MasteringBusinessFinance

ii / Business Management Daily

Authors: NeilGriffin,DonBattle,RaymondJ.Lipay Editor: KathyA.Shipp Editorial Director: PatrickDiDomenico Associate Publisher: AdamGoldstein Publisher: PhillipA.Ash

©2011,2005,1996,BusinessManagementDaily,adivisionofCapitolInformationGroup,Inc.,7600ALeesburgPike,WestBuilding, Suite 300, FallsChurch,VA22043-2004;www.BusinessManagementDaily.com;phone: (800)543-2055.Allrightsreserved.Nopartofthisreportmaybereproducedinanyformorbyanymeanswithoutwrittenpermissionfromthepublisher.PrintedinU.S.A.

ISBN:1-880024-09-8

“Thispublicationisdesignedtoprovideaccurateandauthoritativeinformationinregardtothesubjectmattercovered.It issoldwiththeunderstandingthatthepublisherisnotengagedinrenderinglegal,accountingorotherprofessionalservice.Iflegaladviceorotherexpertassistanceisrequired,theservicesofacompetentprofes-sionalpersonshouldbesought.”—From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a committee of publishers and associations.

Mastering Business Finance / iii

ContentsWhat Every Manager Should Know 1 Are You Savvy About Finance? 2

1. Learning the Tools of the Trade 3 The Balance Sheet 3 Sample Corporate Balance Sheet 4 Assets 5 Liabilities and Equity 5 The Income Statement 5 Sample Income Statement 6 The Statement of Cash Flows 7 Sample Statement of Cash Flows 8

2. How the Financial Pros Use These Tools 10 Troubleshooting With Ratio Analysis 10 Ten Critical Ratios 10 Does your firm have enough cash to pay its bills? 12 To leverage or not to leverage? 12 How profitable is your firm? 12 Should you provide credit to a customer? 12

3. AnsweringSomeDifficultFinancialQuestions 14 AQuestionofProfitMargins 14 A Question of Working Capital 15 RMA’s Annual Statement Studies 15 A Question of Returns 16 A Question of Asset Management 17 A Question of Debt Strategy 18 A Question of Purchasing 19 A Question of Stability 20

4. ProfitFromYourBudget 22 The Budgeting Process 22 Developing a Budget System That’s Right for You 22 Organizing a Budget Team 23 The Budget Committee 24 The Budget Chairman 24 Team Budgeting 24 A Look at Zero-Base Budgeting 25 What Not to Expect From a Budget 27

5. ShouldYouUseaFixedorVariableBudget? 29 Limitations of a Fixed Budget 29 How Rising Sales Can Affect a Fixed Budget 29 How Falling Sales Can Affect a Fixed Budget 30 Comparing Changes 30

iv / Business Management Daily

Using a Variable Budget 30 The Need for Flexibility 30 Budgeting After the Fact 31 Getting What You Pay For 31

6. ProducinganEffectiveBudget,StepbyStep 32 Step 1: Develop a Sales Forecast 32 Step 2: Develop Measures of Activity 33 Step 3: Collect Historical Data 34 Step 4: Do Cost Analysis 34 Step 5: Determine Budget Allowances 35 Expense Budget, Year Ending Dec. 31: ABC Corporation 36 Step 6: Review Expense Budgets 37 Step7:EstimateProfits 37 Using Your Budget 38 Remember to Follow Up 38 Revising Your Budget 38

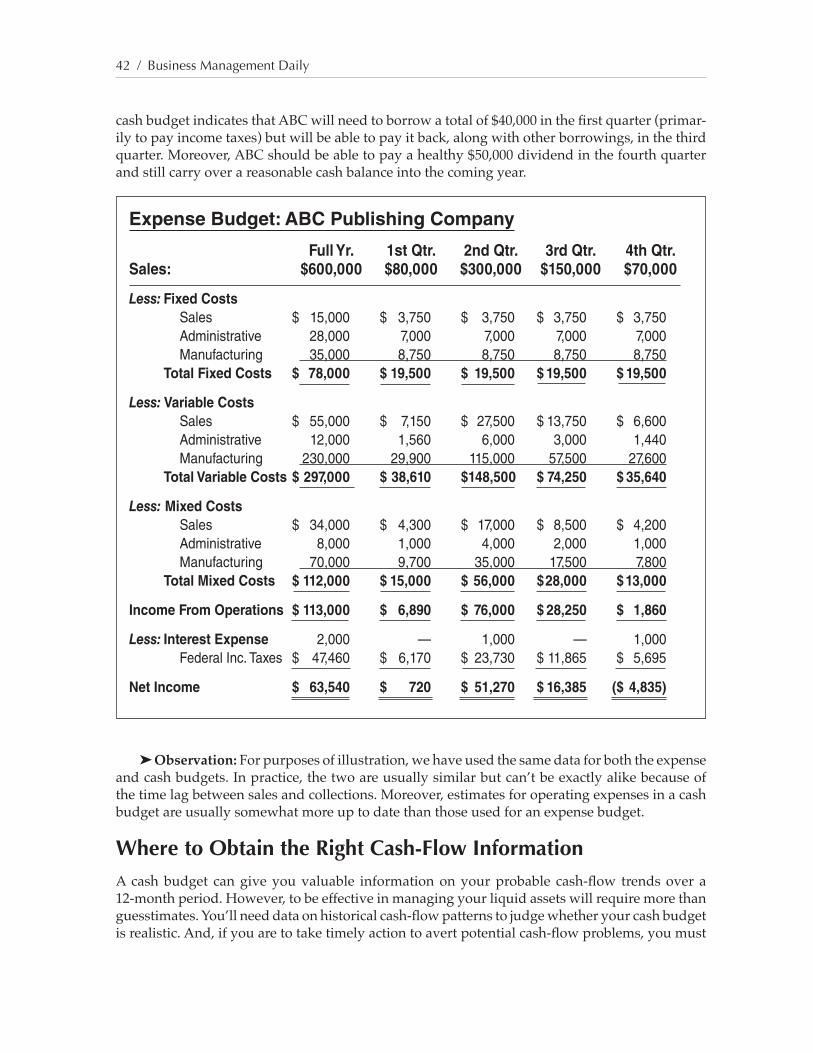

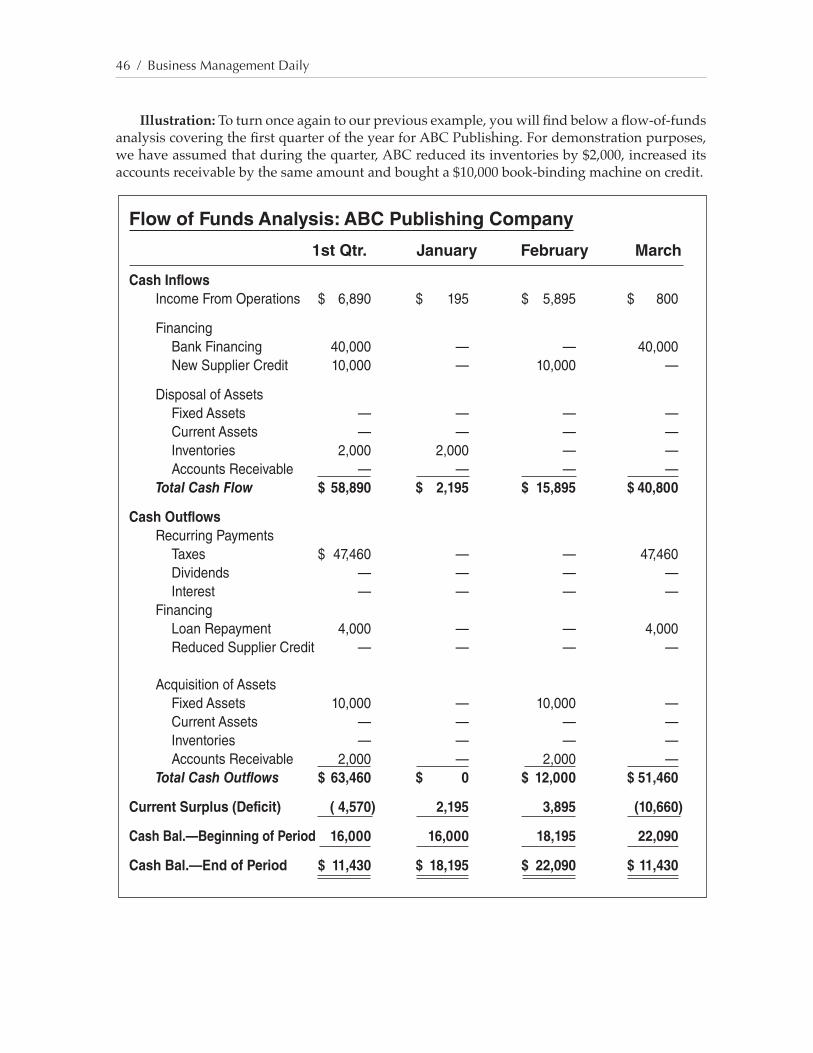

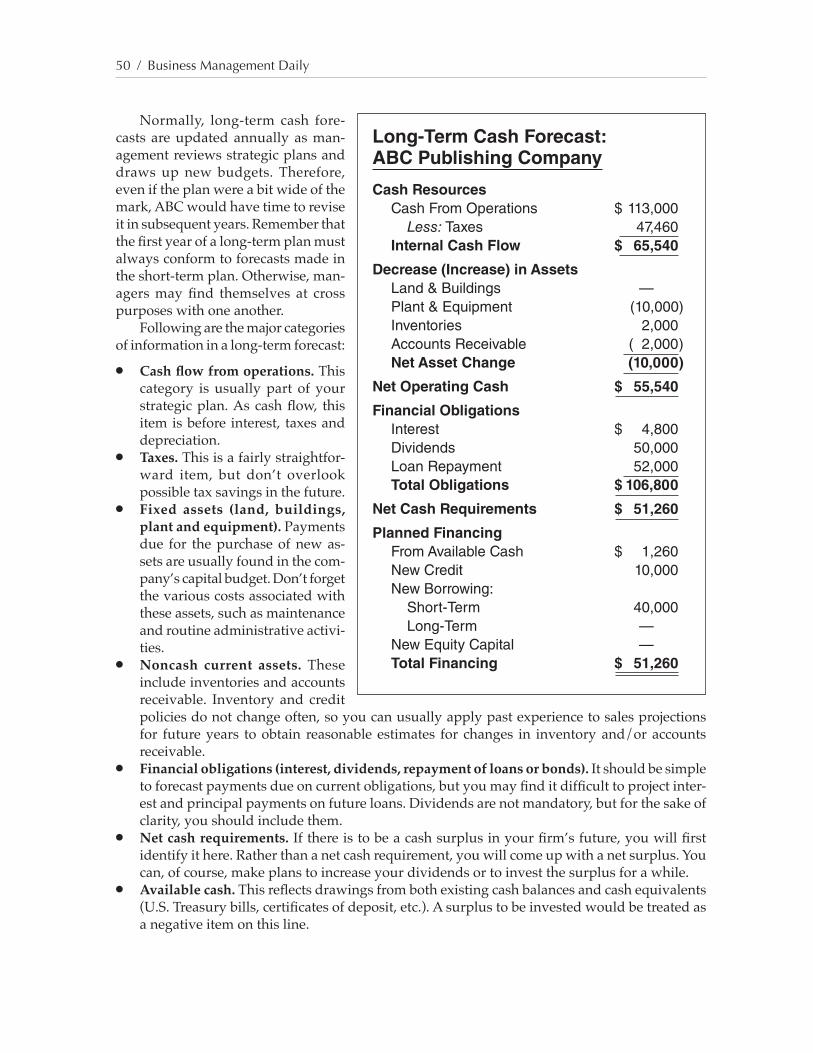

7. ManagingYourCash 40 Making Cash-Flow Decisions 40 Using Your Cash Budget 41 Where to Obtain the Right Cash-Flow Information 42 Expense Budget: ABC Publishing Company 42 Cash Budget: ABC Publishing Company 43 Receipts and Disbursements Analysis 43 Receipts and Disbursements Analysis: ABC Publishing Company 45 Flow of Funds Analysis 45 Flow of Funds Analysis: ABC Publishing Company 46 Forecasting Your Cash Flow 47 Preparing a Short-Term Cash-Flow Forecast 48 Role of Cash-Flow Assumptions 48 Using a Long-Term Cash-Flow Forecast 49 Adapt Flow-of-Funds Analysis 49 Long-Term Cash Forecast: ABC Publishing Company 50 Keeping Cash Flow Under Control 51 The Cash-Flow Statement 51 Liquidity Report 51 Flow-of-Funds Statement 52 Making Your Cash Count 53 Managing a Financial Emergency 53 Priority List 54

8. CapitalInvestmentBasics 56 How to Prepare a Capital Investment Proposal 56 Classifying Capital Spending Projects 56 Avoiding Common Pitfalls 57 Calculating Your True Capital Costs 58 Assessing the Cost of Debt 58 What Are Equity Costs? 58

