THE MANUFACTURING ECONOMIC UPDATE

Dr. Chad MoutrayChief Economist

National Association of Manufacturers

Updated April 8, 2013

2010:1 2010:2 2010:3 2010:4 2011:1 2011:2 2011:3 2011:4 2012:1 2012:2 2012:3 2012:4 2013:140%

50%

60%

70%

80%

90%

100%

69.5%73.9% 74.5% 74.9%

82.8%86.4%

65.4%

80.2%

88.7%

83.1%

69.2%

51.8%

70.1%

Manufacturing Business OutlookBy Quarter, 2010-2013

Source: NAM/Industry Week Survey of ManufacturersNote: Percentage of respondents who characterized the current business outlook at somewhat or very positive. Percentages are annual averages. Q4:2010 and Q1:2011 data are imputed from comparable data using a regression model.

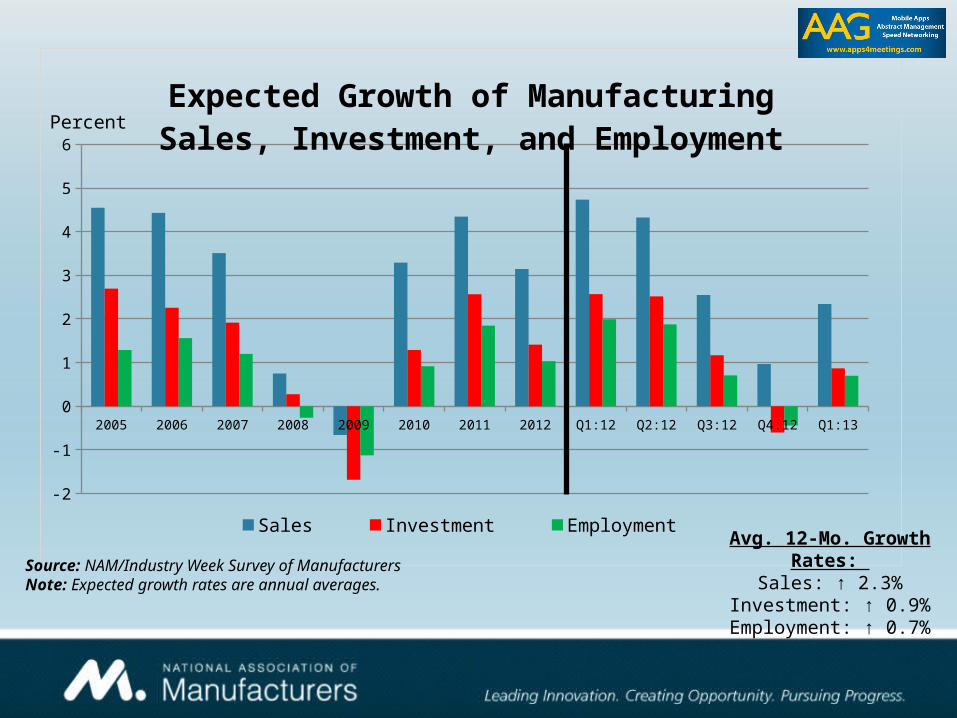

2005 2006 2007 2008 2009 2010 2011 2012 Q1:12 Q2:12 Q3:12 Q4:12 Q1:13

-2

-1

0

1

2

3

4

5

6

Expected Growth of Manufacturing Sales, Investment, and Employment

Sales Investment Employment

Percent

Source: NAM/Industry Week Survey of ManufacturersNote: Expected growth rates are annual averages.

Avg. 12-Mo. Growth Rates:

Sales: ↑ 2.3%Investment: ↑ 0.9%

Employment: ↑ 0.7%

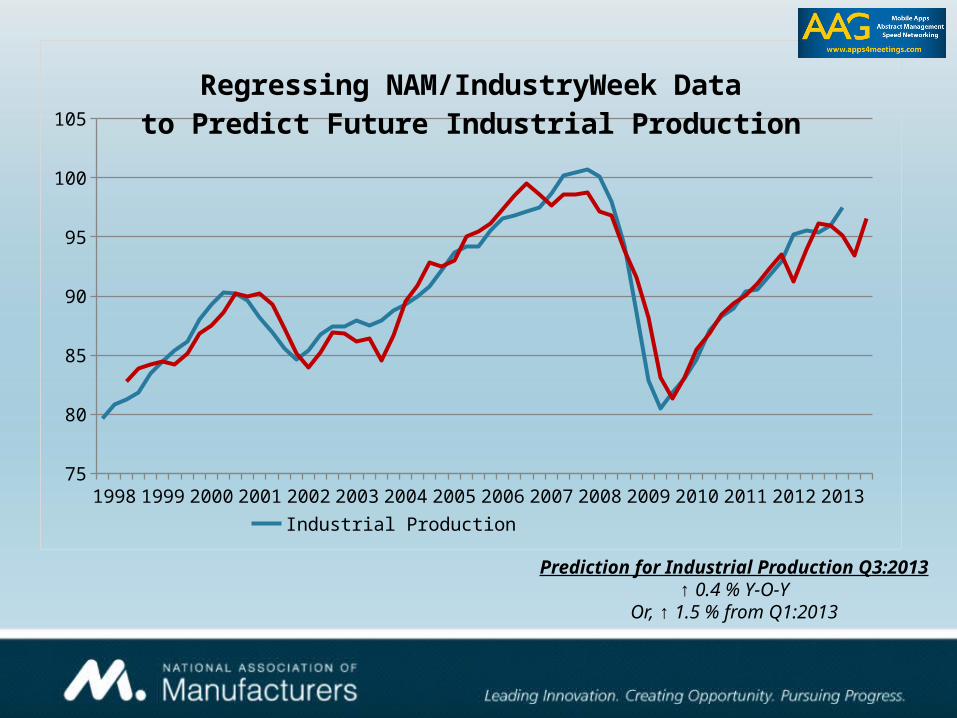

199819992000200120022003200420052006200720082009201020112012201375

80

85

90

95

100

105

Regressing NAM/IndustryWeek Datato Predict Future Industrial Production

Industrial Production Industrial Production (Predicted)

Prediction for Industrial Production Q3:2013

↑ 0.4 % Y-O-YOr, ↑ 1.5 % from Q1:2013

Source: NAM/Industry Week Survey of ManufacturersNote: Respondents were able to check all that apply. Therefore, responses exceed 100 percent.

