1 Copyright © 2012 Mahindra & Mahindra Ltd. All rights reserved. 1

Nov. 2013

M&M Investor Presentation

2

All around us

US on Path of

Growth Europe - Mixed

Emerging

Markets -

Slowing

External Factors

Global story

QE tapering impact

Developed World as “New Emerging World”

3

Political Uncertainty

Policy Action

GDP Growth

Current Account Deficit

Cost of Borrowing

Investment Slowdown

All around us

India story

FY 2014 will be crucial one to watch

4

Double-Edged Sword

Global Domestic

5

Business Sectors

Automotive & Farm Equipment

Aftermarket

Hospitality

Mahindra Partners (Steel, Retail, Trade, Logistics, Boats,

Energy, Media)

2 Wheeler

Systech

Information Technology

Real Estate

Defence Systems

Financial Services

The Mahindra Group comprises 10 business sectors with a presence in 18 Industries

6

Mahindra Group

Market leader in Utility Vehicles in India

Market leader in Tractors in India.

Number One Global tractor manufacturer (Single legal entity)

Mahindra Finance : Leader in rural financing

Tech Mahindra : Leader in Telecom Software

Mahindra Holidays : Leader in ‘Time Share’

Business Leadership

7

Mahindra & Mahindra Ltd.

M&M is one of India's leading utility vehicle and tractor manufacturers

Market leader – for H1FY14 – in UVs (market share 42.8%) and in Tractors

(market share 41.0%)

Equity Structure of the company –

– 25.3% Promoter & Promoter Group, 74.7% Public (44.6% Foreign)

As at Sept. 30, 2013

Manufacturing plants all across India –

– Auto plants – 6, Tractor plants – 7, Foundry plant – 1

– Subsidiaries – Total - 130 , Operational – 62 As at Sept. 30, 2013

Company Overview

8

Life Insurance Corporation of India

Golboot Holdings Ltd (Goldman Sachs)

Dodge & Cox

ICICI Prudential Life Insurance Ltd

First State Investments

Capital Group

General Insurance Corporation of India

Government of Singapore

The New India Assurance Company Ltd

Vanguard Emerging Markets Stock Index

Fund

J P Morgan Group

Top 10 Shareholders with > 1%

Shareholding Pattern …. 30 Sept., 2013

Promoter and

Promoter Group 25.3%

FII / NRI / GDR

44.6%

Insurance Cos.

15.1%

FI / MF / Banks 1.5%

Individuals 13.5%

9

Financials

10

Financial Highlights

Growth in Total income

Rs 9,888 crs

Rs 10,787 crs

-8%

Q2 – FY14 Vs Q2 – FY13 (M&M + MVML)

Rs 1,254 crs

Rs 1,280 crs

-2%

Rs 1,028 crs

Rs 978 crs

5%

Growth in EBIDTA Growth in PAT Growth in PAT

11

Financial Highlights

Growth in Total income

Rs 43,655 crs

Rs 35,005 crs

25%

FY13 Vs FY12 (M&M + MVML)

