Irish League of Credit Unions Foundation

EU ACP Microfinance

West African Credit Unions Programme Against Poverty (WACUPP)

Mid-Term Review

Dean Mahon

June 2014

ii

Acronyms ACCOSCA African Confederation of Cooperative Savings and Credit

Associations ACP Africa, the Caribbean and the Pacific CBL Central Bank of Liberia CCA Canadian Cooperative Association CDA Cooperative Development Agency (Liberia) CSA Credit and Savings Association CU Credit Union CUA Credit Union Association (Ghana) CUTRAC Credit Union Training Center (Ghana) EU European Union GAMFINET Gambia Microfinance Network GH₵ Ghanaian cedi GMF Graduation Microfinance IGA Income Generating Activity ILCUF Irish League of Credit Unions Foundation KM Knowledge Management LCUNA Liberia Credit Union National Association MF Microfinance MFI Microfinance Institution MIS Management Information Systems MTR Mid-Term Review NACCUA National Cooperative Credit Union Association (Sierra Leone) NACCUG National Association of Cooperative Credit Unions of the

Gambia NGO Non-Governmental Organisation OSS Operational Self-Sufficiency PI Poverty Index SBFIC Savings Bank Foundation for International Cooperation

(Germany) SEND Social Enterprise Development Foundation SPM Social Performance Management UCC University of Cape Coast UNCDF United Nations Capital Development Fund VC Value Chain VCF Value Chain Financing VSLA Village Savings and Loan Association WACUPP West Africa Credit Unions against Poverty Programme WOCCU World Council of Credit Unions

iii

Table of Contents Acronyms i

I. Executive Summary 1

A. Principal Findings

B. Conclusions

C. Lessons Learned

II. Introduction 3

A. Purpose

B. By whom and how the document will be used

C. Review criteria

D. Principle questions

E. Methodology used

III. Project Background 5

IV. Comparative country movement key areas 6

A. Minimum share value

B. Representational structure

C. Legislation

D. Regulation/Supervision

E. Taxation

F. Recommendations

V. Country Movements 7

A. The Gambia

B. Ghana

C. Liberia

D. Sierra Leone

VI. Project themes 17

A. Graduation microfinance

B. Value chain

C. Social performance management

D. Knowledge management

VII. Project Implementation Review 23

A. Effectiveness

B. Efficiency

C. Relevance

D. Sustainability

VIII. Alternative Approaches and Strategies 30

IX. Recommendations 30

iv

Appendices

Appendix 1 List of Persons Met 35

Appendix 2 Trip Report 37

1

I. Executive Summary

A. Principal Findings

WACUPP has provided clear evidence that cross-country cooperation is

beneficial to all of the involved credit union movements. While the four

countries involved in this project are each at different levels of development

they have been able to exchange information and provide one another with

training and technical assistance.

A key aspect of the project has also been that it is being implemented by the

Irish League of Credit Unions Foundation. This organisation knows how a

credit union system can be developed and what pitfalls must be avoided. It

has also been able to provide technical assistance to the most advanced

movement (in Ghana) involved in the project. This would not have been

possible if the implementing organization were an international consulting

firm or foundation.

The establishment of a regional hub at the Credit Union Training Center in

Ghana has a great deal of potential for the region. The Center is financially

viable and will only require inputs related to regional development to continue

and expand its role, especially in the area of promoting lateral knowledge

management

B. Conclusions

WACUPP is a very ambitious project, utilizing modest resources to effect

positive change in 4 countries. Yet, it is successful. This has been due to the

efficient use of resources by all parties, as well as the dedication of the

partners and associates. Further, project management has worked to ensure a

high degree of ownership in the programme by the participants, especially at

the national level.

As regards WACUPP’s Performance Indicators and Results Areas, each of

these will be achieved by the end of the project and most already have been

met.

The success of this project demonstrates the possibilities of assistance with a

longer commitment. Fledging credit union movements in countries such as

Liberia and Sierra Leone could be developed, existing movements in the

Gambia and Ghana could be strengthened, and a regional effort could be

undertaken to develop a legal and regulatory framework which enables a safe

and sound credit union environment. In addition, the project approach and

2

methodologies could be extended, not only with the four current target

countries, but also with other countries in the region.

C. Lessons Learned

Credit union system development takes time. It requires more than a project

of 3 or even 5 years. Rather, it is best categorized as requiring generational

development. The end result is a sustainable system which can and will

provide a wide range of financial services to an increasing number of the

otherwise unserved.

Regular information exchanges, such as the current Steering Committee

Meetings, are critical to ensuring that successes are replicated and common

challenges are addressed.

Innovations, such as the current pilots of graduation microfinance (GMF) and

social performance management (SPM) should be extended. If successful,

they should then be integrated into credit union systems as most practical, as

long as they contribute to the movement’s mission and cost/benefit analysis

shows that the effort is worthwhile.

The project’s baseline needed to be adjusted after inception. A project such as

this, with no previous external intervention or established baseline, should

specify that some targets are provisional and will be verified within three

months of the project’s start.

3

II. Introduction

A. Purpose

The Mid Term Review (MTR) was conducted as a requirement of WACUPP

(the West Africa Credit Unions against Poverty Programme). Its purpose was

to help direct the management team and the steering committee to improve

programme implementation in the second period of the programme. The

Midterm Review looked at existing monitoring data gathered since the

beginning of the programme plus additional data gathered as necessary in order

to assess progress and provide indications of outcomes and impact,

to adjust

and feed into planning for the second half of the programme. As this is

relatively early in the programme cycle, impact is difficult to ascertain, so

member satisfaction and other indications of success or otherwise from the

members’ perspective with programme services have been used as proxy

indications. The MTR assesses the progress of WACUPP against the proposal

as submitted by the Irish League of Credit Unions foundation (ILCUF) to EU

(European Union) ACP (Africa, Caribbean and the Pacific) Microfinance.

B. By whom and how the document will be used?

The primary intended audience for this report consists of the stakeholders: the credit union movements in the Gambia, Sierra Leone, Liberia, and Ghana, the Irish League of Credit Unions Foundation, the organizational partners and the EU ACP Microfinance office. It will be used to identify approaches which have been successful, those which have encountered constraints, and lessons learned. These lessons learned will be applied to further the development of inclusive finance through credit unions in West Africa.

C. Review criteria

The review was centered on whether WACUPP will achieve the performance

results by the project’s completion. The project’s thematic areas – GMF, SPM,

knowledge management, and value chain – were examined. Recommendations

are made on actions to be taken to improve the involved credit union

movements and to ensure full implementation of the programme as per the

proposal.

D. Principle questions

The review examined the impact of the project on its primary beneficiaries. Overall, it looked at:

- How to achieve, by end of period, the project objectives described in the proposal

4

- How to identify areas of importance in the credit union movements in the WACUPP region that may be built on within the programme (even if not

explicit in the proposal)

- How to adapt strategy where it is clear objectives are not being achieved

- How to apply project resources best if budgetary constraints are an issue

The Mid Term Review addresses the following:

1. Effectiveness

a. What has been progress against planned activities?

b. What, if any, indications of change have occurred in relation to

objectives?

c. To what extent have the objectives been met?

2. Efficiency

Has the programme demonstrated a good use of resources?

3. Relevance

a. Are the activities being carried out and related approaches

likely to lead to desired changes? If not, what are the

constraints?

b. Are the objectives still valid?

c. What, if anything, needs to be done differently?

4. Sustainability

What are the likely long lasting effects and how sustainable are the

changes?

E. Methodology used

The review entailed several approaches. First, all project reports were studied. Then, the reviewer attended a Project Steering Committee meeting. He subsequently met individually with each of the national stakeholders, the ILCUF West Africa Regional Advisor, a number of credit unions in Liberia and Ghana, representatives of Social Enterprise Development Foundation(SEND)

1 – Ghana, staff of the Credit Union Training Center

(CUTraC) in Ghana and the Credit Union Association of Ghana (CUA) of Ghana. He also reviewed financial statements and statistics for the past 5 years from the apex organisations in the Gambia and Ghana.

2 (The

movements in Sierra Leone and Liberia are too new to have indicative financial statements.)

1 A project partner 2 The MTR’s Trip Report can be reviewed in Appendix 2.

5

III. Project Background

The project is funded for a period of only 29 months, from August 2012 through

December 2014. It was, however, originally designed for a period of 36 months.

