Long-term energy scenarios for Estonia

2. workshop 7.+8. January 2013

1. Welcome (Monday 7.1.2012: 10.00)– Translation

2. Inception report (10.30)– Purpose and general discussion– Scenarios – Balmorel model– Stream model– Next step

3. Theme discussions: Estonia perspective (14.30-16.30)– Oil Shale (Energy carriers group)– 110% rule (Security of supply group)

4. Summary from day 15. Input from expert groups (Tuesday 8.1.2013: 9.00)

– Consumption– Energy carriers (not covered above)– District heating

6. Next steps7. Bilateral meeting with Elering + WEC about inception report

INCEPTION REPORT

Increasing amount of details

• Tender– 5 pages

• Project description– 12 pages

• Inception report (draft) + data report (draft)– 28 + 67 pages

• Final inception report + data report + input from expert groups

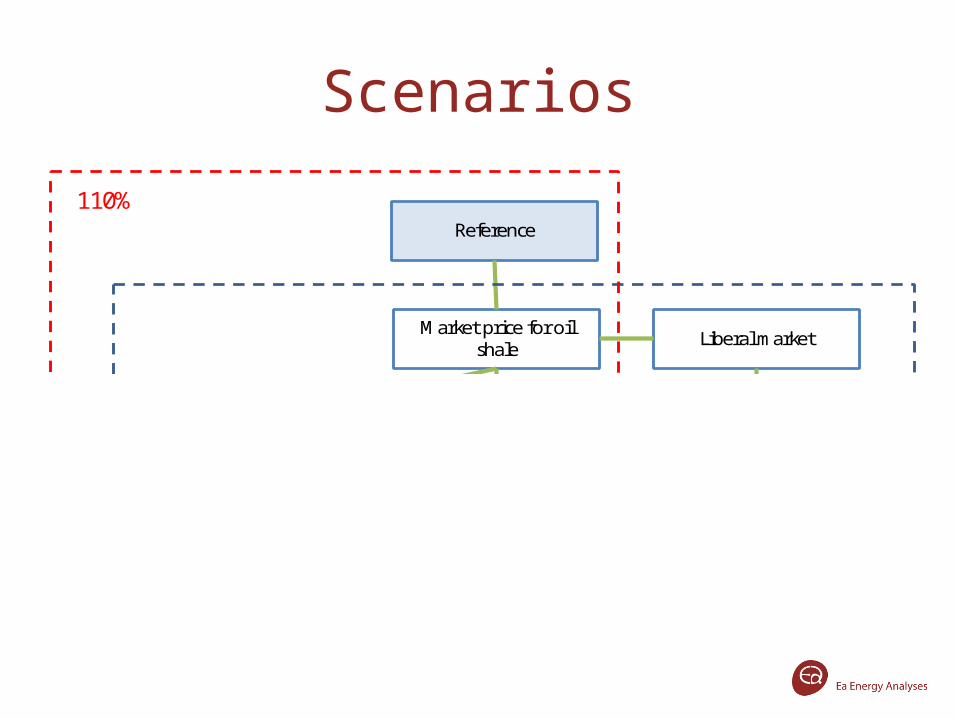

Scenarios

Reference

Market price for oil shale Liberal market

CO2 concern Renewable energy focus

CO2 market collapse

Combination scenario

Single track scenarios

110%

Estonian EE

Scenarios