Mastering Business Finance / v

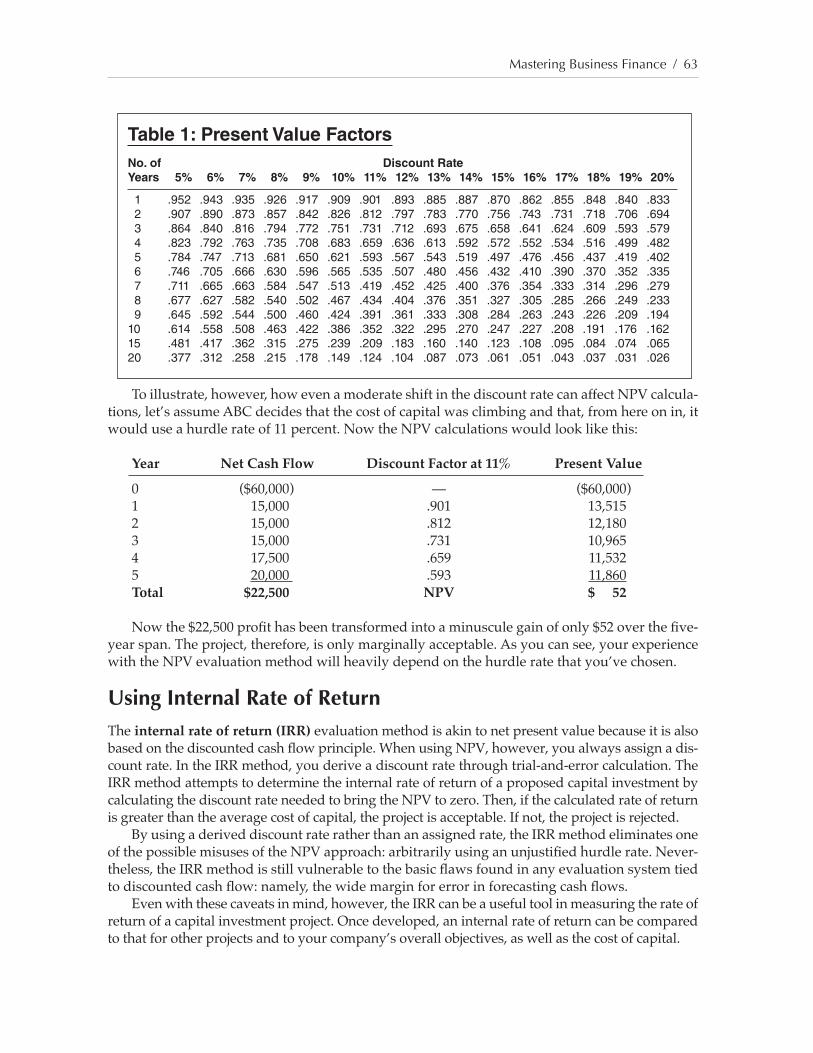

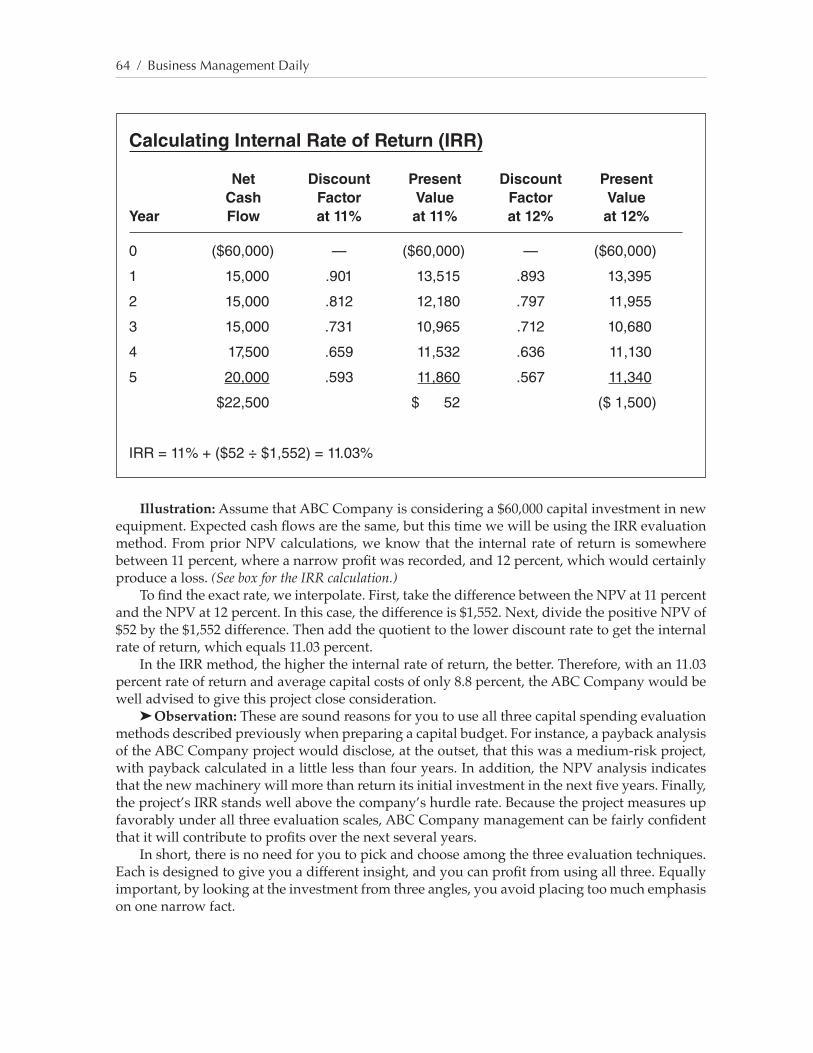

Ways to Measure Your Expected Return 59 The Payback Method 59 Using Net Present Value to Measure Return 61 Understanding the Discounting Concept 61 Discounting to Find NPV 62 Table 1: Present Value Factors 63 Using Internal Rate of Return 63 Calculating Internal Rate of Return (IRR) 64 The Hurdle Point: Uses and Misuses 65 Determining Flexible Hurdle Rates 65 Analyzing Your Capital Investment Risks 66 Weighted-Risk Analysis 67 Adjusting for Probabilities 67 Alternate Scenarios Measure Risk 68 Probability Adjustment—ABC Company 68

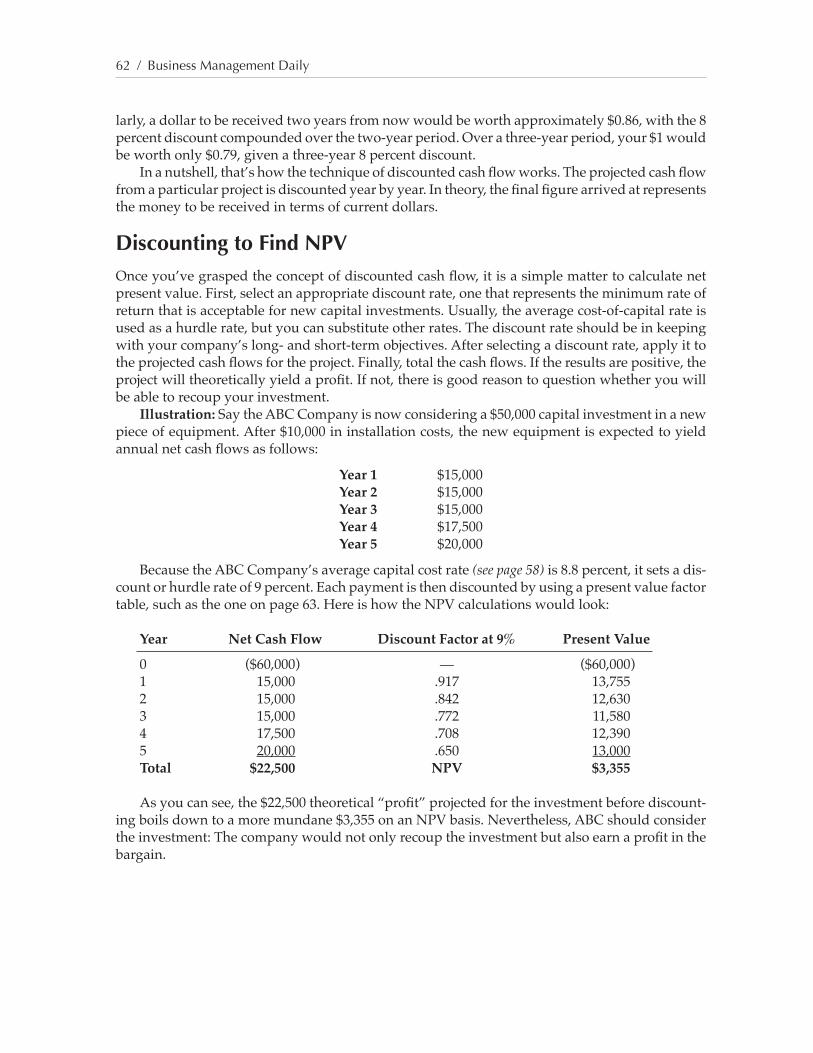

9. HowtoRaiseMoney 69 Keep a Business Plan on Hand 69 Contents of a Business Plan 69 When a Shorter Proposal Will Do 70 Where to Look for Funds 71 Internal Financing 71 Customers Come First 71 Make Your Employees Owners 72 The ABCs of Bank Borrowing 72 Finding the Right Type of Loan 73 Score Your Loan Worthiness 75 The Loan Application 75 If Your Banker Turns You Down... 77 Loan Guarantees From the SBA 77 How PLP Works 78 Loans From Commercial Finance Companies 78 Using a Factor 79 Bond Financing 80 Raising Equity Capital 81 How to Attract a Venture Capitalist 81 Evaluating a Venture Capitalist 82 Dealing With an SBIC 82 The Role of the Private Investor 83 Regulation D Private Placement 84 Raising Capital Through a Public Stock Offering 85 Other Methods of Financing 86 A Look at Leasing 86 Don’t Forget Development Corporations 87

Glossary 88

1

What Every Manager Should Know

Nosubjectseemstopervadeourlivesasmuchasfinance.Whetherit’swres- tlingwithyourfamilybudgetorseeingifyourcompanyqualifiesfora bankloan,financeloomslargerthananyothertechnicalsubjectonadaily

basis.Withdownsizingofcompaniesandstaffs,managersateverylevelarehav-ingtofacefinancialmattersinever-greaterproportionstoday.Ifyouhaven’tyetbeenaskedtoscaledowninventoriesorsetupfinancingfordepartmentalprojects,chancesareyouwillbesoon.

Intoday’scorporateenvironment,nonfinancialmanagersareexpectedtomakefinancialdecisionsfast.Infact,yourdecisionoftenwasdue“yesterday.”Ifthat’snotenoughpressure,thearrivalofcomputersandcyberspacehasgivenyourcompeti-tionaccesstomorefinancialfacts,ingreaterdetailandmorepromptly,thaneverbefore.Theneedtomakefinancialdecisionsquicklyisvitaltoyoursuccess.There’snotimeforanin-depthstudyoffinancialconceptsandtheirmeaningwhenyourbossoryouremployeesareexpectingayesornoanswerrightaway.

Thisreportismeanttostripawaythefearandconfusionyoumayexperienceaboutfinance.Itexplainsexpenseandcapitalbudgets,financialanalysisandcashmanagement,andtellsyouhowtogoaboutraisingmoney—allinlanguagethat’seasytounderstand.Weexplain jargonwherewehavetouseit—andwherewethinkthatapicturewouldbeworthathousandwords,you’llfindanexampleoranillustration.Unlikemostpublicationsonfinance,wegiveyounotjustthehowbutalsothewhyofthefinancialprocess.Ourgoal:tobringyouuptospeedfastonthefinancialtoolsyouneedtosucceedinbusinesstoday.

2 / Business Management Daily

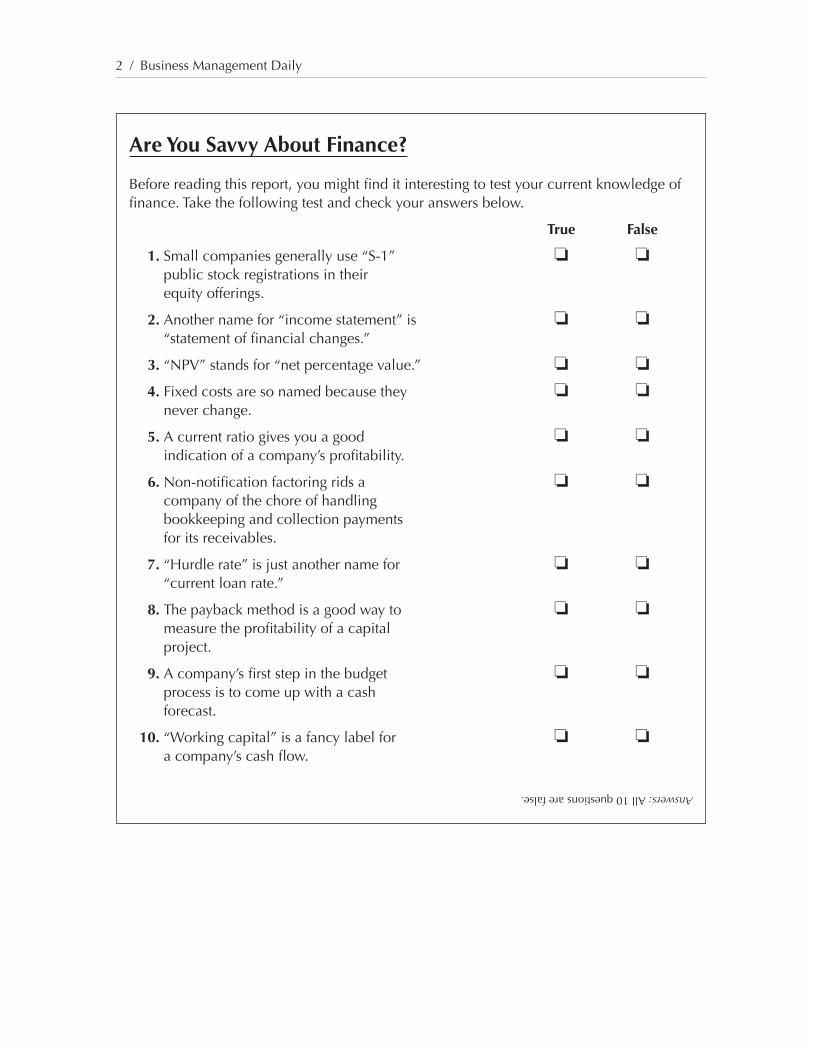

AreYouSavvyAboutFinance?

Beforereadingthisreport,youmightfinditinterestingtotestyourcurrentknowledgeoffinance.Takethefollowingtestandcheckyouranswersbelow.

True False

1. Small companies generally use “S-1” ❏ ❏ public stock registrations in their equity offerings.

2. Another name for “income statement” is ❏ ❏ “statementoffinancialchanges.”

3. “NPV” stands for “net percentage value.” ❏ ❏

4. Fixed costs are so named because they ❏ ❏ never change.

5. A current ratio gives you a good ❏ ❏ indicationofacompany’sprofitability.

6.Non‑notificationfactoringridsa ❏ ❏ company of the chore of handling bookkeeping and collection payments for its receivables.

7. “Hurdle rate” is just another name for ❏ ❏ “current loan rate.”

8. The payback method is a good way to ❏ ❏ measuretheprofitabilityofacapital project.

9.Acompany’sfirststepinthebudget ❏ ❏ process is to come up with a cash forecast.

10. “Working capital” is a fancy label for ❏ ❏ acompany’scashflow.

Answers: All 10 questions are false.

Mastering Business Finance / 3

Learning the Tools of the Trade

Togetthebigpictureoftherolefinancesplayinyourcompany,thinkaboutanymajordecision youorotherswithinyourcompanymake.Thedecisionstohire,fire,buy,sell,startuporclose

down—allarefinancialnature.Almostanyquestionthatmakesitswaytoyourdesk,andthatrequiresadecisionbyyou,canbeputintofinancialterms.

Inthestrictestsense,thefinancialproorofficerinyourcompanyisstilltheonechargedwithmakingsurethecompanyusesitsassetstobringthegreatestpossiblereturnonthemoneyin-vested.Toaccomplishthat,heorshemustmanagethoseassets,measuretheneedforadditionalassets,obtainfundstofinanceexpansionandrepayborrowedfundsfromprofitsthattheassetshavegenerated.Inshort,thefinancialofficerridesherdonincomingandoutgoingdollars.But,infact,everymanagerhasatleastpartofthatresponsibility.

Itshouldcomeasnosurprisetoyou,then,thatthebasictoolsofthetradeusedtocarryoutthesetasksbeginandendindollarsigns.Theyarecalledthebalance sheet,theincome statement andthestatement of cash flows.Thesefinancialstatementsarepreparedbyyouraccountingde-partmentoraccountantontheaccrualbasisofaccounting.Accordingtotheaccrualaccountingmethod,revenuesarerecordedwhenrealizedandexpenseswhenincurred,regardlessofthedatewhencashisactuallyreceivedordisbursed.

