KeyBanc Capital Markets’ Debt Capital Markets

The KeyBanc Capital Markets® Debt Capital Markets team represents

one of the strongest full-service debt-side investment banking, sales,

trading and distribution platforms in the nation. We use a blend of real

world perspectives, backed by robust capabilities and relationships, to

help our clients use leverage to grow, make acquisitions, and enhance

operations.

For additional information regarding this

newsletter, please contact the individuals

listed below: Andrew Frawley 216.689.4288

Steve Rasoletti 216.689.3228

Disclosure: KeyBanc Capital Markets is a trade name under which corporate and investment banking products and services of KeyCorp and its subsidiaries, KeyBanc Capital Markets Inc., Member NYSE/FINRA/SIPC, and KeyBank National Association (“KeyBank N.A.”),

are marketed. Securities products and services are offered by KeyBanc Capital Markets Inc. and its licensed securities representatives, who may also be employees of KeyBank N.A. Banking products and services are offered by KeyBank N.A.

This report was not issued by our research department. The information contained in this report has been obtained from sources deemed to be reliable but is not represented to be complete, and it should not be relied upon as such. This report does not purport to be a

complete analysis of any security, issuer, or industry and is not an offer or a solicitation of an offer to buy or sell any securities. This report is prepared for general information purposes only and does not consider the specific investment objectives, financial situation and

particular needs of any individual person or entity.

Junior Debt Market Analysis

2

Executive Summary

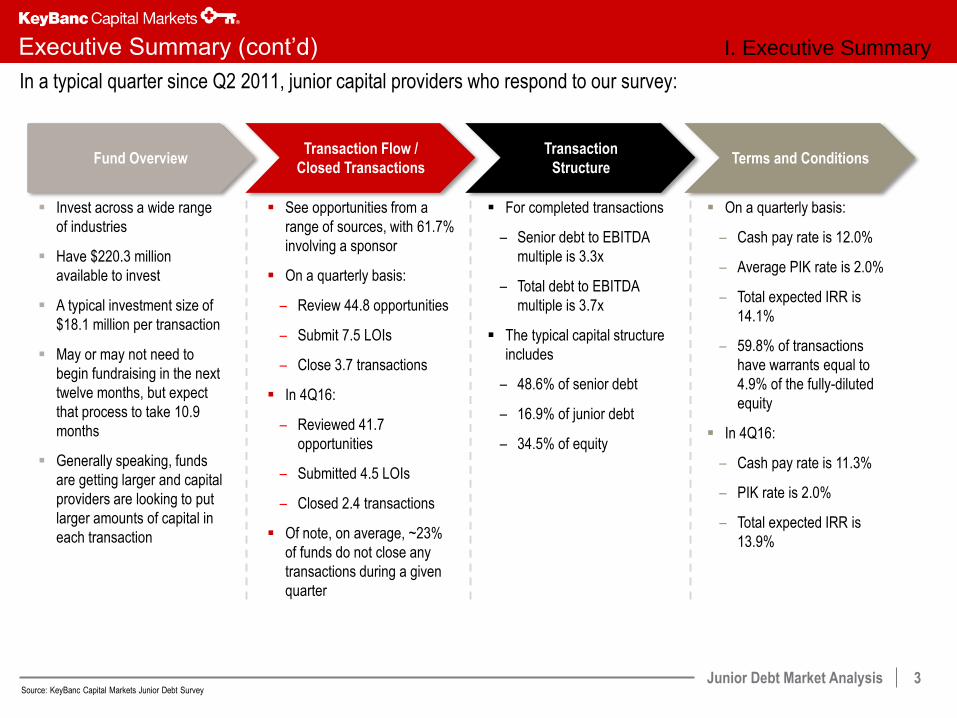

KeyBanc Capital Markets (KBCM) conducts a quarterly survey of mezzanine and junior debt participants to measure

market conditions and transaction terms

The junior debt capital markets (including mezzanine, subordinated, second lien structures, etc.) are not as well documented or

organized as the senior debt markets or the equity or venture capital markets

– This challenge is even more pronounced in the lower end of the middle market (typically companies <$50 million of EBITDA)

Our survey and resulting newsletter is an attempt to address the lack of market information noted above

We have been conducting our survey since 2011 and have aggregated the data for review and analysis

Unless otherwise stated, statistics found in this analysis reflect the average of answers provided since inception of survey

I. Executive Summary

Junior Debt Market Analysis

3

Executive Summary (cont’d)

In a typical quarter since Q2 2011, junior capital providers who respond to our survey:

Transaction Flow /

Closed Transactions

Transaction

Structure Terms and Conditions Fund Overview

Source: KeyBanc Capital Markets Junior Debt Survey

I. Executive Summary

Invest across a wide range

of industries

Have $220.3 million

available to invest

A typical investment size of

$18.1 million per transaction

May or may not need to

begin fundraising in the next

twelve months, but expect

that process to take 10.9

months

Generally speaking, funds

are getting larger and capital

providers are looking to put

larger amounts of capital in

each transaction

See opportunities from a

range of sources, with 61.7%

involving a sponsor

On a quarterly basis:

– Review 44.8 opportunities

– Submit 7.5 LOIs

– Close 3.7 transactions

In 4Q16:

– Reviewed 41.7

opportunities

– Submitted 4.5 LOIs

– Closed 2.4 transactions

Of note, on average, ~23%

of funds do not close any

transactions during a given

quarter

For completed transactions

– Senior debt to EBITDA

multiple is 3.3x

– Total debt to EBITDA

multiple is 3.7x

The typical capital structure

includes

– 48.6% of senior debt

– 16.9% of junior debt

– 34.5% of equity

On a quarterly basis:

– Cash pay rate is 12.0%

– Average PIK rate is 2.0%

– Total expected IRR is

14.1%

– 59.8% of transactions

have warrants equal to

4.9% of the fully-diluted

equity

In 4Q16:

– Cash pay rate is 11.3%

– PIK rate is 2.0%

– Total expected IRR is

13.9%

Junior Debt Market Analysis

4

KBCM Junior Debt Market Analysis

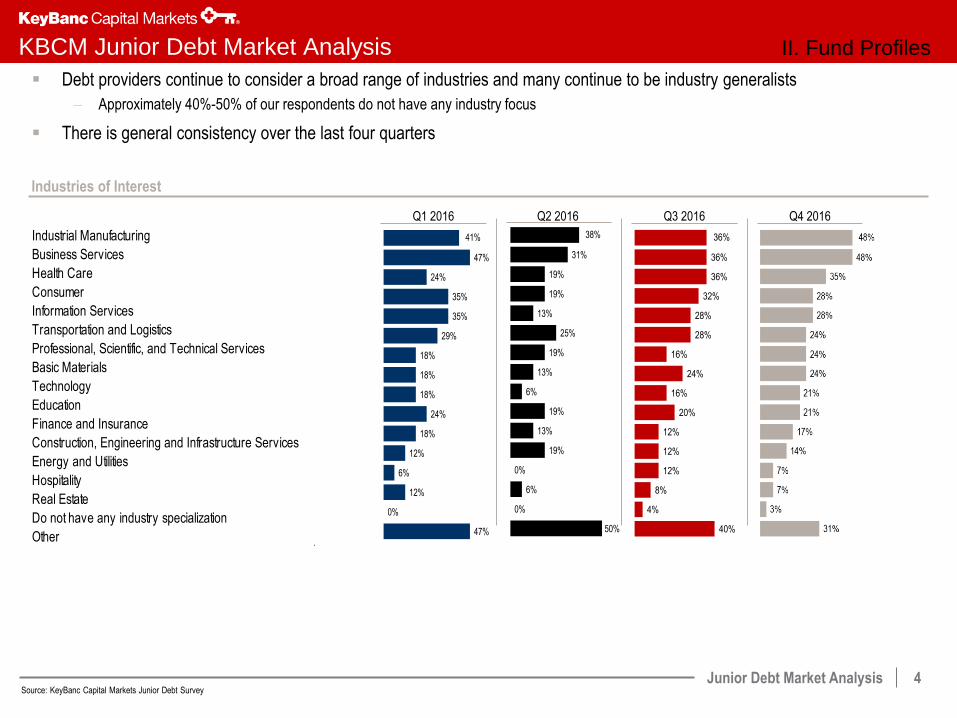

Debt providers continue to consider a broad range of industries and many continue to be industry generalists

– Approximately 40%-50% of our respondents do not have any industry focus

There is general consistency over the last four quarters

Industries of Interest

Source: KeyBanc Capital Markets Junior Debt Survey

II. Fund Profiles

Q1 2016 Q3 2016 Q4 2016 Q2 2016

Industrial Manufacturing

Business Services

Health Care

Consumer

Information Services

Transportation and Logistics

Professional, Scientific, and Technical Services

Basic Materials

Technology

Education

Finance and Insurance

Construction, Engineering and Infrastructure Services

Energy and Utilities

Hospitality

Real Estate

Do not have any industry specialization

Other

41%

47%

24%

35%

35%

29%

18%

18%

18%

24%

18%

12%

6%

12%

0%

47%

38%

31%

19%

19%

13%

25%

19%

13%

6%

19%

13%

19%

0%

6%

0%

50%

36%

36%

36%

32%

28%

28%

16%

24%

16%

20%

12%

12%

12%

8%

4%

40%

Junior Debt Market Analysis

5

KBCM Junior Debt Market Analysis

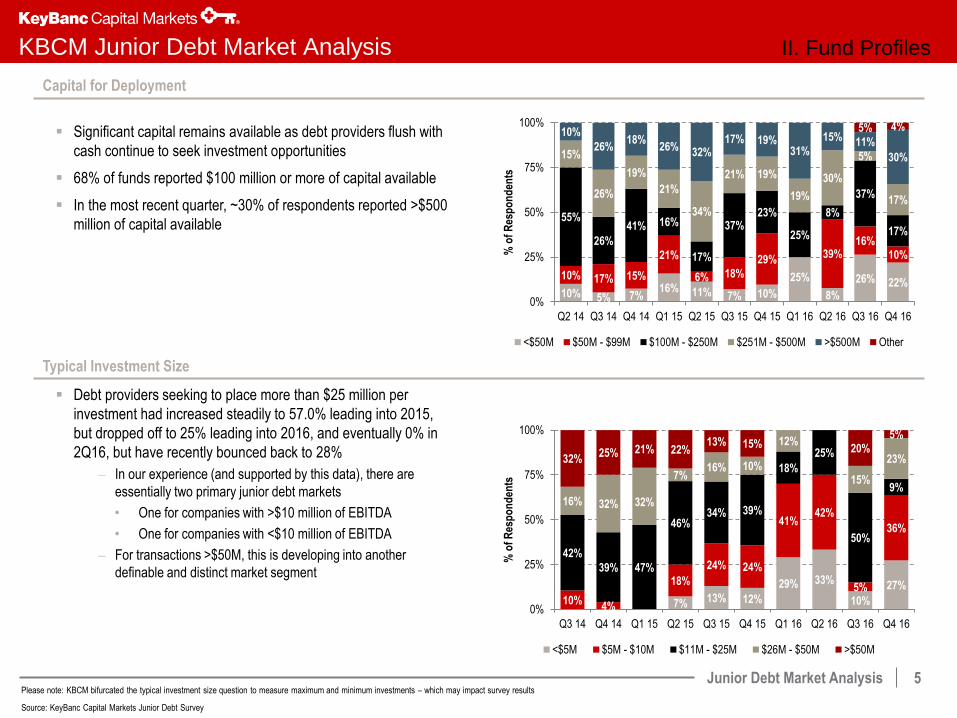

Capital for Deployment

Typical Investment Size

Significant capital remains available as debt providers flush with

cash continue to seek investment opportunities

68% of funds reported $100 million or more of capital available

In the most recent quarter, ~30% of respondents reported >$500

million of capital available

Debt providers seeking to place more than $25 million per

investment had increased steadily to 57.0% leading into 2015,

but dropped off to 25% leading into 2016, and eventually 0% in

2Q16, but have recently bounced back to 28%

– In our experience (and supported by this data), there are

essentially two primary junior debt markets

• One for companies with >$10 million of EBITDA

• One for companies with <$10 million of EBITDA

– For transactions >$50M, this is developing into another

definable and distinct market segment

Please note: KBCM bifurcated the typical investment size question to measure maximum and minimum investments – which may impact survey results