Rs 5,329 crs

Rs 4,150 crs

28%

Rs 3,634 crs

Rs 2,997 crs

21%

Growth in EBIDTA Growth in PAT

Rs 3,544 crs

Rs 2,740 crs

29%

Growth in PAT

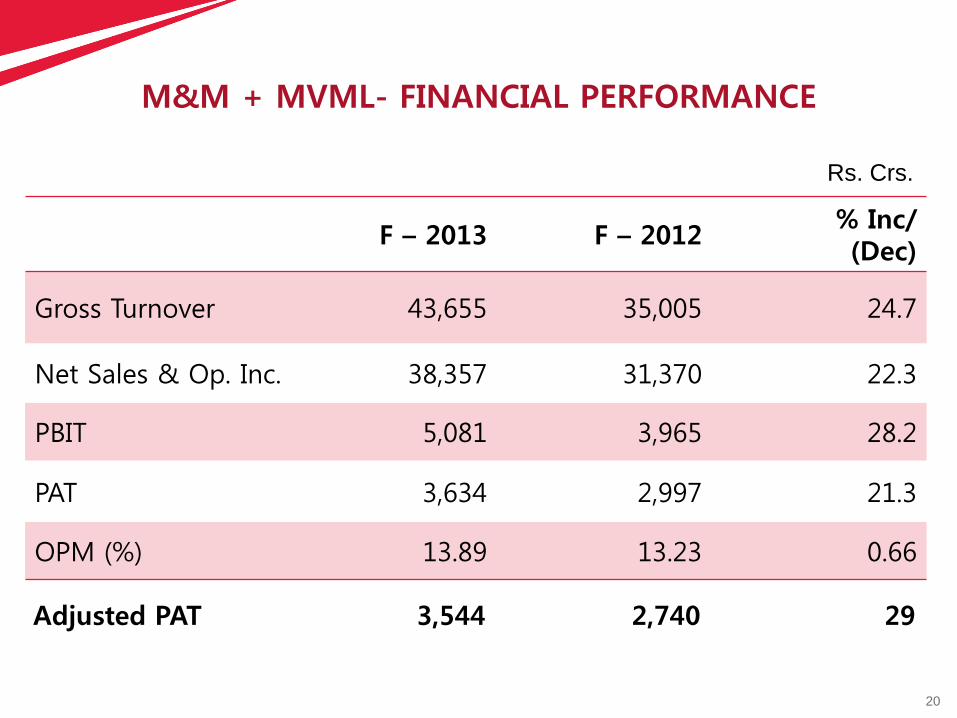

* On like to like comparison, excluding one time benefit of Rs. 257

crores on account of MADPL merger from FY 2012 & Rs. 91 crs in FY 13

of Exceptional Gain on sale of MHRIL shares

Adjusted PAT*

12

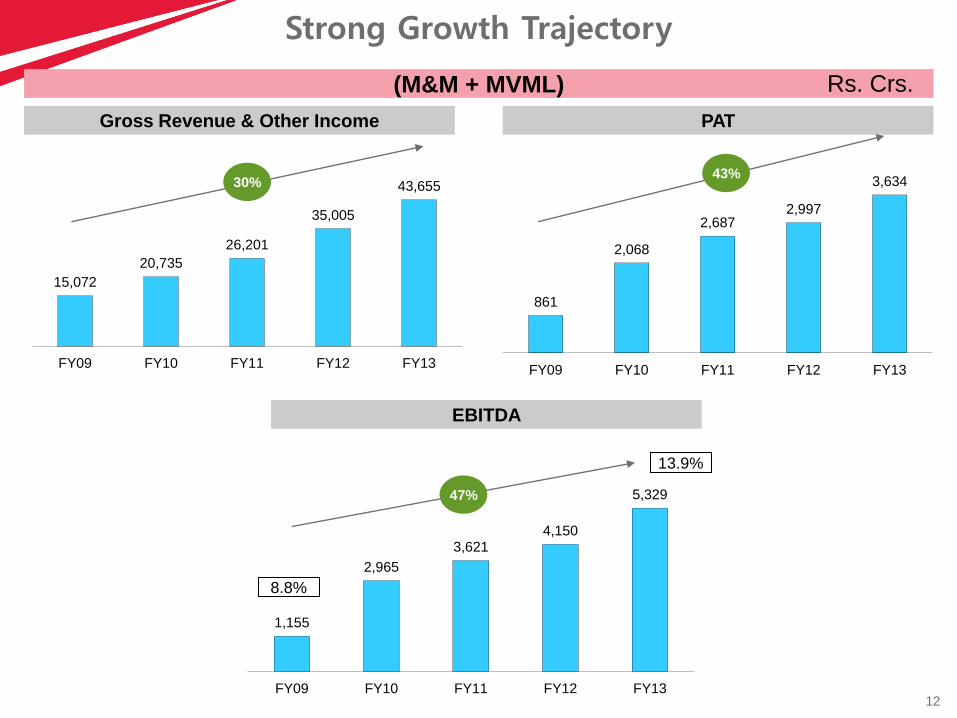

Strong Growth Trajectory

Gross Revenue & Other Income PAT

861

2,068

2,687 2,997

3,634

FY09 FY10 FY11 FY12 FY13

(M&M + MVML)

15,072

20,735

26,201

35,005

43,655

FY09 FY10 FY11 FY12 FY13

30% 43%

EBITDA

1,155

2,965

3,621 4,150

5,329

FY09 FY10 FY11 FY12 FY13

47%

8.8%

13.9%

Rs. Crs.

13 Copyright © 2012 Mahindra & Mahindra Ltd. All rights reserved.

Delivering consistent, long term value

Last 5 years

Note: Adjusted for Bonus & Stock-split Ex Dividend price

Last 11 years

4.1

Last 21 years

6.5

40.4

1.5

1.5

3.2

3.74

7.15

31.54

0 10 20 30 40

Gold

Sensex

M&M

As at 30th September

14

Original Investment Cost Vs. CMP

As on 30th, Sept. 2013 Cost Market Value

Listed Companies

Subsidiaries 3589 14,656

Associates 649 8,282

Total 4,238 22,938

Rs. Crs

15

Unlocking Shareholders Value – Since 2005

Corporate Actions

Bonus Issue – FY 2005 – 1:1

Stock Split – FY 2011 – 1:2

Global Alliance

CIE – Mahindra Deal

16 Copyright © 2012 Mahindra & Mahindra Ltd. All rights reserved.

Strong Credit Profile

0.81

0.45

0.32 0.37

0.3 0.24 0.26

F 2

009

F 2

010

F 2

011

F 2

012

F 2

013

Q2F

13

Q2F

14

2.94

1.12

0.82 0.98 0.76 0.64 0.71

F 2

009

F 2

010

F 2

011

F 2

012

F 2

013

Q2F

13

Q2F

14

DE Ratio M&M + MVML

Gearing Multiple M&M + MVML

Stable Rating AA+ by CRISIL/ICRA/CARE *

* Rating is for M&M Ltd (Standalone Company)

“Healthy financial risk profile supported by considerable financial flexibility arising from market value of investments” - Crisil ‘s Credit Rating Report, April 2013

17

One of the first issuer of GDR of US$ 75 mn in 1993

One of the first issuer of FCCB of US$ 100 mn in 1996

First to issue Rs. 500 Cr. 50 year bullet tenure debentures

XBRL filing – 69 companies within MCA deadline

Financial Milestones

18

Marathon Runner

Prudent Capital Allocation Support growth with Strategic Acquisition Maintain strong Credit Rating