Formanynonfinancialmanagers,theaccrualconceptisconfusingbecausemostofusmanageourpersonalfinancesonacashbasis.Similarly,otherbusinessfinancialconceptscreatefrustra-tionandembarrassmentformanagerswho,oftenunknowingly,attemptto“simplify”thingsbyapplyingpersonalfinancialpractices.

Forinstance,mostofusregardourannualincomeonagrossbasis.Rarelydoweconsiderdepreciatingpersonalitems,suchasacarforwearandtear,oramortizinglesstangiblegoods.Anexaminationofthebalancesheet,incomestatementandstatementofcashflowswillrevealtheimportanceofunderstandingthedifferencebetweenbusinessandpersonalfinance.

TheBalanceSheetThebalancesheetisacomprehensivestatementofthefinancialpictureofyourcompanyonagivendate.Virtuallyeverybusinesspreparesabalancesheetatthecloseofitsfiscalortaxyear.Manyalsopreparesemiannualorquarterlybalancesheets,andmostshoulddoso.

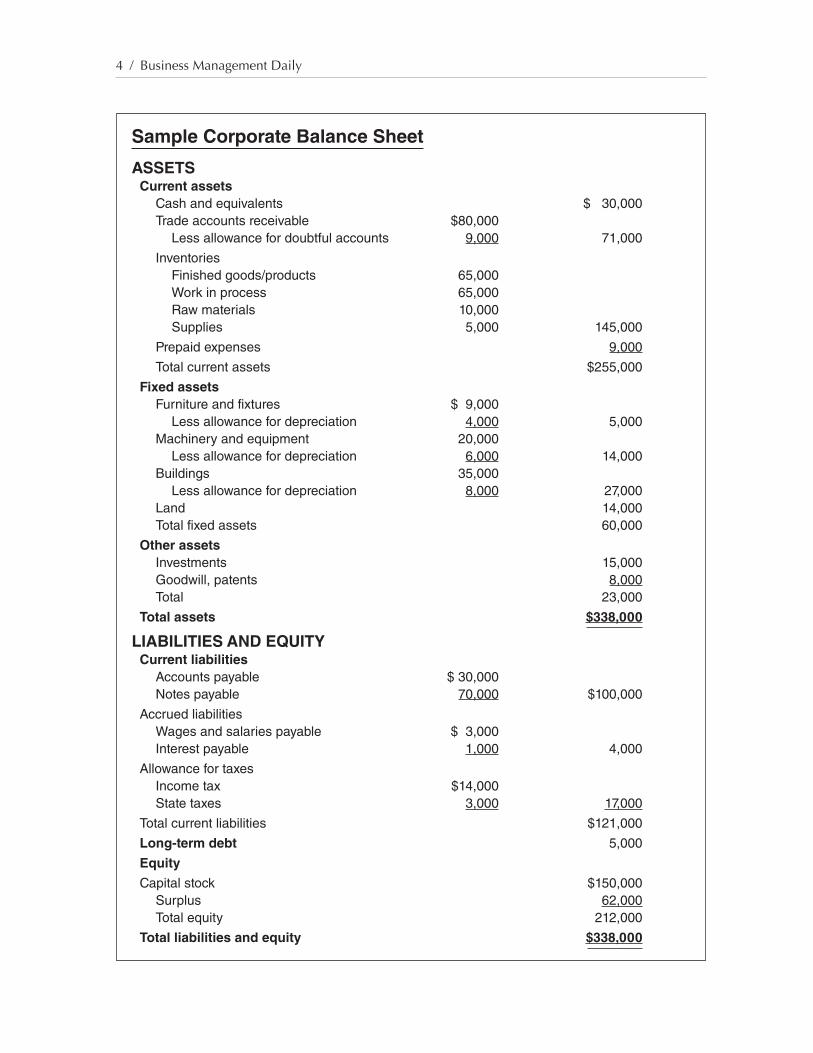

Therearetwoprimarysectionsonthebalancesheet:Thefirstone(theleftside,ifthetwosectionsareshownsidebyside)listsyourcompany’sassets,orwhatitowns.Thesecondsection(right-handside)listsliabilities,ordebts,andtheowner’sequityinthecompany.Totalliabilitiesareclaimsagainsttotalassets.Thesumoftheseliabilitiesandequityalwaysequalstotalassets(assets=liabilities+equity):hence,thename“balancesheet.”Thesimplifiedbalancesheetthatappearsonpage4mightbepreparedbyanymanufacturingcompany.Othercompanieswouldhavesimilarstatements.

1

3

4 / Business Management Daily

Sample Corporate Balance Sheet

ASSETSCurrent assets

Cash and equivalents $ 30,000 Trade accounts receivable $80,000 Less allowance for doubtful accounts 9,000 71,000

Inventories Finished goods/products 65,000 Work in process 65,000 Raw materials 10,000 Supplies 5,000 145,000

Prepaid expenses 9,000

Total current assets $255,000

Fixed assets Furniture and fixtures $ 9,000 Less allowance for depreciation 4,000 5,000 Machinery and equipment 20,000 Less allowance for depreciation 6,000 14,000 Buildings 35,000 Less allowance for depreciation 8,000 27,000 Land 14,000 Total fixed assets 60,000

Other assets Investments 15,000 Goodwill, patents 8,000 Total 23,000

Total assets $338,000

LIABILITIES AND EQUITYCurrent liabilities

Accounts payable $ 30,000 Notes payable 70,000 $100,000

Accrued liabilities Wages and salaries payable $ 3,000 Interest payable 1,000 4,000

Allowance for taxes Income tax $14,000 State taxes 3,000 17,000

Total current liabilities $121,000

Long‑term debt 5,000

Equity

Capital stock $150,000 Surplus 62,000 Total equity 212,000

Total liabilities and equity $338,000

Mastering Business Finance / 5

Followingisadescriptionofeachofthebasicbalance-sheetitemslisted,manyofwhichwillbeusedtoconstructthevariousfinancialratiosexplainedinSection2.

Assets

Current assets:Allcashheld(primarilyinbankbalancesormoneymarketfunds);assetsthatwillbeconvertedtocashinthenormalcourseofbusinesswithinonebusinessyear(tradeaccounts,notesreceivableandinventories);plusotherassetsthatcouldorwillbeconvertedwithinayear(marketableshort-termsecurities,nontradedebtsordebtinstallmentsowedtothecompanywithinayear).Otherthancashandequivalents,currentassetsincludeinventories(invariousstagesofcompletion)andprepaidexpenses(anyrent,interest,insuranceortaxespaidinadvance).

Althoughthetermdoesn’tappearinmostbalancesheets,thefollowingitemsmakeupnon-current assets.

Fixed assets: Allproperty,plantsandequipment(buildings,realestate,machines,transporta-tionequipment,officeequipment,furniture,etc.)usedinthebusiness.Theaccumulateddeprecia-tionontheseitemsisdeductedwhereapplicableinstandardaccountingpractice.

Other assets:Alllong-terminvestments,suchassecurities(stocks,bonds,mortgages),andintangible assets,suchasgoodwill,patents,trademarksandotherpaperassets,whichmaybeassignedavaluefordeterminingthetotalsalepriceofthebusiness.Intangibleassetscanhaveasignificantimpactonabusiness’sabilitytogenerateincome.However,unlikeaplantorequip-ment,theyareoftenconceptsorlegalentitlements.

Total assets: Thesumofthecurrent,fixedandotherassetslistedabove.

Liabilities and Equity

Current liabilities:Outstandingtradedebtsandobligations(tradeaccountspayable,short-termnotesandloanspayable,currentinstallmentsdueonlong-termdebts,etc.)thatwillfalldueinthecourseofnormalbusinesswithinoneyear,plusaccruedbusinessexpensespayableandaccruedfederalincometaxespayable.

Long-term liabilities or debt:Allbusinessdebtsandliabilities(long-termloans,bonds,mort-gages,etc.)payablemorethanoneyearbeyondthedateofthebalancesheet.

Total liabilities: Thesumoftheaboveitems.Shareholders’ equity (net worth):Theparvalueofthecorporation’scommonandpreferred

stock,plusanypaid-inoraccumulatedcapitalsurplusoverthisparvalue,plusanyretained earn-ings foruseinbusiness.Retainedearningsofthebusinessrepresentthetotalincomeearnedbythefirmoveritslifelessanydividendspaidouttotheowners.(Equity=bookvalueofoutstandingstock+capitalsurplus+retainedearnings)

Total liabilities and equity: Thesumoftheabovetwogroups,whichbydefinitionisalsoequaltothetotalassetsofthebusiness.

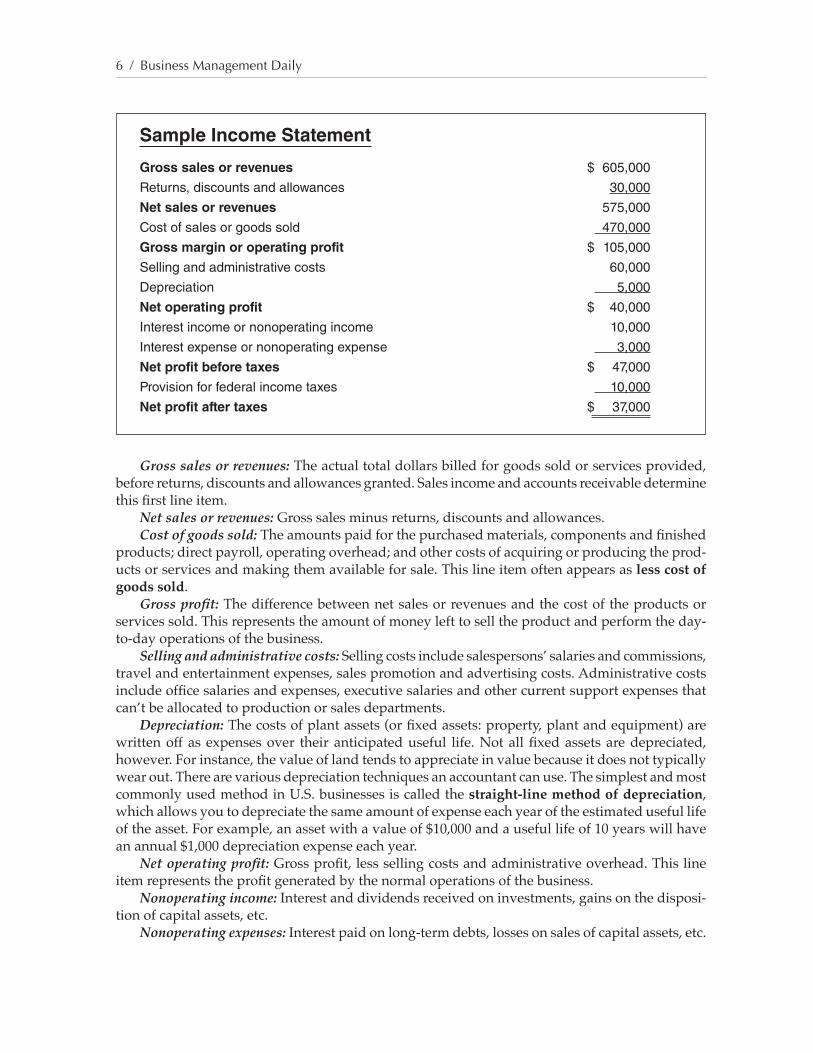

TheIncomeStatementTheincomestatement(alsocalledtheearningsreportorprofit-and-lossstatement)reflectstheresultsofoperationoveraperiodoftime,incontrasttothebalancesheet’ssnapshotviewofthecompany’sfinancialconditionatagiveninstant.Again,everybusinessmustprepareanannualincomestatementfortax,legalandotherpurposes;nevertheless,semiannual,quarterlyorevenmonthlystatementscanbeextremelyuseful.Theitemsincludedinthesimplifiedincomestatementonpage6willoftenbeneededtocreatethefinancialratiosusedinyouranalysisandcoveredinthenextsection.Briefly,hereisadescriptionoftheitemscontainedinacompany’sincomestatement:

6 / Business Management Daily

Gross sales or revenues: Theactualtotaldollarsbilledforgoodssoldorservicesprovided,beforereturns,discountsandallowancesgranted.Salesincomeandaccountsreceivabledeterminethisfirstlineitem.

Net sales or revenues: Grosssalesminusreturns,discountsandallowances.Cost of goods sold:Theamountspaidforthepurchasedmaterials,componentsandfinished

products;directpayroll,operatingoverhead;andothercostsofacquiringorproducingtheprod-uctsorservicesandmakingthemavailableforsale.Thislineitemoftenappearsasless cost of goods sold.

Gross profit:Thedifferencebetweennetsalesorrevenuesandthecostoftheproductsorservicessold.Thisrepresentstheamountofmoneylefttoselltheproductandperformtheday-to-dayoperationsofthebusiness.

Selling and administrative costs:Sellingcostsincludesalespersons’salariesandcommissions,travelandentertainmentexpenses,salespromotionandadvertisingcosts.Administrativecostsincludeofficesalariesandexpenses,executivesalariesandothercurrentsupportexpensesthatcan’tbeallocatedtoproductionorsalesdepartments.

Depreciation: Thecostsofplantassets(orfixedassets:property,plantandequipment)arewrittenoffasexpensesover theiranticipateduseful life.Notallfixedassetsaredepreciated,however.Forinstance,thevalueoflandtendstoappreciateinvaluebecauseitdoesnottypicallywearout.Therearevariousdepreciationtechniquesanaccountantcanuse.ThesimplestandmostcommonlyusedmethodinU.S.businessesiscalledthestraight-line method of depreciation,whichallowsyoutodepreciatethesameamountofexpenseeachyearoftheestimatedusefullifeoftheasset.Forexample,anassetwithavalueof$10,000andausefullifeof10yearswillhaveanannual$1,000depreciationexpenseeachyear.

Net operating profit:Grossprofit,lesssellingcostsandadministrativeoverhead.Thislineitemrepresentstheprofitgeneratedbythenormaloperationsofthebusiness.

Nonoperating income: Interestanddividendsreceivedoninvestments,gainsonthedisposi-tionofcapitalassets,etc.

Nonoperating expenses:Interestpaidonlong-termdebts,lossesonsalesofcapitalassets,etc.

Sample Income Statement

Gross sales or revenues $ 605,000

Returns, discounts and allowances 30,000

Net sales or revenues 575,000

Cost of sales or goods sold 470,000

Gross margin or operating profit $ 105,000

Selling and administrative costs 60,000

Depreciation 5,000

Net operating profit $ 40,000

Interest income or nonoperating income 10,000

Interest expense or nonoperating expense 3,000

Net profit before taxes $ 47,000

Provision for federal income taxes 10,000

Net profit after taxes $ 37,000

Mastering Business Finance / 7

Net profit before taxes:Netoperatingprofit,plusanynonoperatingincomeandminusanynonoperatingexpenses.

Provision for federal income taxes:Theestimatedamounttobepaidonoperatingearningsfortheperiod,nottheamountoftaxespaidduringtheperiod.