Source: KeyBanc Capital Markets Junior Debt Survey

II. Fund Profiles

10% 5% 7% 16% 11% 7% 10%

25%

8%

26% 22% 10% 17% 15%

21%

6% 18%

29% 39% 16%

10%

55%

26%

41% 16%

17%

37% 23%

25%

8%

37%

17%

15%

26%

19%

21%

34%

21% 19%

19%

30%

5%

17%

10%

26% 18%

26% 32% 17% 19%

31%

15% 11%

30%

5% 4%

0%

25%

50%

75%

100%

Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

<$50M $50M - $99M $100M - $250M $251M - $500M >$500M Other

7% 13% 12%

29% 33%

10%

27%

10% 4%

18%

24% 24%

41% 42%

5%

36%

42%

39% 47%

46% 34% 39%

18%

25%

50%

9% 16% 32% 32%

7% 16% 10%

12%

15%

23% 32% 25% 21% 22%

13% 15% 20% 5%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

<$5M $5M - $10M $11M - $25M $26M - $50M >$50M

Junior Debt Market Analysis

6

KBCM Junior Debt Market Analysis

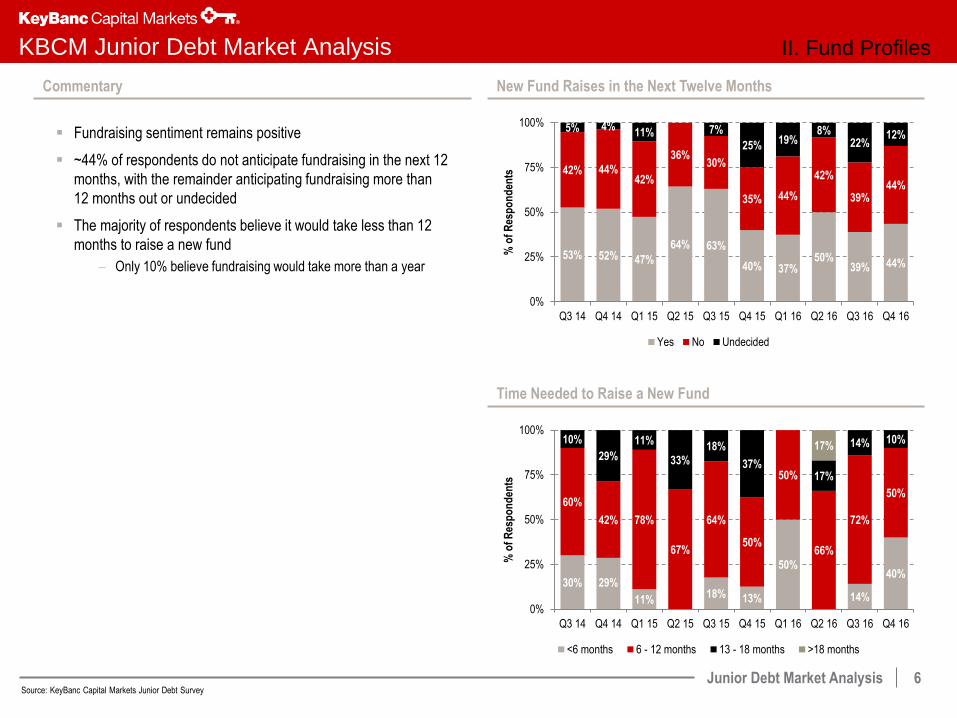

Commentary

Fundraising sentiment remains positive

~44% of respondents do not anticipate fundraising in the next 12

months, with the remainder anticipating fundraising more than

12 months out or undecided

The majority of respondents believe it would take less than 12

months to raise a new fund

– Only 10% believe fundraising would take more than a year

New Fund Raises in the Next Twelve Months

Time Needed to Raise a New Fund

Source: KeyBanc Capital Markets Junior Debt Survey

II. Fund Profiles

53% 52% 47%

64% 63%

40% 37% 50%

39% 44%

42% 44% 42%

36% 30%

35% 44%

42%

39% 44%

5% 4% 11% 7%

25% 19% 8%

22% 12%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Yes No Undecided

30% 29%

11% 18% 13%

50%

14%

40%

60%

42% 78%

67%

64%

50%

50%

66%

72%

50%

10%

29%

11%

33%

18%

37% 17%

14% 10% 17%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

<6 months 6 - 12 months 13 - 18 months >18 months

Junior Debt Market Analysis

7

KBCM Junior Debt Market Analysis

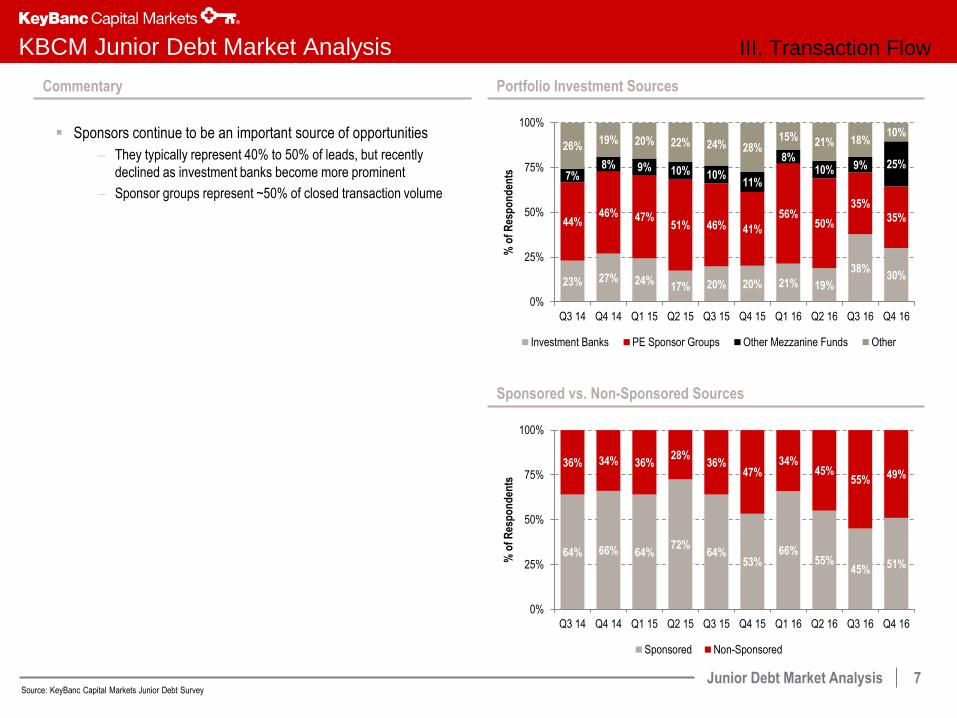

Commentary Portfolio Investment Sources

Sponsors continue to be an important source of opportunities

– They typically represent 40% to 50% of leads, but recently

declined as investment banks become more prominent

– Sponsor groups represent ~50% of closed transaction volume

Sponsored vs. Non-Sponsored Sources

Source: KeyBanc Capital Markets Junior Debt Survey

III. Transaction Flow

23% 27% 24% 17% 20% 20% 21% 19%

38% 30%

44% 46% 47%

51% 46% 41%

56% 50%

35% 35%

7% 8% 9% 10% 10%

11%

8% 10% 9% 25%

26% 19% 20% 22% 24% 28%

15% 21% 18% 10%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Investment Banks PE Sponsor Groups Other Mezzanine Funds Other

64% 66% 64% 72%

64% 53%

66% 55%

45% 51%

36% 34% 36% 28%

36% 47%

34% 45%

55% 49%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Sponsored Non-Sponsored

