New Brunswick Sector Profile:

Industrial Fabrication

June 2012

New Brunswick Career Development Action Group

(Funded by the Government of Canada and the Province of New Brunswick

through the Canada-New Brunswick Labour Market Development Agreements)

Prepared by: InPro Solutions

New Brunswick Sector Profile: Industrial Fabrication

i June 2012

Table of Contents

1 Executive Summary ............................................................................................... 1

2 Introduction ............................................................................................................ 8

2.1 Purpose and Scope ........................................................................................... 8

2.2 Objectives ........................................................................................................... 8

3 Methodology .......................................................................................................... 8

3.1 Primary Research................................................................................................ 9

3.1.1 Contact List .................................................................................................. 9

3.1.2 Interviews ................................................................................................... 10

3.2 Secondary Research ....................................................................................... 10

4 Sector Definition ................................................................................................... 11

4.1 About the Definition ......................................................................................... 12

5 Sector Profile ......................................................................................................... 13

5.1 The New Brunswick Context ........................................................................... 13

5.2 Structure of the Sector ..................................................................................... 15

5.3 Capability .......................................................................................................... 17

5.3.1 Company Size ........................................................................................... 17

5.3.2 Facility Size ................................................................................................. 18

5.3.3 Lifting Capacity ......................................................................................... 18

5.3.4 Heavy, Medium, or Light Duty ................................................................ 19

5.3.5 Manufacturing Materials, Processes, and Technologies .................... 20

5.3.6 Design ......................................................................................................... 22

5.3.7 Certifications .............................................................................................. 22

5.3.8 Capability Analysis .................................................................................... 24

5.4 Regional Distribution ........................................................................................ 26

5.5 Markets .............................................................................................................. 27

5.5.1 Market Segments Served......................................................................... 27

5.5.2 Geographic Reach .................................................................................. 28

5.5.3 Outlook ....................................................................................................... 29

5.5.4 Market Barriers ........................................................................................... 31

5.6 Transportation Infrastructure ........................................................................... 31

5.6.1 Land ............................................................................................................ 31

5.6.2 Sea .............................................................................................................. 32

5.7 Sector Development ....................................................................................... 33

6 Human Resources Profile..................................................................................... 35

6.1 Human Resource Practices ............................................................................ 35

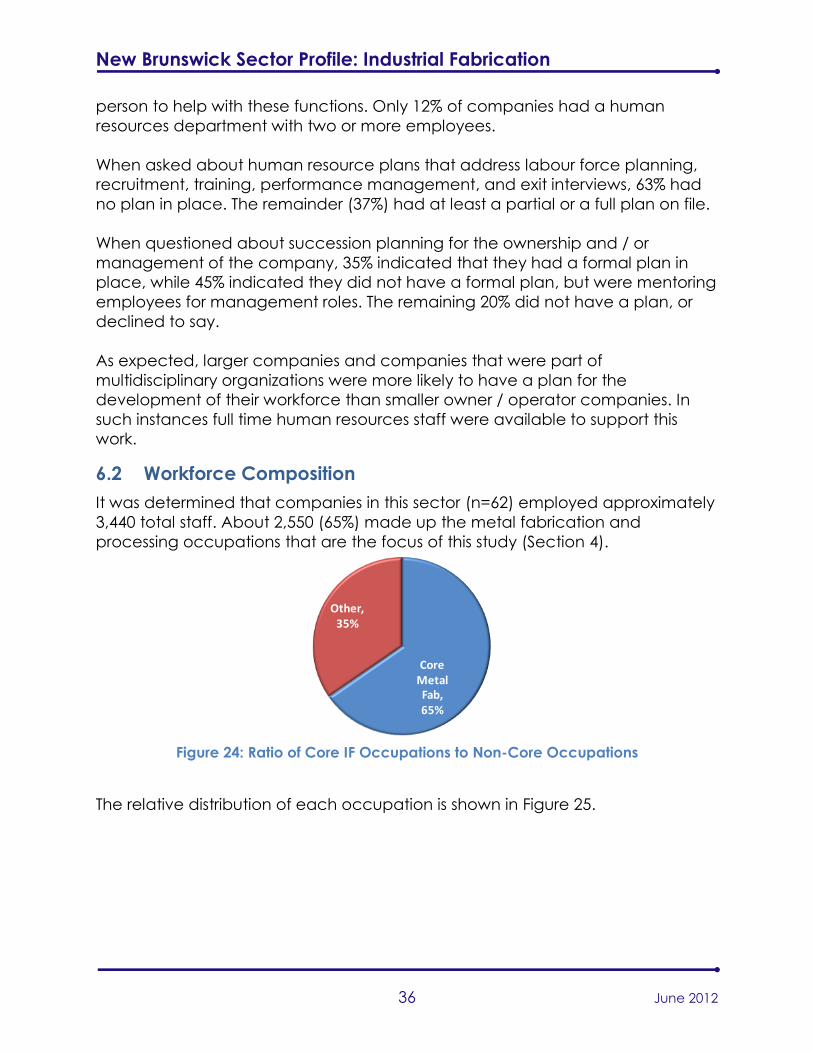

6.2 Workforce Composition .................................................................................. 36

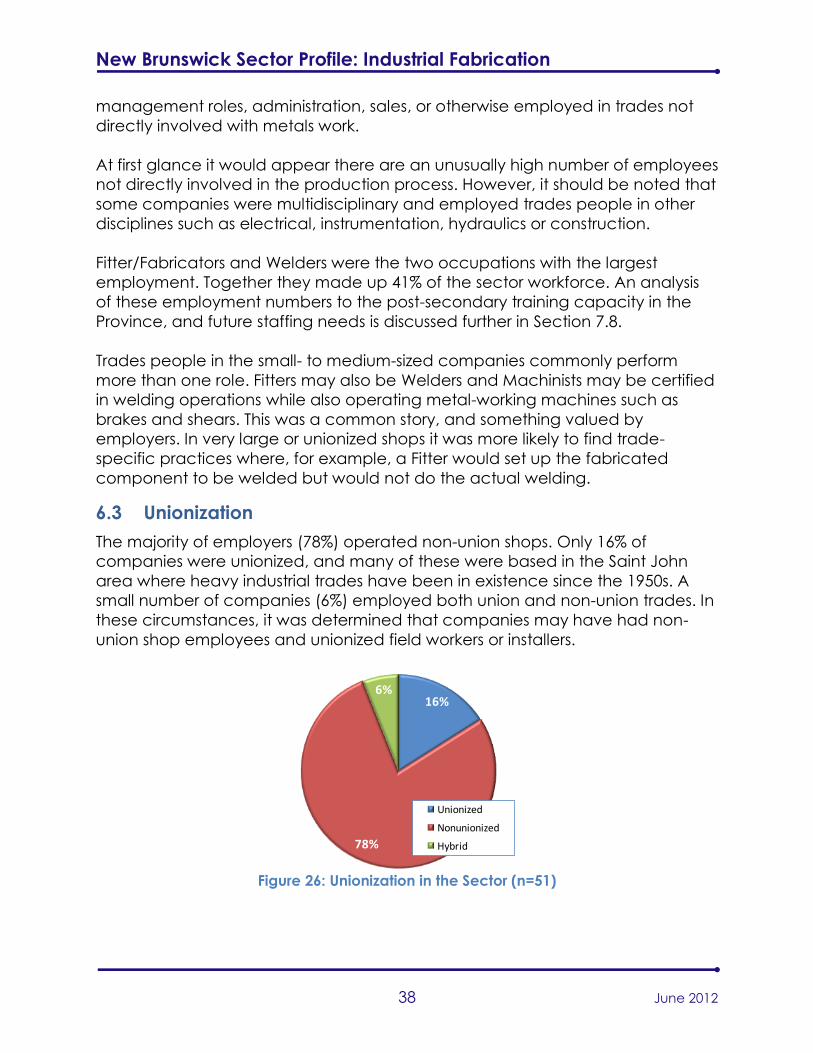

6.3 Unionization ....................................................................................................... 38

6.4 Wages ................................................................................................................ 39

