ABCD

KEY INDIRECT TAX

ISSUES IMPACTING THE

INDIAN NATURAL GAS

SECTOR

KPMG

February 2015

This report contains 16 pages

© 2015 KPMG, an Indian Partnership and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss

entity. All rights reserved.

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

i

© 2015 KPMG. All rights reserved.

TABLE OF CONTENTS

I Purpose of this report 2

II Summary 2

III Indirect Tax challenges under Current Regime 2

A. Service tax on cash calls and reimbursements 2 B. Blockage of Service tax paid on Services consumed in E&P Activities 4

C. Customs exemption on import of Liquefied Natural Gas (LNG) 5 D. Setting up of infrastructure – CENVAT Credit denial 5

E. Value Added Tax and service tax on Sale and Transport of Gas 7 F. Inter-state supplies to customers – Liable to VAT or CST 8 G. Concessional CST against Form C on goods required for laying of

pipeline network 9

IV Proposed GST Regime 10

A. Included under GST 11

B. GST Exempted 12 C. GST Zero Rated 12 D. Way forward 13

2

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

I Purpose of this report

Natural gas has emerged as the most benign fuel and it plays an important role in driving

the economic growth of a country. Being cleanest of all fossil fuels, efficient, and

relatively economical, it fulfils the requirements for fuel in today’s industrial society.

The sector has however, been facing enormous challenges over the last few years in

India on the indirect tax fronts in terms of levy of multiple taxes, interpretation issues,

unfavourable credit structure adding to the overall tax cost.

This document encapsulates the key indirect tax issues including the possible issues

that are likely to arise under the proposed GST regime.

II Summary

At present many challenges such as blockage of credit of taxes paid on inputs and input

services, disputes in relation to applicability of various taxes on output activities,

disparity in tax structure, high tax cost etc. are being faced by the industry.

In view of the same where natural gas is brought under the purview of the proposed

GST regime the issues are likely to be largely addressed providing relief to the industry

in terms of fair and stable tax regime.

III Indirect Tax challenges under Current Regime

A. Service tax on cash calls and reimbursements

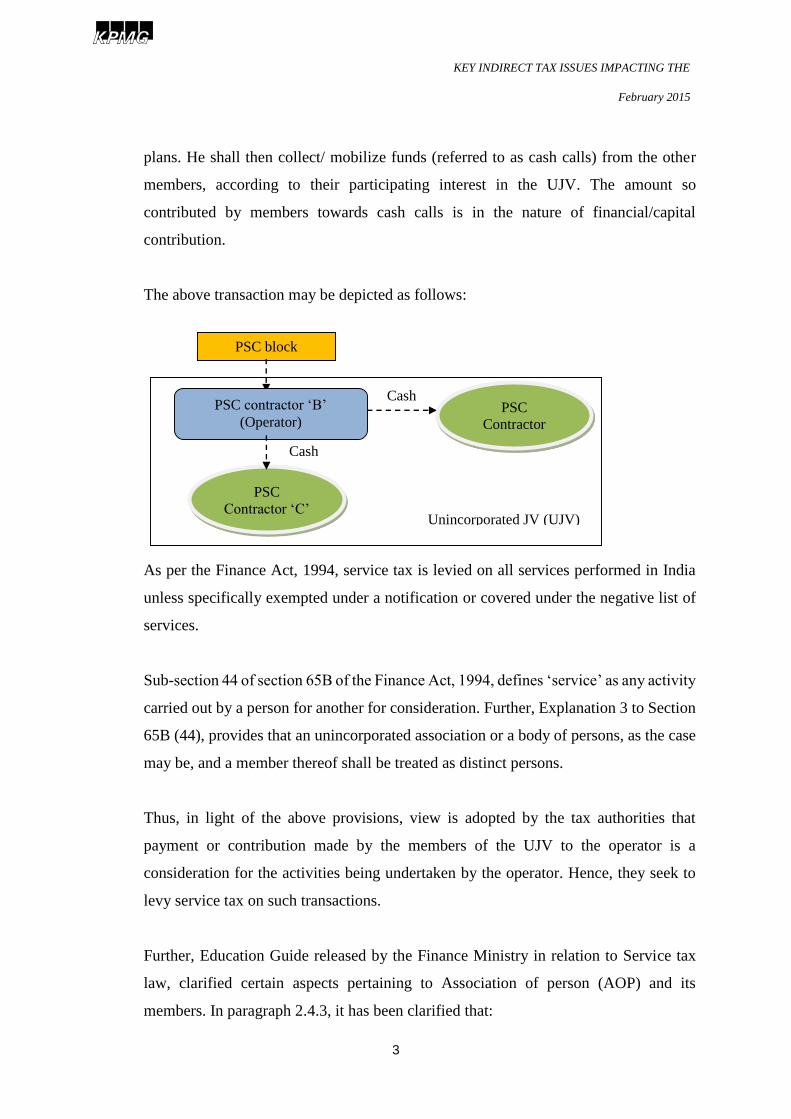

Exploration & Production (E&P) activities are generally carried on by Unincorporated

Joint Ventures (UJVs), on behalf of all members because of the high stakes involved.

