1

R E D E F I N I N G B O U N DA R I E SInsights from the Global C-suite Study

Figure 1. Life Sciences CxOs believe convergence is by far the top trend

Life Sciences Industry

R E D E F I N I N G B O U N DA R I E SInsights from the Global C-suite Study

We surveyed 143 top executives from the Life Sciences industry for our latest C-suite Study. So how do they differ from CxOs in other sectors?

Twin forcesCxOs say industry convergence is the key trend reshaping the business landscape –and Life Sciences CxOs are utterly convinced that’s the case. They think the shift in consumer purchasing power will also have a major impact, as patients get a greater say in how they’re treated and outcomes-based pricing takes hold (see Figure 1).

Industry convergence

66% 83%

50% 50%

46% 30%

43% 53%

32% 22%

25% 26%

24% 15%

The “anywhere”workplace

Rising cyber risk

The redistribution of consumer purchasing power

The sustainability imperative

Alternative finance and financing mechanisms

The sharing economy

Global

Life Sciences

2

R E D E F I N I N G B O U N DA R I E S | Insights from the Global C-suite StudyLife Sciences – Industry Point of View

Yet, even though they’re acutely aware of the extent to which the boundaries between different sectors are blurring, Life Sciences CxOs still expect most of the competition to come from the pharma and healthcare ecosystem. While CxOs in other sectors are steeling themselves to deal with new rivals from unexpected quarters, Life Sciences CxOs seem relatively unfazed about invaders entering their patch (see Figure 2).

Figure 2. Life Sciences CxOs aren’t looking out for rivals from ‘left field’

They’re also much more relaxed about regulation, market pressures and macro-economic factors than they were two years ago. Technology, they told us, is now the main game-changer – and that’s the first time they’ve ever put it ahead of regulatory concerns (see Figure 3).

Global

Life Sciences51% 34%

other industries

29% 54%

More competition expected from…

within the same industry

2015 Life Sciences

2013 Life Sciences

69%

87%

62%

81%

41%

54%

40%

47%

Figure 3. Life Sciences CxOs say tech has now become a bigger influence than regulation

72%

68%

Technology factors

Regulatory concerns

Market factors

People skills

Socio-economic factors

3

R E D E F I N I N G B O U N DA R I E S | Insights from the Global C-suite StudyLife Sciences – Industry Point of View