6.5 Demographics .................................................................................................. 40

New Brunswick Sector Profile: Industrial Fabrication

ii June 2012

6.6 Future Hiring Plans ............................................................................................ 41

6.7 Staffing and Hiring Issues ................................................................................. 43

6.8 Recruitment Methods ...................................................................................... 43

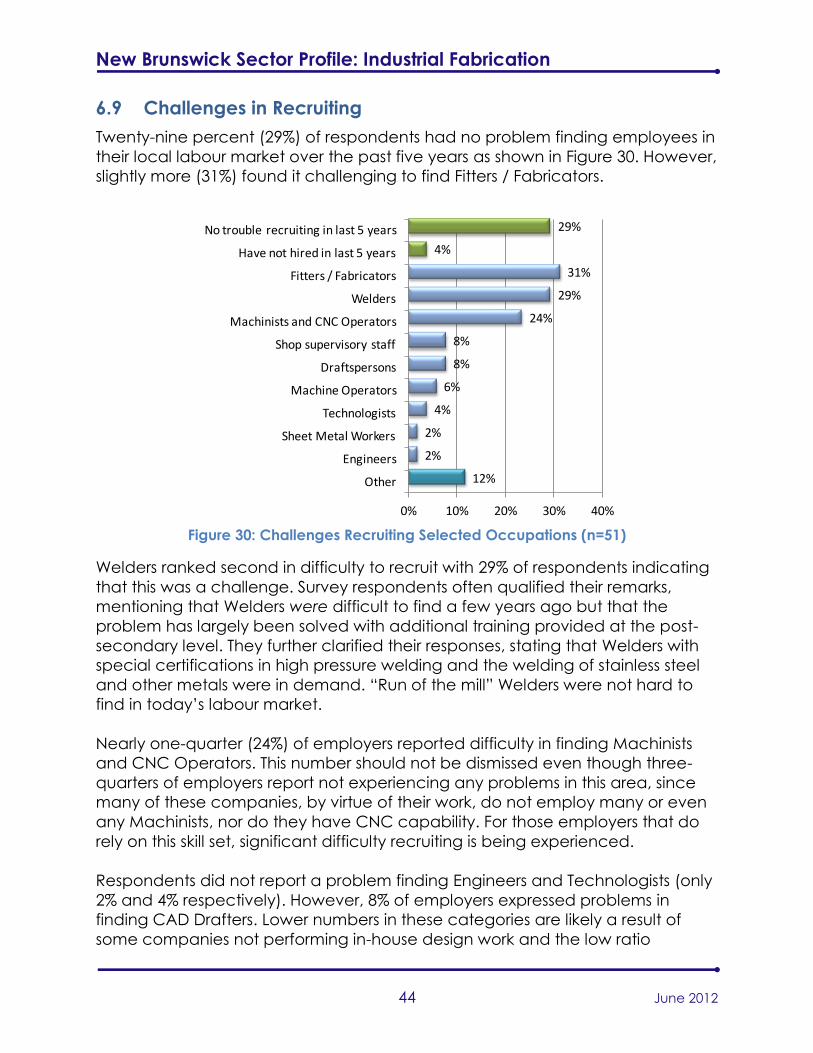

6.9 Challenges in Recruiting ................................................................................. 44

6.10 Skill Deficiencies with New Hires ..................................................................... 45

6.11 Needed Skills for the Future ............................................................................ 46

7 Training Capacity................................................................................................. 47

7.1 Defining Educational Capacity in a Time of Change ................................ 47

7.2 Primary Trades Utilized in the Sector .............................................................. 47

7.3 Paths for New Entrants into the Fabrication Trades .................................... 49

7.4 New Brunswick Trades Colleges ..................................................................... 50

7.4.1 NBCC .......................................................................................................... 51

7.4.2 CCNB .......................................................................................................... 52

7.4.3 BayTech College ....................................................................................... 52

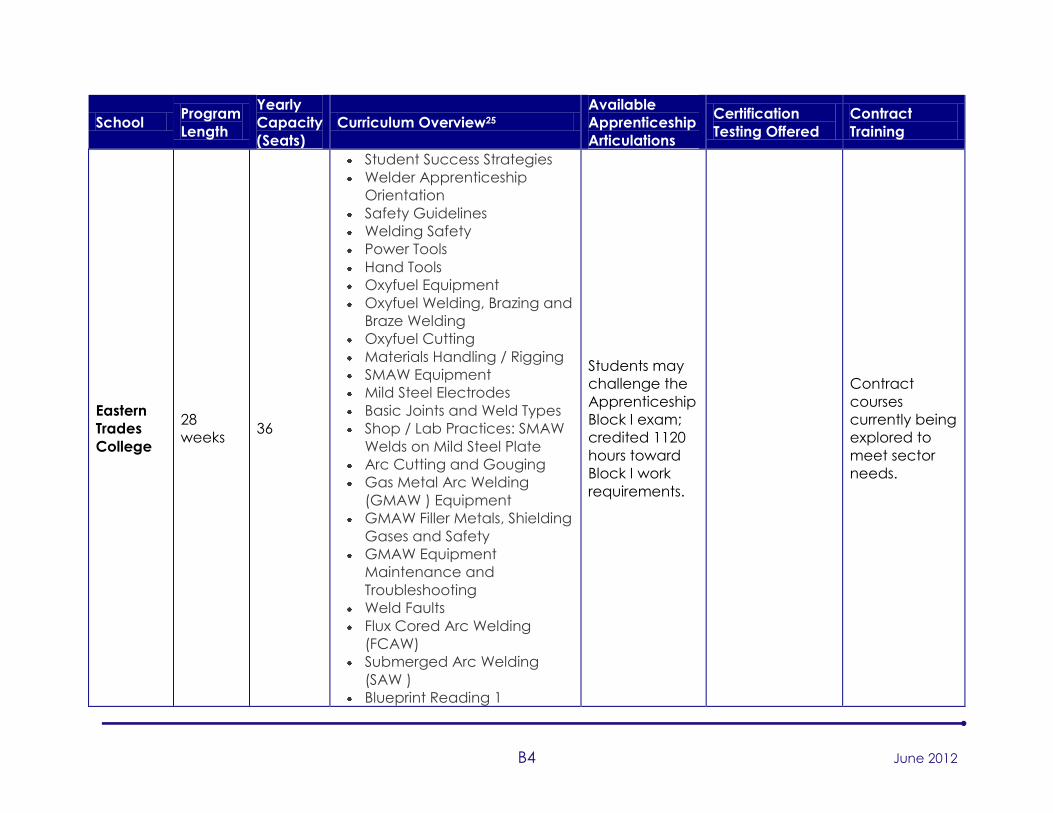

7.4.4 Eastern Trades College ............................................................................ 53

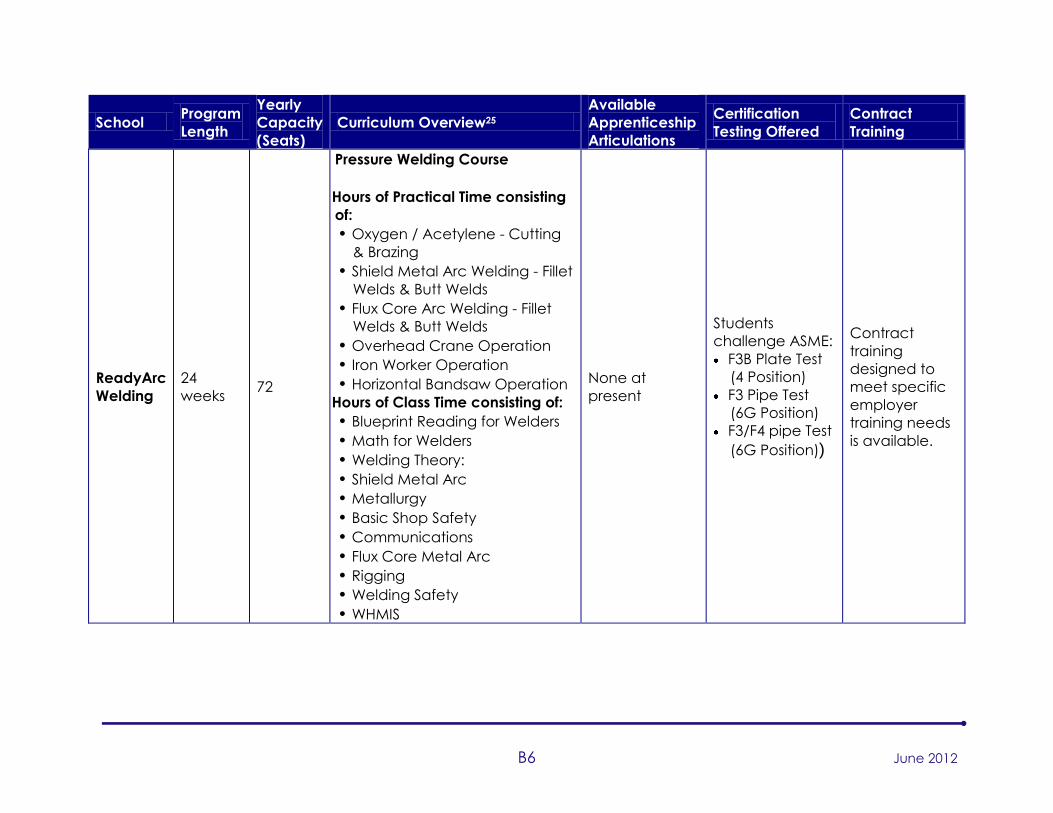

7.4.5 ReadyArc Welding ................................................................................... 54

7.5 Atlantic Canada Public Trades Colleges ..................................................... 54

7.6 Other Canadian Trades Colleges ................................................................. 55

7.6.1 Welding programs .................................................................................... 56

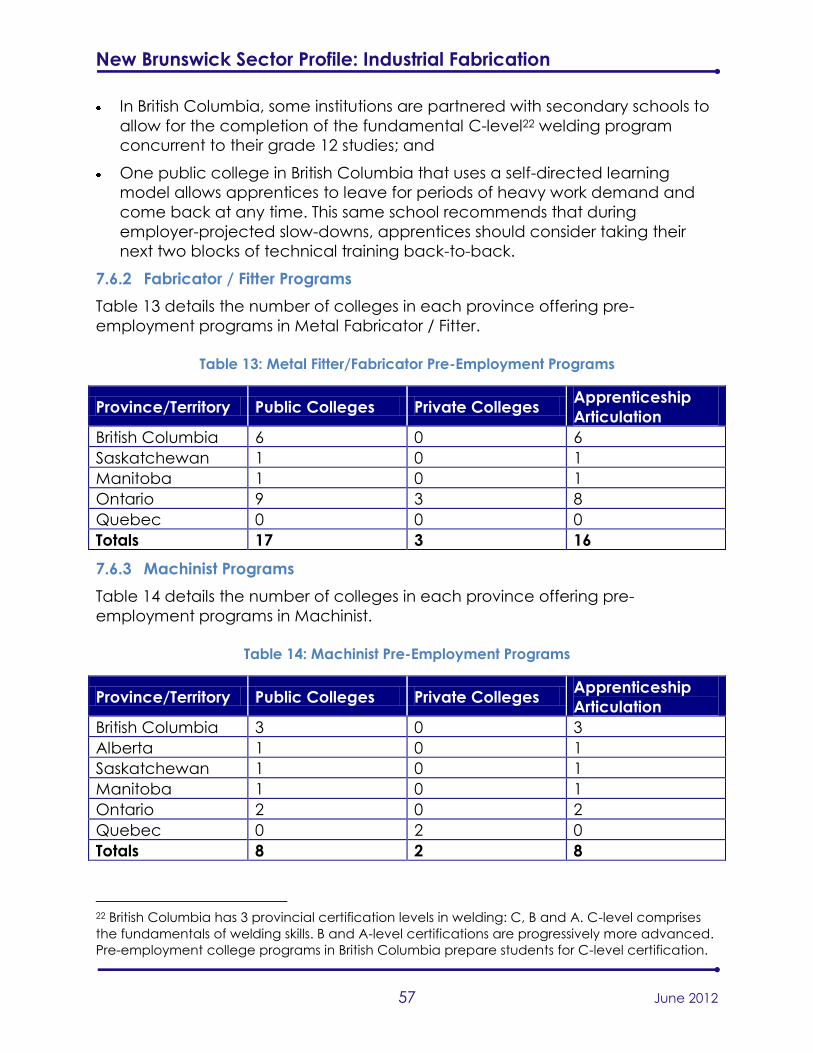

7.6.2 Fabricator / Fitter Programs ..................................................................... 57

7.6.3 Machinist Programs .................................................................................. 57

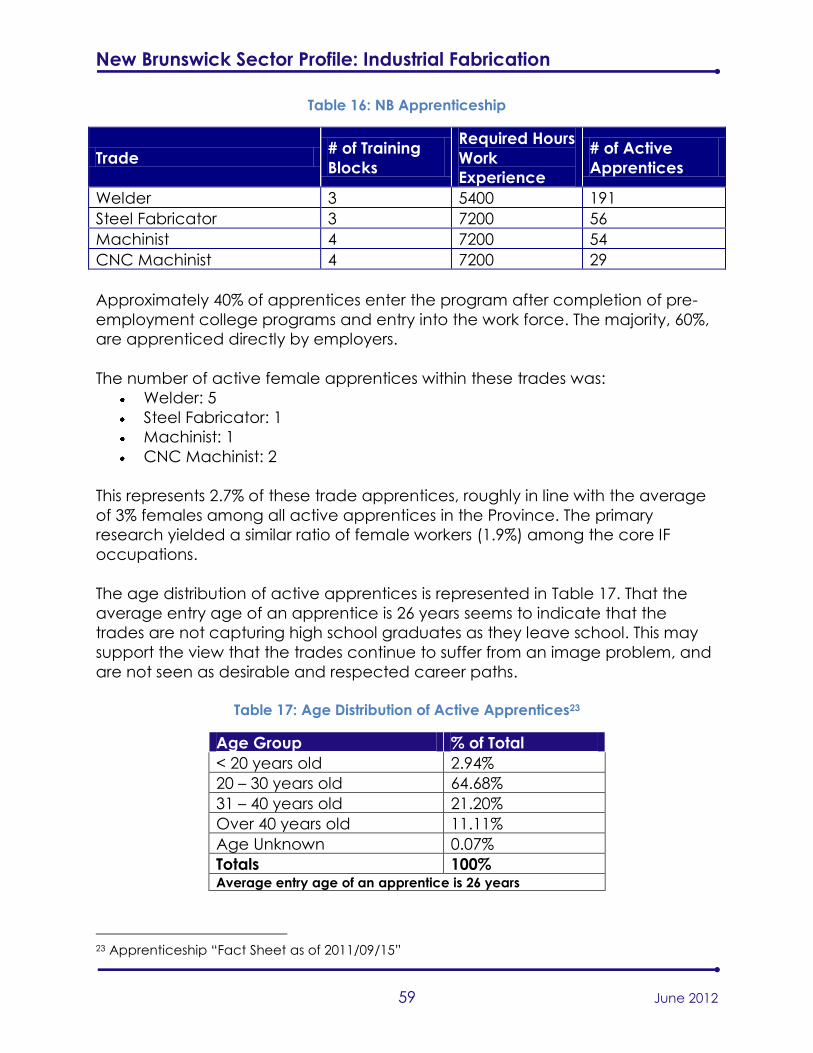

7.7 New Brunswick Apprenticeship ...................................................................... 58

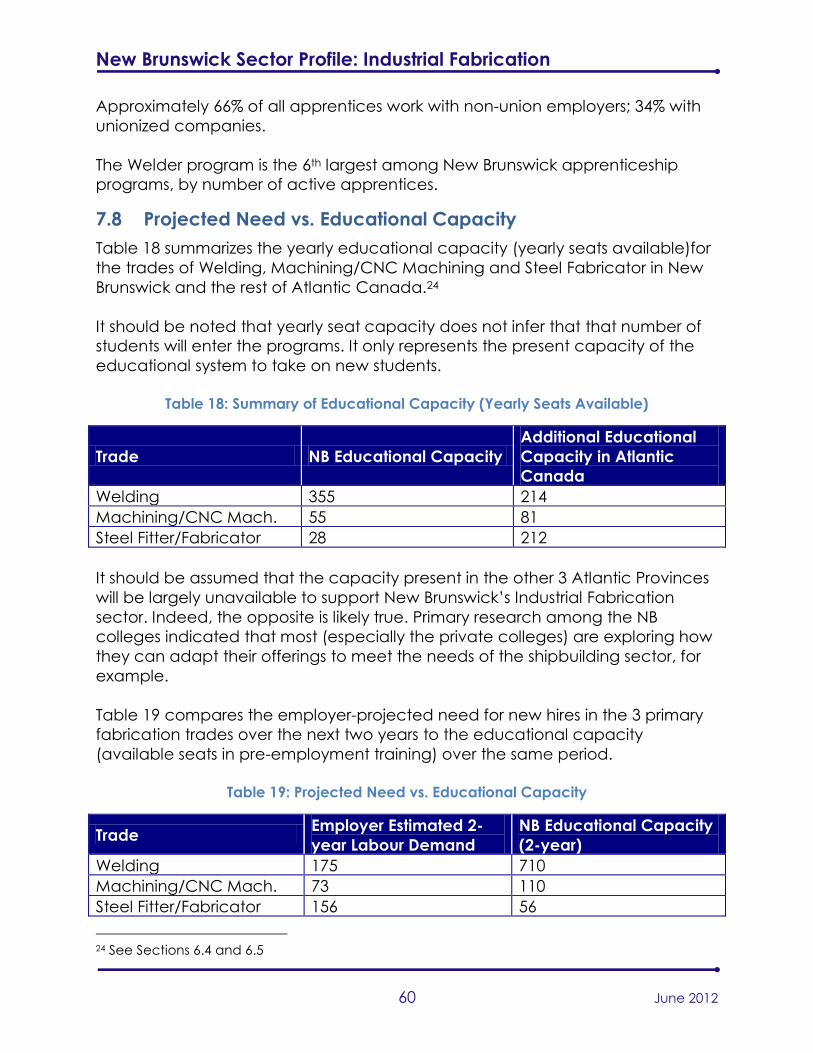

7.8 Projected Need vs. Educational Capacity .................................................. 60

7.9 Summary of Findings Regarding Educational Capacity ........................... 61

Appendix A: Acronyms ................................................................................................ 1

Appendix B: Catalog of College Programs ................................................................ 1

B1.1 Welding Pre-Employment Programs .................................................................. 1

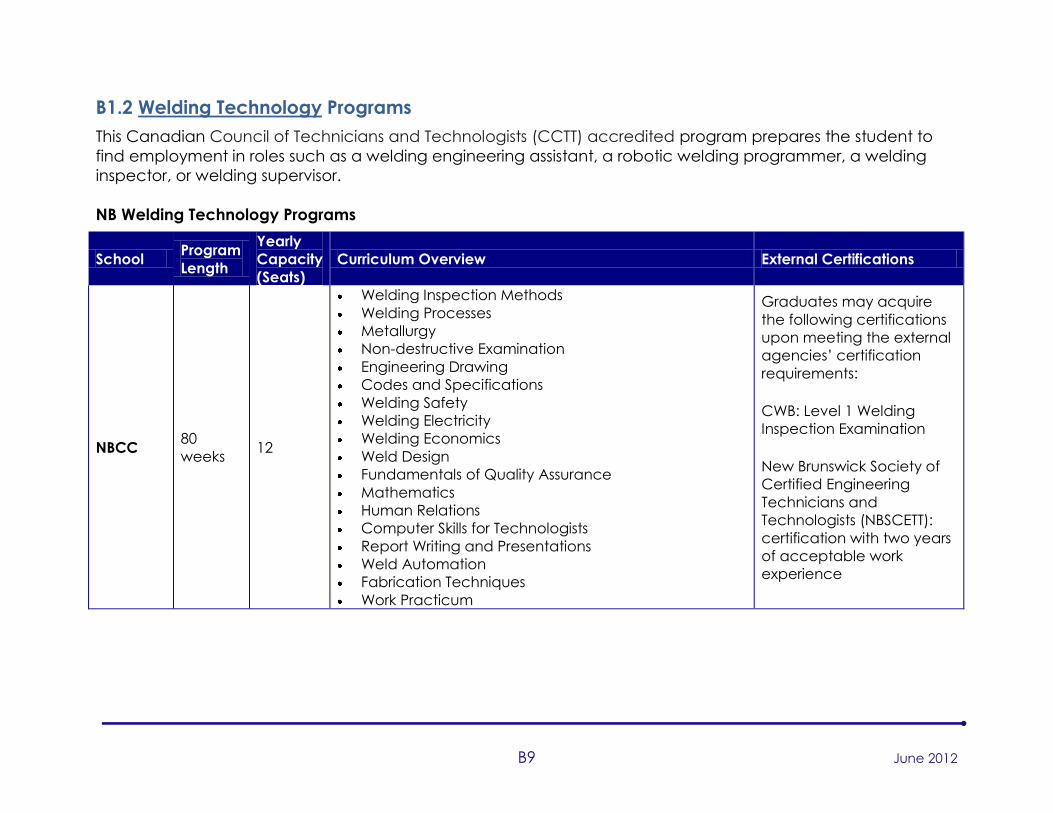

B1.2 Welding Technology Programs ........................................................................... 9

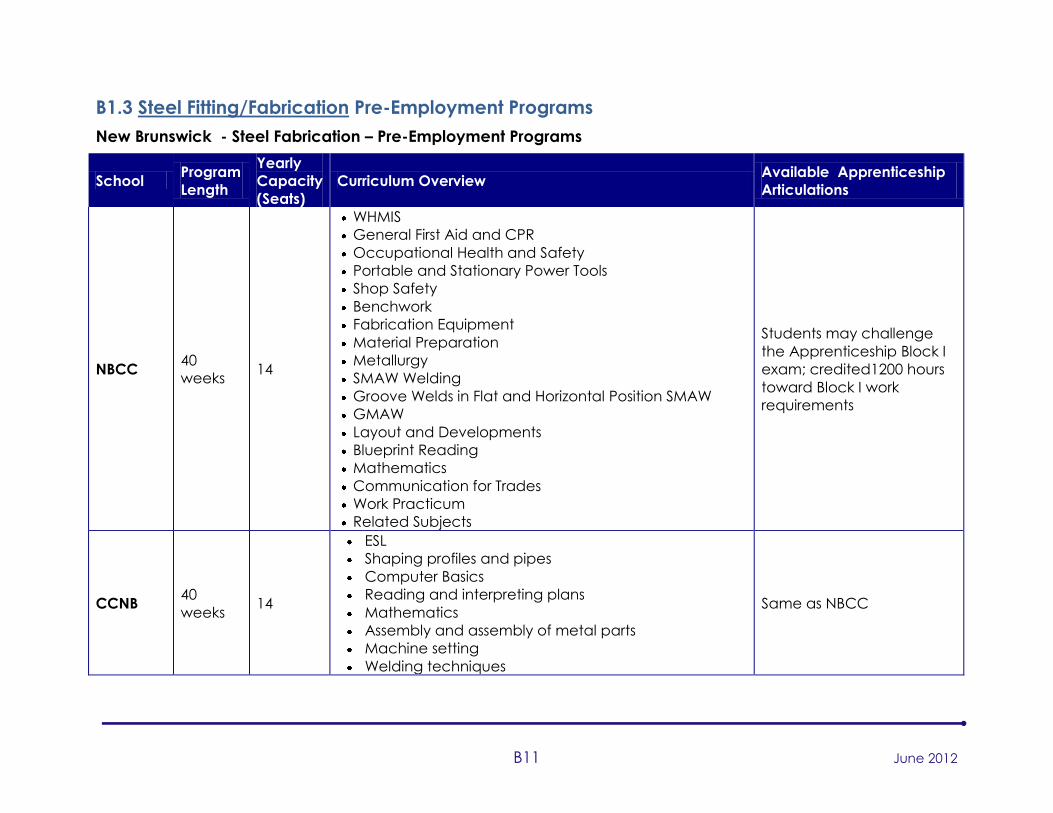

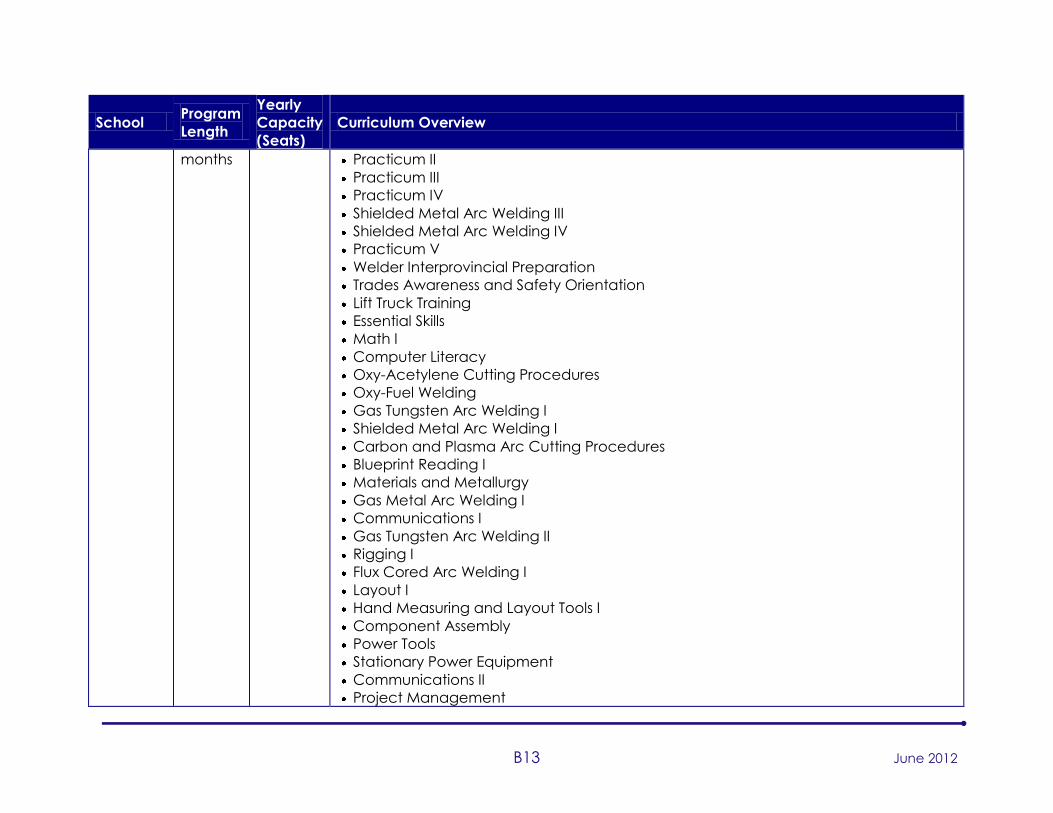

B1.3 Steel Fitting/Fabrication Pre-Employment Programs ..................................... 11