Junior Debt Market Analysis

8

KBCM Junior Debt Market Analysis

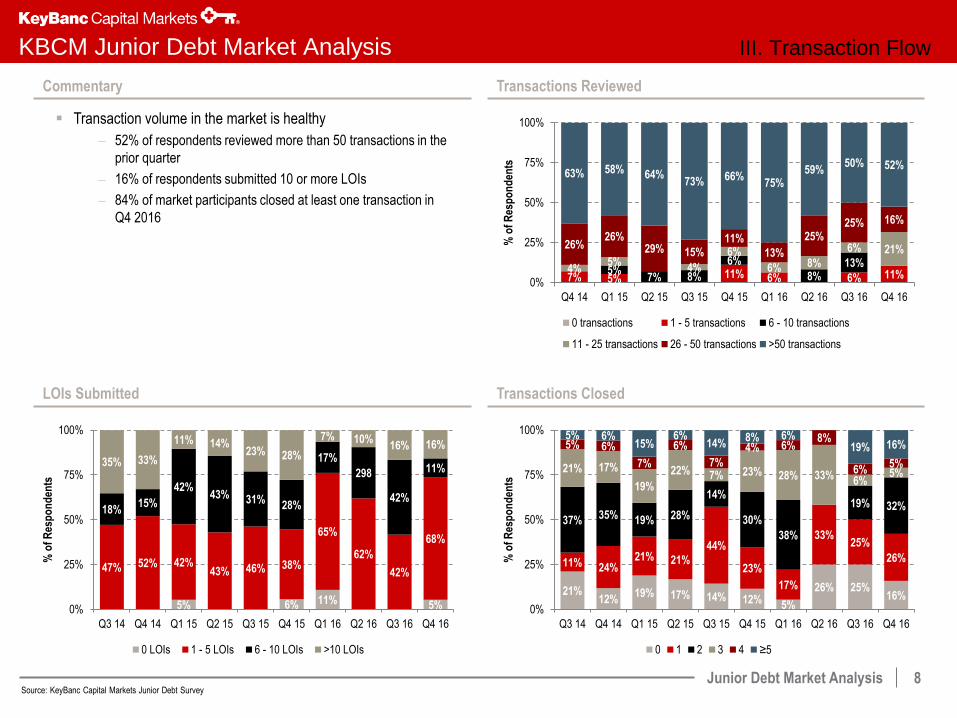

Commentary

LOIs Submitted

Transactions Reviewed

Transaction volume in the market is healthy

– 52% of respondents reviewed more than 50 transactions in the

prior quarter

– 16% of respondents submitted 10 or more LOIs

– 84% of market participants closed at least one transaction in

Q4 2016

Transactions Closed

Source: KeyBanc Capital Markets Junior Debt Survey

III. Transaction Flow

7% 5% 11% 6% 6% 11% 5% 7% 8%

6%

8% 13%

4% 5%

4%

6%

6% 8%

6% 21% 26% 26%

29% 15% 11%

13%

25% 25% 16%

63% 58% 64% 73% 66%

75% 59%

50% 52%

0%

25%

50%

75%

100%

Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

0 transactions 1 - 5 transactions 6 - 10 transactions

11 - 25 transactions 26 - 50 transactions >50 transactions

5% 6% 11% 5%

47% 52% 42% 43% 46% 38%

65%

62%

42%

68%

18% 15%

42% 43% 31%

28%

17%

298

42%

11% 35% 33%

11% 14% 23% 28%

7% 10% 16% 16%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

0 LOIs 1 - 5 LOIs 6 - 10 LOIs >10 LOIs

21% 12%

19% 17% 14% 12% 5%

26% 25% 16%

11% 24% 21% 21%

44%

23%

17%

33% 25%

26%

37% 35% 19% 28%

14%

30%

38%

19% 32%

21% 17%

19%

22% 7% 23% 28% 33% 6% 5%

5% 6%

7%

6%

7%

4% 6% 8%

6% 5%

5% 6% 15%

6% 14%

8% 6% 19% 16%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

0 1 2 3 4 ≥5

Junior Debt Market Analysis

9

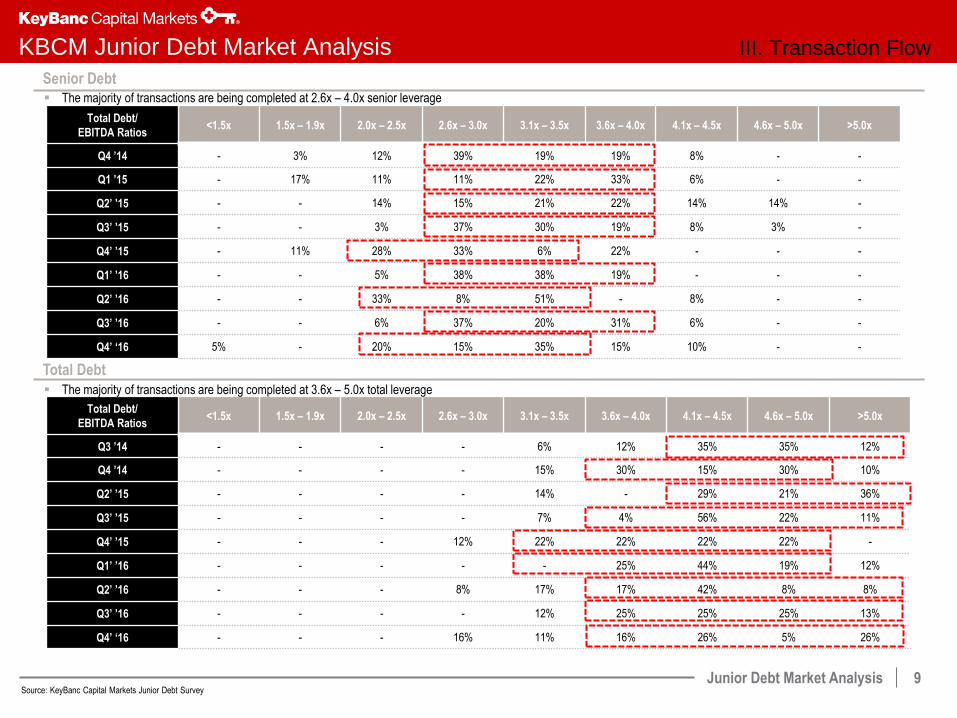

KBCM Junior Debt Market Analysis

Total Debt/

EBITDA Ratios <1.5x 1.5x – 1.9x 2.0x – 2.5x 2.6x – 3.0x 3.1x – 3.5x 3.6x – 4.0x 4.1x – 4.5x 4.6x – 5.0x >5.0x

Q3 ’14 - - - - 6% 12% 35% 35% 12%

Q4 ’14 - - - - 15% 30% 15% 30% 10%

Q2’ ’15 - - - - 14% - 29% 21% 36%

Q3’ ’15 - - - - 7% 4% 56% 22% 11%

Q4’ ’15 - - - 12% 22% 22% 22% 22% -

Q1’ ’16 - - - - - 25% 44% 19% 12%

Q2’ ’16 - - - 8% 17% 17% 42% 8% 8%

Q3’ ’16 - - - - 12% 25% 25% 25% 13%

Q4’ ‘16 - - - 16% 11% 16% 26% 5% 26%

Total Debt/

EBITDA Ratios <1.5x 1.5x – 1.9x 2.0x – 2.5x 2.6x – 3.0x 3.1x – 3.5x 3.6x – 4.0x 4.1x – 4.5x 4.6x – 5.0x >5.0x

