1

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

TIM Brasil Institutional Presentation

1st QTR 2016

2

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Telecom Landscape 4

TIM Brasil 9

TIM’s Strategy 14

Portfolio 19

Quality & Network Evolution 23

Regulatory Update 28

Financial Data 30

Perspectives 34

Agenda

*Click on the page number to access the section

3

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Telecom Landscape

4

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

ARPU Ranking

(US$)

Service Revenues Ranking

Mobile Penetration Ranking Customer Base Ranking

(Mln lines)

49

43

38

37

34

5

182

139

53

24

23

18

1.305

700

356

276

259

Telecom Landscape

Source: Merrill Lynch - Global Wireless Matrix 4Q15 (3Q15 data) | Top 5 + Brazil

Brazilian market is reaching maturity but there is still room for user profitability and the main opportunity is in data

4th (= vs. 3Q15)

17th (-2 vs. 3Q15)

39th (= vs. 3Q15) 9th (-2 vs. 3Q15)

182%

177%

172%

171%

164%

138%

(%)

(US$ bln)

China

India

USA

Brazil

Indonesia

Finland

Arab. Emir.

Russia

Hong Kong

Portugal

Brazil

USA

China

Japan

UK

India

Brazil

Canada

USA

Switzerland

Norway

Qatar

Brazil

5

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações 5

Brazil 2016-18: meeting the challenges

1.8% 2.7%

0.1%

-3.5% -3.8%

0.0%

1.7%

2012 2013 2014 2015E 2016E 2017E 2018E

5.8% 5.9% 6.4%

10.7%

7.0% 5.4% 5.0%

2012 2013 2014 2015 2016E 2017E 2018E

2.04 2.34 2.66

3.90 4.25 4.30 4.31

2012 2013 2014 2015 2016E 2017E 2018E

Source: latest IMF estimates for GDP; Internal Estimates for Exchange Rates forecast, Inflation, MTR Value, SIM/user and market revenues trend

Protecting results in a tougher Macroeconomic Scenario…

…and adapting fast to capture opportunities in a reshaped industry context

0.34 0.30

0.23 0.16

0.10 0.06 0.03 0.02

2012 2013 2014 2015 2016 2017 2018 2019

1.65 1.72

1.81 1.89

2.03 2.00 1.96 1.94

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Real GDP Growth (% YoY)

Inflation Rate (% YoY)

Exchange Rate (R$/USD)

MTR Glide Path (R$/min)

SIM / Unique User

Mobile Market Revenues (R$ bln)

2.7 10.5 23.0

39.7 33.8

45.7

36.5

25.1

36.5

50.8 61.7

64.8

2007 2011 2015e 2018e

Voice

Data

6 Institutional Presentation

TIM Participações

The industry mobile revenue represented 52% of the total industry revenues in 1Q16