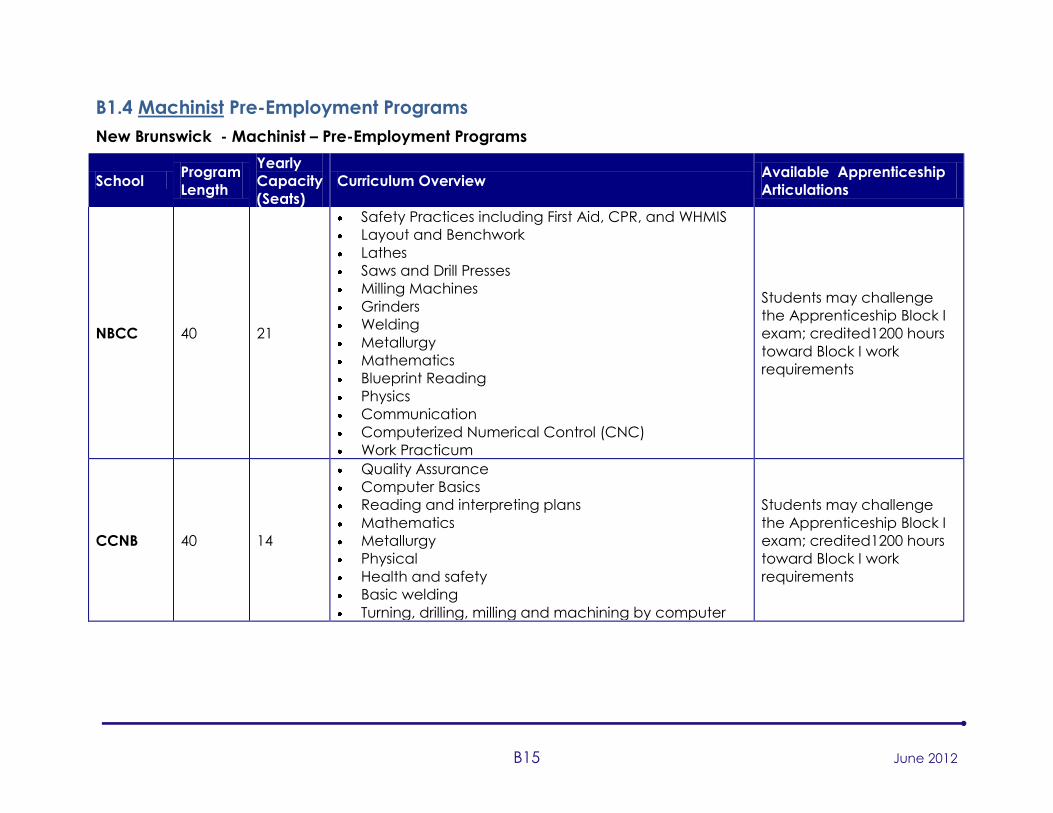

B1.4 Machinist Pre-Employment Programs .............................................................. 15

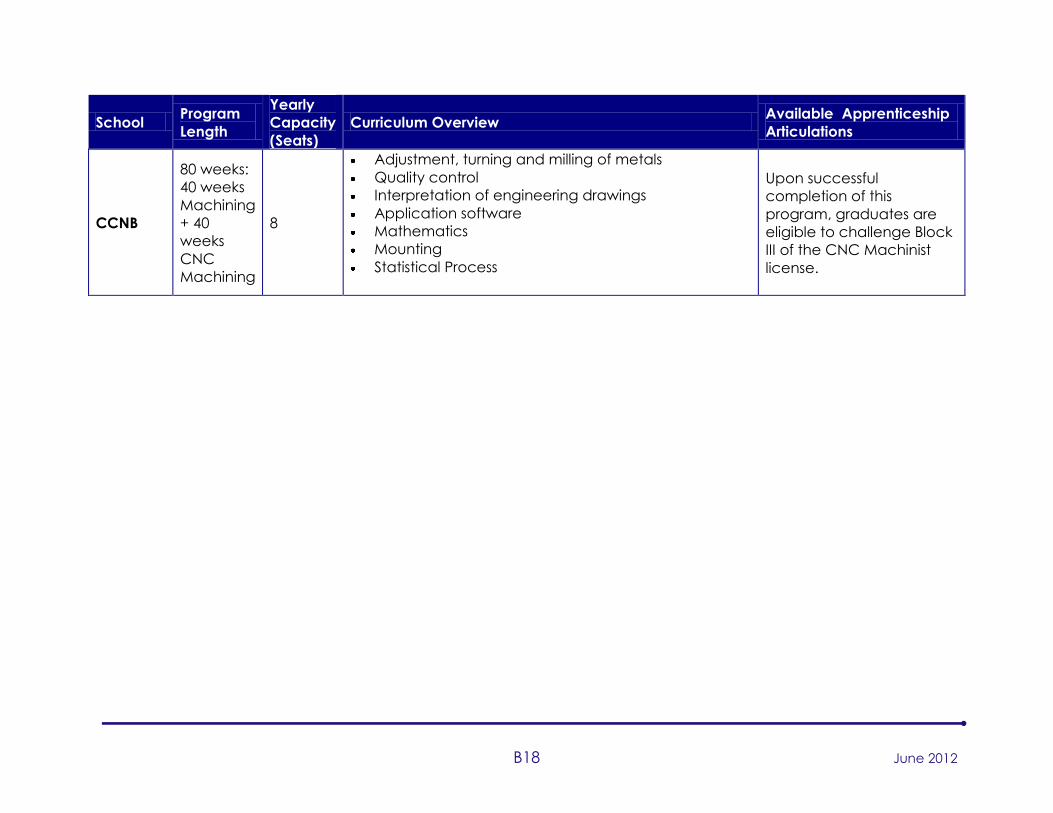

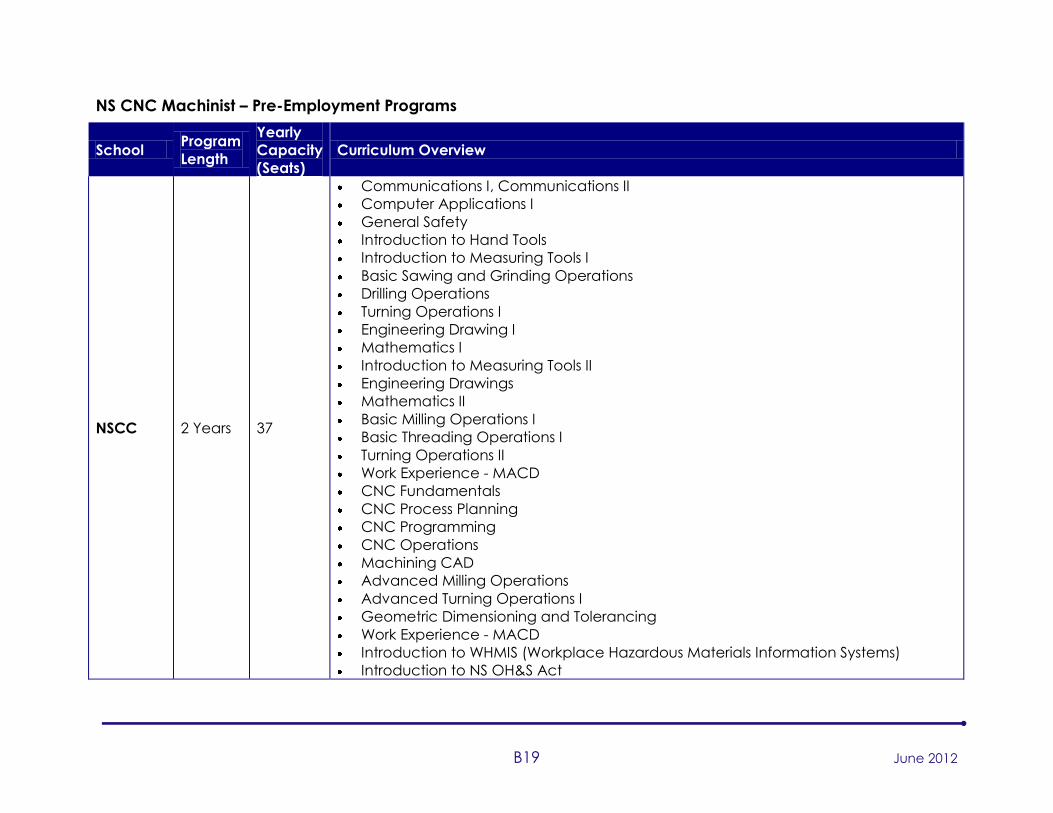

B1.5 CNC Machinist Pre-Employment Programs .................................................... 17

List of Tables

Table 1: Manufacturing Sector and Metal Working Subsector (NB 2009).............. 14

Table 2: Capability Analysis Assessment Criteria ........................................................ 24

Table 3 : Selected Comparison of Survey Responses To COPS Data ..................... 37

Table 4: Wage Rates Reported by Respondents (n=51) .......................................... 39

Table 5: Wage Rates From “Working in Canada – HRSDC” .................................... 39

Table 6: NBCC Yearly Seat Capacity for Primary Fabrication Trades ..................... 51

Table 7: CCNB Yearly Seat Capacity for Primary Fabrication Trades ..................... 52

Table 8: BayTech Pre-Employment Welding Program Seat Capacity ................... 53

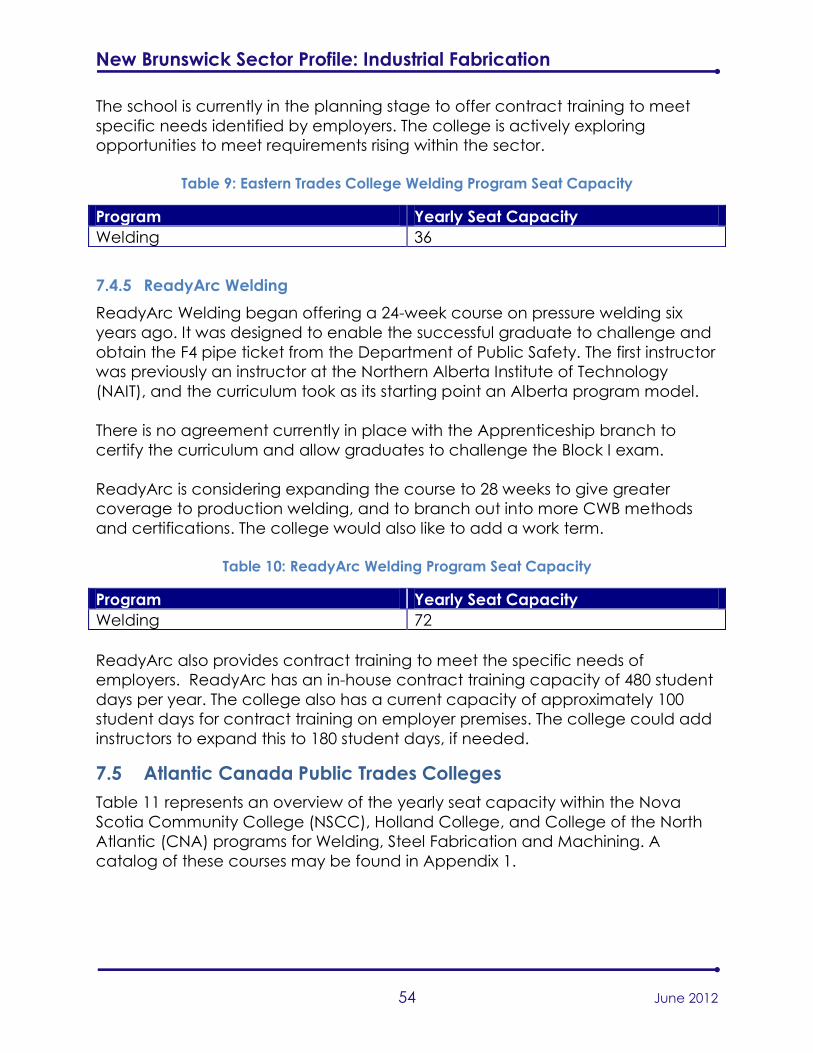

Table 9: Eastern Trades College Welding Program Seat Capacity ........................ 54

New Brunswick Sector Profile: Industrial Fabrication

iii June 2012

Table 10: ReadyArc Welding Program Seat Capacity ............................................. 54

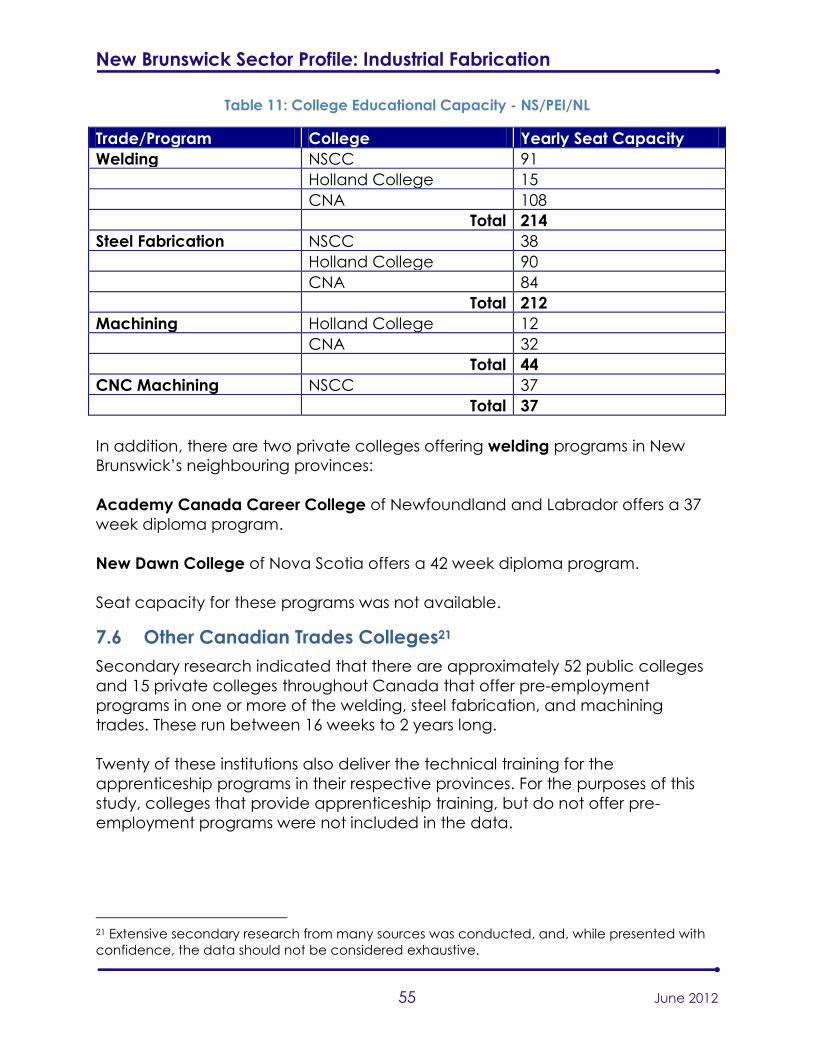

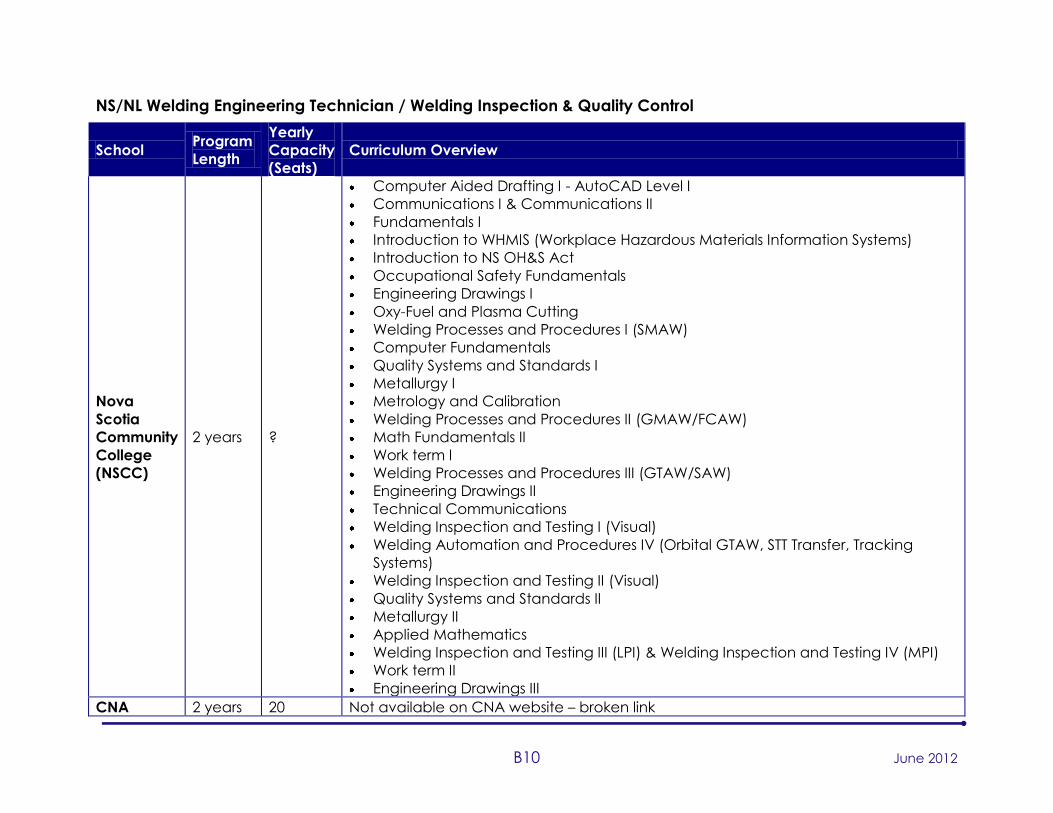

Table 11: College Educational Capacity - NS/PEI/NL ............................................... 55