Deliver long term shareholder value

19

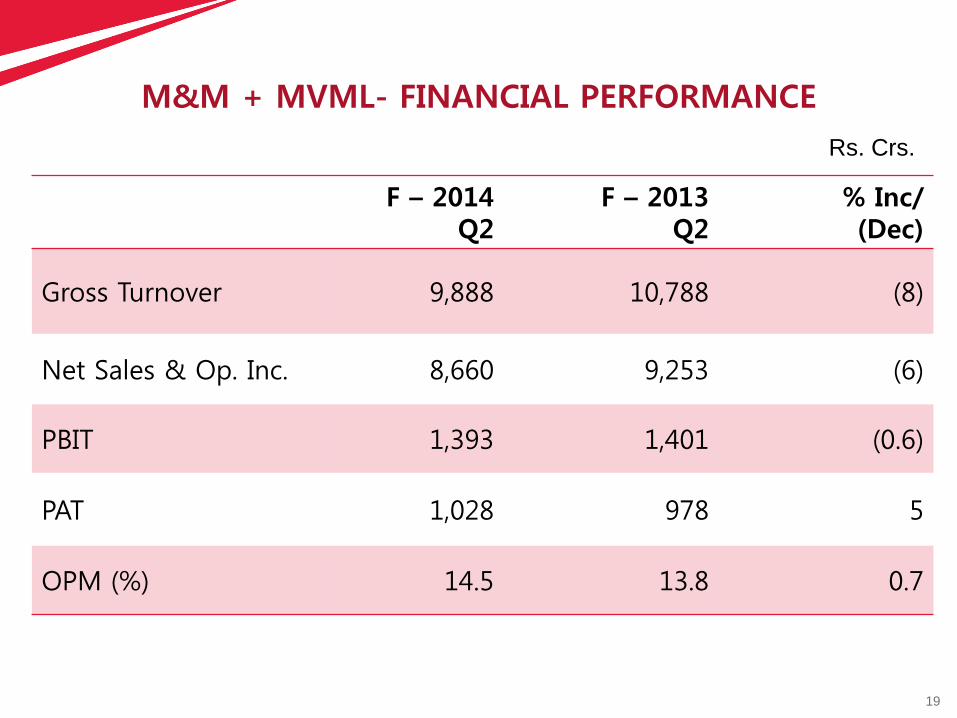

M&M + MVML- FINANCIAL PERFORMANCE

F – 2014 Q2

F – 2013 Q2

% Inc/ (Dec)

Gross Turnover 9,888 10,788 (8)

Net Sales & Op. Inc. 8,660 9,253 (6)

PBIT 1,393 1,401 (0.6)

PAT 1,028 978 5

OPM (%) 14.5 13.8 0.7

Rs. Crs.

20

M&M + MVML- FINANCIAL PERFORMANCE

F – 2013 F – 2012 % Inc/ (Dec)

Gross Turnover 43,655 35,005 24.7

Net Sales & Op. Inc. 38,357 31,370 22.3

PBIT 5,081 3,965 28.2

OPM (%) 13.89 13.23 0.66

PAT 3,634 2,997 21.3

Adjusted PAT 3,544 2,740 29

Rs. Crs.

21

M&M + MVML - BALANCE SHEET

F -2013 F -2012

Source of Funds

Shareholder’s Funds 15,055 12,219

Loan Funds * 4,464 4,544

Deferred Tax Liability 756 589

Total 20,275 17,352

* Includes current maturities of Long Term Liabilities

Rs. Crs.

22

M&M + MVML - BALANCE SHEET

F -2013 F -2012

Application of Funds

Fixed Assets 7,747 6,889

Investments 10,894 9,474

Long Term Loans & Advances 2,562 1,734

Cash & Bank Balances 1,823 1,291

Proposed Dividend (891) (869)

Other Assets (Net) (1860) (1167)

Total 20,275 17,352

Rs. Crs.

23

Segment wise Financials

F – 2014 Q2

Inc / (Dec)

F – 2013 Inc / (Dec)

Segment Revenue AS* 5,555 (16%) 26,489 34%

FES 3,148 19% 11,990 3%

Segment Results@ AS* 624 (23%) 3,117 45%

FES 534 36% 1,858 1%

Segment ROS % AS* 11.2% (0.9%) 11.8% 1%

FES 17% 2% 15.5% 0%

Capital Employed AS* 6,881 16% 6,167 20%

FES 3,320 18% 2,504 7%

Rs. Crs.