Mobile Fixed Fixed BB Pay-TV Group

Customers 2015FY (000´s) 66,234 592 252 n.a. 67,079

Market share 2015FY 25.7% 1.4% 1.0% n.a. ---

Net Adds 12M (000´s) -9,486 190 99 n.a. -9,197

Net Revs 1Q16 (R$ Mln) 3,771 181 3,952

ARPU 1Q16 (R$) 17.2 n.a. n.a. n.a. ---

Mobile Fixed Fixed BB Pay-TV Group

Customers 2015FY (000´s) 73,268 14,868 7,291 1,788 97,216

Market share 2015FY 28.4% 34.1% 28.6% 9.4% 29.2%

Net Adds 12M (000´s) -6,669 -331 347 136 -6,517

Net Revs 1Q16 (R$ Mln) 6,213 4,218 10,431

ARPU 1Q16 (R$) 26,9 n.a. n.a. n.a. ---

Mobile Fixed Fixed BB Pay-TV Group

Customers 2015FY (000´s) 65,978 11,624 8,110 9,897 95,609

Market share 2015FY 25.6% 26.7% 31.7% 52.0% ---

Net Adds 12M (000´s) -5,129 -10 587 -274 -4,826

Net Revs 1Q16 (R$ Mln) 3,006 5,948 8,954

ARPU 1Q16 (R$) 14.0 n.a. n.a. n.a. ---

Mobile Fixed Fixed BB Pay-TV Group

Customers 2015FY (000´s) 48,061 15,105 6,372 1,169 70,707

Market share 2015FY 18,6% 34.7% 24.9% 6.1% ---

Net Adds 12M (000´s) -2,857 -1,324 -181 -134 -4,496

Net Revs 1Q16 (R$ Mln) 2,032 4,507 6,539

ARPU 1Q16 (R$) 16.7 n.a. n.a. n.a. ---

TIM represents 23.1% of the industry mobile revenue1

1 - Mobile revenue considers only the 5 major players. Oi numbers are adjusted to include corporate mobile

Source: Anatel and players’ financial statements

Mobile Revenues Share

Nextel Oi Claro TIM Vivo

Brazilian Telcos X-Ray

30.5% 31.7% 33.2% 36.7% 38.0%

25.6% 26.6% 26.5% 24.1% 23.1%

17.5% 17.7% 17.5% 17.9% 18.4%

18.3% 17.4% 16.6% 15.5% 15.,0%

8.1% 6.6% 6.1% 5.8% 5.4%

2012 2013 2014 2015 1Q16

7

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

A5: PR/SC

* Population 18.1 Mln

* Mobile base 22.9 Mln

* Penetration 126.5%

* TIM’s Market Share 52.4%

A6: RS

* Population 11.3 Mln

* Mobile base 14.8 Mln

* Penetration 131.5%

* TIM’s Market Share 12.4%

Mobile market: Regional overview

Penetration per Estate

(Mar/16)

A1 e A2 A3

A4

A5

A6

A7

A8

A9

A10

Source: Anatel, IBGE

A1 e A2: SP

* Population 44.7 Mln

* Mobile base 64.5 Mln

* Penetration 144.3%

* TIM’s Market Share 26.1%

A3: RJ/ES

* Population 20.6 Mln

* Mobile base 27.0 Mln

* Penetration 131.4%

* TIM’s Market Share 14.1%

A4: MG

* Population 21.0 Mln

* Mobile base 24.6 Mln

* Penetration 117.5%

* TIM’s Market Share 24.8%

A7: CO

* Population 19.7 Mln

* Mobile base 26.6 Mln

* Penetration 135.1%

* TIM’s Market Share 15.1%

A8: NO

* Population 20.4 Mln

* Mobile base 19.2 Mln

* Penetration 93.8%

* TIM’s Market Share 30.1%

A9: BA/SE

* Population 17.5 Mln

* Mobile base 19.1 Mln

* Penetration 108.9%

* TIM’s Market Share 20.9%

A10: NE

* Population 32.4 Mln

* Mobile base 39.1 Mln

* Penetration 120.9%

* TIM’s Market Share 33.0%

64.5 24.6 23.0 16.8 14.8 14.3 11.8 10.8 8.2

8.0 8.5 6.2

.,1

4.7

4.0

4.2 4.2 3.7 3.4 3.9 3.7 2.3

2.2 1.9 0.8 0.7 0.5

144%

118%

139%

110%

131% 128% 126% 121%

99%

120% 124%

209%

88% 117% 101% 127% 121%

92%

127% 122% 111% 101%

121% 123% 99%

95% 93%

SP MG RJ BA RS PR PE CE PA GO SC DF MA PB ES MT RN AM MS PI AL SE RO TO AC AP RR

Base Móvel (MM) Penetração (base/pop)

TIM: Market share leader

TIM: 2nd position in market share

Mobile base (mln)

Penetration (base/pop)

8

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

TIM Brasil

9

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

A solid history of growth

TIM’s Position

1998 2003 2009 2016

Purpose

To connect and take care of every customer, so everyone can do more

Care about the costumer

Transparency

Commitment

Innovation

Agility

Values

New Position & New Brand Shareholders’ Structure

TIM Celular S.A. Intelig

TIM Brasil Serv. e Part. S.A. Free Float

Telecom Italia

100%

TIM Participações S.A.

