www.ovum.com

© Copyright Ovum 2014. All rights reserved.

Mobile Payments: Trends to Watch

Eden Zoller, Principal Analyst, Ovum Consumer Practice

December 2015

2© Copyright Ovum 2014. All rights reserved.

Agenda

Technology

Services

The Consumer Perspective

3© Copyright Ovum 2014. All rights reserved.

Technology trends

NFC & the impact of HCE

Biometrics

Bluetooth Low Energy/beacons

The role of wearables in m-commerce

4© Copyright Ovum 2014. All rights reserved.

The NFC story so far: slow progress in most markets

Big push by operators and GSMA, while all major OEMs ship smartphone models that are NFC enabled

Device availability no longer a show stopper -according to the GSMA around 225 phone models are NFC enabled

But outside of a few markets this has not amounted to mass market adoption by consumers or merchants, or significant revenues for service providers

The majority of NFC services are trials, at an early stage and small scale. Of the 150 launches noted by the GSMA only 60 are commercial services

Opposing views over where the secure service element should reside

As much about control over service provisioning, the customer relationship

and business models as it is NFC security architecture

Articulation of the NFC mobile payments proposition to consumers is not

compelling

This resulted in low consumer awareness, adoption and usage of NFC, which

in turn affects merchant willingness to invest in NFC

Has created a classic “chicken and egg” scenario

5© Copyright Ovum 2014. All rights reserved.

But this could be about to change: the impact of HCE

Solutions based on Host Card Emulation (HCE) could give NFC a much needed boost

HCE is a technology built into the device operating system that enables NFC

transactions without the use of a Secure Element (SE) on the device, in preference for

a virtual SE in the cloud. This is a more flexible model for NFC that makes service

provisioning much easier for issuers, developers and other third parties.

Endorsed by Google, Samsung Visa, MasterCard plus a host of platform suppliers

(Gemalto, Sequent) and developers

Layering on tokenization and biometrics provides additional security

HCE has the potential to open up the NFC market to more innovation and competition

But a disruptive for operators as it displaces the SIM centric model they favour

And HCE does not change consumers’ lack of enthusiasm for NFC payments

6© Copyright Ovum 2014. All rights reserved.

Biometrics - a good user experience above and

beyond their ability to add security

Biometrics, including fingerprint and eye scanning and voice

and photo identification, provide a good level of security, but

not necessarily more than a six-digit or dynamic password

The illusion of added security is more important than the

security that biometrics actually bring

Biometrics prove highly challenging in cases of identity theft

There may also be some reluctance from consumers over

privacy concerns

However, biometrics can enhance the payments authorization

process, which can occur via a simple tap, glance, or word.

They can help create new payment experiences while

reducing the risk of forgotten PINs and passwords.

7© Copyright Ovum 2014. All rights reserved.

The role of Bluetooth Low Energy (BLE) beacons

BLE beacons are an appealing solution for m-commerce

Can enable hyper location applications such as geo-fencing

A low power, low cost solution (Estimote sells three beacons @ $99)

that can be set up quickly and easily

Embraced by various players but notably PayPal (PayPal Beacon) and

Apple (iBeacon)

Merchants are actively experimenting

But despite the hype, BLE beacons are not perfect

A device must have its Bluetooth radio turned on; applications must be

configured to support BLE beacons, while users have to download the

beacon application and opt-in to accept beacon notifications

Privacy issues are heightened

Because BLE/beacon solutions require applications, they are arguably

a better solution for larger retailers/brands that already have a popular

application

8© Copyright Ovum 2014. All rights reserved.

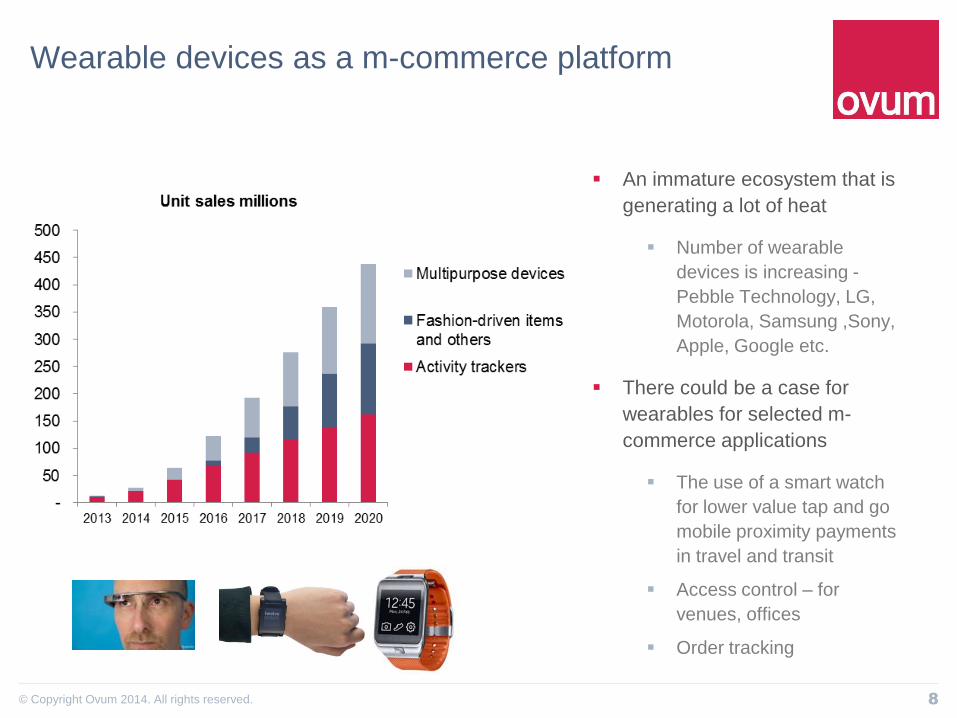

Wearable devices as a m-commerce platform

An immature ecosystem that is

generating a lot of heat

Number of wearable

devices is increasing -

Pebble Technology, LG,

Motorola, Samsung ,Sony,

Apple, Google etc.

There could be a case for

wearables for selected m-

commerce applications

The use of a smart watch

for lower value tap and go

mobile proximity payments

in travel and transit

Access control – for

venues, offices

Order tracking

9© Copyright Ovum 2014. All rights reserved.