Working of UJVs for E&P activities under the Production Sharing Contracts (‘PSC’)

requires designation of one of the participants as operator. Such operator is responsible

for carrying out the operations and incurring expenses based on the approved work

3

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

plans. He shall then collect/ mobilize funds (referred to as cash calls) from the other

members, according to their participating interest in the UJV. The amount so

contributed by members towards cash calls is in the nature of financial/capital

contribution.

The above transaction may be depicted as follows:

As per the Finance Act, 1994, service tax is levied on all services performed in India

unless specifically exempted under a notification or covered under the negative list of

services.

Sub-section 44 of section 65B of the Finance Act, 1994, defines ‘service’ as any activity

carried out by a person for another for consideration. Further, Explanation 3 to Section

65B (44), provides that an unincorporated association or a body of persons, as the case

may be, and a member thereof shall be treated as distinct persons.

Thus, in light of the above provisions, view is adopted by the tax authorities that

payment or contribution made by the members of the UJV to the operator is a

consideration for the activities being undertaken by the operator. Hence, they seek to

levy service tax on such transactions.

Further, Education Guide released by the Finance Ministry in relation to Service tax

law, clarified certain aspects pertaining to Association of person (AOP) and its

members. In paragraph 2.4.3, it has been clarified that:

Cash

Calls

Cash

Calls

PSC block

expenses

PSC contractor ‘B’

(Operator)

PSC

Contractor ‘C’

PSC

Contractor

‘A’

Unincorporated JV (UJV)

4

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

“The services provided, both by the so constituted JV or profit sharing association

of persons (AOP), as well as by each of the individual persons constituting the

JV/AOP will be liable to be taxed separately, subject of course to the availability of

the credit of the tax paid by independent persons to the JV/AOP and as otherwise

admissible under Cenvat Rules.”

The industry is of the view that Service tax should not be applicable on the aforesaid

transactions, as each member including operator is providing service to oneself.

Recently a clarification1 was also issued on the above matter giving partial relief

wherein it was clarified that if cash calls are merely a transaction in money, they are to

be excluded from the definition of service provided in section 65B(44) of the Finance

Act, 1994. Whether a 'cash call' is merely a ‘transaction in money' [in terms of section

65B(44) of the Finance Act. 1994] and hence not in the nature of consideration for

taxable service, would depend on the terms of the Joint Venture Agreement, which may

vary from case to case. The final treatment is left to be determined by the tax authorities.

As there is no intention to provide services by the members among themselves but to

pool their expertise, a clarification should be issued that there is no service involved

amongst the UJV members for execution of works under E&P activities.

B. Blockage of Service tax paid on Services consumed in E&P

Activities

In order to boost the natural gas sector in India, the Government of India has provided

for exemptions from customs/ excise duty to specified goods, used for E&P activities,

when imported or purchased from indigenous manufacturers. However, services

consumed by such E&P entities are subjected to service tax.

Production of natural gas is not liable to Excise duty under the Central Excise Act,

1944. Thus, service tax paid on services consumed by E&P entities is not allowed to be

1 179/5/2014-ST, dated September 24, 2014

5

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

claimed as credit/ refund. Hence, tax so paid becomes a cost adding to the overall tax

cost.

Introduction of a refund mechanism in respect of such taxes can bring parity and make

the E&P tax chain neutral.

C. Customs exemption on import of Liquefied Natural Gas (LNG)

NG is a clean fuel used in many sectors other than power such as fertilizer, city gas

distribution (for transport and domestic use), petrochemical, LPG, steel industry etc.

Recognizing the shortage of natural gas, the Government has encouraged the import of

LNG.

In terms of the notification no. 12/ 2012 dated 17th March 2012, customs duty on import

of LNG is exempt if the same is supplied to power generating companies.

Generally, at the time of importation of LNG, end use of the gas so imported is not

known by the importers and thus, availing exemption under the aforesaid notification

basis end use becomes a difficulty.

Instead an unconditional and a blanket exemption from customs duty on import of LNG

would remove the anomaly in availing the exemption. Further, it would benefit various

sectors including the fundamental ones such as fertilizer and steel.

D. Setting up of infrastructure – CENVAT Credit denial

Infrastructural set up i.e. construction of storage tanks, laying of pipelines, etc. is vital

for the companies engaged in regasification or transportation of gas. Taxes paid on such

construction activities form significant part of project costs.