Net profit (or income) after taxes: Thefinal“bottomline”profitclearedbythebusinessfromallsourcesduringtheperiodcoveredbythestatement.Usingthisvitalfigure,stockholderscanevaluatemanagement,investorscandecideonwhethertopurchasethecompany’sstock,andcreditorscanmeasuretheriskinessofaloan.

The Statement of Cash FlowsThestatementofcashflows,whichshowsthemovementofcashthroughabusiness,presentsthecashreceiptsandcashpaymentsofacompanyoveraperiodoftime.Itcomplementstheincomestatementbyprovidinginformationonacompany’sliquidityandfinancialflexibility.Italsoex-plainsthechangeofcashandcashequivalentsduringaperiod.(Cashequivalentsareshort-term,highlyliquidinvestmentsthatarereadilyconvertibletocashamounts,suchasshort-termTreasurybills,commercialpaperandmoneymarketfunds.)Insimilarfashiontothebalancesheetandtheincomestatement,thestatementofcashflowsmustbepreparedannuallybyeverybusinessbutmayalsobedonesemiannuallyorquarterly.

Note: EffectiveforannualfinancialstatementsforfiscalyearsendingafterJuly15,1988,thestatementofcashflowssupersedesthestatementofchangesinfinancialposition,whichtheFi-nancialAccountingandStandardsBoard(FASB)formerlyrequired.Not-for-profits,however,arenotrequiredtomaketheswitch-over.

Byusingthestatementofcashflowsinconjunctionwithinformationprovidedbythebalancesheetandtheincomestatement,companyowners,creditorsandotherswhousefinancialstate-mentscanassessacompany’sabilitytogeneratefuturenetcashinflows,meetdebtobligationsandpaydividends.Thestatementshouldalsohelpinassessingacompany’sneedforfutureexternalfinancing,aswellastheeffectsofbothcashandnoncashinvestingandfinancingactivitiesonacompany’sfinancialposition.

Thestatementofcashflowsisclassifiedbyoperating,investingandfinancingactivities.(See sample statement on page 8.) Briefly,thesearetheitemscontainedinacompany’sstatementofcashflows:Operating Activities: Cash received from: ● Saleofgoodsorservices. ● Collectionsorsalesofreceivablesthat

arise fromthesalesofgoodsandser-vices.

● Interestonloansandbonds. ● Dividendsonequitysecurities. ● Insuranceandlawsuitsettlements. ● Refundsfromsuppliers.

Cash paid to: ● Acquisitionofmaterials for inventory

ormanufacturingproducts,orforgoodsforresale,includingpaymentsontradeaccountsandnotespayabletosuppliers.

● Creditorsforinterest.

● Employeesforcompensation. ● Governmentalagenciesfortaxes,duties,

fees,finesorpenalties. ● Customersforrefunds. ● Lawsuitsettlements. ● Charitiesforcontributions.

Investing Activities: Cash received from: ● Salesofproperty,plant,equipmentand

otherproductiveassets. ● Salesofabusinessunitsuchasabranch,

divisionorsubsidiary. ● Collectionsofprincipalondebtinstru-

mentsofothercompanies. ● Saleofloans.

8 / Business Management Daily

Cash paid to: ● Acquireproperty,plant,equipmentand

otherproductiveassets. ● Acquireanotherbusiness. ● Make loans toand/orpurchase loans

fromanothercompany. ● Acquiredebtorequityinvestmentsin

othercompanies.

Financing Activities: Cash received from:

● Issuing equity instruments, such asstockinthecompany.

● Issuingbonds,mortgages, notes andotherformsofshort-termorlong-termborrowing.

Cash paid to: ● Ownersofthecompanyintheformof

dividendsorotherdistributions. ● Repayment of amounts borrowedon

short-termandlong-termdebt.

Sample Statement of Cash Flows

Cash flows from operating activities Cash received from customers $110,000 Cash paid to suppliers and employees ( 90,000) Interest received 8,000 Interest paid ( 6,000) Income taxes paid ( 9,000) Net cash provided by operating activities $13,000

Cash flows from investing activities Proceeds from sale of plant $70,000 Purchase of equipment ( 10,000) Net cash provided by investing activities $60,000

Cash flows from financing activities Principal payments on notes ($40,000) Dividends paid ( 15,000) Net cash used in financing activities ($55,000)

Net increase in cash and equivalents 18,000

Cash and equivalents at beginning of year 12,000

Cash and equivalents at end of year $30,000

Reconciliation of net profit to net cash provided by operating activities: Net profit after taxes $37,000

Adjustments to reconcile net profit after taxes to net cash provided by operating activities: Depreciation 2,000 Gain on sale of plant (11,000) Increase in trade accounts receivable ( 7,000) Increase in inventory (10,000) Decrease in accounts and notes payable 5,000 Increase in interest and taxes payable ( 3,000)

Net cash provided by operating activities $13,000

Mastering Business Finance / 9

Themoststraightforwardwaytopresentoperatingactivitiesinastatementofcashflowsisthedirectmethod,whichreportsmajorclassesofoperatingcashreceiptsandpayments.Underthismethod,aseparatescheduleispresentedwiththestatementofcashflowsthatreconcilesnetprofitandnetcashflowfromoperatingactivities.Ineffect,thisreconciliation isaconversionofnetprofitfromtheaccrualtothecashbasisofaccounting.

➤ Observation: You’llfindthebalancesheet,theincomestatementandthestatementofcashflowsinacompany’sannualreport.Inmostannualreportsthesefinancialstatementsarepre-sentedonacomparativebasis:thatis,thecurrentyearalongwithoneormoreprioryears.Usethefiguresinthesestatementstoanalyzeyourowncompanyaswellasyourcompetition,toforecastthefinancialoutcomeforyourentirebusinessordepartmentproject,andtomakeavarietyofotheressentialbusinessdecisions.Inshort,thesereportsarethreeofthebusinessperson’smostimportanttools.

10 / Business Management Daily

How the Financial Pros Use These Tools

Nowthatyouareawareofthemechanicsofabalancesheet,anincomestatementandastate- mentofcashflows,yourworkisnotoveryet.Keepinmindthatalthoughthefiguresin

thosereportsareimportant,theydon’t,inandofthemselves,tellyouhowyourcompanyisdoingcomparedwithothersinyourindustry,whetherithasstayingpowerinourhighlycompetitiveworldorwhatweaknessesitshouldbecorrectingfromwithin.Inshort,thosereportsalonedonottellyouwhetherthecompanyisfinanciallyhealthy.

Todeterminethefinancialstateofyourcompany,youhavetoturntothreemajorconditionswithinyourcompanythatyou,asamanager,canhelpcontrolorchange:● Liquidity,whichissimplytheabilitytogenerateenoughcashtopayyourbillsandexpenses

ontime.● Leverage,whichistherelationshipbetweenyourcompany’stotalliabilitiesandequity.Your

firmissaidtobehighlyleveragedwhenithasa lotofdebt inrelationtoequity.Insomeinstances,carryingalotofdebtcanbeadvantageous.Atothertimes,itcanbeinjurioustoacompany’shealth.Thoseprosandconswillbediscussedlaterinthissection.

● Profitability,whichissimplywhetheryourcompanyendsupwithanymoneyafterallyourexpenses, including taxes,havebeenpaid.Profitability, inotherwords, is reflected in the“bottomline”ofyourincomestatementanddetermineswhetheryoushouldbeinbusinessatall.

TroubleshootingWithRatioAnalysisFinancialanalystsexaminetheliquidity,leverage,profitabilityandothervitalaspectsofafirmbyusingthefiguresinthecompany’sfinancialstatementstoformspecialrelationshipsorratios.Theseratiosarethemostcommonsourceofinformationtheyusetoassesstheperformanceofabusiness.Theycanrelateanyaspectofyourbusinesstoanyotherarea,suchassalestoprofits,orprofitstoassets.Mostimportant,becausetheyaresowidelyusedandreported,itispossibletocompareratiosforyourownbusinesswiththeaverageforyour industry,orforgroupsofcompanieswithinyourindustry.

Sometimes,however,ratioanalysiscanleadyouastrayifyouarenotawareofitslimitations.First,ratioanalysisisgearedtowardgivingyouinsightsratherthanhardbusinessdata.Assuch,itcanpointthewaytopossibletroublespots,butyouwillneedfurtherverificationwhenyougetthere.Forinstance,adownturninyouroperatingprofitmarginmightpointoutanoperatingbottleneck,butyouwillneedtoinvestigatefurthertoisolatetheproblem.Moreover,ratiosdealwithhistoricaldata,whichmayormaynotberelevanttocurrenteconomictrendsorcompanyneeds.Forthisreason,itisalwayswisetoconfirmthatatrendindicatedbyaratioanalysisis,infact,applicabletocurrentoperatingconditions.

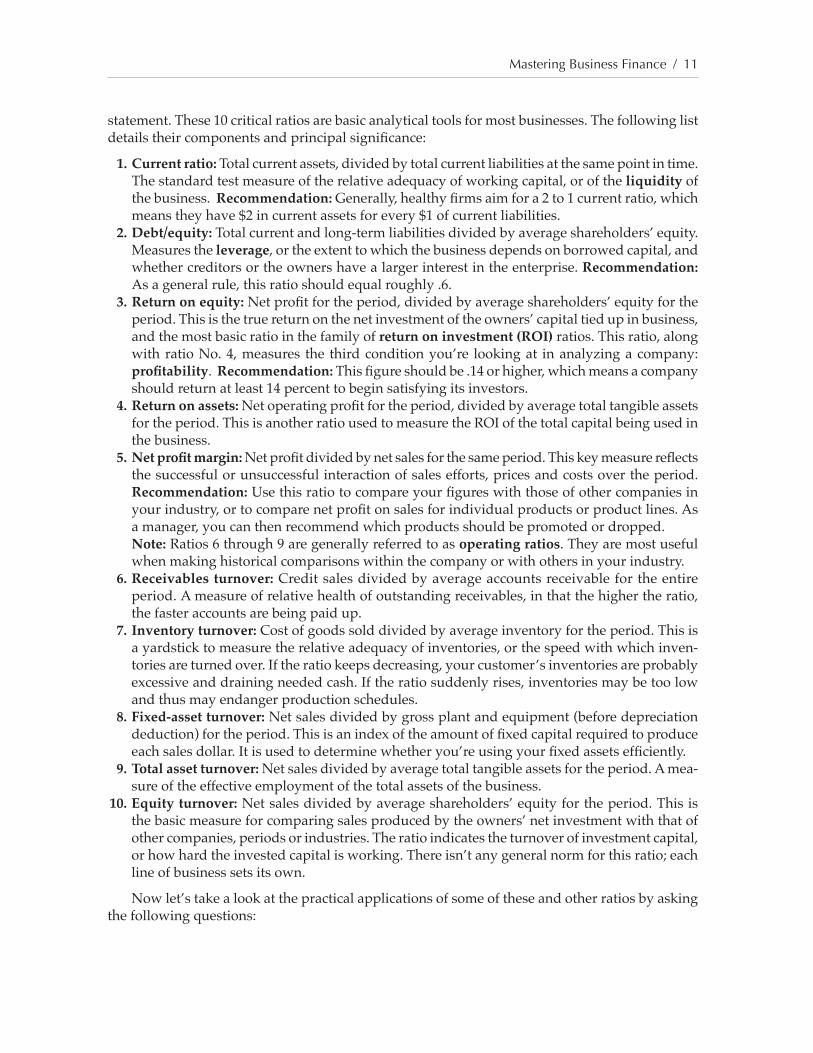

TenCriticalRatiosRatioscomeinallshapesandsizes,andareapplicabletoawiderangeofbusinessproblems.Morethan150financialratiosarecurrentlyinuse.Forourpurposes,wehavechosen10ratios,eachaddressingaspecificpotentialproblemareaandderivedfromthebalancesheetand/orincome

2

10

Mastering Business Finance / 11

statement.These10criticalratiosarebasicanalyticaltoolsformostbusinesses.Thefollowinglistdetailstheircomponentsandprincipalsignificance:

1. Current ratio:Totalcurrentassets,dividedbytotalcurrentliabilitiesatthesamepointintime.Thestandardtestmeasureoftherelativeadequacyofworkingcapital,oroftheliquidity ofthebusiness.Recommendation:Generally,healthyfirmsaimfora2to1currentratio,whichmeanstheyhave$2incurrentassetsforevery$1ofcurrentliabilities.

2. Debt/equity:Totalcurrentandlong-termliabilitiesdividedbyaverageshareholders’equity.Measurestheleverage,ortheextenttowhichthebusinessdependsonborrowedcapital,andwhethercreditorsortheownershavealargerinterestintheenterprise.Recommendation: Asageneralrule,thisratioshouldequalroughly.6.

3. Return on equity:Netprofitfortheperiod,dividedbyaverageshareholders’equityfortheperiod.Thisisthetruereturnonthenetinvestmentoftheowners’capitaltiedupinbusiness,andthemostbasicratiointhefamilyofreturn on investment (ROI) ratios.Thisratio,alongwithratioNo.4,measures the thirdconditionyou’re lookingat inanalyzingacompany:profitability.Recommendation:Thisfigureshouldbe.14orhigher,whichmeansacompanyshouldreturnatleast14percenttobeginsatisfyingitsinvestors.

4. Return on assets:Netoperatingprofitfortheperiod,dividedbyaveragetotaltangibleassetsfortheperiod.ThisisanotherratiousedtomeasuretheROIofthetotalcapitalbeingusedinthebusiness.

5. Net profit margin:Netprofitdividedbynetsalesforthesameperiod.Thiskeymeasurereflectsthesuccessfulorunsuccessfulinteractionofsalesefforts,pricesandcostsovertheperiod.Recommendation:Usethisratiotocompareyourfigureswiththoseofothercompaniesinyourindustry,ortocomparenetprofitonsalesforindividualproductsorproductlines.Asamanager,youcanthenrecommendwhichproductsshouldbepromotedordropped.Note:Ratios6through9aregenerallyreferredtoasoperating ratios.Theyaremostusefulwhenmakinghistoricalcomparisonswithinthecompanyorwithothersinyourindustry.

6. Receivables turnover:Creditsalesdividedbyaverageaccountsreceivablefortheentireperiod.Ameasureofrelativehealthofoutstandingreceivables,inthatthehighertheratio,thefasteraccountsarebeingpaidup.

7. Inventory turnover:Costofgoodssolddividedbyaverageinventoryfortheperiod.Thisisayardsticktomeasuretherelativeadequacyofinventories,orthespeedwithwhichinven-toriesareturnedover.Iftheratiokeepsdecreasing,yourcustomer’sinventoriesareprobablyexcessiveanddrainingneededcash.Iftheratiosuddenlyrises,inventoriesmaybetoolowandthusmayendangerproductionschedules.

8. Fixed-asset turnover:Netsalesdividedbygrossplantandequipment(beforedepreciationdeduction)fortheperiod.Thisisanindexoftheamountoffixedcapitalrequiredtoproduceeachsalesdollar.Itisusedtodeterminewhetheryou’reusingyourfixedassetsefficiently.

