0

Item 602A

Real Estate - Revision to UCRP and GEP Asset Allocation Benchmarks

Committee on Investments / Investment Advisory Committee

April 22, 2003

1

Recap of 3/4/03 meeting points

Pension funds/endowments/other tax-exempt investors, who invest in real estate, invest/target 5-9% of assets in public and/or private real estate

Real estate represents ~ 8% investment universe

Real estate’s historical total return and risk between U.S. stocks and bonds

Real estate has low cross-correlation with other asset classes = diversification benefits

Real estate has high % of total return in current cash yield – important for pension funds and endowments to meet cash obligations and needs

Real estate potential hedge against unanticipated inflation

Addition of real estate can improve portfolio return and lower risk under various investment scenarios

2

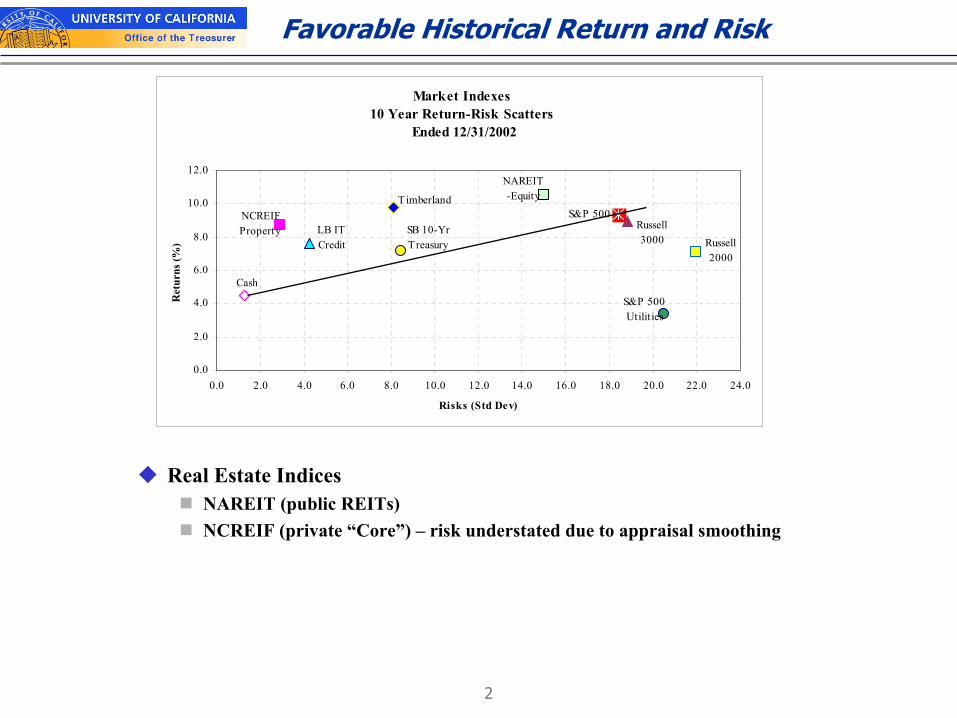

Favorable Historical Return and Risk

Real Estate IndicesNAREIT (public REITs)NCREIF (private “Core”) – risk understated due to appraisal smoothing

Market Indexes10 Year Return-Risk Scatters

Ended 12/31/2002

NCREIF Property

S&P 500Russell 3000 Russell

2000

S&P 500Utilit ies

LB ITCredit

SB 10-YrTreasury

Timberland

Cash

NAREIT-Equity

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.0 22.0 24.0

Risks (Std Dev)

Ret

urns

(%)

3

Public vs. Private Strategies

Public strategy (focus on publicly-traded REITs)Liquidity and real time pricingBenefits from public market oversight and transparencyLow transaction costsInstant diversificationEase of buy and sell decisionsGood alignment of investor and management interests

Private strategy (limited liability investment vehicles, such as limited partnerships, LLC’s, private REIT etc.)

Opportunity to take advantage of private market inefficienciesOpportunity to purchase assets not available publiclyLower correlations with stocks and bonds than public real estateEven better alignment of interests provided sponsor has invested significant portion of personal wealth Investor can have some influence on management’s major decisions