@.- After Exceptional Items

* - AS+MVML

24

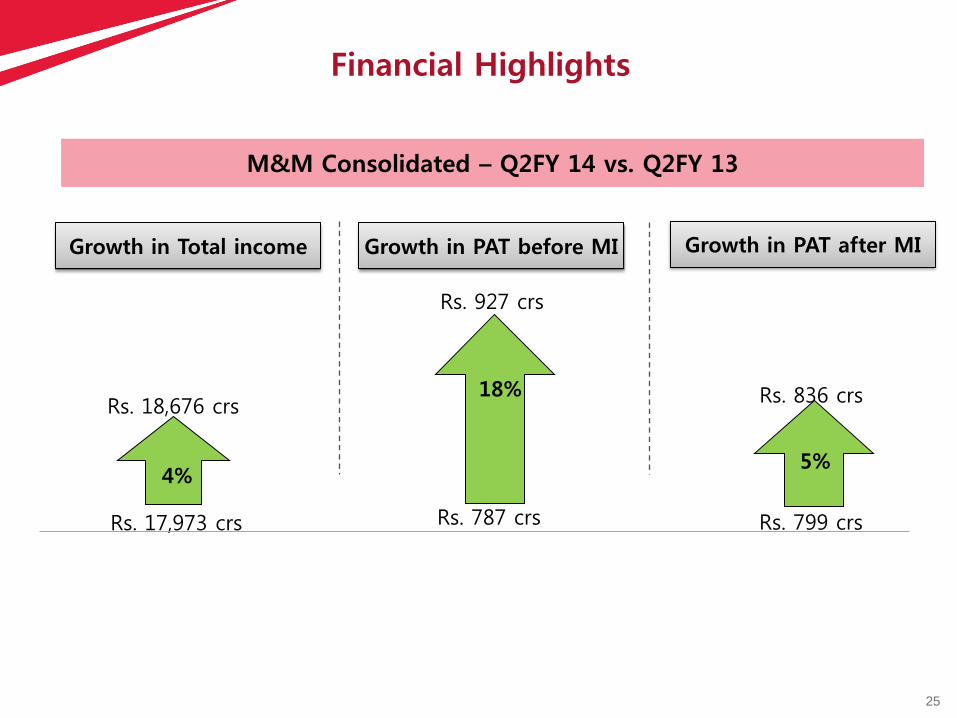

25

Rs. 836 crs

Rs. 799 crs

5%

Financial Highlights

Growth in Total income

Rs. 18,676 crs

Rs. 17,973 crs

4%

M&M Consolidated – Q2FY 14 vs. Q2FY 13

Rs. 927 crs

Rs. 787 crs

18%

Growth in PAT before MI Growth in PAT after MI

26

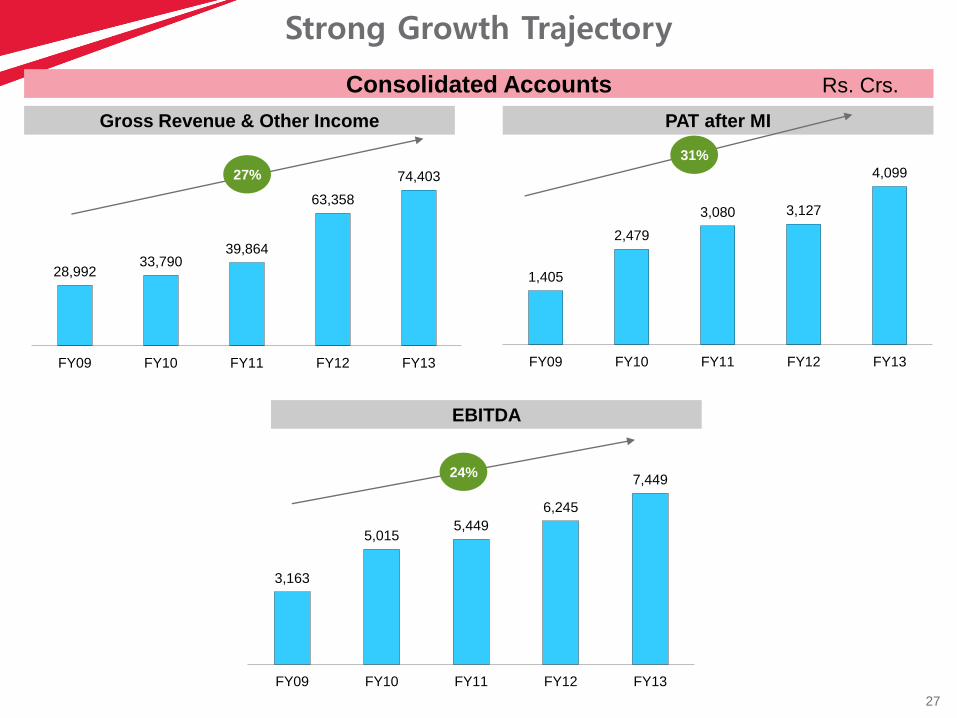

Rs. 4,099 crs

Rs. 3,127 crs

31%

Financial Highlights

Growth in Total income

Rs. 74,403 crs

Rs. 63,358 crs

17%

M&M Consolidated – FY 13 vs. FY 12

Rs. 7,449 crs

Rs. 6,245 crs

19%

Growth in EBIDTA Growth in PAT after MI

27

Strong Growth Trajectory

Gross Revenue & Other Income PAT after MI

1,405

2,479

3,080 3,127

4,099

FY09 FY10 FY11 FY12 FY13

Consolidated Accounts

28,992 33,790

39,864

63,358

74,403

FY09 FY10 FY11 FY12 FY13

27%

31%

EBITDA

3,163

5,015 5,449

6,245

7,449

FY09 FY10 FY11 FY12 FY13

24%

Rs. Crs.

28

M&M Group Consolidated Results

# includes share in profits of Associates

F – 2014 Q2

F – 2013 Q2

% Inc/ (Dec)

Gross Income & Other Income

18,676 17,973 3.9

PAT before MI # 927 787 17.8

PAT after MI 836 799 4.6

Rs. Crs.

29

M&M Group Consolidated Results

# includes share in profits of Associates

F – 2013 F – 2012 % Inc/ (Dec)

Net Sales & Op. Income 68,735 59,398 15.7

PAT before MI # 4,129 3,060 34.9

PAT after MI 4,099 3,127 31.1

Rs. Crs.

30

Group Companies – Top 4 PAT Earners

Q2F14 – Rs.232 crs

Q2F13 – Rs.193 crs

21%

MMFSL

Q2F14 – Rs.29 crs

Q2F13 – Rs. 27 crs

MHRIL

7%

Q2 F14 – Rs. 717 crs

Q2 F13 – Rs. 456 crs

58%

TML

Q2 F14 – Rs.7 crs

Q2 F13 –Rs. (39) crs

SYMC

118%

31

Automotive

Revenue

10,475

3%

10,165

Q2FY 14

Q2FY 13

Automotive

Results

501

20%

625

Q2FY 14

Q2FY 13

Fin. Services

Revenue

1,293

33%

973

Fin. Service

Results

359

25%

288

IDS

Revenue

199

46%

136

IDS

Results

47

13%

41

Hospitality

Revenue

204

13%

181

Hospitality

Results

35

7%

Q2FY 14

Q2FY 13

Q2FY 14

Q2FY 13

Segment Details

Segment Results is before Exceptional items

Rs. Crs.