6

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

As per CENVAT Credit Rules, 2004 (rules prescribing the credit/ setoff of central taxes

paid), credit of inputs and input services used for the construction or execution of works

contract of a building or a civil structure; or laying of foundation for support of capital

goods is not available2.

Further, credit of taxes paid on construction expenses is not allowed to the service

providers (e.g. those engaged in regasification/ transportation) contending that such

storage tanks/ buildings/ pipelines qualify as civil structures/ immovable property. This

leads to substantial increase in already exorbitant cost of operating such business.

Further, in certain cases doubts have been raised on the pipe etc contending the goods

were used as an immovable property hence, no credit of taxes paid in relation to such

goods should be allowed.

The founding principle of CENVAT Credit laws is to provide set off of taxes paid by

the manufacturers/ service providers on inputs and capital goods against the taxes

payable on output reducing the cascading effect of taxes and taxing the value additions.

As storage tanks, pipelines etc. are essentially required to provide services, the non-

availability of set offs in respect of duty paid on goods and services used for

construction of such structures renders such activities tax inefficient.

2 The relevant portion of the definition of ‘inputs’ and ‘input services’ as defined under the CENVAT Credit Rules, 2004 as

follows:

“(k) “input” means -

(iv) .....

but excludes -

(A) ....

(B) any goods used for-

(a) construction or execution of works contract of a building or a civil structure or a part thereof; or

(b) laying of foundation or making of structures for support of capital goods,”

“(l) “input service” means any service, -

(ii) ...excludes,-

(A) service portion in the execution of a works contract and construction services including service listed under clause (b) of

section 66E of the Finance Act] (herein referred as specified services) in so far as they are used for –

(a) construction or execution of works contract of a building or a civil structure or a part thereof; or

(b) laying of foundation or making of structures for support of capital goods, except for the provision of one or more of the

specified services; or”

7

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

To avoid ambiguities around interpretation of law resulting into disputes and following

the underlying principles of CENVAT Credit, a clarification should be issued allowing

credit of the taxes paid on goods and services used for setting up the infrastructure.

E. Value Added Tax and service tax on Sale and Transport of Gas

Transmission charges are collected separately for transmission of gas by the suppliers

in addition to sale price of gas.

Such suppliers selling and transmitting natural gas to the customers’ premises consider

the entire transaction as 'sale' transaction and pay sales tax/VAT3 on the 'total price'

including transmission charges.

Service Tax was made applicable on the category of 'transportation of goods through

pipeline' with effect from 16.06.2005. Thus, disputes by tax authorities have arisen on

the applicability of service tax on such transmission charges recovered from the

customer along with the sale price of gas.

Payment of VAT and service tax on transmission charges results in double taxation and

thus, it has invited huge tax disputes.

In this regard, Hon’ble Gujarat High Court4 held that the manner of raising sale bill

(whether the transportation charges are embedded in the cost of gas or shown

separately) does not alter the basic nature of such contract which remains essentially a

'contract for sale'. This ruling further substantiates that such transactions do not involve

any element of service and are purely sale transactions not liable to service tax.

However, due to overlapping tax provisions under sales tax/VAT and service tax, this

issue continues to be a grey area.

3 Value added tax (VAT) is levied by the State governments on sale of goods within the state. 4 CIT (TDS) v/s Krishak Bharati Cooperative Limited

8

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

A clarification issued by the service tax authorities that such transactions do not involve

any service element and hence not liable to service tax would help to resolve the issue.