Reference

Market price for oil shale Liberal market

CO2 concern Renewable energy focus

CO2 market collapse

Combination scenario

Single track scenarios

110%

Estonian EE

Scenarios

Reference

Market price for oil shale Liberal market

CO2 concern Renewable energy focus

CO2 market collapse

Combination scenario

Single track scenarios

110%

Estonian EE

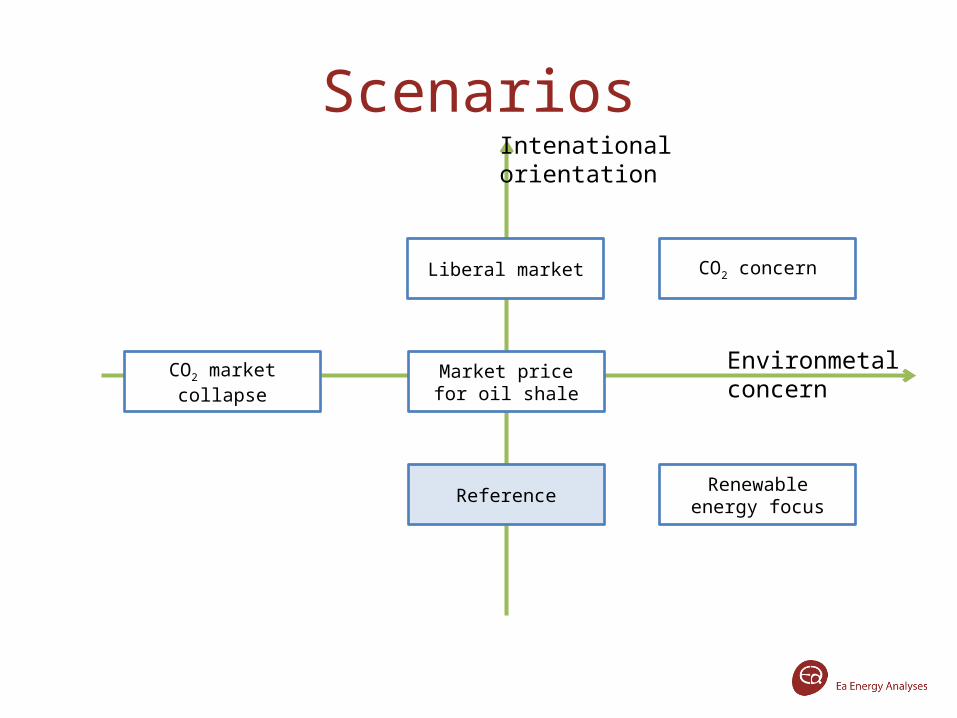

Scenarios

Reference

Market price for oil shale

Liberal market CO2 concern

Renewable energy focus

CO2 market collapseEnvironmetal concern

Intenationalorientation

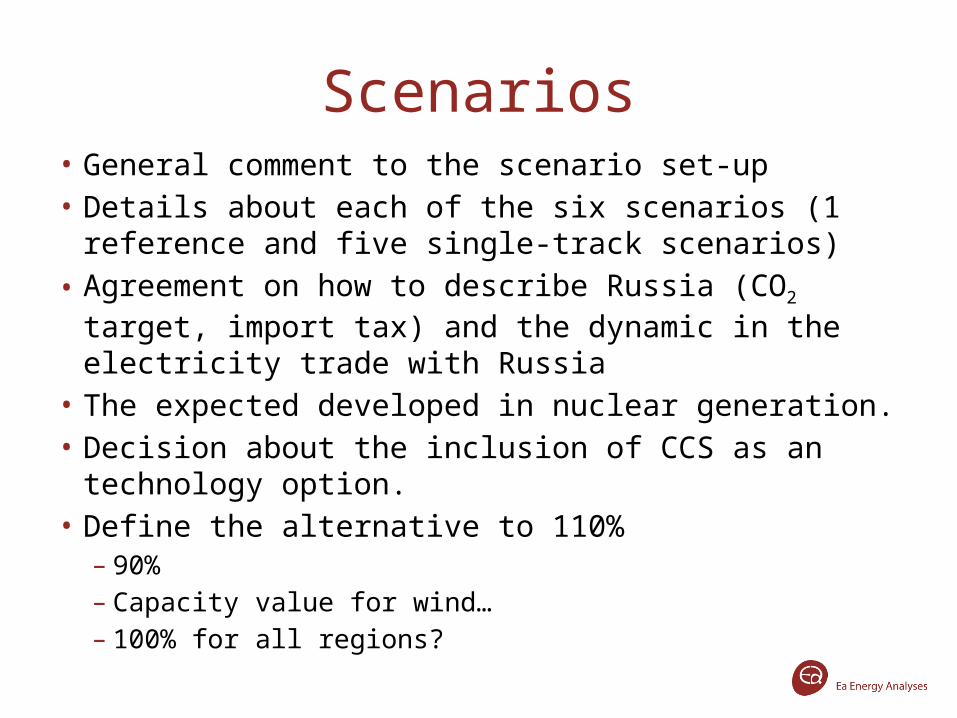

Scenarios• General comment to the scenario set-up• Details about each of the six scenarios (1 reference and

five single-track scenarios)• Agreement on how to describe Russia (CO2 target, import

tax) and the dynamic in the electricity trade with Russia• The expected developed in nuclear generation.• Decision about the inclusion of CCS as an technology

option.• Define the alternative to 110%

– 90%– Capacity value for wind…– 100% for all regions?