9. Total asset turnover:Netsalesdividedbyaveragetotaltangibleassetsfortheperiod.Amea-sureoftheeffectiveemploymentofthetotalassetsofthebusiness.

10. Equity turnover:Netsalesdividedbyaverageshareholders’equityfortheperiod.Thisisthebasicmeasureforcomparingsalesproducedbytheowners’netinvestmentwiththatofothercompanies,periodsorindustries.Theratioindicatestheturnoverofinvestmentcapital,orhowhardtheinvestedcapitalisworking.Thereisn’tanygeneralnormforthisratio;eachlineofbusinesssetsitsown.

Nowlet’stakealookatthepracticalapplicationsofsomeoftheseandotherratiosbyaskingthefollowingquestions:

12 / Business Management Daily

Does your firm have enough cash to pay its bills?

Lackofcashcanbeamajorproblemsimplybecausecashinflowisuncertain,whiletherequiredcashoutflowisconstantandnecessarytomaintainregularbusinessoperations.Forthatreason,abusinessmusttrytomaintaincertainlevelsofcashtopayitsbillsbymaintainingasafecurrent ratio.Inotherwords,itkeepsaneyeonitsliquidity.

Example:Inoursamplebalancesheet(see page 4),thecurrentratiowouldbe:

Currentassets($255,000) Currentliabilities($121,000)

Oursamplecompanyseemstohaveadequateliquidity.

To leverage or not to leverage?

Ahighlyleveragedcompanyhasitsprosandcons.Manyentrepreneursseekoutaleveragedfirmbecausetheybelievetheycanearnenoughwithacompanybothtopaytheinterestondebtandmakeagoodreturn.Inotherwords,leveragecanincreaseprofits.

Inbadtimes,ahighlyleveragedfirmcanreactthesamewayasanindividualdrowningindebt.Interestpaymentsbecomehardtomeet,andcreditorsbeginclosinginforthekill.Forthatreason,bankersandmanagementpeoplepaycloseattentiontothedebt/equityratiotoseeifthere’sanyunduedrainonfunds.

Example:Againinoursamplebalancesheet:

Totalliabilities($126,000) Shareholders’equity($212,000)

Again,oursamplecompanyseemstobesittingpretty!

How profitable is your firm?

Dependingonhowmuchitwantstomake,everycompanyhasitsownnormforwhatthereturn on equityratioshouldbe.Weused14percentasaminimum.Others,however,saythatthereturnshouldatleastmatchthegoingrateforTreasurybills,orafirmmightbebetteroffusingthecapitalinvestedinthefirmforsomeotherpurpose.

Example:Forthisratio,weturnbothtoourbalancesheetfortheequityfigureandtotheincomestatement(see page 6) forthenetincomefigure:

Netincome($37,000) Equity($212,000)

Itlookslikeoursamplefinancialstatementsindicateaveryhealthycompany.

Should you provide credit to a customer?

Often,youwillneedinformationfromacustomertobeabletoanswerthisquestion.Whenthecustomerprovidesabalancesheetorincomestatement,youneedtoknowwhattolookfor.Practi-callyspeaking,theincomestatementislikelytobeoutofdateandwon’trepresentthecompany’scurrentfinancialaffairs.Mostcompaniesprepareincomestatementsonlyonceortwiceeachyear,butmonthlybalancesheetsarecommon.

=2.1

=.59

=17%

Mastering Business Finance / 13

Ifyouobtainanup-to-dateincomestatement,itwillnotrequiremuchadditionalworktocomeupwithacompletepictureofthecompany’scurrentstateofaffairs.Luckily,evenwithoutacurrentincomestatement,youcanlearnmuchfromthebalancesheetbyusingratioanalysis.Asyoucansee,mostratioanalysisrequiresonlybasicmathskills.

Fromourlistof10criticalratios,usethecurrentratiotodeterminewhetherthecustomerisliquidenoughtopayoffdebts,andusethereturnonequityratiotoseewhetherthecustomerisprofitable.Usetheinventoryturnoverratiotodetermineifthecustomerwillbeabletomeetyourproductionschedules.Whenusingratiosthatrequiresalesfigures,thoseforthelatestyearavailablewillsuffice.Inaddition,thefollowingratiosareimportant:● Current liabilities to net worth:howmuchofthefundsinvestedbyyourcustomerswould

beneededtopayoffallshort-termobligations.Thelowertheratio,thebetter.Normally,youshouldshyawayfromafirmwitharatioof66percentorhigher.

● Short-term debt coverage: currentassetsdividedbyshort-termdebt.Thisratioisavariationofthecurrentratio,withtheemphasisonshort-termdebt(debtduewithinoneyear).Ifyourcustomerhas$2ofcurrentassetstocovereach$1ofdebt,youaresafe.A1:1ratiowillsufficeifthecurrentassetsareeasilyconvertedintocash.

● Average collection period: accountsreceivabledividedbycreditsalestimes365.Thisratiowillgiveyouagoodideaofhowfastyourcustomeriscollectingitsbills.Usually,35–45daysisconsiderednormal.Anythingover50daysmayindicatesizableuncollectibleaccountsandshouldgiveyoujustcauseforconcern.

Example: Ifacompanywith$20million increditsalesmaintainedaccountsreceivableof $2million,theaveragecollectionperiodwouldbe36days($2million÷$20millionx365=36.5).

➤ Observation:Onceyoudecidethatanewcustomerhasthewherewithaltopaybillsontime,youmustdeterminehowmuchcredittoextend.Ageneralruleofthumbistofillanyfirstorderupto10percentofthecustomer’snetworthand,afterthat,openaformallineofcredit.Onceapproved,thislineofcreditshouldbeexceededonlywithtopmanagement’sapproval.

14 / Business Management Daily

AnsweringSomeDifficult FinancialQuestions

Ratioanalysiscanbeveryhelpful inpinpointingoperating inefficiencieswithinyourcom- pany.Buttounderstandhowyoucanuseratiostospotproblems,youmustfirstknowthe

rightquestionstoask.Inthissectionweaddresssomeoftheimportantfinancialquestionsthatallmanagersshouldbeasking.

AQuestionofProfitMarginsHas profit growth kept pace with sales growth in recent years? If not, have some markets been more responsible than others for the lag?

Manymanagerswronglybelievethatasacompanygrowsandmatures,profitsalwaysin-creaseataslowerratethansales,evenasbothcontinuetoexpand.Thisiscalledtheprincipleofdiminishingreturnsonaddedvolume.However,thisprincipleisoftenuntrue.Considerthefollowingexample.

Amanufacturerofsmallpartsandcomponentsforfinishedproductsfoundthateconomiesofscaleandothergrowthfactorswerenolongerbringingsatisfactoryprofitgrowth.Rather,itappearedthatincreasedsalesvolumehadcomepartlyfromitsentryintonewmarketsthatweremorecompetitive,moreexpensivetopromoteandserve,andgenerallylessprofitable.

Oneof thefirst analyticalfigures the topmanagers turned towas the familiarnet profit margin,onamarket-by-marketbasis.Tobegin,thefirm’ssalesanalystproducedreportsshowingnetprofitmarginsonsalesbymarketsforeachofthelastthreeyears.Thesereportsshowedallthecostsassociatedwithgettingthesaleandsubtractedthemoutofthegrosssalesfigure.Theseresultsservedasanimportantfactorindecisionsthatlaterledtomajorchangesinthecompany’soverallmarketingstrategy.

Afewoftheindustrygroups,forexample,hadgrowninbothsalesvolumeandprofitabilityoverthepastfewyears.Severalothersaccountedforalargershareofcompanysales,butrevealedshrinkingprofitmarginsinthisanalysisasaresultofsubstantialpricediscounting.Forthetimebeing,atleast,littlecouldbedoneaboutsomeoftheseindustrymarketsbecausethecompanyneededthevolumetheygenerated.

In someof themosthighly competitive industrymarkets,however, analysis showed thecompanywasforgoingprofitswithoutsubstantiallyimprovingitsmarketposition.Furthermore,thetopmarketingpeopleagreedthattherewaslittlelikelihoodofchangingthissituationforthebetterinthenearfuture.Managementdecidedtodeemphasizesaleseffortsinthesemarkets,ex-ceptatfull-profitpricing.Althoughsalesvolumefelloff,thesaleseffortswereretargetedtomoreprofitableindustrysectors.Itwasnotlongbeforethegrowthtrendforoverallnetprofitreverseditsdeclineandslowlybegantoimprove.

Sometimesacompany isunable tobreakdownall itssellingandadministrativecostsbymarketsegmentorsimilarcriteria.Onealternativeissimplytoallocatethesecostsinproportiontothesalesvolumeinthemarketsegmenttowhichtheyarerelated.This,ineffect,assumesthatsellingcostsaremoreorlessuniforminthevariousmarkets,whichmaynotbethecase.

Often,youcanmakeausefulanalysisbydividing grossprofit,insteadofnetoperatingprofit,bynetsales.Thisgross profit marginiswidelyusedinretailingandothernonmanufacturingindustries.

3

14

Mastering Business Finance / 15

Stillanotheroption,whensellingandadministrativecostscannotbefullyallocated,istocal-culatetheratioofgross profit to cost of goods soldinadditionto,oreveninsteadof,theaboveratios.Thisratiocanbeparticularlyusefulinfieldswherebiddingpricesarecalculatedandquotedoncontractsonthebasisofproductioncostestimates.Comparisonsovertime—betweenmarketsorevenbetweencustomers—canrevealpreciselytowhatdegreeprofitsacrificesarebeingmade,intermsofthelowerprofitreturnonproductionoutlays,toobtainvolume.

➤ Observation:Inthisandotherinternalratioanalysesinvolvingprofits,theincomestate-mentitemtostartwithisthenetoperatingprofit,ratherthanthebroadernetprofitbefore(orafter)taxes.First,federalincometaxrateschangefromyeartoyearandwiththesizeofcompanyprofits,sousingafter-taxprofitsforinternalpurposeswouldmerelyintroduceacomplicatingfactor,nottomentiontheneedtoallocateonemoreitem.Second,becausethevariousinternalcomparisonsbeingmadearealwaysbetweenoperatingpartsofthebusiness,theinclusionofanynonoperatingincomeorexpensewoulddistorttheresults.Insomelinesofbusiness,accountantsandindustrygroupsusetheprofitconceptof“earningsbeforeinterestandtaxes”(EBIT),whichisroughlythesameasnetoperatingprofitplusdepreciation.Thisfigureeliminatesbothfederalincometaxesandinterestearnedorpaidonlong-terminvestmentsanddebts.

AQuestionofWorkingCapitalDo you have enough working capital to take advantage of investment opportunities? If not, are some of your departments more to blame and need more tightening up than others?

Thedollardifferencebetweenanybusiness’scurrentassetsanditscurrentliabilitiesisaptlycalledworking capital.Thisistheamountofreadycashandreadilyconvertibleassetsthatyoucanput toworkasneeded,without leaving thecompany inadangerouslyexposedfinancialposition.Workingcapitaliswhatenablesyourfirmtotakeadvantageofspecialdeals,earncashdiscounts,borrowshort-termfundsmoreadvantageouslyorcapitalizeonsimilarprofitoppor-tunities.Italsoenablesthecompanytomeetitstradeobligationsanddebtinstallmentsontime.Theratiomostcommonlyusedtomeasuretheadequacyofworkingcapitalisthecurrent ratio.

Retailoperationsregularlyapplythecurrent-ratioapproachfor internalanalyses,suchascomparing thecreditandfinancialperformancesof theprincipaldepartmentswithinvariousstores,aswellascomparingstoreswitheachother.

RMA’sAnnual Statement Studies

A good way to compare your company’s ratios with other companies’ is to obtain a copy of the Risk Management Association (RMA) Annual Statement Studies. These studies are culledfrommorethan86,000financialstatementsofbankborrowersreviewedbyRMA,anationalorganizationofbanklendingofficers,andtheyincludeinformationoncloselyheld companies and public corporations.

Thedataisclassifiedintotwomainsections:Thefirstcontainscompositebalancesheetandincomestatementcomparisonsforeachof355industriesforthepastfiveyears.Thesecond section contains 17 commonly used ratios, presented as medians and quartiles, for most of the industries. With that information, a manager can zero in very quickly on where a company stands. For further information, go to www.rmahq.org.

16 / Business Management Daily

Toconstructthecurrent-assetscomponentofthesedepartmentalratios,itisarelativelysimplematter tocollectcurrentdataonaccountsreceivable (fromthedepartmentalcodingoncreditcustomers’billing)andoninventories(directlyfromdepartmentrecords).Thesetwocategoriesaccountforthelargestshareoftotalcurrentassetsfoundinthistypeofbusiness.

Forthecurrent-liabilitiescomponent,itisequallysimpleformanagerstobreakdowntradeaccountspayablebydepartmentsbyusingvendorcodesandmerchandisecategoryinformation.Someoftheremainingshort-termdebtsandexpensespayablecanalsobeallocateddirectlytodepartmentswithreasonableaccuracy.Anallocationofremainingcurrentliabilitiesinproportiontodepartmentalvolumedoesnotbiastheresultsinanysignificantway.

Onthecurrent-assetsside,retailoperationsgenerallyapplyanotherratio—receivables turn-over—tohelpanalyzetheirworkingcapitalpositions.

Theidealdepartmentinaretailoperationisonethatbothcontributestoworkingcapital,reflectedinahighcurrentratio,andhasanacceptablerateofreceivablesturnover,indicatedbyalowlevelofoutstandingreceivables.

AQuestionofReturnsWhich areas of the business will provide the best return on an increased investment of capital? How profitably is each area using the assets now assigned to it?

Whereshouldyourcompanyspenditsinvestmentdollars?Intechnology?Salesdevelopmentandtraining?Buildingawarehouse?Perhapsinproductdevelopment?Todetermineacompany’slong-termstrategy,youmustknowwhat thereturnswillbe.Wecan illustrate this importantconceptthroughthefollowingexample.

Adistributorofcleaning/maintenancetoolsandsuppliesoperatesthreedivisions,eachaimedatadifferentmarket:(1)contractandinstitutionalsales,whichsellstolargebuildingmanagementfirms,maintenancecontractors,majorhospitalsandsimilarpurchasers;(2)industrialproducts,whichsellstocommercialandindustrialcustomerslargelythroughagents;and(3)consumerproducts,whichmarketsbrandedandunbrandeditemsthroughretailstores.Themanagersofallthreedivisionshavedemonstratedthattheycouldimprovetheirvolumeandmarketshareswithinfusionsofcapitalforpackaging,warehousing,deliveryandotherequipment.Thecompanyhasdecidedtoaddtoitscapitalinvestmentbutmustdecidewhichdivisionshouldbeallocatedthelion’sshareofthefundinginordertomaximizethereturntoshareholders.

Return on shareholders’ equityiswhatthecorporation’stopmanagerswillbelookingatfirstinthiscase.It’sreasonableforthemtoassumethatthedivisionwiththehighestpresentrateofreturnwillcontinuetoearnthebestreturnasitgrows.Andtheyacceptthepropositionthat,withinpracticallimits,allthreedivisionswouldshowthesamerateofsalesgrowthinproportiontoaddedinvestment.

