International Fixed Income

Topic IVB: International Fixed Income

Pricing -Investment Strategies

Outline

• Strategies– Relation between international

fixed income bonds– Examples of active strategies

• An example: mean-variance analysis

I. Strategies

• Trading strategies in the international fixed income arena are theoretically separable:– Currency bet

• buy fn. Gvt bond - could lose money if interest rates rise

• buy/sell forwards/futures in currency market

– Foreign interest rate bet• buy fn. Gvt bond - could lose money if currency

depreciates• buy forward-hedged, foreign gvt. bonds

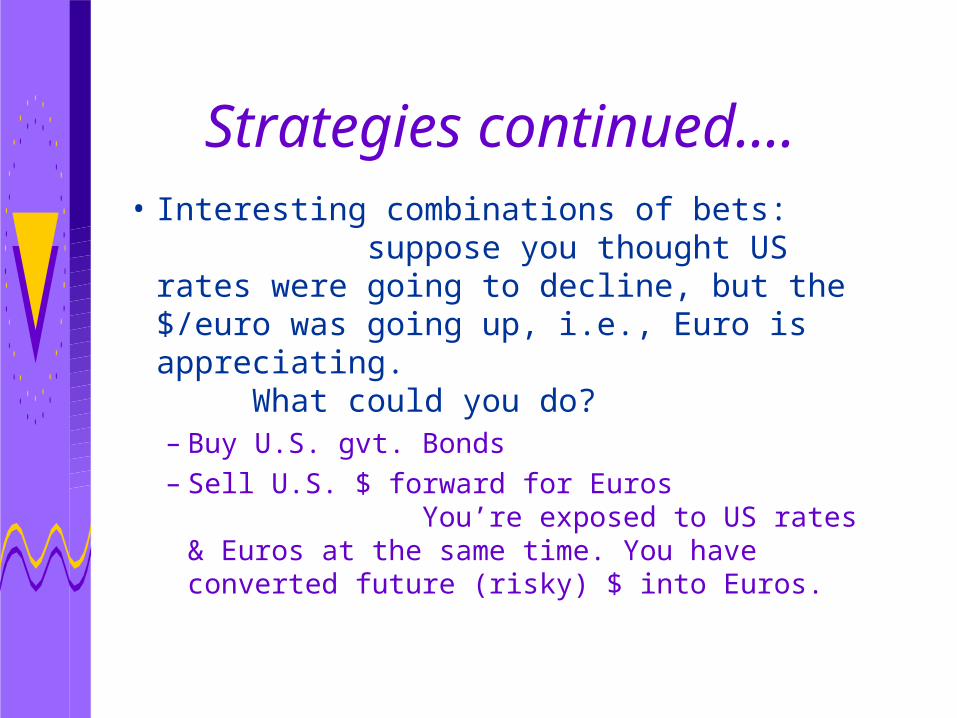

Strategies continued….• Interesting combinations of bets:

suppose you thought US rates were going to decline, but the $/euro was going up, i.e., Euro is appreciating. What could you do?– Buy U.S. gvt. Bonds– Sell U.S. $ forward for Euros

You’re exposed to US rates & Euros at the same time. You have converted future (risky) $ into Euros.

IA: Pricing International Fixed Income Bonds

• How do you price future cash flows?

• What does interest rate parity tell us about relative discount factors across countries?