BALMOREL

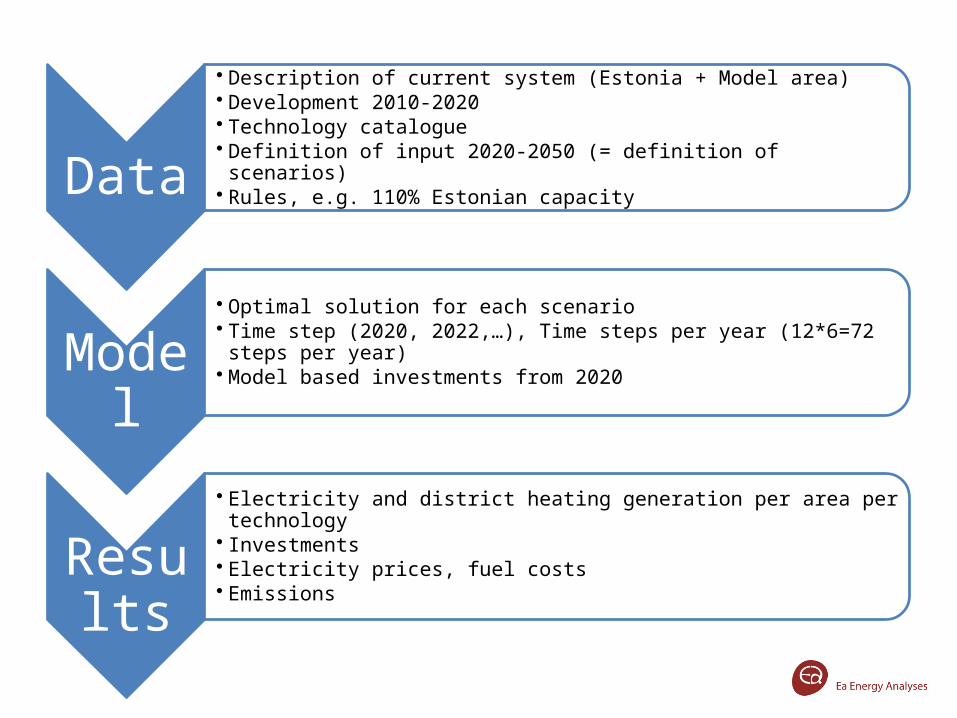

Data

• Description of current system (Estonia + Model area)• Development 2010-2020• Technology catalogue • Definition of input 2020-2050 (= definition of scenarios)• Rules, e.g. 110% Estonian capacity

Model

• Optimal solution for each scenario• Time step (2020, 2022,…), Time steps per year (12*6=72 steps per year) • Model based investments from 2020

Results

• Electricity and district heating generation per area per technology• Investments• Electricity prices, fuel costs• Emissions

Time steps: 1, 2 and 5 years

2010 2015 2020 2025 2030 2035 2040 2045 2050

Predefined capital Model driven investments in generation and transmission

Output

• Raw model results are extremely detailed• Important to maintain overview!– Study aggregated results– Drill down to detailed results• Operation of single unit

Results

• Difference between two scenarios, e.g.: – Marked price for oil shale – Reference– Liberalised market – Marked price for oil shale