Allocating shareholders’ equitydirectly to the threeoperatingdivisionsmay seem likeadifficulttask.Fortunately,however,thereisapracticalalternativethatreducestheproblemtomanageableproportions.

Constructingthreedivisionalbalancesheets,onecanestimateshareholders’equityineachdivisionbysimplysubtractingliabilitiesfromassets.Thenyoucancalculatethethreereturn-on-equityratios,forbothactualandfutureoperations.

Return on assets (ROA) isanothercritical ratio that topmanagerswillwant toexamine.Somefinancialexpertsbelievethatreturnontotalassetsprovidesthebestmeasureofreturnforacompanybecauseitfocusesonshort-termfinancing.Especiallyintheshortrun,returnonassetshasseveralpracticaladvantagesoverthemorecomplexreturn on equity (ROE)ratio.First,ROAdirectlymeasuresthekeyfactorinvolvedinthedecision:aninvestmentintangibleassets,such

Mastering Business Finance / 17

asstorage,packaging,distributionorotherequipment.Second,itavoidsthenecessityofcon-sideringandallocatingliabilities,whichinmanycompaniesmayinvolvemoreuncertaintyandpotentialerrorthanallocatingassets.Finally,itiseasierfornonfinancialmanagerstounderstandandappreciate—anelementthatcannotbeignoredinreachinganagreement.

Itwouldbewise,however,formanagementtouseboththereturnonassetsratioandthereturnonequityratioinitsanalysis,ratherthanusetheassetsratioasasubstitutefortheequityratio.Theequityratioisthetruemeasureoftheshareholders’returnontheirinvestmentinthecompany,andimprovingthisreturnoverthelongrunisthebasicaimofanymajormanagementdecisions.Moreover,theequityratiomayhighlightcertainimportantresultsofanactualdecisionthattheassetratiowouldnotpickupatall.

Oneelementtakenintoaccountintheequityratio,forexample,willbethedifferingeffectsofvariousassetinvestmentdecisionsonthecompany’sliabilitiesovertime.Ifonedivisionwoulduseitsaddedinvestmentforashort-liveddeliveryfleet,whileanotherwoulduseitforaddedwarehousingspace,theimmediateeffectsontheassetratiowouldbeverysimilar.Theeffectsoverafewyearsonbothassetsandliabilities,andthereforeontheequityratio,however,couldbeverydifferent.Thelatter,ofcourse,wouldbethemoreaccuratemeasureofprospectiveratesofreturnonthealternativeinvestmentproposals.

AQuestionofAssetManagementHave recent volume gains been achieved at the price of a disproportionate tie-up of available assets? For example, have the costs of expanding operations into new territories been worth it?

Inanybusiness—manufacturing,distributionorservices—ittakesaninvestmentoftheown-ers’capitalinthebusinessassetstoproducesalesorrevenues.Incapital-intensivemanufacturingindustriesespecially,theamountofassetsrequiredforeachsalesdollarcanbeoneofthemostcriticalelementsinthecompany’ssuccessorfailure.Knowingjustwherethecompany’sassetsarebeingusedmostandleasteffectivelytocreatesales,therefore,isofvitalconcerntomanagement.

Example:Aregionalmanufacturerofplumbingandheatingsystemsmadeabasicdecisiontosetupassemblyfacilitiesprogressivelyinnewlocations,ratherthanextenditsshippingrangefromitsoriginallocation.Themanagementbelievedthiswasthebestpathtogeographicalexpan-sionofitsmarketingarea.Todate,oneundesirableresulthasbeenasteadydeclineinthedollarsofsalesproducedbyeachdollarofcompanyassets,asthetotalinvestmentinplantandequip-menthasgrown.Topmanagershavethereforebegunacompletereviewoftheoriginaldecisiononterritorialexpansion.

Oneofthemostcriticalnumberstoanalyzeisthetotal asset turnover(netsalesdividedbytotaltangibleassets)andequity turnover(netsalesdividedbytotalshareholders’equity).Athirdratiothatwillbeparticularlyusefulintheanalysisisfixed-asset turnover (netsalesdividedbygrossplantandequipment),whichmeasureshowefficientlyfacilitiesareusedtoproducesales.

Thefigurescommontoallthreeoftheseturnoverratios,forthecompany’spurposes,arethesalesdollarsproducedbyeachofitsterritorialplants,aswellasbythehomeplant.Fortunately,itisasimplemattertoobtaintheneededdollarsalesvolumeinformationforeachplantfromshippingrecordscheckedagainstcustomerbillings.Theotherfiguresinvolvedinmakingupeachratioare,respectively,tangibleassets,shareholders’equity,andtheplantandequipment(p&e)foreachplant.Companyrecordswillproducethep&efigurewithlittle,ifany,adjustmentsrequired.Managementwillhavetoestimatethefirsttwoonaplant-by-plantbasisbyusingthemethodsandassumptionsdiscussedearlier.

Becausethecompanycarriedoutitsterritorialdispersionofproductionandassemblyfacilitiesoveraperiodofyears,managementwillwanttolookattheseveralterritorialratiosastheyhave

18 / Business Management Daily

changedover,say,thelastthreeyears.Thiswillenableittoseejusthowthegeneraldeteriorationincompany-wideratioshasdeveloped,andtopinpointtheterritorialdifferencesineffectivenessthatitexpectstofind.

Considering that the company’s turnover ratioshavedefinitelybeen slipping—andhavecoincidedwiththedispersionprogram—itispossibletospeculateonwhattheanalysisislikelytoturnup.First,aseachnewassemblyplantisbuiltandbroughtonstream,ithasundoubtedlycreatedaninitialdrainontheeffectiveuseofcompanyassets.Becausetheadditionalplantshavebeenactivatedoveraperiodofyears,moreover,thisdrainhascontinuedtoaffectturnoverastheprogramhasdeveloped.Thisfindingalonewouldbereasonforchangingthepolicyoffacilitydispersion.

Managementwillalsoprobablyfind,however,thatwhiletheoperatingfiguresofsometerrito-rialplantshaveimprovedwithtimeastheyandtheirsalesterritorieshavebecomeestablished,othershavepersistentlylagged.Insomecases,thereasonmayturnouttobethatthesizeoftheplantisnotgreatenoughtopermitfullyefficientoperations.Inothers,itmaybethatnotenoughsalesvolumehasdevelopedintheterritorytopermiteffectiveutilizationofthenewfacilities.

Atthispoint,managementneedstobeaskingthesequestions:Willtheplant’sresultsimproveasitssalespotentialisachieved?Shouldtheplantbeenlargedtomakeitmoreefficient,orshoulditbecloseddown?Cantheplantbemademoreefficientbyshiftingorderstoitfromotherter-ritoriesorfromthehomeplant?

AQuestionofDebtStrategyAre we using too much—or too little—borrowed capital in our business? In either event, are we using debt financing and leasing in our various fields of operations to the extent that others do?

Thewords“thecorporationisfreeoflong-termdebt”certainlyhaveasolidringinacreditreport.Yetmanydebt-freecompanieshave,infact,givenupvaluablegrowthopportunitiestoachievethisposition.Andtoday,thosethathaveavoidedfinancingorleasingtoacquirecapitalequipmentandmaterialsmayhavenotonlyrestrictedtheiractivities,butneglectedvaluabletaxbenefitsaswell.

Example:Adiversifiedbusinessserviceorganizationusescopyingandduplicatingequip-ment,offsetprinters,addressingandmailingmachines,wordprocessorsandsmallcomputersinitsoperations.Asservicecompaniesgo,itisarelativelycapital-intensiveenterpriseandmustcontinuallydecidewhethertoownorleasenewitemsofequipment.Ifthedecisionistoown,thereisusuallythefurtherquestionoftherelativeadvantageofacashoutlayversuslong-termfinancing.Atthispoint,companymanagementisconcernedabouttheoverallbalancebetweenownedandleasedequipment,andthemorebasicbalancebetweendebtandcapitalinthebusi-ness.Itwouldliketodecideoneachfutureequipmentacquisitionwiththesebalancesinmindandperhapsevenchangethestatusofsomeofitspresentequipment.

Thedebt/equity ratioistheuniversallyacceptedmeasureoftherelationshipbetweenowner-suppliedcapitalandthatborrowedfromsuppliersandothercreditorsinanybusiness.Ahighratiocomparedwiththatofothersinthesameindustrymaybetakenasawarningsign,butitmayalsobean indication thatyours isanaggressivelygrowing (highly leveraged)companycomparedwiththeaverage.Conversely,alowratiomaymeanthatyou’reinahealthy,conserva-tivedebtposition,butyoualsohaven’tusedtheleverageofdebtfinancingaswellasyoucouldandhavemissedopportunities.

Becausethecompanycompeteswithmailingservices,contractprinters,computerservicebureausandotherspecializedserviceorganizations,itwillwanttocompareitsowndebt/equitypositionwiththoseofaveragecompaniesinasmanyofthesefieldsaspossible.Asastarting

Mastering Business Finance / 19

point,ithascollectedinformationfromtheRiskManagementAssociationcollectionofratios,aswellasfromDun&Bradstreet,Inc.

Toconstructitsowndebt/equityratiosforcomparison,itwillbefollowingasomewhatdiffer-entcoursefromthatofthecompaniesintheearlierexamples.Insteadofassigningbothliabilities(debt)andassetsexclusivelytoonefieldoranother,itrecognizesthatitsoperationsfrequentlyoverlapseveralfields.Foreachfieldtowhichitwillbecomparingitself,itisaskingwhichofitsassetsandliabilitieswouldbeusedorwouldexistifitwereonlyinthatfield.Severalassetandliabilityitems,therefore,maybeincludedinmorethanonecomparisonandwillnotalwaysbeproportionallydividedamongthesefields.

Whenithascompletedthisexercise,managementhopestofindthatitsdebtburden,inrela-tiontoitsowners’equityinthebusiness,isnoheavierthanwhatisconsideredgenerallyadvis-ableinthemajorservicefieldsinwhichitoperates.Itwillalsoundoubtedlyfind,however,thatcomparedwithaveragecompaniesinsomeofthesefields,itdependssignificantlymore,orless,ondebtfinancing.Ifthereasonsforthesedifferencesseemunreasonableonanalysis,managementintendstoshiftitsbuy-versus-leasedecisionsforthetypesofequipmentinvolved.

AQuestionofPurchasingHave our inventories, compared with sales volume, gotten out of line with those of others in our industry? Which of our products, in these terms, are showing the best and worst records, and why?

Traditionally,managementhasbeenadvisedthat“20percentofyourproductsprobablyaccountfor80percentofyourinventory,”solooktomakethebiggestcutswheremostoftheinventoryoccurs.Inmanycases,thisapproachcanaccomplishmoreharmthangoodandcanhindersalesanddeliveriesofproductsthatareamongthemostprofitable.Atthesametime,itmayoverlookothersituationsthatcollectivelyaccountformuchoftheexcessinventory.

Example:Amanufacturerofalineofpackagedhousewaressawinventoryvaluesonsuc-cessivereportsclimbing,andsuspectedtheyhadgonetoohigh.Acheckofinventoryturnoverratiosinitsindustryconfirmedthissuspicion.Itbegananinvestigationtodiscoverwhyfinishedproductswerepilingup,andhowtocorrectthesituation.Thetaskwasassignedtothesalesman-agerbecausehewasresponsibleforprojectingsalesandrequisitioningoutputfromproduction.

Hisfirststepwastohavetheavailablesalesandinventorydataorganizedonadetailedprod-uctbasissothathecouldcalculateproduct-by-productinventoryturnoverratios.Itthenbecameapparentthatthesuspectedfinishedproductinventoriesaccountedforonlyaminorfractionoftherising inventoryvaluesreportedonthebalancesheet.Furthermore,becauseofdifferencesinproductioncycles,someproductsgeneratedmuchheavierin-processinventoriesthanothers.

Anotherless-expectedfindingwasthatpurchased-materialsstocksforcertainproductswereabigpartofthetotalinventoryproblem.Somespecializedmaterialswereingeneroussupply,althoughtheproductstheywereintendedforwerenolongersalesleadersorwereactuallybeingphasedoutoftheline.Theinventoryproblem,inotherwords,wasnotonlyaproduct-by-productproblem,butonethatneededtacklingonastage-by-stagebasis.

Thesalesmanager’sreportshowedinventoriesoftheappropriatematerialsforeachproduct,work-in-processandfinisheditemsatthecloseofallofthepastfourquarters.Herelatedeachofthesetoproductsalesforeachquarter,toproduceinventoryturnoverratiosineachcalendarquarter. Basedonhisspecificrecommendations,thecompanytookseveralactions:● Forcertainproducts,itsharplyreducedheavyandagingmaterialsstocks.Excessitemswere

designatedforpossibleuseinotherproducts,assubstitutesforspecifiedmaterials.Thosenot

20 / Business Management Daily

absorbedinthiswayweresoldoff,sometimesatagain.Italsomadeadjustmentsinseasonalorderingandotherpurchasingpracticestominimizefuturebuildups.

● Wherein-processinventorieswerehigh,thecompanyreviewedproductionscheduling.Somepracticesthatithadonceadoptedforconvenience,andtoavoidmorecarefulscheduling,werefoundtobecausingasignificanttie-upofexpensiveinventories—partlyfinisheditemswerebeingtemporarilyshuntedaside.Thesales/in-process stockratioswereusedtozeroinonthese.Thenchangesweremadetoschedules,sizeofproductionrunsandotherpracticesthatwereaddingtotheinventoryload.

● Finally,inarelativelyfewcases,stocksofproductsawaitingshipmentwere,indeed,foundtobeexcessive.Bettercoordinationofshort-runsalesprojectionswithproductionordersreducedsomeofthese.Wheretherewerepile-upsinanticipationofseasonalneeds,specialpreseasonofferstodealersnotonlytrimmedstocksbutoftenresultedinanetincreaseinannualsales.

AQuestionofStabilityHow well could your company withstand adversity—a sudden drop in prices or sales, or an increase in costs?

Oneyardstickusedtoanswerthisquestionisthecompany’sbreak-even point.Expressedinsalesvolume,thisisthepointwhereincomefromsalescoverstotalcosts,bothfixedandvariable.Anotherfactorthatmostmanagerswatchforcontinuously,oncethebasicbreakdownhasbeenprepared,isanysignthatfixedcostsarerising.

Yourfirststep,then,istoseparateallcostsofthecompany’soperationsintothoserelativelyindependentoftherateofoperationsandthosethatvarydirectlywiththenumberofunitspro-duced.Touseanobviousillustrationofthefirstgroup,thecostofrentisfixed,regardlessofthenumberofunitsproduced.Ofcourse,eventheso-calledfixedexpensesmayvaryundercondi-tionsofextremechange(thecompanymaydisposeoforsubletpartoftheplantifvolumefallsenough).Forthepurposesofthisroughcalculation,however,wecansafelyignorethepossibleresultsofsuchextremechanges.Bycontrast,directmaterialscostsvaryalmostexactlyinpropor-tiontotherateofproduction.