Q4 ’14 - 3% 12% 39% 19% 19% 8% - -

Q1 ’15 - 17% 11% 11% 22% 33% 6% - -

Q2’ ’15 - - 14% 15% 21% 22% 14% 14% -

Q3’ ’15 - - 3% 37% 30% 19% 8% 3% -

Q4’ ’15 - 11% 28% 33% 6% 22% - - -

Q1’ ’16 - - 5% 38% 38% 19% - - -

Q2’ ’16 - - 33% 8% 51% - 8% - -

Q3’ ’16 - - 6% 37% 20% 31% 6% - -

Q4’ ‘16 5% - 20% 15% 35% 15% 10% - -

Senior Debt

Total Debt

The majority of transactions are being completed at 2.6x – 4.0x senior leverage

The majority of transactions are being completed at 3.6x – 5.0x total leverage

Source: KeyBanc Capital Markets Junior Debt Survey

III. Transaction Flow

Junior Debt Market Analysis

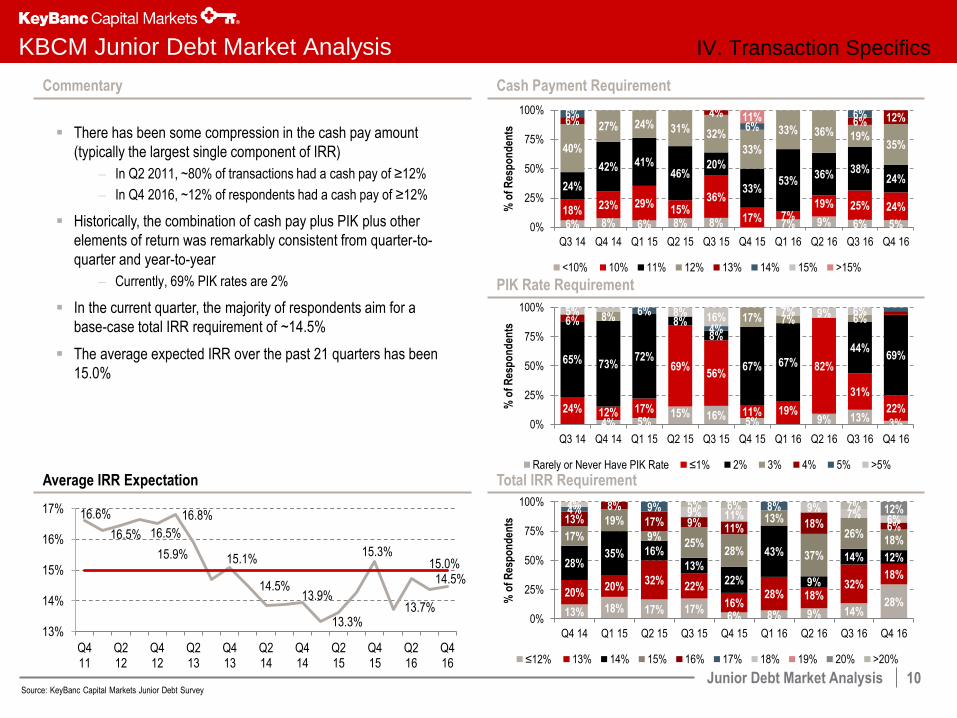

10

Cash Payment Requirement

Total IRR Requirement

PIK Rate Requirement

There has been some compression in the cash pay amount

(typically the largest single component of IRR)

– In Q2 2011, ~80% of transactions had a cash pay of ≥12%

– In Q4 2016, ~12% of respondents had a cash pay of ≥12%

Historically, the combination of cash pay plus PIK plus other

elements of return was remarkably consistent from quarter-to-

quarter and year-to-year

– Currently, 69% PIK rates are 2%

In the current quarter, the majority of respondents aim for a

base-case total IRR requirement of ~14.5%

The average expected IRR over the past 21 quarters has been

15.0%

Commentary

Average IRR Expectation

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Market Analysis IV. Transaction Specifics

6% 8% 6% 8% 8% 7% 9% 6% 5% 18% 23% 29%

15% 36%

17% 7% 19% 25% 24%

24%

42% 41% 46%

20%

33% 53%

36% 38% 24%

40%

27% 24% 31% 32%

33%

33% 36% 19% 35%

6% 4%

6% 12% 6% 6%

6% 11%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

<10% 10% 11% 12% 13% 14% 15% >15%

4% 5% 15% 16%

5% 9% 13% 3%

24% 12% 17%

69% 56%

11% 19%

82%

31%

22%

65% 73% 72%

8%

8%

67% 67%

44% 69%

8% 17% 7% 6% 6% 6%

4%

5% 8% 16% 7% 9% 6%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Rarely or Never Have PIK Rate ≤1% 2% 3% 4% 5% >5%

