Managing the Challenges of Conducting Business in China

Jason Wright

Managing Director

Kroll

Managing the Challenges of Conducting

Business in China

Jason Wright, Managing Director

September 12, 2014

Agenda

Environment and Challenges in China

Conducting Due Diligence in China

Detecting fraud: Knowing the red flags

Case study of fraud: MNCs in China

Managing your asset in China

Proprietary and Confidential — Kroll 3

A challenging environment in China

Many commentators have detected increased hostility to foreign investors recently in mainland China; others see the potential for economic reforms that will eventually improve the prospects for foreign investors

High-profile fraud investigations into MNCs on the part of the Chinese authorities

Antitrust probes and fines for foreign companies

Anti-corruption campaign stepped up

SOE partners also targeted

Economic slowdown

Credit squeeze in certain sectors (e.g. real estate)

Proprietary and Confidential — Kroll 4

Challenges of Doing Business in China

Lack of transparency

Corruption

Unlimited trust in local CEO

Lack of compliance culture

Professional relationships are reliant on personal relationships and favors

Existing local laws are often broad, ambiguous and subject to interpretation by authorities

No right of privacy against the state

» Turns attorney-client privileged communications on its head

Proprietary and Confidential — Kroll 5

Regulatory Landscape in China

Impact to both local and international companies in China

» Both bribe giver and recipient are now penalized

» Clamping down on violations of Anti-Money Laundering and Anti-Trust

» Risk of violating state secrets law

– How does this impact your due diligence and investigation?

» Impact of international regulations

– Need for a “China” approach to compliance

» Is increased enforcement positive? Is China simply moving towards a situation analogous to that in the US or Europe?

Proprietary and Confidential — Kroll 6

No dramatic changes in legislation, but enforcement has increased!

Fraudsters are getting smarter

» Large scale and increased complexity of fraud schemes. Some in high positions or by shareholders.

» Collusion across departments and functions – enables the fraudsters to stay undetected and reap illicit profits

» Conflicts of interest

» Use of external accomplices/ third party intermediaries to distance the fraudsters from the entities

» Use of offshore entities to cover fraudster’s traces

Fraud trends in China: common schemes

Proprietary and Confidential — Kroll 7

The Art of Due Diligence – what do Greek statues and

Chinese businesses have in common?

In September 1983 the J.Paul Getty Museum was offered a statue, an ancient Greek kouros, for almost USD 10 million.

The Getty was cautious and commissioned some scientific tests which seemed to suggest that it was at least genuinely antique.

Yet experts who looked at the statue were able to tell instinctively and immediately that it was a fake.

Proprietary and Confidential — Kroll 8

Instinct and Analysis

Why is it that the experts could decide so quickly, without even being able to explain their decision?

Why were the buyers at the Getty unable to see the problem?

Why were the scientific methods used unable to resolve the issue?

What did later investigation reveal?

How does this relate to the wider question of buying assets?

Proprietary and Confidential — Kroll 9

Instinct and Analysis

“We will never succeed in evaluating works of art, choosing candidates, managing risk, without the skills that can be acquired only through experience; but that experience can always be enhanced by the power of data analysis and the implementation of scientific techniques.

True expertise can never provide a full objective justification of the judgments that emerge; to believe that it could is to misunderstand the nature of true expertise.”

(John Kay)

Proprietary and Confidential — Kroll 10

Why clients often already know the answer…

Asset management firm retained Kroll to undertake due diligence on an investment proposition.

The two potential investors were supposedly Indonesian and Saudi, but appeared to be being represented by a Chinese law firm via its Beijing office. The Indonesian investor claimed to have USD 20 billion in a HSBC account in Jakarta ready to invest.

Subsequent investigation showed that the supposed address of the Beijing office of the law firm was in one of the most deprived areas of the city and also listed as the address of a rather dubious looking accountancy firm.

The individual supposedly representing the law firm in Beijing turned out to be based in small estate in the North of China and to be connected to a series of insolvent companies.

Numerous other discrepancies were uncovered but we knew as soon as we saw the original request that this wasn’t genuine – and I think the client did too, even if he wasn’t admitting it to himself.

And … we didn’t charge the client for this case!

Proprietary and Confidential — Kroll 11

Trust your Instincts!

The absence of information

Unsatisfactory explanations

No one knows the principals

“It sounds too good to be true”

“It just doesn’t make sense”

BUT, do beware of the fact that these “instincts” are rooted in our native cultures. US investors, for example, fall for scams in China that they would never fall for in the US.

Proprietary and Confidential — Kroll 12

Detecting fraud: Red flags

Company culture without accountability

Change in auditors

Delay in publication of financial results

Allegation reports

Frequent change in senior management

M&A transactions unrelated to core business

Unbelievable growth story

Company with high levels of debt

High number of related parties

Proprietary and Confidential — Kroll 13

Conducting Due Diligence in China – the Issues

When entering or investing in China, it is important to understand the mind-set and reputation of the Chinese entrepreneur you are planning to do business with.