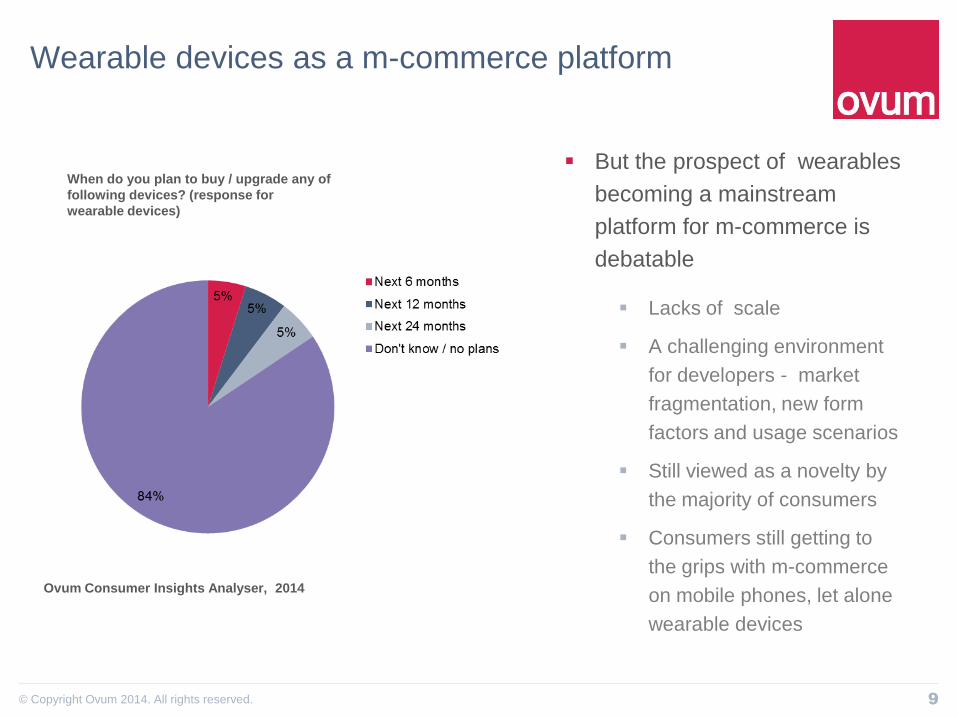

Wearable devices as a m-commerce platform

When do you plan to buy / upgrade any of

following devices? (response for

wearable devices)

Ovum Consumer Insights Analyser, 2014

But the prospect of wearables

becoming a mainstream

platform for m-commerce is

debatable

Lacks of scale

A challenging environment

for developers - market

fragmentation, new form

factors and usage scenarios

Still viewed as a novelty by

the majority of consumers

Consumers still getting to

the grips with m-commerce

on mobile phones, let alone

wearable devices

10© Copyright Ovum 2014. All rights reserved.

Services

The digital wallet application mix

The role of m-loyalty & rewards

P2P transfers

From location to contextual commerce

The prospects for social commerce

The Apple effect

11© Copyright Ovum 2014. All rights reserved.

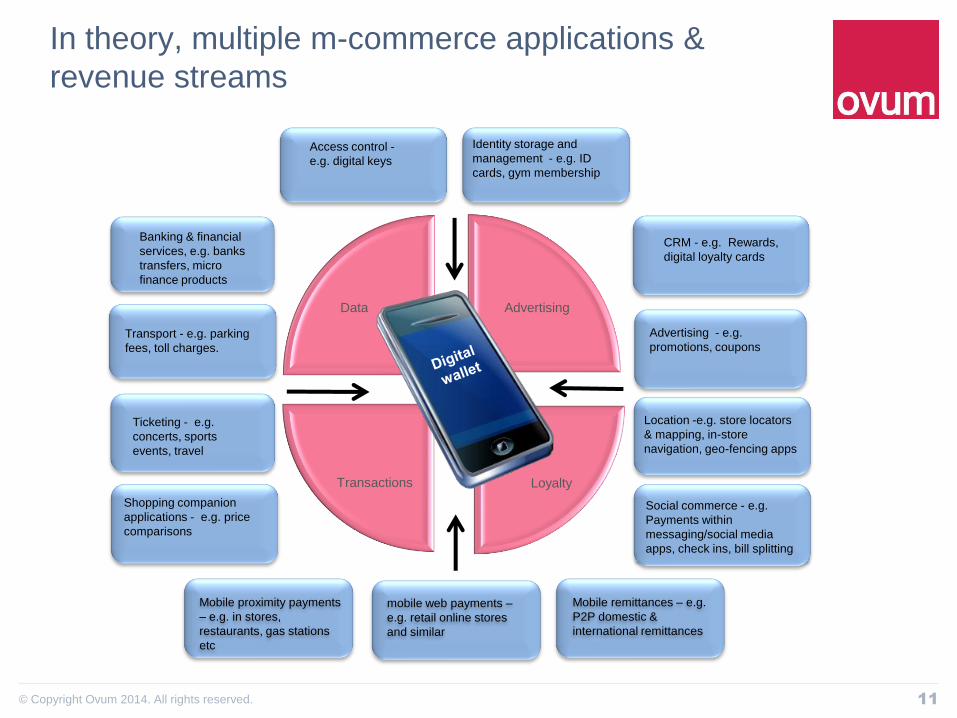

In theory, multiple m-commerce applications &

revenue streams

AdvertisingData

Transactions Loyalty

Mobile proximity payments

– e.g. in stores,

restaurants, gas stations

etc

Location -e.g. store locators

& mapping, in-store

navigation, geo-fencing apps

Ticketing - e.g.

concerts, sports

events, travel

Advertising - e.g.

promotions, coupons

Banking & financial

services, e.g. banks

transfers, micro

finance products

Transport - e.g. parking

fees, toll charges.

Identity storage and

management - e.g. ID

cards, gym membership

Access control -

e.g. digital keys

CRM - e.g. Rewards,

digital loyalty cards

Shopping companion

applications - e.g. price

comparisons

Social commerce - e.g.

Payments within

messaging/social media

apps, check ins, bill splitting

Mobile remittances – e.g.

P2P domestic &

international remittances

mobile web payments –

e.g. retail online stores

and similar

12© Copyright Ovum 2014. All rights reserved.

