© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

If Mobile’s First, what’s left?

#Mobile Day @JoGoyvaerts October 20st 2015

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 3

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 4

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 5

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 6

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Stuck in complexity?

7

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Be bolt/D Be extremely MOBILE

8

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 9

Short Simple Focus Fun

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Acceptance on BeShopping100 webshops

Active users in last 12 months 800k

PayPal in Belgium: Fast Facts

10

63%

Market Share on all online payments 12%

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 11

12 12

Voice of the Consumer:

The Millennial Disruption Index*

* The Millennial Index – 2014, Scratch, Viacom Media Networks

BankingHousehold Goods

Discount retail

MobilePersonal Computing

Online

Identifies the industries most likely to be transformed by Millennials, the largest generation in American history.

“I don’t see the difference between my bank and all the others.”

71%would rather go to the dentist than listen to what banks are saying.

53%don’t think their bank of-fers anything different than other banks.

Banking is at the highest risk of disruption. 1 in 3 are open to switching

banks in the next 90 days.

They believe innovation will come from outside the industry.

Nearly halfare counting on tech start-ups to overhaul the way banks work.

73%would be more excited about a new offering in financial services from GOOGLE, AMAZON, APPLE, PAYPAL, OR SQUARE than from their own nationwide bank.

Methodology:The data represented illumi-nates key findings from the Millennial Disruption Index (MDI), a three-year study of in-dustry disruption at the hands of teens to thirtysomethings. Millennials, a generation born 1981–2000 and more than 84 million strong in the U.S. alone, use technology, collaboration and entrepreneurship to create, transform and reconstruct en-tire industries. As consumers, their expectations are radically different than any generation before them. For the MDI, Scratch surveyed over 10,000 Millennials about 73 companies spanning 15 in-dustries. The results paint a clear picture of which brands are loved, which are meeting consumer needs, and which are poised on the brink of disrup-tion. The Index also sheds light on the topline features of com-panies that Millennials rely on and identify with. A business category with a low MDI score is less vulnerable to disruption. For categories with a high MDI, Scratch forecasts disruption is imminent. Scratch is a creative and strate-gic SWAT team that channels the power of Viacom’s portfolio in new ways. For more information and the complete study, contact us at [email protected].

THE MILLENNIAL DISRUPTION INDEX

3 years•

15 categories•

200+ interviews•

10,000+ respondents

All 4 of the leading Banks are among the ten least loved brands by Millennials.

The change will be seismic.

68%in 5 years, the way we access our money will be totally dif-ferent.

70%in 5 years, the way we pay for things will be totally different.

33%believe they won’t need a bank at all.

Love

Risk

©2013 Viacom Media Networks

BankingHousehold Goods

Discount retail

MobilePersonal Computing

Online

Identifies the industries most likely to be transformed by Millennials, the largest generation in American history.

“I don’t see the difference between my bank and all the others.”

71%would rather go to the dentist than listen to what banks are saying.

53%don’t think their bank of-fers anything different than other banks.

Banking is at the highest risk of disruption. 1 in 3 are open to switching

banks in the next 90 days.

They believe innovation will come from outside the industry.

Nearly halfare counting on tech start-ups to overhaul the way banks work.

73%would be more excited about a new offering in financial services from GOOGLE, AMAZON, APPLE, PAYPAL, OR SQUARE than from their own nationwide bank.

Methodology:The data represented illumi-nates key findings from the Millennial Disruption Index (MDI), a three-year study of in-dustry disruption at the hands of teens to thirtysomethings. Millennials, a generation born 1981–2000 and more than 84 million strong in the U.S. alone, use technology, collaboration and entrepreneurship to create, transform and reconstruct en-tire industries. As consumers, their expectations are radically different than any generation before them. For the MDI, Scratch surveyed over 10,000 Millennials about 73 companies spanning 15 in-dustries. The results paint a clear picture of which brands are loved, which are meeting consumer needs, and which are poised on the brink of disrup-tion. The Index also sheds light on the topline features of com-panies that Millennials rely on and identify with. A business category with a low MDI score is less vulnerable to disruption. For categories with a high MDI, Scratch forecasts disruption is imminent. Scratch is a creative and strate-gic SWAT team that channels the power of Viacom’s portfolio in new ways. For more information and the complete study, contact us at [email protected].

THE MILLENNIAL DISRUPTION INDEX

3 years•

15 categories•

200+ interviews•

10,000+ respondents

All 4 of the leading Banks are among the ten least loved brands by Millennials.

The change will be seismic.

68%in 5 years, the way we access our money will be totally dif-ferent.

70%in 5 years, the way we pay for things will be totally different.

33%believe they won’t need a bank at all.