• Investments in generation and transmission– Per country: Which technology

• Operation (GWh, emissions, electricity prices)– Per country

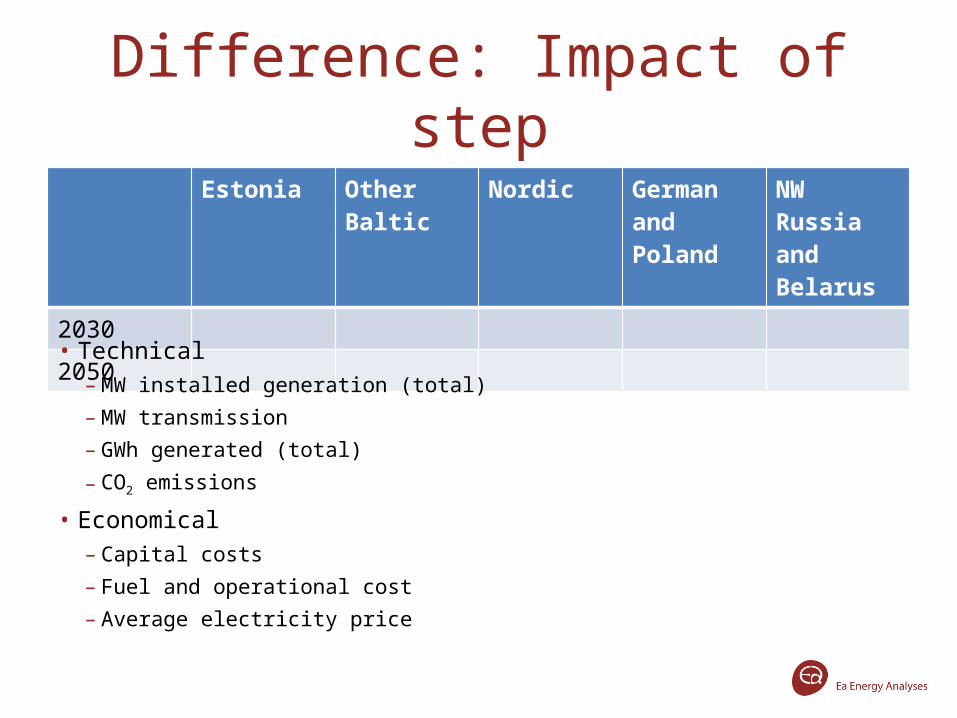

Difference: Impact of stepEstonia Other Baltic Nordic German and

PolandNW Russia and Belarus

2030

2050

• Technical– MW installed generation (total)– MW transmission– GWh generated (total)– CO2 emissions

• Economical– Capital costs– Fuel and operational cost– Average electricity price

Difference: Economic overview20302050

Estonia Other Baltic

Nordic German and Poland

NW Russia

Total

Consumer surplusGenerator profitTSO profit

Total xxx

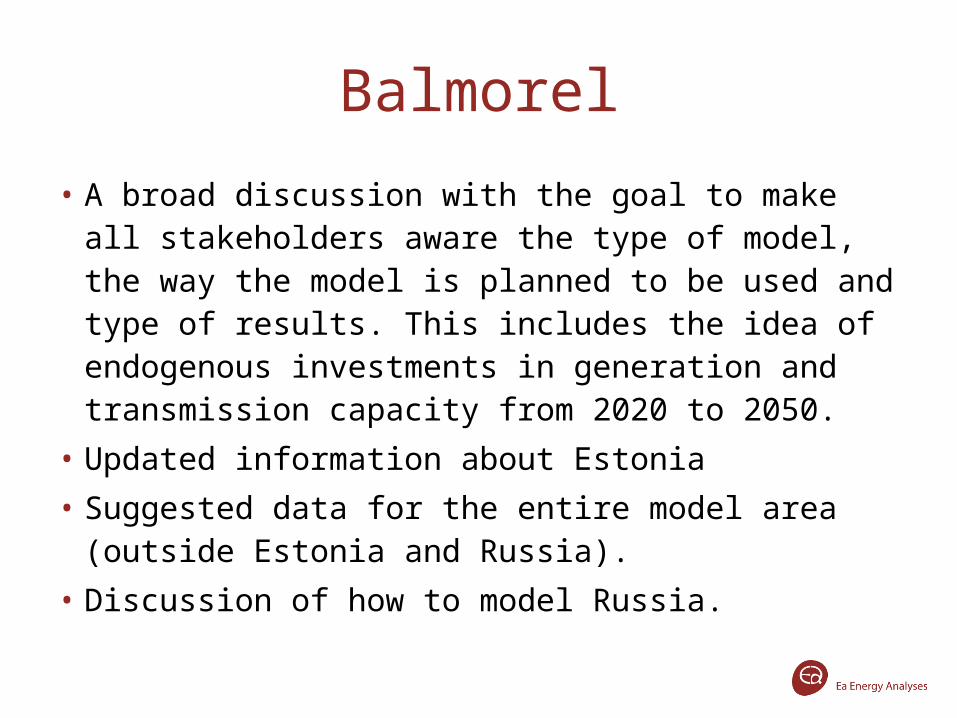

Balmorel

• A broad discussion with the goal to make all stakeholders aware the type of model, the way the model is planned to be used and type of results. This includes the idea of endogenous investments in generation and transmission capacity from 2020 to 2050.

