Draft copy

Submitted

By Pradeep kumar t

1

EXECUTIVE SUMMARY

As we all know IPO – INITIAL PUBLIC OFFERING is the hottest

topic in the current industry, mainly because of India being a developing

country and lot of growth in various sectors which leads a country to

ultimate success. And when we talk about country’s growth which is

dependent on the kind of work and how much importance to which sector is

given. And when we say or talk about industries growth which leads the

economy of country has to be balanced and given proper finance so as to

reach the levels to fulfill the needs of the society. And industries which have

massive outflow of work and a big portfolio then its very difficult for any

company to work with limited finance and this is where IPO plays an

important role.

This report trying to help to find out IPO performance during 2010,

what are the companies which issued during this year. How and what are

the steps taken by the companies before going for any IPO and also the role

of (SEBI) Securities and Exchange Board of India the BSE and NSE , what

are primary and secondary markets and also the important terms related to

IPO. It gives us idea of how IPO is driven in the market and what are

various factors taken into consideration before going for an IPO. And it also

tells us how we can more or less judge a good IPO. Then we all know that

2

scams have always been a part of any sector you go in for which are

covered in it and also few recommendations are given for the same. It also

gives us some idea about what are the expenses that a company undertakes

during an IPO.

IPO has been one of the most important generators of funds

for the small companies making them big and given a new vision in past

and it is still continuing its work and also for many coming years.

3

Chapter

INTRODUCTION

4

INTRODUCTION TO IPO

IPO stands for Initial Public Offering and means the new offer of

shares from a company which was previously unlisted. This is done by

offering those shares to the public, which were held by the promoters or the

private investors prior to the IPO. In the case when other investors or

Promoter held the shares the stake holding comes down to the extent their

shares are offered to the public. In other cases new shares are issued to the

public and the shares, which are with the promoters stay with them. In both

cases the share of the promoters in the total capital comes down.

For example say there are 100 shares in a company and 50 of these

are offered to the public in an IPO then in such a case the promoter’s stake

in the company comes down from 100% to 50%. In another case the

company issues 50 additional shares to the public and the stake of the

promoter comes down from 100% to 67%.

Normally in an IPO the shares are issued at a discount to what is

considered their intrinsic value and that’s why investors keenly await IPOs

and make money on most of them. IPO are generally priced at a discount,

which means that if the intrinsic value of a share is perceived to be Rs.100

the shares will be offered at a price, which is lesser than Rs.100 say Rs.80

5

during the IPO. When the stock actually lists in the market it will list closer

to Rs.100. The difference between the two prices is known as Listing Gains,

which an investor makes when investing in IPO and making money at the

listing of the IPO. A Bullish Market gives IPO investors a clear opportunity

to achieve long term targets in a short term phase.

What is an IPO

An IPO is the first sale of stock by a company to the public. A

company can raise money by issuing either debt or equity. If the company

has never issued equity to the public, it's known as an IPO.

Companies fall into two broad categories: private and public.

A privately held company has fewer shareholders and its owners don't have

to disclose much information about the company. Anybody can go out and

incorporate a company: just put in some money, file the right legal

documents and follow the reporting rules of your jurisdiction. Most small

businesses are privately held. But large companies can be private too. Did

you know that IKEA, Domino's Pizza and Hallmark Cards are all privately

held?

It usually isn't possible to buy shares in a private company. You can

6

approach the owners about investing, but they're not obligated to sell you

anything. Public companies, on the other hand, have sold at least a portion

of themselves to the public and trade on a stock exchange. This is why

doing an IPO is also referred to a “going public”.

Public companies have thousands of shareholders and are subject to

strict rules and regulations. They must have a board of directors and they

must report financial information every quarter. In the United States, public

companies report to the Securities and Exchange Commission (SEC). In

other countries, public companies are overseen by governing bodies similar

to the SEC. From an investor's standpoint, the most exciting thing about a

public company is that the stock is traded in the open market, like any other

commodity. If you have the cash, you can invest. The CEO could hate your

guts, but there's nothing he or she could do to stop you from buying stock.

The first sale of stock by a private company to the public, IPO’s

are often issued by smaller, younger companies seeking capital to expand,

but can also be done by large privately-owned companies looking to

become publicly traded. In an IPO, the issuer obtains the assistance of an

underwriting firm, which helps it determine what type of security to issue

(common or preferred), best offering price and time to bring it to market.

IPO’s can be a risky investment. For the individual investor, it is tough to

7

predict what the stock will do on its initial day of trading and in the near

future since there is often little historical data with which to analyze the

company. Also, most IPO’s are of companies going through a transitory

growth period, and they are therefore subject to additional uncertainty

regarding their future value.

Primary and Secondary markets

In the primary market securities are issued to the public and the

proceeds go to the issuing company. Secondary market is term used for

stock exchanges, where stocks are bought and sold after they are issued to

the public.

PRIMARY MARKET

The first time that a company’s shares are issued to the public, it is by

a process called the initial public offering (IPO). In an IPO the company

offloads a certain percentage of its total shares to the public at a certain

price.

Most IPO’S these days do not have a fixed offer price. Instead they

follow a method called BOOK BUILDIN PROCESS, where the offer price

is placed in a band or a range with the highest and the lowest value (refer to

the newspaper clipping on the page). The public can bid for the shares at

8

any price in the band specified. Once the bids come in, the company

evaluates all the bids and decides on an offer price in that range. After the

offer price is fixed, the company allots its shares to the people who had

applied for its shares or returns them their money.

SECONDRY MARKET

Once the offer price is fixed and the shares are issued to the people,

stock exchanges facilitate the trading of shares for the general public. Once

a stock is listed on an exchange, people can start trading in its shares. In a

stock exchange the existing shareholders sell their shares to anyone who is

willing to buy them at a price agreeable to both parties. Individuals cannot

buy or sell shares in a stock exchange directly; they have to execute their

transaction through authorized members of the stock exchange who are also

called STOCK BROKERS.

Why Go Public?

Basically, going public (or participating in an "initial public offering"

or IPO) is the process in which a business owned by one or several

individuals is converted into a business owned by many. It involves the

offering of part ownership of the company to the public through the sale of

debt or more commonly, equity securities (stock).

9

Going public raises cash and usually a lot of it. Being publicly

traded also opens many financial doors:

Because of the increased scrutiny, public companies can usually

get better rates when they issue debt.

As long as there is market demand, a public company can always

issue more stock. Thus, mergers and acquisitions are easier to do because

stock can be issued as part of the deal.

Trading in the open markets means liquidity. This makes it

possible to implement things like employee stock ownership plans, which

help to attract top talent.

Being on a major stock exchange carries a considerable amount of

prestige. In the past, only private companies with strong fundamentals could

qualify for an IPO and it wasn't easy to get listed.

The internet boom changed all this. Firms no longer needed strong

financials and a solid history to go public. Instead, IPOs were done by

smaller startups seeking to expand their businesses. There's nothing wrong

with wanting to expand, but most of these firms had never made a profit and

didn't plan on being profitable any time soon. Founded on venture capital

funding, they spent like Texans trying to generate enough excitement to

10

make it to the market before burning through all their cash. In cases like

this, companies might be suspected of doing an IPO just to make the

founders rich. This is known as an exit strategy, implying that there's no

desire to stick around and create value for shareholders. The IPO then

becomes the end of the road rather than the beginning.

How can this happen? Remember: an IPO is just selling stock. It's all

about the sales job. If you can convince people to buy stock in your

company, you can raise a lot of money.

Getting In On an IPO

The Underwriting Process

Getting a piece of a hot IPO is very difficult, if not impossible. To

understand why, we need to know how an IPO is done, a process known as

underwriting.

When a company wants to go public, the first thing it does is hire an

investment bank. A company could theoretically sell its shares on its own,

but realistically, an investment bank is required - it's just the way Wall

Street works. Underwriting is the process of raising money by either debt or

equity (in this case we are referring to equity). You can think of

underwriters as middlemen between companies and the investing public.

11

The biggest underwriters are Goldman Sachs, Merrill Lynch, Credit Suisse

First Boston, Lehman Brothers and Morgan Stanley.

The company and the investment bank will first meet to negotiate the

deal. Items usually discussed include the amount of money a company will

raise, the type of securities to be issued and all the details in the

underwriting agreement. The deal can be structured in a variety of ways.

For example, in a firm commitment, the underwriter guarantees that a

certain amount will be raised by buying the entire offer and then reselling to

the public. In a best efforts agreement, however, the underwriter sells

securities for the company but doesn't guarantee the amount raised. Also,

investment banks are hesitant to shoulder all the risk of an offering. Instead,

they form a syndicate of underwriters. One underwriter leads the syndicate

and the others sell a part of the issue.

Once all sides agree to a deal, the investment bank puts together a

registration statement to be filed with the SEC. This document contains

information about the offering as well as company info such as financial

statements, management background, any legal problems, where the money

is to be used and insider holdings. The SEC then requires a cooling off

period, in which they investigate and make sure all material information has

been disclosed. Once the SEC approves the offering, a date (the effective

date) is set when the stock will be offered to the public.

12

During the cooling off period the underwriter puts together what is

known as the red herring. This is an initial prospectus containing all the

information about the company except for the offer price and the effective

date, which aren't known at that time. With the red herring in hand, the

underwriter and company attempt to hype and build up interest for the issue.

They go on a road show - also known as the "dog and pony show" - where

the big institutional investors are courted.

As the effective date approaches, the underwriter and company sit

down and decide on the price. This isn't an easy decision: it depends on the

company, the success of the road show and, most importantly, current

market conditions. Of course, it's in both parties' interest to get as much as

possible.

Finally, the securities are sold on the stock market and the money is

collected from investors.

As you can see, the road to an IPO is a long and complicated one.

You may have noticed that individual investors aren't involved until the

very end. This is because small investors aren't the target market. They don't

have the cash and, therefore, hold little interest for the underwriters. If

underwriters think an IPO will be successful, they'll usually pad the pockets

of their favorite institutional client with shares at the IPO price. The only

13

way for you to get shares (known as an IPO allocation) is to have an

account with one of the investment banks that is part of the underwriting

syndicate. But don't expect to open an account with $1,000 and be showered

with an allocation. You need to be a frequently trading client with a large

account to get in on a hot IPO.

IPO – ADVANTAGES AND DISADVANTAGES

The decision to take a company public in the form of an initial

public offering (IPO) should not be considered lightly. There are several

advantages and disadvantages to being a public company, which should

thoroughly be considered. This memorandum will discuss the advantages

and disadvantages of conducting an IPO and will briefly discuss the steps to

be taken to register an offering for sale to the public. The purpose of this

memorandum is to provide a thumbnail sketch of the process. The reader

should understand that the process is very time consuming and complicated

and companies should undertake this process only after serious

consideration of the advantages and disadvantages and discussions with

qualified advisors.

14

Advantages of going public

Increased Capital

A public offering will allow a company to raise capital to use for

various corporate purposes such as working capital, acquisitions, research

and development, marketing, and expanding plant and equipment.

Liquidity

Once shares of a company are traded on a public exchange, those

shares have a market value and can be resold. This allows a company to

attract and retain employees by offering stock incentive packages to those

employees. Moreover, it also provides investors in the company the option

to trade their shares thus enhancing investor confidence.

Increased Prestige

Public companies often are better known and more visible than

private companies, this enables them to obtain a larger market for their

goods or services. Public companies are able to have access to larger pools

of capital as well as different types of capital.

Valuation

15

Public trading of a company's shares sets a value for the company

that is set by the public market and not through more subjective standards

set by a private valuator. This is helpful for a company that is looking for a

merger or acquisition. It also allows the shareholders to know the value of

the shares.

Increased wealth

The founders of the company often have the sense of increased

wealth as a result of the IPO. Prior to the IPO these shares were illiquid and

had a more subjective price. These shares now have an ascertainable price

and after any lockup period these shares may be sold to the public, subject

to limitations of federal and state securities laws.

Disadvantages of going Public

Time and Expense

Conducting an IPO is time consuming and expensive. A successful

IPO can take up to a year or more to complete and a company can expect to

spend several hundreds of thousands of dollars on attorneys, accountants,

and printers. In addition, the underwriter's fees can range from 3% to 10%

of the value of the offering. Due to the time and expense of preparation of

16

the IPO, many companies simply cannot afford the time or spare the

expense of preparing the IPO.

Disclosure

The SEC disclosure rules are very extensive. Once a company is a

reporting company it must provide information regarding compensation of

senior management, transactions with parties related to the company,

conflicts of interest, competitive positions, how the company intends to

develop future products, material contracts, and lawsuits. In addition, once

the offering statement is effective, a company will be required to make

financial disclosures required by the Securities and Exchange Act of 1934.

