Organization in Geneva, Switzerland and has been adopted by more

than 90 countries worldwide. ISO 9001 embraces all principles of

the GMP and QSR and is the most comprehensive of the quality

assurance standards. ISO certification is based upon adherence to

established quality assurance standards and manufacturing process

control,

101. On April 19, 2001, Lumenis announced that "it expect[ed] sales for the quarter

ended March 31, 2001, to be about $43 million," an increase of approximately 20% over the

reported figure for the same quarter in 2000. Commenting on the Company's expected results,

Defendant Sutton stated: "We are delighted to have experienced continued strong revenue growth

in the first quarter, seasonally a weaker quarter, Excluding one-time charges, the revenues

generated should translate into strong operating results, to be reported in mid May." '.1'he market

reacted approvingly to this news, sending the stock up 6% to $27.94 per share.

102. The revenue figure reported in the April 19' pre-earnings release was materially

false and misleading for the reasons alleged in 1140-54, 61-62, 66-73. Moreover, Sutton's

statement concerning " continued strong revenue growth" was knowingly false and misleading for

the reasons alleged in 111140-54, 61-62, 66-73. Further, Sutton knew that because the expected

revenue figure was based on "sales" achieved through improper accounting techniques, the

Company would report "strong operating results."

38

103. On May 15, 2001, the Company announced its operating results for the first

quarter ended March 31, 2001. Lumenis reported the following results in the May 15' press

release:

The results include sales of $43.9 mm, up 22% from the samequarter in 2000. Fully diluted EPS, excluding one time gains andcharges was $0.22, up from $0.03 for the corresponding quarter in2000. Including one-time charges and gains ESC earned $0.14 perfully diluted share.

104. Commenting on the reported results, Defendant Sutton stated: "Q1 demonstrated

the continued growing strength of our business in what is usually a seasonally slow quarter. I'm

particularly satisfied by our continuing margin expansion. Looking ahead, demand continues to

be strong," The market again responded with approval, raising the Company's stock price

another 6%o to $29.05 per share.

105. The revenue and earnings figures reported in the May 15`' earnings release were

materially false and misleading for the reasons alleged in ¶¶ 40-54, 61-62, 66-73. Moreover,

Sutton's statement concerning continued strong demand was knowingly false and misleading for

the reasons alleged in IM 44-54 , 61-62, 66-73.

106. On May 16, 2001, Sutton was quoted in a Globes article, wherein he discussed the

progress of the integration of CMG into Lumenis. In doing so, Sutton led the market to believe

that the integration of the Companies was thus far successful:

ESC bypasses analysts forecasts ( again).

Where does the Coherent deal stand?

"We completed bureaucracy procedures at the end of April, soCoherent' s medical division belongs to us already . Right now, ESCis on its way to change its name to Lumenis , after approval of

39

shareholders- Regarding the fruit of middle streaming expectedfrom the deal of $25 million we already applied a part ofthem.

It can be said that we have touched half of the fruit of middlestreaming. We announced the Boston offices shut down. Parallelywe announced the closing of the plant in Seattle with 65 employeesand the moving all of its technology to Israel and the manufacturingof products will be here.

Next week we have a convention with 100 of our salespeople in theU.S. and Europe. The salespeople are both of ESC andCoherent's medical division. The employees will receive trainingon both companies products, immediately, so we don't lose themomentum of sales.

If we were to begin the merge in the 1" quarter, the sales of the twocompanies would have reached S98 million, so we are on the trackof $400 million sales, because the completion of the deal will be atthe end of April, we lost a month ofjoint sales therefore, the jointsales for the 2'" quarter will be over $80 million."

107. As alleged in 1¶ 83-84, 206-208, Sutton knew that the integration ofCMG into

ESC was not going smoothly.