13% 18% 17% 17% 6% 8% 9% 14%

28% 20%

20% 32%

22%

16% 28% 18%

32% 18%

28% 35% 16%

13%

22%

43%

9%

14% 12%

17%

19%

9% 25%

28%

13%

37%

26% 18%

13% 8%

17% 9% 11% 18% 6%

4% 9% 8% 4% 9% 11%

9% 7% 6%

12% 5% 6% 7%

0%

25%

50%

75%

100%

Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

≤12% 13% 14% 15% 16% 17% 18% 19% 20% >20%

16.6%

16.5% 16.5%

16.8%

15.9% 15.1%

14.5% 13.9%

13.3%

15.3%

13.7%

14.5% 15.0%

13%

14%

15%

16%

17%

Q411

Q212

Q412

Q213

Q413

Q214

Q414

Q215

Q415

Q216

Q416

Junior Debt Market Analysis

11

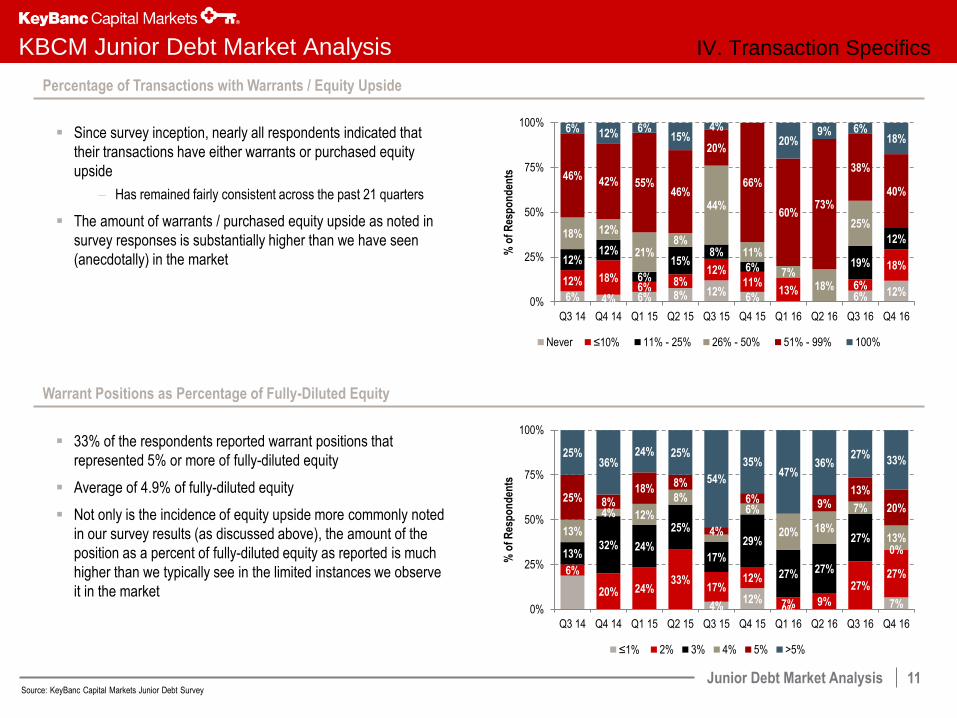

KBCM Junior Debt Market Analysis

Percentage of Transactions with Warrants / Equity Upside

Warrant Positions as Percentage of Fully-Diluted Equity

Since survey inception, nearly all respondents indicated that

their transactions have either warrants or purchased equity

upside

– Has remained fairly consistent across the past 21 quarters

The amount of warrants / purchased equity upside as noted in

survey responses is substantially higher than we have seen

(anecdotally) in the market

33% of the respondents reported warrant positions that

represented 5% or more of fully-diluted equity

Average of 4.9% of fully-diluted equity

Not only is the incidence of equity upside more commonly noted

in our survey results (as discussed above), the amount of the

position as a percent of fully-diluted equity as reported is much

higher than we typically see in the limited instances we observe

it in the market

Source: KeyBanc Capital Markets Junior Debt Survey

IV. Transaction Specifics

6% 4% 6% 8% 12% 6% 6% 12%

12% 18% 6%

8% 12%

11% 13% 6%

18% 12% 12%

6%

15% 8%

6% 19%

12% 18% 12%

21% 8%

44%

11%

7% 18%

25%

46% 42% 55%

46%

20%

66%

60% 73%

38%

40%

6% 12% 6% 15%

4%

20% 9% 6%

18%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Never ≤10% 11% - 25% 26% - 50% 51% - 99% 100%

