1

Mobilising video

advertising: trends, challenges

and opportunities

April 2016

2 3

Contents

Introduction 5

1. Video advertising going mobile 6

a. Differentapproachestoonlinevideo 6b. Digitalismoreandmoremobile 7c. Cost:thebarriertoadaptingTVspots 8

2. Planning for cross-screen 10

a. Pushingbackthepointofdiminishingreturns 10b. Followingtheconsumerthroughouttheday 12c. Adaptingdistribution,creativeandformatformobile 12

3. Adapting video formats to mobile 13

a. Intrusiveformatsdriveadblocking 13b. Nativevideoadsarebettertolerated 14c. Gettinguptospeed 15d. Controliscrucial 16e. Opt-invideoseesgreaterROI 16

4. Mobile as a compass to reset the creative standards 17

a. Challenge 1: Soundon/off 18b. Challenge 2: Goingvertical 19c. Challenge 3: Frombigtosmallscreen 20d. Challenge 4: Timematters 21

5. New opportunities to reach, engage and drive to store 22

a. Opportunity 1: Moreengagingmessages 24b. Opportunity 2: Newchannelsforlivestreaming 25c. Opportunity 3: Second-screening&mobilefirst 26d. Opportunity 4: Drivetostore 27

6. Creating for mobile video 30

a. Whyitmatters:Thetengoldenrulesofmobilenativevideoadvertising 30

Mobileisalsoeverywherewithmorethanhalfoftheglobalpopulationowningasmartphoneortabletanddevelopingadeeplypersonablerelationshipwiththeirdevices.

Asaconsequence,mobileisexpectedtobethemaindriverofglobaladspendgrowthandwillcontributeafull83% of the extra adspend between 2014 and 2017accordingtoZenithOptimediaforecasts.

AtTeads,webelievethatmobileisnotjustanotherscreentobeaddedtothevideostack.Asusersaremoreaversetoadvertisingonmobileandmoresensitivetointrusiveness,theindustryneedstoadaptvideoadformatsandcreativestomobiledevices.Thismeansreducingthelengthofthevideos.TheUSleadstheway,with50%ofcampaignsplannedwithamobileversionoftheadinmind.Ifthisshiftinthinkingdoesn'thappen,weriskspeedinguptheadoptionofad-blockers,missingtheopportunitytomakebrands’messagesresonatewiththeiraudience.

Onmobile,usersareinaparticularstateofmindthatdifferstothatofwatchingTVorworkingonadesktop.Mobile is flexible; it’s adaptable, it satisfies a curious appetite–beitimmediateaccesstoentertainment,shoppingorfriends.

Thedayisfragmentedinhundredsofmicro-momentsthateachbringwiththemanewneedandanewopportunityforbrandstodeliverrelevantandengagingmessages.

Ascontentandcontextplayanimportantpartintheraceforuserattention,itcomesasnosurprisethatnative advertising formats are experiencing such stellar growth.Integratedinthefeedofthecontent,theyareverywelladaptedtomobileconsumption,beingviewablebydefaultbutnotforcedupontheuser.

BasedonTeads’videodistributionexpertise,thiswhite-paperlooksintothetrends,challengesandopportunitiesofferedbynativemobilevideoadvertising.

4 5

Mobile is

everything

wasthemottoofthisyear’sMobileWorldCongress.

6 7

Global Media Spend

2014

83062

2017

1729

55

Daily Screen Share (%) Mins(Video&otherwebbrowsing)

MOBILE COMPUTER TV

2015

52

2127

1Video advertising going mobile

Videoadvertisingisrapidlygrowingonaglobalscale,withadspendforecasttodoublefrom2015to2017.However,itrepresentslessthan10%ofTVadspend,withanapproachthatpushesTVspotsintothevideostreamstilldominatingdigitalvideoadvertising.Withusersandbudgetsshiftingtomobile,brandsareslowlystartingtoadapt.

a. Different approaches to online videoSincevideoisdistributedonline,twoadvertisingapproachesco-exist.

ThetraditionalTVapproachisaclear“push”marketingtechnique,withcontentforced-exposed to users in a bid to pass a TV ad in a video stream.Ontheotherhand,theriseofdigitalvideoandmobiledevicessawthedevelopmentofa“pull”approach:users are given the option to watch apromotionalvideoandcancontrolwhethertoskip,scrollpastorsimplycloseit.ComparedtoTV,videoadvertisingcanalsobedistributedinallcontentstreams,notonlyinvideo,forinstancewithinanarticleorinsocialfeeds.

b. Digital is more and more mobile

Onaverage,peopleviewatotalof3.5 hours of video a day,withhalfofvideoswatchedondigitalscreens.Twothirdsofonlinevideoconsumptionisoccuringonmobile.

Asaconsequence,mobile media spend should double from 2014 to 2017accordingtoZenithOptimedia.

Thedigitalapproach,relyingonbrandsproducingvideocontentfordigitalplatformstocreateuserengagement,hasevolvedsince2010andisshifting towards mobile-centric platformslikeFacebookandothermobile,nativevideoapplicationslikeInstagram,TwitterorSnapchat.

Atthe2015SuperBowl,thereweremoresharesofBigGameadsoccuringonFacebookthanYouTube.Todaythereare8billionvideosvieweddailyonthesocialplatform.

Twitterhasalsowitnesseda150-foldyear-on-yearincreaseinvideoviewsasofSeptember2015,withtweets containing video seeing 6 times more retweets than those only containing images.

Theseplatformscreatenewopportunitiesforbrandstoreachouttotheiraudienceusingvideo formats that are specific to each distribution channel in terms of duration, size, and placement.

Thisfragmentationandtheflexibilityofthedigitalvideolandscapemakesitmorechallengingtoplancontentcreationanddistributionaccordingly.

Source:MillwardBrownAdReactionStudy,November2015

PULLUSERContent

Engagement

BRANDMedia

PUSH

Visibility

Viral video

2010 2015

Skippablepre-roll Click-to-play

Social video

Auto-play

Digital centric

• Pre-rolladoncatchupTV

• TVadshort form

• Pre-rollad(skippableornot)

• TVadshort andlongform

TVcentric

OUTSTREAM FORMAT

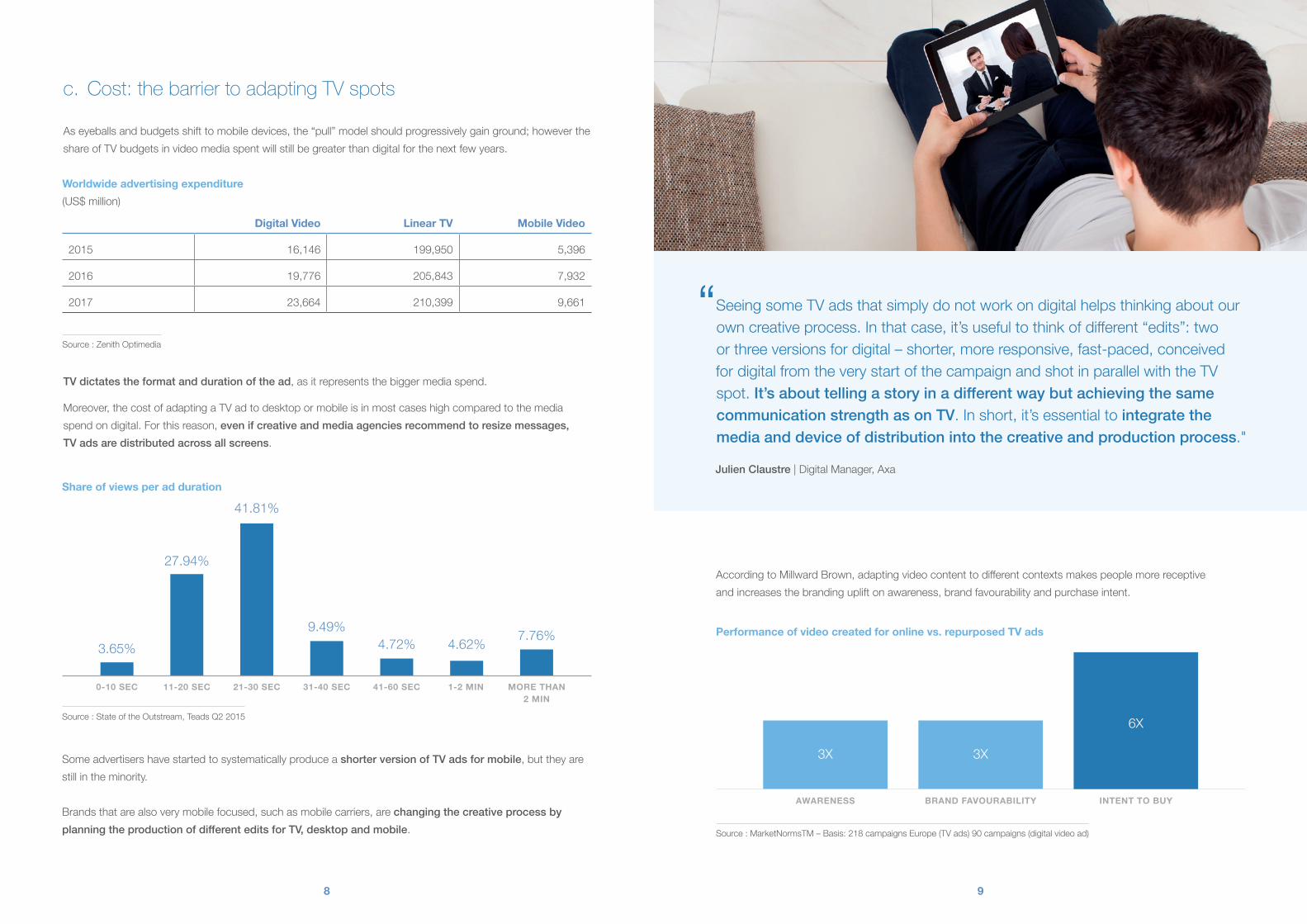

c. Cost: the barrier to adapting TV spots

Aseyeballsandbudgetsshifttomobiledevices,the“pull”modelshouldprogressivelygainground;howevertheshareofTVbudgetsinvideomediaspentwillstillbegreaterthandigitalforthenextfewyears.