ON: 33% (808,249,935) ON: 67% (1,611,969,946)

100% 100%

10

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Knowing TIM better

67 million customers (26% of share)

183 own stores

15 Customer Care Centers

~12 thousand employees

Presence in Brazil since 1998

18th largest Private Company in Brazil (Exame Magazine - 2015)

Approximately R$16 billion of Market Capitalization

15,000 km fiber optical backbone

5,500 km fiber optical backhauling

Growth via Acquisiton

2nd Player Market & Revenue

Share

95% of urban pop. coverage

(3,460 cities)

Leader in 4G coverage

(439 cities)

>9 million 4G users

5%

27% 29% 35%

45% 48%

2010 2011 2012 2013 2014 2015

4.2 4.7

5.1 5.2 5.5 5.4

2010 2011 2012 2013 2014 2015

20.3

24.8 27.8

29.7 29.0 25.8

2010 2011 2012 2013 2014 2015

Gross Revenues (R$ bln)

Data Penetration (over customer base)

EBITDA (R$ bln)

CAGR+5% CAGR

+5%

11

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

Statutory Audit Committee:

• Report to Board of Directors

• Oversight Financial reporting

• Analyze anonymous complaints

Compensation Board and Internal Control and Risk Board

operate indefinitely and act independently

Whistleblower channel website: www.tim.com.br/canal-

denuncia

Brazilian Law “Lei das S.A”

Legal Requirements

Demand for transparency

and disclosures

Highest level of Corporate

Governance Requirement of protection for

minority shareholders

Unique Telco company listed on the Novo Mercado

Committees to Reinforce and Guarantee Solid Corporate Governance

10 members (3 independents)

3 members (1 independent)

3 members (3 independents)

3 members

5 members (2 independents)

8 members

Equal rights: vote, dividends and tag along

Higher liquidity

• Single class of share (ordinary shares)

Greater independence of Board of Directors (at least 30%)

Strict disclosure policy

Corporate Governance

12

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Corporate Social Responsibility

Founded in July, 2013

MISSION: We are committed to creating and strengthening resources and strategies for the

democratization of science and innovation that promote human development in Brazil, with mobile

technology as one of the main facilitators.