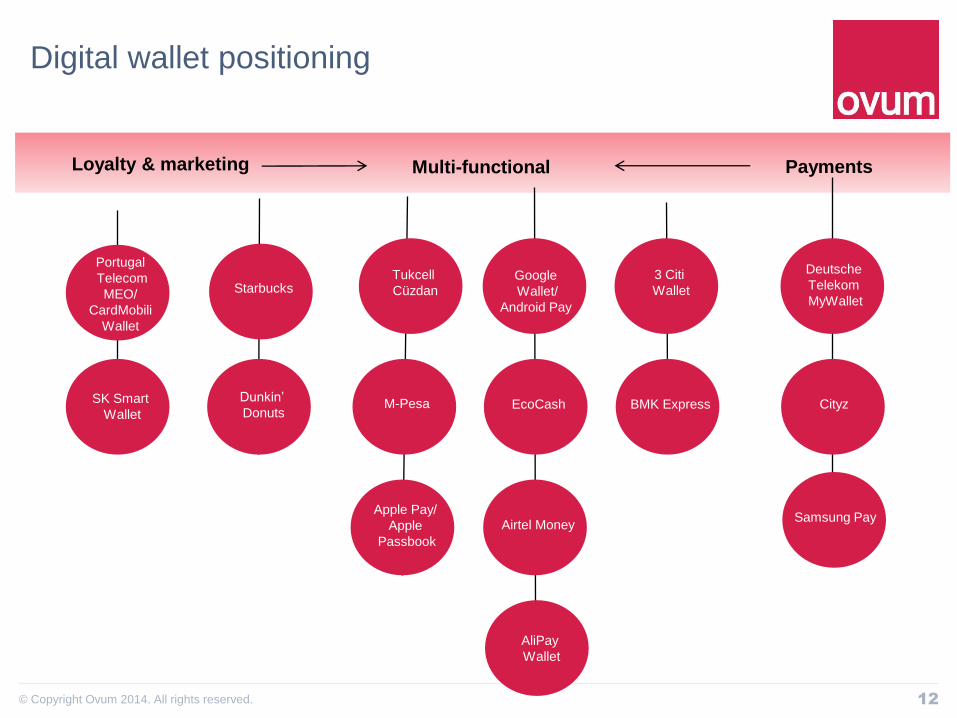

Digital wallet positioning

Starbucks

Cityz

Tukcell

Cüzdan

Dunkin’

Donuts

AliPay

Wallet

SK Smart

Wallet

Apple Pay/

Apple

Passbook

M-Pesa

Portugal

Telecom

MEO/

CardMobili

Wallet

Deutsche

Telekom

MyWallet

3 Citi

WalletGoogle

Wallet/

Android Pay

Loyalty & marketing PaymentsMulti-functional

EcoCash

Airtel MoneySamsung Pay

BMK Express

13© Copyright Ovum 2014. All rights reserved.

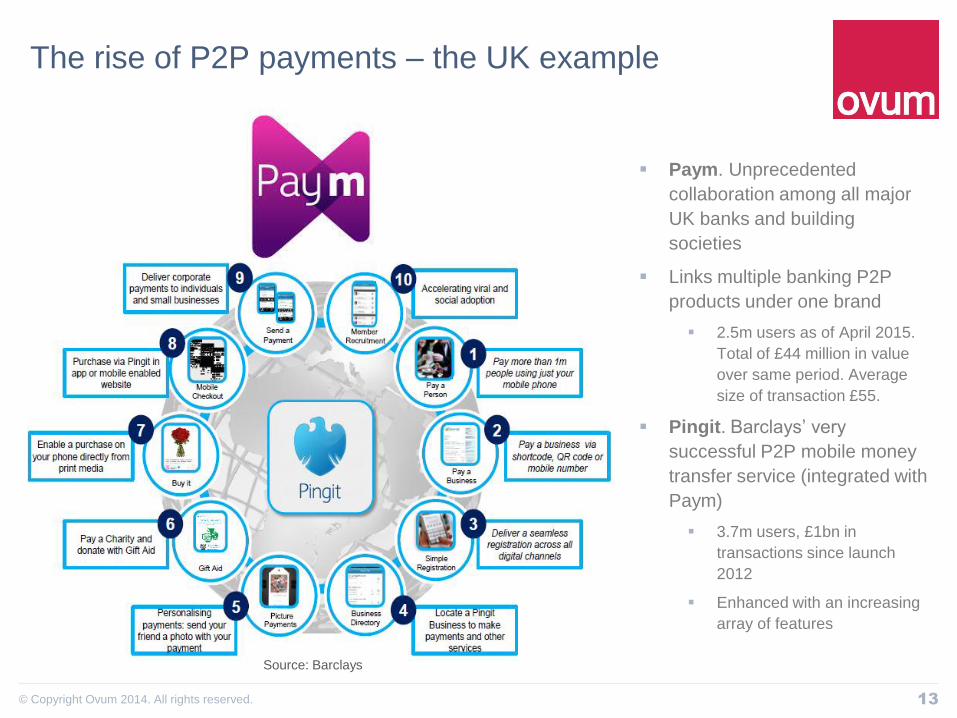

The rise of P2P payments – the UK example

Paym. Unprecedented

collaboration among all major

UK banks and building

societies

Links multiple banking P2P

products under one brand

2.5m users as of April 2015.

Total of £44 million in value

over same period. Average

size of transaction £55.

Pingit. Barclays’ very

successful P2P mobile money

transfer service (integrated with

Paym)

3.7m users, £1bn in

transactions since launch

2012

Enhanced with an increasing

array of features

Source: Barclays

14© Copyright Ovum 2014. All rights reserved.