The purpose of the project is to contribute to poverty reduction by means of

expanding financial inclusion through credit unions. The project is based in the

Gambia, Sierra Leone, Liberia, and Ghana. The project’s Regional Capacity

Building and Knowledge Management Hub is at CUTraC in Kasoa, Ghana. The

achievement of financial inclusion is being achieved through asset building and

income growth for individual members. Growth in membership – from 447,386

to 557,0003 (+25%) – is the primary means by which financial inclusion is

achieved.

The project’s result areas are:

A. Regional capacity building services provide for the development of

sound, community owned credit unions on a cost recovery basis.

B. Economic autonomy of underserved populations increased by

expanding access to both financial and complementary services.

C. Graduation of very poor participants from extreme poverty.

D. Evidence based lessons, approaches, and best practices disseminated

through effective distribution channels.

The methodologies used are:

provision of technical assistance and training on credit union management

expansion of graduation microfinance (GMF)

introduction of social performance management (SPM)

knowledge management

The project also calls for measurable results in the following areas:

- Percentage increase in credit union membership;

- Percentage of poor people among new members;

- Number of credit union apex bodies reaching operational self-sufficiency;

- Percentage of women among new members;

- Number of credit unions launching value chain or graduation microfinance projects;

- Number of credit union apex organisations using social performance indicators and poverty index; and

- Number of new policies introduced by the apex bodies into credit union

movements

3 The baseline and projection had to be adjusted following the start of the project. The initial data was collected during the concept stage. Between then and the start of the programme Ghana showed a decrease of 59,161 due to the closing of dormant accounts and the revision of inaccuracies in some areas. Liberia’s statistics were revised to 0, since there were no accurate statistics and no dues were paid to the apex body. The Gambia and Sierra Leone showed increases due to organic growth.

6

The project began with a workshop in July 20124

which identified the technical

assistance and training needs of each of the four credit union movements. Each country

prioritized the needs which could be met by the limited budget and time frame of the

programme. Most of these have been addressed through March of 2014 and the

remainder should be by project end. However, addressing them, will not, per se, mean

that all issues will be resolved. Rather, further interventions in these areas following the

current project will be necessary.

IV. Comparative country movement key areas

The following are comparisons of the four country credit union movements in

several key areas:

A. Minimum share value in the credit union:

Ghana - $20 (€14.46)

Liberia - $10 (€ 7.23)

Sierra Leone - $ 8 (€ 5.79)

The Gambia - $ 3 (€ 2.17)

B. Representational structure

Country Number of

Credit Unions

Number of

Chapters

Origin of Board members

The

Gambia

69 6 1 from each Chapter + 5

elected by the members and 1

co-opted legal adviser.

Liberia 300?5 4 2 from each Chapter + 1 at

large

Ghana 402 11 1 from each Chapter

Sierra

Leone

17 0 Directly from Credit Unions

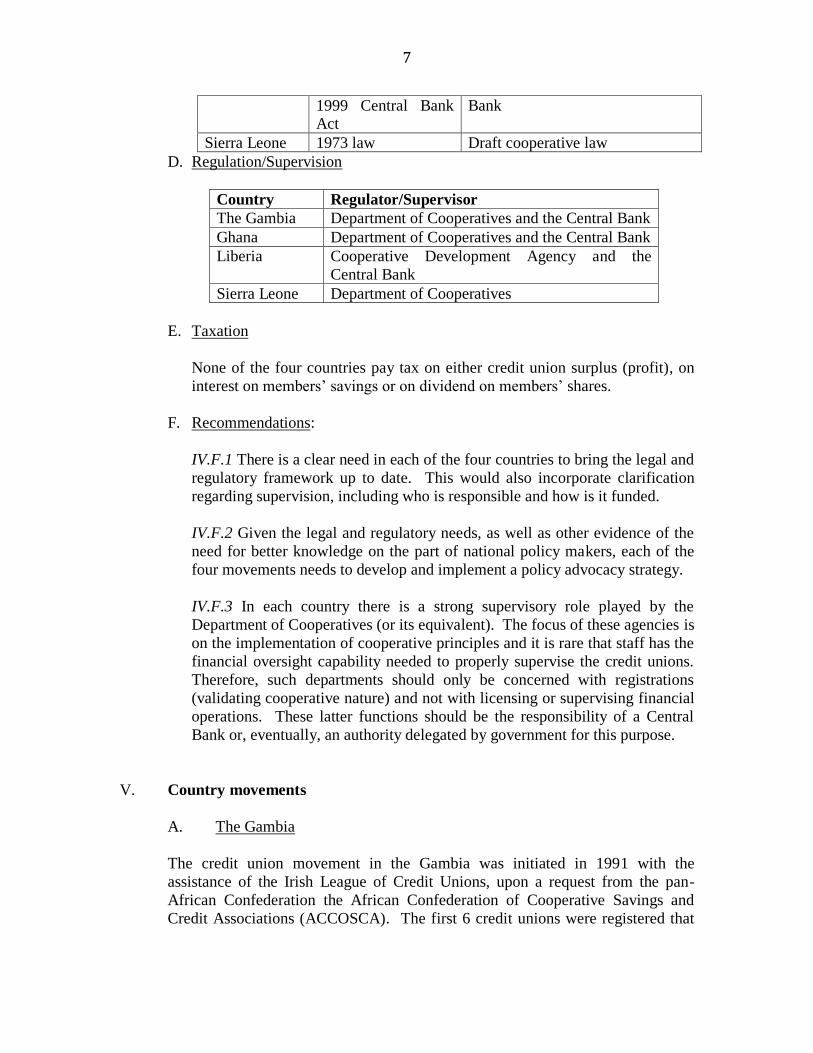

C. Legislation

Country Current Legislation Plans

Gambia 1963 Coop Law

Revised Coop Act

1990 Edition

Draft NBFI law

Ghana 1968 Law Draft CU law with Central Bank

Liberia 1936 Coop Law, Draft regulation under the Central

4 This was three weeks before ILCUF signed the contract with EU ACP. No expenditure relating to this event was charged to the actual programme 5 At time of MTR Liberian CUs were not paying full annual dues, but c 300 CUs were claiming CU status. Since June 2014 LCUNA has formalised this situation and 40 CUs have paid dues and are now full members

7

1999 Central Bank Act

Bank

Sierra Leone 1973 law Draft cooperative law

D. Regulation/Supervision

Country Regulator/Supervisor

The Gambia Department of Cooperatives and the Central Bank

Ghana Department of Cooperatives and the Central Bank

Liberia Cooperative Development Agency and the

Central Bank

Sierra Leone Department of Cooperatives

E. Taxation

None of the four countries pay tax on either credit union surplus (profit), on

interest on members’ savings or on dividend on members’ shares.

F. Recommendations:

IV.F.1 There is a clear need in each of the four countries to bring the legal and

regulatory framework up to date. This would also incorporate clarification

regarding supervision, including who is responsible and how is it funded.

IV.F.2 Given the legal and regulatory needs, as well as other evidence of the

need for better knowledge on the part of national policy makers, each of the

four movements needs to develop and implement a policy advocacy strategy.

IV.F.3 In each country there is a strong supervisory role played by the

Department of Cooperatives (or its equivalent). The focus of these agencies is

on the implementation of cooperative principles and it is rare that staff has the

financial oversight capability needed to properly supervise the credit unions.

Therefore, such departments should only be concerned with registrations

(validating cooperative nature) and not with licensing or supervising financial

operations. These latter functions should be the responsibility of a Central

Bank or, eventually, an authority delegated by government for this purpose.

V. Country movements

A. The Gambia

The credit union movement in the Gambia was initiated in 1991 with the

assistance of the Irish League of Credit Unions, upon a request from the pan-

African Confederation the African Confederation of Cooperative Savings and

Credit Associations (ACCOSCA). The first 6 credit unions were registered that

8

year. Growth and financial viability has been steady and, twenty years later, it is

in many ways a success story.

The national apex organization is the National Association of Cooperative Credit

Unions of the Gambia (NACCUG). Today it groups 72 credit unions with over

52,000 members in 6 chapters. It began a Central Finance Facility (CFF)6 in

1996. Its level of operational self-sufficiency in 2013 was an impressive 100% for

the third year in a row.

The current focus of NACCUG is on: capacity building, the introduction of social

performance management, regulations, and the expansion of financial services

and financial education to rural areas. In the area of regulation it has brought

together the two regulatory agencies - the Central Bank and the Cooperative

Department - and 15 supervisory ratios have been agreed upon. .