• General pricing formula• Example from class

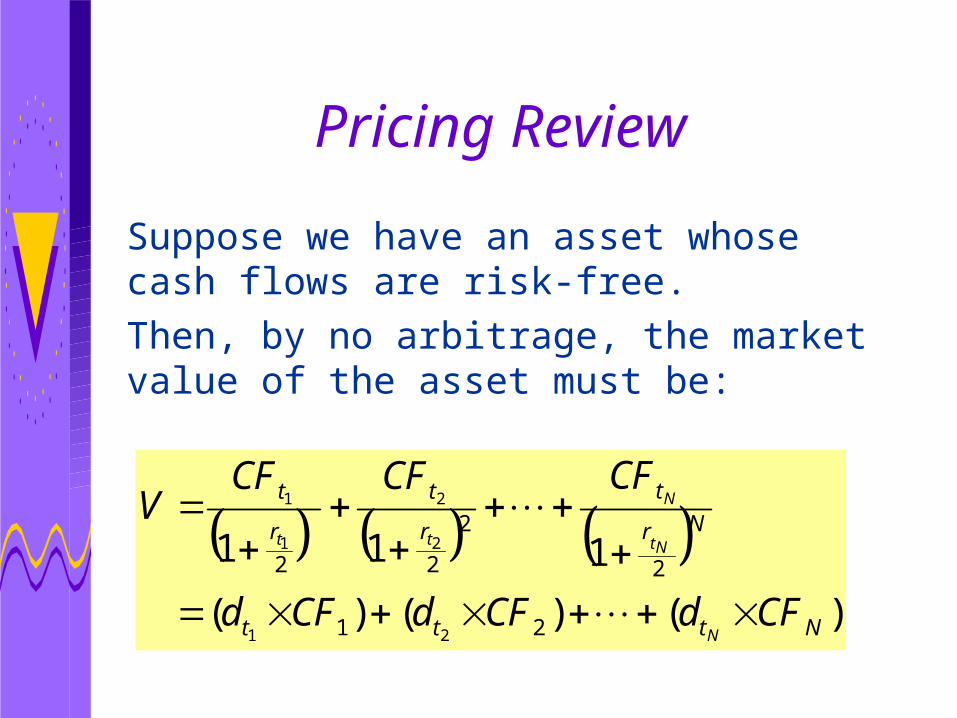

Pricing Review

Suppose we have an asset whose cash flows are risk-free.Then, by no arbitrage, the market value of the asset must be:

)()()(

111

21

2

2

22

21

2

2

1

1

Nttt

Nr

t

r

t

r

t

CFdCFdCFd

CFCFCFV

N

Nt

N

tt

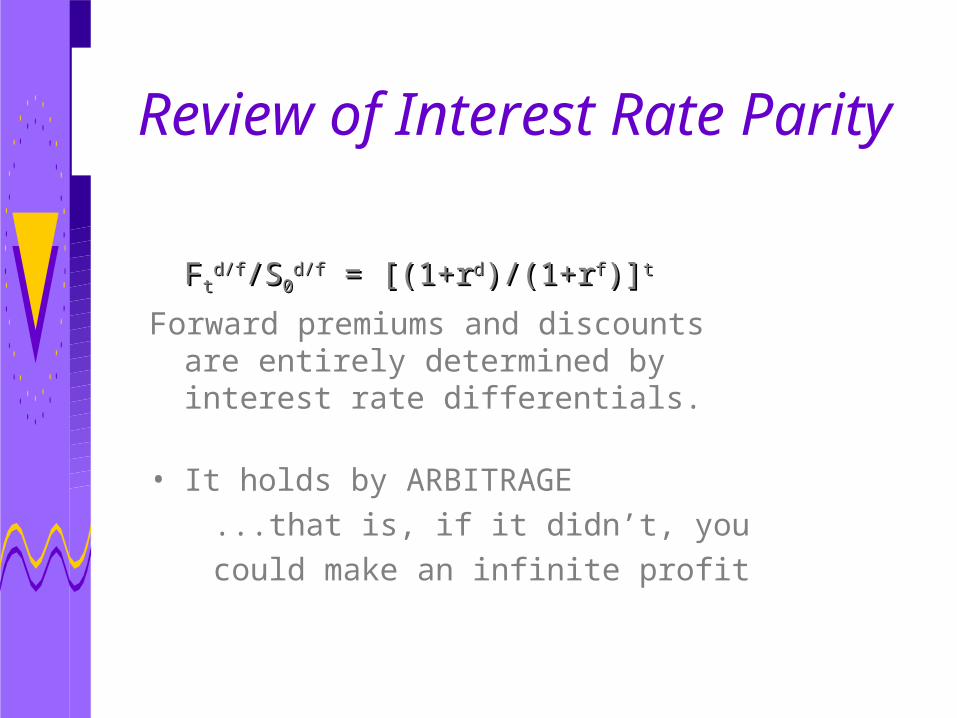

Review of Interest Rate Parity

FFttd/fd/f/S/S00

d/fd/f = [(1+r = [(1+rdd)/(1+r)/(1+rff)])]tt

Forward premiums and discounts are entirely determined by interest rate differentials.

• It holds by ARBITRAGE...that is, if it didn’t, you could make an infinite profit

General Pricing Formula

• What these two no-arbitrage results tell us is that the price of a foreign bond can be described by the (I) domestic bond valuation, and (II) the forward currency curve.