The 1934 Act requires public companies to file quarterly statements

containing unaudited financial statements and audited financial statements

annually. These statements must also contain updated information regarding

nonfinancial matters similar to information provided in the initial

registration statement. This usually entails retaining lawyers and auditors to

prepare these quarterly and annual statements. In addition, a company must

report certain material events as they arise. This information is available to

investors, employees, and competitors.

Decisions based upon Stock Price

17

Management's decisions may be effected by the market price of the

shares and the feeling that they must get market recognition for the

company's stock.

Regulatory Review

The Company will be open to review by the SEC to ensure that the

company is making the appropriate filings with all relevant disclosures.

Falling Stock Price

If the shares of the company's stock fall, the company may lose

market confidence, decreased valuation of the company may effect lines of

credits, secondary offering pricing, the company's ability to maintain

employees, and the personal wealth of insiders and investors.

Vulnerability

If a large portion of the company's shares are sold to the public, the

company may become a target for a takeover, causing insiders to lose

control. A takeover bid may be the result of shareholders being upset with

management or corporate raiders looking for an opportunity. Defending a

hostile bid can be both expensive and time consuming. Once a company has

weighed the advantages and disadvantages of being a public company, if it

decides that it would like to conduct an IPO it will have to retain a lead

18

Parameters to judge an IPO

Good investing principles demand that you study the minutes of

details prior to investing in an IPO. Here are some parameters you should

evaluate:-

Promoters

Is the company a family run business or is it professionally owned?

Even with a family run business what are the credibility and professional

qualifications of those managing the company? Do the top level managers

have enough experience (of at least 5 years) in the specific type of business?

Industry Outlook

The products or services of the company should have a good demand

and scope for profit.

Business Plans

Check the progress made in terms of land acquisition, clearances

from various departments, purchase of machinery, letter of credits etc. A

higher initial investment from the promoters will lead to a higher faith in the

organization.

Financials

19

Why does the company require the money? Is the company floating

more equity than required? What is the debt component? Keep a track on

the profits, growth and margins of the previous years. A steady growth rate

is the quality of a fundamentally sound company. Check the assumptions

the promoters are making and whether these assumptions or expectations

sound feasible.

Risk Factors

The offer documents will list our specific risk factors such as the

company’s liabilities, court cases or other litigations. Examine how these

factors will affect the operations of the company.

Key Names

Every IPO will have lead managers and merchant bankers. You can

figure out the track record of the merchant banker through the SEBI

website.

Pricing

Compare the company’s PER with that of similar companies. With

this you can find out the P/E Growth ratio and examine whether its earning

projections seem viable.

20

Listing

You should have access to the brokers of the stock exchanges where

the company will be listing itself.

Understanding the role of intermediaries

Who are the intermediaries in an issue?

Merchant Bankers to the issue or Book Running Lead Managers

(BRLM), syndicate members, Registrars to the issue, Bankers to the issue,

Auditors of the company, Underwriters to the issue, Solicitors, etc. are the

intermediaries to an issue. The issuer discloses the addresses, telephone/fax

numbers and email addresses of these intermediaries. In addition to this, the

issuer also discloses the details of the compliance officer appointed by the

company for the purpose of the issue.

Who is eligible to be a BRLM?

A Merchant banker possessing a valid SEBI registration in

accordance with the SEBI (Merchant Bankers) Regulations, 1992 is eligible

to act as a Book Running Lead Manager to an issue.

What is the role of a Lead Manager? (pre and post issue)

In the pre-issue process, the Lead Manager (LM) takes up the due

diligence of company’s operations/ management/ business plans/ legal etc.

21

Other activities of the LM include drafting and design of Offer documents,

Prospectus, statutory advertisements and memorandum containing salient

features of the Prospectus. The BRLMs shall ensure compliance with

stipulated requirements and completion of prescribed formalities with the

Stock Exchanges, RoC and SEBI including finalization of Prospectus and

RoC filing. Appointment of other intermediaries viz., Registrar(s), Printers,

Advertising Agency and Bankers to the Offer is also included in the pre-

issue processes. The LM also draws up the various marketing strategies for

the issue.

The post issue activities including management of escrow accounts,

co-ordinate non-institutional allocation, intimation of allocation and

dispatch of refunds to bidders etc are performed by the LM. The post Offer

activities for the Offer will involve essential follow-up steps, which include

the finalization of trading and dealing of instruments and dispatch of

certificates and demat of delivery of shares, with the various agencies

connected with the work such as the Registrar(s) to the Offer and Bankers

to the Offer and the bank handling refund business. The merchant banker

shall be responsible for ensuring that these agencies fulfill their functions

and enable it to discharge this responsibility through suitable agreements

with the Company.

What is the role of a registrar?

22

The Registrar finalizes the list of eligible allottees after deleting the

invalid applications and ensures that the corporate action for crediting of

shares to the demat accounts of the applicants is done and the dispatch of

refund orders to those applicable are sent. The Lead manager co-ordinates

with the Registrar to ensure follow up so that that the flow of applications

from collecting bank branches, processing of the applications and other

matters till the basis of allotment is finalized, dispatch security certificates

and refund orders completed and securities listed.

What is the role of bankers to the issue?

Bankers to the issue, as the name suggests, carries out all the

activities of ensuring that the funds are collected and transferred to the

Escrow accounts. The Lead Merchant Banker shall ensure that Bankers to

the Issue are appointed in all the mandatory collection centers as specified

in DIP Guidelines. The LM also ensures follow-up with bankers to the issue

to get quick estimates of collection and advising the issuer about closure of

the issue, based on the correct figures.

Question on Due diligence

The Lead Managers state that they have examined various

documents including those relating to litigation like commercial disputes,

patent disputes, disputes with collaborators etc. and other materials in

23

connection with the finalization of the offer document pertaining to the said

issue; and on the basis of such examination and the discussions with the

Company, its Directors and other officers, other agencies, independent

verification of the statements concerning the objects of the issue, projected

profitability, price justification, etc., they state that they have ensured that

they are in compliance with SEBI, the Government and any other competent

authority in this behalf.

Current issues

SEBI simplifies IPO process – New Companies to list in 12 days – Benefits

Securities and Exchange Board of India (SEBI) has been making significant

changes to the the stock market rules and proceedings for quite some time now and

especially on the Initial public offering (IPO) front.

First, it was Applications Supported by Blocked Amount (ASBA) process which

simplified IPO applying procedures and reduced hassles of money refunds. Now, the

Sebi has decided to reduce the time between public issue closure and listing to 12 days

from existing period of up to 22 days. And, this comes to effect on May 1, 2010.

This will greatly help to reduce the reduce instances of manipulation in the pre-

listing period. Several IPOs had created havoc before and after listing due to big grey

market plays. Market operators manipulate the IPO process using the long gap in the

listing process.

24

Benefits:

1. When IPO Applied thru ASBA process, your whole IPO bid money stays in your bank account and continues to earn the interests till the IPO allotment status is out. After then, only the money for allotted shares will be debited. So, we don’t have to worry about the refunds from the IPO registrars for you have paid only the exact amount to the registrar.

2. With shorter IPO listing time, duration for which money locked-in your bank account is shorter. You would see the result of IPO allotments and listings in 12 days and the IPO money locked-in would be released sooner enabling us to apply for more IPOs than before. Also, SEBI believes this shorter duration can bring down the grey market manipulations of IPO listing prices.

25

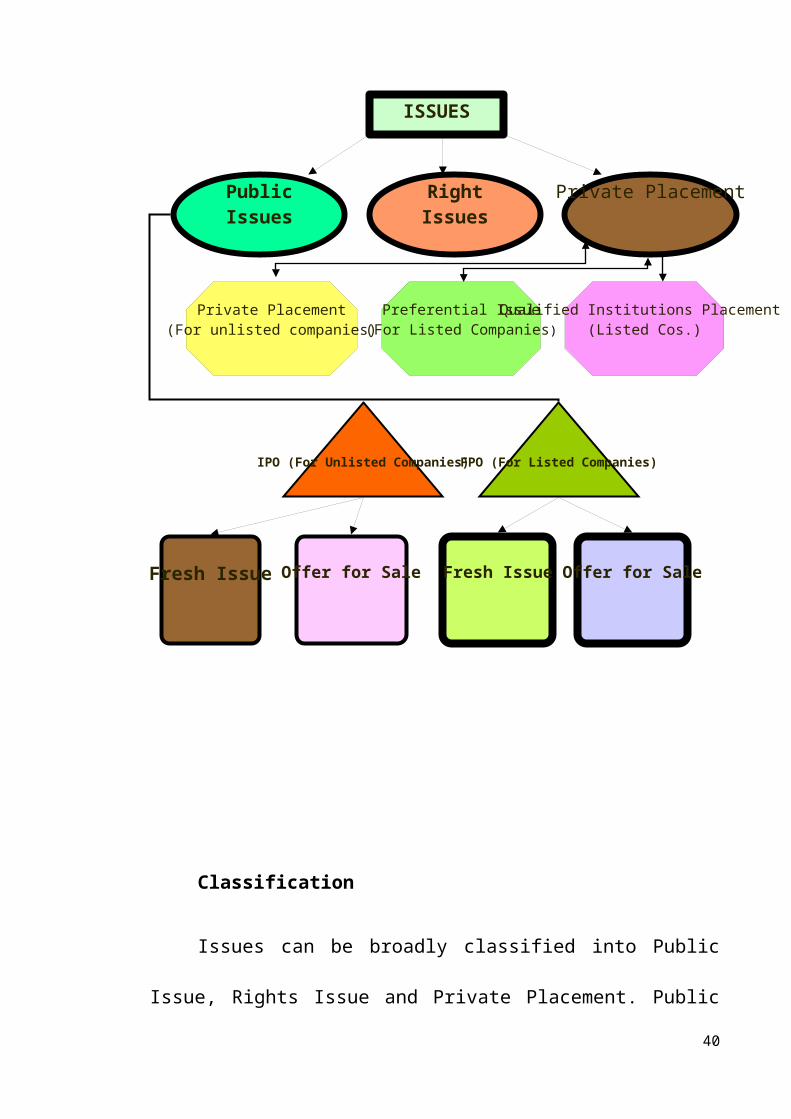

ISSUES

PublicIssues

RightIssues

Private Placement

Private Placement(For unlisted companies)

Preferential Issue(For Listed Companies)

Qualified Institutions Placement (Listed Cos.)

IPO (For Unlisted Companies) FPO (For Listed Companies)

Fresh Issue Offer for Sale Fresh Issue Offer for Sale

The classification of issues can be described as below:

26

VARIOUS TYPES OF ISSUES

Classification

Issues can be broadly classified into Public Issue, Rights Issue and

Private Placement. Public issues can be further classified into Initial Public

offerings and further public offerings. In a public offering, the issuer makes

an offer for new market investors to join their shareholders family. The

issuer company makes detailed disclosures as per the SEBI (DIP)

Guidelines, 2000 in its offer document and offers it for subscription.

The significant features of each type of Issue are illustrated below:

Initial Public Offering

IPO is when an unlisted company makes either a fresh issue of

securities or an offer for sale of its existing securities or both for the first

time to the public. This provides a listing and trading of the issuer’s

securities.

Rights Issue

It is when a listed company which proposes to issue fresh securities to

its existing shareholders as on a record date. The rights are normally offered

in a particular ratio to the number of securities held prior to the issue. This

route is best suited for companies who would like to raise capital without

diluting stake of its existing shareholders unless they do not intend to

subscribe to their entitlements. A private placement is an issue of shares or

27

of convertible securities by a company to a select group of persons under

Section 81 of the Companies Act, 1956 which is neither a rights issue nor a

public issue. This is a faster way for a company to raise equity capital.

Private Placement

Private Placement of shares or of convertible securities by a listed

company is generally known by name of preferential allotment. A listed

company going for preferential allotment has to comply with the

requirements contained in Chapter XIII of SEBI (DIP) Guidelines

pertaining to preferential allotment in SEBI (DIP) guidelines which inter-

alia includes pricing, disclosures in notice etc., in addition to the

requirements specified in the Companies Act.

Further public offering

FPO is when an already listed company makes either a fresh issue of

securities to the public or an offer for sale to the public, through an offer

document. An offer for sale in such scenario is allowed only if it is made to

satisfy listing or continuous listing obligations.

