China’s cosmetics market, 2010

January 2011Li & Fung Research Centre

2

p.7II. Competitive landscape

p.28V. Appendix

p.22IV. Snapshots of sub-sector performance

p.12III. Latest developments

p. 3I. Market Overview

In this issue:

I. Market Overview

3

4

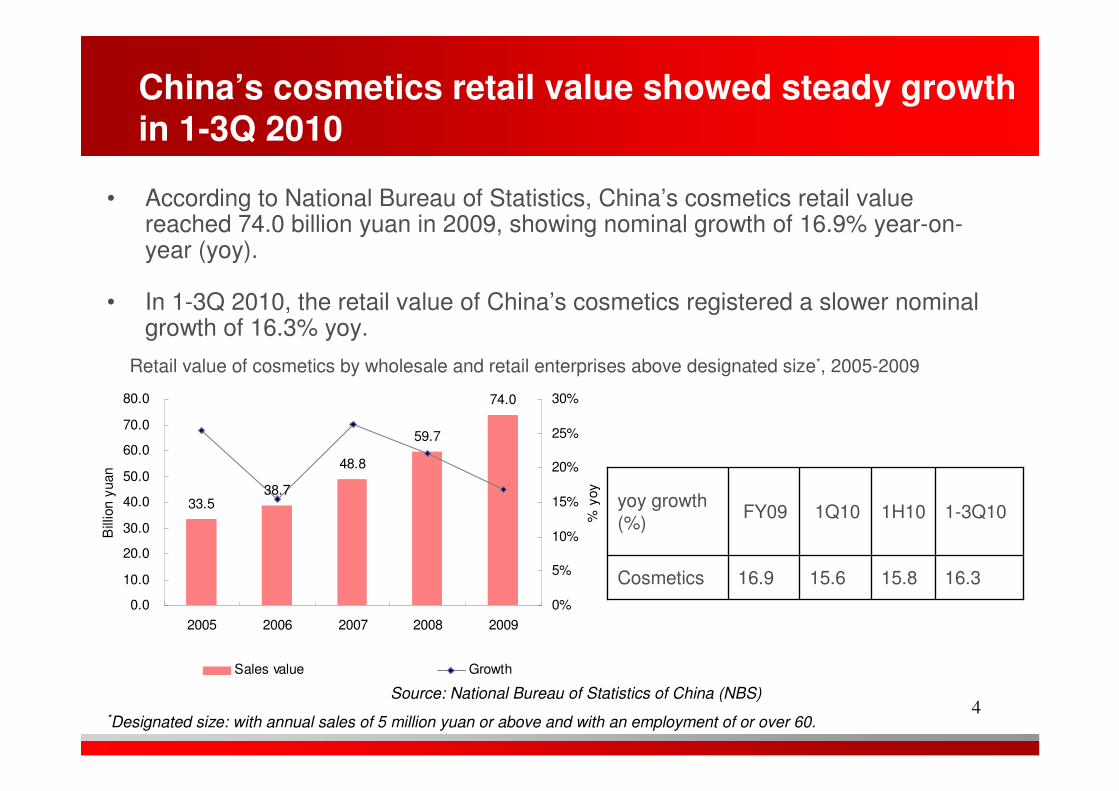

China’s cosmetics retail value showed steady growth in 1-3Q 2010

• According to National Bureau of Statistics, China’s cosmetics retail value reached 74.0 billion yuan in 2009, showing nominal growth of 16.9% year-on-year (yoy).

• In 1-3Q 2010, the retail value of China’s cosmetics registered a slower nominal growth of 16.3% yoy.

Retail value of cosmetics by wholesale and retail enterprises above designated size*, 2005-2009

33.538.7

48.8

59.7

74.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2005 2006 2007 2008 2009

Bill

ion y

uan

0%

5%

10%

15%

20%

25%

30%

% y

oy

Sales value Growth

16.315.815.616.9Cosmetics

1-3Q101H10 1Q10 FY09yoy growth (%)

Source: National Bureau of Statistics of China (NBS)

*Designated size: with annual sales of 5 million yuan or above and with an employment of or over 60.