TV dictates the format and duration of the ad,asitrepresentsthebiggermediaspend.

Moreover,thecostofadaptingaTVadtodesktopormobileisinmostcaseshighcomparedtothemediaspendondigital.Forthisreason,even if creative and media agencies recommend to resize messages, TV ads are distributed across all screens.

8 9

Worldwide advertising expenditure(US$million)

Digital Video Linear TV Mobile Video

2015 16,146 199,950 5,396

2016 19,776 205,843 7,932

2017 23,664 210,399 9,661

Source:ZenithOptimedia

Someadvertisershavestartedtosystematicallyproduceashorter version of TV ads for mobile,buttheyarestillintheminority.

Brandsthatarealsoverymobilefocused,suchasmobilecarriers,arechanging the creative process by planning the production of different edits for TV, desktop and mobile.

Share of views per ad duration

3.65%

0-10 SEC

27.94%

11-20 SEC

41.81%

21-30 SEC

9.49%

31-40 SEC

4.72%

41-60 SEC

4.62%

1-2 MIN

7.76%

MORE THAN 2 MIN

Source:StateoftheOutstream,TeadsQ22015

SeeingsomeTVadsthatsimplydonotworkondigitalhelpsthinkingaboutourowncreativeprocess.Inthatcase,it’susefultothinkofdifferent“edits”:twoorthreeversionsfordigital–shorter,moreresponsive,fast-paced,conceivedfordigitalfromtheverystartofthecampaignandshotinparallelwiththeTVspot.It’s about telling a story in a different way but achieving the same communication strength as on TV.Inshort,it’sessentialtointegrate the media and device of distribution into the creative and production process."

Julien Claustre|DigitalManager,Axa

AccordingtoMillwardBrown,adaptingvideocontenttodifferentcontextsmakespeoplemorereceptive andincreasesthebrandingupliftonawareness,brandfavourabilityandpurchaseintent.

Performance of video created for online vs. repurposed TV ads

Source:MarketNormsTM–Basis:218campaignsEurope(TVads)90campaigns(digitalvideoad)

3X

AWARENESS

3X

BRAND FAVOURABILITY INTENT TO BUY

6X

10 11

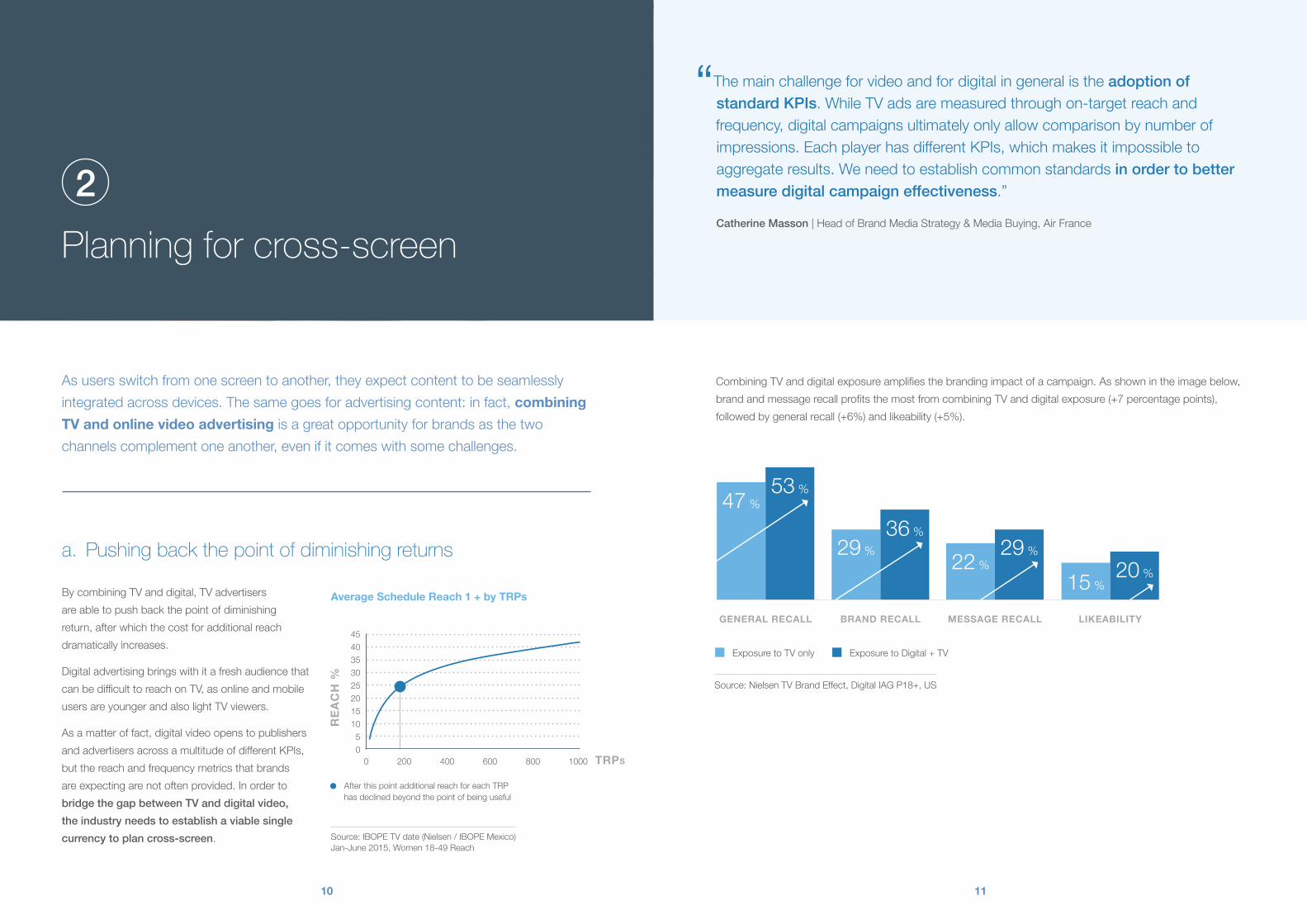

Source:IBOPETVdate(Nielsen/IBOPEMexico) Jan-June2015,Women18-49Reach

454035302520151050

REA

CH

%

TRPS0 200 400 600 800 1000

Average Schedule Reach 1 + by TRPs

AfterthispointadditionalreachforeachTRPhasdeclinedbeyondthepointofbeinguseful

Source:NielsenTVBrandEffect,DigitalIAGP18+,US

ExposuretoTVonly ExposuretoDigital+TV

47%53%

29%36%

22%29%

15%20%

GENERAL RECALL BRAND RECALL MESSAGE RECALL LIKEABILITY

Asusersswitchfromonescreentoanother,theyexpectcontenttobeseamlesslyintegratedacrossdevices.Thesamegoesforadvertisingcontent:infact,combining TV and online video advertisingisagreatopportunityforbrandsasthetwochannelscomplementoneanother,evenifitcomeswithsomechallenges.

CombiningTVanddigitalexposureamplifiesthebrandingimpactofacampaign.Asshownintheimagebelow,brandandmessagerecallprofitsthemostfromcombiningTVanddigitalexposure(+7percentagepoints),followedbygeneralrecall(+6%)andlikeability(+5%).

2Planning for cross-screen

a. Pushing back the point of diminishing returns

BycombiningTVanddigital,TVadvertisersareabletopushbackthepointofdiminishingreturn,afterwhichthecostforadditionalreachdramaticallyincreases.

DigitaladvertisingbringswithitafreshaudiencethatcanbedifficulttoreachonTV,asonlineandmobileusersareyoungerandalsolightTVviewers.

Asamatteroffact,digitalvideoopenstopublishersandadvertisersacrossamultitudeofdifferentKPIs,butthereachandfrequencymetricsthatbrandsareexpectingarenotoftenprovided.Inordertobridge the gap between TV and digital video, the industry needs to establish a viable single currency to plan cross-screen.

Themainchallengeforvideoandfordigitalingeneralistheadoption of standard KPIs.WhileTVadsaremeasuredthroughon-targetreachandfrequency,digitalcampaignsultimatelyonlyallowcomparisonbynumberofimpressions.EachplayerhasdifferentKPIs,whichmakesitimpossibletoaggregateresults.Weneedtoestablishcommonstandards in order to better measure digital campaign effectiveness.”