4

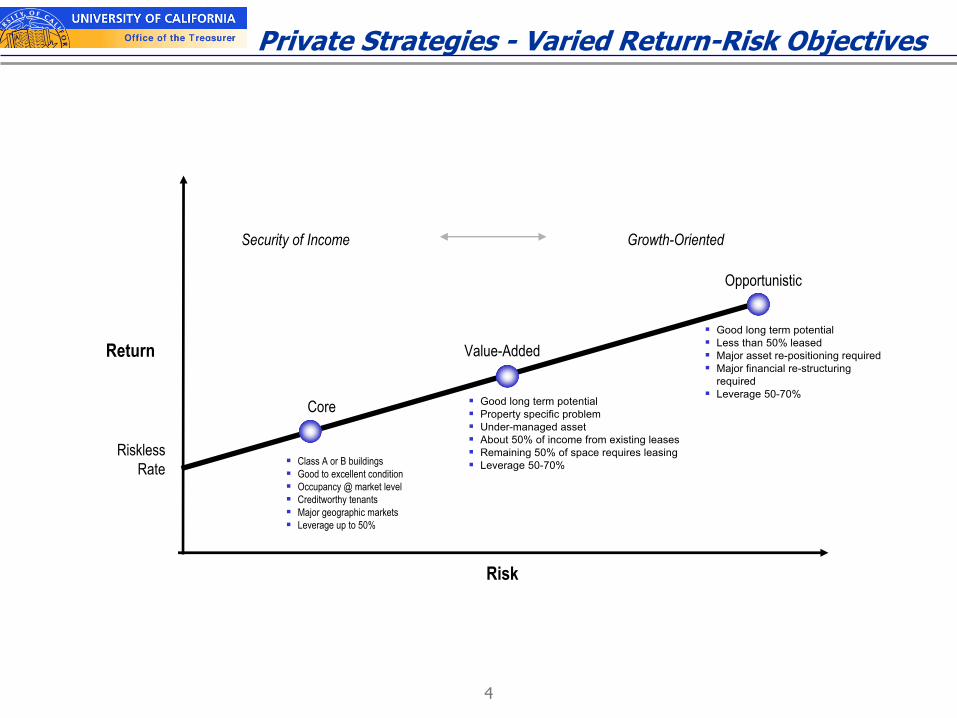

Private Strategies - Varied Return-Risk Objectives

Good long term potentialProperty specific problemUnder-managed assetAbout 50% of income from existing leases Remaining 50% of space requires leasingLeverage 50-70%

Good long term potentialLess than 50% leasedMajor asset re-positioning requiredMajor financial re-structuring requiredLeverage 50-70%

Security of Income Growth-Oriented

Risk

Return Value-Added

Opportunistic

RisklessRate Class A or B buildings

Good to excellent conditionOccupancy @ market level Creditworthy tenantsMajor geographic marketsLeverage up to 50%

Core

5

Recommended Real Estate Allocation

Total Real Estate: 5% UCRP and 5% GEP

Lower end of 5-9% among peers who invest in real estate

Sourced by reducing U.S. stock allocation target by 300 bps and fixed income by 200 bps

But the maximum permitted stock and fixed income %’s remain unchanged because real estate target allocation will take time to complete

Wilshire Associates supports recommendation

6

Total Portfolio if target benchmarks approved

UCRP Asset AllocationCurrent Policy Policy After Adding Real Estate

U.S. Equity 53% 50%Non-U.S. Equity 7% 7%Fixed Income 30% 28%TIPS 5% 5%Private Equity 5% 5%Real Estate 0% 5%

100% 100%

GEP Asset AllocationCurrent Policy Policy After Adding Real Estate

U.S. Equity 45% 42%Non-U.S. Equity 10% 10%Fixed Income 30% 28%TIPS 0% 0%Private Equity 10% 10%Absolute Return 5% 5%Real Estate 0% 5%