5

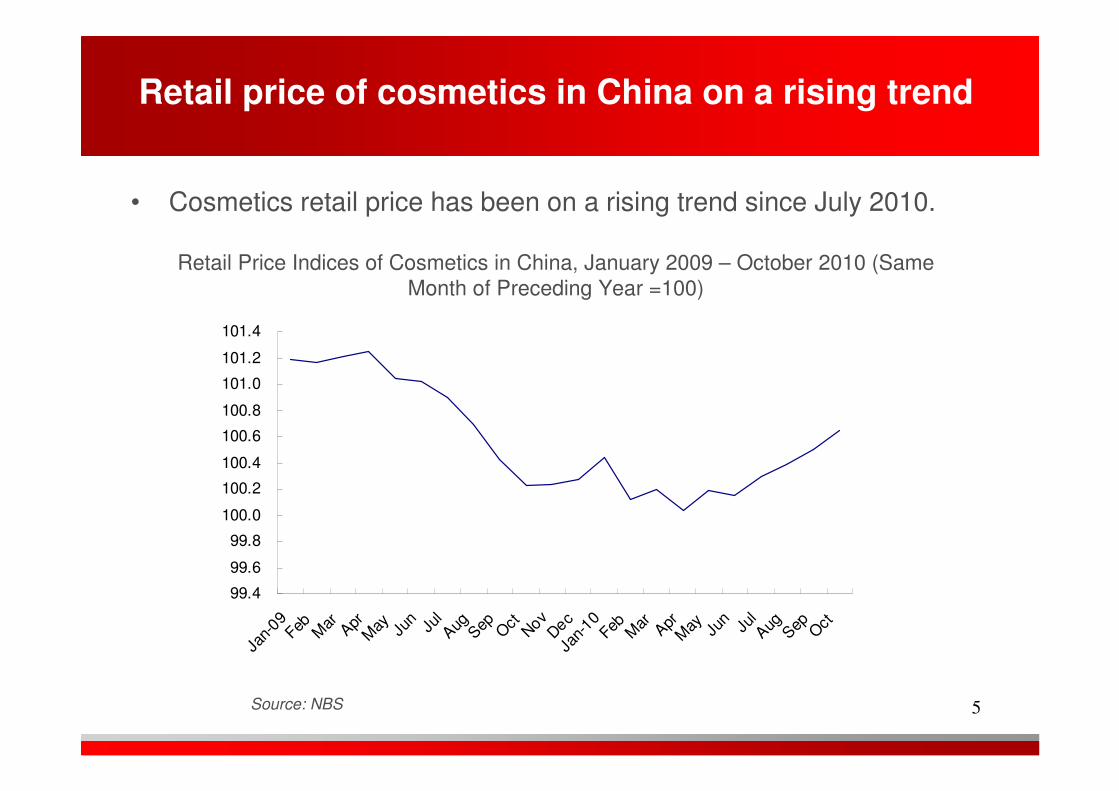

Retail price of cosmetics in China on a rising trend

Retail Price Indices of Cosmetics in China, January 2009 – October 2010 (Same

Month of Preceding Year =100)

Source: NBS

• Cosmetics retail price has been on a rising trend since July 2010.

99.4

99.6

99.8

100.0

100.2

100.4

100.6

100.8

101.0

101.2

101.4

Jan-

09Feb M

ar Apr

May Ju

nJu

lA

ugS

ep OctN

ovD

ecJa

n-10Feb M

ar Apr

May Ju

nJu

lA

ugS

ep Oct

6

• Although retail price has been on a rising trend, industry players said that it has lagged behind the cost increase.

• Increase in costs such as rental, labor, logistics, advertisement, and slotting fee etc. are exerting heavy pressure on cosmetics enterprises.

• Many cosmetics players, especially those with poorer brand equity, have witnessed their profit margin eroding.

Increasing margin pressure on cosmetics

enterprises

II. Competitive landscape

7

8

Foreign players have a strong foothold in the

mid-range to high-end segments

• Comparatively, foreign players have a more extensive brand portfolio than domestic players. (See Appendix)

• Foreign players have a strong foothold in the mid-range to high-end segments.

• China has become one of the most important markets for many foreign cosmetics companies.

– Greater China is the second largest market for Procter & Gamble, after the North American market. According to Access Asia, the sales of P&G in China reached 13.23 billion yuan in 2009, with a market share of 19%.

– L’Oréal International sees China as its major growth engine: Garnierrecorded a sales growth rate of 61.2% yoy in China in 2009; L’Oréal Paris recorded 25.5% yoy growth in China market’s sales in 2009.

9

Foreign enterprises have acquired a number of renowned domestic brands

• As a shortcut to acquire resources such as brand equity, local connections and distribution channels, a number of foreign cosmetics players have been actively exploring merger and acquisitions (M&As) opportunities. A number of well-known local brands were acquired by foreign brands over the past years.

• Homegrown cosmetics brands that had been acquired by foreign companies:

– Acquisition of Dabao (大寳) by Johnson & Johnson in 2008– Acquisition of C-Bons (絲寳) by Beiersdorf in 2007– Acquisitions of Yue-sai (羽西) and Mininurse (小護士) by L’Oréal in

2004

• In December 2010, Coty Inc., one of the leading global beauty companies, had agreed to acquire a majority stake (~400 million USD) in domestic skincare group TJoy Holdings Ltd (丁家宜). Theacquisition is expected to close in January 2011.

10

Domestic brands are more popular in lower-end segments

• Domestic brands generally priced lower and target the mass and lower-end segments.

• They have less extensive brand portfolio compared with foreign counterparts. (See Appendix)

• Though generally weaker in brand building and supply chain management, a number of domestic players have strived hard to move up the value ladder.

• Some are developing new brands to target higher-income consumers.

– e.g. the launch of Herborist (佰草集) and ShanghaiVive (雙妹) by

Shanghai Jahwa co. Ltd (上海家化).

11

Many new players are tapping the market

• An increasing number of retailers in China such as Wal-Mart, Watsons, Sephora and Sasa have launched private label cosmeticsproducts in recent years to improve profitability.

• Brands from other industries also jump on the bandwagon to offer cosmetics products.

– For example, Swedish apparel brand H&M launched a new line of

Ecocert certified organic-ingredient-based skin care products in 2010,

including shower gel, body scrub, moisturizer, hand cream and lip

balm etc.

– Fujifilm introduced its skincare products (Astalift) to mainland China

and Hong Kong markets in 2010. The brand Astalift is also available in

Taobao Mall, one of China’s most popular online shopping platforms.