Catherine Masson|HeadofBrandMediaStrategy&MediaBuying,AirFrance

13

3Adapting video formats to mobile

b. Following the consumer throughout the day

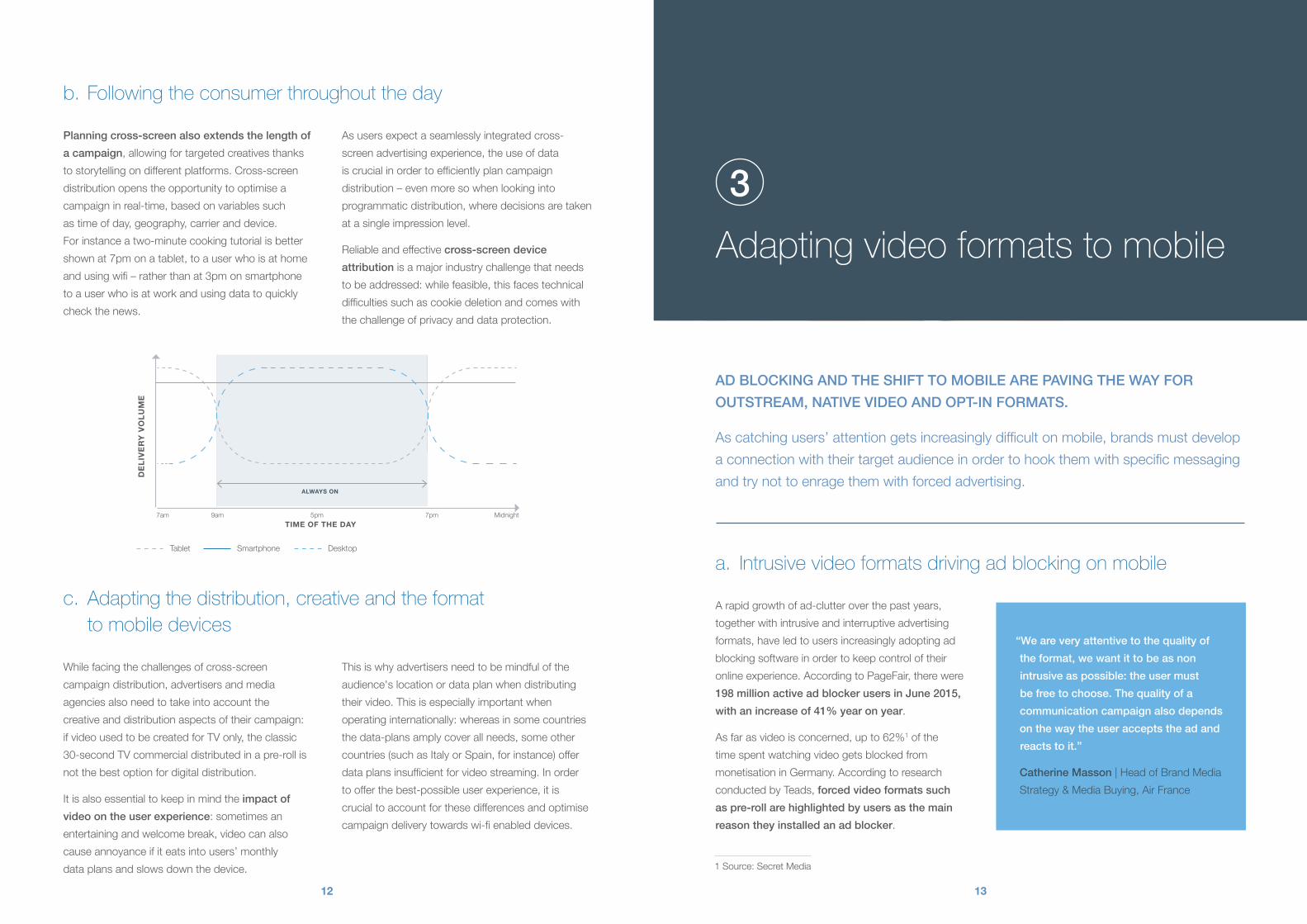

Planning cross-screen also extends the length of a campaign,allowingfortargetedcreativesthankstostorytellingondifferentplatforms.Cross-screendistributionopenstheopportunitytooptimiseacampaigninreal-time,basedonvariablessuchastimeofday,geography,carrieranddevice.Forinstanceatwo-minutecookingtutorialisbettershownat7pmonatablet,toauserwhoisathomeandusingwifi–ratherthanat3pmonsmartphonetoauserwhoisatworkandusingdatatoquicklycheckthenews.

Asusersexpectaseamlesslyintegratedcross-screenadvertisingexperience,theuseofdataiscrucialinordertoefficientlyplancampaigndistribution–evenmoresowhenlookingintoprogrammaticdistribution,wheredecisionsaretakenatasingleimpressionlevel.

Reliableandeffectivecross-screen device attributionisamajorindustrychallengethatneedstobeaddressed:whilefeasible,thisfacestechnicaldifficultiessuchascookiedeletionandcomeswiththechallengeofprivacyanddataprotection.

c. Adapting the distribution, creative and the format

to mobile devices

Whilefacingthechallengesofcross-screencampaigndistribution,advertisersandmediaagenciesalsoneedtotakeintoaccountthecreativeanddistributionaspectsoftheircampaign:ifvideousedtobecreatedforTVonly,theclassic30-secondTVcommercialdistributedinapre-rollisnotthebestoptionfordigitaldistribution.

Itisalsoessentialtokeepinmindtheimpact of video on the user experience:sometimesanentertainingandwelcomebreak,videocanalsocauseannoyanceifiteatsintousers’monthlydataplansandslowsdownthedevice.

Thisiswhyadvertisersneedtobemindfuloftheaudience'slocationordataplanwhendistributingtheirvideo.Thisisespeciallyimportantwhenoperatinginternationally:whereasinsomecountriesthedata-plansamplycoverallneeds,someothercountries(suchasItalyorSpain,forinstance)offerdataplansinsufficientforvideostreaming.Inordertoofferthebest-possibleuserexperience,itiscrucialtoaccountforthesedifferencesandoptimisecampaigndeliverytowardswi-fienableddevices.

12

DEL

IVER

Y VO

LUM

E

TIME OF THE DAY7am 9am 5pm 7pm Midnight

ALWAYS ON

SmartphoneTablet Desktop

AD BLOCKING AND THE SHIFT TO MOBILE ARE PAVING THE WAY FOR OUTSTREAM, NATIVE VIDEO AND OPT-IN FORMATS.

Ascatchingusers’attentiongetsincreasinglydifficultonmobile,brandsmustdevelopaconnectionwiththeirtargetaudienceinordertohookthemwithspecificmessagingandtrynottoenragethemwithforcedadvertising.

a. Intrusive video formats driving ad blocking on mobile

Arapidgrowthofad-clutteroverthepastyears,togetherwithintrusiveandinterruptiveadvertisingformats,haveledtousersincreasinglyadoptingadblockingsoftwareinordertokeepcontroloftheironlineexperience.AccordingtoPageFair,therewere198 million active ad blocker users in June 2015, with an increase of 41% year on year.

Asfarasvideoisconcerned,upto62%1ofthetimespentwatchingvideogetsblockedfrommonetisationinGermany.AccordingtoresearchconductedbyTeads,forced video formats such as pre-roll are highlighted by users as the main reason they installed an ad blocker.

1Source:SecretMedia

“We are very attentive to the quality of the format, we want it to be as non intrusive as possible: the user must be free to choose. The quality of a communication campaign also depends on the way the user accepts the ad and reacts to it.”

Catherine Masson|HeadofBrandMediaStrategy&MediaBuying,AirFrance

14

c. Getting up to speed

Adblockingledtoasubsequentrevenuelossof£22billionforpublishersin2015andrepresentsafurtherbarrierforadvertisersincommunicatingwiththeirtargetaudiences.ItcouldbecomeworsestillifmobileoperatorssuchasThreewentthroughwiththeirplanstoblockadsatanetworklevelduetotheirpartnershipwithIsraeliad-blockercompanyShine.Theyarejustifyingthiscontroversialmovebyarguingthatads,andespeciallyvideoads,consumebandwidthanddamagethequalityofservice.

Tosupportthisposition,thesecondmotivationlistedbyusersforinstallinganadblockeristhatadsslowdownthebrowsingexperience,especiallyonmobile.

Uploadtimeiscriticalastheaveragemobileuserstartsscrollingonawebsitemuchfasterthanondesktop.AccordingtomarketinganalyticscompanyMoat,a mobile user clicks down the page 13 seconds after content begins loading, compared to 24 seconds on desktop,whichgivesadsmoretimetoload.

Inordertoaddressthisproblem,Googlehaslaunchedanindustry-wideinitiativecalledtheAccelerated Mobile Pages (AMP),whichaimstoreducepageuploadtimeby85%comparedtostandardmobilepages.Thisopensourcesolutioncanbeintegrated by publishers and tech platforms such as Teads.Itimpliesthatpublishersgiveupintrusiveformatssuchasinterstitialsorsitetake-overs.