Pricing of an IPO

28

The pricing of an ipo is a very critical aspect and has a direst impact on

the success or failure of the ipo issue. There area many factors that need to

be considered while pricing an ipo and on attempt should be made to reach

an ipo price that is low enough to generate interest in the market and at the

sometimes, it should be high enough to raise sufficient capital for the

company.

The process for determining an optimal price for the ipo involves the

underwriting arranging share purchase commitments from leading

institutional investors.

Process

Once the final prospectus is printed and distributed to investors,

company arrangements meets with their investment bank to choose the final

offering price and size. The investment bank tries to fix an appropriate price

for the ipo depending upon the demand expected and the capital

requirements of the company.

The pricing of an ipo is a delicate balancing act as the investment

firms try to strike a balance between the company and the investors. The

lead underwriters is the responsibility to ensure smooth trading of the

company’s stock. The underwriter is legally allowed to support the pricing

29

of a newly issued stock by either buying them in the market or by selling

them short.

Ipo , pricing differences

It is generally noted, that there is alarge difference between the price

at the time of issue of an ipo, and the price when they start trading in the

secondary market.

These pricing disparities occur mostly when an ipo is considered

“hot”, or in othere words, when is appeals to a large numbers of investors.

An ipo is “hot” when the demand for it far exceeds the supply.

The imbalance between demand and supply causes a dramatic rise in

the price of each share in the first day itself, during the early hours of

trading.

Under pricing and overpricing of IPOs

Under pricing:

The pricing of an IPO at less than its market value is reffered to as

“underpricing”. Under priced IPOs helps to generate additional interest in

the stock when it first becomes publically traded. This might result in

significant gains for investors who have been allocated share at the offering

price. However, under pricing also results in loss of significant amount of

30

capital that could have been raised had the shares been offered at the higher

price.

Overpricing:

The pricing of an ipo at more than its market value is reffered to as

“overpricing”. Even “over pricing”, of shares is not as healthy option. If the

stock is offered at the higher price than what the market is willing to pay,

then it is likely to become difficult for the underwriters to fulfill their

commitment to sell shares. Furthermore, even if the underwriters are

successful in selling all the issued shares and the stocks falls in value of on

the first day itself of trading, then it is likely to lose its marketability and

hence, even more of its value.

Principal steps in an IPO

Approval of BOD : approval of BOD is required for raising capital from the public.

Appointment of lead managers: the lead manager is the merchant banker

who orchestrates the issue in consultation of the company.

Appointment of other intermediaries:

Co-managers and advisors

Underwriters

Bankers

31

Broker and principal bankers

Registrars

Filing the prospectus with SEBI

The prospective or the offer document communicates information about

the company and the proposed security issue to the investing public. All the

companies seeking to make a public issue have to file their offer document

with SEBI. If SEBI or public does not communicate its observations within

21 days from the filing of the offer document, the company can proceed

with its public issue.

Filing of the prospectus with the registrar of the companies

Once the prospectus have been approved by the concerned stock

exchanges and the consent obtained from the banker, auditors, registrar,

underwriters and others, the prospective signed by the directors, must be

filed with the registrars of companies, with the required documents as per

the companies act 1956.

Printing and dispatch of prospectus : After the prospectus

is filed with the registrar of companies, the company should print the

prospectus. The quantity in which prospectus is printed should be sufficient

32

to meet requirements. They should be send to the stock exchanges and

brokers so they receive them atleast 21 days before the first announcement

is made in the news papers.

Filing of initial listing application : Within 10 days of filing the

prospectus, the initial listing application must be made to the concerned

stock exchanges with the listing fees.

Promotion of the issue : The promotional campaign typically commences

with the filing of the prospectus with the registrar of the companies and

ends with the release of the statutory announcement of the issue.

Statutory announcement : The issue must be made after seeking

approval of the stock exchange. This must be published atleast 10 days

before the opening of the subscription list.

Collections of applications : The Statutory announcement specifies when

the subscription would open, when it would close, and the banks where the

applications can be made. During the period the subscription is kept open,

the bankers will collect the applications on behalf of the company.

33

Processing of applications : Scrutinizing of the applications is done.

Establishing the liability of the underwriters : If the issue is

undersubscribed, the liability of the underwriters has to be established.

Allotment of shares : Proportionate system of allotment is to be followed.

Listing of the issue : The detail listing application should be submitted to

the concerned stock exchange along with the listing agreement and the

listing fee. The allotment formalities should be completed within 30 days.

SIGNIFICANCE OF IPO

Investing in IPO has its own set of advantages and disadvantages. Where on

one hand, high element of risk is involved, if successful, it can even result

in a higher rate of return. The rule is: Higher the risk, higher the returns.

The company issues an IPO with its own set of management objectives and

the investor looks for investment keeping in mind his own objectives. Both

have a lot of risk involved. But then investment also comes with an

advantage for both the company and the investors.

34

The significance of investing in IPO can be studied from 2 viewpoints – for

the company and for the investors. This is discussed in detail as follows:

SIGNIFICANCE TO THE COMPANY:

When a privately held corporation needs additional capital, it can

borrow cash or sell stock to raise needed funds. Or else, it may decide to

“go public”. "Going Public" is the best choice for a growing business for

the following reasons:

The costs of an initial public offering are small as compared to the costs

of borrowing large sums of money for ten years or more,

The capital raised never has to be repaid.

When a company sells its stock publicly, there is also the possibility for

appreciation of the share price due to market factors not directly related to

the company.

It allows a company to tap a wide pool of investors to provide it with

large volumes of capital for future growth.

35

SIGNIFICANCE TO THE SHAREHOLDERS:

The investors often see IPO as an easy way to make money. One of

the most attractive features of an IPO is that the shares offered are usually

priced very low and the company’s stock prices can increase significantly

during the day the shares are offered. This is seen as a good opportunity by

‘speculative investors’ looking to notch out some short-term profit. The

‘speculative investors’ are interested only in the short-term potential rather

than long-term gains.

Eligibility norms for making these issues:

SEBI has laid down eligibility norms for entities accessing thee

primary market through public issues. There is no eligibility norm for a

listed company making a rights issue as it is an offer to the existing

shareholders who are expected to know their company.

The main entry norms for companies making a public issue (IPO or

FPO) are summarized as under:

Entry Norm (EN 1):

The company shall meet the following requirements:

a) Net tangible assets of at least Rs. 3 crores for 3 full years.

36

b) Distributable profits in at least three years.

c) Networth of atleast Rs. 1 crore in three years.

d) If change in name, atleast 50% revenue for proceding 1 year should be form the new activity.

e) The issue size does not exceed 5 times the pre-issue networth.

To provide sufficient flexibility and also to ensure that genuine companies

do not suffer on account of rigidity of the parameters, SEBI has provided

two other alternative routes to company not satisfying any of the above

conditions, for accessing the primary market, as under:

Entry Norm 11(EN 11)

a) Issue shall be through book building route, with at least 50% to be

mandatory allotted to the Qualified Institutional Buyers (QIBs).

b) The minimum post-issue face value capital shall be Rs. 10 crore or there

shall be a compulsory market-making for at least 2 years

OR

Entry Form 111 (EN 111)

a) The ‘project’ is appraised and participated to the extent of 15 % by

Fis/Scheduled Commercial Banks of which at leat 10% comes from the

appraiser(s).

37

b) The minimum post-issue face value capital shall be Rs. 10 crores or there

shall be a compulsory market –making for at least 2 years.

In addition to satisfying the aforesaid eligibility norms, the company shall

also satisfy the criteria of having at least 1000 prospective allotters in its.

38

SEBI GUIDELINES

IPO of Small Companies: Public issue of less than five crores has to

be through OTCEI (Over the Counter Exchange of India) and separate

guidelines apply for floating and listing of these issues.

Public Offer of Small Unlisted Companies (Post-Issue Paid-Up

Capital upto Rs.5 crores) Public issues of small ventures which are in

operation for not more than two years and whose paid up capital after the

issue is greater than 3 crores but less than 5 crores the following guidelines

apply.

1. Securities can be listed where listing of securities is screen based.

2. If the paid up capital is less than 3 crores then they can be listed on the Over

The Counter Exchange of India (OTCEI)

3. Appointment of market makers mandatory on all the stock exchanges where

securities are proposed to be listed.

39

Size of the Public Issue

Issue of shares to general public cannot be less than 25%of the total issue.

Incase of IT, Media and Telecommunication sectors, this stipulation is

reduced subject to the conditions that

1. Offer to the public is not less than 10% of the securities issued.

2. A minimum number of 20 lakh securities is offered to the public

3. Size of the net offer to the public is not less than Rs.30 crores.

Promoters Contribution

1. Promoters should bring in their contribution including premium fully before

the issue.

2. Minimum promoter’s contribution is 20-25% of the public issue.

3. Minimum lock in period for promoter’s contribution is five years.

4. Minimum lock in period for firm allotment is three years.

Collection Centers for Receiving Applications

1. There should be at least 30 mandatory collection centers, which should

include invariably the places where stock exchanges have been established.

2. For issues not exceeding Rs.10 crores the collection centers shall be situated

at:-

40

The 4 métropolitain centres vis. Mumbai, Delhi, Kolkata & Chennai

All such centres where stock exchanges are located in the region in which

the registered office of the company is situated.

Regarding allotments of shares

1. Net Offer the general public has to be atleast 25% of the total issue size for

listing on a stock exchange

2. It is mandatory for a company to get its shares listed at the regional stock

exchange where the registered office of the issuer is located.

3. In an issue of more than 25 crores the issuer is allowed to place the whole

issue by book-building.

4. Minimum of 50% of the Net Offer to the public has to be reserved for the

investors applying for less than 1000 shares.

5. There should be atleast 5 investors for every 1 lakh equity offered.

6. Quoting of PAN or GIR No. in application for the allotment of securities is

compulsory where monetary value of investment is Rs.50000/- or above.

7. Indian development financial institutions and Mutual Fund can be allotted

securities up to 75% of the issue amount.

8. A venture capital fund shall not be entitled to get its securities listed on any

stock exchange till the expiry of 3 years from the date of issuance of

securities.

41

9. Allotment to categories of FIIs and NRIs/OCBs is upto maximum of 24%,

which can be further extended to 30% by an application to the RBI-

supported by a resolution passed in the General Meeting.

Timeframes for Issue and Post-Issue Formalities

1. The minimum period for which the public issue is to be kept open is 3

working days and the maximum for which it can be kept open is 10 working

days. The minimum period for right issue is 15 working days and the

maximum is 60 working days.

2. A public issue is effected if the issue is able to procure 90% of the total

issue size within 60 days from the date of the earliest closure of the public

issue.

3. In case of oversubscription the company may have he right to retain the

excess application money and allot shares more than the proposed issue,

which is referred to as “green-shoe” option

4. Allotment has to be made within 30 days of the closure of the Public issue

and 42 days in case of Rights issue

5. All the listing formalities of a Public Issue have to be completed within 70

days from the date of closure of the subscription list.

Dispatch of Refund Order

42

1. Refund orders have to be dispatched within 30 days of the closure of the

issue.

2. Refunds of excess application money i.e. non-allotted shares have to be

made within 30 days of the closure of the issue.

Other Regulations

1. Underwriting is not mandatory but 90% subscription is mandatory for each

issue of capital to public unless it is disinvestment where it is not applicable.

2. If the issue is undersubscribed then the collected amount should be returned

back

3. If the issue size is more than Rs500 crores, voluntary disclosures should be

made regarding the deployment of funds and an adequate monitoring

mechanism put in place to ensure compliance.

4. There should not be any outstanding warrants for financial instruments of

any other nature, at the time of the IPO.

5. In the event of the initial public offer being at a premium and if the rights

under warrants or other instruments have been exercised within 12 months

prior to such offer, the resultant shares will be not taken into account for

reckoning the minimum promoters contribution further, the same will also

be subject to lock-in.

6. Code of advertisement as specified by SEBI should be adhered to.

43

7. Draft prospectus submitted to SEBI should also be submitted

simultaneously to all stock exchanges where it is proposed to be listed.

Restrictions on Allotments

1. Firm allotments to mutual funds, FII and employees are not subject to any

lock-in period.

2. Within 12 months of the public issue no bonus issue should be made.

3. Maximum percentage of shares, which can be distributes to employees

cannot be more than 5% and maximum shares to be allotted to each

employee cannot be more than 200.

INTRODUCTION TO CAPITAL MARKET

Capital market may be defined as a market of borrowings and lending

long term capital funds required by business firms. Capital market is the

market for financial assets that have long or indefinite maturity. In other

words it refers to all the facilities and the institutional arrangements for

borrowings and lending medium term and long term funds.