III. Latest developments

12

13

Department stores, supermarkets and hypermarkets remained the major distribution channels

• According to Access Asia, department stores(56.2%), hypermarketsand supermarkets (20.2%) were the major distribution channels for cosmetics and toiletries* by sales in China in 2009.

• Some other emerging channels that are gaining popularity: – Professional stores

Watsons, Sasa, Sephora and Cosmart (歌詩瑪)

– Beauty parlors

Herborist SPA (佰草集漢方SPA), Chlitina (克麗緹娜) and Natural

Beauty SPA (自然美SPA生活舘)– Online retailing platforms

strawberrynet.com, Sasa.com, www.sephora.cnProfessional online stores

Joyo Amazon

Taobao mall (http://beauty.tmall.com/)

Integrated B2C online retailing

platforms

L’Oréal, DHC, Lancôme, Estée Lauder, Clinique,

Biorthem

Corporate websites

• Many players have opted for multi-channel operations *Include Baby Care, Bath & Shower, Deodorants, Hair Care, Make-up and Colour cosmetics, Men’s Toiletries, Oral Hygiene,

Perfumes & Fragrances, Skin Care and Sun Care.

14

• Sephora, which has already established presence in more than 20 cities including Shanghai, Beijing and Tianjin, had planned to open 100 stores by the end of 2010. It has begun to expand to many 2nd- or 3rd-tier cities such as Wuxi, Wenzhou, Changsha and Changshu.

• Management of Sasa said in 2010 that it planned to increase the store number to 100 in two and half years.

• Watsons, the leading health and beauty retail chain in Asia, hasopened more than 700 outlets in more than 100 cities of mainland China as of December 2010. Watsons aims to have 1,000 outlets by the end of 2011, covered more than 100 cities of mainland China.

Cosmetics retailers are accelerating their penetration into China

15

Massive advertising by cosmetics companies

• According to CTR, the cosmetics and toiletries industry was the biggest spender (67.1 billion yuan), during 1-3Q 2010 on advertising in China when compared to other industries.

• Cosmetics players have spent huge sums of money on advertising in China. According to CTR, P&G was the biggest spender (25.0 billion yuan) on advertising in China during 1-3Q 2010, followed by LO’réal (9.1 billion yuan) and Unilever (8.3 billion yuan).

– P&G has been the biggest spender at the annual auction for primetime advertising slots of the China Central Television (CCTV) for the past few years. Advertising on China’s largest national television network enables P&G to promote brand awareness.

– Thus far, celebrity endorsement is one of the most popular methods for players to create noise in the market.

16

Male grooming market is growing fast

• The male grooming market is growing very fast and still has much untapped potential. According to HKTDC, men’s cosmetics accounted for 12.7% of the total cosmetics market in 2008. The segment is expected to grow exponentially for the next few years.

• The sales of male specific skincare products of brands such as Nivea, L’Oréal, Biotherm and Garnier etc has been growing rapidly.

• LO’réal reported that sales in men’s skincare products in China roseby 27% in 2009 and the company expected it to increase by 40% in 2010, five times the increase of women’s skincare products.

• Domestic companies such as TJoy (丁家宜), Bawang (霸王), GF (高夫), Softto (索芙特) and Inoherb (相宜本草) etc. are increasingly keen to offer cosmetics for men as well.

17

More players tap into the cosmeceuticals market

• Many players (including pharmaceutical companies) have introduced cosmeceuticals in the past few years.

• Companies such as Beijing Tongrentang (北京同仁堂), Shanghai Jahwa (上海家化), Jiangsu Longliqi (江蘇隆力奇),Yunnan Baiyao (雲南白藥), China Shenghuo Pharmaceutical (昆明聖火藥業), Herborn(本草堂),Herborist (佰草集), Inoherb (相宜本草) and Shiseido havetapped the cosmeceuticals market.

• Distribution channels for cosmeceuticals include mainly drug stores, dispensary chains and counters in department stores.

18

Demand for natural and organic cosmetics is growing

• Demand for natural and organic products is growing amid increasing awareness of sustainability.

• Aveda, Origins, Yves Rocher, Clarins, Sisley, Jurlique, and L’Occitane are some well-known brands that offer natural and organic ingredient-based cosmetics products.

19

More stringent regulations on cosmetics

• The State Food and Drug Administration (SFDA) issued the Regulations on Naming of Cosmetics (化妝品命名規定), which was effective from February 2010.

– Wordings, such as names of well-known traditional Chinese herbalists

(e.g. Huatuo華佗, Bianque扁鵲), are prohibited. Besides, the

products should not include wordings such as “anti bacteria”, “detox”,

“anti-allergy”, “fat burning” and “truly natural” in their names.

• Implemented by China’s General Administration of Quality Supervision, Inspection and Quarantine (AQSIQ), the Instruction for Use of Products of Consumer Interest – General Labeling of Cosmetics (消費者使用説明- 化妝品通用標簽 ) was effective from July 2010.

– Cosmetics companies are required to display detailed information

such as ingredients, expiry date etc on the labeling.

20

• Chinese tourists spent a fairly large proportion on shopping (32%), as compared to food (12%) and accommodation (11%). Cosmetics are top on their buying list.

• With increasing income, Renminbi appreciation against US dollar and easing travel restrictions, many Chinese consumers shop forcosmetics products abroad.

• Luxury cosmetics products in mainland are generally more expensive than that in overseas markets. Currently, a consumption tax of 30% is levied on luxury and high-end cosmetics in China. Mainland tourists like to travel abroad to purchase cosmetics due to cheaper price and more product varieties.