Table 12: Welding Pre-Employment Programs in Canada ....................................... 56

Table 13: Metal Fitter/Fabricator Pre-Employment Programs .................................. 57

Table 14: Machinist Pre-Employment Programs ......................................................... 57

Table 15: CNC Machinist Pre-Employment Programs ............................................... 58

Table 16: NB Apprenticeship ......................................................................................... 59

Table 17: Age Distribution of Active Apprentices ...................................................... 59

Table 18: Summary of Educational Capacity (Yearly Seats Available) ................. 60

Table 19: Projected Need vs. Educational Capacity................................................ 60

List of Figures

Figure 1: Regional Distribution of the New Brunswick Labour Force ....................... 13

Figure 2: PWC Modular Fabrication Supply Chain Model ........................................ 15

Figure 3: Structure of the Industrial Fabrication Sector in New Brunswick .............. 16

Figure 4: NAICS Classification of New Brunswick IF Companies .............................. 17

Figure 5: Make Up of IF Sector by Establishment Size Categories (n=62) ............... 18

Figure 6: Size of Manufacturing Space in Square Feet (n=51) ................................. 18

Figure 7: Shop Crane Lifting Capacity of NB IF Companies (n=51) ........................ 19

Figure 8: Self-assessment of Light, Medium, and Heavy Duty Capability (n=51) .. 20

Figure 9: Metals Routinely Used for Manufacture (n=51) .......................................... 20

Figure 10: Use of Advanced Manufacturing Technologies (n=51) ......................... 21

Figure 11: Welding Certifications (n=51) ...................................................................... 23

Figure 12: Quality Program Certifications (n=50) ....................................................... 24

Figure 13: Capability Analysis of New Brunswick IF Companies Surveyed ............. 25

Figure 14: Location of IF Companies in New Brunswick ............................................ 26

Figure 15: Regional Distribution of IF Establishments and Employment (n=62) ...... 27

Figure 16: Market Segments Accounting for 10% of Corporate Revenue (n=51) 27

Figure 17: Top Three Markets by Value of Revenue .................................................. 28

Figure 18: Largest Portion of Revenue – By Geography (N=50) .............................. 29

Figure 19: New Brunsiwck Metal Working Sector International Export History ....... 29

Figure 20: Perception of Past and Future Economic Performance of the Sector 30

Figure 21: Diversification Markets Targeted By Respondents (n=34) ...................... 30

Figure 22: Land Transportation (Road and Rail) Infrastructure in New Brunswick . 32

Figure 23: New Brunswick Ports ..................................................................................... 33

Figure 24: Ratio of Core IF Occupations to Non-Core Occupations ...................... 36

Figure 25: Employment of Selected IF Occupations (n=51) ..................................... 37

Figure 26: Unionization in the Sector (n=51) ................................................................ 38

Figure 27: Age Distribution of IF Core Fabrication Occupations (n=50) ................. 40

Figure 28: Vacant Positions Reported by Respondents (n=49) ................................ 42

Figure 29: Respondent Hiring Expectations in the Next 2 Years (n=49) .................. 42

Figure 30: Challenges Recruiting Selected Occupations (n=51) ............................ 44

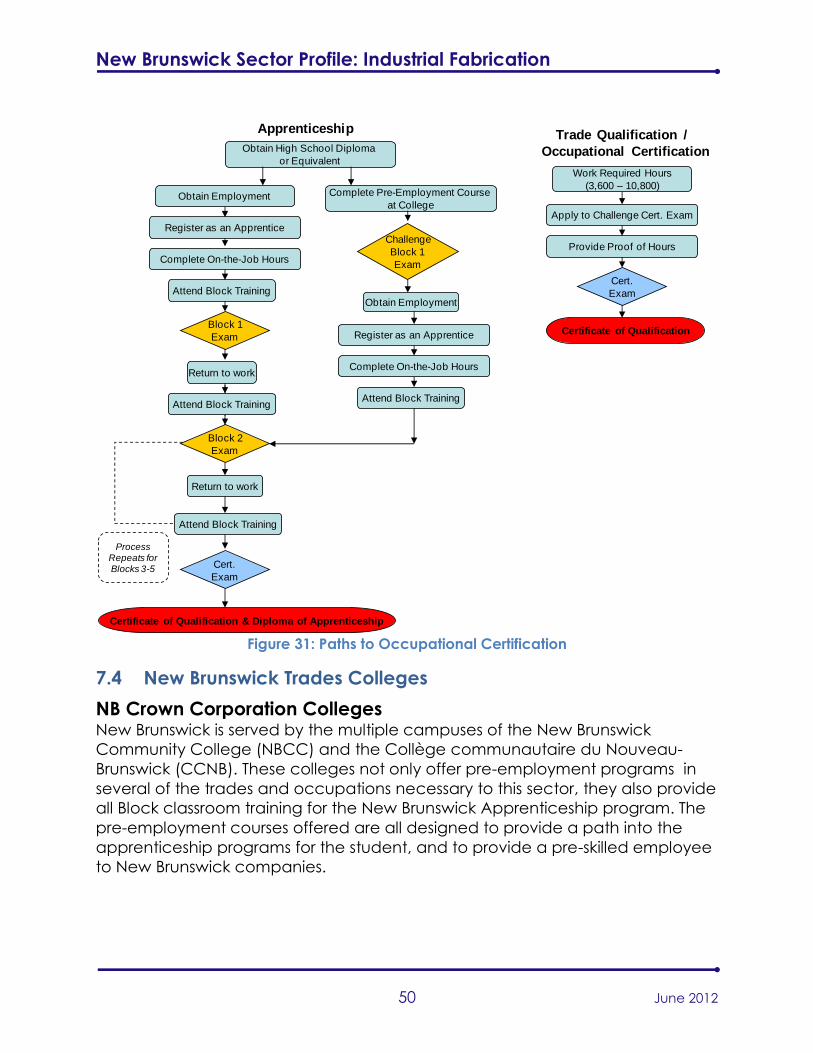

Figure 31: Paths to Occupational Certification .......................................................... 50

New Brunswick Sector Profile: Industrial Fabrication

1 June 2012

1 Executive Summary

The New Brunswick Industrial Fabrication (IF) sector is comprised of metal

fabrication companies that manufacture industrial equipment or systems to

support the construction of large industrial projects common in industries such as

petrochemical, mining, pulp and paper, and utilities. The sector holds many

opportunities to grow the New Brunswick economy, yet also holds many

challenges in meeting workforce and other needs. This report provides a profile

of the sector based upon information gathered from secondary research as well

as interviews with 51 employers, six economic development agencies, and

every relevant training institution in the Province.

SECTOR PROFILE

The sector is made up of a relatively small but influential group of companies,

about 60 – 70, representing 80% of employment within the broader Metal

Working/Metal Fabrication sector (well over 250 companies). As such, the IF

sector employs approximately 10% of all people working in manufacturing, and

just less than 1% of the entire New Brunswick workforce. The study identified 62

New Brunswick companies as being “in-scope”.

From a global perspective, the New Brunswick IF sector is comprised primarily of

smaller companies. However, there are a number of companies capable of

pursuing major industrial projects on their own. A snapshot of sector capability

(capacity + expertise) in New Brunswick is shown below.

Exp

ert

ise

Capacity

New Brunswick Sector Profile: Industrial Fabrication

2 June 2012

This analysis attempts to identify, within the confines of the New Brunswick sector,

the relative position of industry players. To help put this in context, there are no

Engineering, Procurement and Construction (EPC) leaders in New Brunswick.

However, those companies residing in the upper right quadrant are well

positioned to become strategic partners to EPC firms who manage large

industrial mega projects and subcontract work (modular and otherwise) in this

region and beyond. Upper-right-quadrant companies also have the opportunity

to partner with each other, as well as with the skilled niche metals companies

that make up the sector supply chain in the province. All of these companies, as

well as the infrastructure and labour force supporting them, are key to New

Brunswick’s success in this sector.

Lifting capacity, facility size, and workforce size are major indicators of a

company’s ability to compete in the Industrial Fabrication sector. Approximately

73% of the companies identified employ less than 50 people, accounting for

only 23% of total sector employment. Conversely, just over one quarter of the

companies employed three quarters of the labour force. Only 4% of companies

operated facilities larger than 100,000 square feet, and only 10% reported lifting

capacity over 50 tons. These larger companies are typically upper right

quadrant companies that have both the capacity and expertise to compete

and lead in the pursuit of work from industrial mega projects.

The sector, as a whole, has extensively adopted advanced manufacturing

technologies. Almost all (92%) reported having Computer Aided Design (CAD)

software and over 60% reported having Computer Numerical Control /

Computer Aided Manufacturing (CNC/CAM) capabilities. Overall, 80% of IF

companies have the ability to offer clients design services on a routine basis -

over half (55%) using in-house resources, and 25% through contractual

relationships with external engineers, technicians, or design firms.

Shown below is the regional distribution of the 62 Industrial Fabrication

companies identified as “in-scope”. The “Campbellton – Miramichi” and the

“Saint John – St. Stephen” economic regions account for almost 50% of

establishments and almost 70% of sector employment, yet account for only 43%

of the total provincial labour force.

New Brunswick Sector Profile: Industrial Fabrication

3 June 2012

The mining industry is by far the primary source of revenue for most New

Brunswick IF companies. Not surprising, the construction, petrochemical, pulp

and paper, and utility industries are also major sources of revenue. Many

respondents qualified their responses indicating that revenue sources change in

relation to the economy. For example, companies that mainly serve the

petrochemical market today may have principally relied on the pulp and paper

market 10 years ago.

From a geographic market perspective, a significant portion of the companies

interviewed (60%) indicated that the largest portion of their revenue originated

from within New Brunswick (8% from Atlantic Canada, 22% from Canada,

and10% from international markets). It is important to note that this does not

imply that 60% of sector revenue originates from New Brunswick, but rather only

60% of the companies indicate that it is their major source. No major projects

have been announced, or are planned in New Brunswick. If this sector is to

grow, it must seek work from beyond New Brunswick borders. In fact, New

Brunswick stakeholders have identified significant and viable opportunities that

extend from northeastern Canada in the mining sector to southeastern USA in

the oil and gas sector.

5-9

10-49

50-250

250+

New Brunswick Sector Profile: Industrial Fabrication

4 June 2012

Collectively respondents viewed the past performance of the sector over the

last two years as being “somewhat strong” (average rating of 5.3 out of 9).

However, there was much greater optimism for the next 2-5 years where

respondents see performance appreciably increasing (average rating of 6.4 out

of 9). There is no single specific indicator or project that employers pointed to

that would improve business, but rather this positive outlook was a combination

of a recovering economy in the USA, shipbuilding in Nova Scotia, resource

extraction opportunities in northern Canada, and general entrepreneurial

enthusiasm.

A large percentage of respondents (69%) claim to have taken concrete steps to

diversify their markets although many struggled to identify specific capital

expenditures in this regard. It is not surprising, given the recent announcement of

the $25-billion Irving contract to build the next generation of combat ships, that

the majority of respondents (approximately 38% of those claiming diversification

efforts) identified shipbuilding as a diversification area. Despite this, mining

continues to be a market focus for companies. Aerospace and defence are

also high ranking target markets - likely fuelled by the shipbuilding buzz.

While individual companies may face a number of market barriers depending

upon their unique circumstances, there was really only one sector-specific

market barrier identified: access to free and open trade. This is a significant

hurdle since most opportunities in the sector, particularly if growth is to continue,

exist beyond the borders of New Brunswick. It was suggested that the bi-lateral

government agreements between Newfoundland and Labrador with the

Government of Nova Scotia and the Government of Canada are a major

barrier to New Brunswick companies wishing to pursue these regional markets.

Similarly, the union influence and control over construction sites in Quebec

creates challenges for New Brunswick companies that wish to build, ship, and

install modular components in that province. Impacted industry players suggest

that the Provincial government needs to continue to press this issue with other

provinces and the federal government.

Infrastructure, particularly sea ports, are very important to the sector when large

prefabricated industrial modules are required to be exported to distant markets.

Two of the larger Ports, Belledune and Saint John, have undertaken specific

efforts to support and pursue the sector in New Brunswick. In 2010 $13.2 million

was invested in the “Belledune Modular Fabrication Facility” to specifically

position the region to pursue this sector. In 2012 the facility welcomed its first

tenant. In the Saint John area it has been proposed to construct, at a cost of

approximately $6 million, a barge loading terminal to support companies

pursuing the sector. At this point, the project remains unfunded and advocates

continue to seek funding.

New Brunswick Sector Profile: Industrial Fabrication

5 June 2012

In terms of sector development, clustering activities have been initiated in both

the private and public domains in New Brunswick. In the public domain, a

“Provincial Modular Fabrication Committee” with representation that includes

the Department of Business New Brunswick has been established. In the private

sector, the Associated Manufacturing Marketing Group (AMMG) is a consortium

established to specifically pursue this sector. The organization represents six

private companies under one marketing umbrella to pursue business

development opportunities directly in the industrial fabrication sector.

HUMAN RESOURCES PROFILE

Investigation into workforce issues focused on the 21 occupations core to the IF

sector. These occupations were broadly categorized as: Welders, Fitters,

Machinists, Machine Operators, Labourers, Shop Supervisors, Technologists,

Drafters and Engineers. Excluded from the analysis were employees that worked

in management roles, administration, sales, or who were otherwise employed in

trades not directly involved with metals work.

The majority of employers (78%) operated with a non-unionized workforce. Only

16% of companies were unionized, and many of these were based in the Saint

John area where heavy industrial trades have been in existence since the 1950s.

A small number of companies (6%) employed both union and non-union trades.

Findings related to demographics were consistent to what would be expected

of a trade-intensive sector. Only 1.9% (43) of the workforce were female. Only

10% of companies reported employing landed immigrants, and in total only 10

(0.4%) were actually employed in the sector. Only one employer reported hiring

a single temporary foreign worker. Employers who engaged foreign and female

workers all reported positive experiences in relation to their skills and

performance. These underrepresented workforce segments could be key to

further developing the sector workforce.

Many employers did raise concerns about the aging workforce and out-

migration of workers (especially younger workers to Alberta) as being a

significant challenge. However, the survey data collected suggested that a

significant number of younger workers, proportionally similar to their older co-

workers, still remain in New Brunswick.

In terms of skill gaps, the majority of respondents (55%) reported that new

employees lacked the skills required to take on the duties of the workplace.

However, the deficiencies identified were more generic in nature (i.e. common

to many trades in many industries) and not specific to the IF sector. Similarly, very

few respondents identified any skill requirements “new to the sector”.

New Brunswick Sector Profile: Industrial Fabrication

6 June 2012

Fitter/Fabricators, Welders, and Machinists collectively made up 50% of the 2,250

workers employed in the core IF occupations. Wages for these occupations

exhibited a less than 10% variation across the trades; however senior employees

were paid 35-42% higher than their entry-level counterparts. Wages were

generally consistent, with a less than 10% variance, with national database

figures for the region. It was interesting to find that wages for Welders in the

northeastern region were over 20% higher than in the southeastern region, likely

due to the need to attract and retain skilled workers. As expected, wages in

Alberta were considerably higher for all trades.

The table below shows some of the key workforce characteristics provided by

survey respondents for the three occupations Fitters/Fabricators, Welders, and

Machinists.

Employment Current

Vacancies

% of Companies

Experienced

Difficulty Hiring

2-yr Hiring

Expectations

Fitter/Fabricator 511 29 31% 175

Welder 431 26 29% 156

Machinist 157 18 24% 73

TRAINING CAPACITY

The annual seat capacity of post-secondary training institutions in New

Brunswick, and the rest of Atlantic Canada for the Fitter/Fabricator, Welder, and

Machinist trades is shown in the table below.

NB Colleges

Annual

Capacity

Combined

2-Year

Capacity

Other Atlantic

Colleges Annual

Capacity

Combined

2-Year

Capacity

We

ldin

g

NBCC 95

710

NSCC 91

428 CCNB 52 Holland College 15 BayTech 100 CNA 108 Eastern 36

Ready Arc 72

Fitte

r /

Fa

br.

NBCC 14 56

NSCC 38 424 CCNB 14 Holland College 90

CNA 84

Ma

ch

inis

t

Trad. NBCC 21

110

Holland College 12

162 CCNB 14 CNA 32

CNC NBCC 12 NSCC 37 CCNB 8

New Brunswick Sector Profile: Industrial Fabrication

7 June 2012

The “combined 2-year capacity” values were simply calculated by doubling the

annual capacity values at time of writing and do not take into account any

expansion or contraction of program seats. Assuming that the capacity in the

other three Atlantic Provinces would be largely unavailable to the New

Brunswick Industrial Fabrication sector, because of demands outside of New

Brunswick, there is a potential short-fall in educational capacity required to

meet the employer-projected need for Fitters/Fabricators.

Economic development advocates within the province naturally hold different

perspectives on the scope of the opportunity, limitations and labour force issues

faced by New Brunswick in developing the IF sector and modular fabrication

subsector. In southern New Brunswick, the need for a barge terminal is top

priority. In northeastern New Brunswick, attracting and retaining skilled labour

and the need to close deals with EPC players are top priorities.

New Brunswick Sector Profile: Industrial Fabrication

8 June 2012

2 Introduction

2.1 Purpose and Scope

Industrial Fabrication has been identified as a strategic sector in New Brunswick1.