44

The capital market is dealing with various financial instruments that

are used for raising capital resources in capital market are known as capital

market instruments.

The various capital market instruments used by corporate entities in India

for raising resources are as following:-

Preference shares:-

Shares that carry preferrencial rights in comparison with ordinary shares are

called preference shares. Preferential rights regarding payment of dividends

and the distributions of the assets of the company in the events of its

winding up in preference to equity shares.

There are six types of preference shares, which are as follows,

a) Cumulative preference shares

b) Non cumulative preference shares

c) Participating preference shares

d) Redeemable preference shares

e) Fully convertible cumulative preference shares

f) Preference share with warrants attached.

45

Equity shares:

Equity share, also known as ordinary shares are the shares held by the

corporate intity. Since equity shareholders face greater risk and have no

specific preferencial rights. They are given larger shares in profit through

higher dividend then those given to preference share holders that the

company’s performance is excellent. Directors declare no dividends in case

there are no profits in subsequent year. Equity shareholders also enjoy the

benefit of ploughing back of undistributed profits kept as reserve and

surplus for the purpose of business expansion. Often part of these is

distributed to them as bonus shares. Such bonus shares are entitled to a

proportionate or full dividend in the succeeding year.

Debentures and bonds:

A document that either creates a debt of acknowledges it is known as

debentures. Accordingly, any documents that fulfill either of this condition

is a debenture. A debenture, issued under the common seal of the company

usually takes the form of certificate that acknowledges in debt ness of the

company.

46

Importance of capital market

Absence of capital market serves as deterrent factor to capital

formation and economic growth. Resources would remain idle if finances

are not funneled through capital market.

It serves as an important sourse for the productive use of the economy’s

savings.

It provides incentives to saving and facilitates capital formation by offering

suitable rates of interest as the price of the capital.

It provides avenue for investors to invest in financial assets.

It facilitates increase in production and productivity in the economy and

thus enhances the economic welfare of the society.

A healthy market consisting of expert intermediaries promotes stability in

the value of securities representing capital funds.

It serves as an important source for technological up gradation in the

industrial sector by utilizing the funds invested by the public.

Primary market reforms:

Entry barrier for unlisted companies modified as dividend payment in

immediately preceding 3 years.

47

A listed company required to meet the entry norm only if the post issue net

worth becomes morethan five times the pre-issue net worth.

Companies required making their partly paid-up shares fully paid up of

forfeiting the same, before making a public/right issue.

Unlisted company allowed to freely price its securities provided it has

shown net profit in the immediately preceding 3 years subject to its

fulfilling the exisiting disclosure requirements.

The promoter’s contribution for public issues made at 20% irrespective of

the issue size.

Written consent from share holders in regard to lock-in made compulsory

for securities to be offered for promoter’s contribution.

Appointment of registrar to an issue for rights issues made mandatory.

A provision made regarding disclosure of the share holding of the

promoters whose names figure in the paragraph on “promoters and their

background” in the offer document.

The SEBI (Registrars to an Issue and share Transfer Agents ) Rules and

Regulations 1993 have been amended to provide for an arm’s length

relationship between the issuer and the registrars to the issue. It has now

been stipulated that no Registrar to an Issue can act as such for any issue of

48

securities made by any body corporate, if the Registrar to the issue and the

Issuer Company are associates.

With a view to facilitating rising of funds by infrastructure projects, SEBI

has allowed debt instruments ot be listed on the Stock Exchanges without

prior listing of equity. Corporate with infrastructure projects and Municipal

Corporations to be exempted from the requirements of Rule 19(2b) of

securities (contract) Regulation rules to facilitate public offer and listing of

its pure debt instruments as well as debt instruments fully or partly

convertible in to equity without the requirement of prior listing of equity but

subject to conditions like investments grade ratings.

Only body corporate to be allowed to function as Merchant Bankers

Multiple categories of merchant bankers to abolished and there shall be only

one entity viz., merchant banker, presentl, the Merchant Banker allowed to

perform underwriting activity but required to seek separate registration to

function as a portfolio manager under SEBI (portfolio manager ) Rules and

Regulations, 1993.

49

Chapter 2

Research methodology

50

RESEARCH METHODOLOGY AND DESIGN

STATEMENT OF THE PROBLEM:

There is much hype of IPOs nowadays. And while considering the

previous years, the number of companies which going for IPO is increased

during 2010. There are common phenomenons among the investors today

that the return on investing in IPO is not much. Event though investor has

the storm back the IPO and yearly there are huge application received from

the investor to invest in IPO. And we also heared about that the “coal India”

IPO, etc. so now the trend is changing.

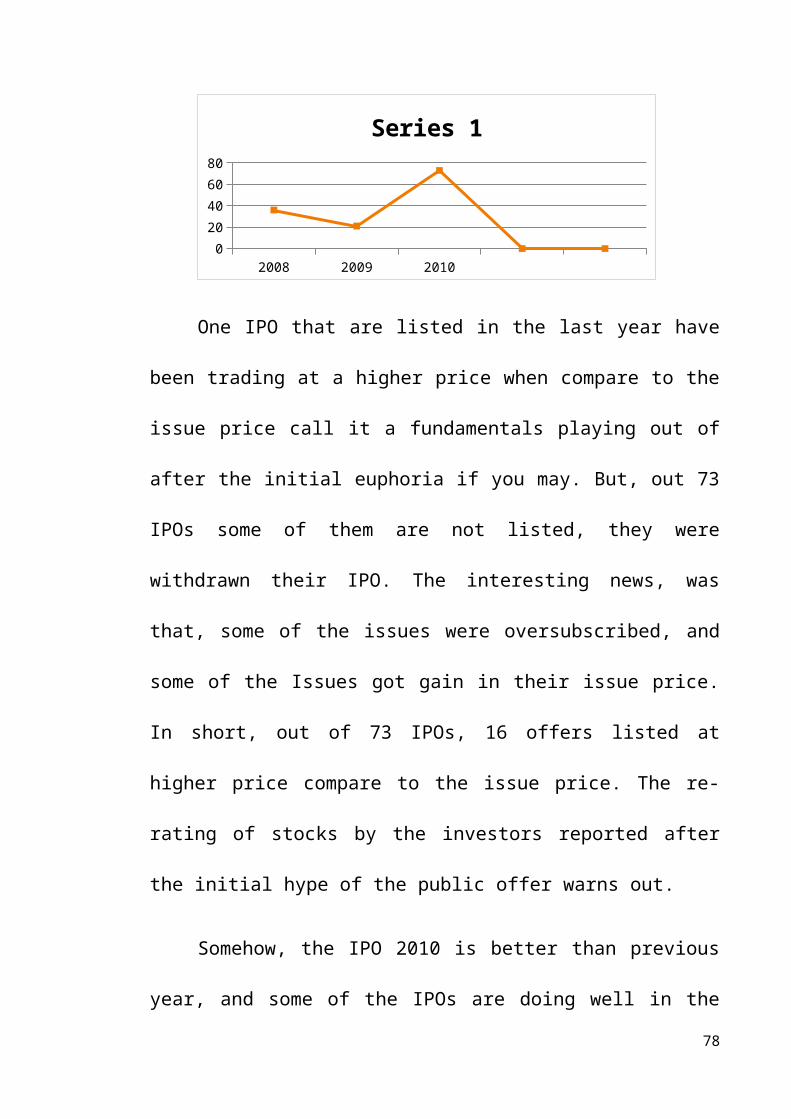

Concider following graph:

2008 2009 20100

20

40

60

80

Series 1

One IPO that are listed in the last year have been trading at a higher

price when compare to the issue price call it a fundamentals playing out of

after the initial euphoria if you may. But, out 73 IPOs some of them are not

listed, they were withdrawn their IPO. The interesting news, was that, some

of the issues were oversubscribed, and some of the Issues got gain in their

51

issue price. In short, out of 73 IPOs, 16 offers listed at higher price compare

to the issue price. The re-rating of stocks by the investors reported after the

initial hype of the public offer warns out.

Somehow, the IPO 2010 is better than previous year, and some of the

IPOs are doing well in the market even after the global crisis. There are

some IPOs whose trade price and the issue price differs significantly. Some

investors are getting more money and some are loosing. The most of IPOs

issued during the year 2010 are traded at the lower prices than their issue

price. So there is a need to know the performance of the IPO. This is the

study to know the performance of the IPO that are issued during the year

2010. The problem here is to know which IPO is doing well and which are

not.

However this study has taken up for the purpose to know:-

The IPO issued during the year 2010

The performance of the IPO during the year.

The investor’s information of the IPO during the year 2010

The economical impact on IPO due to the Market condition.

52

JUSTIFICATION OF THE STUDY:-

The study highlights the performance of the IPO dusing the year

2010. It also deals the future prospects of IPO. It also reviews the

performance of different sector.

OBJECTIVES OF THE STUDY:

The objectives of the study is to know that

Study of the IPO issued during the year 2010

Study the overall performance of the IPO during the year 2010

Comparison of the issue price and the trade price in particular day.

The future prospect of IPO

Types of research

the research includes different options. They are,

1. Explorative Observational research

Fresh data can be gathered by observing the relevant actors and

settings. Under theis method the information is sought by way of

investigatos’s own direst observation withour asking from the respondents,

instead of asking for the brand of wrist watch used by the respondent, may

himself look at the watch the main advantage of this method is subjective

bias is eliminated, if the observation is done accurately. Secondly

53

information obtained under this method related to what is currently

happening. It is not complicated either by past behaviours or future

intentions or attitudes. Thirdly, this mwthod is independent of reposdent’s

willingness to respond and as such is relatively less demanding of active

cooperation on the part of respondents. This method is particularly suitable

in studies which particularly deal with subjects who are not capble of giving

verbal reports of their feelings for one reason or the other.

2. Focus group research.

A focus group is a gathering of six to ten people who are invited to

spend a few hours with a skilled moderator to discuss a product, service,

organization, or other marketing entity. The moderator needs to be

objective, knowledgible on the issue and skilled in group dynamics.

Participants are normally paid a small sum for attending. The meeting is

typically held in pleasant surroundings and refreshments are served.

3. Survey research.

Surveys are best suited for descriptive research. Companies undertake

surveys to learn about people’s knowledge, beliefs, preferances, and

satisfaction, and to measure these magnitudes in the general population. A

company such as Mainstay might prepare its own survey instrument to

gather information it needs, or it might add questions to an omnibus survey

that carries the questions of several companies at much lower cost.

54

4. Experimental research.

The most scientifically valid research is experimental research. The

pupose of experimental research is to capture cause and effect relationships

by eliminating competing explanations of the observes findings to the

extent that the design and execution of the experiment eliminate alternative

hypothesis that might explain the results, research and HR managers can

have confidence in the conclusions. It calls for selecting matched groups of

subjects, subjecting them to different treatments, controlling extraneous

variable, and checking whether observed response differences are

satisfically significan. To ehte extent that extraneous factors are eliminated

of controlled, the observed effects can be related to variation in the

treatments.

Adopted Research Design:-

The research design that is adopted is both explanatory and

experimental research design.

The advantage behind adopting the explorative method is that is helps

on identifying the problems and is finding out the alternative solution to the

problem as herein referred to the effectiveness of the recruitment

campaign.

55

The reason being it is also an experimental study is that is is the

testing of the attitude towards the hypothesis proposed and it is variable as

well as a study of the existing system.

Collection of Data:-

The data required for the study were obtained from,

1. Primary data

2. Secondary data.

The primary data are those data which are collected for the first time.

The primary data was collected through discussions and interviewing wit

some financial experts and bank officers. It includes the eminent

personalities dealing with IPO and some bank expert.

The secondary data and other related information published reports of

corporations like…

Websites

RBI Guidelines

SEBI Guidelines

Newspapers : Economic times, Business lines, Business standards

Text books

Business journals: Dalal street, capital market, ICFAI journals, etc.

56

Tools of Analysis:-

The tools which are used for this study are:

The interviews and discussions has been done with some financia

experts, and share brokers to know the performance of the IPO during the

year 2010.

This research study has been conducted by collecting the secondary

data from various sources like RBI bulletin, Websites, Business journals,

etc. about the FDIand interpreting the same with reference to the year 2010.

Sampling Plan :-

Sampling may be defined as the selection of some part of an

aggregate or totality on basis of which judgement or inference about the

aggregate or totality is made. A sample design is a definite plan for

obtaining a sample from a given population. It refers to a technique or the

procedure the researcher would adopt in selecting the items for the sample.

Since it is a research kind of study about performance of the ipo

issued during the year, 2010, I have taken the sample as the total of

population. I have taken all the 73 IPOs that are issued during the year

2010.