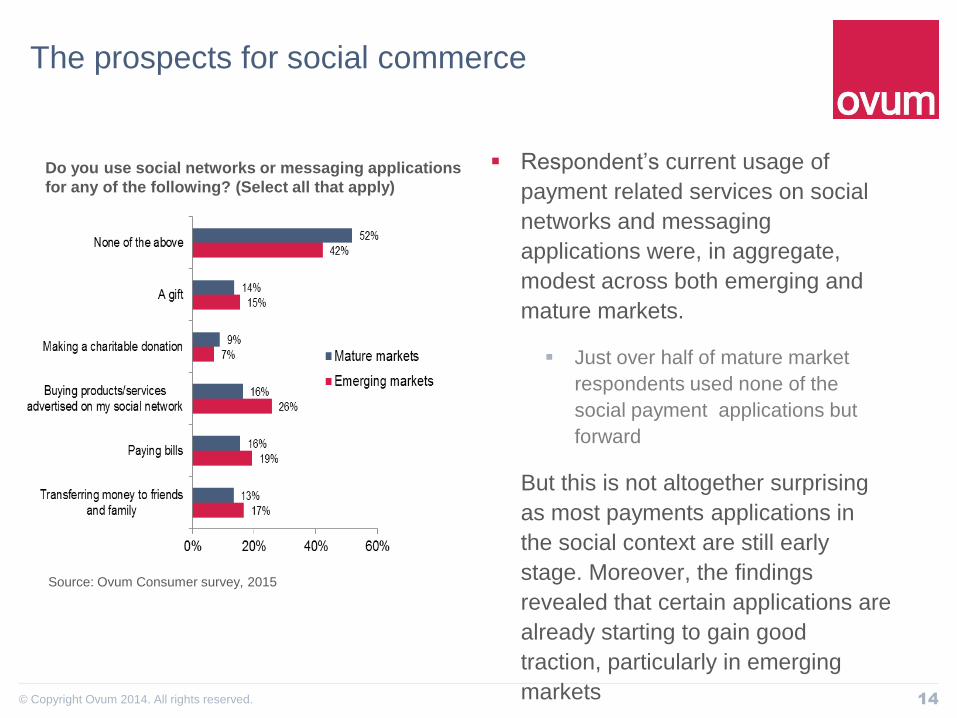

The prospects for social commerce

Respondent’s current usage of

payment related services on social

networks and messaging

applications were, in aggregate,

modest across both emerging and

mature markets.

Just over half of mature market

respondents used none of the

social payment applications but

forward

But this is not altogether surprising

as most payments applications in

the social context are still early

stage. Moreover, the findings

revealed that certain applications are

already starting to gain good

traction, particularly in emerging

markets

Do you use social networks or messaging applications

for any of the following? (Select all that apply)

Source: Ovum Consumer survey, 2015

15© Copyright Ovum 2014. All rights reserved.

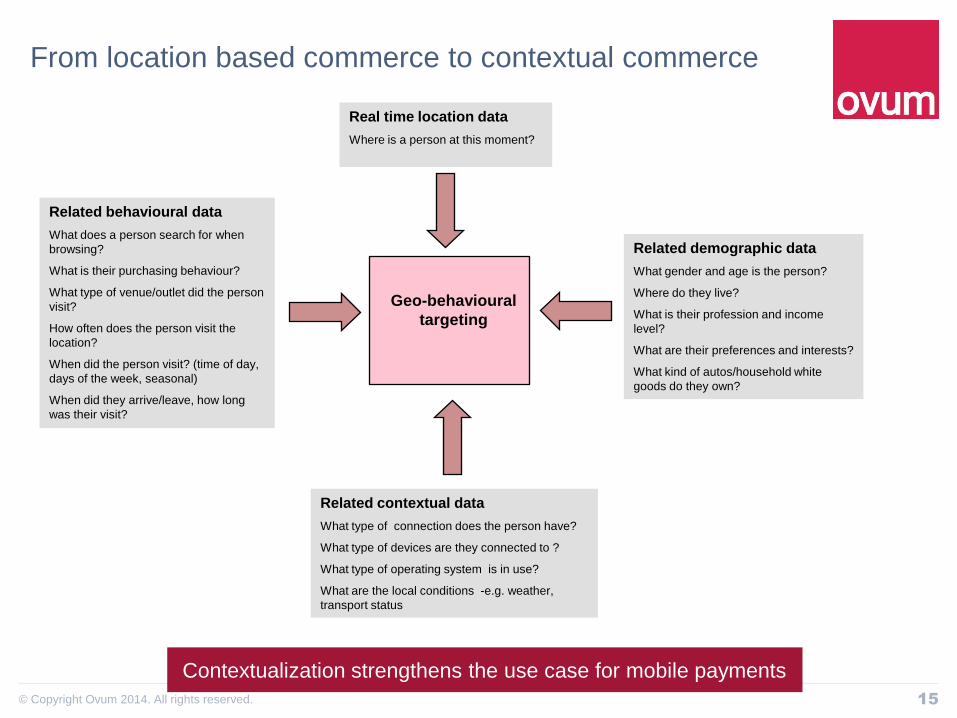

From location based commerce to contextual commerce

Related behavioural data

What does a person search for when

browsing?

What is their purchasing behaviour?

What type of venue/outlet did the person

visit?

How often does the person visit the

location?

When did the person visit? (time of day,

days of the week, seasonal)

When did they arrive/leave, how long

was their visit?

Real time location data

Where is a person at this moment?

Related demographic data

What gender and age is the person?

Where do they live?

What is their profession and income

level?

What are their preferences and interests?

What kind of autos/household white

goods do they own?

Geo-behavioural

targeting

Related contextual data

What type of connection does the person have?

What type of devices are they connected to ?

What type of operating system is in use?

What are the local conditions -e.g. weather,

transport status

Contextualization strengthens the use case for mobile payments

16© Copyright Ovum 2014. All rights reserved.

The Apple effect

Apple’s ultimate goal is to take a central role in the payments/digital wallet

ecosystem. It has a well thought through, compelling proposition to drive

this:

Wide support from banks and retailers: over 100 banks and more than

700,000 retail locations

Device based SE gives Apple maximum control

Supports both NFC proximity and remote m-payments – P2P coming

soon

Apple Pay + Passbook = a more fully articulated digital wallet

Harness the location marketing capabilities of iBeacon

Draw on the mobile advertising capabilities of the iAd platform

Quick to open Apple Pay API to developers

High profile retail outlets to promote Apple Pay, educate consumers

Riding the existing payment rails – aiming to get financial institutions on

side

Will prove effective at marketing m-payments, particularly NFC

Emphasis on security and data privacy - biometrics, tokenization,

embedded SE

Transaction data generated by Apple Pay remains with the merchant and

banks

17© Copyright Ovum 2014. All rights reserved.