Love

Risk

©2013 Viacom Media Networks

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Incidence of buying online via a mobile phone varies by country

13

North America

Western Europe

Nordics Central, Eastern Europe

Middle East Latin America

Asia Pacific

% online shoppers who have bought via a smartphone in past 12 months

31

19

33 26

21

36 34

17

32 23 21 24 20

26 34 37

53 57

34

46

33

68

0 10 20 30 40 50 60 70 80

US CA UK DE FR IT ES NL CH AT SE NO DK PL RU IL TR UA BR MX AU CN

Multi-country average*: 33% of online shoppers have bought online via a smartphone in the past 12 months

*Multi-country average not weighted by country size.

Indicates ‘headroom’ for further growth in this category, especially in mature markets.

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Mobile commerce fueling e-commerce growth

14

North America

Western Europe

Nordics Central, Eastern Europe

Middle East Latin America

Asia Pacific

34 34 36

46 41

22

48 46 41

45 52 54 55

33 28

39 39 39 46

40 45

52

10 14

10 12 16

11 13 8

12 13 13 11 11 10 14 15 17 13

17 21

12

23

0

10

20

30

40

50

60

US CA UK DE FR IT ES NL CH AT SE NO DK PL RU IL TR UA BR MX AU CN

Mobile commerce CAGR Online commerce CAGR

Estimated Compound Annual Growth Rate (CAGR) 2013-2016

Multi-country average*: Mobile commerce expected to grow at 42%, while e-commerce to grow at 13% (CAGR).

Total online spend includes mobile spend. Mobile includes smartphone and tablet spend. .*Multi-country average not weighted by country size. Refer to appendix for how estimates were calculated.

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Smartphone shoppers tend to be younger than online shoppers…

15

North America

Western Europe

Nordics Central, Eastern Europe

Middle East Latin America

Asia Pacific

53 52 58 60 56 52 48

57 55 57 52 50 61 61

73

51

71

32

61

88

74 86

32 31 34 32 37 39 39 30

39 37 33 34 32

49

64 51

61

30

54

78

45

83

- 10 20 30 40 50 60 70 80 90

100

US CA UK DE FR IT ES NL CH AT SE NO DK PL RU IL TR UA BR MX AU CN

% of smartphone shoppers who are aged 18-34yrs old % of online shoppers who are aged 18-34yrs old

Age histogram: % of shoppers who are aged 18-34yrs old

Multi-country average*: 59% of smartphone shoppers are aged between 18-34yrs old vs 44% of total online shoppers

Smartphone shopper is someone who has used a smartphone to purchase online in the past 12 months. Online shopper is someone who has bought online in the past 12 months via any device. *Multi-country average not weighted by country size. Note: Israel and UAE data is 18-30yrs.

Note on interpretation: 53% of smartphone shoppers in the US are aged 18-34yrs

* *

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Incidence of shopping via an app is higher than via a browser on smartphones in most countries.

16

North America

Western Europe

Nordics Central, Eastern Europe

Middle East Latin America

Asia Pacific

72

55

68 61 58

68 69

49 56 53 50

58 47

63 55

67 65 59 58

73 64

84

54 52 48 46 42 44 56 53 52 52

61 53 51

58 53 58 52 52 54 56 55 50

0 10 20 30 40 50 60 70 80 90

US CA UK DE FR IT ES NL CH AT SE NO DK PL RU IL TR UA BR MX AU CN

Shopped via app % shopped via app and/or browser on smartphone in past 12 months

Multi-country average*: 64% have shopped via an app vs 52% via a browser

Q39a/b. Thinking again about shopping online using your mobile device, which of the following ways have you made a purchase in the past 12 months? Base: Those who have shopped on smartphone in past 12 months. Multi-country average not weighted by country size. Multiple answers mean %s add to more than 100%.

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 17

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 18

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

“PayPal is Finally Becoming a Mobile Payments Company”

Link to article in qz.com: http://bit.ly/1GnpVo2

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

There’s no such thing as mobile payments.

20

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Don’t Fix what’s not Broken.