100% 100%

7

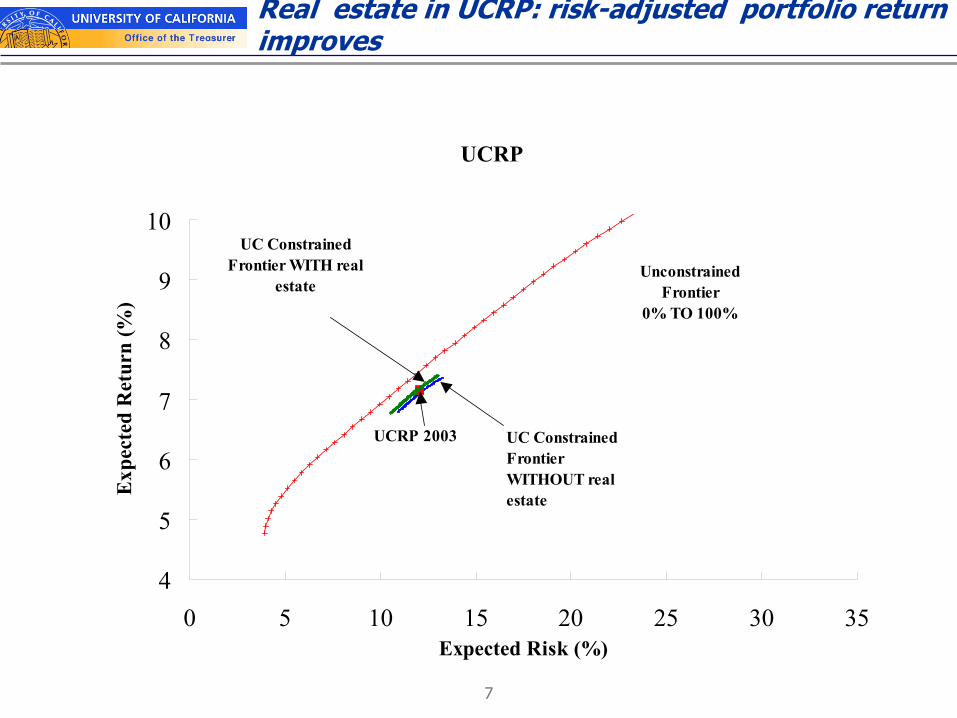

Real estate in UCRP: risk-adjusted portfolio return improves

UCRP

UCRP 2003

4

5

6

7

8

9

10

0 5 10 15 20 25 30 35Expected Risk (%)

Exp

ecte

d R

etur

n (%

)

UnconstrainedFrontier

0% TO 100%

UC ConstrainedFrontier WITH real

estate

UC Constrained Frontier WITHOUT real estate

8

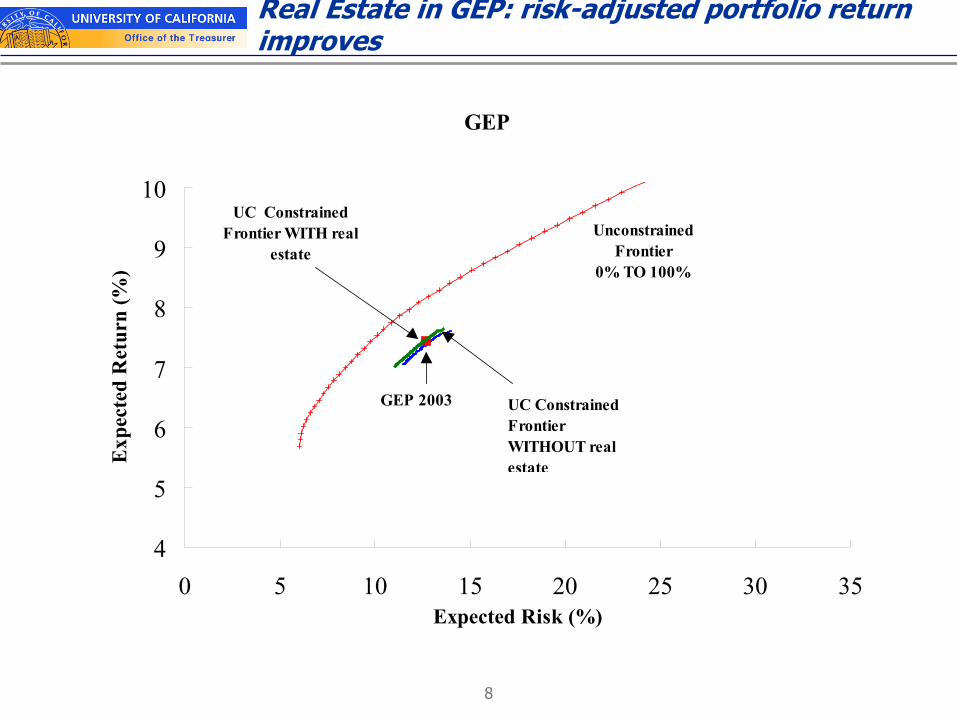

Real Estate in GEP: risk-adjusted portfolio return improves

GEP

GEP 2003

4

5

6

7

8

9

10

0 5 10 15 20 25 30 35Expected Risk (%)

Exp

ecte

d R

etur

n (%

)