ANALYSIS OF DATA

57

Analysis of data has been done,

By taking all the IPO that are issued during the year 2010.

By taking the issue price of the data that are issued during the year 2010.

By taking the trade price pertaining to a particular day.

By comparing the gain or loss during the year 2010.

By relating the data to know which sectors IPO are doing well and how the trade price are changing significantly from the issue price.

Limitation of the study

For this study collecting of primary data with regards to the IPOs is very difficult. Getting the full fledged data on this topic is quite impossible.

The study contains most of the secondary data and analysis of the same.

The study has been taken to the performance of the IPO during the year 2010

It only judge the performance of the IPO based on the issue price and trade price. But there are so many reasons for the success of IPO.

It has not dealt with the cause behind on company is getting the huge success whether other suffers.

It does not deal with the speculation in the capital market.

58

Chapter 3

COMPANY PROFILE

59

KARVY Stock Broking Limited, one of the cornerstones of the

KARVY edifice, flows freely towards attaining diverse goals of the

customer through varied services. It creates a plethora of opportunities for

the customer by opening up investment vistas backed by research-based

advisory services. Here, growth knows no limits and success recognizes no

boundaries. Helping the customer create waves in his portfolio and

empowering the investor completely is the ultimate goal. KARVY Stock

Broking Limited is a member of: 1) National Stock Exchange (NSE) , 2)

Bombay Stock Exchange (BSE).

Member-National Stock Exchange and The Bombay Stock

Exchange .

Karvy Stock Broking Limited, one of the cornerstones of the Karvy

edifice, flows freely towards attaining diverse goals of the customer through

varied services. Creating a plethora of opportunities for the customer by

opening up investment vistas backed by research-based advisory services.

Here, growth knows no limits and success recognizes no boundaries.

Helping the customer create waves in his portfolio and empowering the

investor completely is the ultimate goal.

60

Stock Broking Services

They offer services that are beyond just a medium for buying and selling stocks

and shares. Instead we provide services which are multi dimensional and multi-focused

in their scope. There are several advantages in utilizing our Stock Broking services,

which are the reasons why it is one of the best in the country.

They offer trading on a vast platform ; National Stock Exchange and Bombay

Stock Exchange. More importantly, they make trading safe to the maximum possible

extent, by accounting for several risk factors and planning accordingly. They are

assisted in this task by our in-depth research, constant feedback and sound advisory

facilities. Their highly skilled research team, comprising of technical analysts as well as

fundamental specialists, secure result-oriented information on market trends, market

analysis and market predictions. This crucial information is given as a constant feedback

to our customers, through daily reports delivered thrice daily ; The Pre-session Report,

where market scenario for the day is predicted, The Mid-session Report, timed to arrive

during lunch break , where the market forecast for the rest of the day is given and The

Post-session Report, the final report for the day, where the market and the report itself is

reviewed. To add to this repository of information, we publish a monthly magazine

“Karvy ; The Finapolis”, which analyzes the latest stock market trends

and takes a close look at the various investment options, and products available in the

market, while a weekly report, called “ Karvy Bazaar Baatein”, keeps you

more informed on the immediate trends in the stock market. In addition, our specific

industry reports give comprehensive information on various industries. Besides this, we

also offer special portfolio analysis packages that provide daily technical advice on

61

scrips for successful portfolio management and provide customized advisory services to

help you make the right financial moves that are specifically suited to your portfolio.

In the future, our focus will be on the emerging businesses and to meet this objective, we

have enhanced our manpower and revitalized our knowledge base with enhances focus

on Futures and Options as well as the commodities business.

depository services

The onset of the technology revolution in financial services Industry saw the

emergence of Karvy as an electronic custodian registered with National Securities

Depository Ltd (NSDL) and Central Securities Depository Ltd (CSDL) in 1998.

Karvy set standards enabling further comfort to the investor by promoting paperless

trading across the country and emerged as the top 3 Depository Participants in the

country in terms of customer serviced.

Offering a wide trading platform with a dual membership at both NSDL and

CDSL, we are a powerful medium for trading and settlement of dematerialized shares.

We have established live DPMs, Internet access to accounts and an easier transaction

process in order to offer more convenience to individual and corporate investors. A team

of professional and the latest technological expertise allocated exclusively to our demat

division including technological enhancements like SPEED-e, make our response time

quick and our delivery impeccable. A wide national network makes our efficiencies

accessible to all.

62

Distribution of Financial Products

The paradigm shift from pure selling to knowledge based selling drives the

business today. With our wide portfolio offerings, we occupy all segments in the retail

financial services industry.

A 1600 team of highly qualified and dedicated professionals drawn from the best

of academic and professional backgrounds are committed to maintaining high levels of

client service delivery. This has propelled us to a position among the top distributors for

equity and debt issues with an estimated market share of 15% in terms of applications

mobilized, besides being established as the leading procurer in all public issues.

To further tap the immense growth potential in the capital markets we enhanced

the scope of our retail brand, Karvy – the Finapolis , thereby providing planning and

advisory services to the mass affluent. Here we understand the customer needs and

lifestyle in the context of present earnings and provide adequate advisory services that

will necessarily help in creating wealth. Judicious planning that is customized to meet

the future needs of the customer deliver a service that is exemplary. The market-savvy

and the ignorant investors, both find this service very satisfactory. The edge that we have

over competition is our portfolio of offerings and our professional expertise. The

investment planning for each customer is done with an unbiased attitude so that the

service is truly customized.

Our monthly magazine, Fin polis, provides up-dated market information on

market trends, investment options, opinions etc. Thus empowering the investor to base

every financial move on rational thought and prudent analysis and embark on the path to

63

wealth creation.

Advisory service

Under our retail brand ‘Karvy – the Finapolis', we deliver advisory services to a

cross-section of customers. The service is backed by a team of dedicated and expert

professionals with varied experience and background in handling investment portfolios.

They are continually engaged in designing the right investment portfolio for each

customer according to individual needs and budget considerations with a comprehensive

support system that focuses on trading customers' portfolios and providing valuable

inputs, monitoring and managing the portfolio through varied technological initiatives.

This is made possible by the expertise we have gained in the business over the years.

Another venture towards being investor-friendly is the circulation of a monthly

magazine called ‘Karvy - the Finapolis'. Covering the latest of market news, trends,

investment schemes and research-based opinions from experts in various financial

fields .

Private client group

This specialized division was set up to cater to the high net worth individuals and

institutional clients keeping in mind that they require a different kind of financial

planning and management that will augment not just existing finances but their life-style

as well. Here we follow a hard-nosed business approach with the soft touch of dedicated

customer care and personalized attention.

64

For this purpose we offer a comprehensive and personalized service that

encompasses planning and protection of finances, planning of business needs and

retirement needs and a host of other services, all provided on a one-to-one basis.

Our research reports have been widely appreciated by this segment. The delivery and support

modules have been fine tuned by giving our clients access to online portfolio information,

constant updates on their portfolios as well as value-added advise on portfolio churning, sector

switches etc. The investment recommendations given by our research team in the cash market

has enjoyed a high success rate .

KARVY CONSULTANT LTD.

As the flagship company of the Karvy Group, Karvy Consultants

Limited has always remained at the helm of organizational affairs,

pioneering business policies, work ethic and channels of progress. Having

emerged as a leader in the registry business, the first of the businesses that

we ventured into, we have now transferred this business into a joint venture

with Computershare Limited of Australia, the world’s largest registrar. With

the advent of depositories in the Indian capital market and the relationships

that we have created in the registry business, we believe that we were best

positioned to venture into this activity as a Depository Participant. We were

one of the early entrants registered as Depository Participant with NSDL

(National Securities Depository Limited), the first Depository in the country

and then with CDSL (Central Depository Services Limited). Today, we

service over 6 lakhs customer accounts in this business spread across over

65

250 cities/towns in India and are ranked amongst the largest Depository

Participants in the country. With a growing secondary market presence, we

have transferred this business to Karvy Stock Broking Limited (KSBL), our

associate and a member of

BSE NSE and HSE.