Joined UN Global Compact in 2008

Member of ISE (Sustainability Index) for

8 consecutive years

Member of ICO2 (Efficient Carbon Index) for 6 consecutive years

ISO 14001 certified since 2010, 1st Brazilian

telco Sustainability

TIM Stands out in Sustainability

In public schools

185,000 children and 6,300 professors

In museums and science and technology centers

More than 70,000 people

R$2.5 million in funding

In public administration

Participatory Urban Caretaker

o 4 municipalities

Cultural maps

o 7 municipalities and RS & CE government

In the federal institutions of professional and technological education

TIM Tec

o MOOC platform

Partnership with 5 federal institutes

Commitment with the 2014-16 Social Investment Plan: R$45 million

13

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

TIM’s Strategy

14

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações 14

Strategic Guidelines

Telecom industry transformation from Voice to Data

Market maturity and user behavior change impacting Customer Base and Positioning

Challenging Macroeconomic Scenario

Infrastructure requirements evolving with Data and 4G

Context Changes Key Strategic Priorities

Reset positioning: Network Quality / Offer Innovation / Customer Experience

Protect value of Prepaid base: From Market Share to Revenue Share

Increase share of Mid/High Value customers: focus on higher value

Stabilize Corporate Business: accelerate Top /Enterprise and turnaround SMB

Sustain Network Investment with prioritized approach and focus on 4G

Focus on Efficiency: as a structural element

I

II

III

IV

V

VI

15

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

98

210

07 08 09 10 11 12 13 14 15e 16e 17e 18e

0.41 0.42 0.42 0.42 0.42 0.36 0.32 0.24

0.16 0.10 0.06 0.03 0.02

07 08 09 10 11 12 13 14 15e 16e 17e 18e 19e

64

602

14 15e 16e 17e 18e 19e

Community Era

MTR

Stabilization Market

conditions require a new

STRATEGY

Multiple SIM cycle

Prepaid segment to follow SIM

card cycle

Data traffic booming

Data overcoming voice

revenues by 2016

Expansion Consolidation

07 08 09 10 11 12 13 14 15 16e 17e 18e 11 12 13 14 15e 16e 17e

Brazil Mobile Traffic (PB)

Mln customers

82 min

07 08 09 10 11 12 13 14 15e 16e

Voice slowdown

Avg Market MOU(min)

Source: Internal estimates and BofA ML Global Matrix

< 117 min

Data Era

R$

Reality Check: Transition Phase

Transition

Industry Evolution Path

16

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

o Volume Driven (market share)

o Base of Pyramid

o Offer Based on Community

o Handset leadership (focus on volume)

o Mass Channels

o Mobile + B2C

o Value Driven (value share)

o Big Middle of Pyramid + Value Clients

o Bundle of Voice + Data + Off-net

o Handset Support (focus on value)

o Value Channels

o Mobile + B2C + B2B + selective convergence

15 16 17 18 19

OLD go2market

NEW go2market

Commercial Strategy Evolution

Recurring billing

Protection of data value

Customer spending

concentration

Voice + data bundles

On-net + off-net voice

NEW PORTFOLIO

MODEL

17

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

Fast reaction in multiple fronts, positioned for recovery path

Keep investment focus

+394 new cities with 4G vs. 1Q15

4G leadership position

Increasing customer base value

Off-net to all plans & focus on

mobile bundle

Defending results from tax impact

Actions to offset

ICMS increase

Workforce Restructuring program

Adapting to market reality

Company repositioning

New brand launch: quality,

innovation, customer experience

~10% of customer base in the new

portfolio

Price repositioning to

compensate tax

Rightsizing workforce

On track with Efficiency Plan

> R$ 1 bln in efficiency (2015-17)

~40% of program achieved in 1Q16

New phase launched in 2Q16

Infrastructure Offer Portfolio Efficiency Actions Positioning

18

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Portfolio

19

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

28% market share

Data reaccelerating, driven by 4G

Fast growing on 4G

Changing

revenue profile

Data penetration increase Traffic acceleration

(BOU: bytes of use per data customers) (million users)

4G penetration

3G penetration

Innovative Revenues

(R$ bln; YoY growth) (R$; YoY growth)

Source: Anatel

340

502

1Q15 2Q15 3Q15 4Q15 1Q16

26% 48% YoY Growth

(3G & 4G user over customer base)