21

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

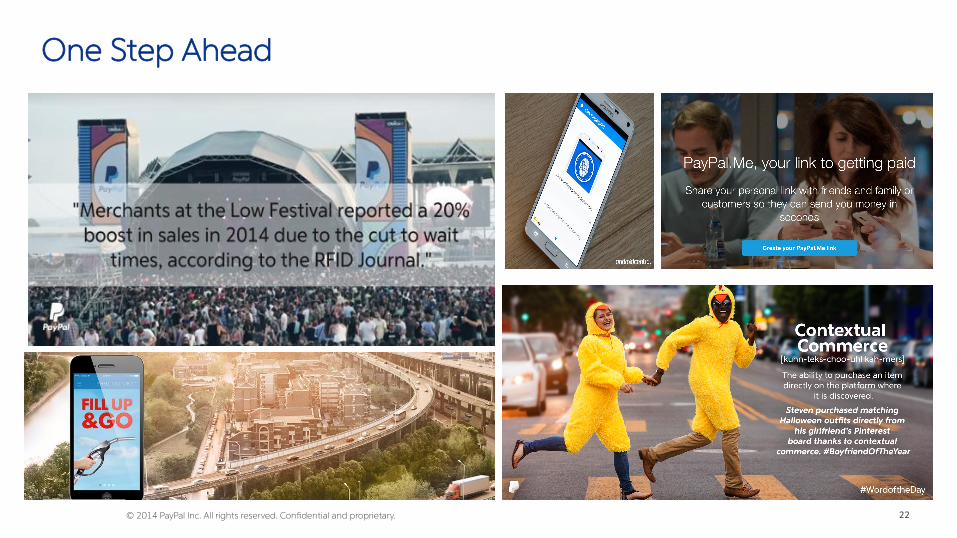

One Step Ahead

22

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Fill Up & Go

23

Diesel or Unleaded? Dry & Warm

in your car

The precise Amount

Faster Process

In control

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

PayPal.Me Pay with your personal url Paypal.me/jogoyvaerts

24

Also for Buffalos

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

How to be Bolt/D? Become Mobile First

25

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 26

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 27

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 28

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Monetize

29

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Remove all friction on payment

30

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Is this your Mobile Payment Conversion today?

31

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Authenticate Back-End Confirm

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Fix Now Your Mobile Payment Conversion

32

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Authenticate Back-End Confirm

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 33

A B C Authenticate

Who are you?

Back-End

Can I trust you?

Confirmation

Do you buy?

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 34

A Authenticate

Though way: 2 factor

Easy: email pswd

Authenticate in Mobile

1x Sign Up Customer chooses

Sharing Biometrics

Am

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 35

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 36

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 37

Back-End

Realtime Risk modelling

B Bm

Back-End

Location based Device based

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 38

C Cm

Confirmation

Personalise Concrete &complete

Confirmation

Embedded

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 39

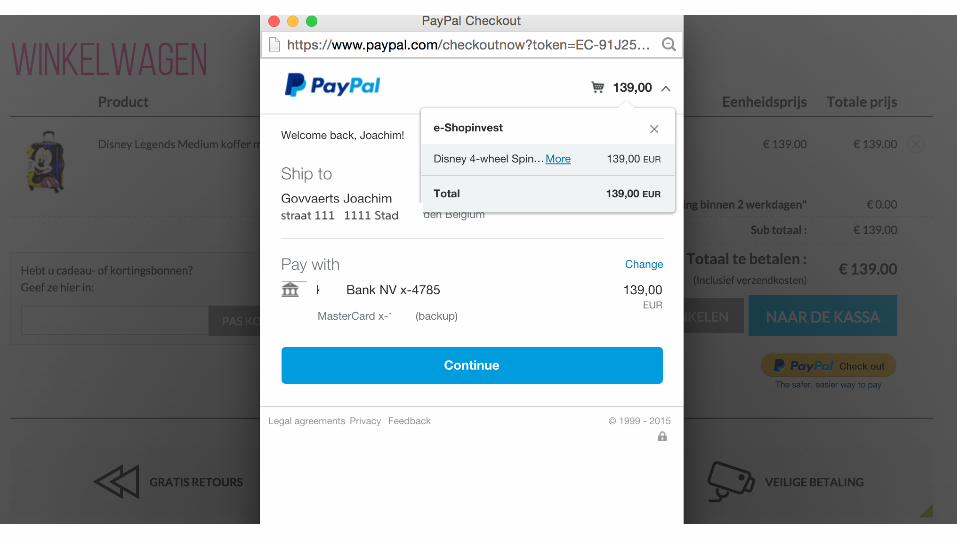

straat 111 1111 Stad

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 40

straat 111 1111 Stad

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 41

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 42

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

"You’re going down the highway, and it’s a bit foggy. You’ve got to keep your eyes on the road and your hand on the steering wheel. You can only see so far ahead. If you keep solving interesting problems, you get somewhere you didn’t expect.”

43

Travis Kalanick http://www.fastcompany.com/3050250/what-makes-uber-run

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary.

Act of Paying is gone. There’s only Shopping Experience.

44

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 45

© 2015 PayPal Inc. All rights reserved. Confidential and proprietary.

One Touch across web and mobile web raises the bar.

46

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 47

Go for Gold in 2016

Short Simple Focus

Fun

© 2014 PayPal Inc. All rights reserved. Confidential and proprietary. 48

Joachim Goyvaerts Head of BeLux [email protected] @jogoyvaerts