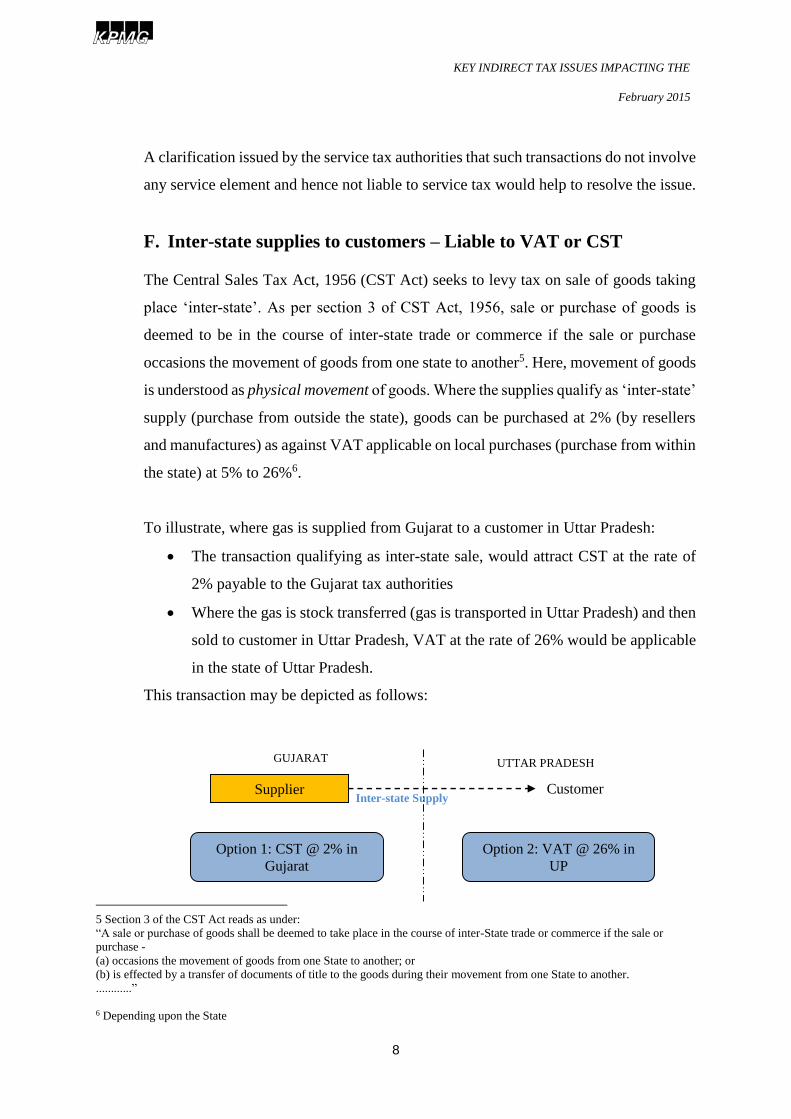

F. Inter-state supplies to customers – Liable to VAT or CST

The Central Sales Tax Act, 1956 (CST Act) seeks to levy tax on sale of goods taking

place ‘inter-state’. As per section 3 of CST Act, 1956, sale or purchase of goods is

deemed to be in the course of inter-state trade or commerce if the sale or purchase

occasions the movement of goods from one state to another5. Here, movement of goods

is understood as physical movement of goods. Where the supplies qualify as ‘inter-state’

supply (purchase from outside the state), goods can be purchased at 2% (by resellers

and manufactures) as against VAT applicable on local purchases (purchase from within

the state) at 5% to 26%6.

To illustrate, where gas is supplied from Gujarat to a customer in Uttar Pradesh:

The transaction qualifying as inter-state sale, would attract CST at the rate of

2% payable to the Gujarat tax authorities

Where the gas is stock transferred (gas is transported in Uttar Pradesh) and then

sold to customer in Uttar Pradesh, VAT at the rate of 26% would be applicable

in the state of Uttar Pradesh.

This transaction may be depicted as follows:

5 Section 3 of the CST Act reads as under:

“A sale or purchase of goods shall be deemed to take place in the course of inter-State trade or commerce if the sale or

purchase -

(a) occasions the movement of goods from one State to another; or

(b) is effected by a transfer of documents of title to the goods during their movement from one State to another.

............”

6 Depending upon the State

Inter-state Supply Supplier

Option 1: CST @ 2% in

Gujarat

Customer

UTTAR PRADESH GUJARAT

Option 2: VAT @ 26% in

UP

9

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

As the availability of natural gas in the country is not enough to cater to the needs of

the various industries, the same is also imported from outside India. Gas available from

different sources (domestic as well as imported) is co-mingled/ pooled and supplied

through common pipeline network to fulfil the requirements of gas on pan India basis.

As it is not possible to have separate pipeline infrastructure for each source, different

suppliers from different states commonly access the pipeline network. Due to above

trends of co-mingling and pooling, it has become difficult to demonstrate physical

movement of gas originating from each source corresponding to its final delivery/sale

to consumers. Since tax treatment under existing VAT/CST laws is largely dependent

on physical movement of goods, it is very challenging to ascertain real tax liability

under the circumstances where gas originating from different sources is co-mingled.

Where suitable amendments are made in the existing provisions of the CST Act so as

to facilitate trading of goods through pipeline network, the above could be resolved.

G. Concessional CST against Form C on goods required for laying of

pipeline network

Under the CST Act, concessional rate of tax at 2% is applicable on inter-state sale of

goods used for certain specified purposes (resale, use in manufacture/processing or for use

in mining, generation of electricity or any other form of power) against issuance of Form C.

As the goods required for use in natural gas pipeline network are not covered above,

natural gas transmission companies are not able to issue Form C for purchase of goods

for construction of pipeline network at concessional tax of 2%.