• Please refer to our newsletter China’s Outbound Tourism : “http://www.lifunggroup.com/eng/knowledge/research/china_dis_issue75.pdf” for more information.

Buying cosmetics products abroad is popular

21

• Multi-functional products (e.g. color cosmetics with skincare function, BB Cream etc.) are gaining popularity.

• More players now try to incorporate advanced biotechnologies in new product developments, e.g. sulphate-free shampoo.

• Kids’ cosmetics market is still underdeveloped. Major players include Frog Prince (青蛙王子), Coati (小浣熊), Mentholatum, Yumeijing (鬱美淨) and Johnson & Johnson.

Other trends to watch

IV. Snapshots of sub-sector performance

22

23

Background

• The China National Commercial Information Centre (CNCIC) conducts monthly survey to around 200 major department stores* in China to study the performance of different cosmetics sub-sectors.

• In this newsletter, performance of 5 sub-sectors is examined: – Shampoos and conditioners

– Other hair care products

– Skincare products

– Color cosmetics

– Fragrances

*Note: It is noteworthy that the CNCIC data covers sales in major department stores only. Retailers of other formats such as specialty stores are growing in popularity. The actual overall market share of cosmetics brands may deviate from the CNCIC data.

24

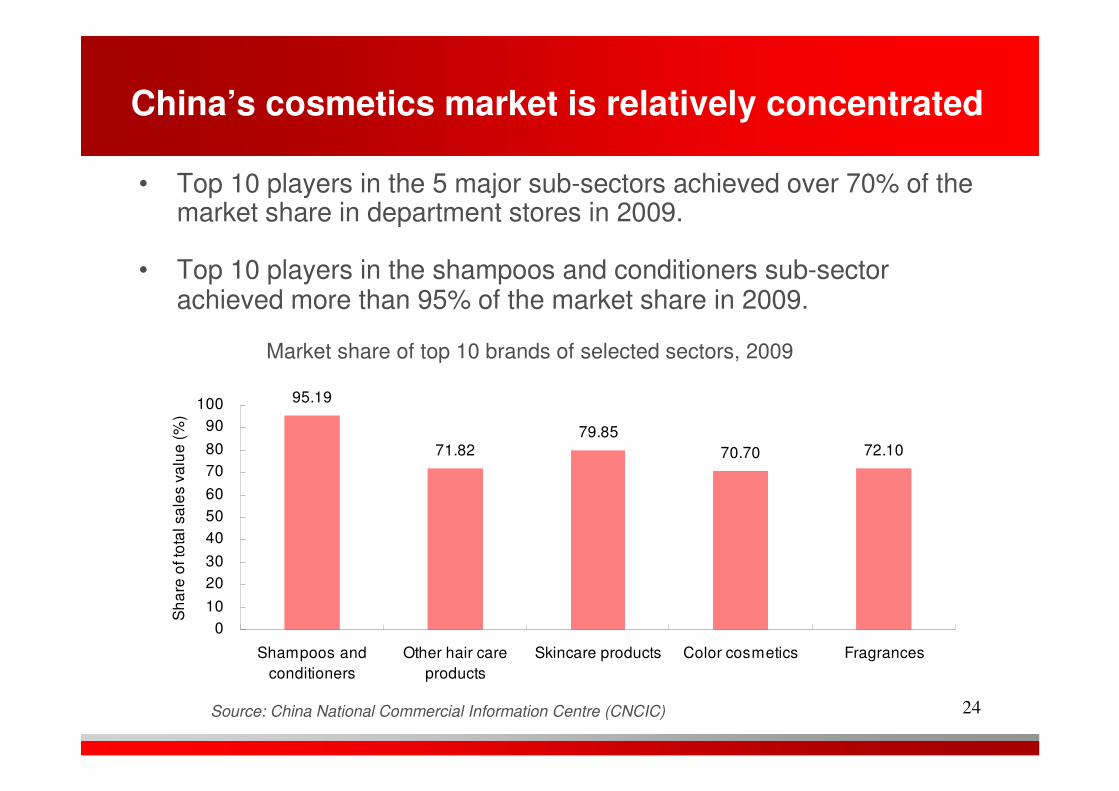

China’s cosmetics market is relatively concentrated

• Top 10 players in the 5 major sub-sectors achieved over 70% of the market share in department stores in 2009.

• Top 10 players in the shampoos and conditioners sub-sector achieved more than 95% of the market share in 2009.

Source: China National Commercial Information Centre (CNCIC)

Market share of top 10 brands of selected sectors, 2009

95.19

71.8279.85

70.70 72.10

0

10

20

30

40

50

60

70

80

90

100

Shampoos and

conditioners

Other hair care

products

Skincare products Color cosmetics Fragrances

Sh

are

of to

tal sa

les v

alu

e (

%)