• Updated information about Estonia• Suggested data for the entire model area (outside

Estonia and Russia). • Discussion of how to model Russia.

STREAM

Stream• Heat demand in household and service sector

– Development of building stock– New buildings (energy standards – are these complied with?)– Demolishment of existing buildings– Rates for renovation of existing buildings (cost and potentials)– Change in composition of building stock (e.g. multistory buildings => single-family house)– Demographic factors (e.g. rural => urban)

• Heat supply in household and service sector– Economic comparison of costs of energy of heat supply using different collective and individual

heating technologies– For different types of buildings: multistory, single-family, new dwellings– To determine scenarios for the expansion or contraction of district heating supply– To determine supply of energy in areas not supplied by district heating

• Electricity demand in household and service sector– Choice of methodology– Historic trends, coupling with GDP, experience from other countries– Bottom-up, vintage modeling: require information about stock of electrical equipment, projections

for their dissemination and development in specific demand

• Energy demand with industry– Sector specific projections– Historic trends per sector coupled with GDP– Input from expert groups on expected future developments for most important

branches• Transport sector

– Growth rates in the demand for transport (personkilometers)– Coupling to GDP (historic trends),experience from other countries concerning

saturation in transport demand– Development in efficiency of conventional combustion engine technologies– Introduction rate for new technologies such as electric vehicles, Compressed natural

gas– Modal-change (car => bus/train/…)– Blending rates for biofuels– Diesel produced from oil-shale

NEXT STEP

SUMMARY OF DAY 1

• Data report…

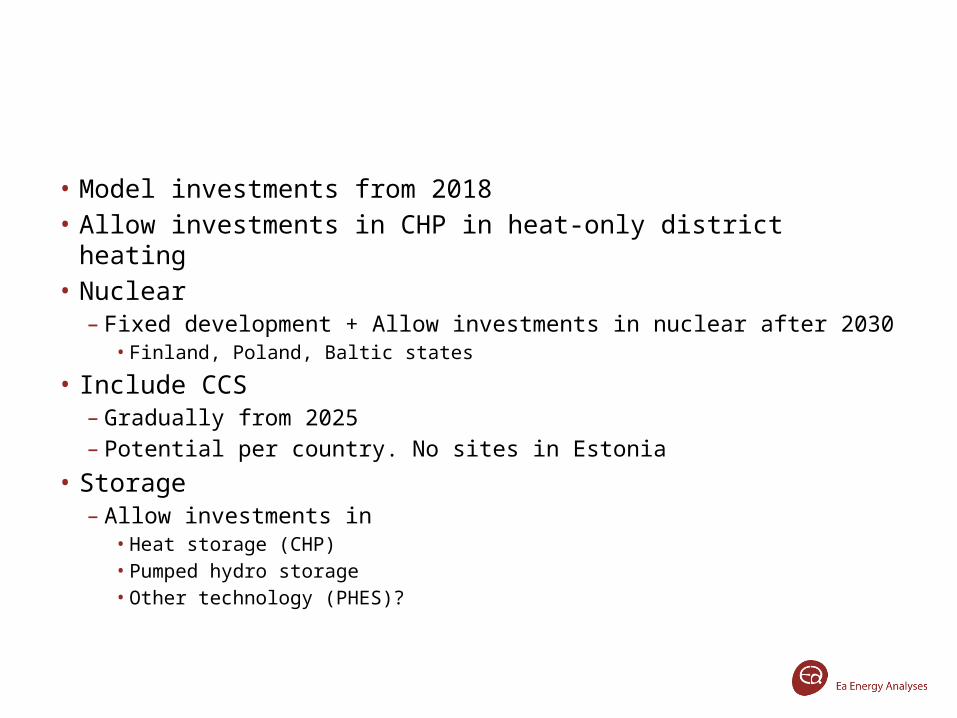

• Model investments from 2018• Allow investments in CHP in heat-only district heating • Nuclear

– Fixed development + Allow investments in nuclear after 2030 • Finland, Poland, Baltic states

• Include CCS– Gradually from 2025– Potential per country. No sites in Estonia

• Storage– Allow investments in

• Heat storage (CHP)• Pumped hydro storage• Other technology (PHES)?