Underlying Mathematics

dt

ft

tr

tr

fd

fdt

d

d

S

Fft

dt

2

2

2

2/

0

/

1

1

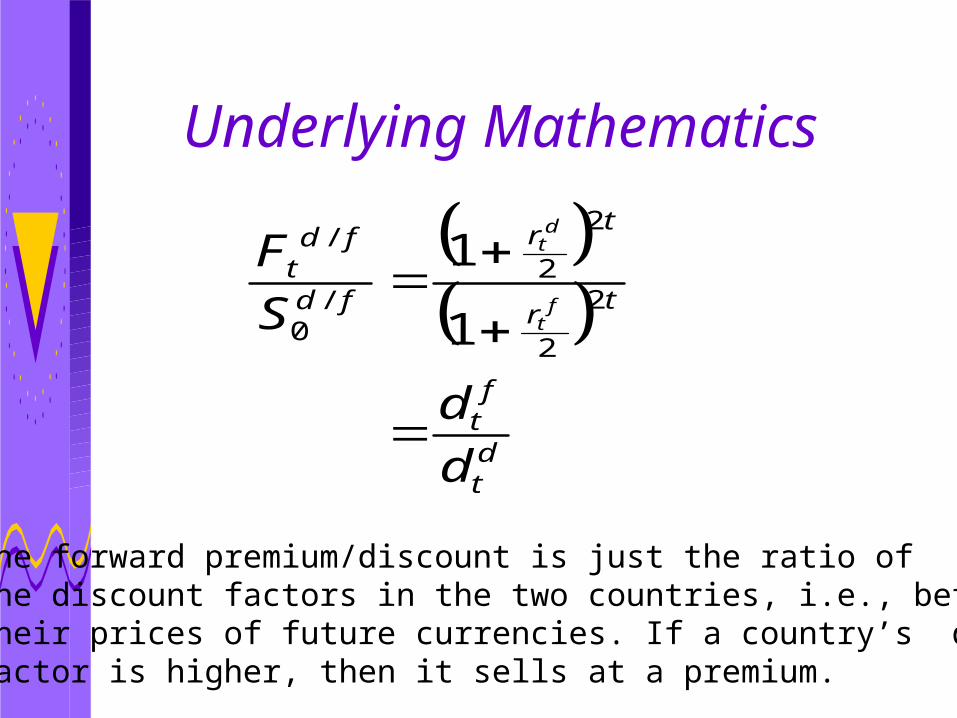

The forward premium/discount is just the ratio ofthe discount factors in the two countries, i.e., between their prices of future currencies. If a country’s discountfactor is higher, then it sells at a premium.

General Pricing Formula

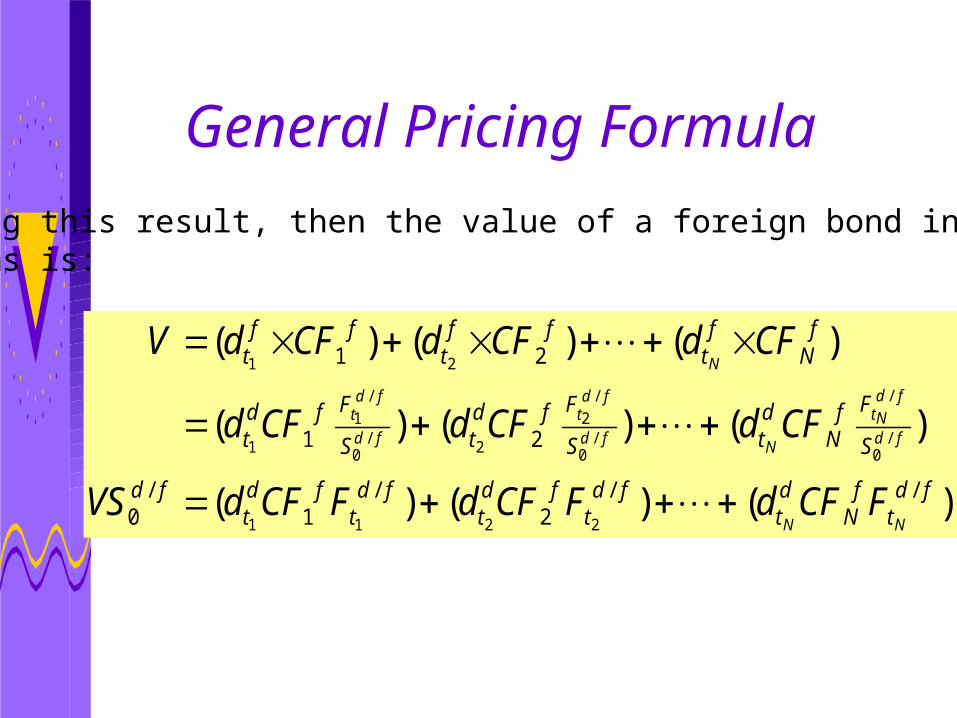

Using this result, then the value of a foreign bond in dollarterms is:

)()()(

)()()(

)()()(

//2

/1

/0

21

21

2211

/0

/

/0

/2

2/

0

/1

1

21

fdt

fN

dt

fdt

fdt

fdt

fdt

fd

S

FfN

dtS

FfdtS

Ffdt

fN

ft

fft

fft

NN

fd

fdNt

Nfd

fdt

fd

fdt

N

FCFdFCFdFCFdVS

CFdCFdCFd

CFdCFdCFdV

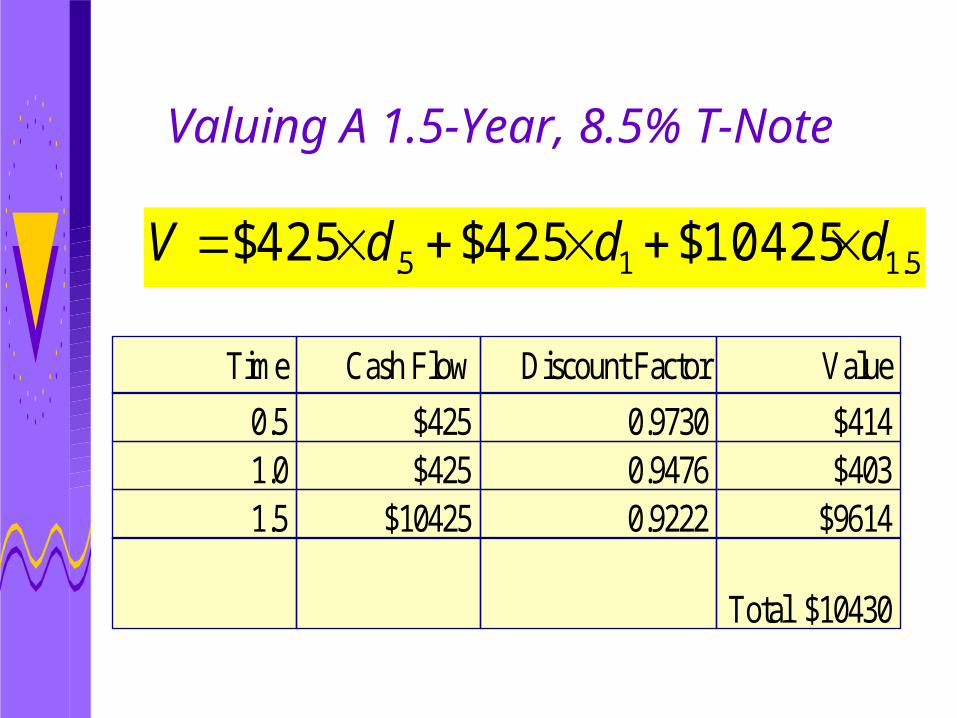

Example of U.S. Treasury Bond

• From class earlier in semester, recall that the 6-mth, 1-yr and 1.5-yr discount factors for the U.S. were 0.9730, 0.9476 and 0.9222, respectively.

• The corresponding exchange rate for $/DEM is a spot rate of .7095, and corresponding forward rates of .7158, .7214 and .7256.