ILCUF continues to provide technical and financial assistance and, with the

financial support of Irish Aid, information technology is being provided to 11

credit unions, the regional structure and its offices. With ILCUF, Irish Aid and

Irish and Gambian CU support, NACCUG has recently led the introduction of

modern CU software to 11 major CUs. NACCUG holds the license for this

software and is introducing it to rural CUs through a regional office infrastructure.

In addition to the steering committee meetings, the introduction of SPM (Social

Performance Management) and audit training, the project has also financed the

bringing together the two regulatory arms of Credit Unions (CBG and

Cooperatives) to a common platform to discuss governance and Prudential issues

which resulted to the formulation of prudential return to be sent to the CBG

through the National Apex quarterly. The project has also facilitated the

introduction of SBFIC (the Savings Bank Foundation for International

Cooperation – Germany)7 , which will provide pedagogical and financial training

in the near future.

In recent years membership growth in the Gambian credit union movement has

been steady, reflecting the measured growth of the movement.

Membership

2009 35,492 annual increase

2010 40,546 14.24%

2011 44,847 10.61%

2012 47,632 6.21%

2013 52,094 9.37%

6 A CFF is a “credit union for credit unions”. It is an entity which is either a service or a subsidiary of a national apex organization, which accepts deposits from member credit unions and lends these funds to members. 7 A project associate.

9

The Gambia has no poverty index and therefore NACCUG uses a hybrid of Sierra

Leone and Senegal indexes.

Observations:

NACCUG management appreciates that WACUPP has provided capacity

building to the four national apex organizations. In addition, the technical

exchanges between the apexes have been very helpful.

Recommendations:

V.A.1 The project could have more impact if there was a pool of trainers for each

country. In this way, the apexes could deliver training for its credit unions.

V.A.2 The Gambia should play a larger role in mentoring the credit union

movement in Sierra Leone. Their situations are similar and specific exchanges,

e.g. with the Teachers Credit Unions would be very appropriate.

B. Ghana

The first credit union in Africa was formed in 1955 in Jirapa, in what is now the

Upper West Region of Ghana. In 1967 the first two chapters were formed in the

north and the south. A conference in Tamale in 1968 resulted in the creation of

the Ghana National Union and Thrift Association, the predecessor of the Credit

Union Association – CUA. CUA’s initial duties were: promotion, education,

organization and support of the credit union movement. The movement declined

in the 1980s but was revitalized in the 1990s with major support from Canadian

Cooperative Association (CCA)8

There are currently 585 credit unions and study groups9 within 11 chapters

affiliated to CUA. CUA’s services are quite extensive. They are: training, risk

management (loan protection and life savings insurance), deposit guarantee,

health, youth savings, central finance, and supervision. Not all member credit

unions benefit from each of these services as this is determined by their level of

development.

CUA has three main units: Operations, Human Resources and Finance.

Operations includes: audit, field services, MIS (management information

systems), training, youth savings, and health. Human Resources consists of

human resources and administration, and Finance is comprised of: the central

finance facility, risk management, and accounts.

8 A project associate 9 A pre-credit union which only accepts savings, does not grant loans, and is not registered. The term of existence of these study groups is usually 12 – 18 months.

10

Training is delivered through CUTraC, mainly in its purpose built residential

training center about 35 kilometers west of Accra. This was opened in May 2011

by the then Vice-President of Ghana10

. In addition to providing training to the

Ghanaian credit unions, it was created to be the Center of Excellence for the

region. Course offering have been in such areas as: Member Care, Loan Officer,

Board of Directors, and Credit Union Operations. The Manager of the Liberian

Credit Union National Association (LCUNA) and representatives from the Sierra

Leone credit union movement has already attended accounting and basic credit

union operations courses. The current staff is 29. CUTraC is supported technically

by SBFIC, which has helped it to develop its business plan and course materials.

SBFIC began work in Ghana in 2012 and is an associate in the WACUPP project.

WACUPP has enabled CUTRaC and SBFIC to interact with the Gambia, Sierra

Leone and Liberia for the first time. This has resulted in the first international

participation on CUTraC courses and has enabled SBFIC to factor in these

countries when considering its assistance to the region. The resident SBFIC

representative in Ghana would like to see even closer collaboration with

WACUPP

The risk management programme started in 1986. The number of credit unions

participation as at December 2013 was 265. The program runs two important

services; thus the Loan Protection Plan (LPP) and the Life Savings Plan (LSP).

These plans provide policy cover against death total and permanent disability.

Cover limit for the LPP is up to GH₵ 50,000.00 (€14,463); however any amount

in excess of CUA’s retention is ceded to Quality Life Assurance the reinsurers.

Members pay the premium to insure the loan they contract from the Credit Union

whilst the Credit Union pays the premium on the life savings on behalf of the

members as a service.

The loan protection premium rate is 0.1% per month on every GH₵ 1,000.00. The

life savings premium rate is two tiered; savings portfolio less or equal to GH₵

100,000.00 attract premium rate of GH₵ 0.00085, whilst amount in excess of

GH₵ 100,000.00 attract GH₵ 0.00065.

The major challenge faced by the department is that the Life Savings Plan is not

selling as well as the Loan Protection.

The health education programme was started in 1992, at the initiative of the

Canadian Cooperative Association (CCA). At the time, credit unions in East

Africa were severely affected by HIV. At first the programme focused solely on

HIV/AIDS with coordinators in each chapter. It has now expanded to include

cancer, hypertension and diabetes. The major difficulty is that the health

10 Current president, John Dramani Mahama

11

education office does not always receive information early from regional offices

and the credit unions in order to attend their Annual General Meetings (AGM).

The Central Finance Facility (CFF) serves 500 credit unions11

. At the moment

45 have loans outstanding and the accounts of 72 Credit Unions are classified as

dormant due to liquidity issues. These 72 illiquid CUs comprise a serious

situation which CUA should address as a priority, canvassing donor support if

necessary. Participating credit unions pay in 5% of their assets after an audit.

These funds earn interest and the credit unions are then eligible for loan. The CFF

has a loan loss reserve.

The CFF also operates CUALink, a money transfer facility, through

AFRICXPRESS.

CUA’s Youth Savings programme began in 1999. Its objective is to draw

children and youth into credit unions. At the time of its initiation the average age

of a credit union member was 45. With the assistance of CCA, clubs were set up

in 10 high schools, each with an annual membership meeting, effectively as a

prototype of a credit union. The 2010 CUA Biennial decided that all credit

unions should have a youth savings club. These clubs are now providing training

to youth, in such forms as quiz competitions.

Youth are defined as those between the ages of 18 and 35. While the law

stipulates that one reaches the age of legal capacity at 18, persons can save at

credit unions before then. While the primary targets are youth, they are also seen

as change agents who can explain credit union membership and its benefits to

their parents. An objective for the future is to have a youth board observer or

board member in each credit union. The current challenges are in mobilization

and coordination, especially with the training department.

CUA established a stabilization fund about thirteen (13) years ago. This has been replaced with a Deposit Guarantee Scheme fund since December 2013. Currently 80 Credit Unions are participating in the scheme, mostly those classified with grades A, B and C. The Credit Unions contributions to the scheme depend on their classification grades. Audits are compulsory for all Credit Unions to be undertaken by CUA and DOC Auditors. The Audit is currently the basis for the classification. The lower the grade obtained by a Credit Union, the higher the premium it must pay by way of contribution to the Deposit Guarantee Scheme fund. Grade A - 0.20% of total savings annually Grade B - 0.25% Grade C - 0.30% Grade D - 0.35%

11 Each has paid in shares

12

Grade E - 0.40% The Credit Union should not be in arrears of its contributions to the stabilization fund. In case of distress, members would be paid their full savings but to the Credit Unions, the coverage of payment is graded. The maximum insurable amounts for now are as follows: Grade A = 50% of savings Grade B = 40% Grade C = 30% Grade D = 20% Grade E = 10%

CUA’s Supervision Service monitors credit union performance vis-à-vis targets.

It is in the field 50% of the time. The biggest challenge for the field services

department is that each credit union is to submit a monthly report. CUA and the

Department of Cooperatives are currently working on a decree for supervision.