Source: Anatel

Data ARPU

1.0

1.3

1Q15 1Q16

5.7

7.4

1Q15 1Q16

68% +13pp YoY

Smartphone

penetration

+29% +26%

3.0

9.2

1Q15 2Q15 3Q15 4Q15 1Q16

~55%

~14%

1Q15 1Q16

20

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

POSTPAID PREPAID

Portfolio evolution: a better experience leading to higher ARPU

TIM PRÉ 150 R$7/week recurring

150MB + 100min off-net + SMS

TIM PRÉ 500 R$10/week

recurring 500MB + 100min off

+ Deezer

TIM PRÉ Classic R$8/week

recurring 250MB + unlimited

on-net + SMS

TIM PRÉ 1GB R$35/month

recurring 1GB + 400 min off-

net + SMS

CONTROLE

TIM CONTROLE R$50/month

1.5GB + 500min off-net + WhatsApp

TIM PÓS R$139/month

5GB + 1,000min off-net + WhatsApp

Recurrence as base of all

propositions

VALUE BASE

Offer segmentation to

improve convenience

Better customer experience

for higher ARPU

New Portfolio Evolution

TIM PRÉ 300 R$10/week recurring 300MB + 100min off-

net + SMS

TIM PRÉ 150 R$7/week

recurring 150MB + 100min off-

net + SMS

TIM CONTROLE R$50/month

1GB + 500min off-net + WhatsApp

TIM PÓS R$99/month

2GB + 1,000min off-net + WhatsApp

New Portfolio

at launch

Upselling to improve

profitability

21

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

Base New OfferBase New Offer

New portfolio presenting positive results

Mobile number portability update

Improving Quality of Revenues…

ARPU improvement

in all segments 10% of total

base in the new offer

% of new offers over gross adds

Prepaid ARPU Postpaid ARPU

(postpaid users)

(R$) (R$)

17%

20%

1Q15 1Q16

Postpaid mix

63%

65%

nov/dec-15 1Q16

(postpaid and control users)

22

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Quality & Network Evolution

23

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

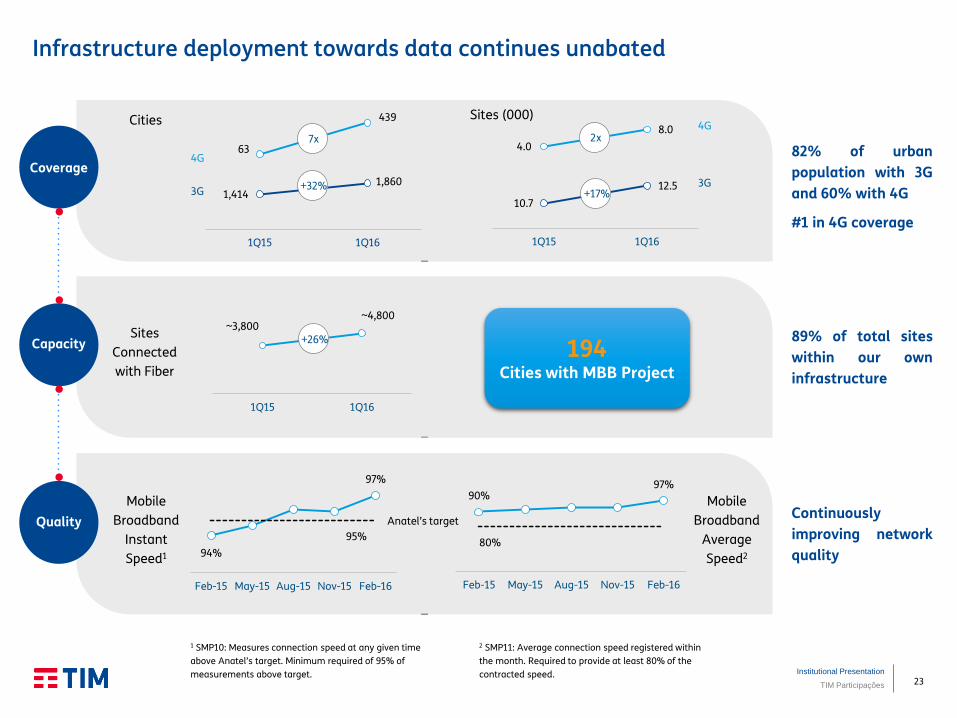

63

439

1,414 1,860

1Q15 1Q16

Infrastructure deployment towards data continues unabated

Coverage

Capacity

Quality

82% of urban

population with 3G

and 60% with 4G

#1 in 4G coverage

89% of total sites

within our own

infrastructure

Continuously

improving network

quality

Sites

Connected

with Fiber

Cities Sites (000)

194 Cities with MBB Project

94%

97%

95%

Feb-15 May-15 Aug-15 Nov-15 Feb-16

90% 97%

80%

Feb-15 May-15 Aug-15 Nov-15 Feb-16

Mobile

Broadband

Instant

Speed1

Mobile

Broadband

Average

Speed2

1 SMP10: Measures connection speed at any given time

above Anatel’s target. Minimum required of 95% of

measurements above target.