Laying of cross country pipelines including connecting gas source to ultimate

consumers is a priority for achieving the energy security of the country. Amendment of

the existing CST provisions so as to make the pipeline transmission projects eligible

for inter-state procurement of goods against Form C will reduce the project cost and

will ultimately benefit the consumers.

10

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

IV Proposed GST Regime

GST was first announced to be introduced with effect from 2010, way back in 2006.

GST is set to replace the plethora of indirect taxes both at the Central (excise duty, CST,

etc.) as well as State Government’s level (VAT, entry tax, etc.), reducing the cascading

effect of taxes, simplifying the tax compliances and administration and creating a

common market.

Extensive discussions over last several years have taken place on the issue of inclusion

of petroleum products (diesel, petrol, ATF) including Natural gas in the ambit of GST.

While Centre wanted petroleum products (including natural gas) to be part of GST,

some States were averse due to revenue considerations (as States generally levy VAT

at a rate higher than the standard rate).

The recent Constitutional Bill tabled in the Parliament seeks to keep both the options

open. Natural gas has neither been specifically excluded from GST ambit nor the power

of the Central and State Government to levy Excise duty and VAT on the same has

been withdrawn. Further, the GST Council has been empowered to recommend a date

from which GST shall be levied on natural gas. The Constitutional Amendment Bill is

likely to be taken up for voting in the upcoming budget session around March 2015.

In the above backdrop, there are three possible scenarios regarding the treatment of

natural gas under the GST ambit:

It is included within GST ambit

Its exempted from GST

It is zero rated under the GST regime

In the following sections, we have discussed the possible implications on the overall

gas value chain under the above scenarios.

11

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

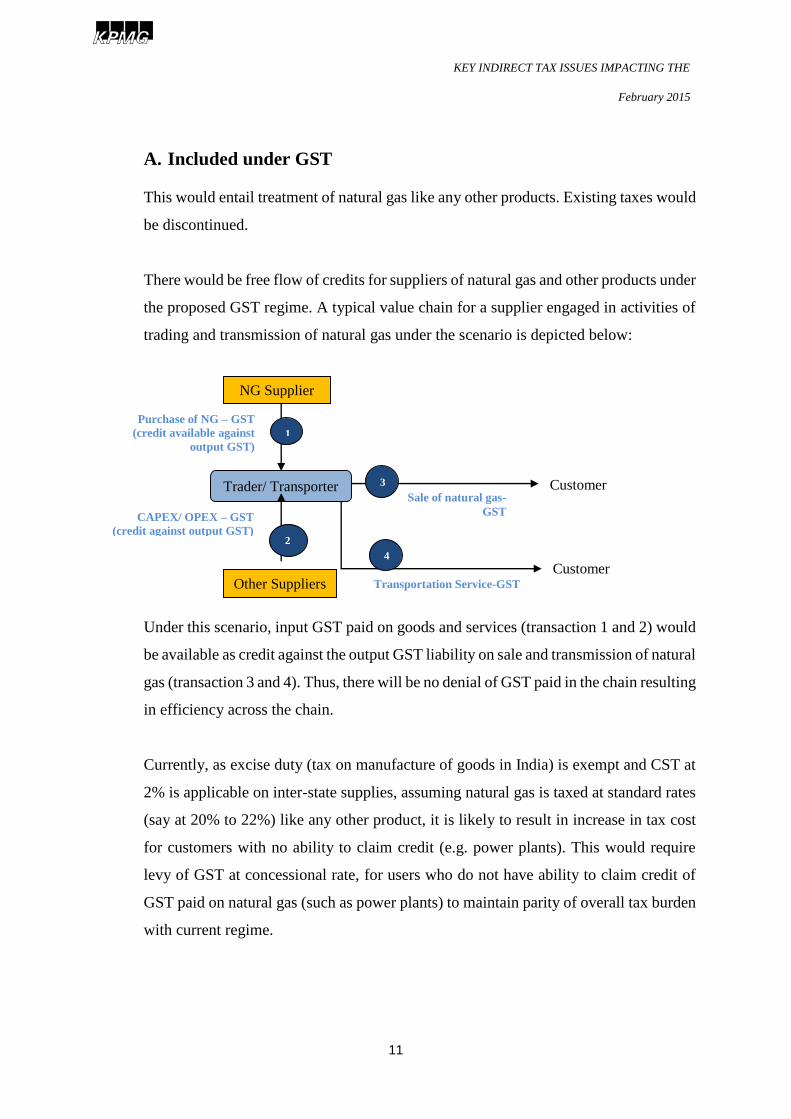

A. Included under GST

This would entail treatment of natural gas like any other products. Existing taxes would

be discontinued.