• Russia and Belarus– 3 x 500 MW capacity + 700 MW to Kaliningrad– Carbon leakage…

• Border tax reflecting CO2 price

• Oil shale– Electricity generation from oil shale 100% sold on

market from 1.1.2013– Delete Oil shale at market price?

• Alternative to 110%– 0%

Reference

Liberal marketCO2 concern Renewable energy focus

CO2 market collapse

Combination scenario

110%

Scenarios

Reference

Liberal market

CO2 concern

Renewable energy focus

CO2 market collapse

Environmental concern

Internationalorientation

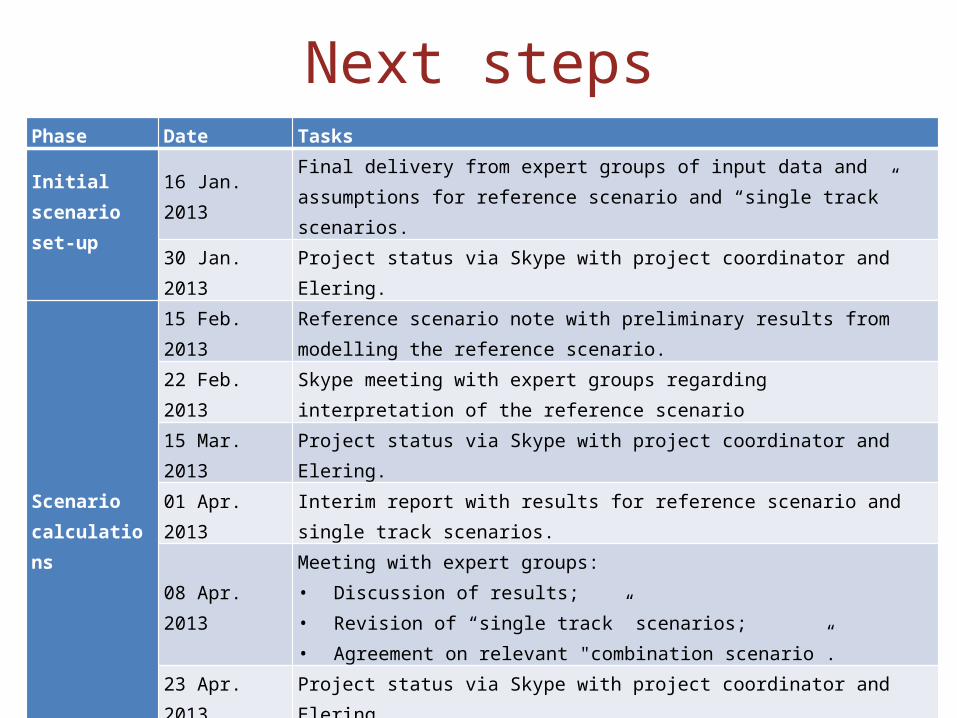

Next stepsPhase Date TasksInitial scenario set-up

16 Jan. 2013 Final delivery from expert groups of input data and assumptions for reference scenario and “single track” scenarios.

30 Jan. 2013 Project status via Skype with project coordinator and Elering.

Scenario calculations

15 Feb. 2013 Reference scenario note with preliminary results from modelling the reference scenario.

22 Feb. 2013 Skype meeting with expert groups regarding interpretation of the reference scenario

15 Mar. 2013 Project status via Skype with project coordinator and Elering. 01 Apr. 2013 Interim report with results for reference scenario and single track scenarios.

08 Apr. 2013

Meeting with expert groups:• Discussion of results;• Revision of “single track” scenarios;• Agreement on relevant "combination scenario”.

23 Apr. 2013 Project status via Skype with project coordinator and Elering.

Conclusions

07 May 2013 Draft final report

14 May 2013

Meeting with expert groups:• Discussion of main conclusions;• Identification of recommendations for important actions in the short-term in

order to achieve long-term goals and identification of important barriers.

31 May 2013 Final report and transfer of data and models.