32

Farm Equip.

Revenue

3,742

22%

3,059

Q2FY 14

Q2FY 13

Farm Equip.

Results

532

66%

321

Q2FY 14

Q2FY 13

Others

Revenue

790

31%

603

Others

Results

(143)

64%

(88)

Segment Details

Segment Results is before Exceptional items

Rs. Crs.

33

Systech

Revenue

1,290

3%

1,250

Q2FY 14

Q2FY 13

Systech

Results

(12)

18%

(10)

Q2FY 14

Q2FY 13

STP *

Revenue

275

29%

389

STP *

Results

20

22%

25

IT Services

Revenue

65

88%

556

IT Services

Results

7

89%

64

Segment Details

* STP – Steel Trading & processing Segment Results is before Exceptional items

Rs. Crs.

34

Automotive Sector

35

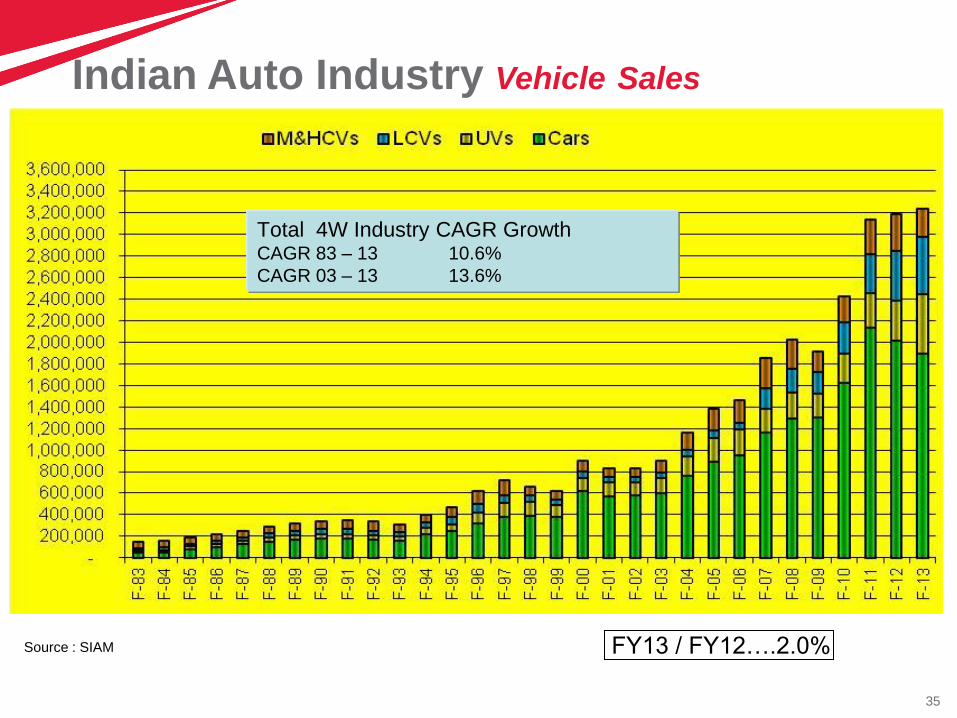

Indian Auto Industry Vehicle Sales

Total 4W Industry CAGR Growth CAGR 83 – 13 10.6%

CAGR 03 – 13 13.6%

FY13 / FY12….2.0% Source : SIAM

36

M&M Auto Sector sales – Domestic + Export

87117

145 149178

231 230

298

377

483

563

F03 F04 F05 F06 F07 F08 F09 F10 F11 F12 F13

Total AS Sales (‘000)

21%

CAGR

37

*M&M Ltd. is the largest utility vehicle company in India SIAM data

Utility

Vehicle

Player in

India

38

20

L

5L 12 .5L 15

L

10

L

7 .4L 10 .8L

8L 11 .5L

11 .0L 14 .7L

18 .5L 20 .6L

6 .7L 7 .4L

5 .9L 7 .7L

Presence across all price points

39

6 .2

L

1L 3L 4L 2L

3 .4L

1 .62L 1 .69L

1 .9L

5L

4 .1L 4 .5L

5 .5L

5 .5L 6 .2L

3 .7L 3 .8L

3 .7L 3 .5L

Presence across all price points

40

H1F14 Domestic Market Performance Period : April – September

UV Total

Cars (Verito)

MPV Total

LCV < 2T

2T > LCV < 3.5T

3W Total

AD (Dom.) Total

LCV > 3.5 T Total

MHCV (Goods)

AS (Dom.) Total

Non Participating Segments

MHCV Passenger

MCV Goods

Cars (Excl. Super Compact)