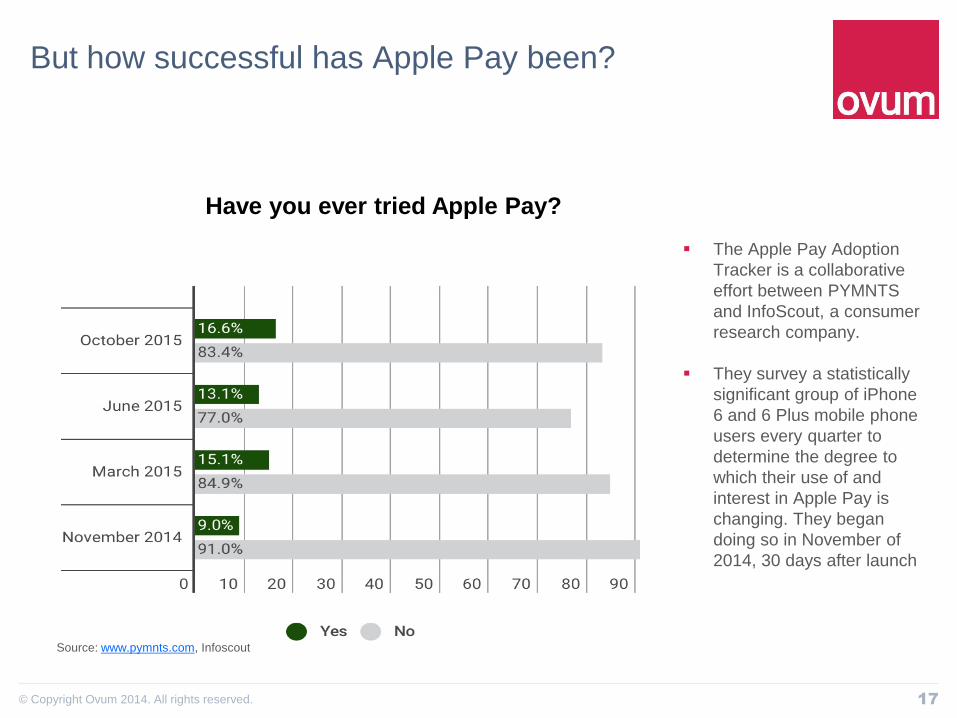

But how successful has Apple Pay been?

Have you ever tried Apple Pay?

Source: www.pymnts.com, Infoscout

The Apple Pay Adoption

Tracker is a collaborative

effort between PYMNTS

and InfoScout, a consumer

research company.

They survey a statistically

significant group of iPhone

6 and 6 Plus mobile phone

users every quarter to

determine the degree to

which their use of and

interest in Apple Pay is

changing. They began

doing so in November of

2014, 30 days after launch

18© Copyright Ovum 2014. All rights reserved.

The consumer perspective

Selected findings and insights from a new Ovum

bespoke consumer m-commerce survey (2015)

19© Copyright Ovum 2014. All rights reserved.

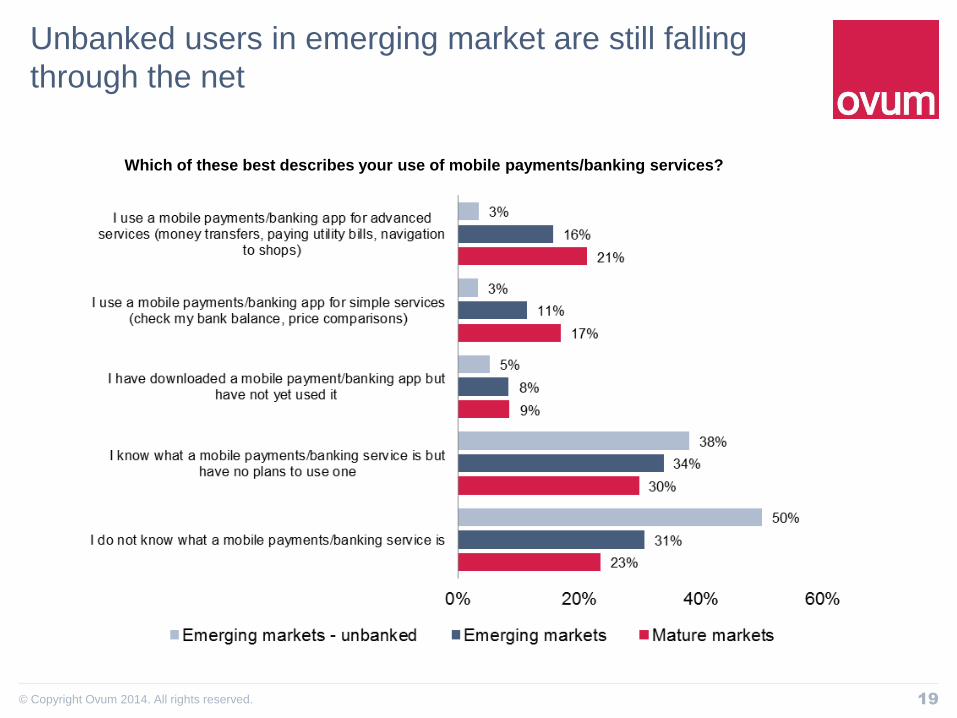

Unbanked users in emerging market are still falling

through the net

Which of these best describes your use of mobile payments/banking services?

20© Copyright Ovum 2014. All rights reserved.