Challenges with access to capital or other forms of financing

Weaker global growth and slower export sales

Rising energy and raw material costs for our products

Attracting and retaining a quality workforce

Weaker domestic economy and sales for our products to U.S. customers

Unfavorable business climate (e.g., taxes, regulation)

Uncertainties related to the political climate (e.g., debt/deficit debate, pending budget cuts)

Rising health care/insurance costs

4.7%

27.9%

37.3%

41.1%

49.9%

67.7%

72.1%

74.0%

Primary Current Business Chal-lenges,

First Quarter 2013

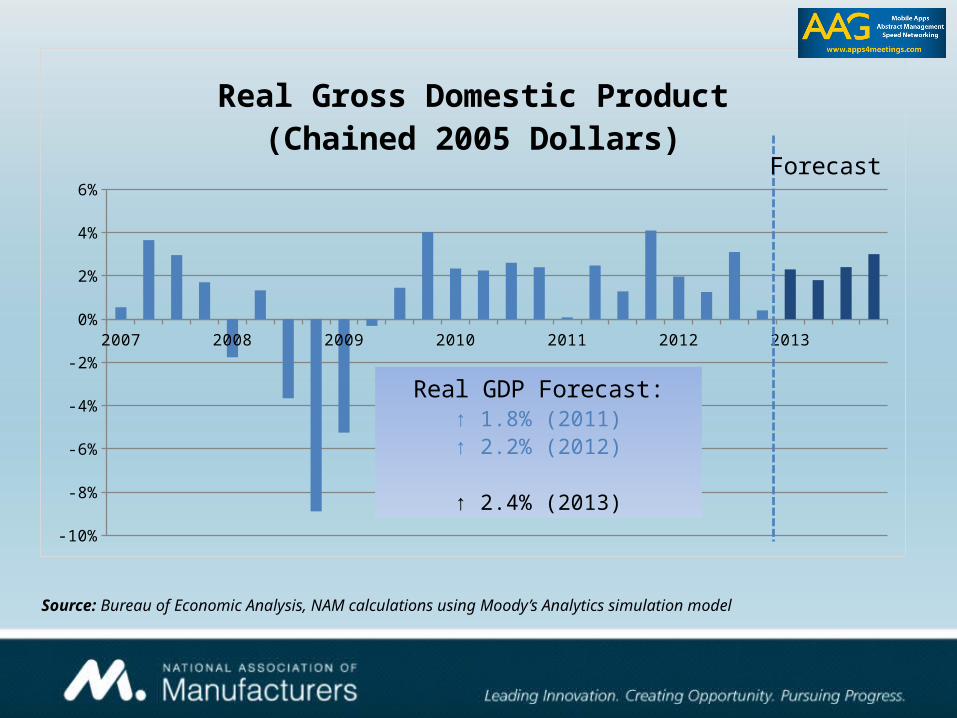

2007 2008 2009 2010 2011 2012 2013

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Real Gross Domestic Product(Chained 2005 Dollars)

Real GDP Forecast:↑ 1.8% (2011)↑ 2.2% (2012)

↑ 2.4% (2013)

Forecast

Source: Bureau of Economic Analysis, NAM calculations using Moody’s Analytics simulation model

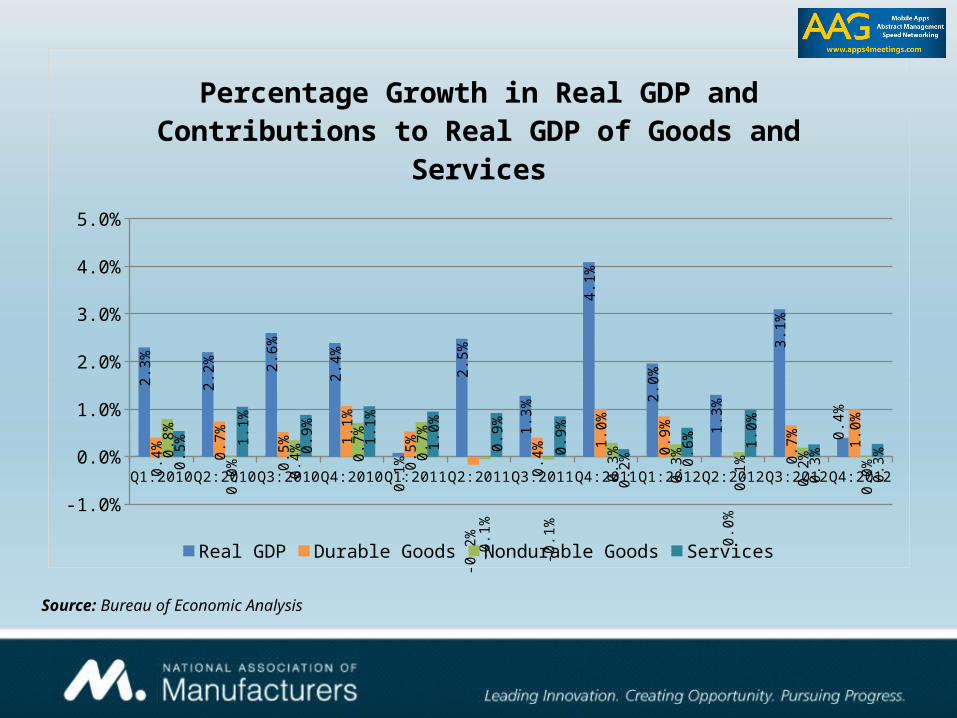

Q1:2010

Q2:2010

Q3:2010

Q4:2010

Q1:2011

Q2:2011

Q3:2011

Q4:2011

Q1:2012

Q2:2012

Q3:2012

Q4:2012

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2.3

%

2.2

% 2.6

%

2.4

%

0.1

%

2.5

%

1.3

%

4.1

%

2.0

%

1.3

%

3.1

%

0.4

%

0.4

% 0.7

%

0.5

% 1.1

%

0.5

%

-0.2

%

0.4

% 1.0

%

0.9

%

0.0

%

0.7

% 1.0

%

0.8

%

0.0

% 0.4

% 0.7

%

0.7

%

-0.1

%

-0.1

%

0.3

%

0.3

%

0.1

%

0.2

%

0.0

%0.5

% 1.1

%

0.9

%

1.1

%

1.0

%

0.9

%

0.9

%

0.2

% 0.6

% 1.0

%

0.3

%

0.3

%

Percentage Growth in Real GDP andContributions to Real GDP of Goods and

Services

Real GDP Durable Goods Nondurable Goods Services

Source: Bureau of Economic Analysis

2005 2006 2007 2008 2009 2010 2011 2012 2013$130

$150

$170

$190

$210

$230

$250

Manufactured Durable Goods(in Billions of Dollars)