Credit unions can only be closed in collaboration with the Central Bank

CUA undertakes audits with the Department of Cooperatives, although there are

cases where CUA undertakes this alone. CUA audit staff are in each region:10 in

Accra, 3 – Tamale, 2 – Central, 2 – Western, 5 – Ashanti, 2 – Eastern, 2 – Volta, 1

– Upper East, 1 – Upper West, 2 – Northern. The fiscal year is from July through

June and all audits are on-site. The greatest challenges are human resources and

record keeping. Some credit unions are only open on Sunday and have no office

or staff. This all contributes to delays. In some cases these delays can be for as

long as 9 months.

CUA has created its own CU software, called CUSoft, which it sells to CUs at

very reasonable rates. It has been determined by CUA that asset size should be

the criteria for introducing software. The criteria are in three categories with the

least category being credit unions with asset size less than GH₵ 200,000 (US$

70,300). CUA can obtain information in 4 to 5 days. 90 – 100 credit unions send

information via on-line. In the other cases CUA staff must go to the credit unions

and get the information. Staff that can assist with installation and maintenance of

the software are available in two chapters.

Major challenges are personnel who need to be trained on the system and

inadequate IT logistics for software support and maintenance. Marketing of the

software needs to be intensified. In addition, credit unions that are not on-line

make the information flow quite slow.

About 20 credit unions use other software. Some, especially new ones, are using

Easy Book, which is an Excel based system

Recommendations

13

V.B.1 The Stabilization Fund is being replaced by the Deposit Guarantee Scheme.

The understanding at CUA is that these two programs provide the same

protection. However, the former is for the credit unions, while the latter is for the

members. Both programs exist in such movements as those in: Ireland, the USA,

and the Canadian Provinces of British Columbia, Nova Scotia, and New

Brunswick. Therefore, the Stabilization Fund should not be terminated.

V.B.2 Credit union supervisions can be 9 months late. Each credit union is

supervised on-site. Supervisions can be brought up to date by triaging credit

unions. Credit unions can be listed by asset size and a cut-off point should be

determined at which it would be certain that those credit unions could be

supervised on-site in a timely manner. The remainder would be supervised off-

site, only requiring an on-site visit if any irregularities are found.

V.B.3 Consideration should be given to having the credit union pay for both loan

protection and life savings insurance. The cost will, of course, be reflected in the

interest spread. But such an approach would have two benefits: highlight the fact

that this is a service from the movement to individual members and impress upon

the credit unions that it is generating income for them. Naturally, an information

program will be necessary.

V.B.4 The fact that so few credit unions are on-line is disturbing. CUA has tried

as many options as seem possible to expand the number, including the provision

of portable modems. Efforts should continue in this regard. One other possibility

could be the establishment of service centers – which were, in fact, previously

used in some West African countries. Service centers are common points which

are financed by a group (perhaps 10) of credit unions. The services provided

depend upon the needs expressed by the credit unions. Sometimes it could an

itinerant bookkeeper and sometimes it could be a data collection point.

C. Liberia

The credit union movement in Liberia was started in 1966 and LCUNA was

established in 1969. By 1989 there were 68 member credit unions with 20,000 m-

individual members and €7.2 million in savings. The wars devastated the

country, including credit unions. There is now a revival under the reinvigorated

apex organisation – Liberia Credit Union National Association (LCUNA)12

.

Data is difficult to identify, as LCUNA’s systems are in a state of development.

Prior to the project it was reported that there were 6,000 credit union members in

Liberia. This is difficult to verify and the number of credit unions is estimated to

be about 300 according to CBL, but there is no reliable data. One major problem

is that there is also no agreement on what is and is not a real credit union. For

instance, there are many savings clubs which may or may not identify themselves

12 This is the same organization which existed prior to the wars

14

as such and there is a growing number of VSLAs (Village Savings and Loan

Associations)13

.

The Central Bank of Liberia (CBL) has been providing support to credit unions

(and other microfinance organisations) in the form of loans. Other support is

provided by the World Council of Credit Unions (WOCCU), with funding from

the United Nations Capital Development Fund (UNCDF). This project is funding

the creation of four regional credit unions and providing some logistical support

to the offices of LCUNA. The WOCCU Microlead programme aims to have

40,000 members in 4 regional CUs by the end of 2017.

WOCCU has given assistance to LCUNA with training, transport resources and

refurbishment of its headquarters. WACUPP has assisted with training, technical

assistance and international exposure. However, unlike the other 3 partner

countries LCUNA does not have a long term international partner to support it on

a comprehensive development programme.

Several credit unions14

were visited during the MTR. The following were

observations:

- Credit unions do not produce annual audited accounts

- An accounting system to produce monthly an annual accounts is needed

- Some credit unions are multi-functional. In addition to financial services,

they undertake trading activities. These are all in the same building.

- There is some confusion between WACUPP and the WOCCU project. This may be due to the fact that both projects collaborate in order to

deliver training to Liberian CU personnel. Assistance is needed with

strategic plans, accounts, computerization and governance

- The training provided through the project is much appreciated.

The leadership of LCUNA provided the following insight of the project from their

perspective:

- The opportunity to exchange information and experiences through WACUPP is very critical

- Previously there had been no standards for credit unions. Now these are

being developed.

- There is a concern that WOCCU’s approach may be inconsistent with LCUNA development strategy in some areas. For instance, WOCCU is

asking small CUs to exhort their members to join the 4 regional CUs.

WOCCU is also asking CUs to deposit their surplus savings in the

regional CUs. This could affect the establishment of a Central Finance

13 These are difficult to track in terms of development, or even possible graduation. They close their accounts at the end of each fiscal year and return all funds to members. 14 Airport Workers, Financial and Capacity Development, and In God We Trust

15

Facility at LCUNA which would provide income for services to the entire

movement.

- The duration of WACUPP is too short.

- In depth analysis and policy development must be undertaken especially in

such areas as: central finance, youth savings, and governance.

- The relationship with the other countries involved with WACUPP must be

maintained.

- In addition to the threats posed by the CBL loans and the WOCCU project, dues payments from credit unions is a critical issue. Currently

very little dues are being collected by LCUNA from CUs

- Training support is need. They have the basic concept, but no resources and training of trainers is essential.

- WACUPP has been a success and both ILCUF and the EU should be

commended.

Recommendations

- V.C.1 LCUNA must strictly apply its requirement of member credit unions

to pay dues. Those which do not should not be allowed to vote at the next

Annual General Meeting.

- V.C.2 LCUNA should work with the CBL and CDA (the Cooperative Development Agency) in determining a strict definition of a credit union.

This should be based on international best practices.

- V.C.3 WOCCU should be encouraged to work more closely with LCUNA. In addition, all efforts should be made to ensure that the regional credit

unions do not undertake any of the current or future functions of the

national apex.

- V.C.4 Annual credit union audits must be carried out.

- V.C.5 No credit union should be multi-functional. There is too much of a

risk of mixing cost centers and there have been no examples of successful

multi-functional credit unions round the world.

- V.C.6 Assistance should be provided with strategic plans, accounts, computerization (in select credit unions), and governance.

- V.C.7 Training, such as that provided by the project, should be continued.

- V.C.8 Experience and information exchanges with other credit union movements in the region must be continued.

- V.C.9 The CBL program of providing loans directly to credit unions

should be terminated. It is not the role of government to play this role and

it is a conflict of interest for a regulatory body like the CBL to lend to the

entities which it regulates.

D. Sierra Leone

Sierra Leone had a thriving credit union movement through the ‘70s and

‘80s which was devastated by the civil war. Since 2010, efforts have been

16

made by CCA and ILCUF to revive the movement. This project utilizes

the technical assistance of credit union experts from Ghana. The focus is

on: training to strengthen the capacity of functioning credit unions; expanding membership; and modernizing services, management and governance practices.

ILCUF and CCA have been implementing a small programme to rebuild

the CU movement since 2010. Initially there were 6 pilot credit unions,

now there are 17. The apex organisation National Association of

Cooperative Credit Unions of Sierra Leone (NACCU SL) was created in

November 2013. There are 5 board members and 3 supervisory

committee members.

The credit union affiliation fee is $45 and dues are $22 per credit union.

The CCA/ILCUF project will be in place for 2 more years.

NACCU has no staff, but the CCA/ILCUF project is staffed by an

expatriate and two Sierra Leoneans and it supports the apex. The

CCA/ILCUF project is providing exposure, base documentation,

monitoring and training, while WACUPP supports training and promotes

graduation microfinance (GMF). NACCU attributes new membership

within some CUs to GMF.

NACCU will take steps to utilize social performance management (SPM)

beginning in July. The SPM survey will take place before the end of the

year.