66

Chapter 4

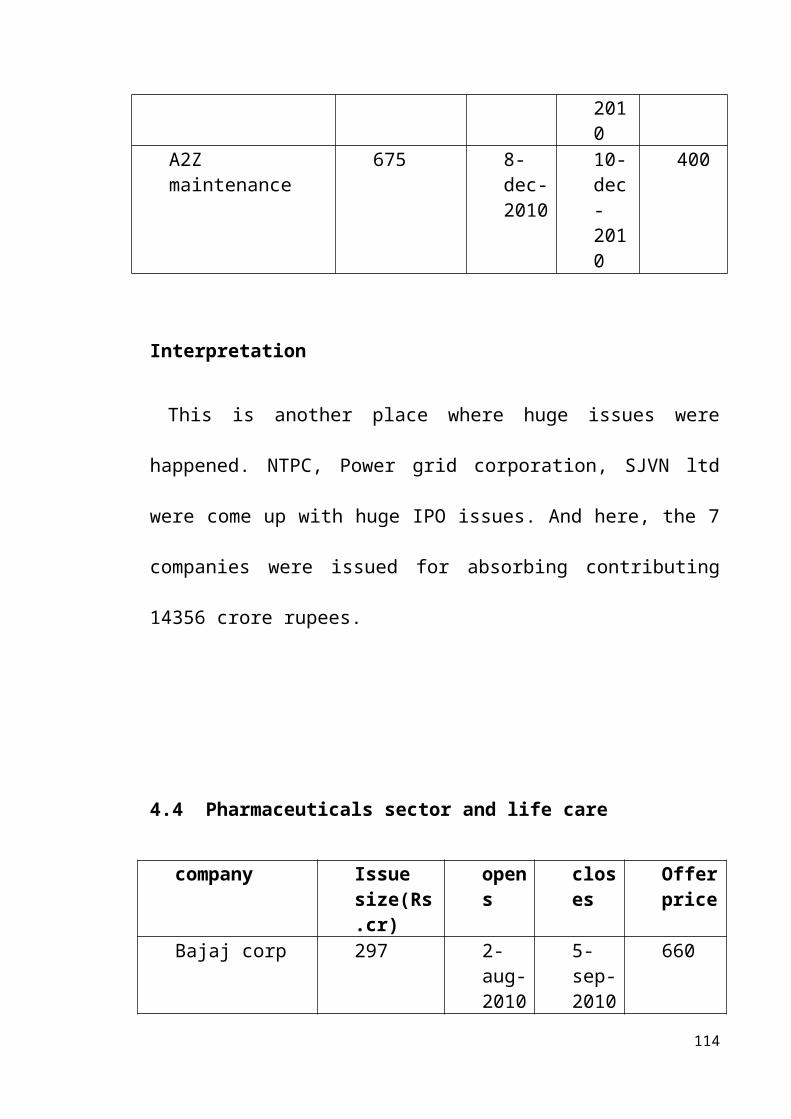

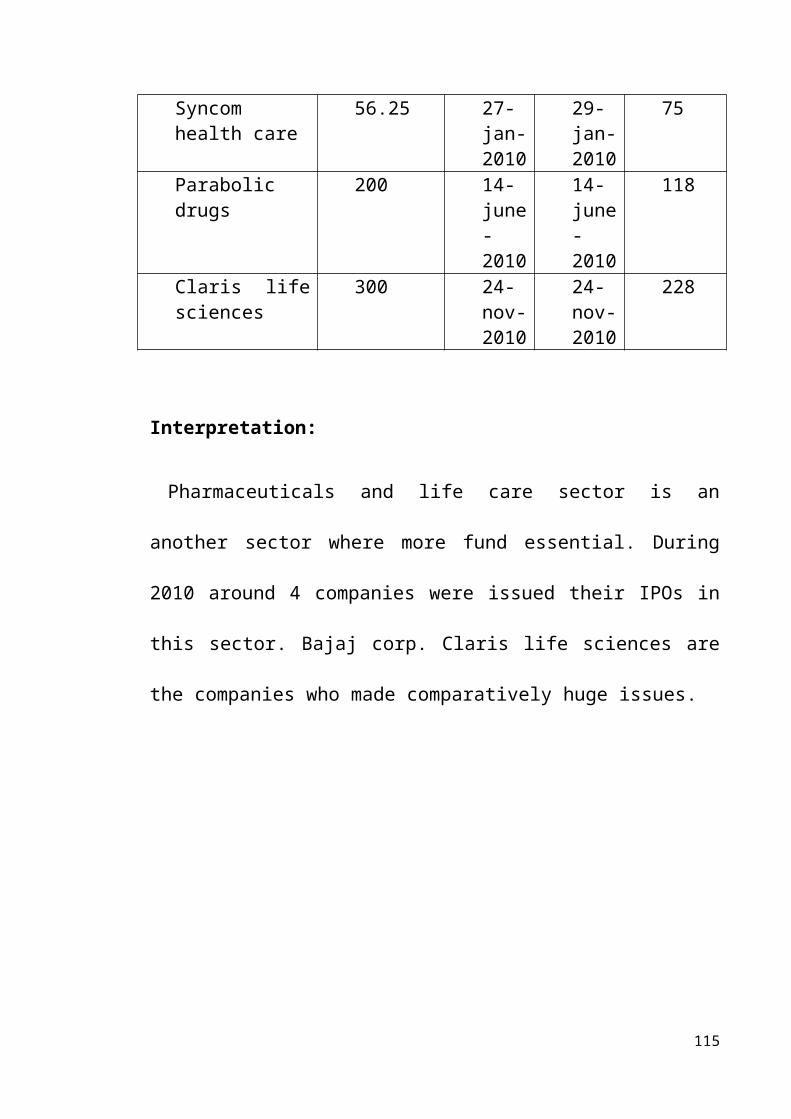

LIST OF IPO ISSUED DURING THE YEAR

2010

67

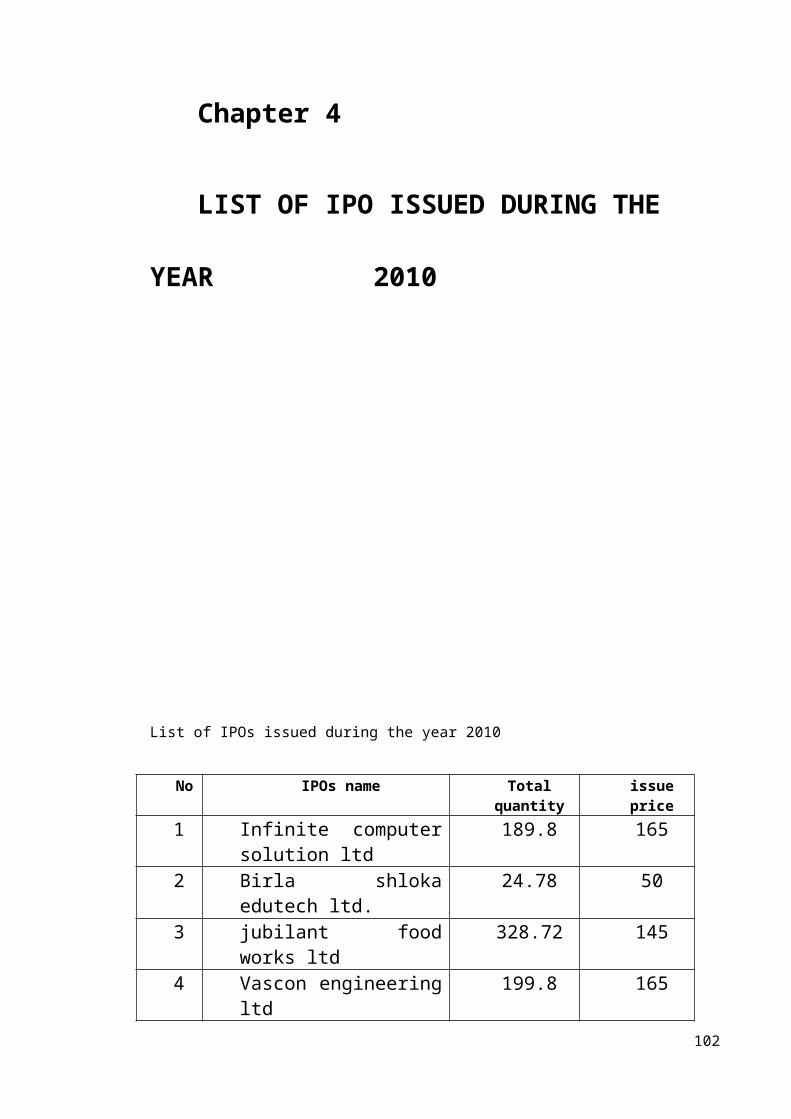

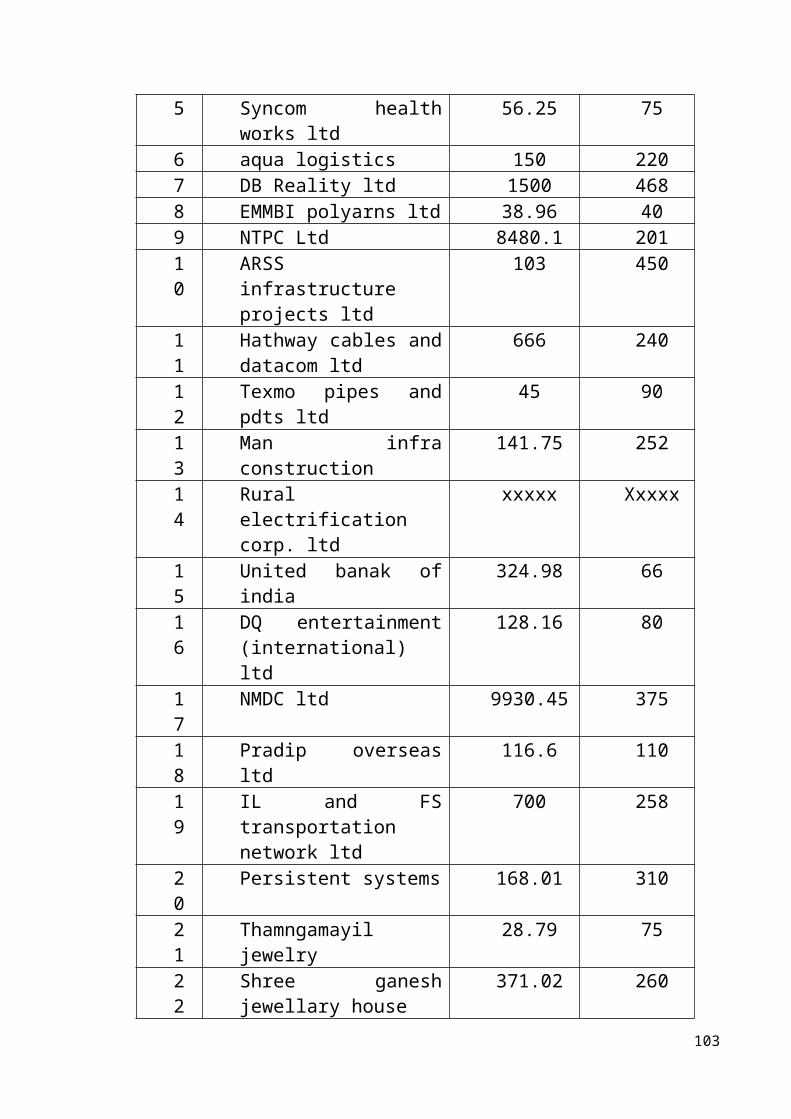

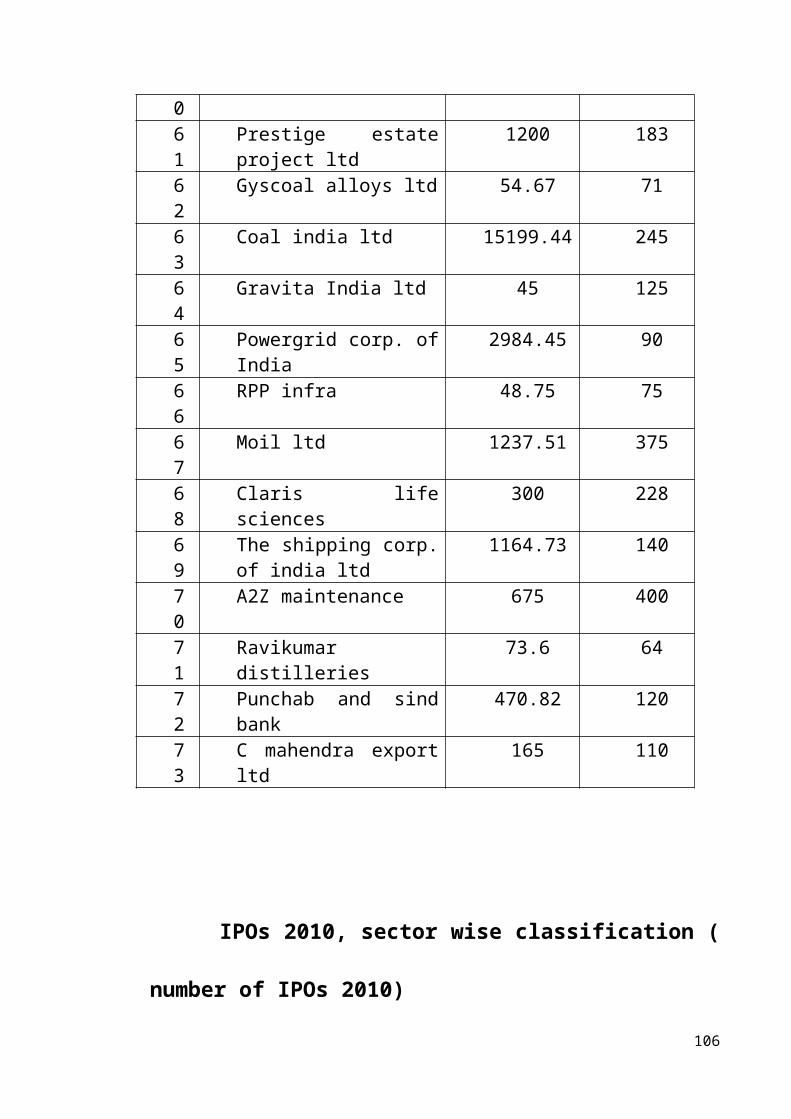

List of IPOs issued during the year 2010

No IPOs name Total quantity issue price

1 Infinite computer solution ltd

189.8 165

2 Birla shloka edutech ltd. 24.78 503 jubilant food works ltd 328.72 1454 Vascon engineering ltd 199.8 1655 Syncom health works ltd 56.25 756 aqua logistics 150 2207 DB Reality ltd 1500 4688 EMMBI polyarns ltd 38.96 409 NTPC Ltd 8480.1 20110 ARSS infrastructure

projects ltd103 450

11 Hathway cables and datacom ltd

666 240

12 Texmo pipes and pdts ltd 45 9013 Man infra construction 141.75 25214 Rural electrification corp.

ltdxxxxx Xxxxx

15 United banak of india 324.98 6616 DQ entertainment

(international) ltd128.16 80

17 NMDC ltd 9930.45 37518 Pradip overseas ltd 116.6 11019 IL and FS transportation

network ltd700 258

20 Persistent systems 168.01 31021 Thamngamayil jewelry 28.79 7522 Shree ganesh jewellary

house371.02 260

23 Infrasoft technologies ltd 53.65 14524 Goenka diamond and

jewels126.51 135

25 Talwalkers better value fitness ltd

77.44 128

25 Nitesh estates ltd 450 5426 Tarapur transformers ltd 63.75 75

68

27 Mandhana industries ltd 107.9 13028 SJVN ltd 1064.74 2629 Jaypee infratech ltd 1650 10230 Tara health food ltd xxxxx Xxxxxx32 Standard chartered plc 2486.35 10433 Fatpipe network india ltd xxxxx Xxxxx34 Parabolic drugs ltd 200 11835 Aster silicates ltd 53.10 11836 Technofab engineers ltd 71.66 24037 Hindustan media venture