New Orders Shipments

Source: U.S. Census Bureau

2007 2008 2009 2010 2011 2012 201365

70

75

80

85

90

95

100

105Industrial Production

Industrial Production Capacity Utilization

Industrial Production/Capacity Utilization %

Source: Federal Reserve Board

Jan-12 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 13-Jan Feb

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

% Changes in Manufacturing Production, 2012-2013

Manufacturing Durable Goods Nondurable Goods

Percent

Source: Federal Reserve Board

2008 2009 2010 2011 2012 201320.0

30.0

40.0

50.0

60.0

70.0

ISM Manufacturing Indices

Purchasing Managers Index New Orders Index Employment IndexInventories Index

Source: Institute for Supply Management

2011 2012 2013

-30

-20

-10

0

10

20

30

40

80

82

84

86

88

90

92

94

96

98

100

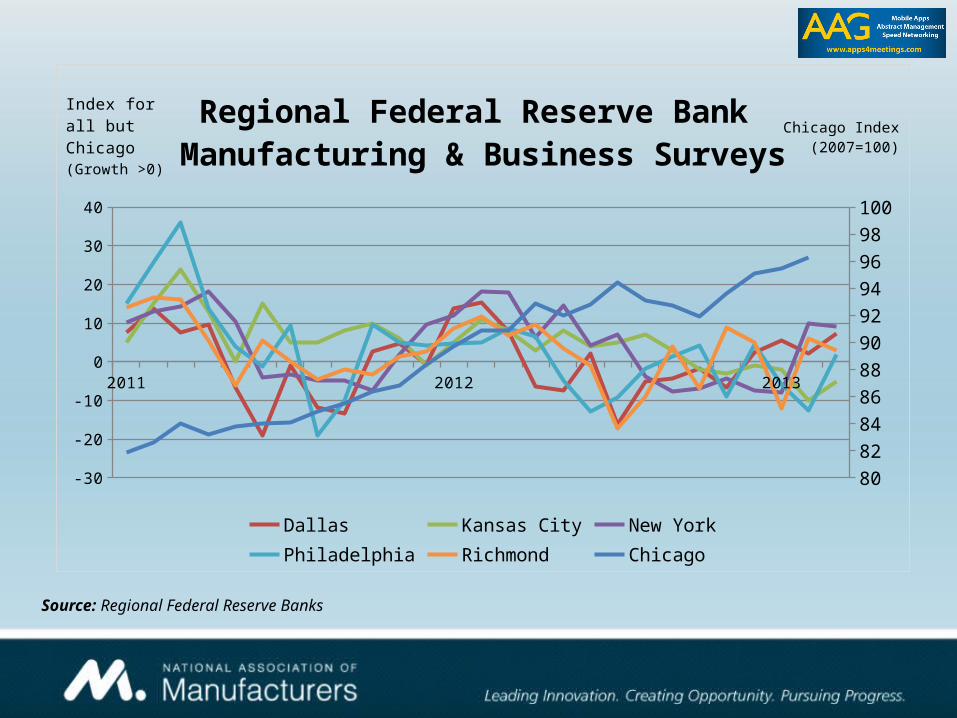

Regional Federal Reserve Bank Manufacturing & Business Surveys

Dallas Kansas City New YorkPhiladelphia Richmond Chicago

Index for all but Chicago(Growth >0)

Chicago Index(2007=100)

Source: Regional Federal Reserve Banks

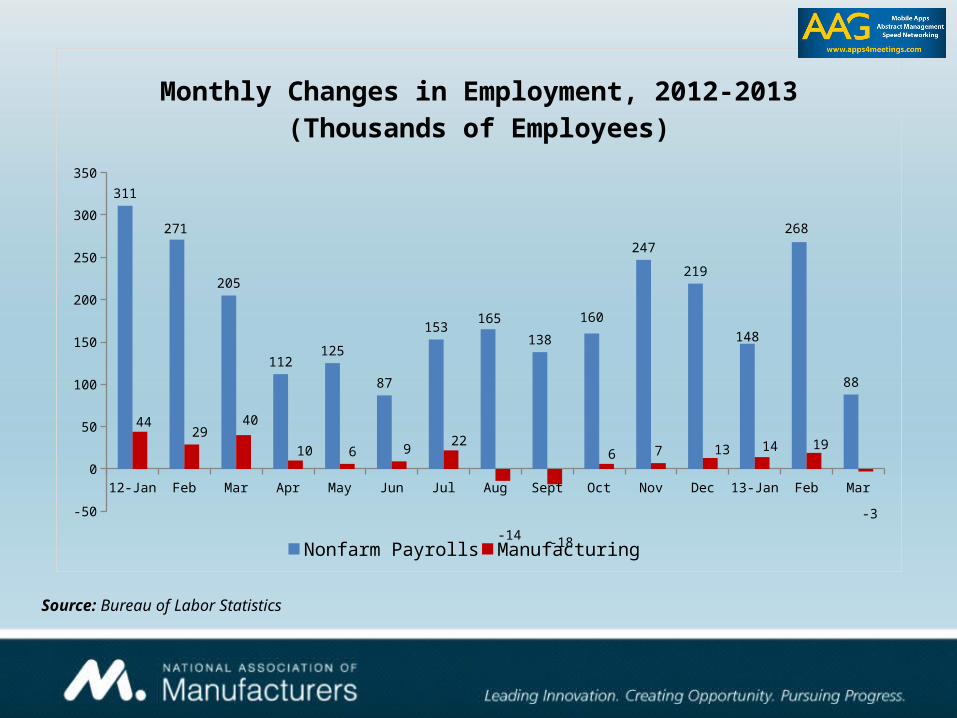

12-Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec 13-Jan Feb Mar

-50

0

50

100

150

200

250

300

350

311

271

205

112125

87

153165

138

160

247

219

148

268

88

4429

40

10 6 922

-14 -18

6 7 13 14 19

-3

Monthly Changes in Employment, 2012-2013

(Thousands of Employees)