UnconstrainedFrontier

0% TO 100%

UC ConstrainedFrontier WITH real

estate

UC Constrained Frontier WITHOUT real estate

9

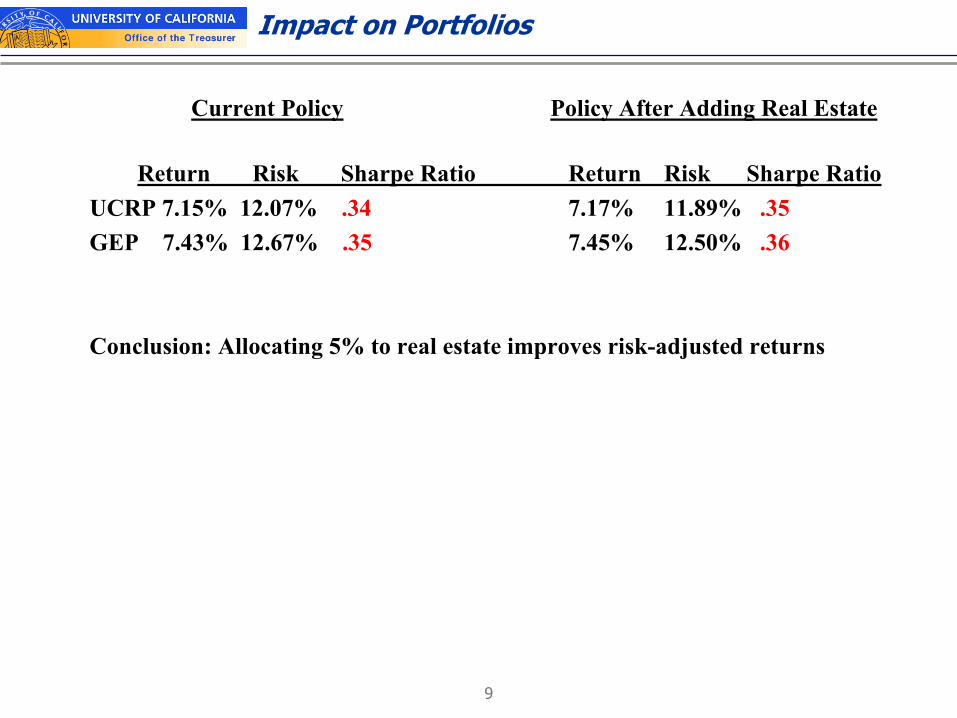

Impact on Portfolios

Current Policy Policy After Adding Real Estate

Return Risk Sharpe Ratio Return Risk Sharpe RatioUCRP 7.15% 12.07% .34 7.17% 11.89% .35GEP 7.43% 12.67% .35 7.45% 12.50% .36

Conclusion: Allocating 5% to real estate improves risk-adjusted returns

10

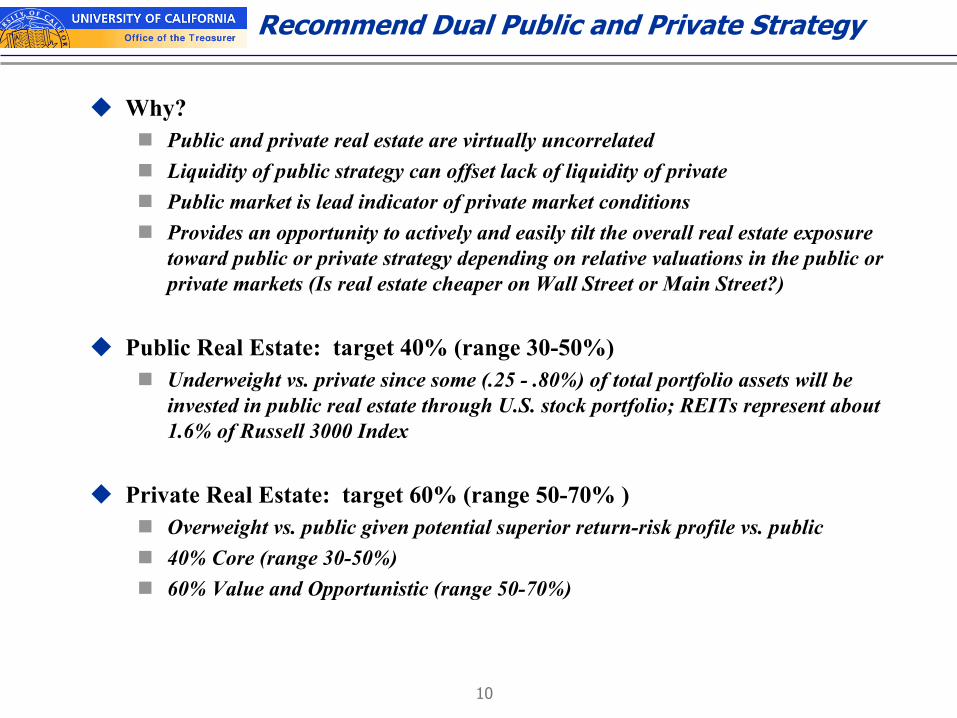

Recommend Dual Public and Private Strategy

Why?Public and private real estate are virtually uncorrelatedLiquidity of public strategy can offset lack of liquidity of privatePublic market is lead indicator of private market conditions Provides an opportunity to actively and easily tilt the overall real estate exposure toward public or private strategy depending on relative valuations in the public or private markets (Is real estate cheaper on Wall Street or Main Street?)