Valuing A 1.5-Year, 8.5% T-Note

5.115. 10425$425$425$ dddV

Time Cash Flow Discount Factor Value

0.5 $425 0.9730 $4141.0 $425 0.9476 $4031.5 $10425 0.9222 $9614

Total $10430

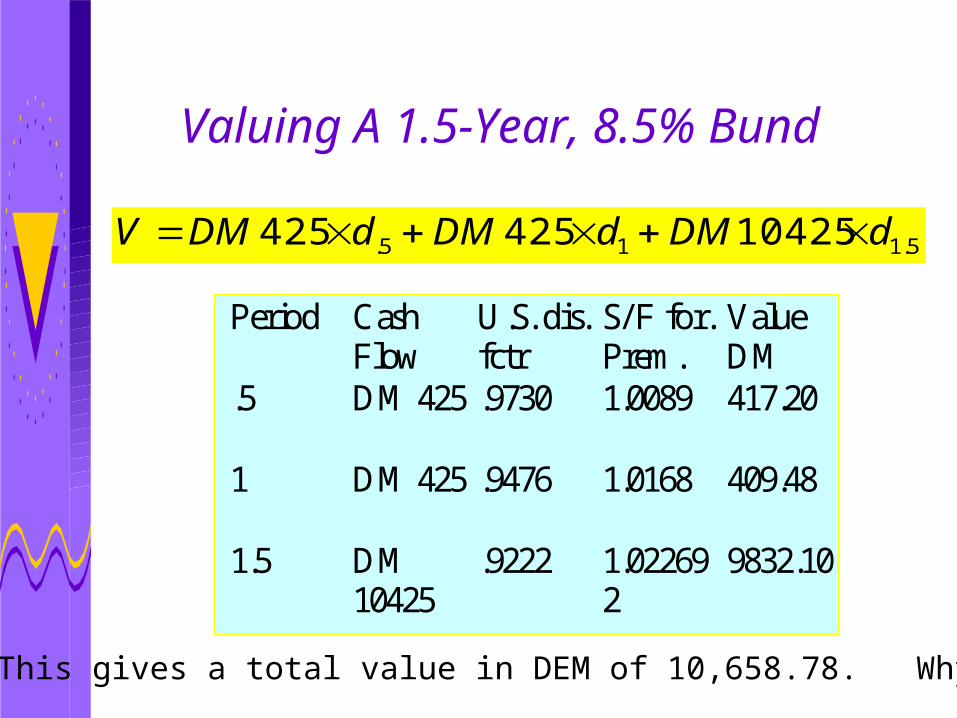

Valuing A 1.5-Year, 8.5% Bund

5.115. 10425425425 dDMdDMdDMV

Period CashFlow

U.S. dis.fctr

S/F for.Prem.

ValueDM

.5 DM 425 .9730 1.0089 417.20

1 DM 425 .9476 1.0168 409.48

1.5 DM10425

.9222 1.022692

9832.10

This gives a total value in DEM of 10,658.78. Why?

Intuition

• What happened if the prices of these bonds were different?– Translate the German bund into a

U.S. bond by converting future DEM cash flows into US $.

– Take US$ and discount them at U.S. rates. If this value is different then the bund value times the $/DEM exchange rate, you have arbitrage!

IB. Popular Active Strategies

• Tactical hedging strategy:– Hedge only a percentage of the currency

risk, depending on strength of currency forecasts (e.g., if you expect currency to appreciate, don’t hedge as much)

– R($)=Ru(1-P)+Rh(P), where P=% hedged

• Currency overlay strategy:– Hedged foreign currency position, plus a

currency bet– R($)=Rh+P(St+1/Ft), where -1<P<1

Comparison of Strategies

• 4 strategies (hedge, no hedge, tactical, currency overlay) based on forecasts

• Levich-Thomas (1993) study of 5 markets (DM,C$,GBP,Yen,Global) over 1977-90 period.

• Sharpe Ratio measures (-r)/ , i.e., excess return/risk During this period, it was 0.12 for US gvts.

Sharpe Ratios

0

0.2

0.4

0.6

0.8

1

1.2

1.4

UK

JPN

CAN

GE

R

GLO

BAL

UnhgeHdgeTacticalOverlay

Sharpe Ratios in Subperiods for Global Portfolio of Intl. Bonds

-1

-0.5

0

0.5

1

1.5

2

2.5

1977-90 77-78 79-81 82-84 85-87 88-90

UnhgeHdgeTacticalOverlay$ strat.

II. Mean-Variance Analysis

• One popular criteria for judging an investment is to consider its expected return (its mean) versus its risk (its volatility)

• Mean-variance portfolios find the weights in each individual security (in this case, intl. Gvt. Bonds) which give minimum volatility for a given level of expected return.

Procedure

• Consider a portfolio of intl. Government bonds, each with return, Ri.

• The expected return on the portfolio is

where wi is the weight in each bond.• Find the weight wi that, for a given

E[R], minimizes the risk, i.e., the vol. Of the portfolio:

][i

ii REw

i

iiRwvol

Example of Mean-Variance Efficient Portfolios (unhedged and

hedged), 1977-90

Example of Mean-Variance Efficient Portfolios (unhedged and

hedged), 1977-90

General Conclusions

• “Substantial” benefits in terms of risk reduction by diversifying across bond markets - diversify away idiosyncratic central bank and economy risks that do not get incorporated into exchange rates.

• There seem to be gains from actively managing international bond portfolios by using forecast methods for exchange rates:– these methods were discussed earlier in the

course, and involve such techniques as market-based and model-based (e.g., technical and fundamental) methods.