Through the New Brunswick Career Development Action Group (NBCDAG),

InPro Solutions was commissioned to study and develop a fact-based profile of

the Industrial Fabrication (IF) sector with a focus on the metal working labour

force.

The study was intended to provide information that can be used by

stakeholders, policy makers, and training institutions to support their respective

goals and objectives.

The scope of the study is limited to companies participating in the Industrial

Fabrication (IF) sector as explicitly defined in Section 4. In addition, analysis is

confined to the geography and issues faced by the sector in the province of

New Brunswick.

2.2 Objectives

The overall objective of the study was to provide a detailed sector profile, with a

focus on the labour market, of the Industrial Fabrication sector in New Brunswick.

To support this, four sub-objectives were identified:

1. Develop a clear definition of the sector, followed by an identification of

which companies in New Brunswick fall within the sector;

2. From secondary data sources, develop a summary profile of the sector (i.e.

number of companies operating in this sector, those not in the sector but

which employ similarly-skilled workers, the size of the workforce in this sector,

revenues, etc.);

3. Conduct a survey to gather detailed information about the workforce of this

sector (age, occupation, skills, education, etc.), and skills they will require to

work in this sector in the near to medium-term future (2 to 5 years); and

4. Conduct a review of the educational capacity for skills related to this sector

in the province, and in a less comprehensive manner, the rest of Canada.

3 Methodology

Study methodology was based on a combination of both primary and

secondary research activities as described below. The focus however was on

1 Department of Business New Brunswick, (December 2011). 2010-2011 Annual report. Fredericton

NB: Department of Business New Brunswick.

New Brunswick Sector Profile: Industrial Fabrication

9 June 2012

primary research efforts where a census survey of Industrial Fabrication

companies was intended.

3.1 Primary Research

3.1.1 Contact List

One of the greatest project challenges was the development of a reliable

contact list. Because a census survey was intended, great efforts were made in

an attempt to ensure that all “in-scope” companies were captured.

The starting point was a composite list provided by LMAB which was compiled

from a number of sources including Service Canada and the Department of

Business New Brunswick (BNB). The list was then augmented with:

1. Canadian Welding Bureau (CWB) (n=109): Downloaded from the CWB

website listing all New Brunswick organizations with certification

(downloaded January 2012).

2. Yellow Pages (n=63): An online search for New Brunswick companies using

“welding” as a keyword (downloaded January 2012). A manual

elimination of duplicate companies was conducted before integrating

into the list.

The Master Contact List was thus created when all of the sources identified

above were merged and “cleaned” into a single worksheet (n=329). All

information for a particular company, as listed by the multiple sources, was

integrated into a single record.

Through an iterative process involving both secondary (websites, directory

listings, Google Maps, etc.) and primary (phone interviews) research efforts, the

Master Contact List was filtered for “in-scope” companies (n=62). Inclusion

criteria included:

Company must be a manufacturer (ex. repair-only companies excluded);

Company must fit the sector definition;

Company must employ five or more staff; and

Company must still be in business.

In total 267 companies were determined to be out of scope based on these

criteria.

The Master Contact List was validated by cross-referencing it against recently

compiled reports related to the sector:

New Brunswick Sector Profile: Industrial Fabrication

10 June 2012

2010 PWC Report2 (x=43);

2011 New Brunswick Community College (NBCC) Report3 (x=49); and

2007 Metal Working Association of New Brunswick (NWANB) Directory4

(x=127).

Where appropriate, additional information related to an already captured “in-

scope” company was added to the spreadsheet. The “x=” notation in the

above list refers to the number of companies common to the respective list and

the Master Contact List. No additional “in-scope” companies were identified.

3.1.2 Interviews

To support interview activities, three discussion guides were designed for

telephone interview purposes. Once drafted, they were submitted for review

and approval by the project Steering Committee. They included:

1. Employer Survey (56 questions);

2. Economic Development Organizations (EDO)/Association Survey (20

questions); and

3. College/Training Institute Survey (14 questions).

Interviews were conducted by four interviewers, in English and French as

required, during the period of February-March 2012. In total 63 interviews were

completed:

1. Employers: 51 completed (82%)5, 8 refused to participate (13%), and 3

were unable to be reached (5%);

2. EDO/Associations: 6 completed (100%); and

3. College/Training Institutes: 6 completed (100%).

3.2 Secondary Research

Secondary research efforts contributed significantly to the study. Numerous

sources were accessed and are appropriately referenced throughout this

document. Research activities include:

o Literature search of related studies;

o General internet search for sector information, industry directories, etc.;

o Review of IF company websites;

o Statistics Canada data sources; and

o Industry Canada data sources.

2 PricewaterhouseCoopers LLP, (2010, October 20). Comparative benchmarking study – modular

fabrication facility. Beldune, NB: Enterprise Chaleur. 3 Mackellar Cunningham & Associates Ltd., (2012, February). Labour market analysis: metals

processing. Fredericton, NB: New Brunswick Community College. 4 The Metal Working Association of New Brunswick. 2006-2007 New Brunswick directory of metal

working companies. Moncton, NB: The Metal Working Association of New Brunswick 5 Two employers chose to complete the survey themselves - one on line, and the other by fax.

New Brunswick Sector Profile: Industrial Fabrication

11 June 2012

4 Sector Definition

The Industrial Fabrication sector is comprised of metal fabrication companies

that manufacture industrial equipment or systems to support the construction

and erection of large industrial projects in sectors such as petrochemical,

mining, pulp and paper, and utilities. A key capability of companies in this sector

is the ability to manufacture large “modular” components that can be

transported and integrated into the mega-project site. In this definition, these

firms are deemed to be “primary” metal fabricators for heavy industry and

generally have the capacity to supply modular fabricated products to large

industrial projects.

Also of interest, particularly in the New Brunswick context, are companies whose

focus is currently not in this sector, but have the capability in terms of

equipment, facilities, and workforce to supply to the sector. Also within this

categorization are smaller firms with unique capability to supply and

subcontract and thus round out the supply chain. Under this definition these

firms are deemed to be important suppliers to the sector, and are labelled as

“secondary” metal fabricators for heavy industry.

Common processes used in the sector involve the cutting, bonding, forming,

machining, and assembly of metal products – usually on a large scale.

Equally important to the definition is the exclusion of metal fabrication firms not

involved in such industrial projects. This includes companies that manufacture

products primarily for the commercial or consumer markets. Also not included

are companies with metal manufacturing capabilities not likely to be interested,

or skilled, in large industrial project work. For the purposes of this study these firms

are labelled as “non-industrial” metal fabricators.

Companies within scope, as defined above, typically supply to large

multinational organizations known as Engineering Procurement and

Construction (EPC) companies who usually lead these large industrial projects.

Using the North American Industry Classification System (NAICS 2007), the sector

is defined as encompassing companies classified according to the following 4-

digit industry groups:

1. 3323 Architectural and Structural Metals Manufacturing;

2. 3324 Boiler, Tank and Shipping Container Manufacturing;

3. 3327 Machine Shops, Turned Product, and Screw, Nut and Bolt

Manufacturing;

4. 3329 Other Fabricated Metal Product Manufacturing;

5. 3331 Agricultural, Construction and Mining Machinery Manufacturing;

6. 3332 Industrial Machinery Manufacturing;

New Brunswick Sector Profile: Industrial Fabrication

12 June 2012

7. 3334 Ventilation, Heating, Air-Conditioning and Commercial

Refrigeration Equipment Manufacturing;

8. 3336 Engine, Turbine and Power Transmission Equipment Manufacturing;

and

9. 3339 Other General-Purpose Machinery Manufacturing

While there are in the vicinity of 150 different occupations within this sector (as

defined above), the following occupations6 have been determined to be core

to the industry and are the focus of this study:

1. 2131 Civil Engineers

2. 2132 Mechanical Engineers

3. 2141 Industrial and Manufacturing Engineers

4. 2142 Metallurgical and Materials Engineers

5. 2231 Civil Engineering Technologists and Technicians

6. 2232 Mechanical Engineering Technologists and Technicians

7. 2233 Industrial Engineering and Manufacturing Technologists and

Technicians

8. 2253 Drafting Technologists and Technicians

9. 7211 Supervisors, Machinists and Related Occupations

10. 7231 Machinists and Machining and Tooling Inspectors

11. 7232 Tool and Die Makers

12. 7261 Sheet Metal Workers

13. 7262 Boilermakers

14. 7263 Structural Metal and Platework Fabricators and Fitters

15. 7264 Ironworkers

16. 7265 Welders and Related Machine Operators

17. 7266 Blacksmiths and Die Setters

18. 9511 Machining Tool Operators

19. 9514 Metalworking Machine Operators

20. 9516 Other Metal Products Machine Operators

21. 9612 Labourers in Metal Fabrication

4.1 About the Definition

The concept of an “Industrial Fabrication (IF)” sector was born out of the

modular fabrication trend that has been gaining traction in the construction

industry. New Brunswick stakeholders for this project had the intention of

focussing on “heavy industrial” development projects versus “building

envelope” construction projects. This focus swayed the emphasis toward metal

fabrication and away from other building materials such a precast concrete

and wood.

6 as defined by the National Occupation Classification (NOC 2006)

New Brunswick Sector Profile: Industrial Fabrication

13 June 2012

As such, some of the larger players in the IF sector using metal-working

processes, equipment, and skilled employees have become a hybrid of

classical manufacturing (NAICS 33) and construction (NAICS 23) companies.

Some companies integrate both shop (manufacturing) and field (construction)

staff under one homogenous entity, while others have created distinct divisions,

and yet others have created separate legal operating entities.

This report attempts to look at all companies serving this sector and looks at

some of the characteristics and skills issues affecting their entire metal-working

labour force.

5 Sector Profile

5.1 The New Brunswick Context

In order to gain an appreciation of the scope and impact of the Industrial

Fabrication sector it is first useful to understand the size and composition of the

New Brunswick economy.

In 2011, New Brunswick’s population was estimated to be 755,5007 with 619,400

individuals aged 15 and older making up the working age population. The total

labour force was comprised of 389,200 individuals where 352,000 found

employment, leaving 37,100 to the ranks of the unemployed8. The regional

distribution of the entire New Brunswick labour force is shown in Figure 1.

Figure 1: Regional Distribution of the New Brunswick Labour Force

7 Source: Statistics Canada, CANSIM, table 051-0001. Last modified: 2011-09-28. (accessed: 2012-

03-28) 8 Source: Statistics Canada. Table 282-0055 - Labour force survey estimates (LFS), by provinces,

territories and economic regions based on 2006 Census boundaries. (accessed: March 27, 2012)

20%

27% 23%

19%

11% Campbellton-Miramichi [1310]

Moncton-Richibucto [1320]

Saint John-St. Stephen [1330]

Fredericton-Oromocto [1340]

Edmundston-Woodstock [1350]

New Brunswick Sector Profile: Industrial Fabrication

14 June 2012

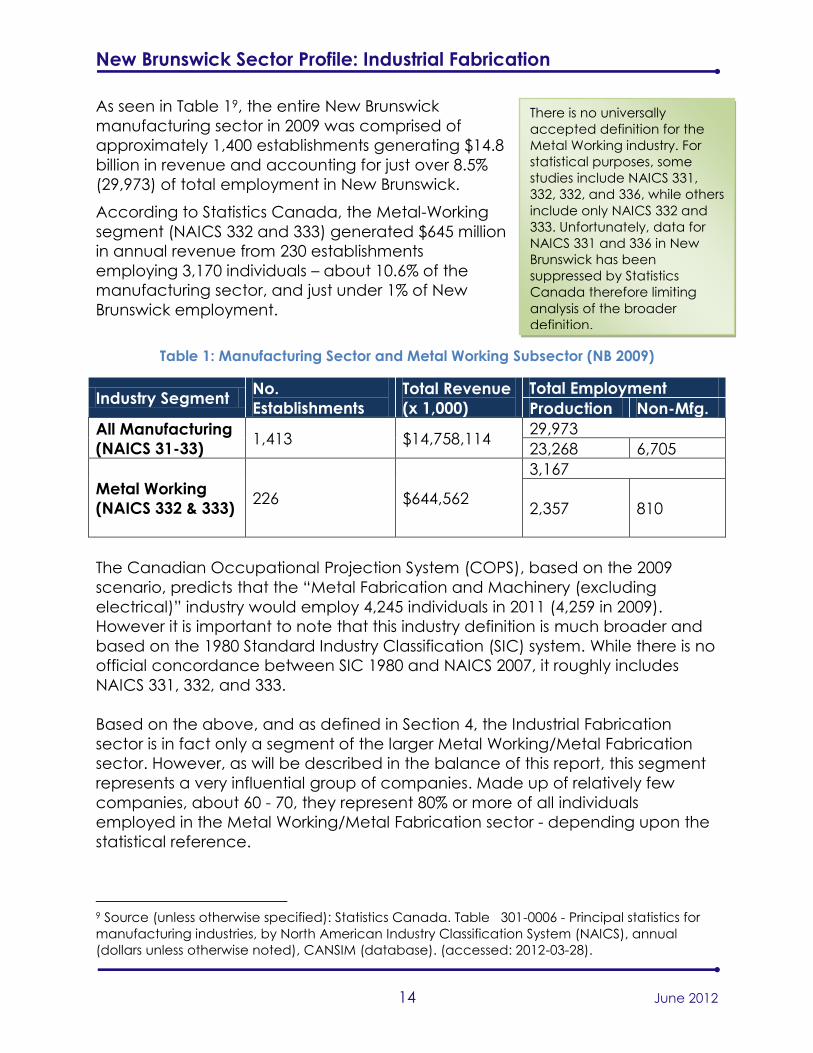

As seen in Table 19, the entire New Brunswick

manufacturing sector in 2009 was comprised of

approximately 1,400 establishments generating $14.8

billion in revenue and accounting for just over 8.5%

(29,973) of total employment in New Brunswick.

According to Statistics Canada, the Metal-Working

segment (NAICS 332 and 333) generated $645 million

in annual revenue from 230 establishments

employing 3,170 individuals – about 10.6% of the

manufacturing sector, and just under 1% of New

Brunswick employment.

Table 1: Manufacturing Sector and Metal Working Subsector (NB 2009)

Industry Segment No.

Establishments

Total Revenue

(x 1,000)

Total Employment

Production Non-Mfg.

All Manufacturing

(NAICS 31-33) 1,413 $14,758,114

29,973

23,268 6,705

Metal Working

(NAICS 332 & 333)

226 $644,562

3,167

2,357 810

The Canadian Occupational Projection System (COPS), based on the 2009

scenario, predicts that the “Metal Fabrication and Machinery (excluding

electrical)” industry would employ 4,245 individuals in 2011 (4,259 in 2009).

However it is important to note that this industry definition is much broader and

based on the 1980 Standard Industry Classification (SIC) system. While there is no

official concordance between SIC 1980 and NAICS 2007, it roughly includes

NAICS 331, 332, and 333.

Based on the above, and as defined in Section 4, the Industrial Fabrication

sector is in fact only a segment of the larger Metal Working/Metal Fabrication

sector. However, as will be described in the balance of this report, this segment

represents a very influential group of companies. Made up of relatively few

companies, about 60 - 70, they represent 80% or more of all individuals

employed in the Metal Working/Metal Fabrication sector - depending upon the

statistical reference.

9 Source (unless otherwise specified): Statistics Canada. Table 301-0006 - Principal statistics for

manufacturing industries, by North American Industry Classification System (NAICS), annual

(dollars unless otherwise noted), CANSIM (database). (accessed: 2012-03-28).

There is no universally

accepted definition for the

Metal Working industry. For

statistical purposes, some

studies include NAICS 331,

332, 332, and 336, while others

include only NAICS 332 and

333. Unfortunately, data for

NAICS 331 and 336 in New

Brunswick has been

suppressed by Statistics

Canada therefore limiting

analysis of the broader

definition.

New Brunswick Sector Profile: Industrial Fabrication

15 June 2012

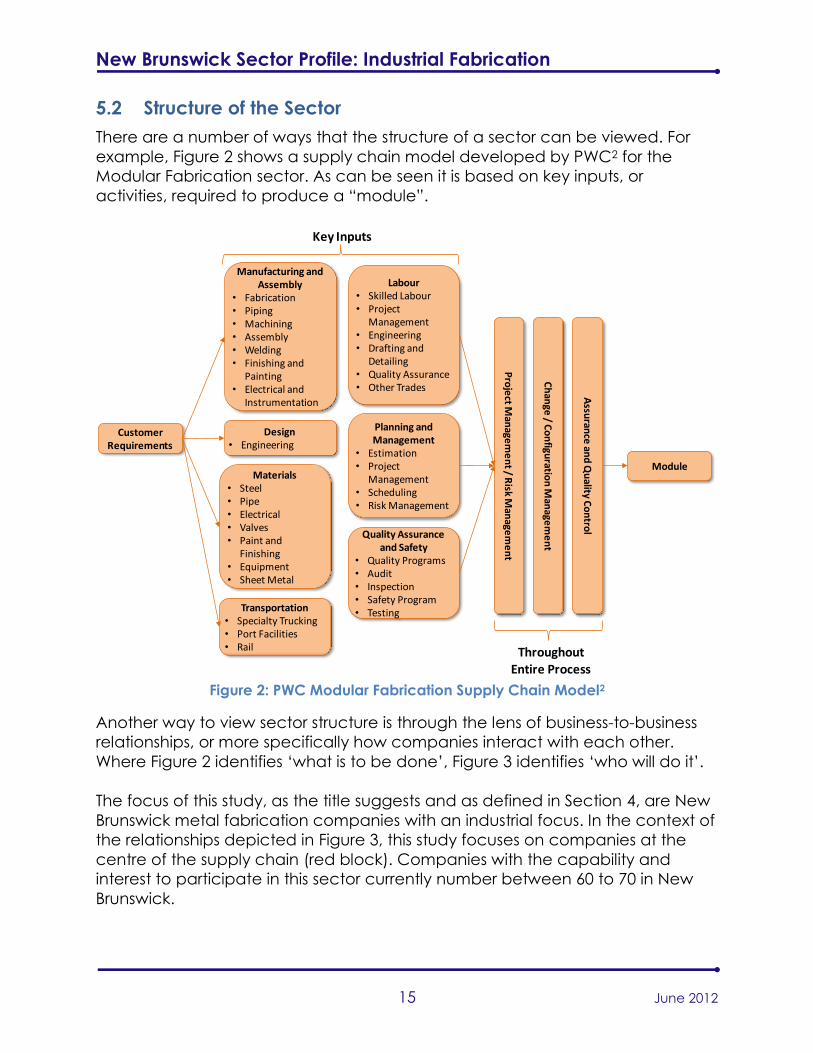

5.2 Structure of the Sector

There are a number of ways that the structure of a sector can be viewed. For

example, Figure 2 shows a supply chain model developed by PWC2 for the

Modular Fabrication sector. As can be seen it is based on key inputs, or

activities, required to produce a “module”.