Public Real Estate: target 40% (range 30-50%)Underweight vs. private since some (.25 - .80%) of total portfolio assets will be invested in public real estate through U.S. stock portfolio; REITs represent about 1.6% of Russell 3000 Index

Private Real Estate: target 60% (range 50-70% )Overweight vs. public given potential superior return-risk profile vs. public40% Core (range 30-50%) 60% Value and Opportunistic (range 50-70%)

11

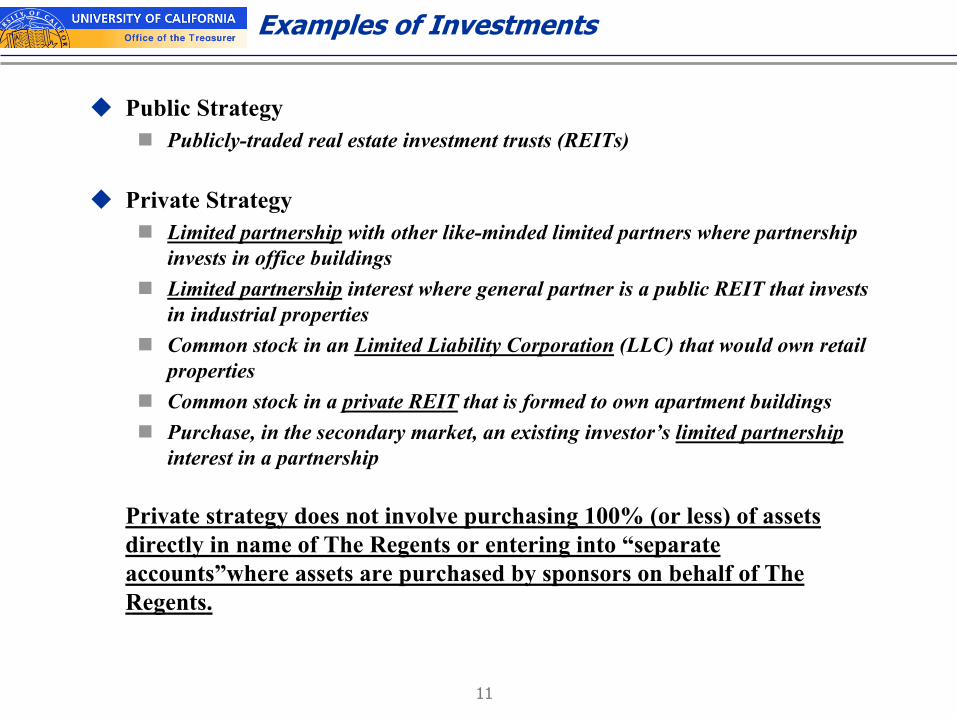

Examples of Investments

Public StrategyPublicly-traded real estate investment trusts (REITs)

Private Strategy Limited partnership with other like-minded limited partners where partnership invests in office buildings Limited partnership interest where general partner is a public REIT that invests in industrial propertiesCommon stock in an Limited Liability Corporation (LLC) that would own retail propertiesCommon stock in a private REIT that is formed to own apartment buildingsPurchase, in the secondary market, an existing investor’s limited partnershipinterest in a partnership

Private strategy does not involve purchasing 100% (or less) of assets directly in name of The Regents or entering into “separate accounts”where assets are purchased by sponsors on behalf of TheRegents.