% of people who rank pre-roll as highly intrusive

% of people who rank in-article native video as highly intrusive

57%Argentina 13%

55%Mexico 14%

54%Spain 21%

52%UnitedStates 25%

52%Germany 27%

51%UnitedKingdom 23%

51%Italy 25%

49%France 22%

43%Brazil 21%

Source:TeadsResearch,“ProfileofanAdBlocker”,fieldingbyResearchNow,analysisbyTeads,December2015.Pre-rolladsincludebothskippableandunskippableformats.

15

Nativevideoisanalternativetopre-roll,whichisplacedbeforevideocontent.

It is seamlessly integrated within editorial content, the video being ideally contextually relevant and adding value to the user experience.

Contextiskeywhenitcomestodistribution,asnotonlydoesitallowforanadtobenativelypositioned,thusenablingbettertargetingbasedoninterestsandmind-set.ResearchconductedbyAdblockPlusshowsthat41% of users don’t mind being shown branded content as long as the quality and the user experience match the editorial environment thattheadisplacedin.

Contextalsospeaksforthequalityoftheadasuserstendtoassociatetheeditorialqualityoftheenvironmenttheadisshowninwiththeadvertisingbrand.Thisisparticularlyimportantwhenitcomestofindingpremium,brand-safe environments onmobile.

Thistypeofoutstream video formatsolvesaproblemthatmanypublishersface,whichishavingenoughvideosupplythattheycanmonetise.

Usingoutstreamvideoadvertisingallowspublisherstomonetisetheireditorialcontent,preventingthemfromhavingtoinvestincreatingadditionalvideofootage.Italsoallowsforauser-friendlyexperienceastheconsumercanskipitatanypoint:itdoesn’tinterruptcontentconsumption.

2Source:http://www.adweek.com/news/technology/how-can-marketers-be-certain-their-mobile-ads-are-actually-getting-seen-167748

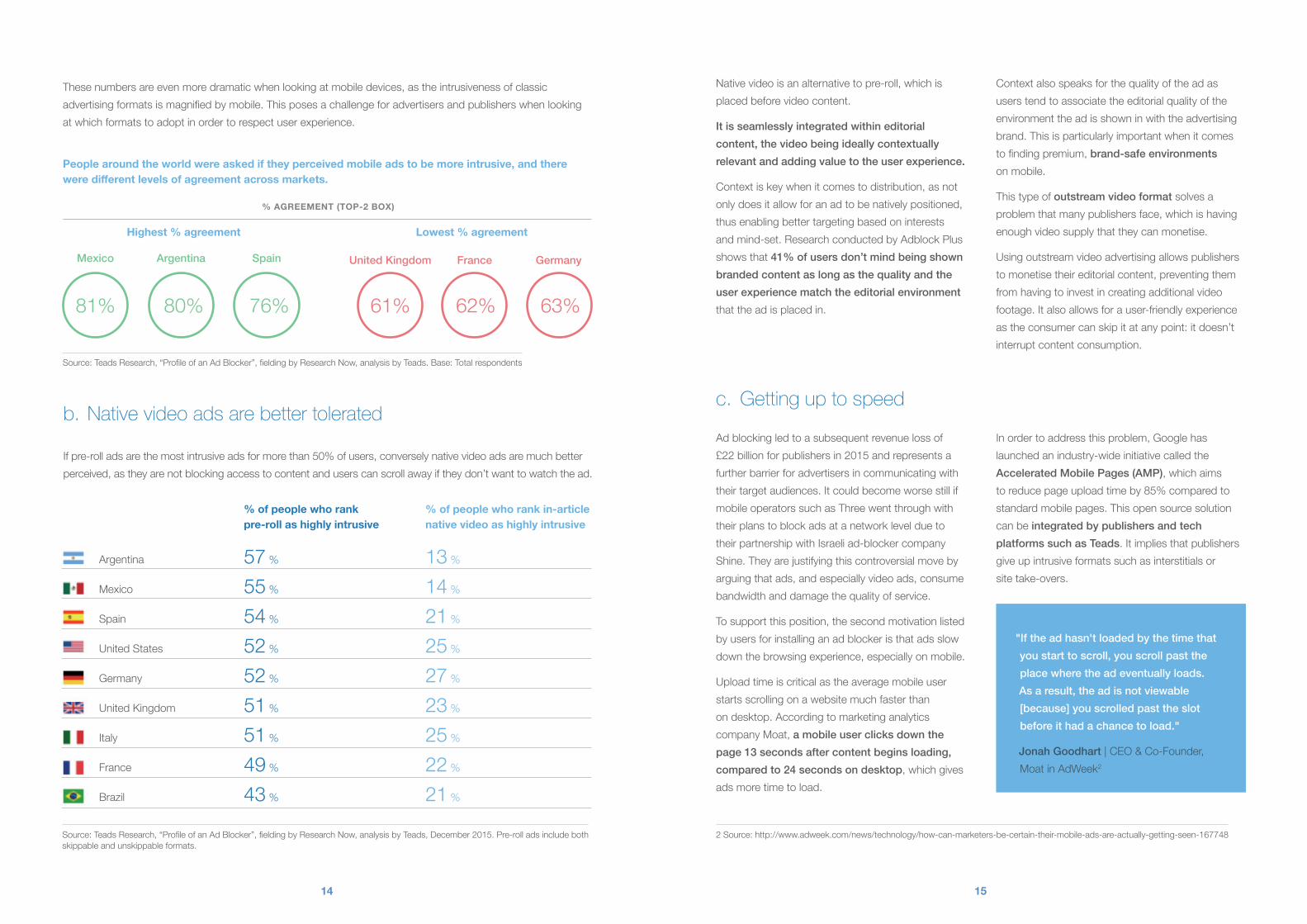

People around the world were asked if they perceived mobile ads to be more intrusive, and there were different levels of agreement across markets.

Thesenumbersareevenmoredramaticwhenlookingatmobiledevices,astheintrusivenessofclassicadvertisingformatsismagnifiedbymobile.Thisposesachallengeforadvertisersandpublisherswhenlookingatwhichformatstoadoptinordertorespectuserexperience.

Highest % agreement

% AGREEMENT (TOP-2 BOX)

Lowest % agreement

Source:TeadsResearch,“ProfileofanAdBlocker”,fieldingbyResearchNow,analysisbyTeads.Base:Totalrespondents

81% 80% 76%

Mexico Argentina Spain

61% 62% 63%

United Kingdom France Germany

b. Native video ads are better tolerated

Ifpre-rolladsarethemostintrusiveadsformorethan50%ofusers,converselynativevideoadsaremuchbetterperceived,astheyarenotblockingaccesstocontentanduserscanscrollawayiftheydon’twanttowatchthead.

"If the ad hasn't loaded by the time that you start to scroll, you scroll past the place where the ad eventually loads. As a result, the ad is not viewable [because] you scrolled past the slot before it had a chance to load."