AS (Dom.) Total

Segment H1 F14Actual

243,640 -4.8%

164,879 33.2%

101,834 -9.8%

87,016 -26.6%

94,447 17.1%

239,539 -4.4%

931,355 -1.2%

39,688 -12.6%

44,375 -30.9%- 0.0%

1,015,418 -3.5%- 0.0%- 0.0%

22,791 -11.1%

38,331 -25.2%

690,439 -10.7%

1,766,979 -7.1%

Industry

GrowthH1 F14Actual

104,357 -14.0%

6,134 -21.2%

14,773 -4.2%

15,223 -28.0%

55,194 19.4%

28,409 -8.4%

224,090 -7.8%

3,429 -27.8%

917 -33.3%- 0.0%

228,436 -8.3%- 0.0%- 0.0%

- 0.0%

- 0.0%

- 0.0%

228,436 -8.3%

M&M AS

GrowthH1 F14 H1 F13

Actual Actual

42.8% 47.4%

3.7% 6.3%

14.5% 13.7%

17.5% 17.8%

58.4% 57.3%

11.9% 12.4%

24.1% 25.8%

8.6% 10.5%

2.1% 2.1% 0.0% 0.0%

22.5% 23.7% 0.0% 0.0% 0.0% 0.0%

0.0% 0.0%

0.0% 0.0%

0.0% 0.0%

12.9% 13.1%

M&M Mkt. Share

41

M&M International Market Performance

F13 Concern Markets

• Sri Lanka 18% Mkt. drop + duty impact

• Bangladesh 63% Mkt. drop

• Bhutan 77% Regulation for import payment

F13 Growth Markets

• South Africa 57%

• Chile 48%

• Nepal 47%

High growth in FY13 H1, Slowdown from FY13 H2 onwards …

12,956

18,190

H1 F12 H1 F13

H1 F13

20,313

15,601

F13 F14

Apr-Sept

16,220 14,226

H2 F12 H2 F13

H2 F13

12% 40% 23%

42

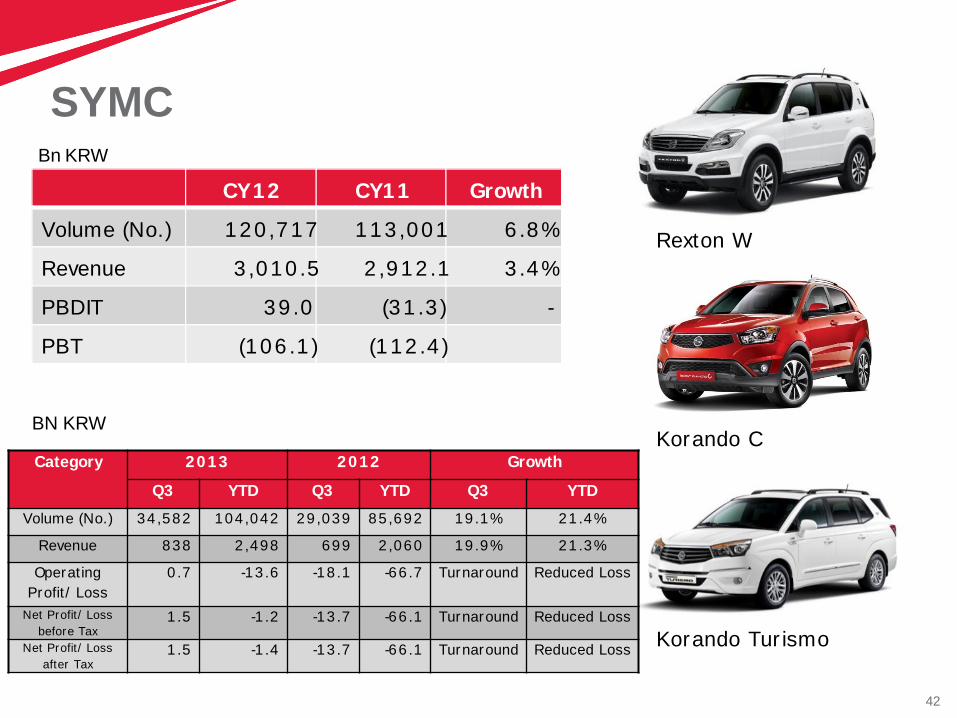

SYMC

Korando Tur ismo

Rexton W

Korando C

CY 12 CY11 Growth

Volume (No.) 120 ,717 113 ,001 6 .8%

Revenue 3 ,010 .5 2 ,912 .1 3 .4%

PBDIT 39 .0 (31 .3 ) -

PBT (106 .1 ) (112 .4 )

H1 CY 14 H1 CY13 Growth

Bn KRW

Category 2013 2012 Growth

Q3 YTD Q3 YTD Q3 YTD

Volume (No.) 34 ,582 104 ,042 29 ,039 85 ,692 19 .1% 21 .4%

Revenue 838 2 ,498 699 2 ,060 19 .9% 21 .3%

Operating

Profit / Loss

0 .7 -13 .6 -18 .1 -66 .7 Turnaround Reduced Loss

Net Profit/ Loss

before Tax 1 .5 -1 .2 -13 .7 -66 .1 Turnaround Reduced Loss

Net Profit/ Loss

after Tax 1 .5 -1 .4 -13 .7 -66 .1 Turnaround Reduced Loss

BN KRW

43

Improved Customer Satisfaction Sales Satisfaction Index (2013)

803

820

841

2011 2012 2013

Rank – 8 th

Rank – 6 th

Rank – 3 rd

M&M Rank

Source: 2013 JD Power Sales Satisfaction Study

44

Improved Customer Satisfaction Customer Satisfaction Index (2013)

Source: 2013 JD Power Customer Satisfaction Study

744

798

813

2011 2012 2013

Rank –

11 th

Rank –

5 th

Rank – 4 th

M&M Rank

45

Presence in every nook and corner

Sales Network – 1372 Service Network - 1231

Network reaching more than 70% of the districts in India

Reaching 900+ towns/semi-urban and rural areas across the country

46

Financial Performance – AD + MVML

Q2FY2014 %YoY FY2013 %YoY

Segment Revenue Rs. 5,555 -16% Rs. 26,489 34%

Segment Results (after

exceptional items)

Rs.624 -23% Rs. 3,118 45%

Segment capital

employed

Rs. 6,881 16% Rs. 6,167 20%

Rs. Crs.