Nonfarm Payrolls Manufacturing

Source: Bureau of Labor Statistics

2008 2009 2010 2011 2012 20136

7

8

9

10

11

12

13

14

4%

5%

6%

7%

8%

9%

10%

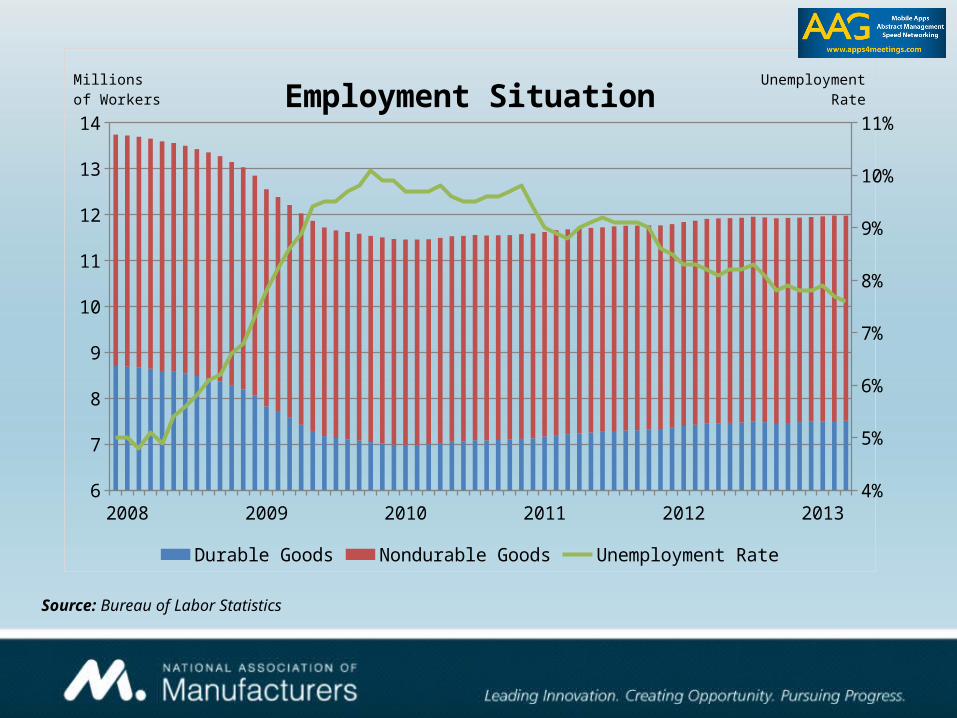

11%Employment Situation

Durable Goods Nondurable Goods Unemployment Rate

Millionsof Workers

Unemployment Rate

Source: Bureau of Labor Statistics

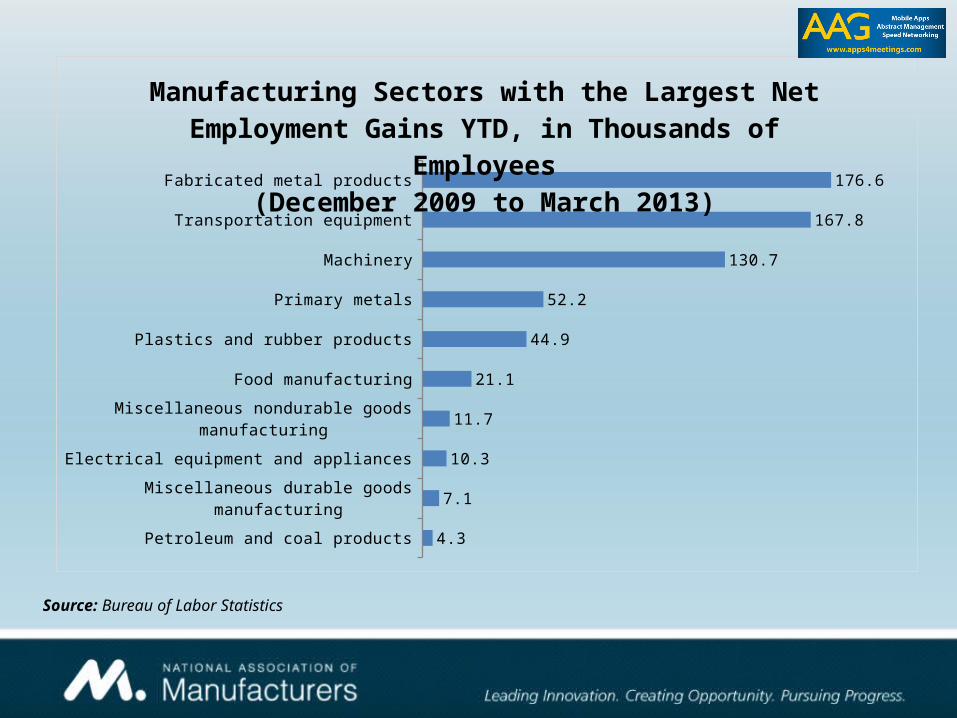

Petroleum and coal products

Miscellaneous durable goods manufacturing

Electrical equipment and appliances

Miscellaneous nondurable goods manufacturing

Food manufacturing

Plastics and rubber products

Primary metals

Machinery

Transportation equipment

Fabricated metal products

4.3

7.1

10.3

11.7

21.1

44.9

52.2

130.7

167.8

176.6

Manufacturing Sectors with the Largest Net Employment Gains YTD, in Thousands of

Employees(December 2009 to March 2013)