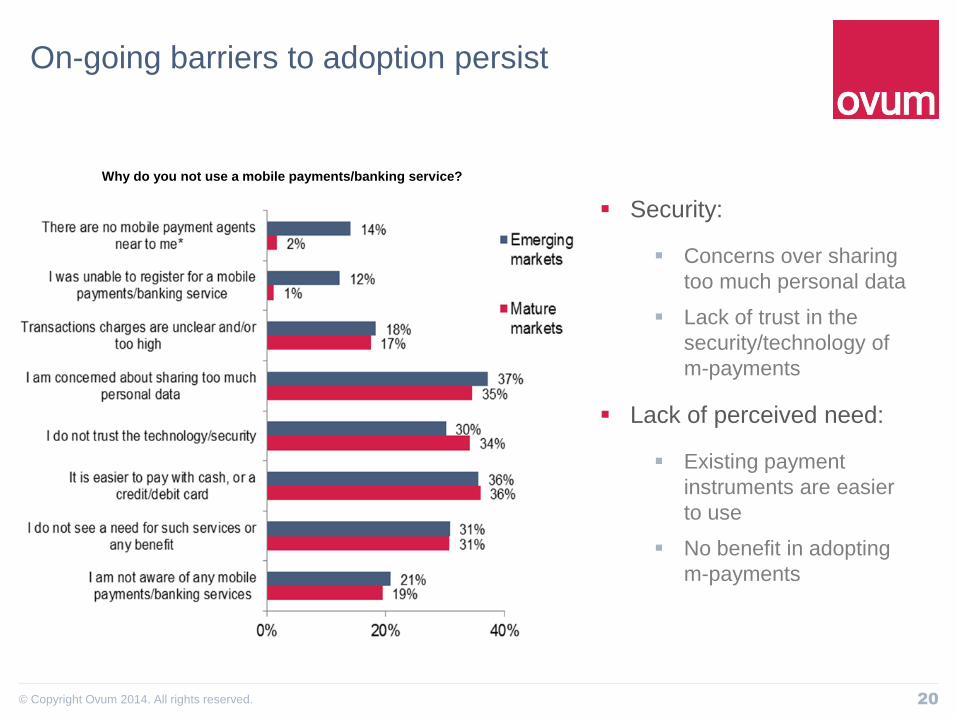

On-going barriers to adoption persist

Why do you not use a mobile payments/banking service?

Security:

Concerns over sharing

too much personal data

Lack of trust in the

security/technology of

m-payments

Lack of perceived need:

Existing payment

instruments are easier

to use

No benefit in adopting

m-payments

21© Copyright Ovum 2014. All rights reserved.

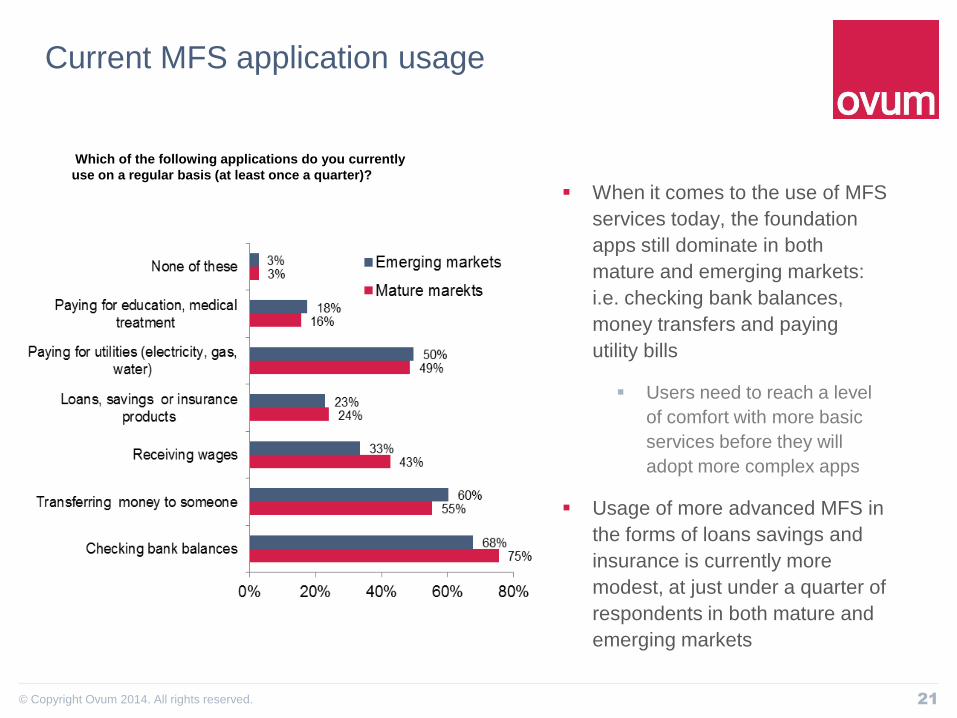

Current MFS application usage

When it comes to the use of MFS

services today, the foundation

apps still dominate in both

mature and emerging markets:

i.e. checking bank balances,

money transfers and paying

utility bills

Users need to reach a level

of comfort with more basic

services before they will

adopt more complex apps

Usage of more advanced MFS in

the forms of loans savings and

insurance is currently more

modest, at just under a quarter of

respondents in both mature and

emerging markets

Which of the following applications do you currently

use on a regular basis (at least once a quarter)?

22© Copyright Ovum 2014. All rights reserved.

Anticipated change in MFS usage levels

Emerging markets will see the strongest increase in the usage of MFS over the next 12 months.

This is encouraging, and confirms that active users in emerging markets have strong appetite for mobile FS applications.

But in mature markets the majority of users (59%) expect current usage to remain unchanged, while just over a third anticipating increased usage.

Service providers need to stimulate the former user group as otherwise there is a risk that usage will stagnate.

Over the next 12 months will your use of the applications you

selected (in previous question) change?

23© Copyright Ovum 2014. All rights reserved.