Youwillrunintosomeproblemsindealingwiththemanycoststhatdonotclearlyfallintoeithercategory—or,morecorrectly,containbothfixedandvariablecosts.Anobviousexampleispowercosts.Thebasicconnectedloadchargemustbeborneregardlessoftheactualoperatingrate.Onceacompanypaystheminimum,itpaysfortheadditionalconsumptionbasedonactualuse.Inthiscase,thetwoelementsmaybeseparatedfairlyeasily;inothers,itwillbemoredifficult.

Toillustrate,herearesomeguidelinesforbreakingdownlaborcostsintofixedandvariablecategories.Ifsalesfalloff,youmaybeabletoreducethenumberofworkersinaspecificopera-tion,butatwhatpointcanyoualsoreducethenumberofsupervisors?Ifyouhaveonlyone,heorsheisarelativelyfixedexpenseaslongasyouhaveevenafewpersonnel.Inthecaseoflaborcosts,youmaybeabletodeterminetheminimumorganizationthatmustberetainedandclassifythisasafixedexpense.

Totakeanothercommonitem,yourwarehousingcostscontainsomefixedelements(theex-penseofspaceandequipment,andatleastsomesupervision)andsomethatarevariable(wagesofworkerswhomaybeshiftedtoanotherpartoftheoperationifthewarehouseworkloadfallsoff).

Tosegregatefixedandvariableelementsofyourcompany’smixedcosts,youwillundoubtedlywanttoconsultyourcompany’saccountant.Askhertotakeeachcostitemforthelastfullyearandroughlyestimatethepercentagethatisfixedorvariablewithinthenormalrangeofopera-tions.Thepercentagesforthreeorfourpreviousyearsandthecurrentyearcanbeestimatedthe

Mastering Business Finance / 21

sameway,orthoseforthelatestfullyearcanbeusedafteradjustingforanymajordifferences(suchasmakingatransitionfrommanualworktotheuseofmachines).

Onceyouhavethisinformation,calculatethebreak-evenpointinthefollowingmannerforasingleyear:Let’ssayyoudeterminethatyourfixedcosts(FC)are$100,000,sincetheydon’tchangethatmuchfromyeartoyear.Becauseyou’retryingtoforecastyourbreak-evenpointforafuturetime,you’renotsureofyourvariablecosts.Historically,however,theyhaverepresentedapproximately80percentofsales(variablecostsdividedbysales).Whatkindofsalesdoyouneedtobreakeven?Yoursetupwouldlooklikethis:

VC=variablecosts(asapercentageofsales) S = total sales you’ll need to break evenFC=fixedcosts P = profit

Yourbreak-evenformulais: P = S – (FC + VC)Therefore,yourformulawouldbe: P = S – ($100,000 + .8 x S)Sinceprofit,orP,is0atthebreak-evenpoint: 0 = S – ($100,000 + .8S), or

S = $100,000 + .8S

SolvingforS: S – .8S = $100,000 .2S = $100,000 S = $500,000

Thismeansyouwouldhavetochalkup$500,000insalesjusttocoveryourtotalcosts.

22 / Business Management Daily

ProfitFromYourBudget

Fewpeopleenjoybudgeting.Ittakestimeandrequiresself-restrainttosticktoit.Nonetheless, there’snobetterwaytokeepacompanyonfinancialtrackthanthroughaproperlymaintained

budgetprogram.Despitethealmostuniversaldistasteforbudgetaryrestraintswithindepartments,rarelyisthereacompanytodaythatoperateswithoutabudget.Thekeytosuccessfulbudgetingistoinvolvemanagersinalldepartmentsandatalllevelsfromthebeginningstages.

TheBudgetingProcessThebudgetingprocessisanattempttoestablishasetofrealisticstandardsfortheoperationofacompany.Initsfinalform,thebudgetwillbeasetofspecificobjectivesfortheyearahead.Al-thoughtheseobjectivesareidentifiedonlyaftercarefulstudy,theyaremerelyforecasts.Recognizethattheoriginalbudgetwillprobablyneedsomerevision.

Theprocessonlybeginswiththeformulationofthebudgetitself.Everybudgetingsystemmustcontainprovisionsnotonlyforactuallypreparingthebudget,butalsoforimplementingasystem,includingcoordination,control,follow-upandmaintenance.

Tobeeffective,abudgetmustbetailoredtothespecificneedsofyourcompany.Mostwell-designedbudgetprogramsshareanumberofcharacteristics,outlinedasfollows:● Clear lines of responsibility.Tosucceed,yourbudgetingteammustbeabletoassigndefinite

responsibilityfortheperformanceofeachunitmeasured.Thepersonassignedthisresponsi-bilitymusthavefullauthoritytoapplythestandardssetdowninthebudget.

● Management support.Anunsupportedbudgetwillalmostsurelyfail.Youroperatingdepart-mentsmustknowthatyouwillusethebudgetasatoolformeasuringtheirperformance.

● Clear-cut reporting procedures.Whenfinished,yourbudgetshouldbeaprojectionofwhatyourfinancialstandardswilllooklikeatsomepointinthefuture.Therefore,themorecloselyyourbudgetsystemfollowsyouraccountingandreportingclassification,thebetteritschancesforsuccess.

● Realistic standards.Don’texpectyourbudgetprogramtoworkmiraclesovernight.Themosteffectiveonessetthestageforachievableincomeandcostimprovementsduringtheyear.Theyaredesignedtofostercontinuousimprovementinoperatingperformance.Thebudgetisjustoneofmanytoolsinthisongoingeffort,butonethatiseffectiveinpointingouttheweakspots.

DevelopingaBudgetSystemThat’sRightforYouTherearethreebasicapproachestobudgeting,eachwithinnumerablevariations.Inthissectionweexaminethestrengthsandweaknessesofeachapproach.

1. Budgeting from the top down:Inasmallelectronicscomponentsmanufacturer,topman-agementwillgeneratetheprimarybudget.Thentheallocationsaresentdowntothevariousdepartmentmanagersfortheirestimatesofexpensesandprofits.

● Strengths:Thisisbyfarthesimplestapproachtobudgeting.Italsoensuresthatmanagement’sgoalsarealwaysreflected.

4

22

Mastering Business Finance / 23

● Weaknesses:Thistypeofbudgetingassumesthatmanagementhastheoperationalknowl-edgenecessarytobudgetforeverypartoftheorganization.Also,thelackofparticipationbyoperatingpersonnelcanleadtoalackofsupportfor,andcommitmentto,thebudget.

➤ Recommendation:Thisapproachisbestsuitedtothesmallerorganization,wherethereisaneasyfamiliaritybetweenstaffandlinefunctions.Inasmallercompany,managementismorelikelytobeawareofoperationalproblemsandcaneasilybringdepartmentheadsintothediscussions.

2. Budgeting from the bottom up:Budgetingbeginsat theoperatinglevelforadiversified,midsizeplasticsmanufacturer.Itgraduallyprogressesupthroughhighermanagementlevelsuntilitreachesthetopechelons.Ateverylevel,personnelwillreviewandreviseit,butonlywithintheconfinesofbroadcorporateobjectivesthataresetdownattheoutset.

● Strengths:This typeofbudgetprovideseveryoperating levelwithagreaterunderstand-ingofthebusiness.Italsoensuresactiveparticipationandgreatercommitmentfromlowermanagementlevels.Everymanagerknowswhatisexpectedintermsofperformanceduringaspecificbudgetaryperiod.

● Weaknesses:Itrequiresalotoftimetomovethroughtheprocessandcompletethenecessaryadministrativeprocedures.Operatingunitswilloftentendtobeveryconservativeinproject-ingrevenuesandoverlyliberalinallocatingcosts.Somemayevenholdbackonperformancetoprotectthemselves.

➤ Recommendation:Thisbudgetsystemisbestsuitedtoamultiproductcompany,wheremanydiverseoperationshavetobeincludedinasinglebudget.Itrequiresalargestaff,sotheapproachmightnotbeeffectiveinasmallcompany.

3. The two-pronged approach:Ahigh-techcompanybasedinNewEnglandusesacombina-tionofthetwomethodsdiscussedabove.Specificobjectivesforfinancialperformanceareestablishedatthecorporatelevel,andthenaresubmittedtooperatingmanagers,whopreparebudgetsbasedonoperating-levelobjectives.Theirbudgetsarethenapproved,disapprovedorrevisedbymanagementandsentbackdownforpossiblefurtheractionbythedepartments.Theprocesscontinuesuntilafinalbudgetisapproved.

● Strengths:Theformalbudgetrepresentsatruemeetingofthemindsbyallpartiesandrequiresparticipationatallmanagementlevels.Theoretically,thisresultsinacommitmenttoagreed-upongoals.

● Weaknesses:Theprocess canbevery time-consuming if topmanagementandoperatingdepartmentscan’tagreeonthebasicobjectives.It’salsobyfarthemostcomplicatedapproach.Schedulesandsurveysareusuallynecessarytosupportdeliberationsatvirtuallyallmanage-mentlevels.

➤ Recommendation:Thisapproachisbestsuitedtoacompanythathasdevelopedacertainamountofsophisticationinpreparingbudgets.Thesizeofthecompanyshouldnotbeanover-whelmingconsideration,butkeepinmindthatpreparingthedatanecessarytobackupthistypeofprogramwillconsumeasignificantnumberofperson-hours.

OrganizingaBudgetTeamOnceyourcompanydecidesonabudgetingsystem,youcanbegintoassembleateamtooverseetheprocess.Notethatwehavenotincludedapermanentbudgetstaffinourdescriptionoforga-nization(see next page),butprefertousethetalentsofmanagementpersonnelalreadyinplacein

24 / Business Management Daily

variousdepartments.Ifyoudecidelaterthatthecompanyneedsapermanentbudgetstaff,youcouldaddoneundertheaegisofthebudgetdirector.

The Budget Committee

Thebudgetcommitteeatoneservicecompanyincludesthepresident,chiefoperatingofficerandseniormanagementfromeachdivision.Theirprincipaltasksaretoappointabudgetchairmanandtooverseetheentirebudgetingprocess.Specificfunctionsinclude:● Resolvingbudgetingconflictsthatmightarisebetweendepartmentsorbetweenthebudget

chairmanandoperatingdepartments.● Reviewingbudgetestimatesandrecommendingchanges,ifnecessary,toappropriatedepart-

mentordivisionheads.● Reviewingperformancereportsandrecommendingactionwhenneeded.● Approvingthebudgetmanual,whichdetailstheadministrativeprocedurestobefollowedin

compilingthebudgetandcontainstheformsandinstructionsnecessarytocompilethedata.

The Budget Chairman

Thebudgetchairmanisresponsibleforcoordinatingthebudgetestimatesdevelopedbythelinedepartments.Heprovidestechnicalassistancetotheoperatingdepartments,whenevernecessary.Otherfunctionsinclude:● Advisingonbudgetarymatterstoboththebudgetcommitteeandthosewhoareresponsible

foroperations.● Recommendingprocedurestobefollowedbythoseresponsibleforeachbudgetcomponent.● Developingtimetablesforeachstageofthebudget.● Compilingforms,schedulesortablesnecessarytocompletethebudget.● Supplyingsupportdata,suchasrevenueorcostanalysis,whichcouldassistoperatingunits.● Recommendingactiontomanagementbasedonbudgetresults.● Analyzingandinterpretingvariancesbetweenbudgetedperformancelevelsandactualresults.

TeamBudgetingAsbusinesshasgrownsteadilymorecomplex,team budgetinghasproventobeavaluabletoolfordrawingthemanagementgrouptogetheranddirectingitseffortstowardcommonobjectives.Usingtheteamapproach,eachmanageriscalledontoplanandbudget—andwillbejudgedonhisperformance—inhisareaofresponsibility.Toparticipateinthisprocess,eachmanagerisgivenaccountingdataaboutpastandcurrentoperations.

Whatarethebenefitsoftheteamapproach?Managersareencouragedtothinkaheadandbepreparedforchangingconditions.Whentheyanticipatedifficultiesorproblems,theycanmoreeasilyavoidorcorrectthem.Theskillsoftheentireorganizationcanbebroughttobearindeter-miningthemostprofitablecoursesofaction.Throughteambudgeting,performancegenerallyimprovesbecausethepeopleresponsibleforattainingcompanyobjectivesshareinsettingthem.Finally,theconversionofeachmanager’splansintodollar-and-centsbudgetsprovidesherwithafinancialblueprintofheroperationsfortheperiodahead.Thisservesasabenchmarkagainstwhichtomeasureamanager’sperformanceandtospottroubleearly.

A limitation of the team approach:InadequateorfaultyplanningistheNo.1reasonwhybudgetsfail.It’snotunusual,forexample,tohavethebudget(1)provideforacostreduction,withnomentionofwho’sgoingtoaccomplishitorhow;or(2)projectasharpboostinsales,withno

Mastering Business Finance / 25

programspellingouthowthiswillbedoneoratwhatcost.Openingupabudgetprocesstokeymanagerscanincreasethepossibilityofthiskindofwishfulthinking.Itwillbeuptothetopexecu-tive,duringhisorherreviewoftheback-upbudgets,totestthesoundnessofunderlyingplans.

ALookatZero-BaseBudgetingAnothercurrentlypopularapproachtobudgetingiszero-basebudgeting.WhenPresidentCarterdecidedin1977thatthegovernmentwouldadoptzero-basebudgeting,theconceptmushroomedovernightfromasubjectprincipallyofconcerntofinancialexecutivesandorganizationalheadsintoamatterofinteresttoallmanagers.

Thenamezero-base budgeting (ZBB)forbusinessesismisleading.Manypeople,recallingthegovernment initiative,believe thatZBB is a tool forfindingandeliminatingunnecessaryfunctions.That’snotthecase.

Thefactis,inanyorganizationmost,ifnotall,ofthefunctionscurrentlyperformedarenec-essarytoitscontinuedoperation.ZBBisusuallyappliedtohelpmanagementdecidewhethereachofthesefunctionswillmakeitsmaximumcontributiontotheoveralleffectivenessoftheorganizationatitspresentlevelofexpenditure,aloweroneorahigherone.Intheprocess,somefunctionsmaybeeliminated,but thathappensunderanykindofbudgetaryreview. Inmanyinstances,ZBB results in theapprovalof sizable increases in funding foractivitieswhere theanticipatedpayoffwarrantsit.

ZBBisdesignedtohelpmanagementrelateexpenditurestotheresultsexpectedtobeachieved.Eachmanagerpresentsseparatebudgetproposalsforeachfunctionoftheunithemanages.Thus,itissimilartotheteambudgetingapproach.Theseparateproposals,calleddecisionpackages,arewhatdifferentiateZBBfromteambudgetingorthemoretraditionaltypeofbudgetingprocess.

Example:Underconventionalline-itembudgeting,apersonnelmanagerwouldspecifyde-partmentalexpendituresforsalaries,supplies,paymentstoemploymentagencies,etc.Topman-agementwouldthenreviewthetotalofthesecosts.UnderZBB,thepersonnelmanagerwouldpresentseparatesetsofdecisionpackagesforeachofthedepartment’sfunctionalactivities,suchasrecruitingandhiring,EEOcomplianceandbenefitsadministration.