Source: Bureau of Labor Statistics

Kansas

Colorado

Oregon

Pennsylvania

South Carolina

Minnesota

Kentucky

Washington

Ohio

Texas

6.97.68.19.3

11.211.7

13.515.116.518.018.0

22.122.8

27.529.8

34.950.1

54.158.7

88.3

Top 20 States for Manufacturing Job Creation,

December 2009 to February 2013(in Thousands of Workers)

Source: Bureau of Labor Statistics

2008 2009 2010 2011 2012 201375

80

85

90

95

100

105

Manufacturing Employment Growth(December 2007 = 100)

Nonfarm Payrolls ManufacturingDurable Goods Nondurable Goods

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

2007 2008 2009 2010 2011 2012 201350

100

150

200

250

300

350

400

450

500

550

Manufacturing Job Hires & Sepa-rations

(January 2007 to February 2013)

Job Openings Hires Separations

1987 1990 1993 1996 1999 2002 2005 2008 201190

110

130

150

170

190

210

230

250

270

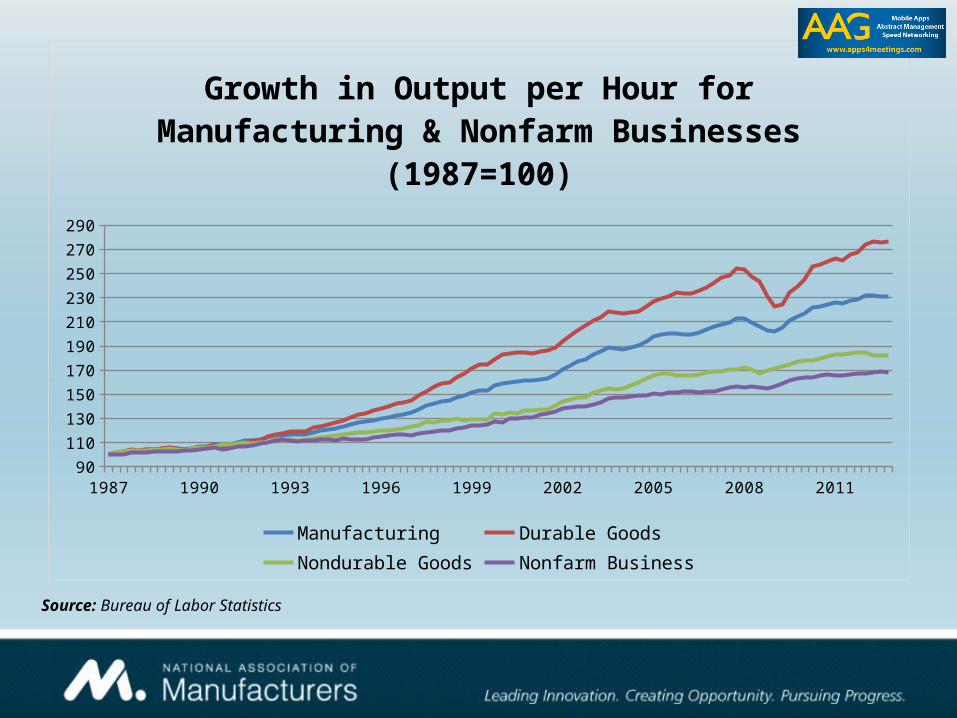

290

Growth in Output per Hour for Man-ufacturing & Nonfarm Businesses

(1987=100)