Figure 2: PWC Modular Fabrication Supply Chain Model2

Another way to view sector structure is through the lens of business-to-business

relationships, or more specifically how companies interact with each other.

Where Figure 2 identifies ‘what is to be done’, Figure 3 identifies ‘who will do it’.

The focus of this study, as the title suggests and as defined in Section 4, are New

Brunswick metal fabrication companies with an industrial focus. In the context of

the relationships depicted in Figure 3, this study focuses on companies at the

centre of the supply chain (red block). Companies with the capability and

interest to participate in this sector currently number between 60 to 70 in New

Brunswick.

Customer Requirements

Manufacturing and Assembly

• Fabrication• Piping• Machining• Assembly• Welding• Finishing and

Painting• Electrical and

Instrumentation

Labour• Skilled Labour• Project

Management• Engineering• Drafting and

Detailing• Quality Assurance• Other Trades

Design• Engineering

Planning and Management

• Estimation• Project

Management• Scheduling• Risk Management

Materials• Steel• Pipe• Electrical• Valves• Paint and

Finishing• Equipment• Sheet Metal

Quality Assurance and Safety

• Quality Programs• Audit• Inspection• Safety Program• TestingTransportation

• Specialty Trucking• Port Facilities• Rail

Assu

rance

and

Qu

ality Co

ntro

l

Ch

ange

/ Co

nfigu

ration

Man

agem

en

t

Pro

ject M

anage

me

nt / R

isk Man

agem

en

t

Module

Key Inputs

ThroughoutEntire Process

New Brunswick Sector Profile: Industrial Fabrication

16 June 2012

Figure 3: Structure of the Industrial Fabrication Sector in New Brunswick

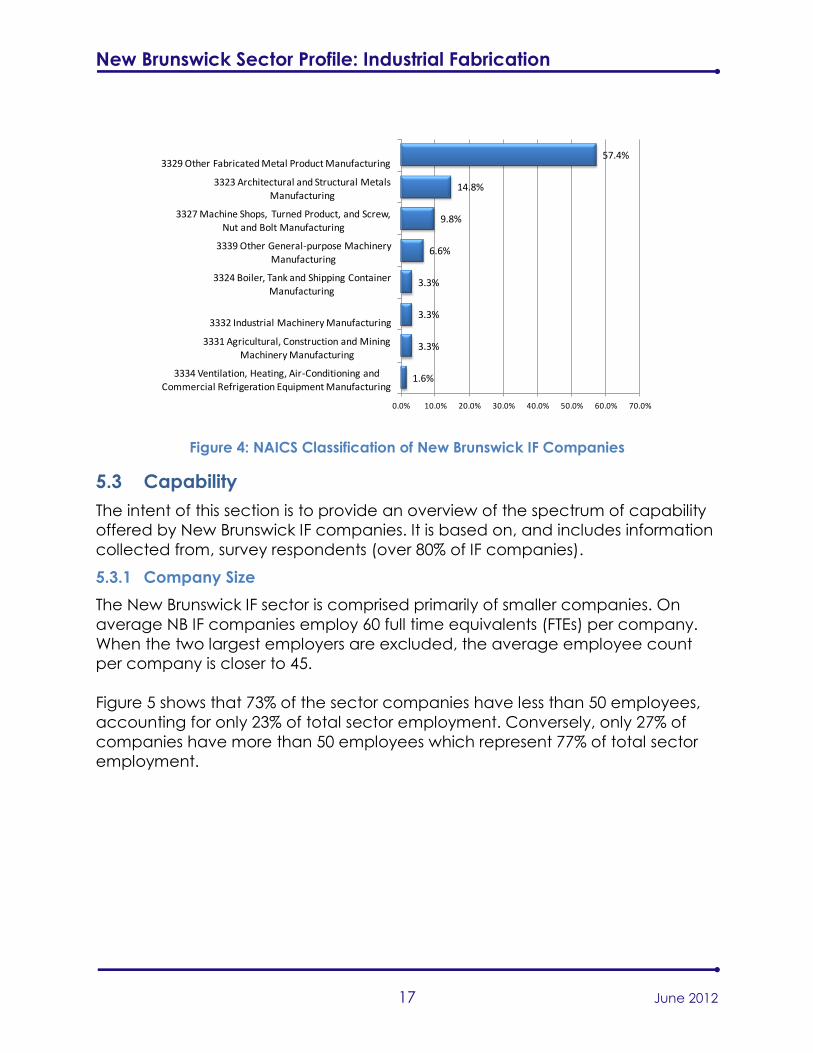

Of the New Brunswick companies identified to be in-scope, over 80% were

classified as; “NAICS 3329 Other Fabricated Metal Product Manufacturing”

(57%), “3323 Architectural and Structural Metals Manufacturing” (15%), and

“3327 Machine Shops, Turned Product, and Screw, Nut and Bolt Manufacturing”

(10%). The entire breakdown is shown in Figure 410.

10 NAICS assignments were determined through assessment by the author based on a number of

factors including but not limited to; company self identification, listings on the Industry Canada

Canadian Company Capability website, as identified in the Service Canada regional database,

company website information, and responses to survey questions (where applicable).

VALUE CHAIN SUPPLIERS

NB INDUSTRIAL FABRICATION SECTOR

EPC COMPANY

LARGEINDUSTRIAL

PROJECT

Drafting & Detailing Co’s

Ind. Comp. Supply Co’s.

Design Service Co’s

MODULARFABRICATIONCOMPANIES

Primary Secondary

Capable Metal Fab. Co’s:• Welding

• Machining• Plate Work• Sheet Metal

Plating and Painting Co’s

Inspection and NDT Co’s

Raw Material Supply Co’s

Electrical & Control System Co’s

Hyd . & Pneu. System Co’s

New Brunswick Sector Profile: Industrial Fabrication

17 June 2012

Figure 4: NAICS Classification of New Brunswick IF Companies

5.3 Capability

The intent of this section is to provide an overview of the spectrum of capability

offered by New Brunswick IF companies. It is based on, and includes information

collected from, survey respondents (over 80% of IF companies).

5.3.1 Company Size

The New Brunswick IF sector is comprised primarily of smaller companies. On

average NB IF companies employ 60 full time equivalents (FTEs) per company.

When the two largest employers are excluded, the average employee count

per company is closer to 45.

Figure 5 shows that 73% of the sector companies have less than 50 employees,

accounting for only 23% of total sector employment. Conversely, only 27% of

companies have more than 50 employees which represent 77% of total sector

employment.

1.6%

3.3%

3.3%

3.3%

6.6%

9.8%

14.8%

57.4%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

3334 Ventilation, Heating, Air-Conditioning and Commercial Refrigeration Equipment Manufacturing

3331 Agricultural, Construction and Mining Machinery Manufacturing

3332 Industrial Machinery Manufacturing

3324 Boiler, Tank and Shipping Container Manufacturing

3339 Other General-purpose Machinery

Manufacturing

3327 Machine Shops, Turned Product, and Screw, Nut and Bolt Manufacturing

3323 Architectural and Structural Metals

Manufacturing

3329 Other Fabricated Metal Product Manufacturing

New Brunswick Sector Profile: Industrial Fabrication

18 June 2012

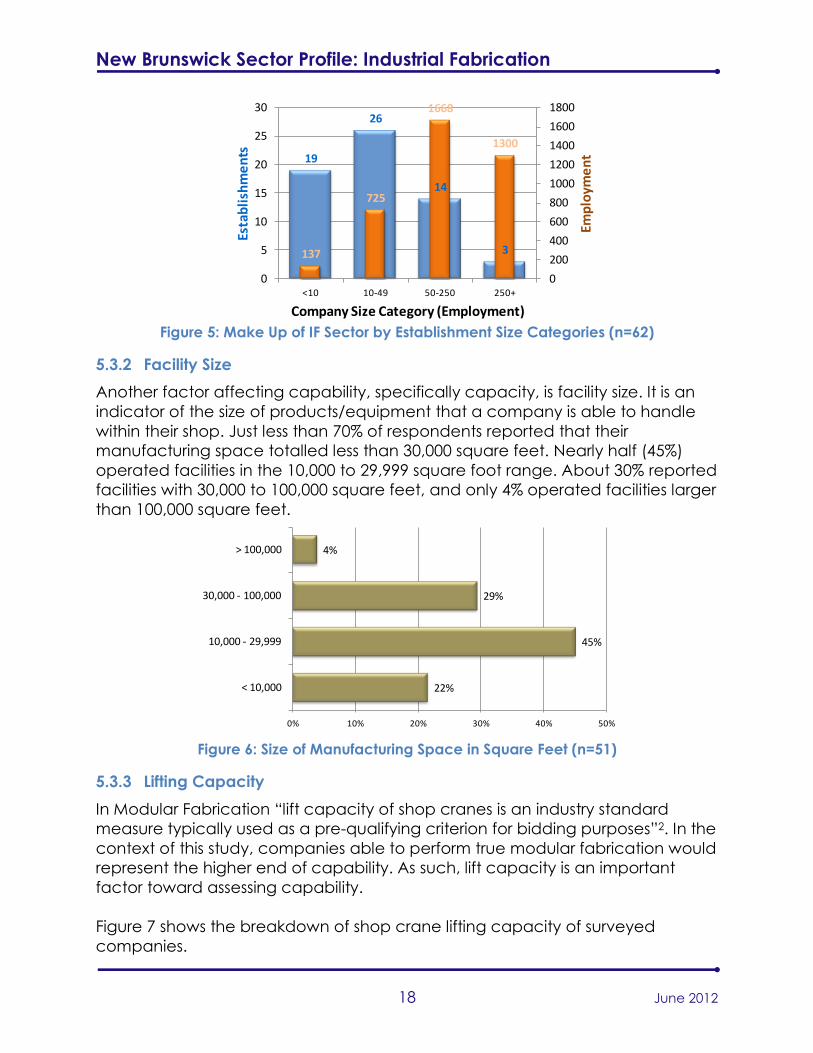

Figure 5: Make Up of IF Sector by Establishment Size Categories (n=62)

5.3.2 Facility Size

Another factor affecting capability, specifically capacity, is facility size. It is an

indicator of the size of products/equipment that a company is able to handle

within their shop. Just less than 70% of respondents reported that their

manufacturing space totalled less than 30,000 square feet. Nearly half (45%)

operated facilities in the 10,000 to 29,999 square foot range. About 30% reported

facilities with 30,000 to 100,000 square feet, and only 4% operated facilities larger

than 100,000 square feet.

Figure 6: Size of Manufacturing Space in Square Feet (n=51)

5.3.3 Lifting Capacity

In Modular Fabrication “lift capacity of shop cranes is an industry standard

measure typically used as a pre-qualifying criterion for bidding purposes”2. In the

context of this study, companies able to perform true modular fabrication would

represent the higher end of capability. As such, lift capacity is an important

factor toward assessing capability.

Figure 7 shows the breakdown of shop crane lifting capacity of surveyed

companies.

19

26

14

3137

725

1668

1300

0

200

400

600

800

1000

1200

1400

1600

1800

0

5

10

15

20

25

30

<10 10-49 50-250 250+

Emp

loym

en

t

Esta

bli

shm

en

ts

Company Size Category (Employment)

22%

45%

29%

4%

0% 10% 20% 30% 40% 50%

< 10,000

10,000 - 29,999

30,000 - 100,000

> 100,000

New Brunswick Sector Profile: Industrial Fabrication

19 June 2012

Figure 7: Shop Crane Lifting Capacity of NB IF Companies (n=51)

Many companies, through the use of mobile cranes, had the ability to lift

greater tonnage than rated above; however the intent was to examine in-shop

fabrication capacity. Where applicable, total lift capacity was reported. For

example, if a company had two 10 ton cranes that were configured to provide

a combined lift capacity of 20 tons – 20 tons was reported.

A distinct gap above 30 tons is apparent where relatively few companies have

this ability. In fact, these same companies have the ability to lift over 50 tons.

5.3.4 Heavy, Medium, or Light Duty

When asked “How would you characterize the capacity of your staff skills and

facilities in relation to the size of materials and projects your company can

reasonably manage?” respondents were given three options:

1. My company has heavy duty capacity and can easily handle the

heaviest and largest materials that are to be manufactured in the region

typically found in very large industrial projects.

2. My company would be considered a medium duty shop that can do

large projects as found in commercial or industrial job sites.

3. My company is a light duty metal shop and usually works with lighter

materials typically found in light industrial and commercial projects such

as miscellaneous metals.

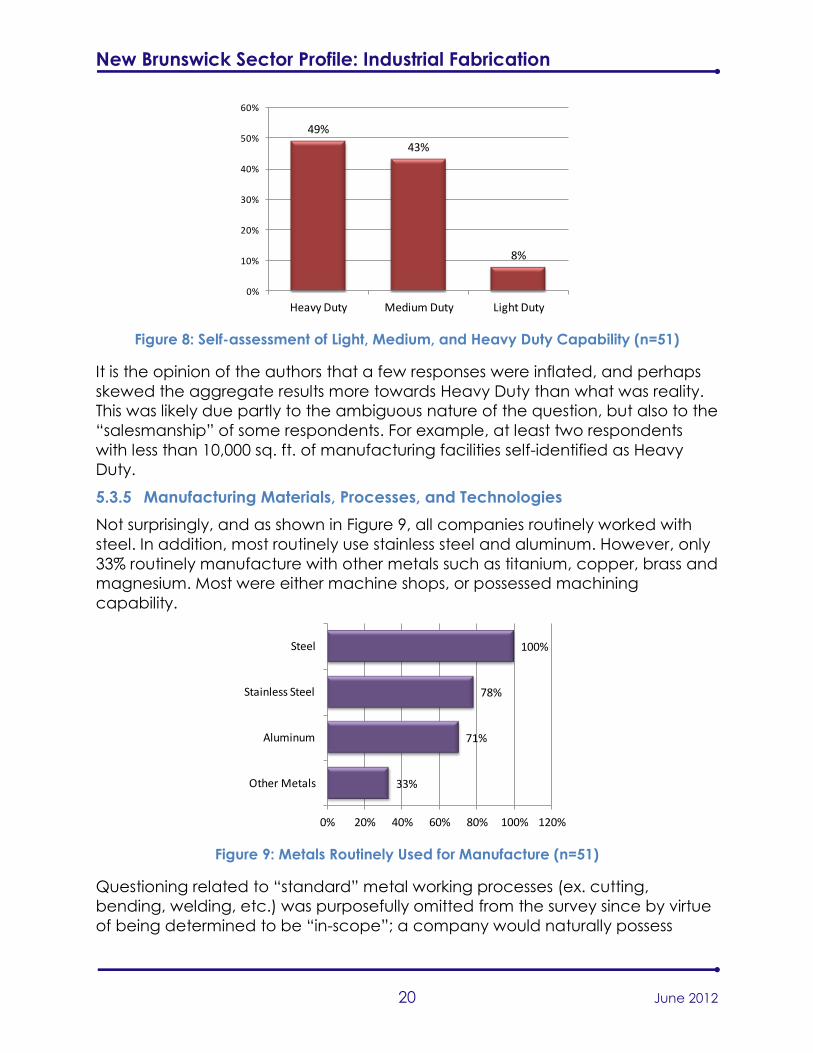

Almost half (49%) of the respondents self identified as “Heavy Duty”, 43% as

“Medium Duty”, and only 8% as “Light Duty”, as shown in Figure 8.

33%

20%

25%

12%

0%

10%

0% 10% 20% 30% 40%

1-5

6-10

11-20

21-30

31-49

50+

Percentage of Companies

Ton

nag

e

New Brunswick Sector Profile: Industrial Fabrication

20 June 2012

Figure 8: Self-assessment of Light, Medium, and Heavy Duty Capability (n=51)

It is the opinion of the authors that a few responses were inflated, and perhaps

skewed the aggregate results more towards Heavy Duty than what was reality.

This was likely due partly to the ambiguous nature of the question, but also to the

“salesmanship” of some respondents. For example, at least two respondents

with less than 10,000 sq. ft. of manufacturing facilities self-identified as Heavy

Duty.