2 SMP11: Average connection speed registered within

the month. Required to provide at least 80% of the

contracted speed.

Anatel’s target

+32%

~3,800 ~4,800

1Q15 1Q16

+26%

10.7

12.5

1Q15 1Q16

4G

3G +17%

4G

3G

7x 4.0

8.0 2x

24

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações 24

Capex Cycle: Accelerating 3G and 4G Data Coverage

3.9

4.7

2014 2015 2016e 2017e 2018e

After the 2015-16 cycle, Capex intensity* to gradually decline

4G coverage to overtake 3G

*Excluding Spectrum

• Fast transition from 3G to 4G: better quality and more efficient

• FTTS to support 4G reaching >80% of total traffic

Urban Population Covered

Capex per Technology

>14 bln

<14 bln

2014

2015

2016e

2017e

2018e

4G 3G 2G

• Leadership in 4G Coverage and match 3G coverage in 2 years

• Competitive 3G coverage in all states

• Refarming of 1.8 GHz as a short-term competitive advantage

Number of Sites (000)

36%

59%

79% 82%

~90%

2014 2015 2016e 2017e 2018e

4G

3G

Capex Plan (R$)

4G

Total Sites 12.5

13.3

15.0 16.4

17.7 19.5

2013 2014 2015 2016e 2017e 2018e

Other

Capex/Sales 20% 27%

25

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Transforming the fixed infrastructure

SP

RJ

National fiber Backbone: 10 POPs and 14,500 km

National Voice Backbone: 9 switching voice centrals

and 150 interconnection points

International Interconnection: two nodes in RJ and

SP managing international traffic

Satelite networks links in 9 cities

AES Atimus acquisition in 2011, later called TIM Fiber

Extensive optical fiber network with 5.5 thousand km

Coverage in metropolitan areas of RJ and SP

Potential market of 8.5 million households and 550

thousand companies in 21 cities

Intelig Atimus

Central Switch Fiber Network Satelite Station Central ATM and IP network Submarine cable MAN – Metropolitan Network Presence

26

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Asset Optimization

2013a 2014a 2015e 2016e 2017e Indoor coverage increase in cities already covered with LTE

% of urban population covered with 4G

4G with 1.8

4G with 2.5 only

+6 p.p.

+7 p.p.

Refarming to be applied in other cities

Towers Sale: Largely supporting capex

increase

Possible Technologies

850 MHz

Band 900 MHz

1800 MHz

2100 MHz

2500 MHz

700 MHz

2G 3G

2G 3G

2G 4G

3G 4G 4G

Efficient use of spectrum portfolio

to… Towers sold

Asset optimization

Estimated value of the deal

Towers to be transferred to

American Tower

3 Closings in 2015 (April, September and December)

Cash in from towers sale

From…

Refarming 1,800MHz

27

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Regulatory Update

28

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações 28

Main regulatory topics

2Q16

May June

New regulatory model (1/3) • MiniCom Public

consultation.closed on Jan. 15th.

Net Neutrality • Minister of Justice

launched Public Consultation with the Decree proposal (pubished on May)..

Digital TV • New Analog TV

Switch Off Schedule Approval

• Approval of EAD’s 2nd Payment 1-year postponement to 31/1/2017.

Auction • Resuming Auction of

remaining 1.800, 1.900 and 2.500 MHz spectrum, with local blocks.

Digital TV • Feb 29th - Rio

Verde’s TV Analog Switch Off

Condecine • The Justice granted

preliminary suspension Condecine tax for companies affiliated SinditeleBrasil

April

1Q16

February March January

Auction • Expected Terms

signature of the Auction of remaining 1.800, 1.900 and 2.500 MHz spectrum, with local blocks.

New regulatory model (3/3) • Expected final

ANATEL decision on fixed concession conditions to 2016-2020 review.

Pay TV • New Regulation of

SeAC (Pay TV) under Public Consultation until June.