Manufacturing Durable GoodsNondurable Goods Nonfarm Business

Source: Bureau of Labor Statistics

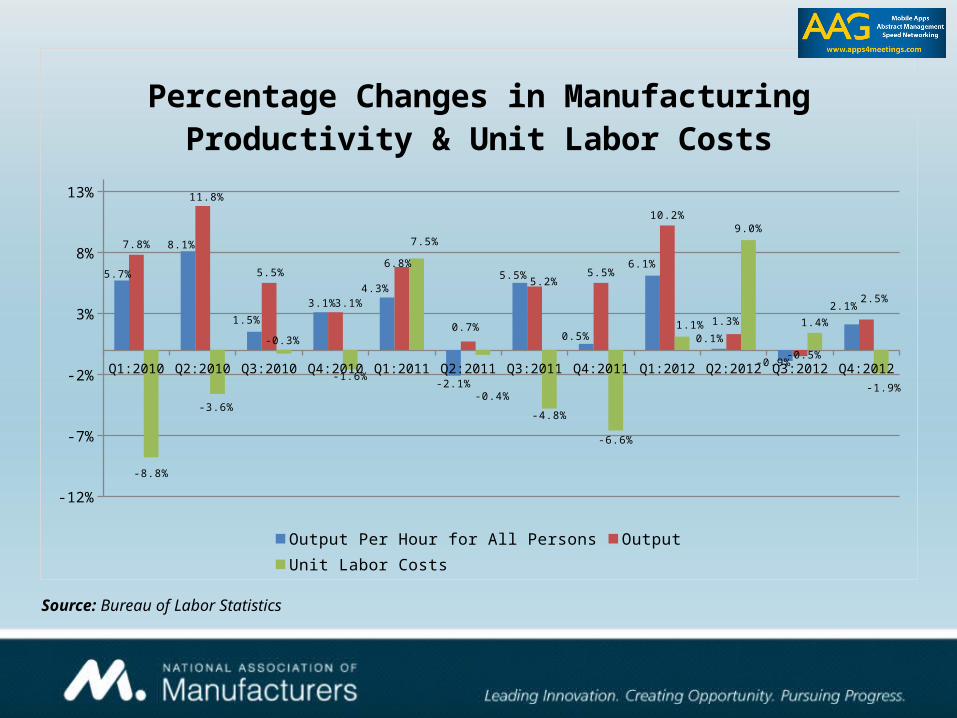

Q1:2010 Q2:2010 Q3:2010 Q4:2010 Q1:2011 Q2:2011 Q3:2011 Q4:2011 Q1:2012 Q2:2012 Q3:2012 Q4:2012

-12%

-7%

-2%

3%

8%

13%

5.7%

8.1%

1.5%

3.1%

4.3%

-2.1%

5.5%

0.5%

6.1%

0.1%

-0.9%

2.1%

7.8%

11.8%

5.5%

3.1%

6.8%

0.7%

5.2%5.5%

10.2%

1.3%

-0.5%

2.5%

-8.8%

-3.6%

-0.3%

-1.6%

7.5%

-0.4%

-4.8%

-6.6%

1.1%

9.0%

1.4%

-1.9%

Percentage Changes in Manufactur-ing Productivity & Unit Labor Costs

Output Per Hour for All Persons Output Unit Labor Costs

Source: Bureau of Labor Statistics

Some Ongoing Strengths in the Economy

A Recovering Housing Market

Historically Low Interest Rates

Modest Growth in Consumer Spending

Growth in Exports, Albeit at a Slower Pace

Lower Energy Costs, Aided by Shale Exploration

Increased Signs of Reshoring, Improved Global Competitiveness

2005 2006 2007 2008 2009 2010 2011 2012 20130

500

1,000

1,500

2,000

2,500

0

10

20

30

40

50

60

70

80

Housing Market Situation

Housing Starts Housing PermitsNAHB Housing Market Index

NAHB Housing Market Index

Housing Starts, Permits (in thou-sands of units)

Source: U.S. Census Bureau, National Association of Home Builders

2

3

4

5

6

7

8

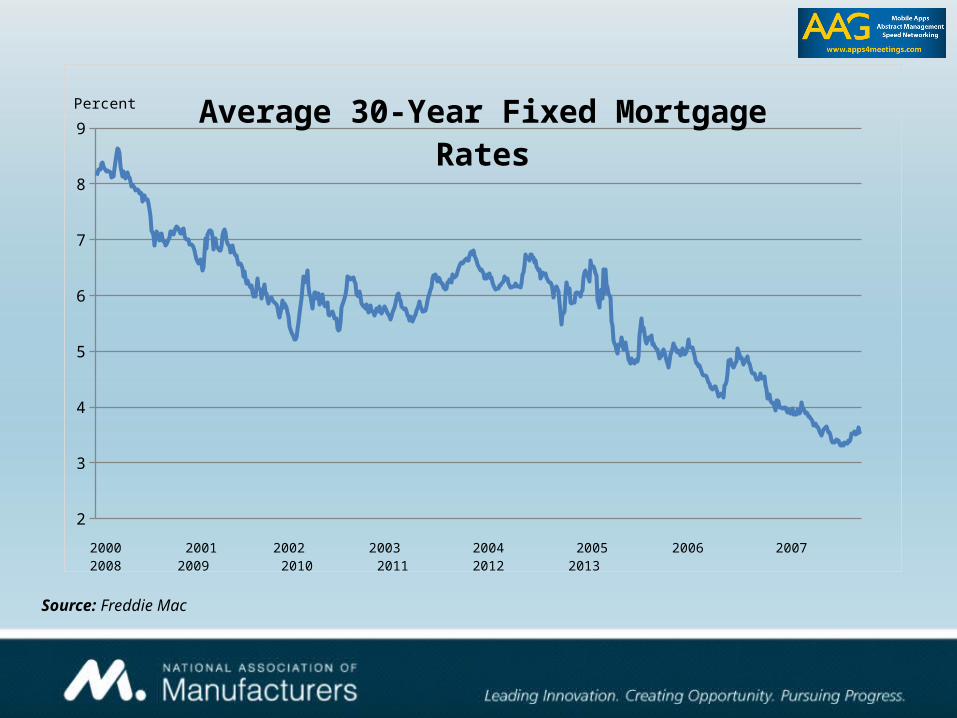

9Average 30-Year Fixed Mortgage

Rates

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Percent

Source: Freddie Mac

2005 2006 2007 2008 2009 2010 2011 2012 2013$20

$30

$40

$50

$60

$70

New Manufacturing Construction Spending

(Value of Private Construction Put in Place, in Billions of Dollars)

Source: U.S. Census Bureau

2010 2011 2012 2013

-5

-4

-3

-2

-1

0

1

2

3

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Personal Income and Spending

Personal Income Personal Spending Savings Rate

Personal Income/Spending (% Change)

Savings RatePercentage

Source: Bureau of Economic Analysis

2005 2006 2007 2008 2009 2010 2011 2012 201320

30

40

50

60

70

80

90

100

110

120

70

75

80

85

90

95

100

105

110

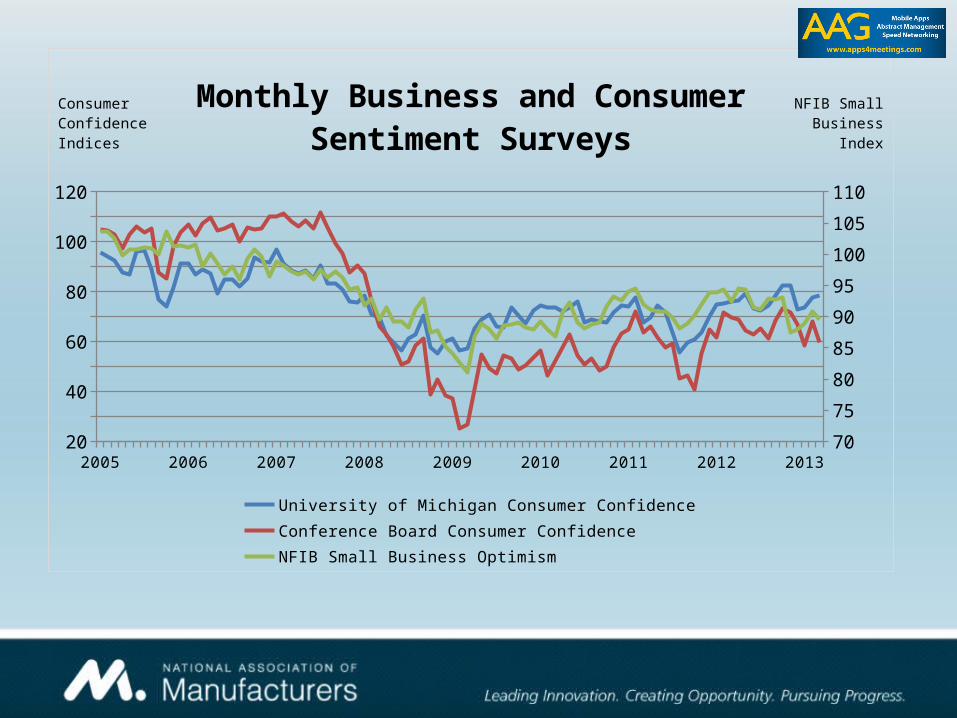

Monthly Business and Consumer Sentiment Surveys

University of Michigan Consumer Confidence Conference Board Consumer ConfidenceNFIB Small Business Optimism