WACUPP is recognized by the leadership of NACCU as building the

capacity of credit unions in Sierra Leone, providing the opportunity to

attend meetings with other national organisations, facilitating familiarity

with other national movements in Africa, and training trainers.

Recommendations:

V.D.1 Information exchanges with other credit union movements in the

region are critical and must be continued.

V.D.2 Given the state of renewal of the movement the basics of grass roots

promotion and developing NACCU as a service organisation must be

continued.

V.D.3 Capacity building for the staff and board are a high priority.

V.D.4 Since new CU membership is attributed to GMF, this activity

should be extended.

17

VI. Project themes

The project began with four innovations to be researched and promoted in order

to achieve the project’s objectives and reach the performance indicators. These

are: graduation microfinance, value chain, social performance management, and

knowledge management.

A. Graduation microfinance

Graduation microfinance is an approach which was developed by SEND in 1998

by CEO Mr. Siapha Kamara (a Liberian). SEND registered in Ghana as an

integrated NGO promoting: food security, reproductive health, gender, human

rights & peace building, and enterprise development. Support was provided by

CCA. Initially SEND tried to introduce a financial component of integrated

intervention by NGOs, but this didn’t work and then they turned to credit unions.

The first impression of the reviewer was that the MFG approach was inconsistent

with traditional credit union development. In the traditional development model

in many countries15

study groups are first established. New members first save

for a period of 12 to 18 months prior to borrowing. These have existed in Ghana

for decades and were initiated in the Kailahun District of Sierra Leone16

. The

GMF approach requires external loan funds, a method which is contrary to that

which has been proven successful. Also, SEND promotes GMF by stating that

the price of a share is too high, thus justifying the need for External Loanable

Funds. However, an easier solution would be to simply lower the par value of a

share. Nevertheless, a more extensive review of the application of the system

was justified.

The purpose of GMF is to provide financial services to female entrepreneurs for

income generating activities (IGA). Savings is a prerequisite, but this is in terms

of frequency and not amount. Groups of 5 to 7 persons are created and 30 of

these groups then form a Credit and Savings Association (CSA). The CSAs

generally charge a fee of 1% per loan cycle (4 months). Each CSA decides how

much a member should save in order to begin borrowing. The CSA buys a share

in the local credit union. Thus, it is key to this approach that the credit union

must be in existence first.

GMF, with SEND support, is in two countries supported by this project: Sierra

Leone and Ghana. Credit unions offering GMF were proven to be successful,

especially in terms of increasing female membership, in the north of Ghana prior

to the project. Based on this, EU funding has made it possible for the programme

to expand and have a positive impact on more individual members. Since the

15 Some of these are: in Anglophone West Africa, in the Caribbean, Albania, and Ireland 16 In 3 chiefdoms a credit union programme was developed, while in 4 chiefdoms a microfinance programme (involving other entities) was developed.

18

beginning of WACUPP the number of participating credit unions has increased

in Sierra Leone by 1, and in Ghana by 717

.

Persons who were previously hesitant to join a credit union or who didn’t not

have the initial resources have now become fully active members. Loans have

been provided to a variety of trades, such as; farmers, millers, blacksmiths, and

foodstuff traders. These have changed life of some members by allowing them to

pay for school fees and afford better housing. There has also been a multiplier

effect felt through the local communities. Through the project, about 4 female

leaders have been trained, leading to their further development and they are now

councilors or MPs.

The key success of WACUPP in this regard is that it has persuaded CUs to

introduce GMF within their own resources, whereas before WACUPP GMF

existed only in CUs which were being subsidized by SEND projects.

Observations

GMF definitely adds value to credit unions. It maintains the credit union ethos of

emphasizing savings first, promotes female membership, and is focused on local

income generation.

Four credit unions undergoing GMF training were interviewed18

. They each

agreed that, if the project was not funding the training, their credit unions would

pay for it. However, they did admit that they were influenced by the fact that they

knew the programme. Therefore, it was suggested that GMF general education be

provided at the CUA Biennials and that it be put into a credit union’s education

budget with the fees specified.

Loans under GMF do not follow credit union rules (i.e.; they do not require

collateral). This makes graduation more difficult.

GMF record keeping and data regarding GMF delinquency need to be improved.

Recommendations

VI.A.1 Graduation Microfinance should be extended to more credit unions,

especially in Sierra Leone and Ghana. These should be well functioning credit

unions with staff, computerized systems and office space.

VI.A.2 GMF should be monitored by the credit union board and management, as

well as the programme’s promoters.

17 In Ghana there are 2 new ones in the Northern region and 5 in the Central Region. The Central Region was chosen since it is the 4th poorest (of 10) in the country. 18 Oguaa Teachers, Swedru Emmanuel, University of Cape Coast, and Progressive Women.

19

VI.A.3 Records should be maintained as applies to GMF delinquency. These

should then be compared to rates for traditional loans by the credit union.

VI.A.4 The cost effectiveness of GMF should be investigated. The key variables

to study would include: comparative delinquency, CSA loan charges, and staff

time (i.e.; whether GMF requires more).

B. Value chain

A value chain (VC) is a chain of activities that a firm operating in a specific

industry performs in order to deliver a valuable product or service for the market.

This concept comes from business management and was first popularized by

Michael Porter19

.

The idea of the value chain is based on the process view of organizations, the idea

of seeing a manufacturing (or service) organisation as a system, made up of

subsystems each with inputs, transformation processes and outputs. Inputs,

transformation processes, and outputs involve the acquisition and consumption of

resources - money, labour, materials, equipment, buildings, land, administration

and management. How value chain activities are carried out determines costs and

affects profits.

Credit unions provide financial services to the un-banked who are excluded from

the mainstream financial system in emerging countries. They are considered as a

powerful development tool, as they consist of providing micro or small “income

generating” loans, deposits, remittances and insurance schemes to micro-

entrepreneurs and small-businesses.

They provide financial services for both social and productive purposes. In order

to provide loan facilities to micro-entrepreneurs, credit unions receive savings

from members. The credit union movement is well structured with a clear split of

responsibilities at all levels of the value chain. In order to examine how this

might be best exploited in the project area, WACUPP undertook a study in 2012

in Ghana to appraise the applicability of value chain financing to the project.

The project management’s Report Number 2, for the second quarter of 2012

stated:

“The field research has shown that there are major challenges facing any credit

union movement which seeks to become involved in Value Chain Financing

(VCF). VCF requires significant expertise and financial resources. It requires

strong partners from the agricultural development sector and the private sector.

Investment in VCF requires time to come to fruition. The results are also highly

dependent on external forces such as weather, markets and trade policies.

19 Porter, Michael E. (1985). Competitive Advantage: Creating and Sustaining Superior Performance. New York: Simon and Schuster.

20

Graduation microfinance research has shown much more positive outcomes

within CUs however. For this reason WACUPP may achieve more by focusing its

resources on the introduction of Graduation Microfinance into the CU systems

rather than VCF.”

Further, the 3rd

report (1st quarter of 2013) noted:

“The workshop on graduation microfinance and the review of the field research

confirmed the views that were expressed in the previous report - that there are

major challenges facing any CU movement which seeks to become involved in

Value Chain Financing (VCF). VCF requires significant expertise and financial

resources. It requires strong partners from the agricultural development sector

and the private sector. Investment in VCF requires time to come to fruition. The

workshop confirmed the potential for CUs to innovate in graduation microfinance

and we therefore seek approval to amend performance indicator 5 to include the

launch of Graduation Microfinance projects.”

Therefore, it was determined not to pursue further investigations as regards value

chain financing. The decision demonstrated sage project management, especially

as regards determining what results would be feasible, given limited project

resources and a short time frame.

C. Social performance management

The Universal Standards for Social Performance Management ("Universal

Standards") is a comprehensive manual of best practices created by and for people

in microfinance as a resource to help financial institutions achieve their social

goals. Developed through broad industry consultation, the Universal Standards

apply to all microfinance institutions pursuing a double bottom line20

.

Each dimension contains standards, which are simple definitions of what the

institution should achieve, as well as essential practices, which are the

management practices that the institution must implement in order to meet the

standard. There are also one or more indicators per essential practice, which an

institution can use to assess whether it has implemented the practice. Meeting the

Universal Standards signifies that an institution has strong SPM practices.

Credit unions have always been concerned with the welfare of their members.

However, they must be equally focused on the financial sustainability of the

institution. Credit unions which manage only their financial performance will

almost certainly be driven only by financial outcomes, so institutions that also

have social goals must manage their social performance as well. By defining and

promoting strong SPM, the Universal Standards contribute to refocusing

institutions on the member.