5.3.5 Manufacturing Materials, Processes, and Technologies

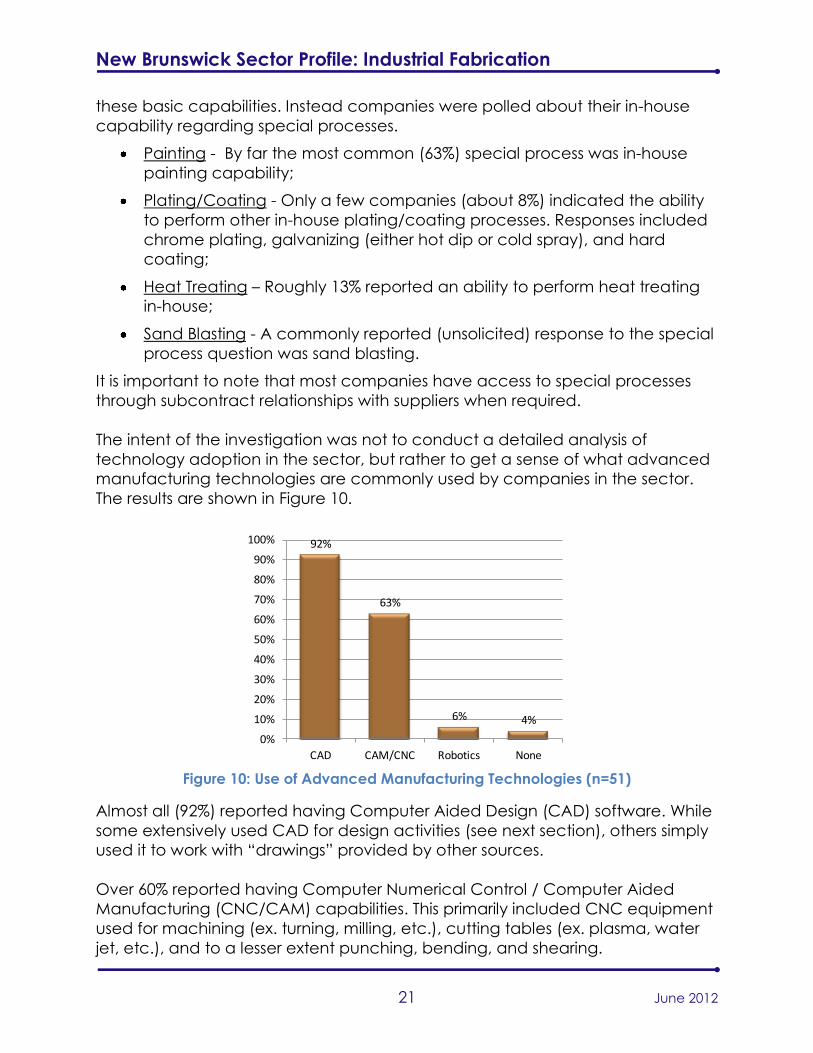

Not surprisingly, and as shown in Figure 9, all companies routinely worked with

steel. In addition, most routinely use stainless steel and aluminum. However, only

33% routinely manufacture with other metals such as titanium, copper, brass and

magnesium. Most were either machine shops, or possessed machining

capability.

Figure 9: Metals Routinely Used for Manufacture (n=51)

Questioning related to “standard” metal working processes (ex. cutting,

bending, welding, etc.) was purposefully omitted from the survey since by virtue

of being determined to be “in-scope”; a company would naturally possess

49%

43%

8%

0%

10%

20%

30%

40%

50%

60%

Heavy Duty Medium Duty Light Duty

33%

71%

78%

100%

0% 20% 40% 60% 80% 100% 120%

Other Metals

Aluminum

Stainless Steel

Steel

New Brunswick Sector Profile: Industrial Fabrication

21 June 2012

these basic capabilities. Instead companies were polled about their in-house

capability regarding special processes.

Painting - By far the most common (63%) special process was in-house

painting capability;

Plating/Coating - Only a few companies (about 8%) indicated the ability

to perform other in-house plating/coating processes. Responses included

chrome plating, galvanizing (either hot dip or cold spray), and hard

coating;

Heat Treating – Roughly 13% reported an ability to perform heat treating

in-house;

Sand Blasting - A commonly reported (unsolicited) response to the special

process question was sand blasting.

It is important to note that most companies have access to special processes

through subcontract relationships with suppliers when required.

The intent of the investigation was not to conduct a detailed analysis of

technology adoption in the sector, but rather to get a sense of what advanced

manufacturing technologies are commonly used by companies in the sector.

The results are shown in Figure 10.

Figure 10: Use of Advanced Manufacturing Technologies (n=51)

Almost all (92%) reported having Computer Aided Design (CAD) software. While

some extensively used CAD for design activities (see next section), others simply

used it to work with “drawings” provided by other sources.

Over 60% reported having Computer Numerical Control / Computer Aided

Manufacturing (CNC/CAM) capabilities. This primarily included CNC equipment

used for machining (ex. turning, milling, etc.), cutting tables (ex. plasma, water

jet, etc.), and to a lesser extent punching, bending, and shearing.

92%

63%

6% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CAD CAM/CNC Robotics None

New Brunswick Sector Profile: Industrial Fabrication

22 June 2012

The few respondents (6%) that reported having robotic capability use it for

welding processes.

Only two companies reported not using any of the above mentioned

advanced manufacturing technologies. It would appear that the sector, as a

whole, has extensively adopted advanced manufacturing technologies. It is

worth noting that small companies with fewer than 5 employees were

considered out of scope and not surveyed. Smaller operations are less likely to

have expensive automated equipment.

5.3.6 Design

Design capability was singled out as an offering that could potentially

differentiate one IF company from another by offering a greater breadth of

service. Overall, 80% of IF companies polled have the ability to offer clients

design services on a routine basis, whereas 20% do not. A wide spectrum of

design capabilities exists within the sector; ranging from companies with fully

rounded engineering departments to companies with a single employee that

might create a sketch for the shop floor.

Over half (55%) of respondents reported having in-house design capabilities,

whereas the remaining 45% have access to external engineers, technicians, or

design firms through contractual relationships.

5.3.7 Certifications

The two most common and most relevant areas of sector certifications relate to

welding and quality.

Welding: The welding certification environment is relatively complicated.

Certification applies to process (ex. SMAW, GTAW, PAW, etc.)11, material (ex.

steel, aluminum, etc.), application (ex. structural, high pressure, etc.), and

other factors. Within New Brunswick, the Canadian Welding Bureau (CWB)

certifies both companies and individual welders according to standards

established by the Canadian Standards Association (CSA). The New

Brunswick Department of Public Safety certifies welders according to ASME12

standards for pipe and pressure vessel welding.

Individual welder certifications or “tickets” are mandatory based on the

specific technologies, substrates, positions and techniques required for the

type of work/product being produced. Welders require certifications for the

11 SMAW=Shielded Metal Arc Welding, GTAW=Gas Tungsten Arc Welding, PAW=Plasma Arc

Welding 12 The American Society of Mechanical Engineers

New Brunswick Sector Profile: Industrial Fabrication

23 June 2012

processes utilized by their employer. The “mix” of required certifications varies

from company to company based on industries served and products

produced.

The intent of the investigation was not to conduct a detailed examination

and classification of IF company welding certification in New Brunswick, but

rather to identify if companies have actually achieved welding certification

and if so, what “type”. As shown in Figure 11, over ¾ of respondents possess

some form of structural welding certification. Of these, all possessed

Canadian Welding Bureau (CWB) certification, and 13% also had

certification with the American/Canadian Institute of Steel Construction

(AISC/CISC).

Figure 11: Welding Certifications (n=51)

Approximately one third (35%) of the companies interviewed possess pressure

welding certifications (ASME - pipe or pressure vessel). With few exceptions,

companies with this certification also possess structural welding certifications.

Only two companies reported achieving welding certification for nuclear

applications. A surprising 16% have not achieved any welding certification

(or were unable to accurately report). However, over half of these were

machine shops.

Quality: Certification of quality programs is another differentiating factor in the

sector. As shown in Figure 12, almost half (48%) of respondents reported

having an externally certified quality program. ISO 9001 (including AS9100 in

a few instances) made up most (79%) of the external certifications while

AISC/CISC quality certification made up the balance (21%).

16%

4%

35%

76%

0% 20% 40% 60% 80% 100%

None

Other: Nuclear

Pressure (ex. ASME)

Structural (ex. CWB, AISC/CISC)

New Brunswick Sector Profile: Industrial Fabrication

24 June 2012

Figure 12: Quality Program Certifications (n=50)

Another 42% of respondents reported having a documented in-house quality

program, and 10% had no formal quality program in place.

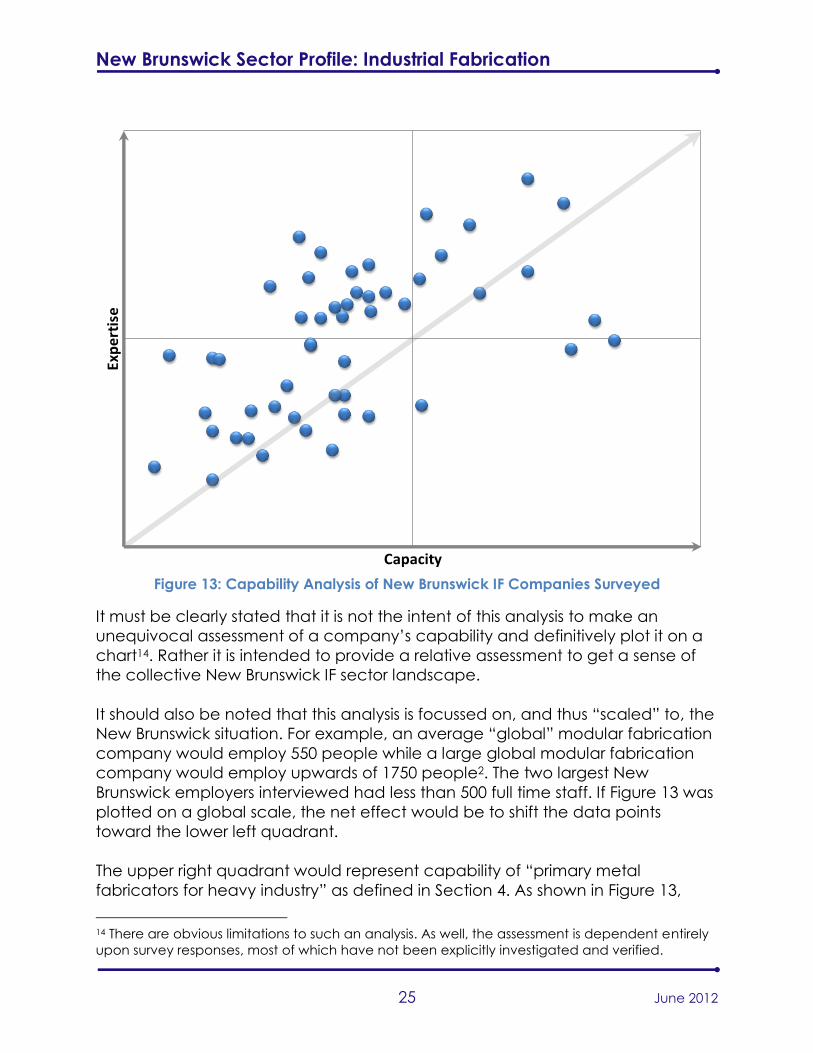

5.3.8 Capability Analysis

To provide insight into the relative capability of IF companies, and the New

Brunswick sector as a whole, an algorithm was developed to quantitatively

assess companies against a number of relevant factors unique to the IF sector.

Shown in Figure 13 is a plot of IF companies based on values calculated for

Capacity (X-Axis) and Expertise (Y-Axis). Coordinates for each company were

calculated based on a weighted average of numerical values assigned to

selected survey responses as outlined in Table 2 below13:

Table 2: Capability Analysis Assessment Criteria

Factor Weight

Ca

pa

city

Ax

is

Size of Shop 25%

Shop Lift Capacity 25%

Heavy, Medium or Light Duty 20%

Total Number of Employees 20%

Revenue Range 10%

Ex

pe

rtis

e

Ax

is

Participation in Industrial Markets 25%

Welding Certifications 25%

In-House Design Capability

Engineers/Technicians on Staff (10%)

CAD Capability (5%)

Offer Design Services (5%)

20%

Geographic Market Reach 10%

Quality Program Certification 10%

Ratio of Production to Total Employment 5%

Metals Routinely Worked With 5%

13 Sections 5.3 and 5.5 provide greater insight into the various factors.

Externally Certified

48%In-House Program

42%

No Formal Program

10%

New Brunswick Sector Profile: Industrial Fabrication

25 June 2012

Figure 13: Capability Analysis of New Brunswick IF Companies Surveyed

It must be clearly stated that it is not the intent of this analysis to make an

unequivocal assessment of a company’s capability and definitively plot it on a

chart14. Rather it is intended to provide a relative assessment to get a sense of

the collective New Brunswick IF sector landscape.

It should also be noted that this analysis is focussed on, and thus “scaled” to, the

New Brunswick situation. For example, an average “global” modular fabrication

company would employ 550 people while a large global modular fabrication

company would employ upwards of 1750 people2. The two largest New

Brunswick employers interviewed had less than 500 full time staff. If Figure 13 was

plotted on a global scale, the net effect would be to shift the data points

toward the lower left quadrant.

The upper right quadrant would represent capability of “primary metal

fabricators for heavy industry” as defined in Section 4. As shown in Figure 13,

14 There are obvious limitations to such an analysis. As well, the assessment is dependent entirely

upon survey responses, most of which have not been explicitly investigated and verified.

Exp

ert

ise

Capacity

New Brunswick Sector Profile: Industrial Fabrication

26 June 2012

there are relatively few companies in this quadrant who would have the

capacity and expertise to “go it alone” when pursuing mega project

prefabricated modules.

Anecdotal evidence established through interviews indicated that a number of

smaller companies are currently supplying products and services to larger New

Brunswick companies in the sector. For smaller progressive companies wishing to

pursue the sector, the situation presents potential partnering opportunities. Due

to this reality, specific sector development efforts are taking place in the

province by both private and public stakeholders (see Section 5.7).

5.4 Regional Distribution

Figure 14 shows the regional distribution of 62 Industrial Fabrication companies in

New Brunswick.

Figure 14: Location of IF Companies in New Brunswick

5-9

10-49

50-250

250+

New Brunswick Sector Profile: Industrial Fabrication

27 June 2012

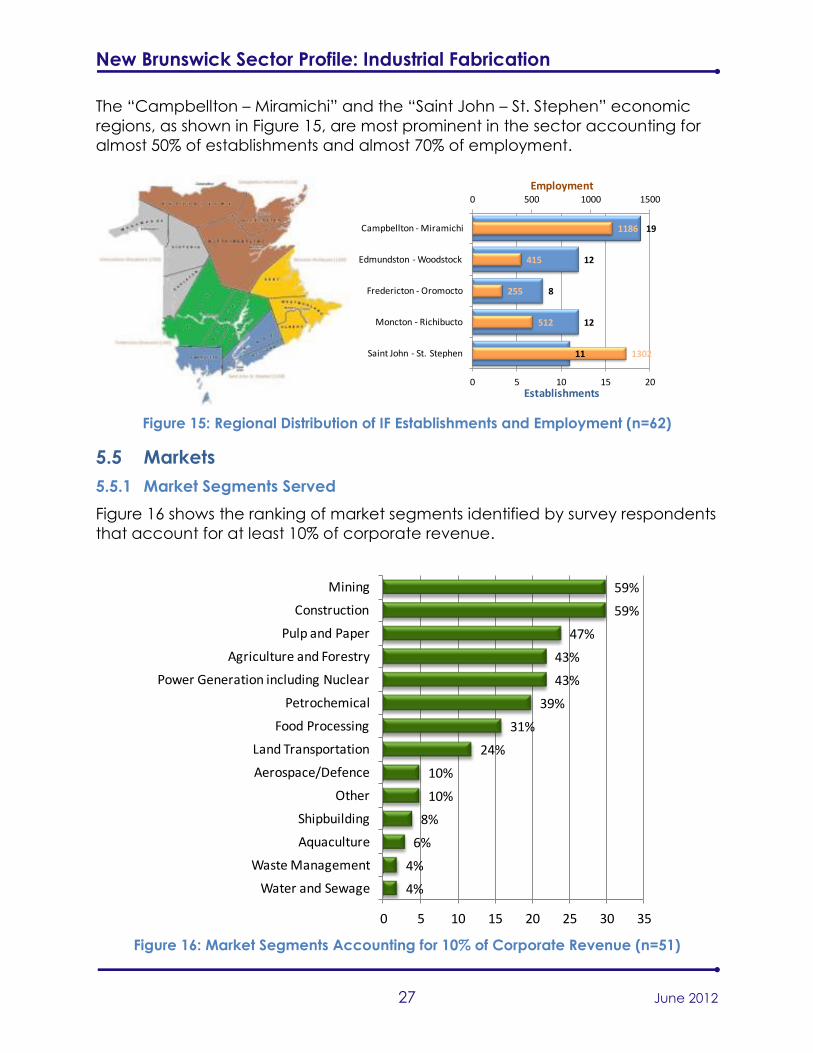

The “Campbellton – Miramichi” and the “Saint John – St. Stephen” economic

regions, as shown in Figure 15, are most prominent in the sector accounting for

almost 50% of establishments and almost 70% of employment.

Figure 15: Regional Distribution of IF Establishments and Employment (n=62)

5.5 Markets

5.5.1 Market Segments Served

Figure 16 shows the ranking of market segments identified by survey respondents

that account for at least 10% of corporate revenue.