Consumer Confidence Indices

NFIB Small Business Index

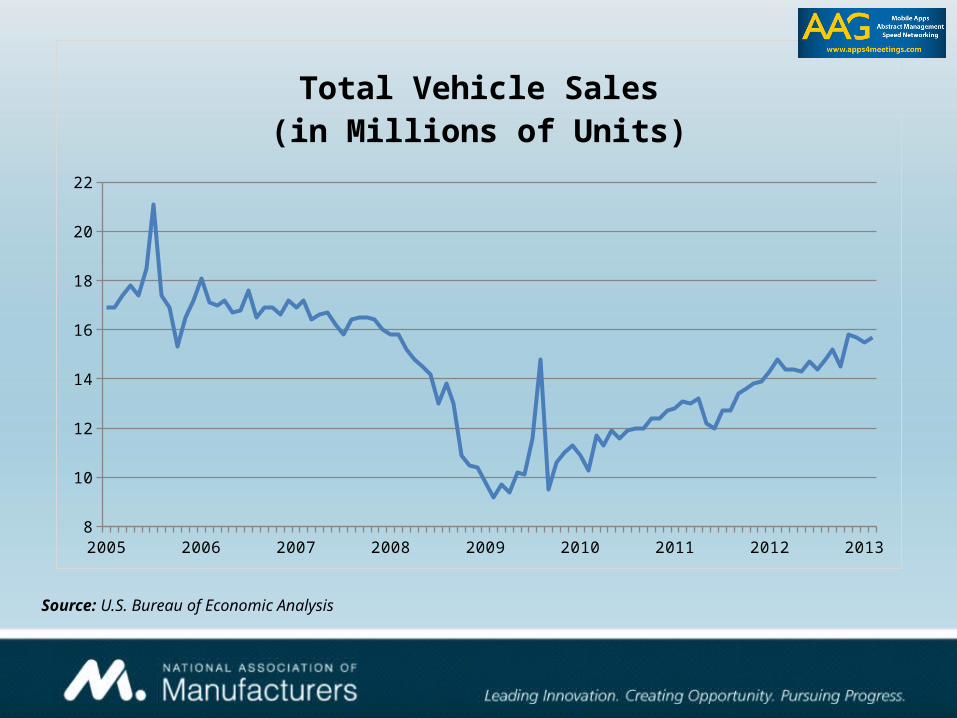

2005 2006 2007 2008 2009 2010 2011 2012 20138

10

12

14

16

18

20

22

Total Vehicle Sales(in Millions of Units)

Source: U.S. Bureau of Economic Analysis

Canada Mexico FTA Asia Europe South America

TOTAL0%

5%

10%

15%

20%

25%

13.0%

20.1%

16.9%

10.8%

17.2%

23.8%

15.9%

4.1%

10.1%

6.8%

2.6%

0.3%

13.3%

5.5%

% Growth of Manufactured Goods Exports, 2011-2012

2011 2012

Source: U.S. Department of Commerce

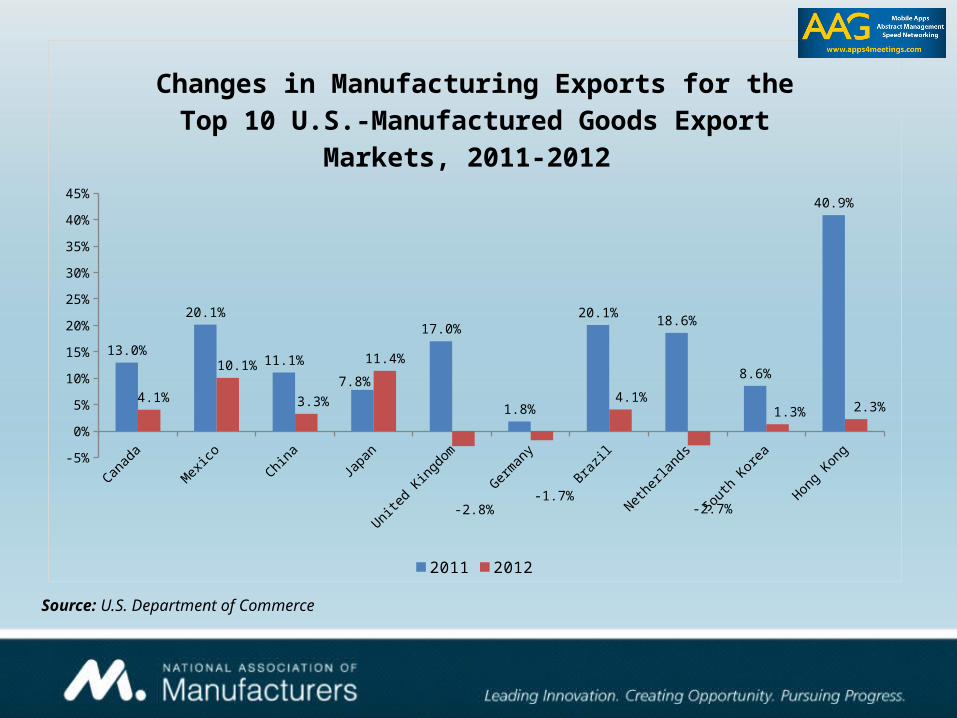

Canada Mexico China Japan United Kingdom

Germany Brazil Netherlands South Korea Hong Kong-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