Jonah Goodhart|CEO&Co-Founder,MoatinAdWeek2

16

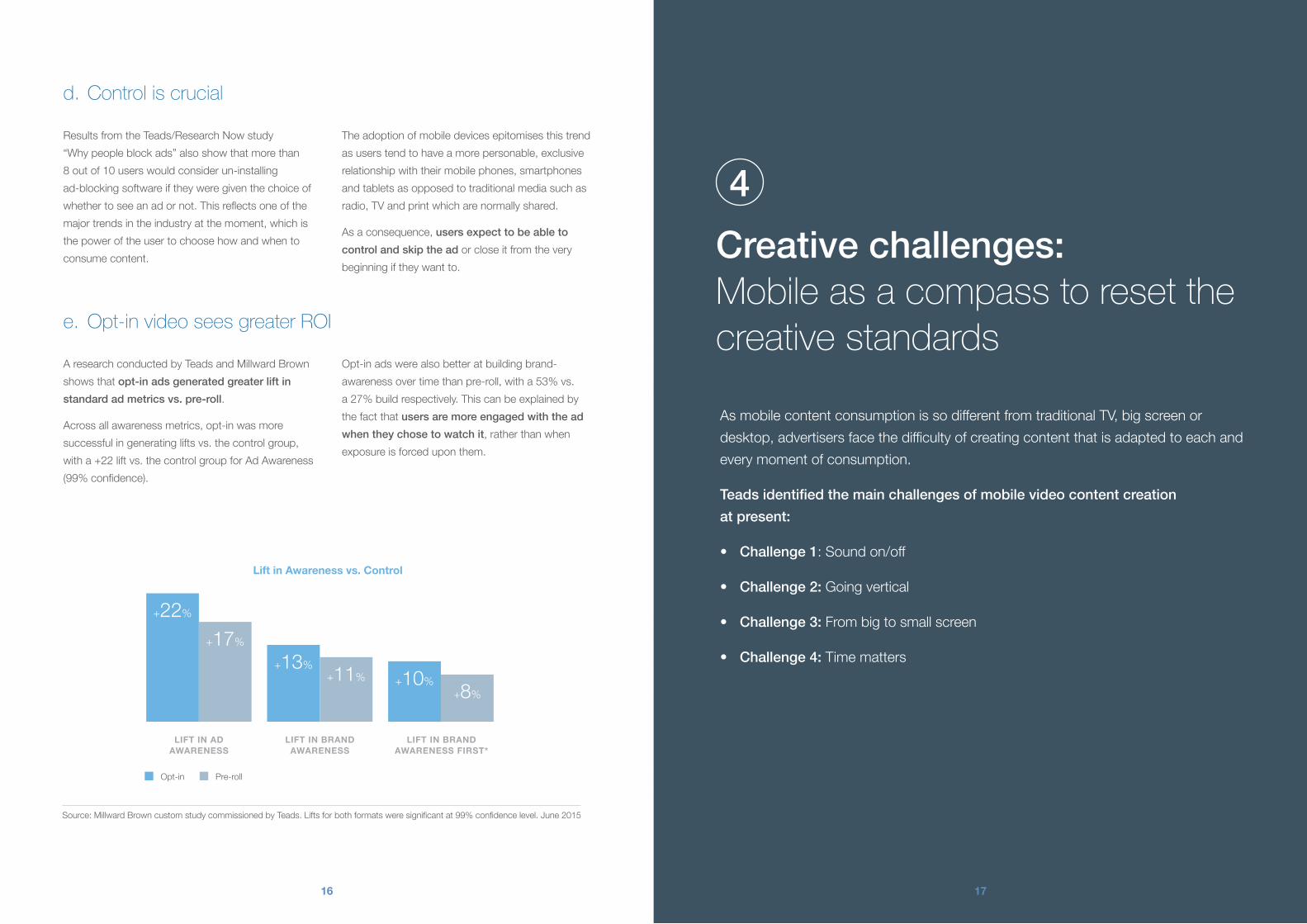

Opt-in Pre-roll

+22%

+17%

+13%+11% +10%

+8%

LIFT IN AD AWARENESS

LIFT IN BRAND AWARENESS

LIFT IN BRAND AWARENESS FIRST*

Lift in Awareness vs. Control

Source:MillwardBrowncustomstudycommissionedbyTeads.Liftsforbothformatsweresignificantat99%confidencelevel.June2015

17

d. Control is crucial

ResultsfromtheTeads/ResearchNowstudy“Whypeopleblockads”alsoshowthatmorethan8outof10userswouldconsiderun-installingad-blockingsoftwareiftheyweregiventhechoiceofwhethertoseeanadornot.Thisreflectsoneofthemajortrendsintheindustryatthemoment,whichisthepoweroftheusertochoosehowandwhentoconsumecontent.

Theadoptionofmobiledevicesepitomisesthistrendasuserstendtohaveamorepersonable,exclusiverelationshipwiththeirmobilephones,smartphonesandtabletsasopposedtotraditionalmediasuchasradio,TVandprintwhicharenormallyshared.

Asaconsequence,users expect to be able to control and skip the adorcloseitfromtheverybeginningiftheywantto.

e. Opt-in video sees greater ROI

AresearchconductedbyTeadsandMillwardBrownshowsthatopt-in ads generated greater lift in standard ad metrics vs. pre-roll.

Acrossallawarenessmetrics,opt-inwasmoresuccessfulingeneratingliftsvs.thecontrolgroup,witha+22liftvs.thecontrolgroupforAdAwareness(99%confidence).

Opt-inadswerealsobetteratbuildingbrand-awarenessovertimethanpre-roll,witha53%vs.a27%buildrespectively.Thiscanbeexplainedbythefactthatusers are more engaged with the ad when they chose to watch it,ratherthanwhenexposureisforceduponthem.

AsmobilecontentconsumptionissodifferentfromtraditionalTV,bigscreenordesktop,advertisersfacethedifficultyofcreatingcontentthatisadaptedtoeachandeverymomentofconsumption.

Teads identified the main challenges of mobile video content creation at present:

• Challenge 1:Soundon/off

• Challenge 2:Goingvertical

• Challenge 3:Frombigtosmallscreen

• Challenge 4: Timematters

4Creative challenges: Mobile as a compass to reset the

creative standards

Challenge1

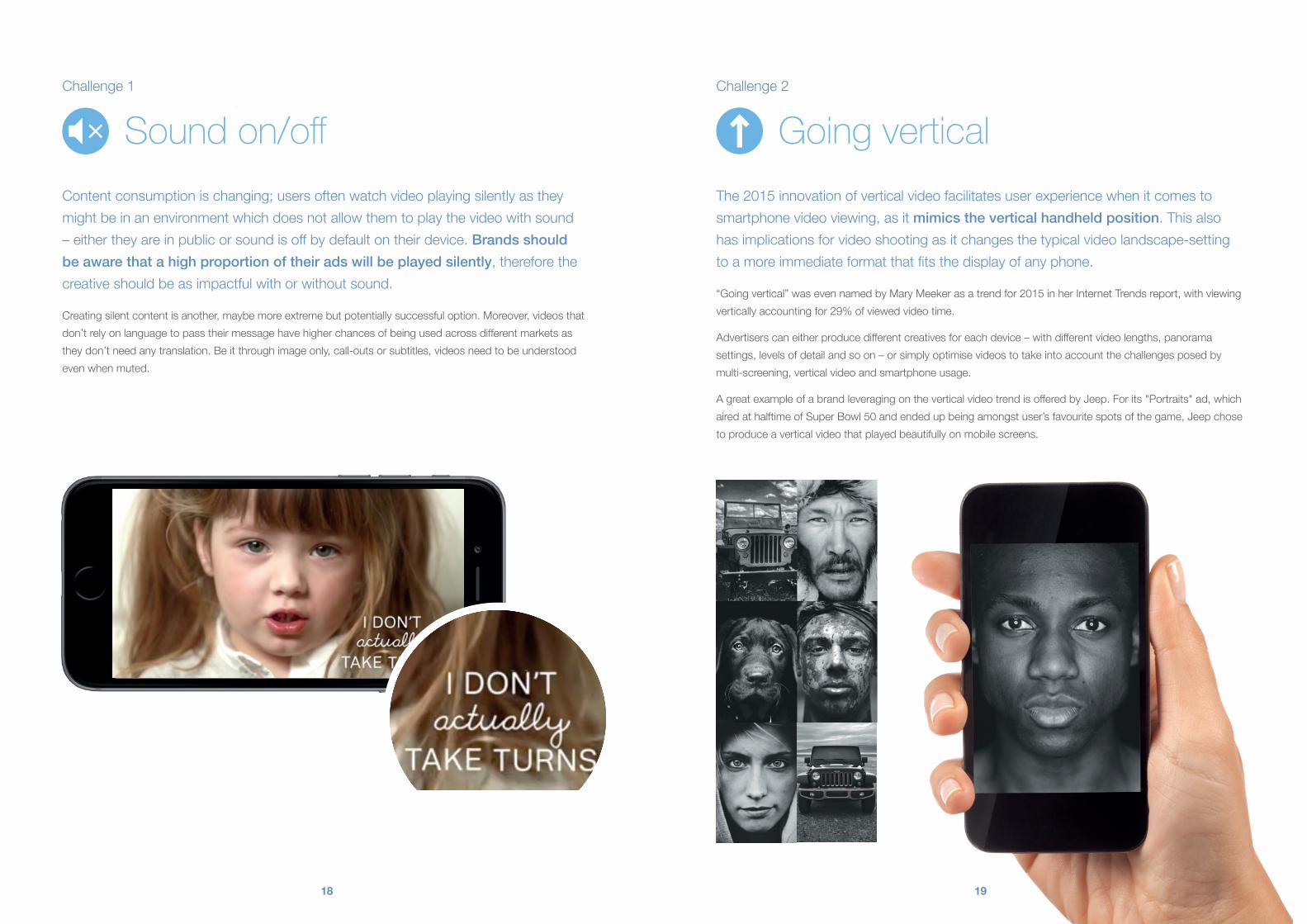

Sound on/offContentconsumptionischanging;usersoftenwatchvideoplayingsilentlyastheymightbeinanenvironmentwhichdoesnotallowthemtoplaythevideowithsound–eithertheyareinpublicorsoundisoffbydefaultontheirdevice.Brands should be aware that a high proportion of their ads will be played silently,thereforethecreativeshouldbeasimpactfulwithorwithoutsound.

Creatingsilentcontentisanother,maybemoreextremebutpotentiallysuccessfuloption.Moreover,videosthatdon’trelyonlanguagetopasstheirmessagehavehigherchancesofbeingusedacrossdifferentmarketsastheydon’tneedanytranslation.Beitthroughimageonly,call-outsorsubtitles,videosneedtobeunderstoodevenwhenmuted.

18 19

Challenge2

Going vertical

The2015innovationofverticalvideofacilitatesuserexperiencewhenitcomestosmartphonevideoviewing,asitmimics the vertical handheld position.Thisalsohasimplicationsforvideoshootingasitchangesthetypicalvideolandscape-settingtoamoreimmediateformatthatfitsthedisplayofanyphone.

“Goingvertical”wasevennamedbyMaryMeekerasatrendfor2015inherInternetTrendsreport,withviewingverticallyaccountingfor29%ofviewedvideotime.

Advertiserscaneitherproducedifferentcreativesforeachdevice–withdifferentvideolengths,panoramasettings,levelsofdetailandsoon–orsimplyoptimisevideostotakeintoaccountthechallengesposedbymulti-screening,verticalvideoandsmartphoneusage.