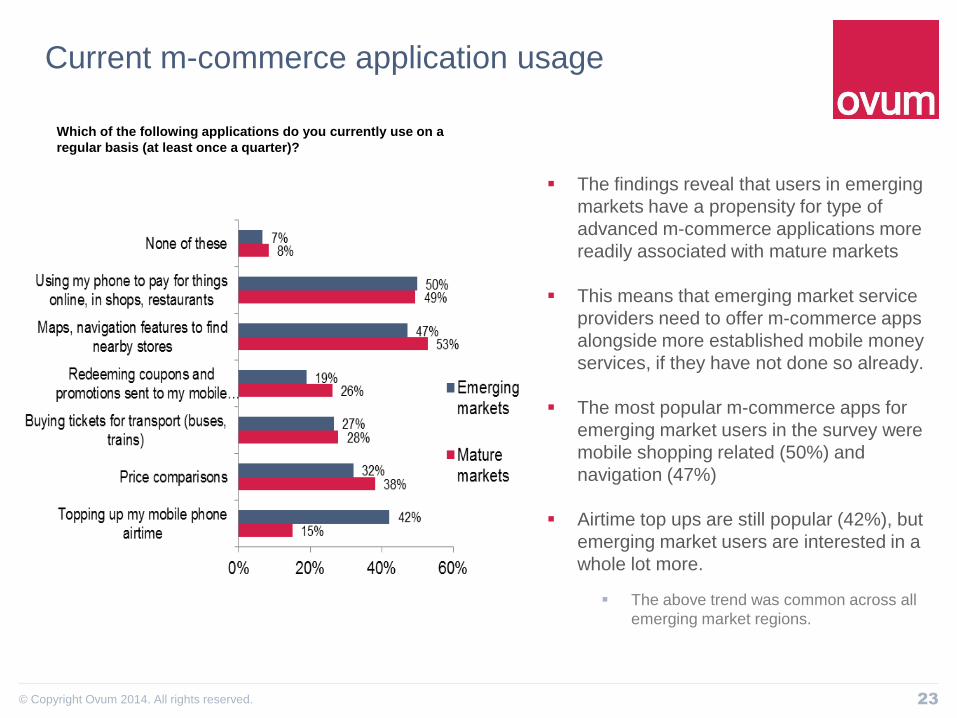

Current m-commerce application usage

Which of the following applications do you currently use on a

regular basis (at least once a quarter)?

The findings reveal that users in emerging

markets have a propensity for type of

advanced m-commerce applications more

readily associated with mature markets

This means that emerging market service

providers need to offer m-commerce apps

alongside more established mobile money

services, if they have not done so already.

The most popular m-commerce apps for

emerging market users in the survey were

mobile shopping related (50%) and

navigation (47%)

Airtime top ups are still popular (42%), but

emerging market users are interested in a

whole lot more.

The above trend was common across all

emerging market regions.

24© Copyright Ovum 2014. All rights reserved.

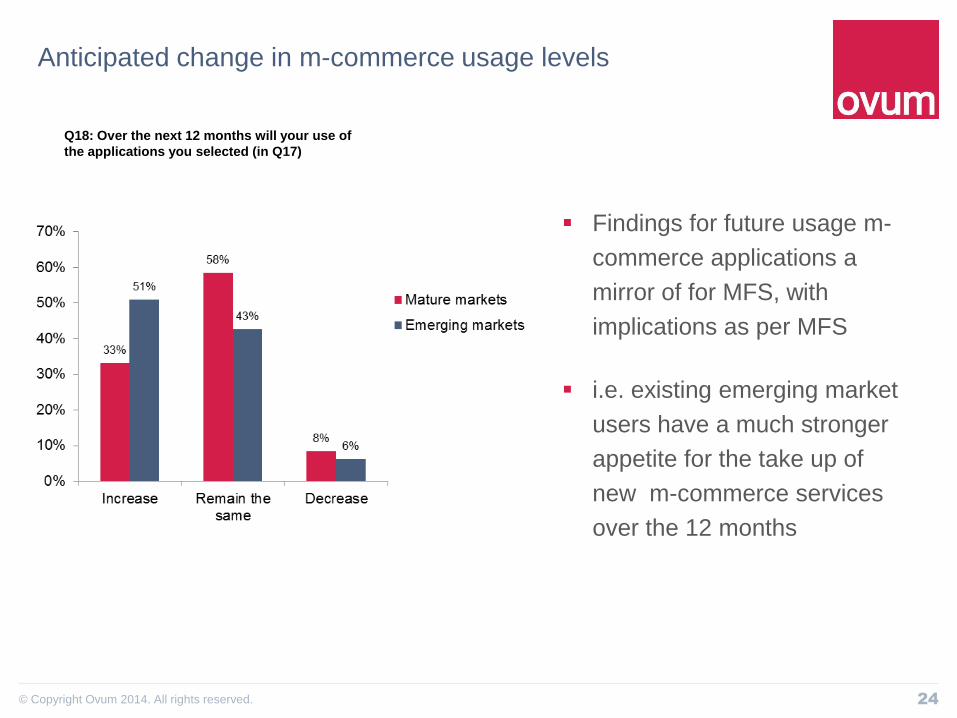

Anticipated change in m-commerce usage levels

Findings for future usage m-

commerce applications a

mirror of for MFS, with

implications as per MFS

i.e. existing emerging market

users have a much stronger

appetite for the take up of

new m-commerce services

over the 12 months

Q18: Over the next 12 months will your use of

the applications you selected (in Q17)

25© Copyright Ovum 2014. All rights reserved.

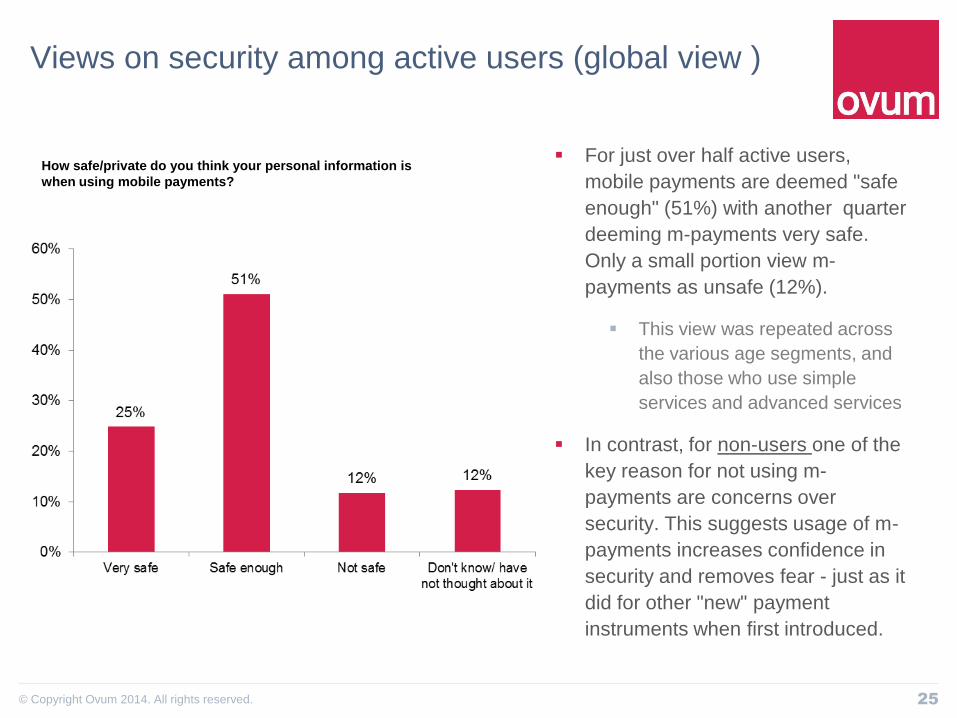

Views on security among active users (global view )

For just over half active users,

mobile payments are deemed "safe

enough" (51%) with another quarter

deeming m-payments very safe.