There would be free flow of credits for suppliers of natural gas and other products under

the proposed GST regime. A typical value chain for a supplier engaged in activities of

trading and transmission of natural gas under the scenario is depicted below:

Under this scenario, input GST paid on goods and services (transaction 1 and 2) would

be available as credit against the output GST liability on sale and transmission of natural

gas (transaction 3 and 4). Thus, there will be no denial of GST paid in the chain resulting

in efficiency across the chain.

Currently, as excise duty (tax on manufacture of goods in India) is exempt and CST at

2% is applicable on inter-state supplies, assuming natural gas is taxed at standard rates

(say at 20% to 22%) like any other product, it is likely to result in increase in tax cost

for customers with no ability to claim credit (e.g. power plants). This would require

levy of GST at concessional rate, for users who do not have ability to claim credit of

GST paid on natural gas (such as power plants) to maintain parity of overall tax burden

with current regime.

NG Supplier

Customer Trader/ Transporter

Other Suppliers Customer

Purchase of NG – GST

(credit available against

output GST)

CAPEX/ OPEX – GST

(credit against output GST)

Transportation Service-GST

Sale of natural gas-

GST

1

2

3

4

12

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

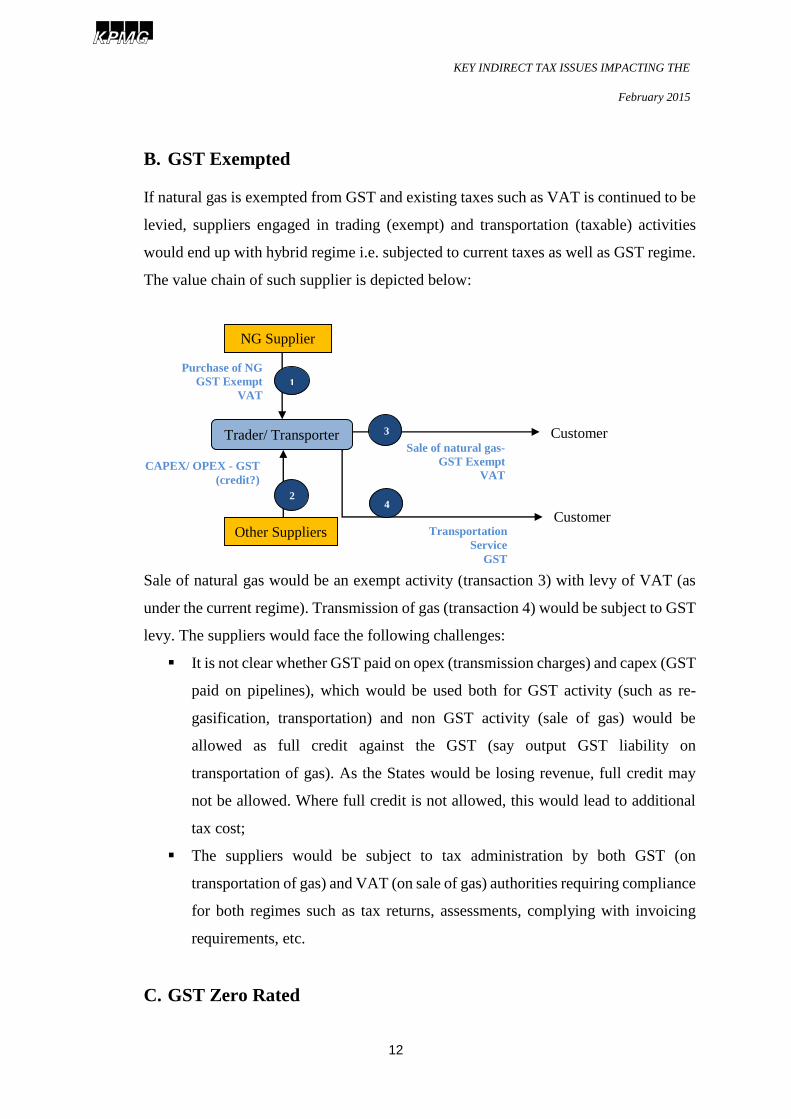

B. GST Exempted

If natural gas is exempted from GST and existing taxes such as VAT is continued to be

levied, suppliers engaged in trading (exempt) and transportation (taxable) activities

would end up with hybrid regime i.e. subjected to current taxes as well as GST regime.

The value chain of such supplier is depicted below:

Sale of natural gas would be an exempt activity (transaction 3) with levy of VAT (as

under the current regime). Transmission of gas (transaction 4) would be subject to GST

levy. The suppliers would face the following challenges:

It is not clear whether GST paid on opex (transmission charges) and capex (GST

paid on pipelines), which would be used both for GST activity (such as re-

gasification, transportation) and non GST activity (sale of gas) would be

allowed as full credit against the GST (say output GST liability on

transportation of gas). As the States would be losing revenue, full credit may

not be allowed. Where full credit is not allowed, this would lead to additional

tax cost;

The suppliers would be subject to tax administration by both GST (on

transportation of gas) and VAT (on sale of gas) authorities requiring compliance

for both regimes such as tax returns, assessments, complying with invoicing

requirements, etc.