ltd270 166

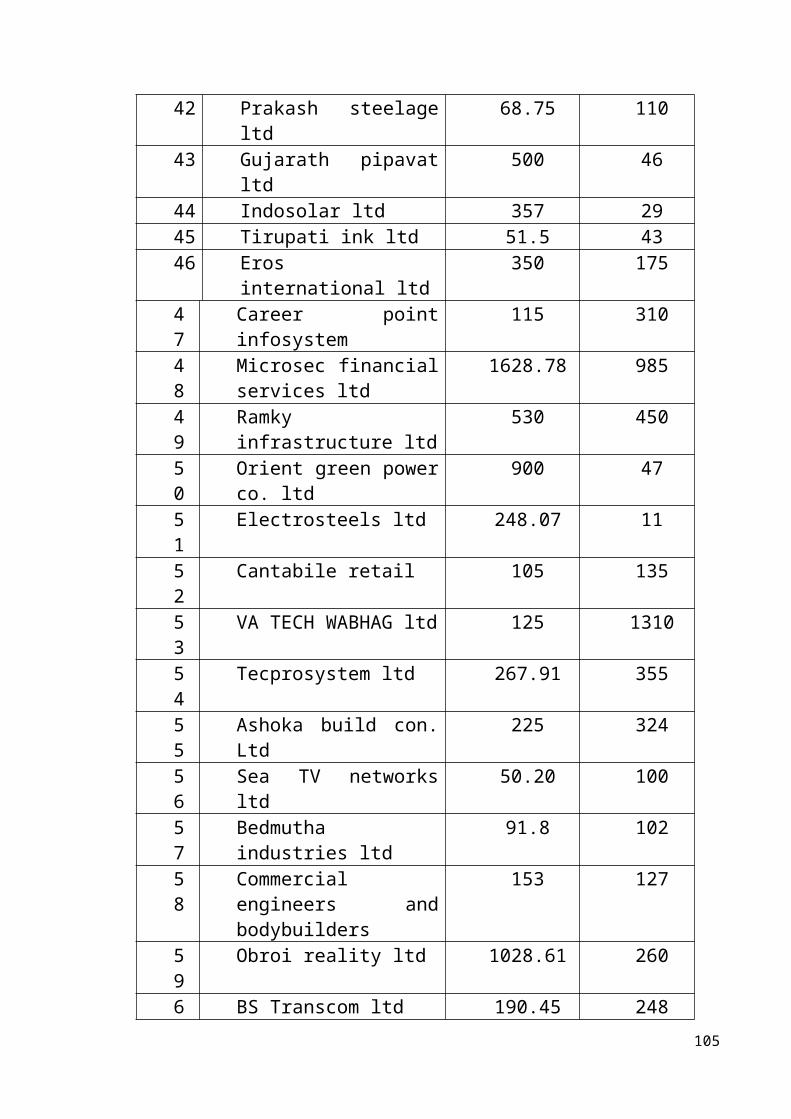

38 Midfield industries ltd 59.85 13339 Engineers india ltd 959.65 29040 SKS micro fin ltd 1628.78 98541 Bajaj corp. ltd 297 66042 Prakash steelage ltd 68.75 11043 Gujarath pipavat ltd 500 4644 Indosolar ltd 357 2945 Tirupati ink ltd 51.5 4346 Eros international ltd 350 17547

Career point infosystem 115 310

48

Microsec financial services ltd

1628.78 985

49

Ramky infrastructure ltd 530 450

50

Orient green power co. ltd 900 47

51

Electrosteels ltd 248.07 11

52

Cantabile retail 105 135

53

VA TECH WABHAG ltd 125 1310

54

Tecprosystem ltd 267.91 355

55

Ashoka build con. Ltd 225 324

56

Sea TV networks ltd 50.20 100

57

Bedmutha industries ltd 91.8 102

69

58

Commercial engineers and bodybuilders

153 127

59

Obroi reality ltd 1028.61 260

60

BS Transcom ltd 190.45 248

61

Prestige estate project ltd 1200 183

62

Gyscoal alloys ltd 54.67 71

63

Coal india ltd 15199.44 245

64

Gravita India ltd 45 125

65

Powergrid corp. of India 2984.45 90

66

RPP infra 48.75 75

67

Moil ltd 1237.51 375

68

Claris life sciences 300 228

69

The shipping corp. of india ltd

1164.73 140

70

A2Z maintenance 675 400

71

Ravikumar distilleries 73.6 64

72

Punchab and sind bank 470.82 120

73

C mahendra export ltd 165 110

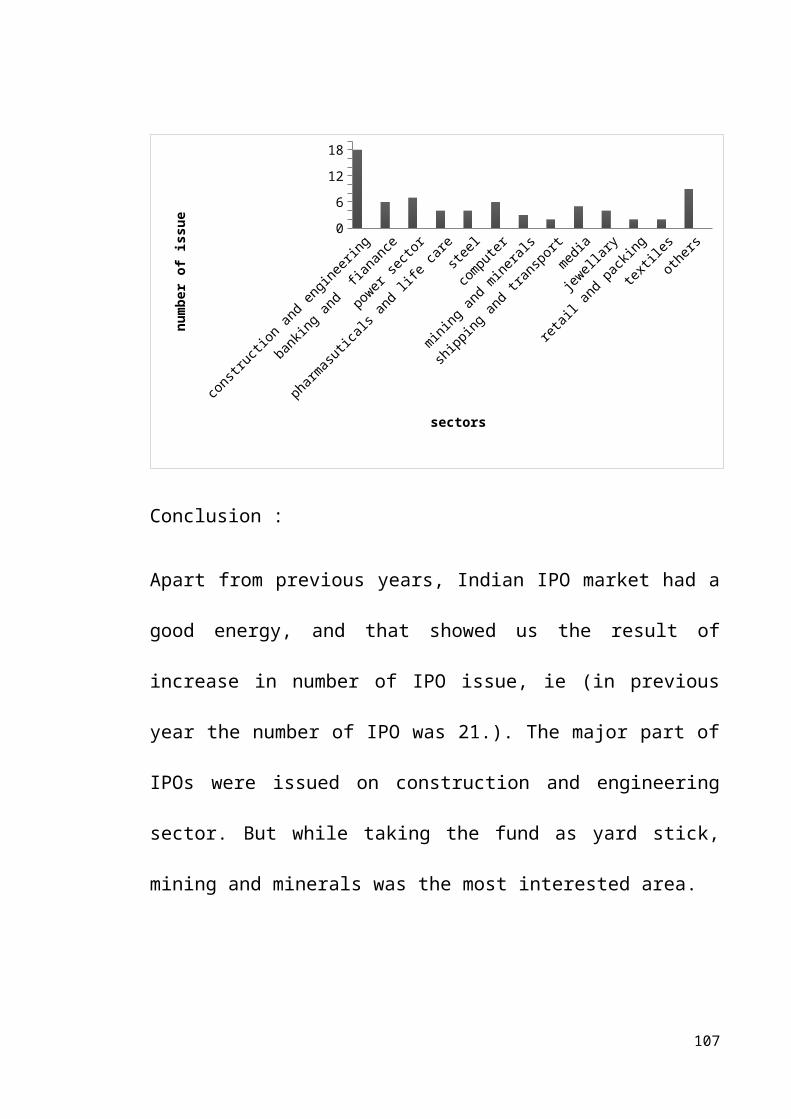

IPOs 2010, sector wise classification ( number of IPOs 2010)