Figure 16: Market Segments Accounting for 10% of Corporate Revenue (n=51)

11

12

8

12

19

1302

512

255

415

1186

0 500 1000 1500

0 5 10 15 20

Saint John - St. Stephen

Moncton - Richibucto

Fredericton - Oromocto

Edmundston - Woodstock

Campbellton - Miramichi

Employment

Establishments

4%

4%

6%

8%

10%

10%

24%

31%

39%

43%

43%

47%

59%

59%

0 5 10 15 20 25 30 35

Water and Sewage

Waste Management

Aquaculture

Shipbuilding

Other

Aerospace/Defence

Land Transportation

Food Processing

Petrochemical

Power Generation including Nuclear

Agriculture and Forestry

Pulp and Paper

Construction

Mining

New Brunswick Sector Profile: Industrial Fabrication

28 June 2012

The most common market segments served (59%) are mining and construction.

The significant participation in construction illustrates the “cross-industry” nature

of companies in this sector.

Figure 17 drills down further and shows how respondents identified the top 3

industrial markets served, by revenue. In viewing the data it is important to note

that while all respondents identified their primary (n=51) market, not all identified

their secondary (n=41) and tertiary (n=37) markets.

Figure 17: Top Three Markets by Value of Revenue

The mining industry is by far the primary source of revenue for most New

Brunswick IF companies. Not surprising, the construction, petrochemical, pulp

and paper, and utility industries are also major sources of revenue. Most

respondents did qualify their responses indicating that revenue sources change

in relation to the economy. For example, companies that mainly serve the

petrochemical market today may have principally relied on the pulp and paper

market 10 years ago.

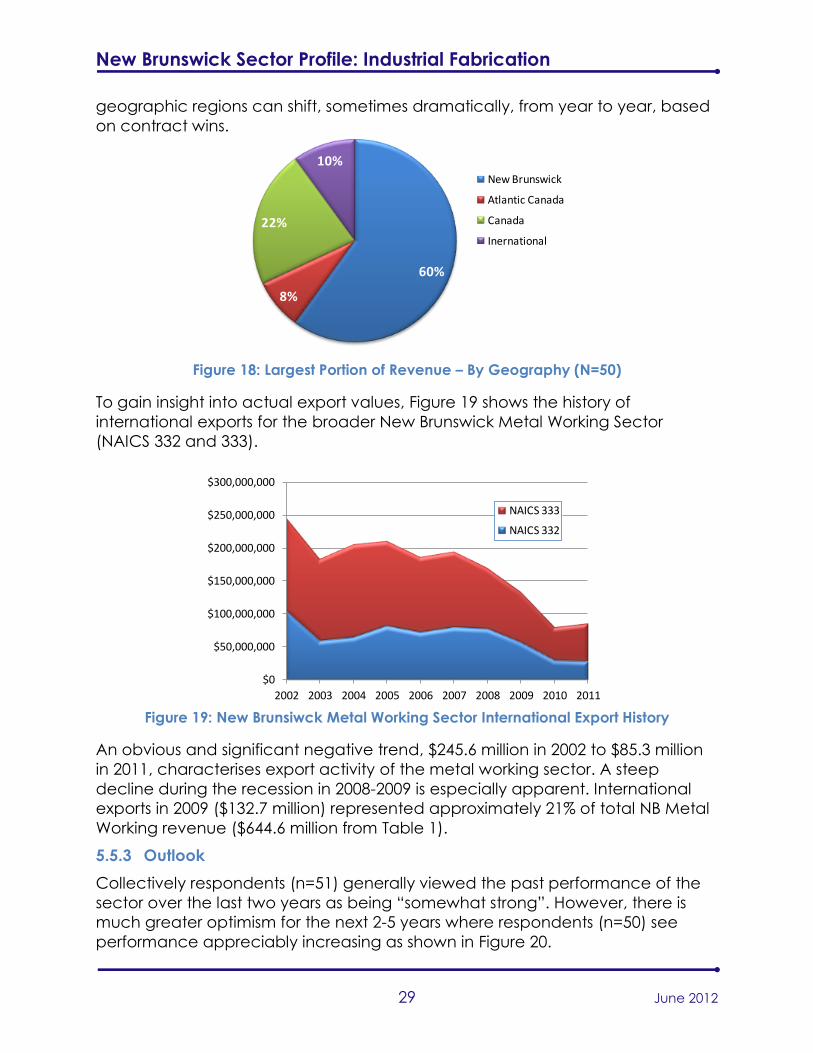

5.5.2 Geographic Reach

As shown in Figure 18, a large portion (60%) of the companies interviewed

indicated that the largest portion of their revenue originates from within New

Brunswick. It is important to note that this does not imply that 60% of sector

revenue originates from New Brunswick, but rather only 60% of the companies

indicate that it is their major source. The same companies are likely to have

interprovincial and export revenue as well. It should be noted that respondents

indicated that the percentage of their revenue coming from various

0 5 10 15 20

Other

Shipbuilding

Land Transport

Agriculture and Forestry

Aerospace/Defence

Food Processing

Pulp and Paper

Power Generation including Nuclear

Petrochemical

Construction

Mining

Primary

Secondary

Tertiary

New Brunswick Sector Profile: Industrial Fabrication

29 June 2012

geographic regions can shift, sometimes dramatically, from year to year, based

on contract wins.

Figure 18: Largest Portion of Revenue – By Geography (N=50)

To gain insight into actual export values, Figure 19 shows the history of

international exports for the broader New Brunswick Metal Working Sector

(NAICS 332 and 333).

Figure 19: New Brunsiwck Metal Working Sector International Export History

An obvious and significant negative trend, $245.6 million in 2002 to $85.3 million

in 2011, characterises export activity of the metal working sector. A steep

decline during the recession in 2008-2009 is especially apparent. International

exports in 2009 ($132.7 million) represented approximately 21% of total NB Metal

Working revenue ($644.6 million from Table 1).

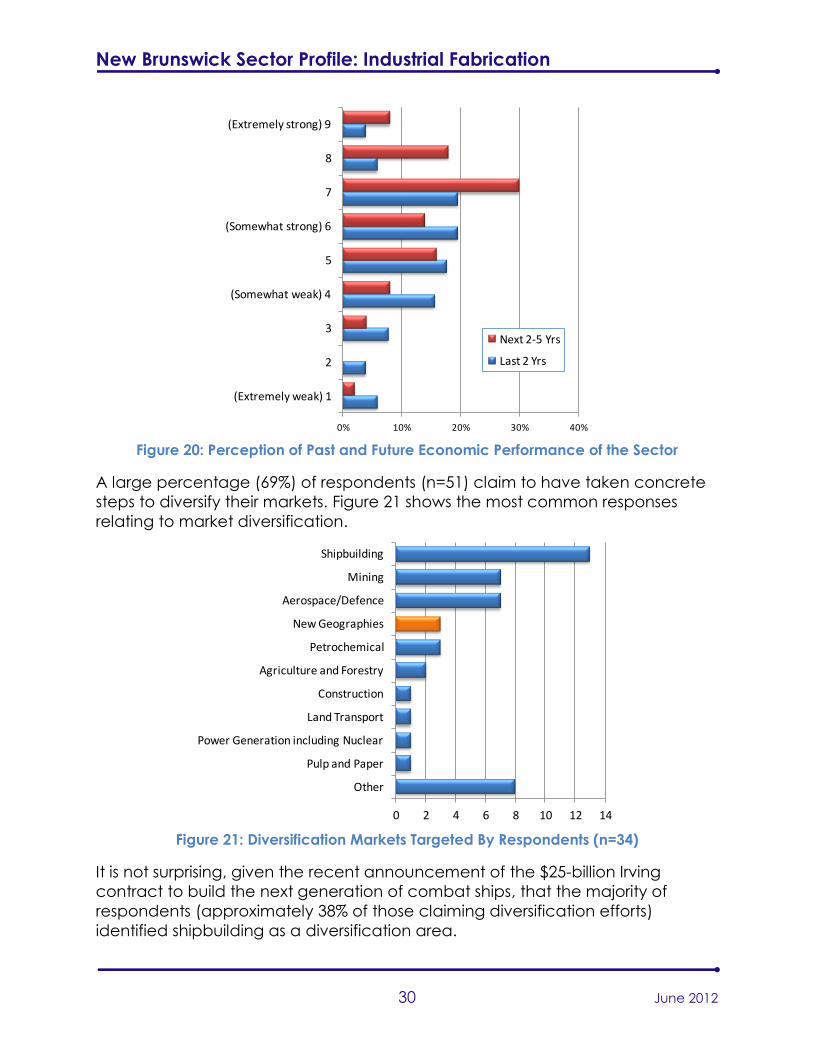

5.5.3 Outlook

Collectively respondents (n=51) generally viewed the past performance of the

sector over the last two years as being “somewhat strong”. However, there is

much greater optimism for the next 2-5 years where respondents (n=50) see

performance appreciably increasing as shown in Figure 20.

60%

8%

22%

10%New Brunswick

Atlantic Canada

Canada

Inernational

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

NAICS 333

NAICS 332

New Brunswick Sector Profile: Industrial Fabrication

30 June 2012

Figure 20: Perception of Past and Future Economic Performance of the Sector

A large percentage (69%) of respondents (n=51) claim to have taken concrete

steps to diversify their markets. Figure 21 shows the most common responses

relating to market diversification.

Figure 21: Diversification Markets Targeted By Respondents (n=34)

It is not surprising, given the recent announcement of the $25-billion Irving

contract to build the next generation of combat ships, that the majority of

respondents (approximately 38% of those claiming diversification efforts)

identified shipbuilding as a diversification area.

0% 10% 20% 30% 40%

(Extremely weak) 1

2

3

(Somewhat weak) 4

5

(Somewhat strong) 6

7

8

(Extremely strong) 9

Next 2-5 Yrs

Last 2 Yrs

0 2 4 6 8 10 12 14

Other

Pulp and Paper

Power Generation including Nuclear

Land Transport

Construction

Agriculture and Forestry

Petrochemical

New Geographies

Aerospace/Defence

Mining

Shipbuilding

New Brunswick Sector Profile: Industrial Fabrication

31 June 2012

Despite this, mining continues to be a market focus for companies. Aerospace

and defence are also high ranking target markets - likely fuelled by the

shipbuilding buzz.

Although not asked specifically, only three respondents identified that they will

be pursuing new geographic markets.

In terms of expansion or contraction plans (machinery or buildings), none of the

respondents indicated that they plan to contract. Forty-nine percent (49%)

indicated that they plan to expand, whereas the remaining 51% plan to

maintain current operations.

5.5.4 Market Barriers

While individual companies may face a number of market barriers depending

upon their unique circumstances, there was really only one sector-specific

market barrier identified – access to free and open trade. This is a significant

hurdle since most opportunities in the sector, particularly if growth is to take

place, exist beyond the borders of New Brunswick.

It was suggested that the bi-lateral government agreements between

Newfoundland and Labrador with the Government of Nova Scotia and the

Government of Canada are a major barrier to New Brunswick companies

wishing to pursue these regional markets. Similarly, the union influence and

control over construction sites in Quebec creates challenges for New Brunswick

companies that wish to build, ship, and install modular components in that

province.

New Brunswick government officials acknowledge there are challenges in this

area, and that the New Brunswick government must continue to raise these

issues with their provincial and federal counterparts.

5.6 Transportation Infrastructure

Transportation infrastructure is critically important to the New Brunswick IF sector.

The nature of business – fabrication of large metal products for installation at

distant industrial sites – demands appropriate transportation infrastructure to

move goods to distant markets. Infrastructure to support land (road and rail)

and sea transportation in New Brunswick is briefly discussed below15.

5.6.1 Land

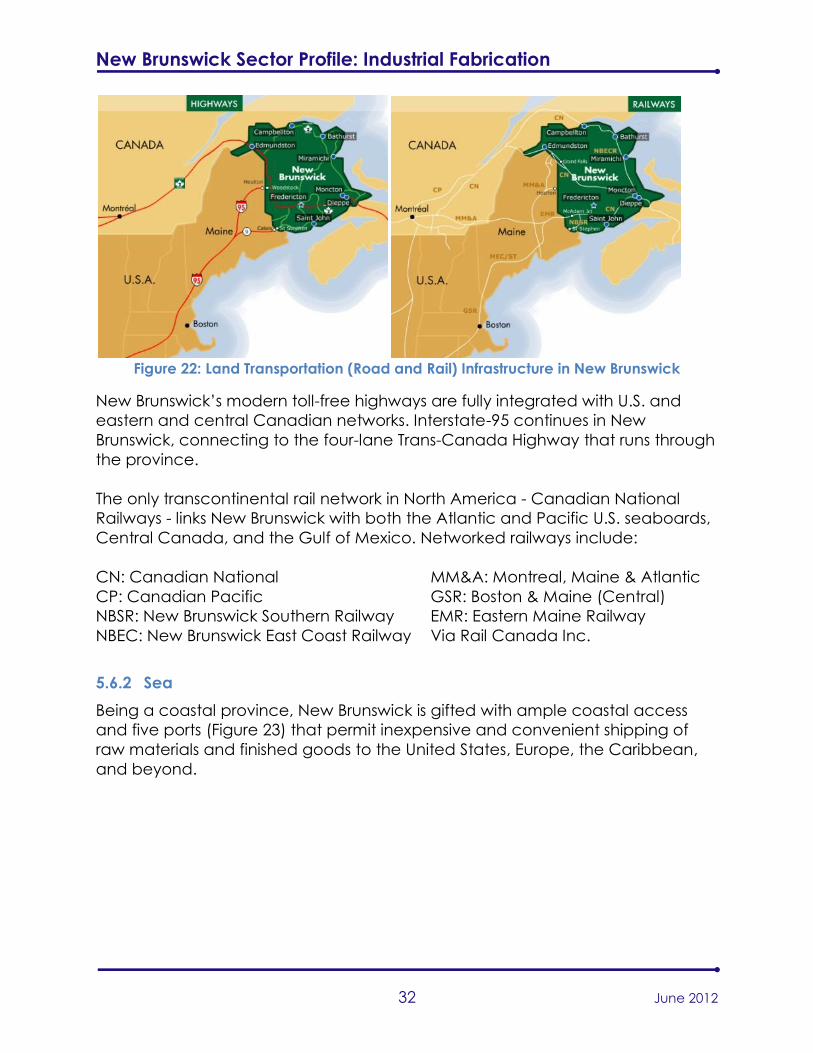

New Brunswick’s land transportation infrastructure is shown in Figure 22.

15 Unless otherwise specified, information in this section is taken primarily from the New Brunswick

Department of Economic Development website -

http://www2.gnb.ca/content/gnb/en/departments/economic_development/Export_Trade.html

New Brunswick Sector Profile: Industrial Fabrication

32 June 2012

Figure 22: Land Transportation (Road and Rail) Infrastructure in New Brunswick

New Brunswick’s modern toll-free highways are fully integrated with U.S. and

eastern and central Canadian networks. Interstate-95 continues in New

Brunswick, connecting to the four-lane Trans-Canada Highway that runs through

the province.

The only transcontinental rail network in North America - Canadian National

Railways - links New Brunswick with both the Atlantic and Pacific U.S. seaboards,

Central Canada, and the Gulf of Mexico. Networked railways include:

CN: Canadian National MM&A: Montreal, Maine & Atlantic

CP: Canadian Pacific GSR: Boston & Maine (Central)

NBSR: New Brunswick Southern Railway EMR: Eastern Maine Railway

NBEC: New Brunswick East Coast Railway Via Rail Canada Inc.

5.6.2 Sea

Being a coastal province, New Brunswick is gifted with ample coastal access

and five ports (Figure 23) that permit inexpensive and convenient shipping of

raw materials and finished goods to the United States, Europe, the Caribbean,

and beyond.

New Brunswick Sector Profile: Industrial Fabrication

33 June 2012

Figure 23: New Brunswick Ports

Sea ports are particularly important to the sector when very large prefabricated

industrial modules are required to be exported to distant markets. Two of the

larger Ports, Belledune and Saint John, have undertaken specific efforts to

support and pursue the sector in New Brunswick.

Belledune: In 2010 the Port of Belledune and the Provincial Government formed

a strategic partnership to construct the “Belledune Modular Fabrication

Facility” with $13.2 million in funding from the Federal and Provincial

governments. The endeavour included the construction of a new 40,000

square foot facility and the acquisition for another 90,000 square foot facility.

The first tenant of the facility was announced in March 2012.

Saint John: In 2010 Saint John Industrial Park Ltd. commissioned an engineering

study for a site review of a barge loading facility in Saint John16 citing that:

“Metal fabricators in Saint John are seeking to provide a barge loading

facility that will allow the proponents to ship (or receive) large components

that exceed rail and truck capability or limitations.” In 2012 a news report17

indicated that the $6 million project was supported by local companies such

as Lorneville Mechanical and that construction could begin in the fall of

2012.

5.7 Sector Development

As presented in Sections 5.3.1and 5.3.8, the very nature of the New Brunswick IF

sector (comprised primarily of smaller companies) presents opportunities for,

16 “Site Reviews for a Barge Loading Facility in Saint John, NB for Fabricated Steel Modules for

Heavy Industry”, Cormier Management Consulting Ltd. in association with Fundy Engineering Ltd,

June 2010 17 “Proposed barge docking site could boost business”, CBC News, March 7, 2012

New Brunswick Sector Profile: Industrial Fabrication

34 June 2012

and in some cases necessitates, partnering to pursue larger projects. A logical