4% 12%

0% 7%

6%

20% 24% 33%

17% 12%

7% 9%

27% 27%

13% 32% 24%

25%

17%

29%

27% 27%

27% 0%

13%

4% 12%

8% 6%

20% 18%

7%

13%

25% 8% 18%

8%

4%

6% 9% 13%

20%

25% 36%

24% 25%

54%

35% 47%

36% 27%

33%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

≤1% 2% 3% 4% 5% >5%

Junior Debt Market Analysis

12

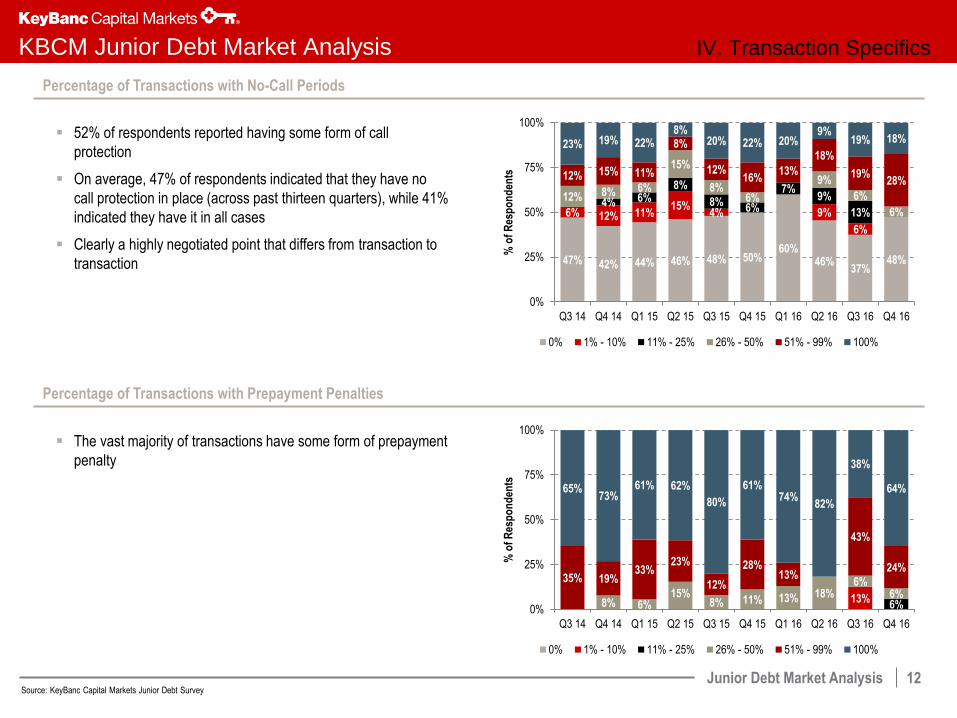

KBCM Junior Debt Market Analysis

Percentage of Transactions with No-Call Periods

Percentage of Transactions with Prepayment Penalties

The vast majority of transactions have some form of prepayment

penalty

52% of respondents reported having some form of call

protection

On average, 47% of respondents indicated that they have no

call protection in place (across past thirteen quarters), while 41%

indicated they have it in all cases

Clearly a highly negotiated point that differs from transaction to

transaction

Source: KeyBanc Capital Markets Junior Debt Survey

IV. Transaction Specifics

47% 42% 44% 46% 48% 50% 60%

46% 37%

48%

6% 12% 11% 15%

4% 9%

6%

4% 6% 8%

8% 6%

7% 9%

13%

12% 8% 6%

15%

8% 6%

9%

6%

6%

12% 15% 11%

8%

12% 16%

13%

18%

19% 28%

23% 19% 22% 8%

20% 22% 20% 9%

19% 18%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

0% 1% - 10% 11% - 25% 26% - 50% 51% - 99% 100%

13% 6% 8% 6%

15% 8% 11% 13% 18%

6% 6%

35% 19% 33%

23%

12%

28% 13%

43%

24%

65% 73%

61% 62%

80%

61% 74%

82%

38%

64%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

0% 1% - 10% 11% - 25% 26% - 50% 51% - 99% 100%

Junior Debt Market Analysis

13

KBCM Junior Debt Market Analysis

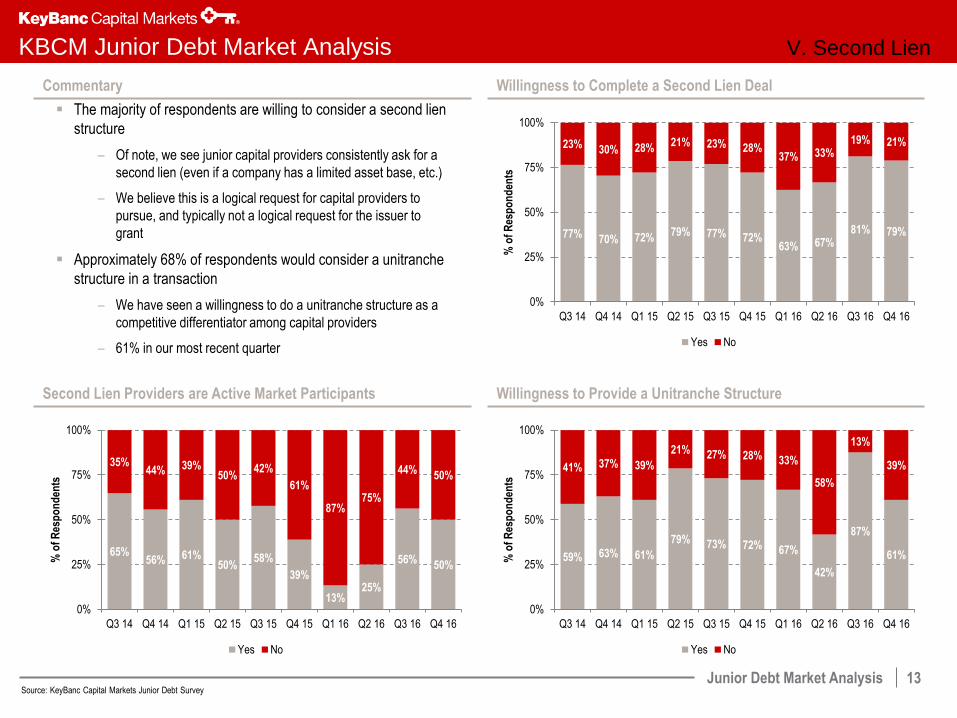

Commentary

Second Lien Providers are Active Market Participants

Willingness to Complete a Second Lien Deal

The majority of respondents are willing to consider a second lien

structure

– Of note, we see junior capital providers consistently ask for a

second lien (even if a company has a limited asset base, etc.)