25

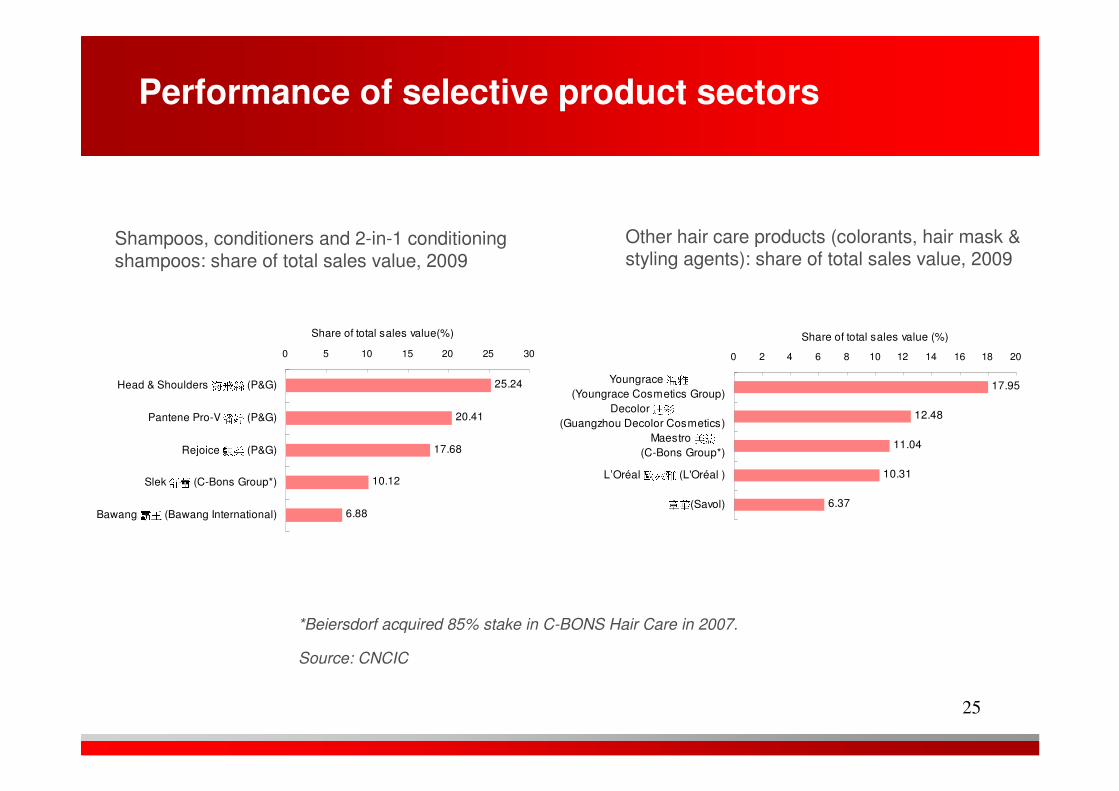

Performance of selective product sectors

25.24

20.41

17.68

10.12

6.88

0 5 10 15 20 25 30

Head & Shoulders 海飛絲 (P&G)

Pantene Pro-V 潘婷 (P&G)

Rejoice 飄柔 (P&G)

Slek 舒蕾 (C-Bons Group*)

Bawang 霸王 (Bawang International)

Share of total sales value(%)

Shampoos, conditioners and 2-in-1 conditioning shampoos: share of total sales value, 2009

*Beiersdorf acquired 85% stake in C-BONS Hair Care in 2007.

Source: CNCIC

17.95

12.48

11.04

10.31

6.37

0 2 4 6 8 10 12 14 16 18 20

Youngrace 溫雅(Youngrace Cosmetics Group)

Decolor 迪彩(Guangzhou Decolor Cosmetics)

Maestro 美濤(C-Bons Group*)

L’Oréal 歐萊雅 (L'Oréal )章華(Savol)

Share of total sales value (%)

Other hair care products (colorants, hair mask & styling agents): share of total sales value, 2009

26

Skin care products: share of total sales value, 2009

Source: CNCIC

Performance of selective product sectors (Cont’d)

19.02

17.98

16.22

7.96

5.31

0 2 4 6 8 10 12 14 16 18 20

Olay 玉蘭油 (P&G)

L’Oréal 歐萊雅 (L'Oréal )

Aupres 歐珀萊 (Shiseido)

Lancôme 蘭蔻 (L'Oréal )

Estée Lauder 雅詩蘭黛 (Estée Lauder)

Share of total sales value (%)

27.20

12.62

6.13

5.79

4.87

0 5 10 15 20 25 30

Maybelline 美寶蓮 (L'Oréal )

L'Oréal 歐萊雅 (L'Oréal )

Aupres 歐珀萊 (Shiseido)

Christian Dior 迪奧 CD

(Christian Dior (China) Fragrance &

Olay 玉蘭油 (P&G)

Share of total sales value (%)