C. GST Zero Rated

NG Supplier

Customer Trader/ Transporter

Other Suppliers Customer

Purchase of NG

GST Exempt

VAT

CAPEX/ OPEX - GST

(credit?)

Transportation

Service

GST

Sale of natural gas-

GST Exempt

VAT

1

2

3

4

13

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

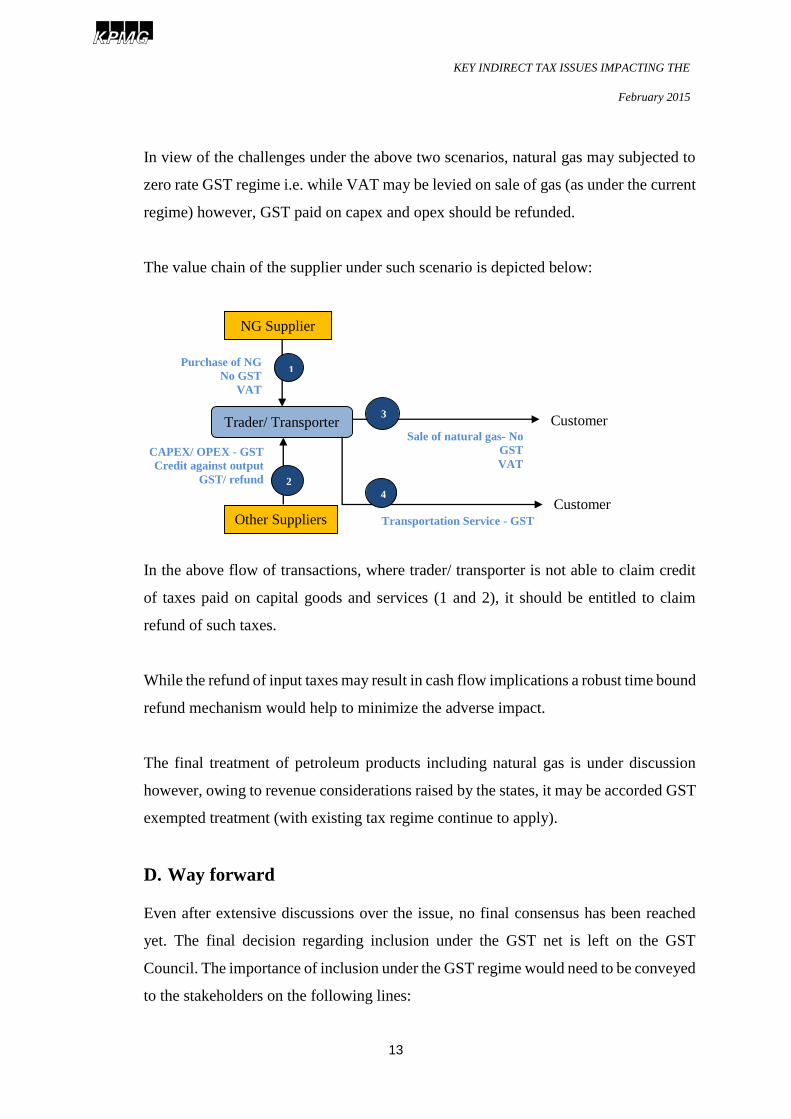

In view of the challenges under the above two scenarios, natural gas may subjected to

zero rate GST regime i.e. while VAT may be levied on sale of gas (as under the current

regime) however, GST paid on capex and opex should be refunded.

The value chain of the supplier under such scenario is depicted below:

In the above flow of transactions, where trader/ transporter is not able to claim credit

of taxes paid on capital goods and services (1 and 2), it should be entitled to claim

refund of such taxes.

While the refund of input taxes may result in cash flow implications a robust time bound

refund mechanism would help to minimize the adverse impact.

The final treatment of petroleum products including natural gas is under discussion

however, owing to revenue considerations raised by the states, it may be accorded GST

exempted treatment (with existing tax regime continue to apply).