– We believe this is a logical request for capital providers to

pursue, and typically not a logical request for the issuer to

grant

Approximately 68% of respondents would consider a unitranche

structure in a transaction

– We have seen a willingness to do a unitranche structure as a

competitive differentiator among capital providers

– 61% in our most recent quarter

Willingness to Provide a Unitranche Structure

Source: KeyBanc Capital Markets Junior Debt Survey

V. Second Lien

77% 70% 72% 79% 77% 72%

63% 67% 81% 79%

23% 30% 28% 21% 23% 28%

37% 33% 19% 21%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Yes No

59% 63% 61%

79% 73% 72% 67%

42%

87%

61%

41% 37% 39%

21% 27% 28% 33%

58%

13%

39%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Yes No

65% 56% 61%

50% 58%

39%

13% 25%

56% 50%

35% 44% 39%

50% 42%

61%

87% 75%

44% 50%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Yes No

Junior Debt Market Analysis

14

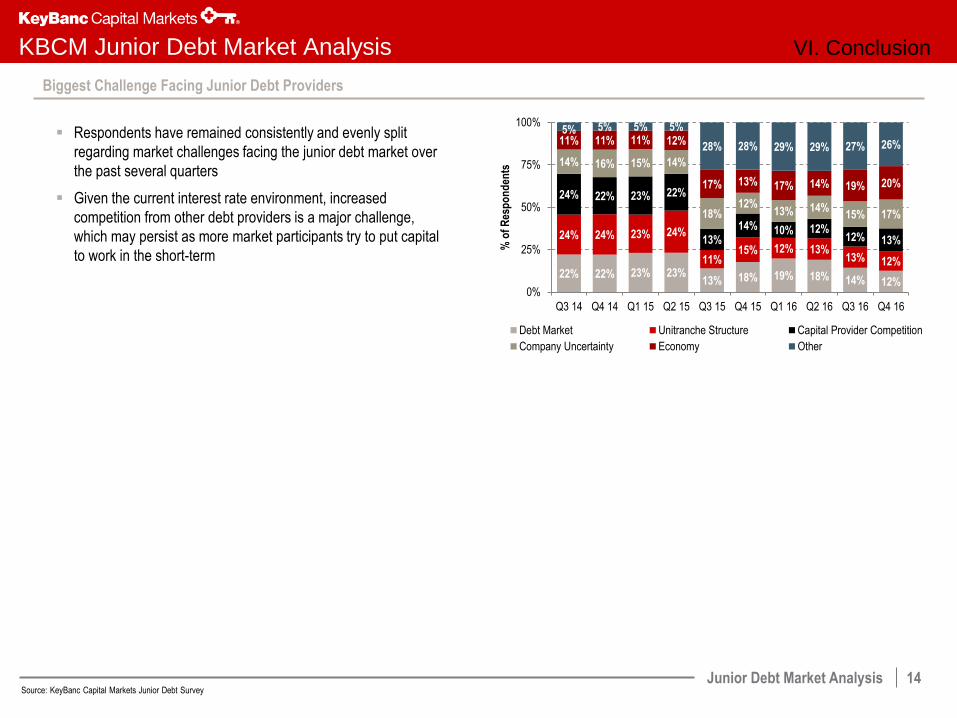

KBCM Junior Debt Market Analysis VI. Conclusion

Biggest Challenge Facing Junior Debt Providers

Respondents have remained consistently and evenly split

regarding market challenges facing the junior debt market over

the past several quarters

Given the current interest rate environment, increased

competition from other debt providers is a major challenge,

which may persist as more market participants try to put capital

to work in the short-term

Source: KeyBanc Capital Markets Junior Debt Survey

22% 22% 23% 23% 13% 18% 19% 18% 14% 12%

24% 24% 23% 24%

11% 15% 12% 13%

13% 12%

24% 22% 23% 22%

13%

14% 10% 12% 12% 13%

14% 16% 15% 14%

18% 12%

13% 14% 15% 17%

11% 11% 11% 12%

17% 13% 17% 14% 19% 20%

5% 5% 5% 5%

28% 28% 29% 29% 27% 26%

0%

25%

50%

75%

100%

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

% o

f R

esp

on

den

ts

Debt Market Unitranche Structure Capital Provider Competition

Company Uncertainty Economy Other