Color cosmetics: share of total sales value, 2009

27

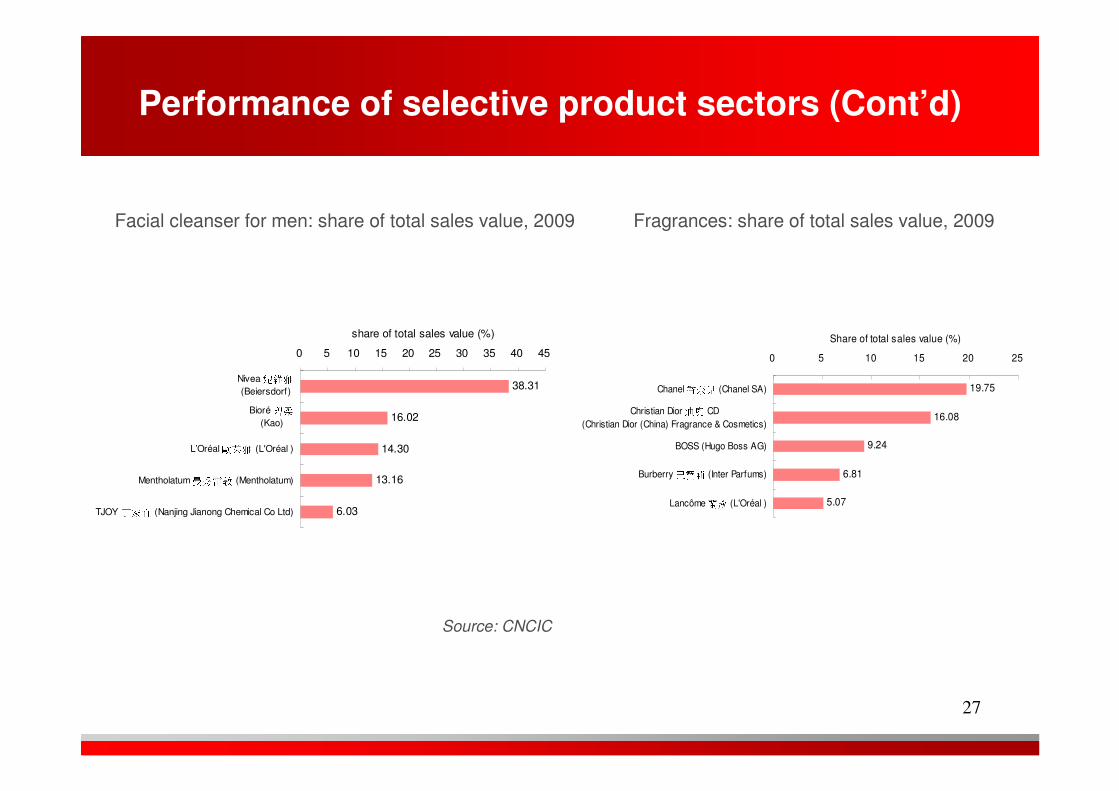

Facial cleanser for men: share of total sales value, 2009

Source: CNCIC

Performance of selective product sectors (Cont’d)

38.31

16.02

14.30

13.16

6.03

0 5 10 15 20 25 30 35 40 45

Nivea 妮維雅(Beiersdorf)

Bioré 碧柔(Kao)

L’Oréal 歐萊雅 (L'Oréal )

Mentholatum 曼秀雷敦 (Mentholatum)

TJOY 丁家宜 (Nanjing Jianong Chemical Co Ltd)

share of total sales value (%)

19.75

16.08

9.24

6.81

5.07

0 5 10 15 20 25

Chanel 香奈兒 (Chanel SA)

Christian Dior 迪奧 CD

(Christian Dior (China) Fragrance & Cosmetics)

BOSS (Hugo Boss AG)

Burberry 巴寳莉 (Inter Parfums)

Lancôme 蘭蔻 (L'Oréal )

Share of total sales value (%)