47

Farm Equipment Sector

48

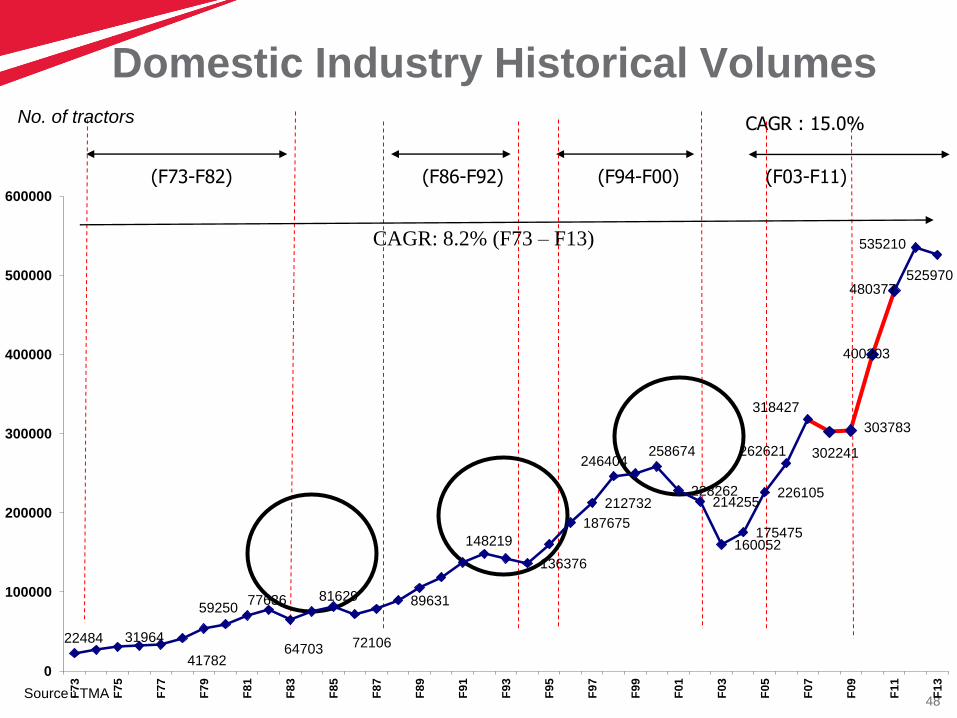

Domestic Industry Historical Volumes

CAGR : 15.0%

(F73-F82) (F86-F92) (F94-F00) (F03-F11)

No. of tractors

CAGR: 8.2% (F73 – F13)

Source : TMA

22484 31964

41782

59250 77636

64703

81629

72106

89631

148219

136376

187675

212732

246404 258674

228262 214255

160052 175475

226105

262621

318427

302241

303783

400203

480377

535210

525970

0

100000

200000

300000

400000

500000

600000

F7

3

F7

5

F7

7

F7

9

F8

1

F8

3

F8

5

F8

7

F8

9

F9

1

F9

3

F9

5

F9

7

F9

9

F0

1

F0

3

F0

5

F0

7

F0

9

F1

1

F1

3

49

M&M Ltd. is the largest tractor company in the world, by volume

*

50

M&M Domestic Market Performance

41,282 44,807 60,005

78,048

95,006 90,509

113,269

166,359

202,513

221,730 211,596

F03 F04 F05 F06 F07 F08 F09 F10 F11 F12 F13

18%

CAGR

51

Tractor Industry & M&M : Pick Up in Momentum…..

253055

313523

F13 F14

103358

128626

F13

Industry M&M

Continued Domination

FES MS : 41.0%

Period : April – September

52

Tractor Market Share Total no. of Tractors

52

40.8 41.4 42.0 41.4 40.2 41.0

22.3 22.0 20.4 23.4 25.0 25.1

13.5 13.3 13.2 11.4 11.7 10.8

8.9 8.7 8.6 8.3 9.7 10.1 3.1 2.8 2.6 2.8 2.5 2.5 5.3 4.8 5.1 5.2 5.2 4.9 6.0 7.0 8.0 7.5 5.7 5.6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

F09 F10 F11 F12 F13 H1F14

JD

FNH

Others

Sonalika

Escorts

Tafe+Eicher

Mahindra

400,203 303,921 480,377 525,970 535,210

Source : TMA

215,211

53

Exports

5,385

6,981 7,525

8,533

6,933

8,837

11,812

13,722

12,289

6063 5215

F05 F06 F07 F08 F09 F10 F11 F12 F13 H1F13 H1 F14

Degrowth in SAARC Countries

54

Customer Satisfaction Index

F08 F09 F10 F11 F12 F13

84

89

93 93 96

108

76 79

83

96

106

115

Mahindra & Swaraj : among Top 2 Brands

55

Beyond tractors…

…towards ‘Farm Tech Prosperity’

56

Agri Business

Growth in F&V (49%) and Agri

inputs (47%)

Retained No. 1 position in

Grapes

Expanding current portfolio and

exploring new segments of agri

value chain

33% Growth

156.2

208.5

H1 F13 H1 F14

Agri Business Revenue (Rs. crs)