D. Way forward

Even after extensive discussions over the issue, no final consensus has been reached

yet. The final decision regarding inclusion under the GST net is left on the GST

Council. The importance of inclusion under the GST regime would need to be conveyed

to the stakeholders on the following lines:

NG Supplier

Customer Trader/ Transporter

Other Suppliers Customer

Purchase of NG

No GST

VAT

CAPEX/ OPEX - GST

Credit against output

GST/ refund

Transportation Service - GST

Sale of natural gas- No

GST

VAT

1

2

3

4

14

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

Natural gas, unlike other petroleum products, is used primarily as an industrial

input (and not as fuel in vehicles, etc. akin to HSD, Petrol in scale) by power/

fertilizer units, which are all thrust sectors for the economy. As natural gas is

predominantly used in industrial sector and is an environmental friendly fuel, it

should be considered for inclusion even without including other petroleum

goods

Natural gas does not generate any negative externalities and hence, should not

be treated as a demerit product

Share of contribution of natural gas to state revenue in comparison to

contribution of other petroleum goods (such as diesel, petrol, ATF) is not

substantial. Some states have already accorded a concessional VAT rate at least

for certain users (e.g. domestic supplies). Thus, inclusion of natural gas in the

ambit of GST may not have significant effect on the exchequer of the states

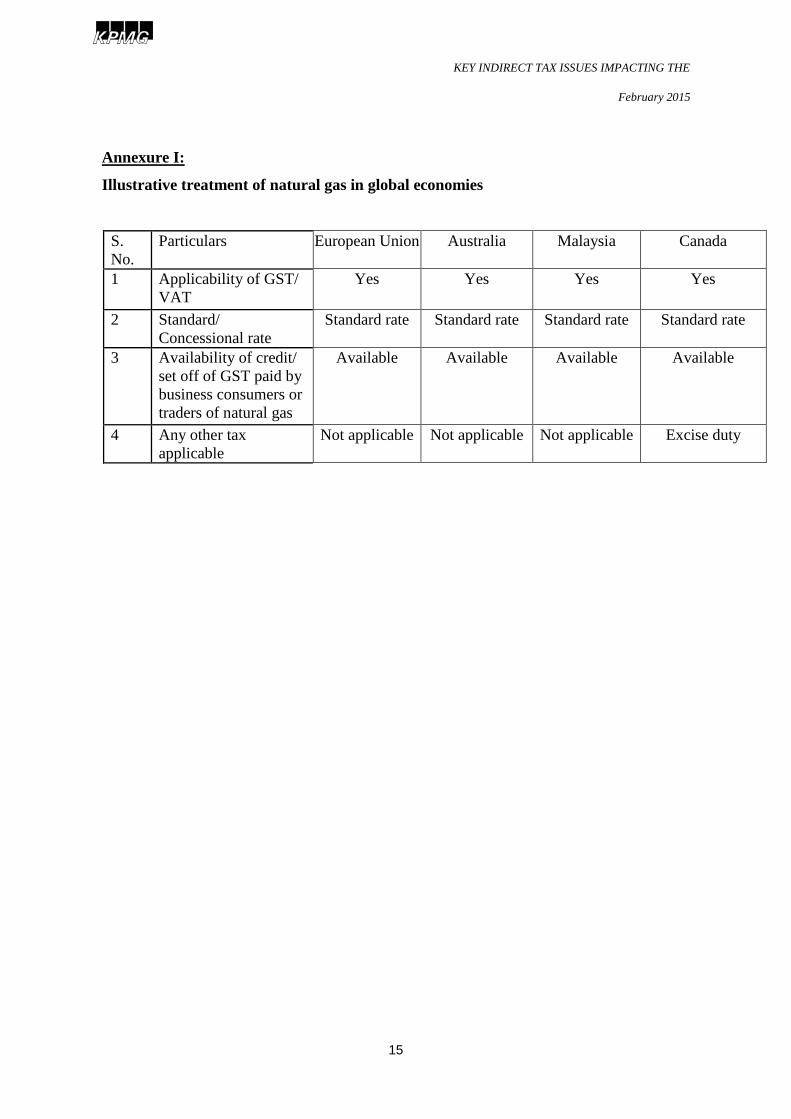

Internationally natural gas is generally accorded similar treatment as other

goods under GST. For the treatment under key economies refer Annexure 1

Even if it is finally decided to exclude natural gas from GST, it should at least

be zero-rated with time bound refund mechanism and not exempted.

15

ABCD

KEY INDIRECT TAX ISSUES IMPACTING THE

INDIAN NATURAL GAS SECTOR

February 2015

Annexure I:

Illustrative treatment of natural gas in global economies

S.

No. Particulars European Union Australia Malaysia Canada

1 Applicability of GST/

VAT Yes Yes Yes Yes

2 Standard/

Concessional rate Standard rate Standard rate Standard rate Standard rate

3 Availability of credit/

set off of GST paid by

business consumers or

traders of natural gas

Available Available Available Available

4 Any other tax

applicable Not applicable Not applicable Not applicable Excise duty