20 Financial and social

21

In the past year, financial institutions21

have engaged with the Standards in

several ways:

self-assessment of their SPM practices against the “essential practices” listed in the Universal Standards,

development of action plans to change practice in areas where the self-

assessment showed gaps, and

implementation of essential practices that were not yet in place in their

institution.

A major focus of WACUPP is poverty reduction. The introduction and

institutionalization of SPM is the cornerstone of long term poverty reduction. This

aspect of the project is intended to:

- develop recommendations and strategies from the baseline assessment of

social performance of apex and emerging apex organisation

- develop a Poverty Index for each country to construct poverty indicators in piloted areas and adaptation of MIS to ensure routine collection;

- develop reporting and accountability mechanisms which place social performance on an equal basis with financial performance;

- review SPM based on assessments including client satisfaction and depth of outreach.

In the third quarter of 2013 ILCUF developed the key questionnaire tool which

apex bodies can use to test credit unions for their level of social performance22

. The

tool was presented to WACUPP partners and was very well received. In November

an expert launched the tool with CUA and NACCUG which began the collection of

data under a 3 month programme involving 40 CUs.

The NACCUG SPM exercise was undertaken by an expert from the Gambia MFI

Network (GAMFINET). Credit unions were selected at random for testing. In

Ghana a workshop was held with several credit unions. This was facilitated by the

Project Coordinator. Two of the involved credit unions23

were interviewed during

the MTR. They indicated that they understood the purpose of the SPM.

Observations

When a social performance survey is completed, the results are presented to the

financial institution’s board which then develops an action plan. It is unclear

whether or not the credit unions involved in the survey receive feedback from the

managers of the process. The process is very useful in determining the segment of

the population which is served by a credit union.

21 Through the international SPTF (Social Performance Task Force) 22 Tools were reviewed from organisations such as: Cerise, OikoCredit, and CCA (Development Ladder Assessment for Co-operative Enterprise). A questionnaire was then customized for credit unions. 23 Teachers Credit Union and Emmanuel Credit Union

22

Recommendations

V.C.1 Simply developing an action plan is not an adequate next step. The goal of

achieving positive double bottom line should be the ultimate focus. The SPM

survey should be integrated with a financial and statistical survey, with the financial

being based on operating ratios and the statistical on growth. Each of the variables

being examined must be measurable. The results of the survey should be analyzed

and the key deficiency areas should be identified as those which require technical

assistance and training. A follow-up survey would indicate the level of impact

(success) of the interventions. In this way, SPM would have a purpose of being

integrated into the credit union movement’s existing operations and a follow-up to

the results would be ensured.

V.C.2 It is not critical that all credit unions be surveyed. However, random

selection is inappropriate. The first such survey should cover as many credit unions

as possible. Then, those (possibly 20) which are closest to the mean should be

identified as the sample group for follow-on assessments.

D. Knowledge management

Knowledge Management (KM) is the process of capturing, distributing and

effectively using knowledge. WACUPP is primarily about knowledge

management, harnessing existing learning from both international sources and

within the region, and developing a high level of professional and practical

expertise throughout the credit union movements. This will help credit unions

comply with international best standards.

The project’s KM function is based at CUTraC. It is an approach which is evident

through all aspects of the project. The Project Steering Committee gathers the

representatives of all primary stakeholders to discuss national updates and share

innovations. Training offered by CUA in Sierra Leone and Liberia shares

successful practices. A recent visit by representatives of NACCUG to CUA

observed the implementation of the risk management programme. In February

2013 a website was initiated to share information internally to the project and

externally.

The project hub at CUTraC does not appear to be very pro-active. The majority of

knowledge management initiatives come from ILCUF. For the benefit of the longer

term, the hub should not be reactive, but rather it should initiate knowledge

exchanges and activities which would then result from discussions based on such

exchanges.24

24 One reason for this may be that telecommunications are still very poor across the region. Internet access is still very poor across the region, phone communication from Ghana to the other West African countries is far more expensive than it is from Ireland.

23

The website is seen as a platform for best practices. It contains information about

risk management, central finance, and training and includes manuals. The Financial

Literacy Manual from the Gambia is on the site and there will soon be a GMF

research manual.

Observations

The periodic Steering Committee meetings are critical. Given the minimal

resources of the Liberian and Sierra Leonean movements, they will, however, not

be able to be continued without external (project) funding.

The website is a very important mechanism which ensures that all stakeholders

have access to each other’s information in a timely manner and can adapt tools to

their own environment. At the moment, the website exists as an inventory of events

and documentation. The challenge is to identify how it can best be used and

managed. This is especially problematic in a region where website usage is very

low. In addition, access is very difficult and slow in all of the project’s countries,

with the possible exception of the Gambia.

Recommendations:

V.D.1 The activities of the project hub should be more pro-active.

V.D.2 All efforts should be made to identify further support for the Steering

Committee exchanges.

V.D.3 The website should ensure that all project documents, such as manuals and

policies, are posted.

V.D.4 The website must be interactive. This can be achieved through several means.

For instance, blogs should be encouraged, especially as pertains to specific topics.

The online discussions which to be generated would provide insight as to the

practical application of approaches, especially pro-poor ones. WACUPP would also

be able to generate discussions by starting a blog on a given topic.

Efforts should continually be made to ensure that the website is user friendly.

VII. Project Implementation Review

A. Effectiveness

1. What has been progress against planned activities?

The best way to measure progress against planned activities is by

reviewing the project’s performance results.

24

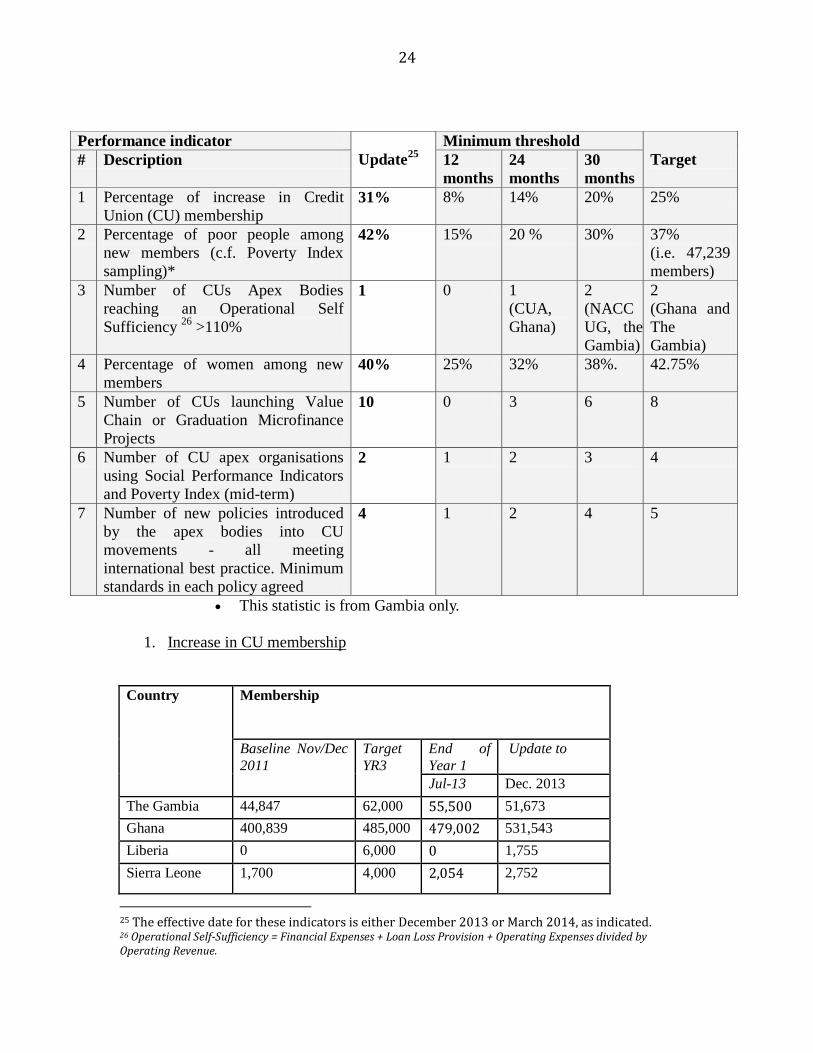

This statistic is from Gambia only.