AgreatexampleofabrandleveragingontheverticalvideotrendisofferedbyJeep.Forits"Portraits"ad,whichairedathalftimeofSuperBowl50andendedupbeingamongstuser’sfavouritespotsofthegame,Jeepchosetoproduceaverticalvideothatplayedbeautifullyonmobilescreens.

20

Challenge3

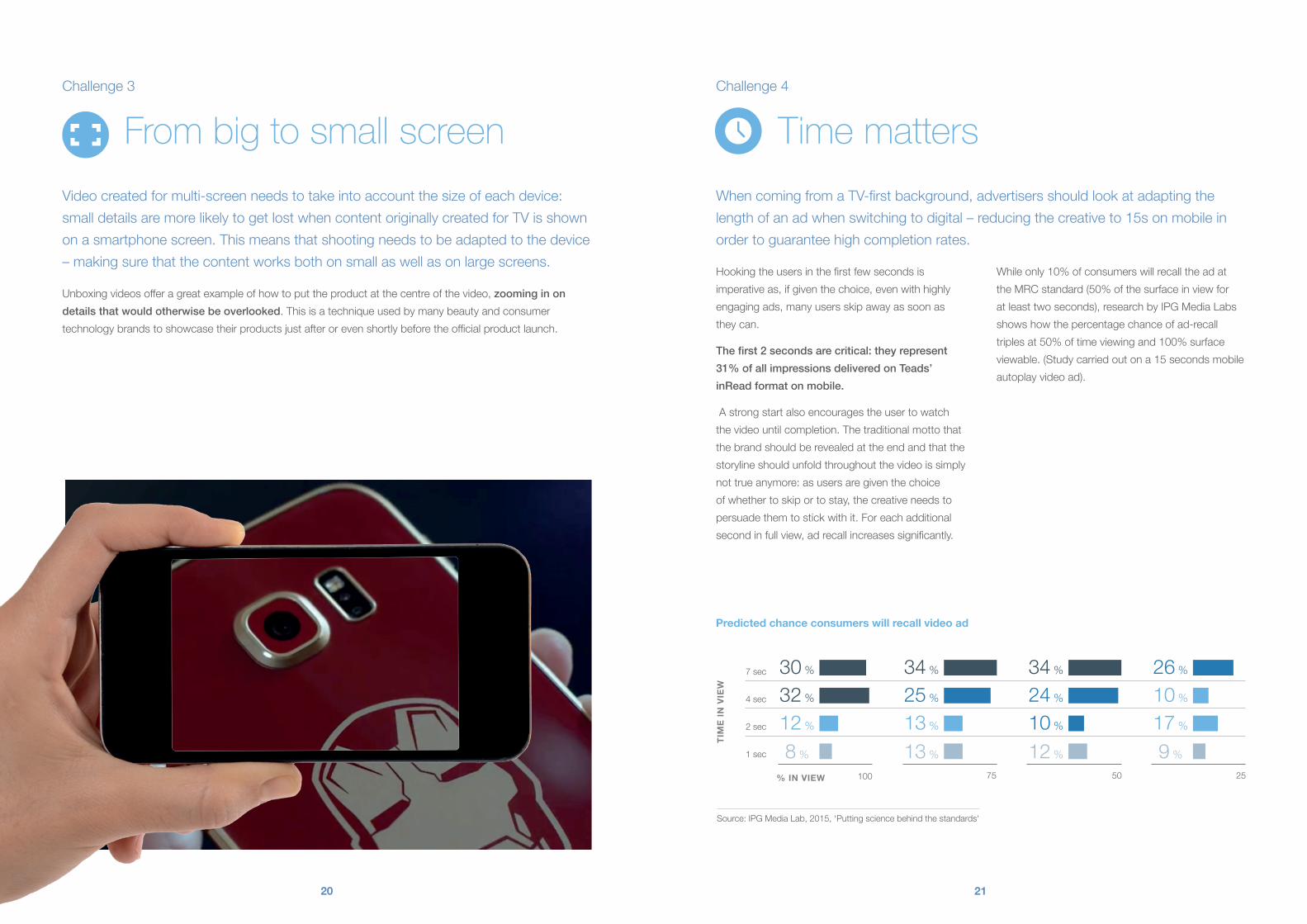

From big to small screen

Videocreatedformulti-screenneedstotakeintoaccountthesizeofeachdevice:smalldetailsaremorelikelytogetlostwhencontentoriginallycreatedforTVisshownonasmartphonescreen.Thismeansthatshootingneedstobeadaptedtothedevice–makingsurethatthecontentworksbothonsmallaswellasonlargescreens.

Unboxingvideosofferagreatexampleofhowtoputtheproductatthecentreofthevideo,zooming in on details that would otherwise be overlooked.Thisisatechniqueusedbymanybeautyandconsumertechnologybrandstoshowcasetheirproductsjustafterorevenshortlybeforetheofficialproductlaunch.

21

Challenge4

Time matters

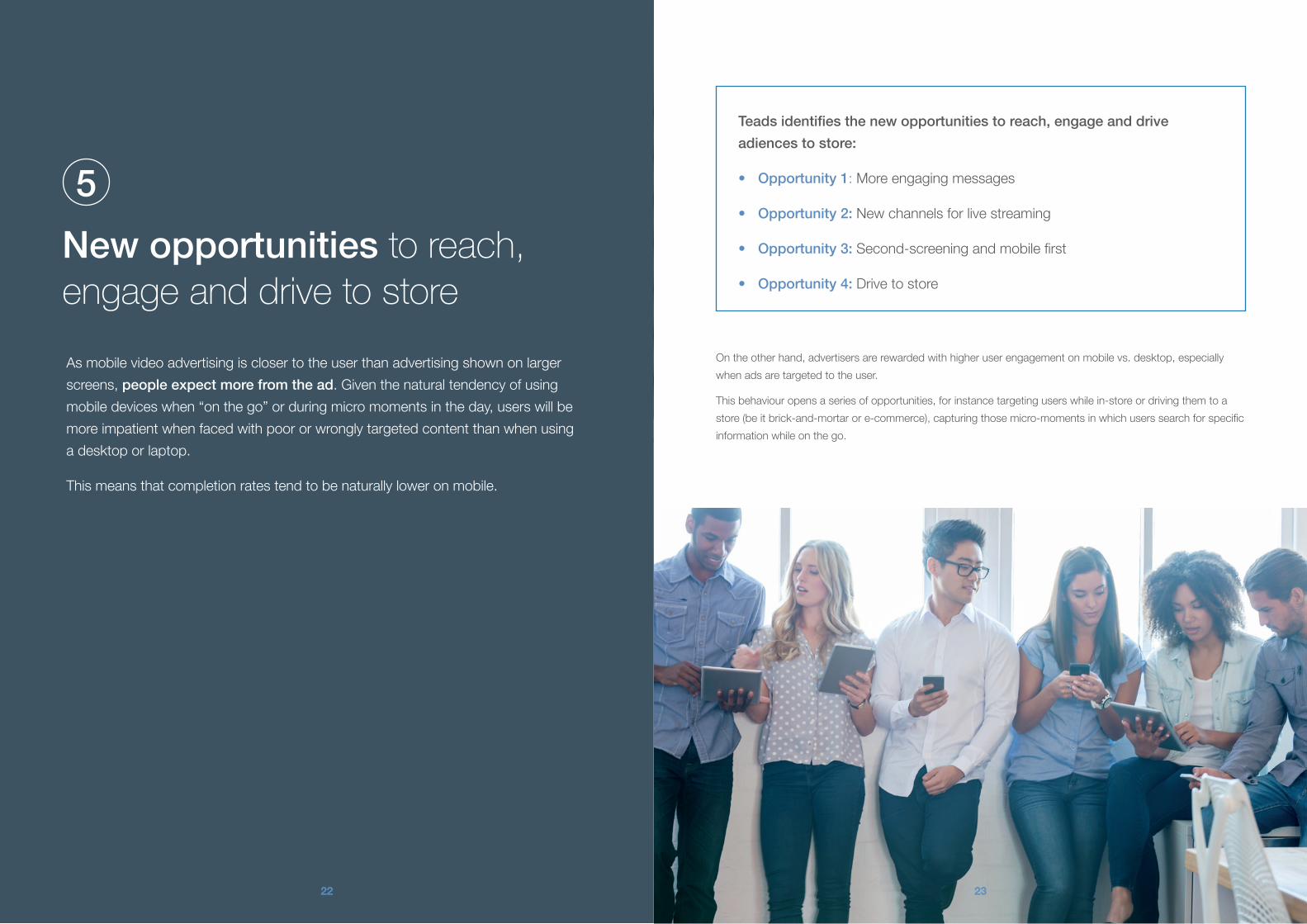

Source:IPGMediaLab,2015,‘Puttingsciencebehindthestandards'

TIM

E IN

VIE

W

% IN VIEW

7sec

4sec

2sec

1sec

100

30%

32%

12%

8%

34%

25%

13%

13%

34%

24%

10%

12%

75 50 25

26%

10%

17%

9%

WhencomingfromaTV-firstbackground,advertisersshouldlookatadaptingthelengthofanadwhenswitchingtodigital–reducingthecreativeto15sonmobileinordertoguaranteehighcompletionrates.