Condecine • The Supreme Court

determines the obligatory payment of Condecine and suspends the preliminary decision.

Broadband • Fixed data-capped

plans temporarily banned, until ANATEL’s decision

700 MHz • LTE deployment

approval in Rio Verde (expected June).

Res. 664/2016 • ANATEL postponed

(Dec/16) the review of concession contracts and universalization goals.

New regulatory framework (2/3) • MiniCom final report

with competition diagnosis and guideline for ANATEL's actions

Net Neutrality • Presidential Decree

published on May 11th including topics as Traffic discrimination, Transparency, Personal Data and Business Models (Zero Rating).

Brasil Inteligente • Lauched targets to

promote universal internet access (2019)

29

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Financial Data

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

30 Institutional Presentation

TIM Participações

Revenue transformation continues

Business Generated Revs Mix Data Revenues Mix

Data Growth Reacceleration

21% 21%

17%

9%

14%

1Q15 2Q15 3Q15 4Q15 1Q16

(%YoY)

SMS

Innovative Services +26 %

-37 %

39% 47%

61%

53%

1Q15 2Q15 3Q15 4Q15 1Q16

Data

Voice

(% of business generated net revenues)

1Q15 1Q16

(VAS net revenues mix; % YoY)

Service Net Revenues

(%YoY)

-4% -5%

-7%

-8% -8%

1Q15 2Q15 3Q15 4Q15 1Q16

Trend stopped

31

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

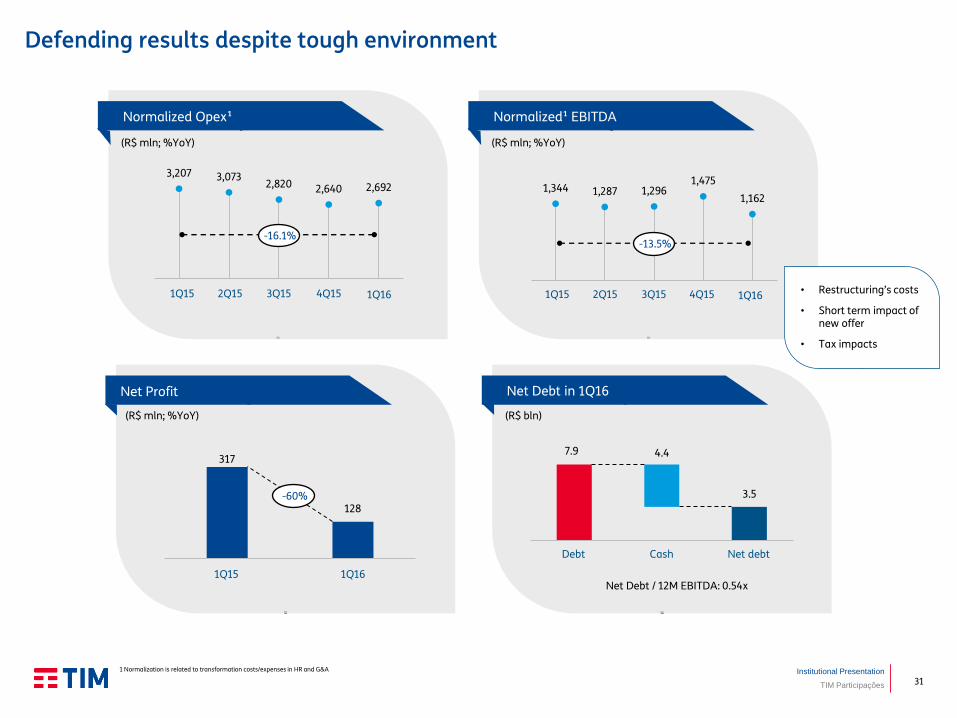

Defending results despite tough environment

1 Normalization is related to transformation costs/expenses in HR and G&A

317

128

Net Profit

(R$ mln; %YoY)

1Q15 1Q16

Net Debt in 1Q16

7.9

3.5

4.4

(R$ bln)