1. Increase in CU membership

Country Membership

Baseline Nov/Dec

2011

Target

YR3

End of

Year 1

Update to

Jul-13 Dec. 2013

The Gambia 44,847 62,000 55,500 51,673

Ghana 400,839 485,000 479,002 531,543

Liberia 0 6,000 0 1,755

Sierra Leone 1,700 4,000 2,054 2,752

25 The effective date for these indicators is either December 2013 or March 2014, as indicated. 26 Operational Self-Sufficiency = Financial Expenses + Loan Loss Provision + Operating Expenses divided by Operating Revenue.

Performance indicator

Update25

Minimum threshold

Target # Description 12

months

24

months

30

months

1 Percentage of increase in Credit

Union (CU) membership 31% 8% 14% 20% 25%

2 Percentage of poor people among

new members (c.f. Poverty Index

sampling)*

42% 15% 20 % 30% 37%

(i.e. 47,239

members)

3 Number of CUs Apex Bodies

reaching an Operational Self

Sufficiency 26

>110%

1 0 1

(CUA,

Ghana)

2

(NACC

UG, the

Gambia)

2

(Ghana and

The

Gambia)

4 Percentage of women among new

members 40% 25% 32% 38%. 42.75%

5 Number of CUs launching Value

Chain or Graduation Microfinance

Projects

10

0 3 6 8

6 Number of CU apex organisations

using Social Performance Indicators

and Poverty Index (mid-term)

2 1 2 3 4

7 Number of new policies introduced

by the apex bodies into CU

movements - all meeting

international best practice. Minimum

standards in each policy agreed

4 1 2 4 5

25

TOTAL 447,386 557,000 536,556 587,723

Yr3 %age over

baseline 125%

Actual results

120% 131%

The overall target of 557,000 members has been surpassed. This is due mainly to the

great increase in Ghana membership. WACUPP hopes that all countries will meet their

own national targets by project end.

Status: target achieved.

2. Percentage of poor people among new members.

The target of new members under the poverty line is 37%.

Surveying in Gambia showed that 42% of new members are below the poverty line as of

the end of 2013. Surveying is to be done in Ghana and Sierra Leone.

In Ghana about 60% of the new members reached live in the extreme poverty zones in

the coastal and northern areas of Ghana, therefore, it is estimated that 40% of these new

members are below the poverty line. However this estimate needs to be validated by

surveying.

Status: part achieved

3. Number of CUs Apex Bodies reaching an Operational Self Sufficiency (OSS)

greater than 110%.

The target is that 2 apex organisations will reach this level.

CUA has reached the target, achieving an OSS ratio of 124.72% in 2013.

In 2013 NACCUG reached 100.25%. In 2011 it was 107.59% and in 2012 it was

100.72%. Therefore, there has been a three year annual trend of surpassing 100%. This

reflects a stable rate of financial sustainability. However, since the focus is on surpassing

110%, a special effort must be made in 2014 to take measures which ensure this.

It is reasonable to expect that CUA will reach the OSS target by the project’s end and that

NACCUG will also surpass this indicator if the proper steps are taken.

Status: part achieved

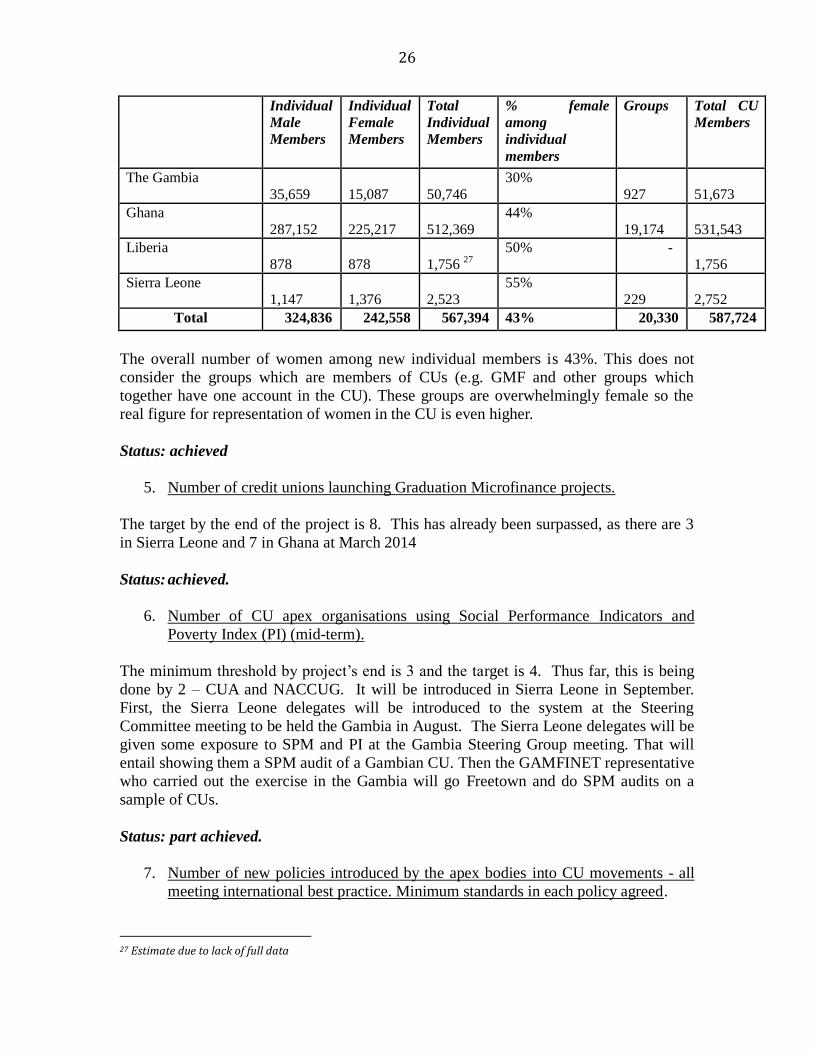

4. Percentage of women among new members

The following is the breakdown of new members during the project period:

26

Individual

Male

Members

Individual

Female

Members

Total

Individual

Members

% female

among

individual

members

Groups Total CU

Members

The Gambia

35,659

15,087

50,746

30%

927

51,673

Ghana

287,152

225,217

512,369

44%

19,174

531,543

Liberia

878

878

1,756 27

50% -

1,756

Sierra Leone

1,147

1,376

2,523

55%

229

2,752

Total 324,836 242,558 567,394 43% 20,330 587,724

The overall number of women among new individual members is 43%. This does not

consider the groups which are members of CUs (e.g. GMF and other groups which

together have one account in the CU). These groups are overwhelmingly female so the

real figure for representation of women in the CU is even higher.

Status: achieved

5. Number of credit unions launching Graduation Microfinance projects.

The target by the end of the project is 8. This has already been surpassed, as there are 3

in Sierra Leone and 7 in Ghana at March 2014

Status: achieved.

6. Number of CU apex organisations using Social Performance Indicators and

Poverty Index (PI) (mid-term).

The minimum threshold by project’s end is 3 and the target is 4. Thus far, this is being

done by 2 – CUA and NACCUG. It will be introduced in Sierra Leone in September.

First, the Sierra Leone delegates will be introduced to the system at the Steering

Committee meeting to be held the Gambia in August. The Sierra Leone delegates will be

given some exposure to SPM and PI at the Gambia Steering Group meeting. That will

entail showing them a SPM audit of a Gambian CU. Then the GAMFINET representative

who carried out the exercise in the Gambia will go Freetown and do SPM audits on a

sample of CUs.

Status: part achieved.

7. Number of new policies introduced by the apex bodies into CU movements - all

meeting international best practice. Minimum standards in each policy agreed.

27 Estimate due to lack of full data

27

At the recent (March 2014) Steering Committee Meeting in Liberia, 4 policies were

introduced:

- Membership

- Governance and Volunteers

- Standards of Conduct and Ethical Behavior for Officers

- Credit Control

At the next meeting (in August) two more policies – Gender and Operational

Management – will be introduced.

Status: part achieved.

2. What, if any, indications of change have occurred in relation to

objectives?

The only major change has been the judicious decision not to pursue value chain. Project

resources have since been focused on graduation microfinance, which is appreciated by

the credit unions and results in increased female membership and more locally generated

income.

3. To what extent have the objectives been met?

The project’s objectives are in the process of being met. The project has only been active

for less than 2 years and final results are pending. Nevertheless, the prognosis is that all

objectives will certainly be met, as defined by the performance indicators. Given the

short time frame, this is impressive in that, as is understandable given the regional nature

of the project across 4 countries, the project was slow to start-up.