13.0%

20.1%

11.1%

7.8%

17.0%

1.8%

20.1%18.6%

8.6%

40.9%

4.1%

10.1%

3.3%

11.4%

-2.8%-1.7%

4.1%

-2.7%

1.3% 2.3%

Changes in Manufacturing Exports for the Top 10 U.S.-Manufactured Goods Export

Markets, 2011-2012

2011 2012

Source: U.S. Department of Commerce

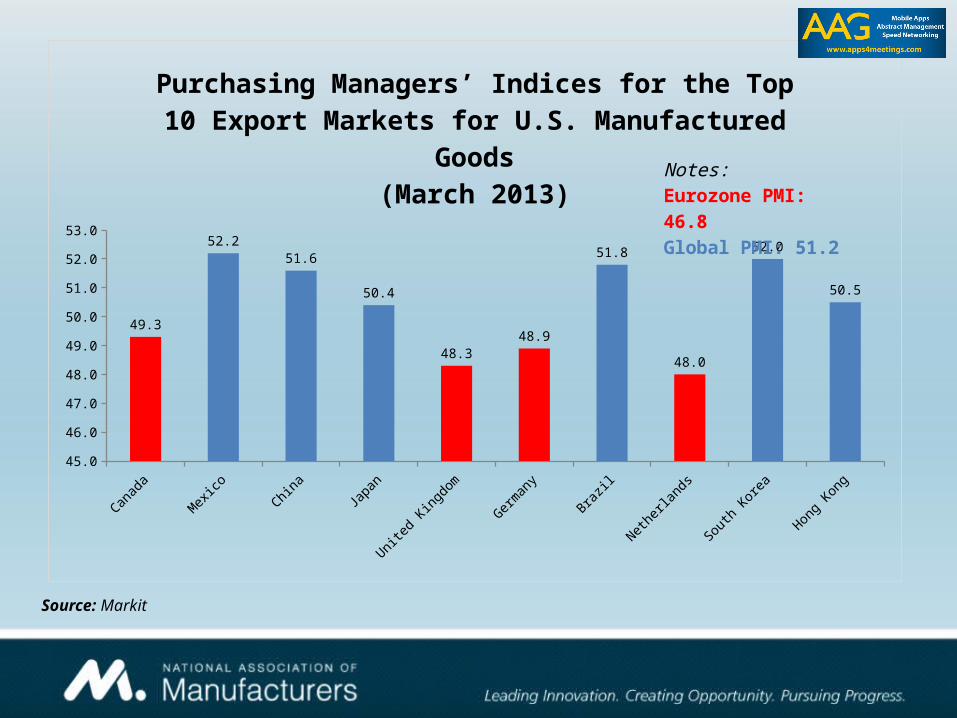

Canada Mexico China Japan United Kingdom

Germany Brazil Netherlands South Korea Hong Kong45.0

46.0

47.0

48.0

49.0

50.0

51.0

52.0

53.0

49.3

52.2

51.6

50.4

48.3

48.9

51.8

48.0

52.0

50.5

Purchasing Managers’ Indices for the Top 10 Export Markets for U.S. Manufactured

Goods(March 2013) Notes:

Eurozone PMI: 46.8Global PMI: 51.2

Source: Markit

Tremendous Promise of Shale Gas

– PwC (December 2011) with the NAM: U.S. manufacturing companies could employ approximately one

million more workers by 2025 due to the benefits of affordable energy and demand for products used to extract the gas.

This same study found that, because of increased shale exploration, lower feedstock and energy costs could help U.S. manufacturers reduce natural gas expenses by as much as $11.6 billion annually through 2025.

– We have already seen how the shale gas revolution has transformed communities, helped to lift employment, and provide tremendous potential moving forward.

– Energy costs are a competitive advantage for U.S. manufacturers right now.

2010 2011 2012 20130%

1%

2%

3%

4%

5%

6%

7%

8%

Producer Price IndexYear-Over-Year Percentage Changes

for Each Month

PPI - Finished Goods PPI - Finished Goods Less Food & Energy

Percent

Source: Bureau of Labor Statistics

1947 50 55 60 65 70 75 80 85 90 95 2000 05 10 1210%

12%

14%

16%

18%

20%

22%

24%

26%

28%

Federal Government Receipts & Expen-ditures as a % of Gross Domestic Prod-

uct, 1947 to Present

Federal Receipts as a % of GDP Federal Expenditures as a % of GDP

23.8%

16.9%

Source: Bureau of Economic Analysis

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

Federal Mandatory Spending, 2012-2023(in Trillions of Dollars)

Social Security Medicare, Net of ReceiptsTotal Mandatory Spending Medicaid

Source: Congressional Budget Office, February 2013

The United States needs a comprehensive plan for economic growth and competitiveness.

GOAL 1The United States will be the best place in the world to manufacture and attract foreign direct investment.

Manufacturers have an array of attractive options around the world when deciding where to invest, conduct research, build new facilities and create jobs.

Create a pro-manufacturing tax policy.

Embrace an “all-of-the above” approach to energy production.

Modernize and invest in infrastructure.

Ensure that the benefits of regulations justify their costs to manufacturers in the United States.

Implement common-sense, fair legal reform.

Reduce health care costs for both patients and providers.

Manufacturers in the United States will be the world’s leading innovators.

Innovation propelled the United States to its global leadership position in manufacturing. But other nations are eager to take our place and are establishing more attractive R&D incentives than those offered by the United States.

Provide a strong, permanent and competitive R&D incentive.

Support federal research agencies and public- and private-sector research.

Recognize IP as the basis of America’s innovative economy.

Develop appropriate general and industry-specific best practices for improved cybersecurity.

Support the growth of a healthy information and communication technology ecosystem.

GOAL 2

The United States will expand access to global markets to enable manufacturers to reach the 95 percent of consumers who live outside our borders.

Promote a global trade policy that opens international markets, enhances competitiveness and reduces regulatory and tariff barriers.

Reduce trading costs, domestic export barriers and unnecessary red tape.

Boost exports through improved export promotion programs and export credit assistance for both small and large manufacturers.

Ensure a level playing field for manufacturers by enforcing trade laws and international agreements.

GOAL 3

Manufacturers in the United States will have access to the workforce that the 21st–century economy demands.

Address regulations and mandates that undermine employer flexibility and ultimately discourage the hiring of new employees.

Develop a more productive workforce and encourage innovation through education reforms and improvements.

Enact comprehensive immigration reform.

Attract the best and brightest to the United States.

GOAL 4

Questions?

Dr. Chad MoutrayChief Economist

National Association of Manufacturers

(202) 637-3148