Hookingtheusersinthefirstfewsecondsisimperativeas,ifgiventhechoice,evenwithhighlyengagingads,manyusersskipawayassoonastheycan.

The first 2 seconds are critical: they represent 31% of all impressions delivered on Teads’ inRead format on mobile.

Astrongstartalsoencouragestheusertowatchthevideountilcompletion.Thetraditionalmottothatthebrandshouldberevealedattheendandthatthestorylineshouldunfoldthroughoutthevideoissimplynottrueanymore:asusersaregiventhechoiceofwhethertoskiportostay,thecreativeneedstopersuadethemtostickwithit.Foreachadditionalsecondinfullview,adrecallincreasessignificantly.

Whileonly10%ofconsumerswillrecalltheadattheMRCstandard(50%ofthesurfaceinviewforatleasttwoseconds),researchbyIPGMediaLabsshowshowthepercentagechanceofad-recalltriplesat50%oftimeviewingand100%surfaceviewable.(Studycarriedoutona15secondsmobileautoplayvideoad).

Predicted chance consumers will recall video ad

Teads identifies the new opportunities to reach, engage and drive adiences to store:

• Opportunity 1:Moreengagingmessages

• Opportunity 2:Newchannelsforlivestreaming

• Opportunity 3: Second-screeningandmobilefirst

• Opportunity 4: Drivetostore

Ontheotherhand,advertisersarerewardedwithhigheruserengagementonmobilevs.desktop,especiallywhenadsaretargetedtotheuser.

Thisbehaviouropensaseriesofopportunities,forinstancetargetinguserswhilein-storeordrivingthemtoastore(beitbrick-and-mortarore-commerce),capturingthosemicro-momentsinwhichuserssearchforspecificinformationwhileonthego.

22

Asmobilevideoadvertisingisclosertotheuserthanadvertisingshownonlargerscreens,people expect more from the ad.Giventhenaturaltendencyofusingmobiledeviceswhen“onthego”orduringmicromomentsintheday,userswillbemoreimpatientwhenfacedwithpoororwronglytargetedcontentthanwhenusingadesktoporlaptop.

Thismeansthatcompletionratestendtobenaturallyloweronmobile.

5New opportunities to reach,

engage and drive to store

23

Mobileisthemostpersonalmediaandassuchitoffersagreatopportunitytocreateamoreengagingcommunicationwithconsumers.

ForitsChristmascampaign,BritishretailerJohnLewiscreatedanemotivefilminwhichayounggirl,ondiscoveringthatanelderlypersonwaslivingaloneonthemoon,findsawaytosendhimagift.

Thetweetreleasingthevideowasre-tweeted52,000timesbyconsumers;eachofthemreceivedatweetbackfromJohnLewis,includingathank-youvideopersonalisedwiththeuser’sname.

Thisisagreatexampleofhowto combine a mainstream, TV-centric approach, with further engagement via digital platforms.

Opportunity1

More engaging messages

24 25

Opportunity2

New channels for live streaming

Withthewindowbetweentimeofpublicationandtimeofconsumptionnarrowing,live-streamingisbecominganeffectivewaytoengagewithaudiencesonmobile.

PlatformssuchasSnapchat,PeriscopeandMeerkatallowreal-timetransmissionofcontentforuserswhoareonthelook-outforraw,(seemingly)uneditedcontent.Thisshiftalsobringswithittheappearanceofunfilteredimagesandcontent,althoughthefilteringandeditingsimplypassesstraighttothehands(andeyes)ofthepersonrecording.Nevertheless,these channels allow users to feel close to the centre of the events;fashionbrandssuchasBurberryuseMeerkatandPeriscopetolive-streamtheirfashionshows,creatingauniqueconnectionbetweenthepeoplephysicallypresentintheroomandthosewatchingtheshowfromthecomfortoftheirhome.

Thisisperhapsironicwhenconsideringthatlive-streamingisrisingalongwithon-demandandcatch-upTV –aparalleldevelopmentthatissimilartothe‘eventisation’originallyoccurringaroundTVgatherings,backinthedayswhenpeoplewouldwaitthewholedayforaprogrammetoair.

Source:TheDrum,Burberryfashionshow

26

Opportunity3

Second-screening

and mobile first

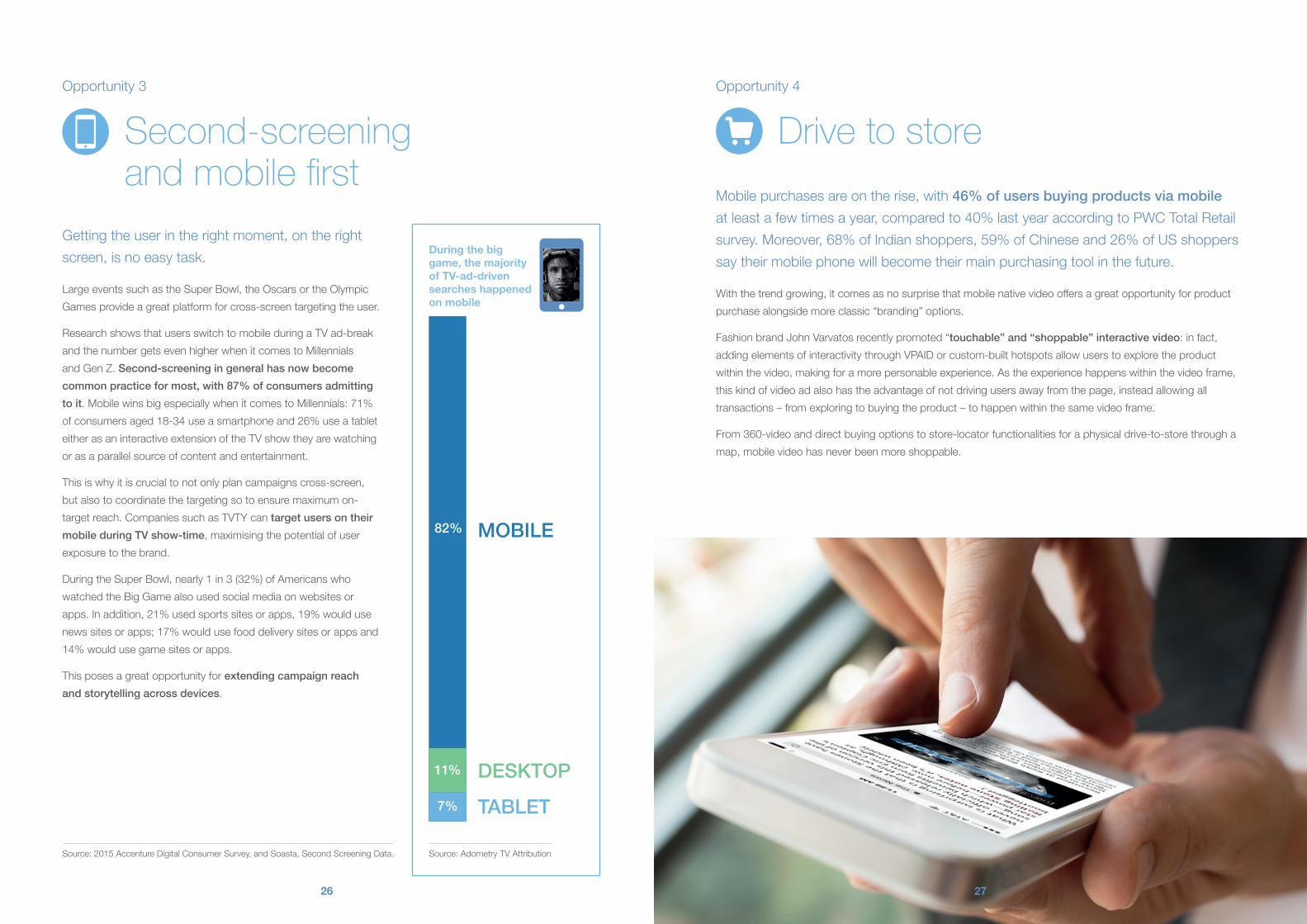

TABLET

DESKTOP

MOBILE

7%

11%

82%

Source:AdometryTVAttributionSource:2015AccentureDigitalConsumerSurvey,andSoasta,SecondScreeningData.

Gettingtheuserintherightmoment,ontherightscreen,isnoeasytask.

LargeeventssuchastheSuperBowl,theOscarsortheOlympicGamesprovideagreatplatformforcross-screentargetingtheuser.

ResearchshowsthatusersswitchtomobileduringaTVad-breakandthenumbergetsevenhigherwhenitcomestoMillennialsandGenZ.Second-screening in general has now become common practice for most, with 87% of consumers admitting to it.MobilewinsbigespeciallywhenitcomestoMillennials:71%ofconsumersaged18-34useasmartphoneand26%useatableteitherasaninteractiveextensionoftheTVshowtheyarewatchingorasaparallelsourceofcontentandentertainment.

Thisiswhyitiscrucialtonotonlyplancampaignscross-screen,butalsotocoordinatethetargetingsotoensuremaximumon-targetreach.CompaniessuchasTVTYcantarget users on their mobile during TV show-time,maximisingthepotentialofuserexposuretothebrand.