108. On May 29, 2001, the Company announced its new post-merger product offerings

and Defendant Sutton again misled the investing public by extolling the complementary product

lines and integrated sales and distribution teams purportedly brought to bear by the CMG

acquisition. As alleged above in IN 83-84, 206-208, these comments concealed the fact that the

synergies promised from the combination were illusory ones. The May 29a press release stated in

pertinent part:

New Ultra-Portable High-power LightSheerTM LasersI nt.roduced

ESC Medical Systems Ltd. (NASDAQ: ESCM) announced todaythe introduction of two new models of its highly successfulLightSheer diode lasers for hair removal . The LightSheer ST and

40

LightSheer ET feature the same high-power diode laser technologyas the fifll-sized LightSheer lasers, in a table-top portable design.The LighSheer product line was added to ESC as a part of therecent acquisition of Coherent Medical Group.

Yacha Sutton, CEO and President of £SC Medical commented,"We foresee many cross-selling opportunities with these newsystems, especially with our IPL photo rejuvenation products. Theultra compact design and cutting edge technical specifications alsoopen up a new replacement market for existing hair removalsystems. Earlier, we only focused on penetrating new accounts."During the next few months ESC will be rolling out an additionalfour products, all ofwhich hold the promise to become the leader intheir respective applications.

1. U.S. shipments of the Selecta 7000 to treat open angleglaucoma, the leading cause ofpreventable blindness for patientsover 40 years of age are now under way. FDA clearance for thisdevice was recently granted. Open angle glaucoma affects over 50million people worldwide.

2. The GyneLase, for treating menorrhagia, or excessive menstrualbleeding, will begin large-scale shipments, under the multi-milliondollar arrangement with Karl Storz GnnbH this quarter.

3. Opus 5, the new dental diode laser for tooth whitening andminor soft tissue applications, will be launched this quarter inmarkets around the world-

4. ClearLight, the breakthrough acne treatment system, isbeginning shipments outside the United States.

Mr. Sutton concluded. "We are focused on maximizin our stropworld-wide distrib ution channel by leveragin g co ntinded internaldevelopment alongside selective acquisitions of complementaryproduct lines."

Separately, Mr. Sutton commeted, "We are continuing toexperience strong demand for our products. We are in the finalstage of setting up integrated sales and distribution teams. Lastweek over 100 salespeople from the US and Europe participated inproduct cross training sessions. Our Asian sales team completed a

41

similar program earlier. We have already closed several dealsinvolving cross marketing opportunities.

(Emphasis added.)

109. The Company announced its post-combination organizational structure in a press

release dated July 10, 2001. In that press release, Defendant Sutton again falsely touted the

synergies realized by the CMG transaction:

ESC Medical Announces Organizational Structure

Esc Medical Systems (NASDAQ: ESCM) announced today that ithas finalized the reorganization of its senior management to reflectthe integration of Coherent Medical Group.

Excluding our smaller dental and industrial units, ESC will beoperating under a matrix organizational structure to allow thenewly combined company to focus upstream marketing, R&D, andmanufacturing activities within product application areas whileintegrating efforts geographically to ensure efficient downstreammarketing and sales activities. This structure is designed toleverage administration expenses geographically across theorganization, while allowing for flexibility in the discreetmanagement of each target market's product lines.

`"Throughout the company, we enjoy a deep base of talent andindustry expertise . Wc'vc now got the key leaders in place to driveour continued growth," said President and Chief Executive OfficerYacha Sutton. "The establishment of this structure and leadershipteam should facilitate a smooth completion of our integration

efforts. We look forward to continuing to build our business with

the new organization."

The members of the corporate team include: Yacha Sutton, CEO

and President ; Louis P. Scafuri , Chief Operating Officer, Sagi A.

Genger, Chief Financial Officer; Asif Adil, Executive Vice President

for Business Development ; Yossi Gal, Executive Vice President for

Human Resources; Mono Greacel, Executive Vice President for

Operations ; Hadar Solomon, Executive Vice President , General

Counsel and Corporate Secretary,

42

(Emphasis added.)