The following are the project’s results areas and their status:

a. Regional capacity building services provide for the development of

sound community owned CUs on a cost recovery basis.

Capacity building has been provided in several ways. Experts from CUA have provided

training in Liberia and Sierra Leone. Representatives from the Gambia have visited CUA.

Liberian and Sierra Leonean staff have been trained at CUTraC. Training has been

provided at each Steering Committee meeting. In addition, specialized staff from the

Irish credit union movement have traveled to each of the four countries and provided on-

site technical assistance and training.

b. Economic autonomy of underserved populations increased by

expanding access to both financial and complimentary services.

Increased access to financial and complimentary services has been demonstrated by the

increase in credit union membership in each of the four countries. In percentage terms

28

this has been particularly striking in Liberia and Sierra Leone. It is equally important to

note that female membership has increased as a percentage of the whole during the

project period.

c. Graduation of very poor participants from extreme poverty.

Graduation has been achieved primarily through the GMF component of the project.

While this has been limited to several credit unions in Ghana and Sierra Leone, as a pilot

activity it has proven to be successful and replicable.

5. Evidence based lessons, approaches and best practices disseminated

through effective distribution channels.

The project’s emphasis on knowledge management has demonstrated that approaches and

lessons learned can be shared quite successfully. This has been through steering

committees, meetings, trainings, and the website.

A. Efficiency

Has the programme demonstrated a good use of resources?

The use of resources has been excellent. This project covers 4 countries and directly

benefits over half a million persons. Yet, external funding is relatively minimal for such

an endeavor. The successes to date have been due to the dedication of the credit union

movements in the Gambia, Sierra Leone, Liberia, Ghana, and Ireland. Each of these has

committed its own time and resources to achieving project objectives.

The contribution of the EU has been very generous. In addition, the ILCUF has provided

40% of the project’s financial resources. Given the fact that the project will only be

operational for 29 months, rather than 36 (80% of the intended time frame), the

achievement of the objectives has only been possible due to the dedication of the

stakeholders.

The estimated value of the project is €475,000 Euros. The number of new members

during the project period is projected to be about 153,00028

. Therefore, the cost per new

member is €3.02 over a period of 29 months. However WACUPP is of benefit to all CU

members as it improves the services and security of CUs for all members. At project end

there will be 600,000 CU members, therefore the project cost per member is €0.79

The project cost per beneficiary is much lower again as the entire family of the member

benefits from CU membership.

The use of EU funds has been particularly effective in that it has leveraged 40% of the

project’s value with its contribution. Thus, about 67% of additional resources were

generated for a common purpose.

28 Membership at project start was 447,386 and projected membership at the end of the project will be 600,000 (revised estimate at March 2014).

29

B. Relevance

1. Are the activities being carried out and related approaches likely to lead

to desired changes? If not, what are the constraints?

The activities which are being carried out will result in achievement of the planned

performance indicators. However, this should be viewed as just a start. The project’s

duration is very short. Through the prism of such a time frame, the activities and

approaches are certainly relevant. But, the changes must continue and, for this to

happen, approaches should be continued with relevant activities. An example of changes

effected by the project is SPM. Although this has existed in the microfinance world for a

number of years, it has been introduced to the credit union movements through

WACUPP.

A number of technical assistance and training activities are planned for the remainder of

2014. These should remain as scheduled. However, more specificity is needed to

describe the training to be provided from CUA staff to the Liberian credit unions.

2. Are the objectives still valid?

The objectives can be categorized as being on several levels. The first is poverty

reduction. Then, there is the overall objective of financial inclusion. The final level is

that of building sustainable member owned and controlled financial systems. Each of

these is still valid.

3. What, if anything, needs to be done differently?

The national stakeholders demonstrate a high degree of ownership in the project. The

project management (through ILCUF, CUA and the steering committee) is dedicated,

meticulous, inclusive, and extremely hard working. The only aspect which needs some

improvement is that of awareness of the project and its interventions by credit unions and

their members. Some of these are involved in SPM or GMF and have first-hand

experience as to impact. But these are a minority.

C. Sustainability

What are the likely long lasting effects and how sustainable are the changes?

Effective credit union movement development is generational. Under the proper

circumstances there can be positive outcomes in the short term. However, if these are to

be sustainable, efforts must be continued over longer periods. Systems must be

developed and become operational. Capacity building must take place from the credit

union to the apex organization level.

30

In the cases of the Gambia and Ghana financial sustainability of the apex bodies will be

achieved by the end of the project. But this will not preclude the need for an extended

outreach in terms of services. For instance, in Ghana, not all credit unions have access to

the CFF or risk management or the deposit guarantee scheme. Not all credit unions are

inspected on time. This risks problems being detected too late. NACCUG and its

membership are beginning to implement new services. These must be tested and rural

outreach (generally more expensive) must be achieved.

Liberia and Sierra Leone are in the beginning stages of reviving credit union movements

which have been devastated by war. Clearly the development of these movements will

take years. In the best of scenarios, a thriving credit union movement serving an

increasing number of members through a financially viable apex organization offering a

variety of services takes 6 to 10 years to achieve. This assumes a calm economic

environment, a safe and sound legal and regulatory framework, and technical competency

at key levels of the movement.

VIII. Alternative Approaches and Strategies

There are barely six months remaining in the project. The introduction of alternative

approaches and strategies, if feasible, would be limited within such parameters.

Nevertheless, the alternatives which can be introduced in this period are those found in

this report’s recommendations. Their implementation will enhance the achievement of

the project’s objectives, as well as set the stage for follow-on interventions.

IX. Recommendations

The following are recommendations listed by the entity responsible for

implementing each. These are: ILCUF, WACUPP, NACCUG, CUA, LCUNA,

and NACCUSL. The recommendations are listed in priority order for each

entity29

.

A. ILCUF

1. The Irish League of Credit Unions Foundation, preferably in concert with the

EU, should begin to design a follow-on project (and identify necessary

funding) which will apply the lessons learned from this successful

intervention.

2. ILCUF should ensure that the credit union movements involved in WACUPP

provide maximum input to the design of further interventions.

B. WACUPP

29 The recommendations for WACUPP are categorized by overall project needs and themes.

31

1. There is a clear need in each of the four countries to bring the legal and

regulatory framework up to date. This would also include clarification

regarding supervision, including who is responsible and how is it funded.

2. Given the legal and regulatory needs, as well as other evidence of the need for

better knowledge on the part of national policy makers, each of the four

movements needs to develop and implement a policy advocacy strategy.

3. Cooperative departments (or their equivalents) should only be concerned with

registrations (validating cooperative nature) and not with licensing financial

operations.

4. Experience and information exchanges with other credit union movements in

the region are critical and must be continued.

5. Consideration should be given in the future to establishing a subset of

indicators for each country.

6. The project might have more impact if there was a pool of trainers for each

country. In this way, the apexes could deliver training for its credit unions.

Graduation Microfinance

7. The cost effectiveness of GMF should be investigated. The key variables to

study would include: comparative delinquency, CSA loan charges, and staff

time (i.e.; whether GMF requires more).

8. Records should be maintained as applies to GMF delinquency. These should

then be compared to rates for traditional loans by the credit union.

9. GMF should be monitored by the credit union board and management, as well

as the programme’s promoters.

10. GMF should be extended to more credit unions, especially in Sierra Leone

and Ghana. These should be well functioning credit unions with staff, a

computer and office space.

Social Performance Management

11. The SPM survey should be integrated with a financial and statistical survey,

with the financial being based on operating ratios and the statistical on

growth. Each of the variables being examined must be measurable. The

results of the survey should be analyzed and the key deficiency areas should

be identified as those which require technical assistance and training. A

follow-up survey would indicate the level of impact (success) of the

32

interventions. In this way, SPM would have a purpose of being integrated

into the credit union movement’s existing operations and a follow-up to the

results would be ensured.

12. Random selection of credit unions for the SPM survey is inappropriate. The

first such survey should cover as many credit unions as possible. Then, those

(possibly 20) which are closest to the mean should be identified as the sample

group for follow-on assessments.

Knowledge Management

13. All efforts should be made to identify support for the Steering Committee-

type exchanges.

14. The activities of the project hub should be more pro-active.

15. Efforts should continually be made to ensure that the website is user friendly.

16. The WACUPP website should ensure that all project documents, such as

manuals and policies, are posted.