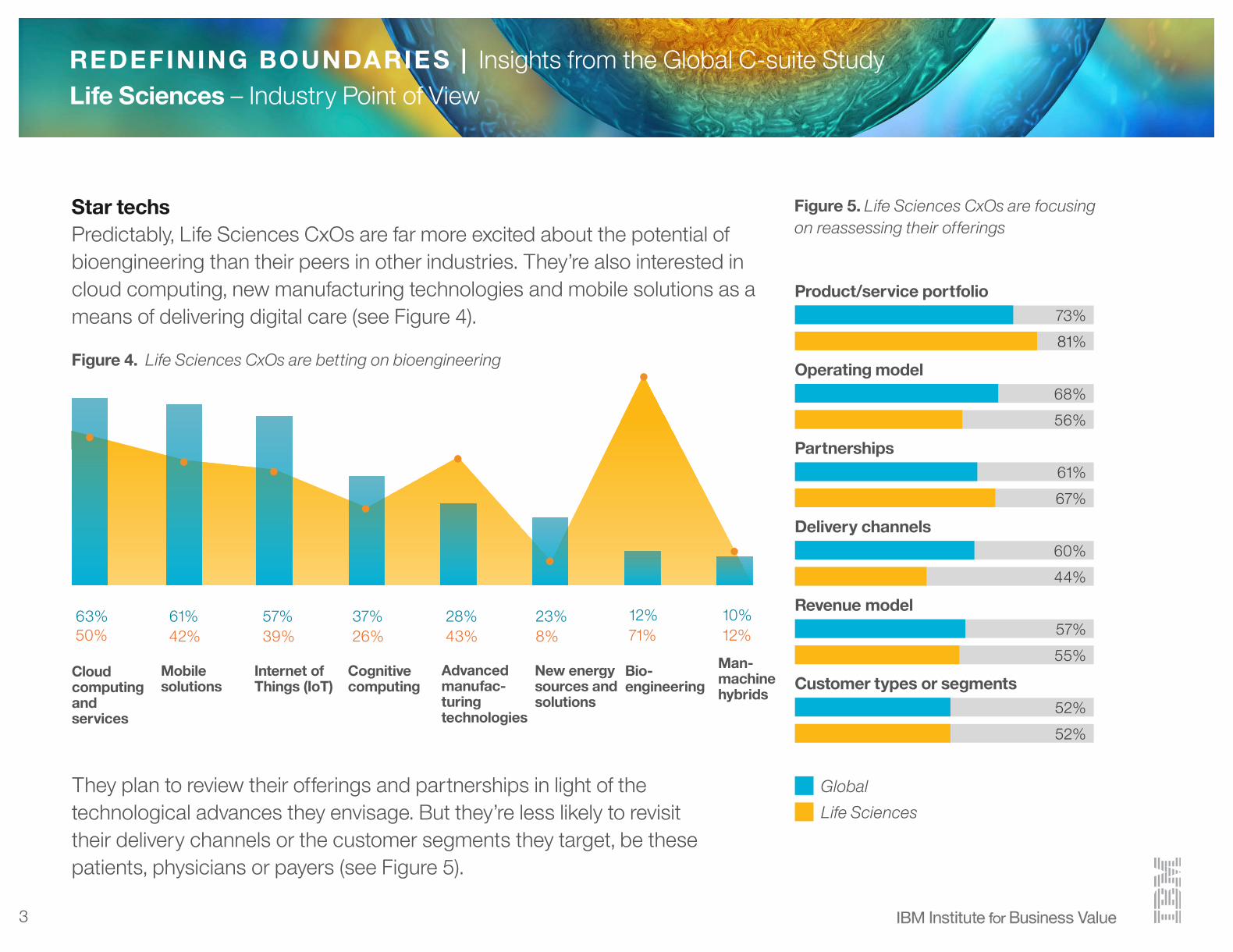

Star techs Predictably, Life Sciences CxOs are far more excited about the potential of bioengineering than their peers in other industries. They’re also interested in cloud computing, new manufacturing technologies and mobile solutions as a means of delivering digital care (see Figure 4).

Figure 4. Life Sciences CxOs are betting on bioengineering

They plan to review their offerings and partnerships in light of the technological advances they envisage. But they’re less likely to revisit their delivery channels or the customer segments they target, be these patients, physicians or payers (see Figure 5).

Cloud computing and services

63% 50%

61% 42%

57% 39%

37% 26%

28% 43%

23% 8%

12% 71%

10% 12%

Mobile solutions

Internet ofThings (IoT)

Cognitive computing

Advanced manufac-turingtechnologies

New energysources andsolutions

Bio-engineering

Man-machinehybrids

Global

Life Sciences

68%

56%

61%

67%

60%

44%

57%

55%

Figure 5. Life Sciences CxOs are focusing on reassessing their offerings

73%

81%

Product/service portfolio

Operating model

Partnerships

Delivery channels

Revenue model

52%

52%

Customer types or segments

4

14%less

© Copyright IBM Corporation 2016.Produced in the United States of America

IBM, the IBM logo, ibm.com and IBM Global Business Services are trademarks of International Business

Machines Corp., registered in many jurisdictions worldwide. Other product and service names might

be trademarks of IBM or other companies. A current list of IBM trademarks is available on the

web at “Copyright and trademark information” at ibm.com/legal/copytrade.shtml.

IBM Global Business Services Route 100

Somers, NY 10589U.S.A.

R E D E F I N I N G B O U N DA R I E S | Insights from the Global C-suite StudyLife Sciences – Industry Point of View

They also realize new technologies bring new risks. Like Healthcare CxOs, they’re especially concerned about regulatory compliance violations. But loss of intellectual property and financial risks also prey on their minds.

That said, Life Sciences CxOs are much bolder than their peers in many other industries. We identified a small group of highly successful enterprises in our overall sample. Torchbearers, as we call them, are particularly comfortable leading the way, when they’re launching new business models or new offerings. Most Life Sciences CxOs also aspire to be market pioneers (see Figure 6).

Figure 6. Most Life Sciences CxOs aim to reach the market first

Global Torchbearers

Life Sciences

80%

69%

You can see the various installments of our latest Global C-suite Study at ibm.com/csuitestudy