33%

Agri Inputs 33%

F&V 26% MIS

41%

Agri Business Revenue Share

57

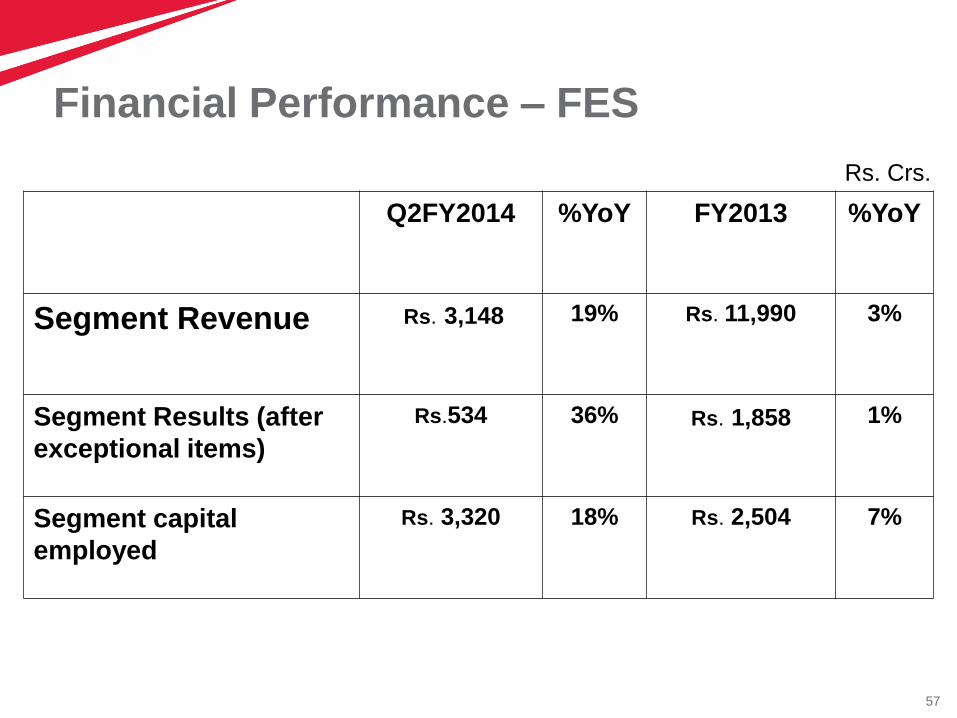

Financial Performance – FES

Q2FY2014 %YoY FY2013 %YoY

Segment Revenue Rs. 3,148 19% Rs. 11,990 3%

Segment Results (after

exceptional items)

Rs.534 36% Rs. 1,858 1%

Segment capital

employed

Rs. 3,320 18% Rs. 2,504 7%

Rs. Crs.

58

F14 : Industry Outlook

Industry expected to grow at 15 - 17%

59

Sustainability

Released annual sustainability reports since 2008 to map triple bottom line

performance

Sustainbility reports realeased since 2008 are externally assured & GRI

checked for Application level A+

Ranked 1st in S&P’s ESG India Index-2012

One of the top rankers in the Asian Sustainability Ratings (“ASR”)

Winner in the automobiles category, under the Energy Intensive industries

cluster, in the Green Business Leaders award 2011-12 instituted by

Emergent Ventures India & Financial Express.

CII Sustainability Plus Rating:-

– M & M rated no.1 in transport equipment sector in Gold category and

secured 9th place out of total 100 rated companies in the year 2012.

Carbon Disclosure Leadership Index:-

– M&M Limited was rated with a second highest score of 82 among the top

200 Indian companies in the CDLI ratings for 2012.

60

Commitment to Society

The Mahindra Group

has pledged to dedicate

1% of its Profit after Tax to CSR

initiatives

61

Disclaimer

Mahindra & Mahindra herein referred to as M&M, and its subsidiary companies provide a wide array of presentations and reports,

with the contributions of various professionals. These presentations and reports are for informational purposes and private circulation

only and do not constitute an offer to buy or sell any securities mentioned therein. They do not purport to be a complete description of

the markets conditions or developments referred to in the material. While utmost care has been taken in preparing the above, we

claim no responsibility for their accuracy. We shall not be liable for any direct or indirect losses arising from the use thereof and the

viewers are requested to use the information contained herein at their own risk. These presentations and reports should not be

reproduced, re-circulated, published in any media, website or otherwise, in any form or manner, in part or as a whole, without the

express consent in writing of M&M or its subsidiaries. Any unauthorized use, disclosure or public dissemination of information

contained herein is prohibited. Unless specifically noted, M&M or any of its subsidiary companies is not responsible for the content of

these presentations and/or the opinions of the presenters. Individual situations and local practices and standards may vary, so

viewers and others utilizing information contained within a presentation are free to adopt differing standards and approaches as they

see fit. You may not repackage or sell the presentation. Products and names mentioned in materials or presentations are the property

of their respective owners and the mention of them does not constitute an endorsement by M&M or its subsidiary companies.

Information contained in a presentation hosted or promoted by M&M is provided “as is” without warranty of any kind, either expressed

or implied, including any warranty of merchantability or fitness for a particular purpose. M&M or its subsidiary companies assume no

liability or responsibility for the contents of a presentation or the opinions expressed by the presenters. All expressions of opinion are

subject to change without notice.

Copyright © 2012 Mahindra & Mahindra Ltd. All rights reserved.

Thank you Visit us at www.mahindra.com