12

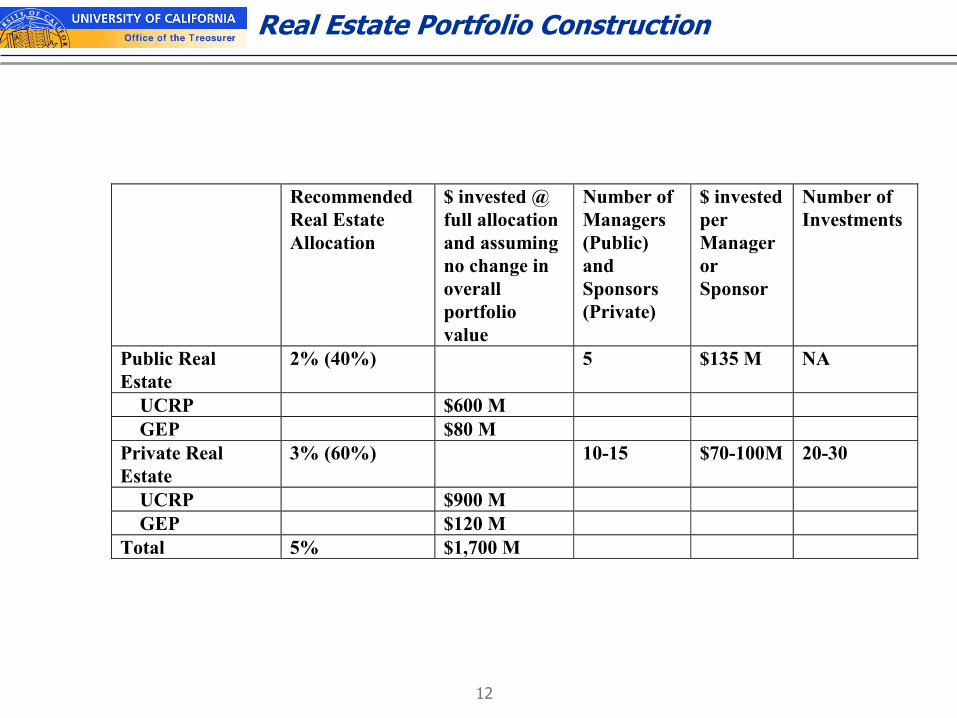

Real Estate Portfolio Construction

Recommended Real Estate Allocation

$ invested @ full allocation and assuming no change in overall portfolio value

Number of Managers (Public) and Sponsors (Private)

$ invested per Manager or Sponsor

Number of Investments

Public Real Estate

2% (40%) 5 $135 M NA

UCRP $600 M GEP $80 M Private Real Estate

3% (60%) 10-15 $70-100M 20-30

UCRP $900 M GEP $120 M Total 5% $1,700 M

13

Item 602B

Real Estate Investment Process and Portfolio Guidelines

Committee on Investments / Investment Advisory Committee

April 22, 2003

14

Real Estate Consultant

Russell Real Estate Advisors retained conditional on Regents’ approval of investing in real estate

Established in 1971; office located in San Diego

Experienced team of 12 professionals with many years of service w/ firm

Good blend of mid/large sized and public/private client base with real estate assets totaling $35 billion

Extensive property market knowledge and database

Strong research capabilities

Services: portfolio construction and strategy advice, due diligence services, portfolio analytics, program oversight, and investment structuring

Wilshire Associates and Russell support the recommended investment process and guidelines

15

Implementation of Public and Private Strategy

Investment Philosophy

Investment Return Objective

Investment Process

Portfolio Construction (reviewed in Open Session Item)

Portfolio Guidelines

Portfolio Benchmarks

16

Public Strategy – Investment Philosophy/Objective

Investment PhilosophyInvest primarily for the long term

Focus on larger, more liquid securities

Invest in companies with sustainable cash flow that can grow andsupport the dividend pay-out

Invest in companies that act in shareholder’s interests

Reasonable valuations with focus on Net Asset Value (private market value) per share

Investment Return Objective5% real rate of return

17

Public Strategy – Process

Hire external managers selected thorough due diligence process focusing on the following criteria:

ExperienceClear and sustainable strategyTrack record of superior performance and relatively low volatility with little or no leverageRisk management procedures and controlsClient service and operations, including researchTrading capabilities

Detailed due diligence process similar to that used for absolute return strategy

Hire independent consultant to perform parallel due diligence processStaff and consultant must concur prior to manager selection

18

Public Strategy Process

Report to Investment Committee and Investment Advisory Committee

Reject

Reject

Screen manager to meet minimum criteriaReject

RejectInitial consideration by Treasurer’s Office

Consultant Initial Review Treasurer’s Office Further Review

Reject Accept Reject/Track

Prioritize for Due Diligence

Consultant Due Diligence Treasurer’s Office Due Diligence

Review by Treasurer’s Office Real Estate CommitteeCo

Manager contract negotiated and investment made

Reject Reject/Track

Approval byTreasurer’s Office

19

Public Strategy – Guidelines/Benchmark

Minimum 90% must be in benchmark; up to 10% in other G-10 countries

No property type may exceed 2 X its benchmark weight

Individual security not more than 3 X its benchmark weight

Individual security not to exceed 5% of equity market cap

No investment with single manager can represent more than 25% ofthe public real estate portfolio

No investment with any single manager may exceed 25% of that manager’s total assets under management

Benchmark – Wilshire REIT Index

20

Private Strategy – Investment Philosophy/Objective

Investment PhilosophyInvest for the long term, although select sponsors with a sell discipline

Emphasize alignment of interest by requiring meaningful sponsor co-investment and not merely asset accumulation

Invest through limited liability investment vehicles

Appropriate governance mechanisms

Investment Return Objective5% real rate of return

21

Private Strategy – Process

Hire sponsors selected thorough due diligence process focusing on the following criteria:

ExperienceClear and sustainable strategyTrack record of superior performance and relatively low volatilityRisk management procedures and controlsClient service and operations, including researchAcquisition/Disposition/Asset Management capabilities