Fragrances: share of total sales value, 2009

V. Appendix

28

Foreign cosmetics enterprises and their major brands in China

Company Name Brands L’Oréal 歐萊雅 L’Oréal Paris 巴黎歐萊雅

Garnier 卡尼爾

Maybelline New York 美寶蓮紐約

L’Oréal Professional 歐萊雅專業美髮

Kérastase 卡詩

Lancôme 蘭蔻

Biotherm 碧歐泉

Helena Rubinstein HR 赫蓮娜

Kiehl’s

shu uemura 植村秀

Giorgio Armani 喬治 阿瑪尼

La Roche-Posay 理膚泉

Mininurse 小護士

Yue Sai 羽西

Vichy 薇姿

Matrix 美奇絲

Skinceuticals

P&G 寶潔 Head & Shoulders 海飛絲

Rejoice 飄柔

SK-II Pantene 潘婷

Olay 玉蘭油

Vidal Sasson 沙宣

Clairol Herbal Essences 伊卡璐

Wella 威娜

Camay 卡玫爾

Shiseido資生堂 Shiseido 資生堂

Shiseido Men資生堂男士

Clé de peau beauté 珂麗柏蒂

Revital 悅薇

UV White 優白

Anessa 安熱沙

Aupres 歐珀萊

Supreme Aupres 思魅歐珀萊

Urara 悠萊

Elixir 怡麗絲爾

Elixir Superieur怡麗絲爾優悅活顏

Melanreduce 臻白無瑕

Asplir 愛泊麗

Whitia 白娣顔

Selfit 珊妃

UNO 吾諾

PF-Cover 無瑕修顏

DQ 蒂珂

Shiseido Eudermine 紅色蜜露

Za 姬芮

Aqua Label 水之印

Be 彼嘉

Aquair 水之密語

Perfect 洗顔專科

Kuyura 可悠然

Super Mild 惠潤

Maquillage 心機彩妝

Tessera 欣香

Hand Cream 美潤護手霜

Handasui 肌水

Tsubaki 絲蓓綺

Pure & Mild 泊美

Shanghai Bouquet 上海花漪

Qi 綺怡

Zen 世紀禈香氛

Unilever 聯合利華 Vaseline 凡士林

Lux 力士

Dove 多芬

Hazeline 夏士蓮

Pond’s 旁氏

Clear 清揚

Rexona 舒耐

Johnson & Johnson 強生 Clean & Clear 可伶可俐

Neutrogena 露得清

Johnson’s Baby 強生嬰兒

Dabao 大寶*

Johnson’s body care 強生美肌

Estée Lauder 雅詩蘭黛

Estée Lauder 雅詩蘭黛

Aramis 雅男士

Clinique 倩碧

M.A.C. 魅可

La Mer 海藍之謎

Bobbi Brown 芭比波朗

Tommy Hilfiger 唐美希緋格

Donna Karan Cosmetics 唐娜凱倫

Beiersdorf 拜爾斯道夫

NIVEA 妮維雅

Nivea for men

La Prairie 莱珀妮

Eucerin Florena

C-Bons Hair Care**

Slek 舒雷

Sdew 風影

Hairsong 順爽

Maestro 美濤

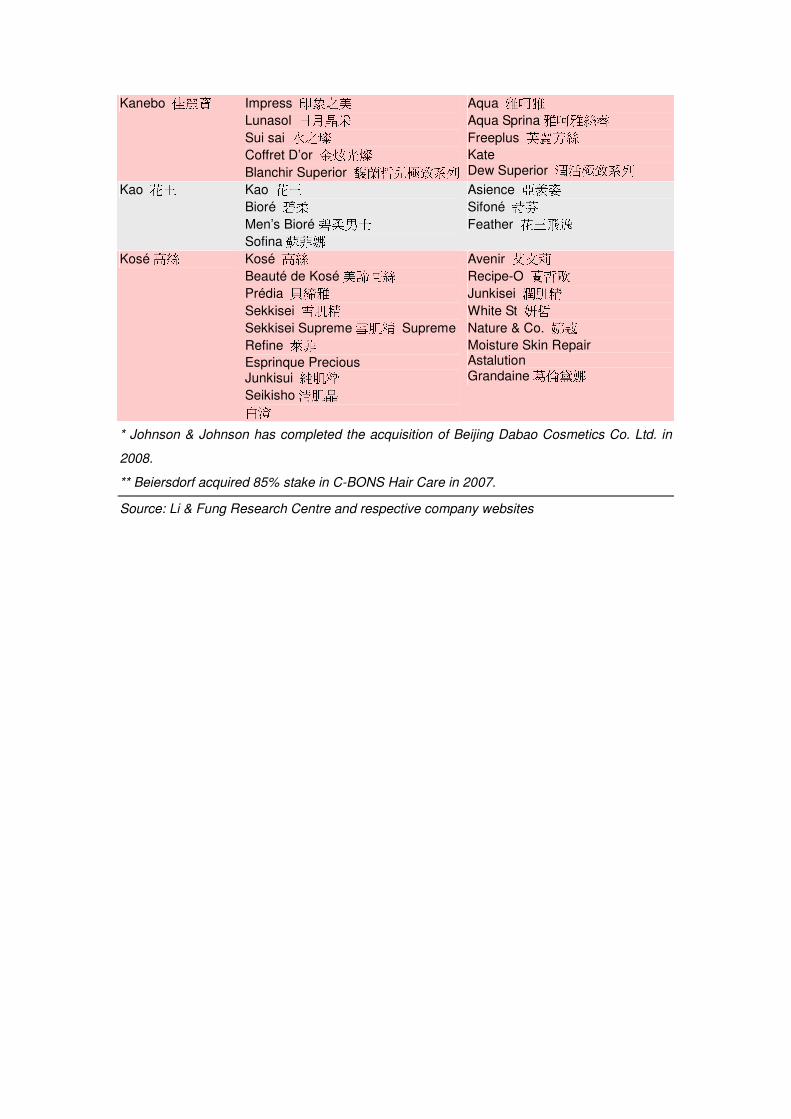

Kanebo 佳麗寶 Impress 印象之美

Lunasol 日月晶采

Sui sai 水之璨

Coffret D’or 金炫光燦

Blanchir Superior 馥蘭哲兒極致系列

Aqua 雅呵雅

Aqua Sprina雅呵雅絲睿

Freeplus 芙麗芳絲

Kate Dew Superior 潤活極致系列

Kao 花王 Kao 花王

Bioré 碧柔

Men’s Bioré碧柔男士

Sofina蘇菲娜

Asience 亞羨姿

Sifoné 詩芬

Feather 花王飛逸

Kosé高絲 Kosé 高絲

Beauté de Kosé美諦高絲

Prédia 貝締雅

Sekkisei 雪肌精

Sekkisei Supreme雪肌精 Supreme

Refine 萊菲

Esprinque Precious Junkisui 純肌粋

Seikisho清肌晶 白澄

Avenir 艾文莉

Recipe-O 蘭哲歐

Junkisei 潤肌精

White St 妍哲

Nature & Co. 娜蔻

Moisture Skin Repair Astalution Grandaine葛倫黛娜

* Johnson & Johnson has completed the acquisition of Beijing Dabao Cosmetics Co. Ltd. in

2008.