DuringtheSuperBowl,nearly1in3(32%)ofAmericanswhowatchedtheBigGamealsousedsocialmediaonwebsitesorapps.Inaddition,21%usedsportssitesorapps,19%wouldusenewssitesorapps;17%wouldusefooddeliverysitesorappsand14%wouldusegamesitesorapps.

Thisposesagreatopportunityforextending campaign reach and storytelling across devices.

During the big game, the majority of TV-ad-driven searches happened on mobile

27

Opportunity4

Drive to store

Mobilepurchasesareontherise,with46% of users buying products via mobile atleastafewtimesayear,comparedto40%lastyearaccordingtoPWCTotalRetailsurvey.Moreover,68%ofIndianshoppers,59%ofChineseand26%ofUSshopperssaytheirmobilephonewillbecometheirmainpurchasingtoolinthefuture.

Withthetrendgrowing,itcomesasnosurprisethatmobilenativevideooffersagreatopportunityforproductpurchasealongsidemoreclassic“branding”options.

FashionbrandJohnVarvatosrecentlypromoted“touchable” and “shoppable” interactive video:infact,addingelementsofinteractivitythroughVPAIDorcustom-builthotspotsallowuserstoexploretheproductwithinthevideo,makingforamorepersonableexperience.Astheexperiencehappenswithinthevideoframe,thiskindofvideoadalsohastheadvantageofnotdrivingusersawayfromthepage,insteadallowingalltransactions–fromexploringtobuyingtheproduct–tohappenwithinthesamevideoframe.

From360-videoanddirectbuyingoptionstostore-locatorfunctionalitiesforaphysicaldrive-to-storethroughamap,mobilevideohasneverbeenmoreshoppable.

28 29

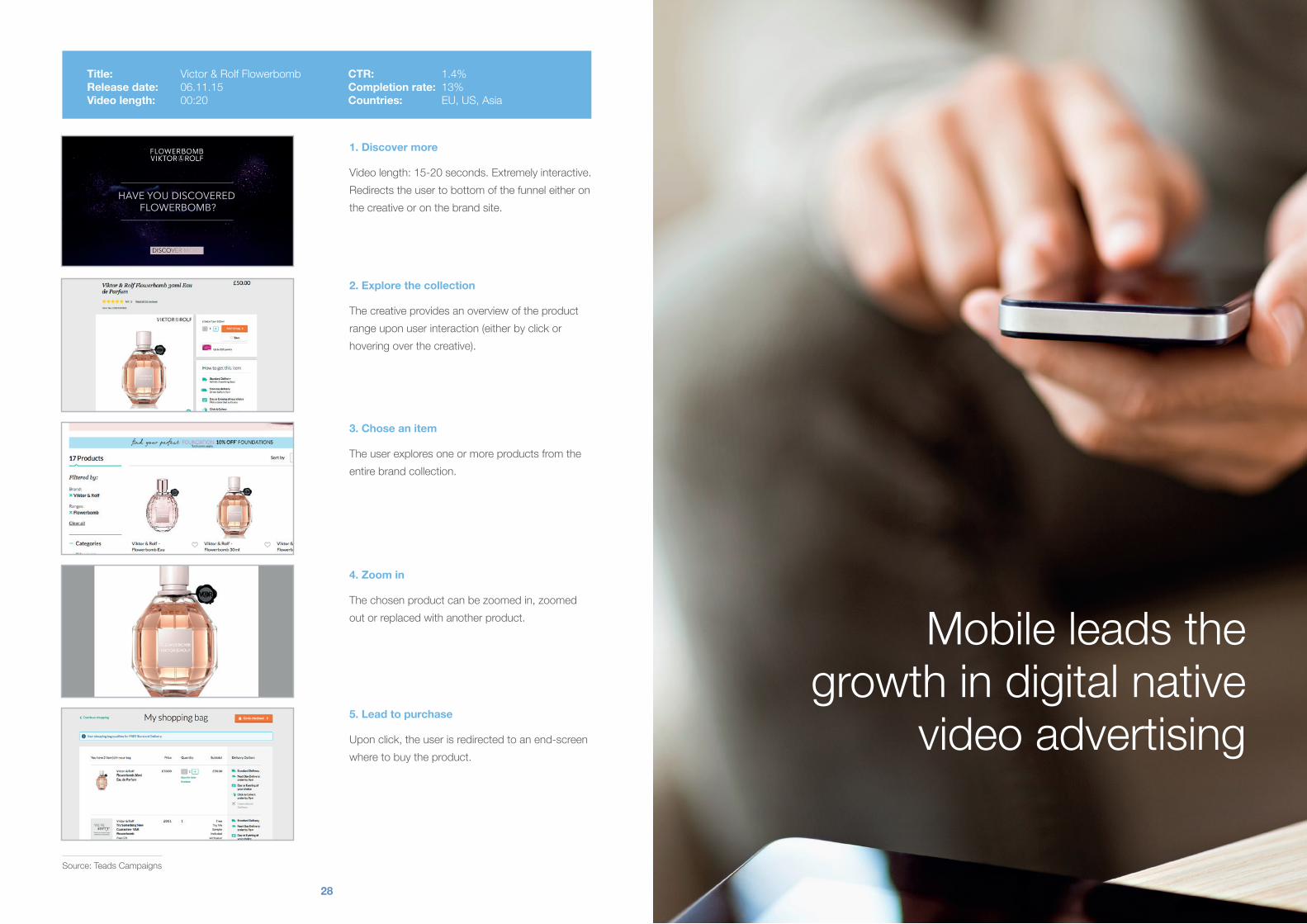

1. Discover more

Videolength:15-20seconds.Extremelyinteractive.Redirectstheusertobottomofthefunneleitheronthecreativeoronthebrandsite.

2. Explore the collection

Thecreativeprovidesanoverviewoftheproductrangeuponuserinteraction(eitherbyclickorhoveringoverthecreative).

3. Chose an item

Theuserexploresoneormoreproductsfromtheentirebrandcollection.

4. Zoom in

Thechosenproductcanbezoomedin,zoomedoutorreplacedwithanotherproduct.

5. Lead to purchase

Uponclick,theuserisredirectedtoanend-screenwheretobuytheproduct.

Source:TeadsCampaigns

Title: Victor&RolfFlowerbombRelease date: 06.11.15Video length: 00:20

CTR: 1.4%Completion rate: 13%Countries: EU,US,Asia

Mobileleadsthegrowthindigitalnative

videoadvertising

31

5. Show brand and product

Theshiftfromlargetosmallerscreensimpliestheneedtoadaptcreativestoaportabledevice,wherelittledetailsmightbemissed.Makesurebrand,productandmessagingareclearlyvisibleevenonatinyscreen.

6. Create shorter content

Creatingformobilemeanssnackablecontentbutalsohookingtheusersinthefirstseconds:giventhechoice,evenwithhighlyengagingads,manyusersskipawayassoonastheycan.

7. Personalise your messaging

Makesuretheclassicvideodistributionapproachiscomplementedbyengagingfansandcommunities.Personalisationandcustomisationarerisingtrendsthatmakeforgreatengagementbetweentheuserandthebrand.

8. Explore live streaming

Immediacyand360-degreeformatsallowuserstofeelmoreinvolved,generatingmoretransversalcontentthatgoesbeyondadvertisingforaspecificproduct.

9. Use second screening, go mobile first

Asover80%ofusersturntotheirmobiledeviceswhilewatchingTV,mobileshouldbethefocalpointofanyvideocampaign,notjustTV’sancillary.

10. Drive to store

Mobilevideogoesbeyondbranding:withm-commercesurging,videocanbeshoppable,too.InteractiveVPAIDformatsallowuserstoengagedirectlywiththecontent.

To find out more about how Teads can help you plan your cross-screen campaign effectively, get in touch for a demo.

6Creating for mobile video:

Why it matters

30

As mobile truly revolutionised video advertising, it is time for brands to mobilise their creative genius, too. With TV losing ground, mobile leads the growth in digital video advertising.

So why does mobile video matter?

In a recap of our findings, Teads presents:

TEN GOLDEN RULES OF MOBILE VIDEO

1. Plan cross-screen but think mobile first

Anintegratedapproachofdigital+TVhelpspushbackthepointofdiminishingreturnsascampaignsfollowtheuserjourneyacrossdevices.Asusersaremorereceptivetoadintrusiononmobile,useitasastandardtodefinetheadvertisingexperience.

2. Choose native video formats

Withadblockingbehaviourontherise,especiallyonmobile,advertisersneedtorefrainfromintrusiveadformatsandusenativevideoads,thatareseamlesslyintegratedinthefeedofthecontentratherthanforcedtotheuser.

3. Make it work with no sound

Videosareoftenplayedsilently.Makingthevideoworkbothwithorwithoutsoundisimperativetoyieldgoodresults.

4. Adapt to viewing behaviour

Notallvideoisconsumedhorizontally–squareandverticalformatsareequallyimportantandneedtobetakenintoaccountbycreatingcontentthatworksacrossallformats.

32

REINVENTINGVIDEOADVERTISING

Would you like to challenge us

or tell us anything we missed?

TEADS.TV