70

constr

uction an

d engin

eerin

g

bankin

g and fi

anan

ce

power sec

tor

pharmasu

ticals a

nd life c

are steel

computer

mining and m

inerals

shipping a

nd tran

sport

media

jewell

ary

retail

and pack

ing

textiles

others02468

101214161820

sectors

num

ber o

f iss

ue

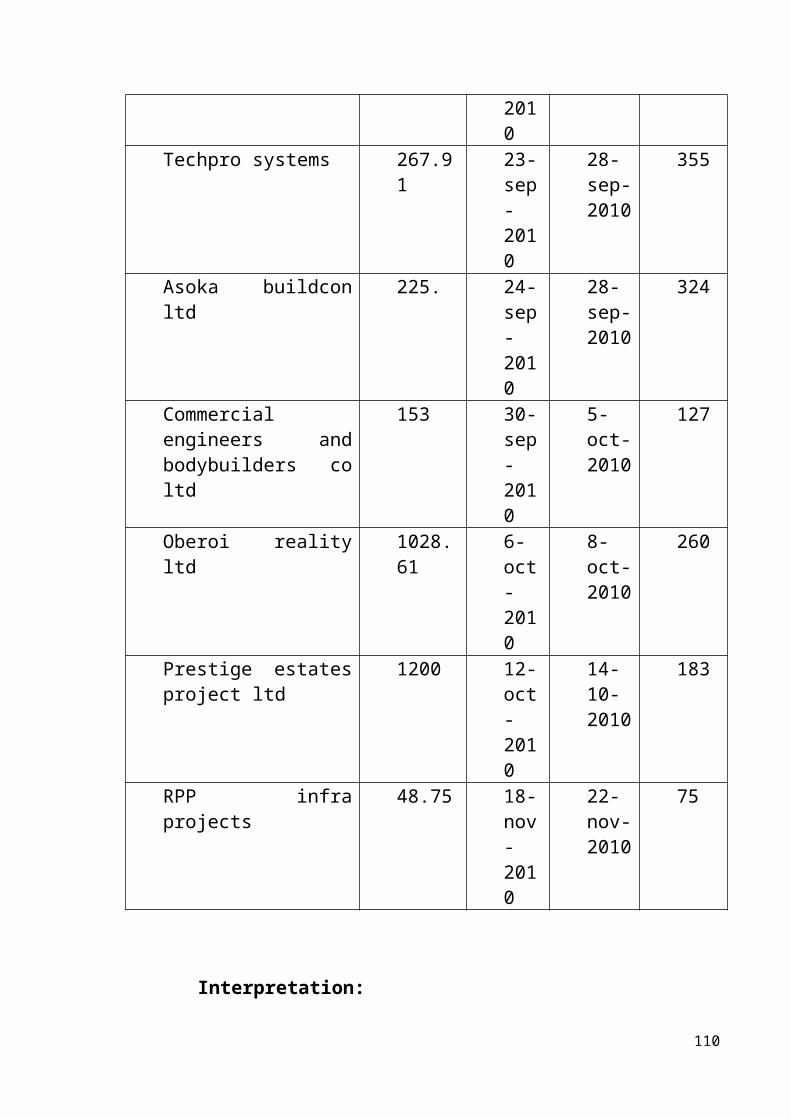

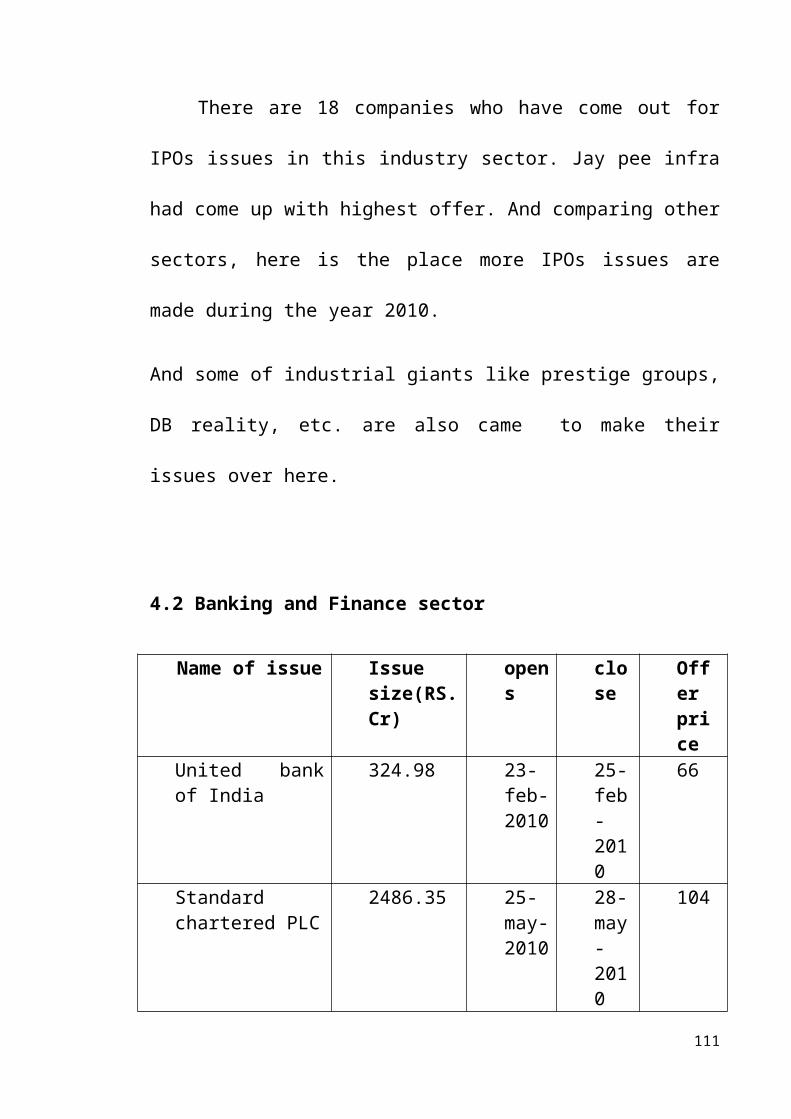

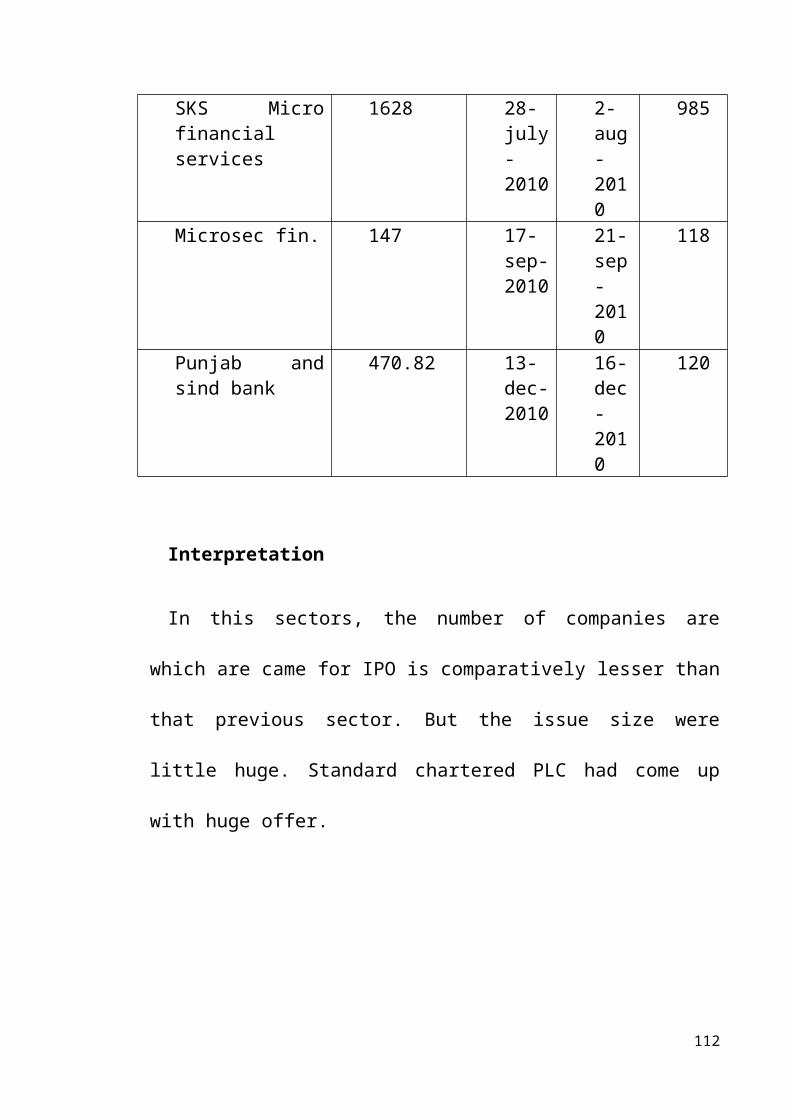

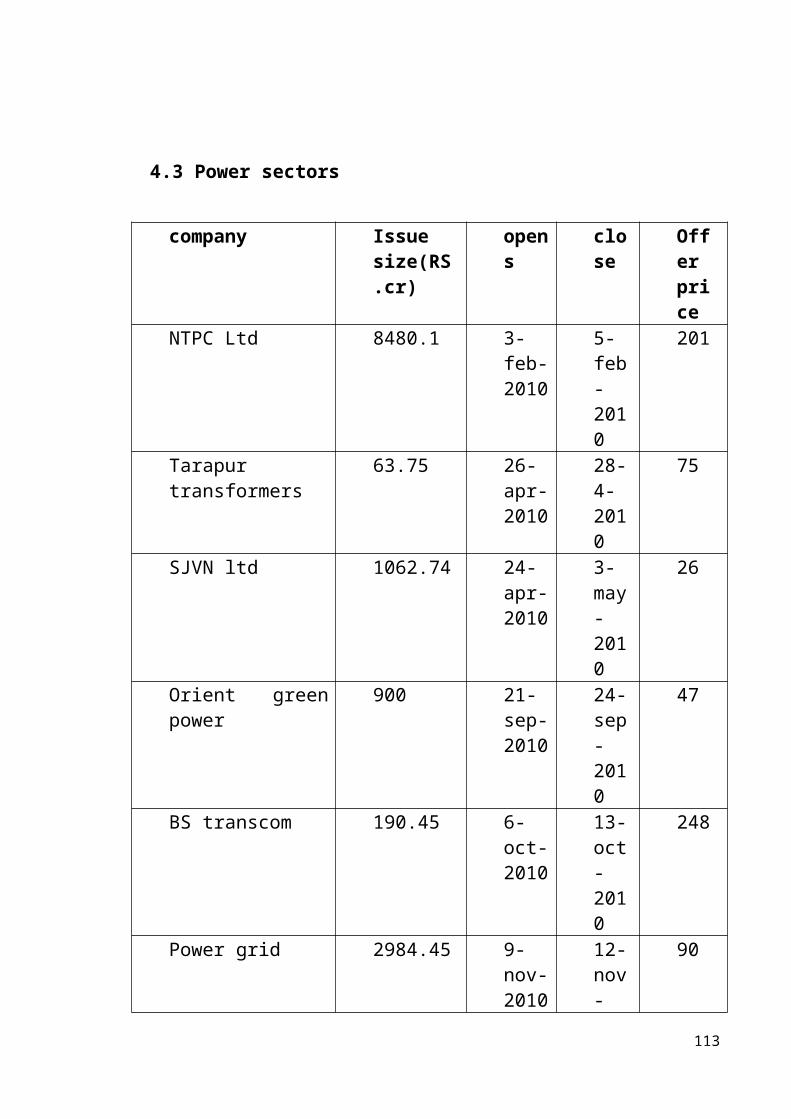

Conclusion :

Apart from previous years, Indian IPO market had a good energy, and that

showed us the result of increase in number of IPO issue, ie (in previous year

the number of IPO was 21.). The major part of IPOs were issued on

construction and engineering sector. But while taking the fund as yard stick,

mining and minerals was the most interested area.

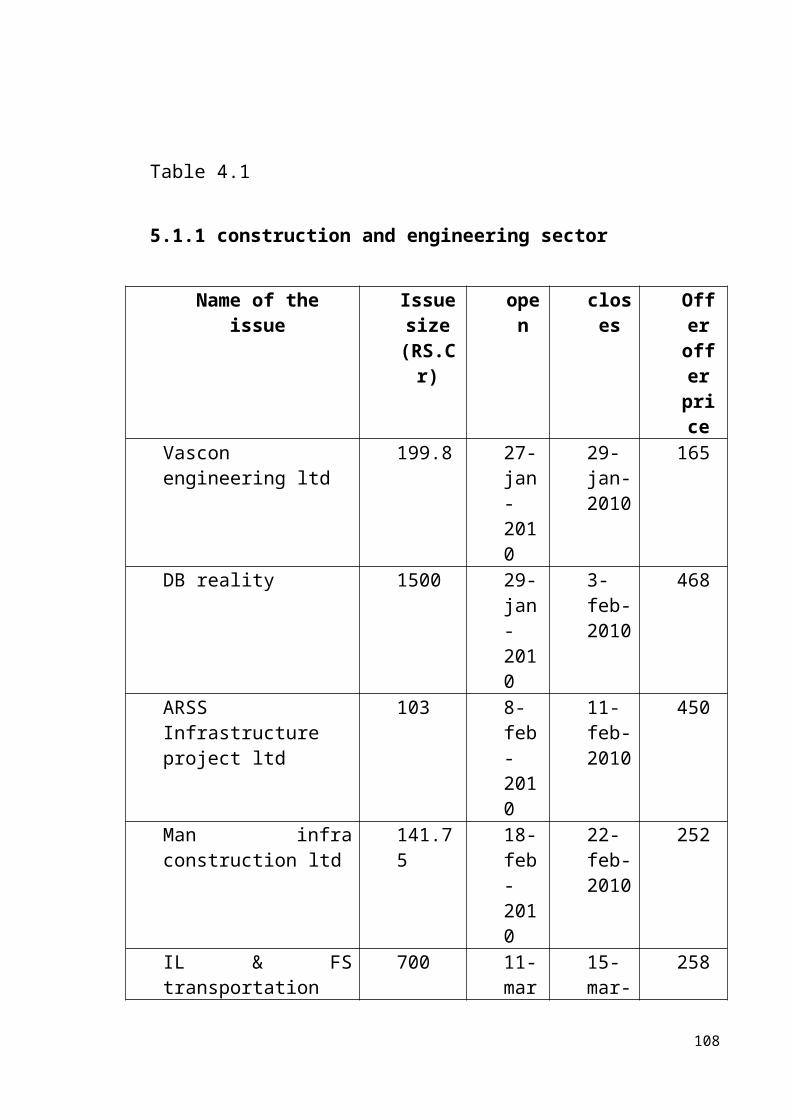

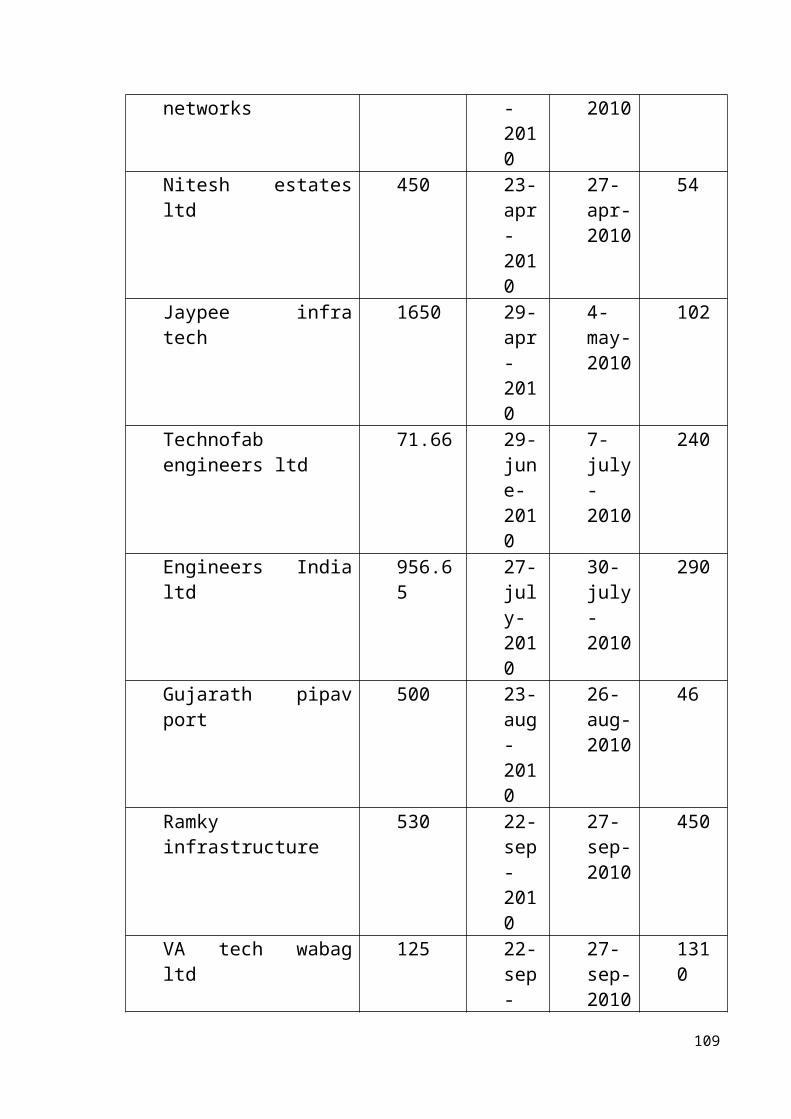

Table 4.1

5.1.1 construction and engineering sector

71

Name of the issue Issue size

(RS.Cr)

open closes Offer offer price

Vascon engineering ltd 199.8 27-jan-2010

29-jan-2010

165

DB reality 1500 29- jan-2010

3-feb-2010

468

ARSS Infrastructure project ltd

103 8-feb-2010

11-feb-2010

450

Man infra construction ltd

141.75 18-feb-2010

22-feb-2010

252

IL & FS transportation networks

700 11-mar-2010

15-mar-2010

258

Nitesh estates ltd 450 23-apr-2010

27-apr-2010

54

Jaypee infra tech 1650 29-apr-2010

4-may-2010

102

Technofab engineers ltd 71.66 29-june-2010

7-july-2010

240

Engineers India ltd 956.65 27-july-2010

30-july-2010

290

Gujarath pipav port 500 23-aug-2010

26-aug-2010

46