** Beiersdorf acquired 85% stake in C-BONS Hair Care in 2007.

Source: Li & Fung Research Centre and respective company websites

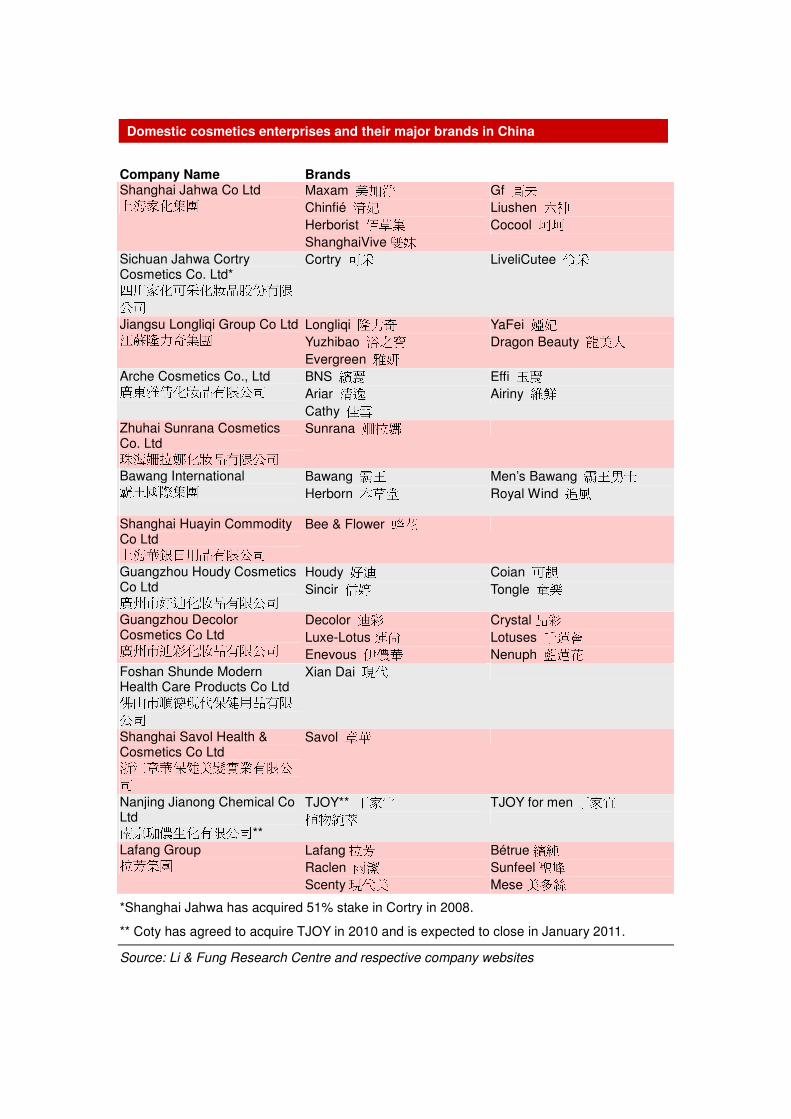

Domestic cosmetics enterprises and their major brands in China

Company Name Brands Shanghai Jahwa Co Ltd 上海家化集團

Maxam 美加淨

Chinfié 清妃

Herborist 佰草集

ShanghaiVive雙妹

Gf 高夫

Liushen 六神

Cocool 珂珂

Sichuan Jahwa Cortry Cosmetics Co. Ltd* 四川家化可采化妝品股份有限公司

Cortry 可采 LiveliCutee 伶采

Jiangsu Longliqi Group Co Ltd 江蘇隆力奇集團 Longliqi 隆力奇

Yuzhibao 浴之寶

Evergreen 雅妍

YaFei 婭妃

Dragon Beauty 龍美人

Arche Cosmetics Co., Ltd 廣東雅倩化妝品有限公司 BNS 繽麗

Ariar 清逸

Cathy 佳雪

Effi 玉麗

Airiny 維鮮

Zhuhai Sunrana Cosmetics Co. Ltd 珠海姍拉娜化妝品有限公司

Sunrana 姍拉娜

Bawang International 霸王國際集團

Bawang 霸王

Herborn 本草堂

Men’s Bawang 霸王男士

Royal Wind 追風

Shanghai Huayin Commodity Co Ltd 上海華銀日用品有限公司

Bee & Flower 蜂花

Guangzhou Houdy Cosmetics Co Ltd 廣州市好迪化妝品有限公司

Houdy 好迪

Sincir 信婷

Coian 可靚

Tongle 童樂

Guangzhou Decolor Cosmetics Co Ltd 廣州市迪彩化妝品有限公司

Decolor 迪彩

Luxe-Lotus蓮尚

Enevous 伊儂華

Crystal晶彩

Lotuses 千蓮薈

Nenuph 藍蓮花

Foshan Shunde Modern Health Care Products Co Ltd 佛山市順德現代保健用品有限公司

Xian Dai 現代

Shanghai Savol Health & Cosmetics Co Ltd 浙江章華保健美髮實業有限公司

Savol 章華

Nanjing Jianong Chemical Co Ltd 南京珈儂生化有限公司**

TJOY** 丁家宜 植物純萃

TJOY for men 丁家宜

Lafang Group 拉芳集團 Lafang拉芳

Raclen 雨潔

Scenty 現代美

Bétrue繽純

Sunfeel 聖峰

Mese美多絲

*Shanghai Jahwa has acquired 51% stake in Cortry in 2008.

** Coty has agreed to acquire TJOY in 2010 and is expected to close in January 2011.

Source: Li & Fung Research Centre and respective company websites

Li & Fung Research Centre

11/F, LiFung Tower, 868 Cheung Sha Wan Road, Kowloon, Hong Kong

Tel: 2300 2470 Fax: 2635 1598Email: [email protected]://www.lifunggroup.com/

For more information