Detailed due diligence process similar to that used for private equity strategy

Hire independent consultant to perform parallel due diligence processStaff and consultant must concur prior to manager selection

22

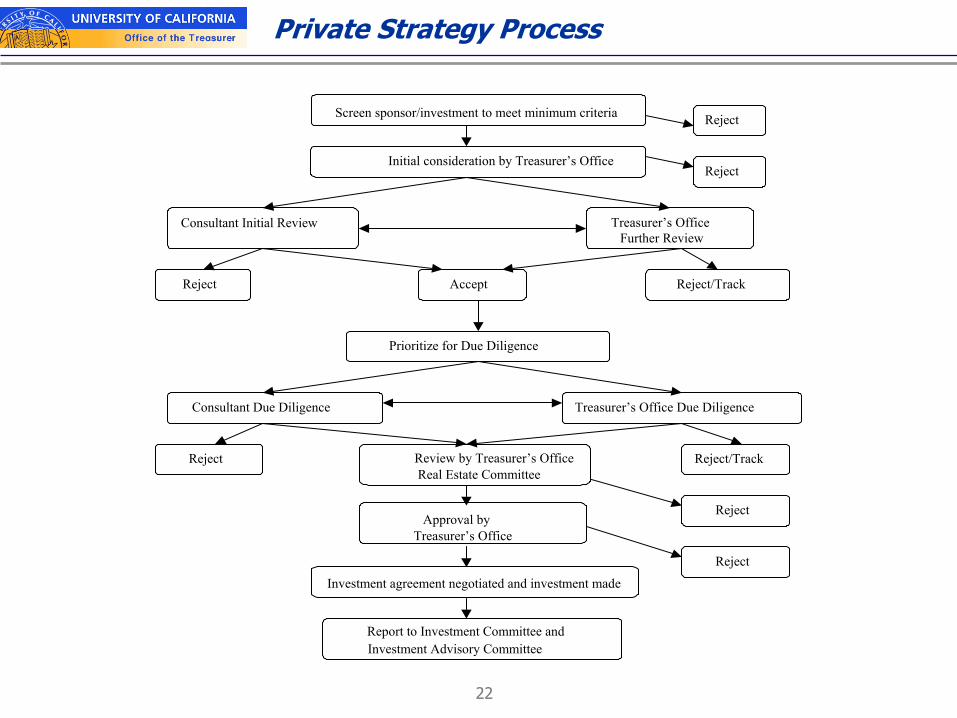

Private Strategy Process

Report to Investment Committee and Investment Advisory Committee

Reject

Reject

Screen sponsor/investment to meet minimum criteria Reject

RejectInitial consideration by Treasurer’s Office

Consultant Initial Review Treasurer’s Office Further Review

Reject Accept Reject/Track

Prioritize for Due Diligence

Consultant Due Diligence Treasurer’s Office Due Diligence

Review by Treasurer’s OfficeReal Estate Committee

Investment agreement negotiated and investment made

Reject Reject/Track

Approval by Treasurer’s Office

23

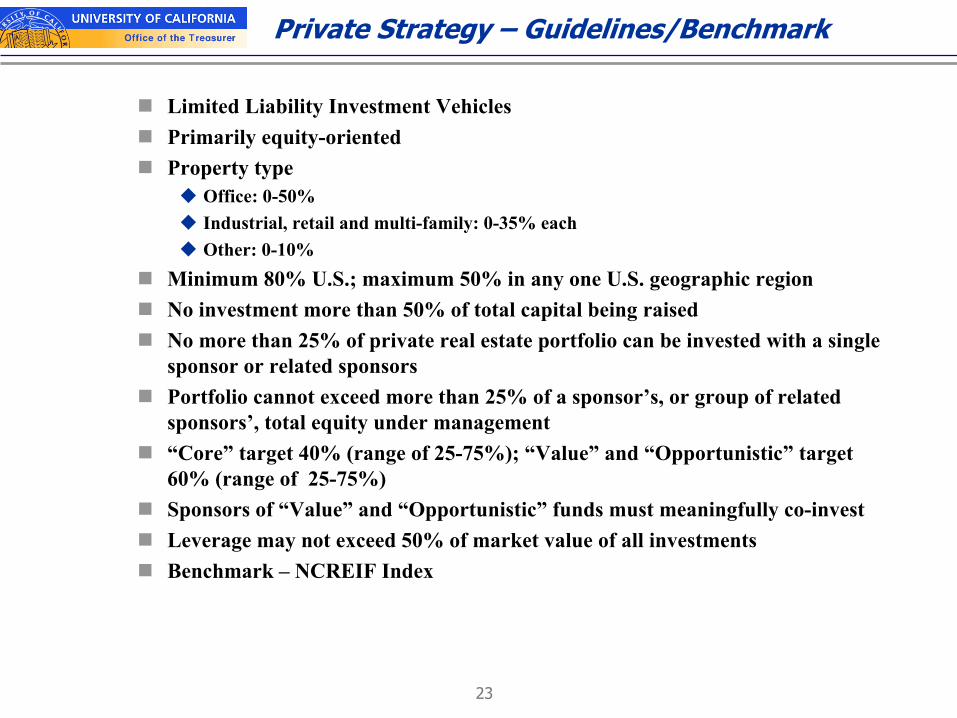

Private Strategy – Guidelines/Benchmark

Limited Liability Investment VehiclesPrimarily equity-orientedProperty type

Office: 0-50%Industrial, retail and multi-family: 0-35% eachOther: 0-10%

Minimum 80% U.S.; maximum 50% in any one U.S. geographic regionNo investment more than 50% of total capital being raised No more than 25% of private real estate portfolio can be invested with a single sponsor or related sponsorsPortfolio cannot exceed more than 25% of a sponsor’s, or group of related