Only a small portion view m-

payments as unsafe (12%).

This view was repeated across

the various age segments, and

also those who use simple

services and advanced services

In contrast, for non-users one of the

key reason for not using m-

payments are concerns over

security. This suggests usage of m-

payments increases confidence in

security and removes fear - just as it

did for other "new" payment

instruments when first introduced.

How safe/private do you think your personal information is

when using mobile payments?

26© Copyright Ovum 2014. All rights reserved.

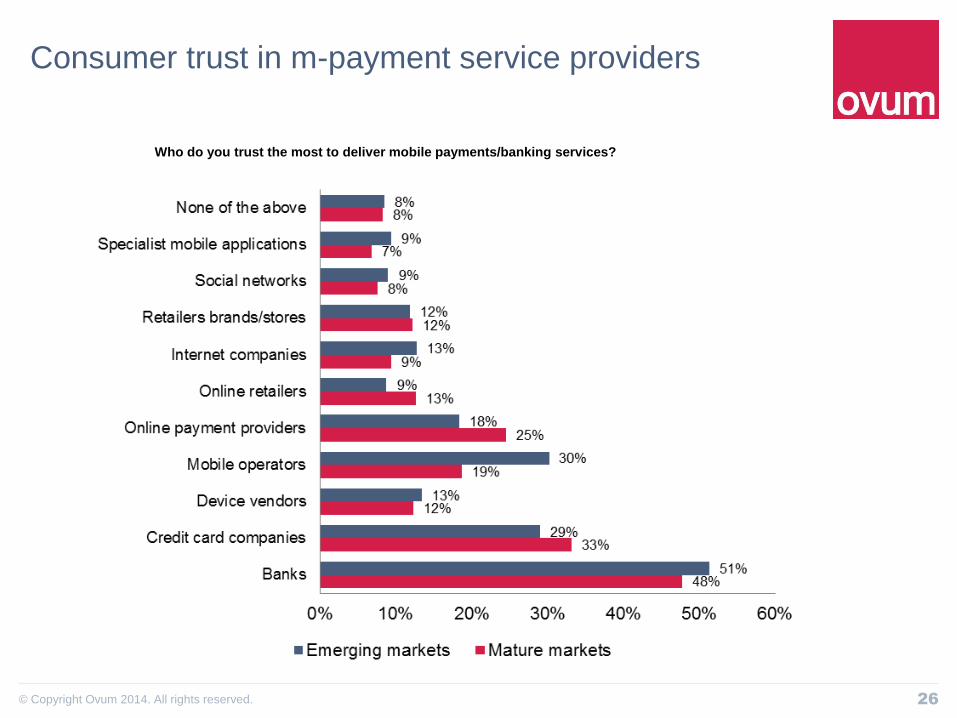

Consumer trust in m-payment service providers

Who do you trust the most to deliver mobile payments/banking services?

27© Copyright Ovum 2014. All rights reserved.

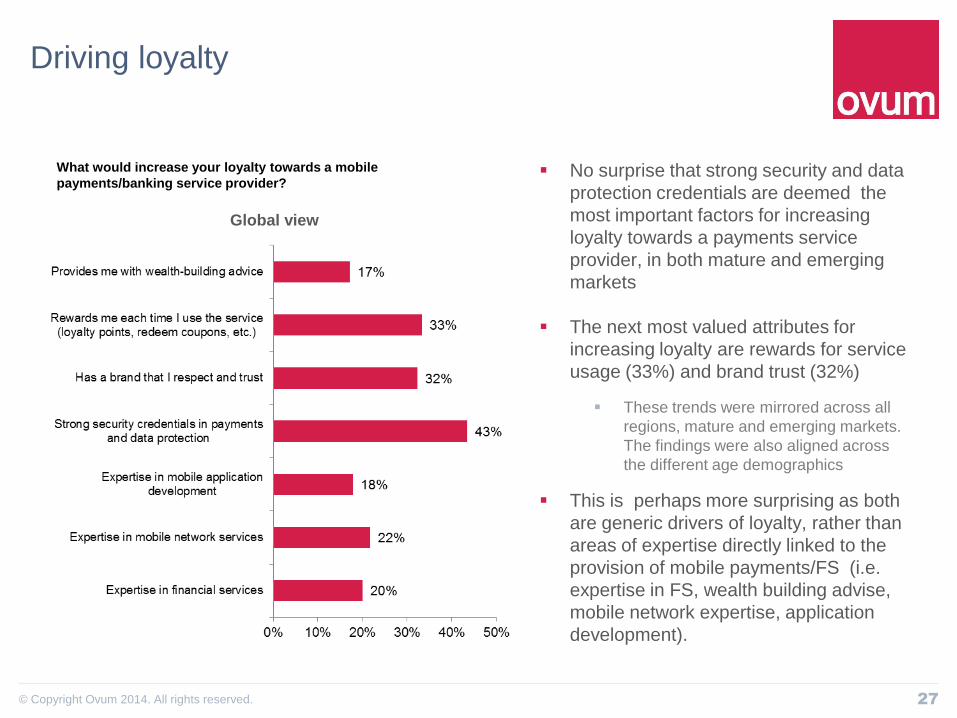

Driving loyalty

No surprise that strong security and data

protection credentials are deemed the

most important factors for increasing

loyalty towards a payments service

provider, in both mature and emerging

markets

The next most valued attributes for

increasing loyalty are rewards for service

usage (33%) and brand trust (32%)

These trends were mirrored across all

regions, mature and emerging markets.

The findings were also aligned across

the different age demographics

This is perhaps more surprising as both

are generic drivers of loyalty, rather than

areas of expertise directly linked to the

provision of mobile payments/FS (i.e.

expertise in FS, wealth building advise,

mobile network expertise, application

development).

What would increase your loyalty towards a mobile

payments/banking service provider?

Global view

28© Copyright Ovum 2014. All rights reserved.

Thank-you