IfyourcompanydecidestointroduceZBBandyou,asamanager,areincludedintheprocess,youwillreceiveinstructionsandformsfromhighermanagement.Althoughtheoddsarethatnotwoorganizationswillgoaboutitexactlythesameway,thepatterninmostorganizationswillfollowthesegeneralsteps:

1. Identifying your objectives:ThesecretoflivingsuccessfullywithZBBliesincarefullyandthoughtfullyestablishingobjectives.Yourbestbetistostartfromscratchbysittingdownandmakingtwolists:everythingyourunitmustaccomplish,asmandatedbylaworbyhighermanagement,andeverythingyouwouldliketodoorbelievewouldimprovetheperformanceofyourunit.Thiscouldincludeprojectsthathavebeenshotdowninthepast.Byallmeans,includeyourkeysubordinatesinthethinkingatthisstage.

2. Refining your objectives:Whenyouhavecompletedyourlists,youmayendupwith20,30ormoreitems.Thenextstepistoconsolidatethemundermoregeneralcategories.Example: Amedicalofficer’slistsmightincludeyearlyphysicalsforexecutives,employeehealtheduca-tion,voluntaryexerciseclasses,flushots.Allofthesemightfallintothecategoryofpreventivemedicine.

Ifyouwindupwithsixorfewercategories,you’rereadytogoontothenextstep.(Thenumberofdecisionpackagesamanagercanproposeisgenerallylimited,asapracticalmatter,tofiveorsix.)Ifyouhavemorethansix,you’llprobablyhavetodosomehardthinkingaboutyourpriorities.

26 / Business Management Daily

3. Stating your objectives:Youarenowreadytowriteupyourobjectivesinfinalformforthedecisionpackages.Thisisacriticalstep.Youwanttostate,asclearlyaspossible,thepurposeofyouractivityandtheresultsyouplantoachieveinrelationtoorganizationalgoals.Example: Supposeyouarethemanagerofsecurityforamanufacturingplant.Agoodstatementofob-jectiveswouldbe:“Toprotect—atthelowestpossiblecost—againstlossesduetopilferage,burglary,robbery,vandalismandfire,thuscontributingtoprofit.”Bycontrast,apoorstate-mentwouldbe:“Topatrolthegroundswithguardsanddogs,andmaintainthesecurityofthefenceandguardpoststopreventunauthorizedactivities.”Thatismoreadescriptionofactivitythanastatementofgoals.

4. Supporting your objectives:Onceyouhavedeterminedtheobjectivesforeachpackage,thenextstepistoexplorealternativewaysofreachingthem.Forestablishedactivities,thecurrentmethodisalwaysonealternative.Othersmightbetocontractouttheactivity,eliminateitorcombineitwithanotherone.

Usually,managersareaskedtospecifytwoalternativesthathavebeenconsidered,andexplainbrieflywhytheyarenotrecommended.Sometimesthismayseemlikeameaninglessexercisebecausetheonebestwayisobvioustoyou.Butthepurposeistoensurethatyoudon’tblindyourselftootherpossibilities,andthiscanoftenbehelpful.

5. Allocating costs:Afteryou’veselectedyourpreferredalternativeforeachobjective,youhavetodecidehowmuchshouldbespenttoaccomplishit.Yourstartingpointwillgenerallybeyourcurrentbudgetandcontrollable-costreports.Onepracticalwaytobeginistosetupaworksheetshowinglineitemsdowntheleft-handsideandobjectivesacrossthetop.Thenal-locateyourlineitemsasbestyoucantoeachoftheobjectives.Thisshowsyourcurrentlevelofeffort(spending)andwillbespelledoutinadecisionpackage.

Dependingontherequirementsestablishedbyyourorganization,youwillalsobeexpectedtodefinetwoormorelevelsofeffortinrelationtoeachobjective.Ifthecurrentfundingdoesnotaccomplish100percentoftheobjectiveyouarerecommending,thenoneormoreoftheadditionallevelswillbehigherthanthepresentexpenditure.Youwillalsobeaskedtospelloutsomelevelsbelowthecurrentfundingthatwouldbefeasible,butnotnecessarilydesirable.Oneofthesemaybeaminimumlevel,belowwhichitisnotworthwhiletocontinuethefunction.Manyorganiza-tionssetfiguresinpercentagesforthelowestlevelofeffort.

6. Preparing your decision package:Nowyouarereadytofillouttheformsthatwillbecomeyourdecisionpackages foreachobjective.Mostorganizationsdesign theirown,buteachpackageshouldincludethefollowing:

● Adescriptionofgoalsorobjectivesforeachlevelofeffort(expenditure).● Abriefdescriptionoftheactivitytobeundertakenandthecostsinvolved.● Theexpectedbenefitthislevelofeffortwillprovide.● Theprobableunfavorableconsequencesifthefundingisnotapproved.

Usually,youwillalsobeaskedtonotethealternativesthatyouconsideredbutdidnotulti-matelyrecommend.

Next,youmustrankthecompletedpackagesinorderofimportance.Ifyouhavefiveobjec-tives,youwillhavefivesetsofdecisionpackages,eachofwhichmustberankedagainst theothers.Thenthepackagesaresentontoyoursuperiorortosomeotherdesignatedindividualintheorganization.

Mastering Business Finance / 27

7. Evaluating decision packages: Evaluationproceduresdiffer amongorganizations. Somebusinessesuseagroupsystem.Managersonagivenlevel,workingasarankingcommittee,discussoneanother’sproposalsandrankthembeforesubmittingthemtotheofficerinchargeofZBB.Inothercases,alldecisionpackagesgodirectlytotopmanagement.

Oncemanagementhasdecidedwhichdecisionpackagestoacceptandatwhichlevelofeffort,themanagerisusuallynotifiedbyherimmediatesuperior.Theamountsapprovedthenbecomethelimitswithinwhichthemanagerpreparestheconventionalline-itembudget.Thisisused,asusual,foraccountingpurposesandtomonitorcurrentexpendituresduringtheyear.

WhatNottoExpectFromaBudgetTherearelimitstothebenefitsabudgethastooffer—limitsthatmanagementissometimesslowtorecognize.Herearesometrapstoavoidwhenimplementingorreorganizingyourownbudget,whetheritbeforadepartmentorawholecompany:

✔ No substitute for a cost-reduction program:Atone timemanagementviewed itsbudgetprimarilyasacost-reductiontool.Itprovidedmeaningfulreductionsincostsduringthefirstyearortwoafterinstallation.Afterthefathadbeentrimmed,however,costreductionsbecamemoredifficulttoachievesimplybecausetherewasalimittotheimprovementsanoperatingmanagercouldproducewithoutadditionalmanagementsupport.

Oncethislimithadbeenapproached,furthertighteningofbudgetstandardswasself-defeating.Operatingmanagers,realizingthatthenew,morestringentbudgetstandardscouldnotbemet,simplyignoredthem.Becausemanagementcouldn’tdischargeallthemanagers,varianceswereoverlookedandthebudgetbecameineffective.

➤ Observation:Cost-reductionsystemscostmoney.Whetheritbenewcapitalequipment,moresophisticatedcostaccounting,additionalengineeringsupportorawork-measurementpro-gram,aconcertedprogramtoreducecostsmustinvolvemuchmorethanabudget.Thebudgetingfunctioncanhelpidentifytheseneedsandcanspottheimprovementwhenitcomes.Itcannotdothejobalone,however.

✔ Not written in stone:Allbudgetsshouldbesubjecttoperiodicreviewandrevision.Budgetsshouldneverberegardedasthefinalwordonhowtorunanoperation.Yet,inmanyinstances,operatingmanagersattempttoadheretooutdatedbudgets,eventhoughtheyrecognizethatthebestinterestsofthecompanymightbebetterservedbyabudgetrevision.

Example:Adepartmentheadcomesupwithagoodideathatwillsavemoneyinthelongrunbutwillincreasecostsinthenextfewmonths.Ifyousidetracktheideabecauseofbudget-aryconstraints,yourcompanyneedstoreviseitsconceptofbudgeting.Bythesametoken,anoptimisticproductionplannotquicklyalteredinaneconomicdownturncanplayhavocwiththecompany’sfinances.

✔ No substitute for a long-range plan:Manycompanies,afterinstallingaformalbudget,be-lievetheyhavealsotakencareofanynecessaryplanning.Nothingcouldbefurtherfromthetruth.Corporateplanningisakintobudgetinginmanyrespects,butitisfarafieldinsomeall-importantareas.

First, there is thegoal-setting function.Abudgetusuallyassumes that theoperationsofthecompanywillremainmoreorlessintactforatime.Aplanmakesnosuchassumption.Onthecontrary,oneofthepurposesofplanningistosetnewgoalsformanagement.Second,there

28 / Business Management Daily

aretiming considerations.Byit’sverynature,budgetingisconcernedsolelywithshort-rangedecisions.Budgetsusuallyhavearangeofoneyear,brokendownintoquartersandmonths.Bycontrast,planningplacesprimaryemphasisonthelong-termoutlook.Fiveyearsisusuallytheminimumperiodinvolvedinlong-termplanning.

➤ Observation:Intruth,budgetingandplanningcomplementeachother.Companiesthatfailtotakethetimeandefforttoworkoutlong-termgoalsoftenfindthattheirshort-termobjec-tivesareinconflictandarewastingcorporateassets.Thosewhofailtosetdefiniteshort-termplansmayoftenfindthatlong-rangegoalsareunattainablesimplybecausetheywerebasedonerroneousassumptions.

Mastering Business Finance / 29

ShouldYouUseaFixed orVariableBudget?

Onceyouhavedeterminedyourbudgetingapproachandhaveassignedcertainfunctionsto yourstaff,youcanproceedtothenextstep:developingthebudgetitself.Therearetwo

formatsyoucanuse:fixedorvariable.Eachhasitsstrengthsandweaknesses.Yourdecisiononwhichformtousewill,inthefinalanalysis,dependonwhatyouwantyourbudgettoaccomplish.

Fixedbudgets areby far themost common,particularly in smaller companies.Theyarerelativelysimpletopreparebuthavedefinitelimitations.Variable,orflexible,budgetsrequireabitmoreworktoinstall.Theyare,however,mucheasiertoadjustforinflationandforchangesinthelevelofoperatingactivity.Theemergenceofinflationasarelativelypermanentfixtureonthebusinessscene—anditsconsequentimpactonbusinessactivity—hasinevitablyledtotheincreaseduseofvariable-budgettechniques.

LimitationsofaFixedBudgetInasmallmetalworkingfirmusingafixedbudget,preparationsbeginaboutmidwaythrougheachfiscalyear.Eachdepartment,withthehelpofaccounting,preparesanoperating-costbudget,whichisthensenttoseniormanagement,whomayreviseit.

Ifrevisionisnecessary,theywillholddiscussionsandironouttheirdifferences.Then,nearthebeginningofthenewfiscalyear,thenewbudgetiscirculated,completewithmonthlyactivitygoalsandcostallowancesfortheentireyear.Meanwhile,managementhasusedthebudgettoestablishoverallsalesandprofitprojectionsfortheyear,andhassetcapitalexpendituresaswell.

➤ Observation:Aslongassalesorrevenuestayreasonablyclosetobudgetedlevels,theearn-ingsestimateandcoststandardsshouldholdupfairlywell.However,shouldtheactivitylevelvarytoanysubstantialdegreefromtheoriginalforecast,costallowanceswillquicklygetoutofline.

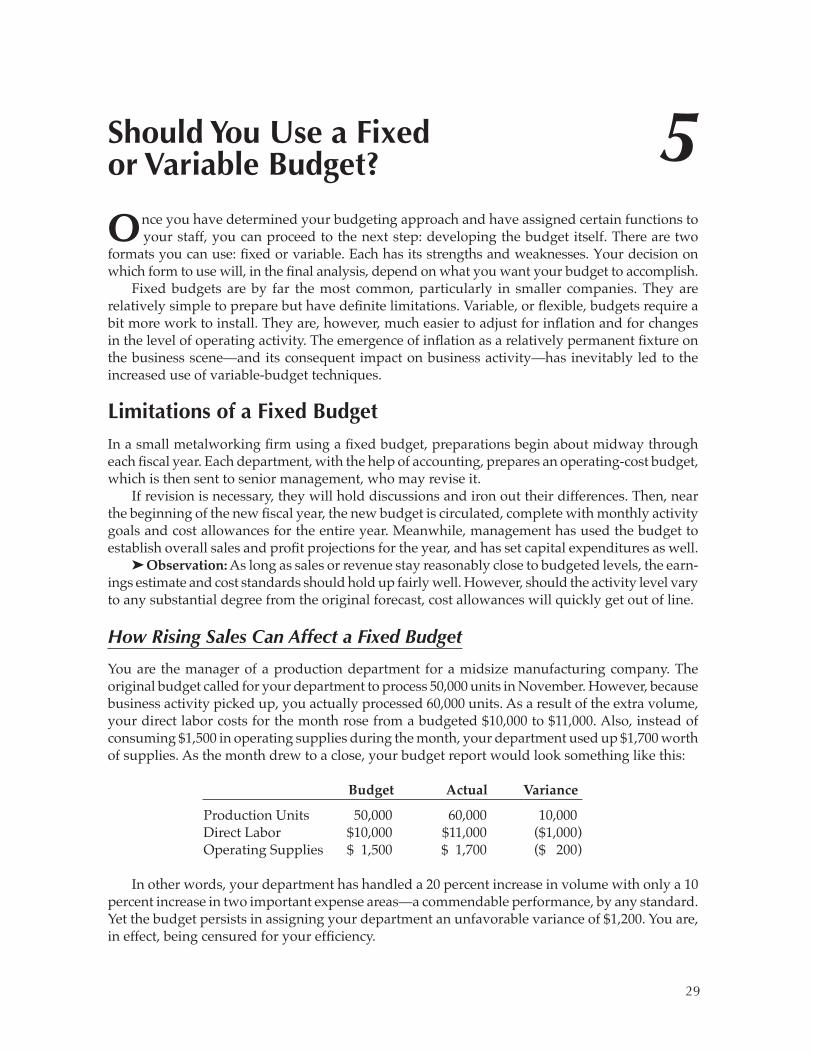

How Rising Sales Can Affect a Fixed Budget

Youare themanagerofaproductiondepartment foramidsizemanufacturingcompany.Theoriginalbudgetcalledforyourdepartmenttoprocess50,000unitsinNovember.However,becausebusinessactivitypickedup,youactuallyprocessed60,000units.Asaresultoftheextravolume,yourdirectlaborcostsforthemonthrosefromabudgeted$10,000to$11,000.Also,insteadofconsuming$1,500inoperatingsuppliesduringthemonth,yourdepartmentusedup$1,700worthofsupplies.Asthemonthdrewtoaclose,yourbudgetreportwouldlooksomethinglikethis:

Budget Actual Variance

ProductionUnits 50,000 60,000 10,000 DirectLabor $10,000 $11,000 ($1,000) OperatingSupplies $1,500 $1,700 ($200)