sponsors’, total equity under management“Core” target 40% (range of 25-75%); “Value” and “Opportunistic” target 60% (range of 25-75%)Sponsors of “Value” and “Opportunistic” funds must meaningfully co-investLeverage may not exceed 50% of market value of all investmentsBenchmark – NCREIF Index

24

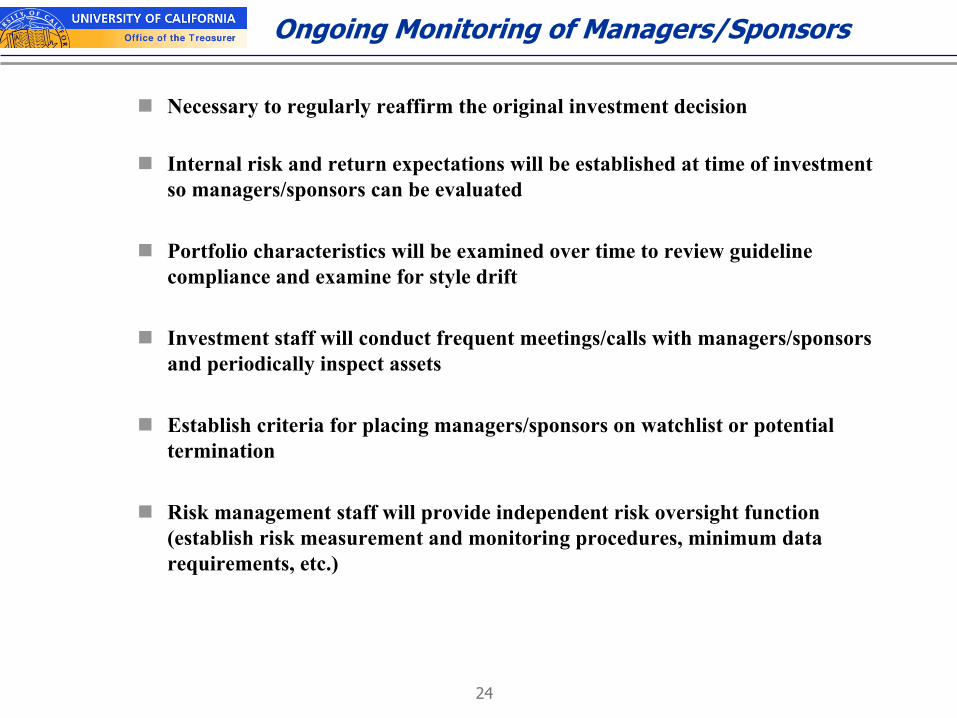

Ongoing Monitoring of Managers/Sponsors

Necessary to regularly reaffirm the original investment decision

Internal risk and return expectations will be established at time of investment so managers/sponsors can be evaluated

Portfolio characteristics will be examined over time to review guideline compliance and examine for style drift

Investment staff will conduct frequent meetings/calls with managers/sponsors and periodically inspect assets

Establish criteria for placing managers/sponsors on watchlist or potential termination

Risk management staff will provide independent risk oversight function (establish risk measurement and monitoring procedures, minimum data requirements, etc.)

![Australian Centre for Education (ACE) for All Campuses.pdf · GEP Beginners 2 [j] GEP 1, arious GEP Various GEP6 arious GEP 7A, 7B, 8 [Various] GEP 9A, 9B, 10 Various GEP ITA, 11B](https://static.documents.pub/doc/80x56/5fa44d495ec9ac37f767e1bf/australian-centre-for-education-ace-for-all-campusespdf-gep-beginners-2-j.jpg)