For example:

Understand the relationship between the Chinese partner and government

Identify family relationships and any potential conflicts of interest

How did the Chinese partner make their first pot of gold?

How trustworthy is the potential partner? Is he associated with individuals of ill-repute?

Proprietary and Confidential — Kroll 14

Conducting Due Diligence in China – the Process

Public records are available but are not centralized, chaotically-managed and seldom obtained using online databases

For a full picture of a subject, it is important to look at the subject’s related parties

Need to widen scope to third party relationships

Necessary reliance on source intelligence and unannounced site visits

Consideration of state secrets and data privacy legislation

Proprietary and Confidential — Kroll 15

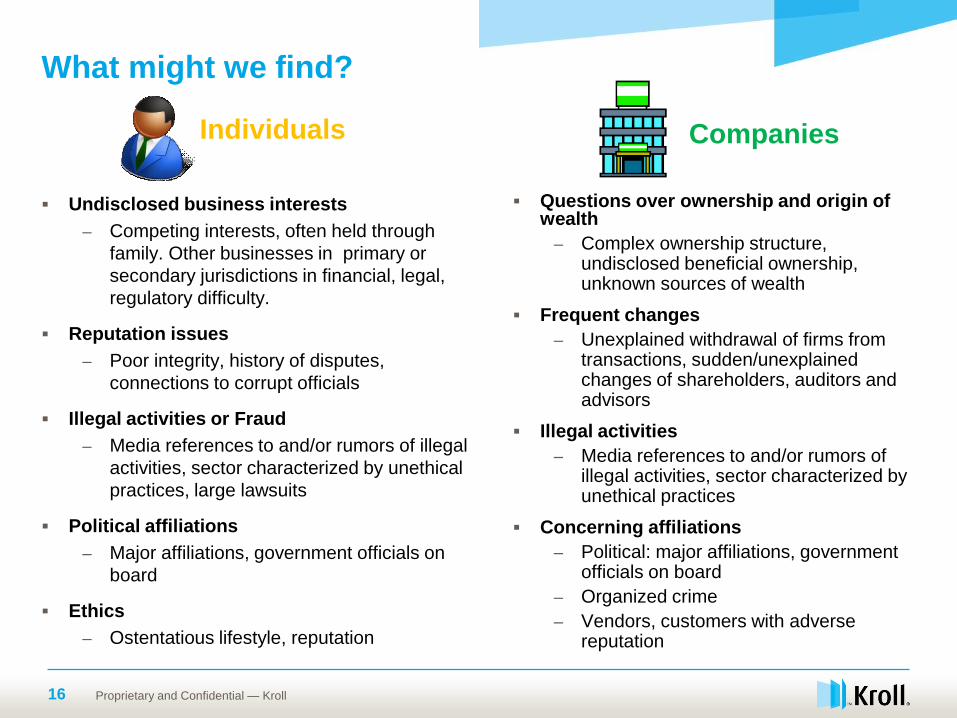

What might we find?

Individuals

Undisclosed business interests

– Competing interests, often held through

family. Other businesses in primary or

secondary jurisdictions in financial, legal,

regulatory difficulty.

Reputation issues

– Poor integrity, history of disputes,

connections to corrupt officials

Illegal activities or Fraud

– Media references to and/or rumors of illegal

activities, sector characterized by unethical

practices, large lawsuits

Political affiliations

– Major affiliations, government officials on

board

Ethics

– Ostentatious lifestyle, reputation

Companies

Questions over ownership and origin of wealth

– Complex ownership structure, undisclosed beneficial ownership, unknown sources of wealth

Frequent changes

– Unexplained withdrawal of firms from transactions, sudden/unexplained changes of shareholders, auditors and advisors

Illegal activities

– Media references to and/or rumors of illegal activities, sector characterized by unethical practices

Concerning affiliations

– Political: major affiliations, government officials on board

– Organized crime

– Vendors, customers with adverse reputation

Proprietary and Confidential — Kroll 16

Increasing Scrutiny of FCPA Compliance

Regulators expect anti-corruption due diligence in high risk countries or emerging markets

Regulators expect anti-corruption due diligence will be a standard component of any transaction that involves a potential FCPA risk