Net Debt / 12M EBITDA: 0.54x

Debt Cash Net debt

Normalized¹ EBITDA

(R$ mln; %YoY)

1Q15 2Q15 3Q15 4Q15 1Q16 • Restructuring’s costs

• Short term impact of new offer

• Tax impacts

Normalized Opex¹

(R$ mln; %YoY)

3,207 3,073 2,820 2,640 2,692

1Q15 2Q15 3Q15 4Q15 1Q16

-16.1%

1,344 1,287 1,296 1,475

1,162

-13.5%

-60%

32

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

Process Improvement

Digging deeper into cost reduction – Efficiency Program 2.0

Optimization / Control

Strategic Sourcing

Organization/ Rightsizing

and Efficiency

Process Improvement

Business Model

Changes

> R$1 bln in savings

Jan/15 Dec/17

Business Model

Changes

• 3 years program

• Between R$ 300-350 mln per year

Mar/16

Corporate Efficiency Plan

Additional Efficiency & Cost Restructuring

• Enhancement of corporate efficiency program;

• Additional efforts in Sales & Marketing (commissioning

model and advertising);

• Full cash cost approach;

+ Sales & MKT

New Approach

Optimization / Control

+

Strategic Sourcing

+

Organization/ Rightsizing

and Efficiency

+

~ 40%

33

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Perspectives

34

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações

Conclusion & Outlook

Less impact from

MTR

-8.7% -9.2%

4Q15 1Q16 2Q16 3Q16 4Q16

-5.3%

-13.5%

4Q15 1Q16 2Q16 3Q16 4Q16

Mobile Service Net Revenues (%YoY)

Normalized¹ EBITDA (%YoY)

1 Normalization is related to transformation costs/expenses in HR and G&A

Headwinds should gradually reduce…

Traditional business

stabilization

Data services

resuming growth

Better customer

base mix

Continuous cost

efficiency program

intensified

Keeping focus on

Infrastructure

35

R 000 G 070 B 145

R 235 G 000 B 040

R 000 G 081 B 135

R 000 G 110 B 184

R 000 G 156 B 222

R 244 G 209 B 000

R 243 G 150 B 016

R 231 G 055 B 140

R 220 G 104 B 075

R 158 G 004 B 073

R 197 G 189 B 193

R 116 G 175 B 039

R 000 G 000 B 000

Institutional Presentation

TIM Participações 35

Guidance Summary

Targets reaffirm commitment to long term value creation for all shareholders

KPIs Targets

> R$1 bln in savings between 2015-17 Opex

Margin expansion for every year between 2016-18 EBITDA Margin

< R$14 bln between 2016-18 Capex*

Data as main revenue component from 2016, focus on Revenue Share Service Revenues

*Excluding Spectrum

36

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações

Safe Harbor

TIM on the Web

Statements in this presentation, as well as oral statements made by the

management of TIM Participações S.A. (the “Company”, or “TIM”), that are not

historical fact constitute “forward looking statements” that involve factors that

could cause the actual results of the Company to differ materially from historical

results or from any results expressed or implied by such forward looking

statements. The Company cautions users of this presentation not to place undue

reliance on forward looking statements, which may be based on assumptions

and anticipated events that do not materialize.

TIM website: www.tim.com.br

Investor Relations website: www.tim.com.br/ir

TIM on Twitter: @TIMBrasil

Investor Relations Twitter: @TIM_RI

TIM on Facebook: www.facebook.com/timbrasil

TIM on YouTube: www.youtube.com/timbrasil

37

R 000

G 070

B 145

R 235

G 000

B 040

R 000

G 081

B 135

R 000

G 110

B 184

R 000

G 156

B 222

R 244

G 209

B 000

R 243

G 150

B 016

R 231

G 055

B 140

R 220

G 104

B 075

R 158

G 004

B 073

R 197

G 189

B 193

R 116

G 175

B 039

R 000

G 000

B 000

Institutional Presentation

TIM Participações 37