FCPA transaction testing as part of the due diligence process

Newly acquired businesses should be brought into full FCPA compliance

Pre-closing due diligence may allow avoidance/limitation of successor liability

Self-reporting being taken into account by DOJ/SEC

Proprietary and Confidential — Kroll 17

How Fraud is Uncovered Tips are by far the most common detection method

Source: ACFE – 2014 Report to the Nations

Proprietary and Confidential — Kroll 18

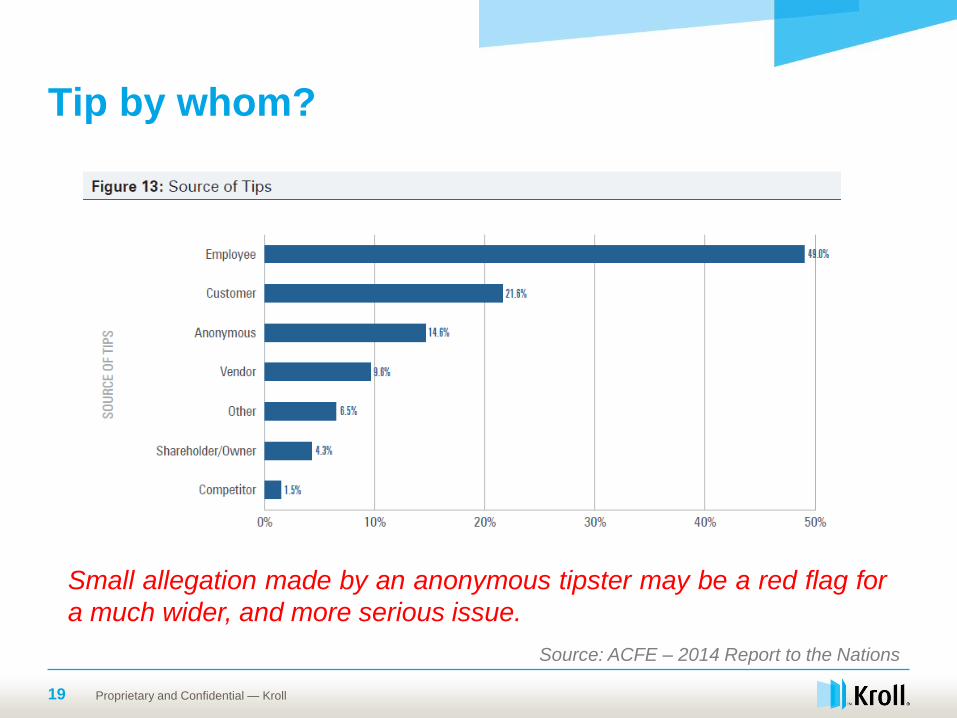

Tip by whom?

Source: ACFE – 2014 Report to the Nations

Proprietary and Confidential — Kroll 19

Small allegation made by an anonymous tipster may be a red flag for

a much wider, and more serious issue.

Case study of fraud: MNCs in China

BACKGROUND

An anonymous tip was received alleging that one of the client’s regional offices was making up revenue figures.

An initial review of documents by the company’s internal audit team did not reveal any irregularities and the transactions seemed to be substantiated by proper documentation.

Management requested an independent investigation to validate the allegation.

WHAT WE DID:

Investigation involved a thorough review of the regional office’s sales contracts, sales orders, commission payments, rebates and receipt records. Interviews with the sales and customer service teams were also conducted.

The review identified that some sales recorded in the accounting ledgers could not be vouched to genuine supporting documents. The sales contracts were found to be fictitious, with discrepancies noted between the regional office’s copies and the copies provided to the company’s headquarters.

Proprietary and Confidential — Kroll 20

As a result, the investigation was expanded to review documents kept in other regional offices and compare the same with the headquarters’ records.

It was found that a large proportion of the contracts was not legitimate. The company was eventually ordered by the SEC to restate their revenue for the past three years due to unreliable reported financial performance.

Case study of fraud: MNCs in China

Proprietary and Confidential — Kroll 21

Potential challenges we can expect during

internal investigations

Taking into account cultural differences and

attitudes to books and records

Internal disciplinary - company has already

terminated the employment of the suspect employee

Data protection – transporting cross-border and personal data on corporate device etc.

Do we need to report our findings to law enforcement or to any other regulator and if so under what circumstances?

Internal investigation relating to fraud or regulatory issue - wider reaching implications beyond the obligation to self-report or pursue actions for recoveries?

Proprietary and Confidential — Kroll 22

Managing assets in China

Advice we give our clients

Mitigation/compliance measures put in place must be instituted by local personnel but originate from head office

Unannounced visits by someone from head office or with little advance. Often internal audits are pre-planned, making it easy for the local office to “prepare” documents to comply with auditors

Fraud training for internal auditors is critical in spotting red flags

Regular data analytics

Proprietary and Confidential — Kroll 23

QUESTIONS AND ANSWERS

Proprietary and Confidential — Kroll 24

Jason Wright

Managing Director

Kroll

1701-02 Central Plaza

18 Harbour Road

Wanchai, Hong Kong

Tel: +852 2884 7705