FEBRUARY 26, 2014

OECD’S COUNTRY BY COUNTRY REPORTING: IMPLICATIONS & PRACTICAL APPLICATION OF THE PROPOSED TEMPLATE

AGENDA

• Overview

• Local File

• Master File for Risk Assessment

• Country by Country Reporting

• Practical Takeaways

OVERVIEW

• Background

– January 30, 2014 proposed Chapter V of OECD Transfer Pricing

Guidelines

– Follow-up to OECD’s White Paper on Transfer Pricing Documentation

– Part of the OECD Action Plan on Base Erosion and Profit Shifting

• Promised to suggest ways that documentation requirements to

enhance transparency taking into compliance costs

OVERVIEW

• Stated Goals

– Ensure that multinationals appropriately consider arm’s length standard

when setting intercompany transactions

– Provide tax authorities with information necessary to conduct an informed

transfer pricing risk assessment

– Provide tax authorities with the information needed to conduct a thorough

audit of specific intercompany transactions relevant to that tax authority

• Contemplated Design of Documentation

– Master file that includes country by country reporting template to facilitate transfer pricing risk assessment

– Local file that addresses country specific intercompany transactions that would inform a national tax authority in the event of an actual transfer pricing inquiry

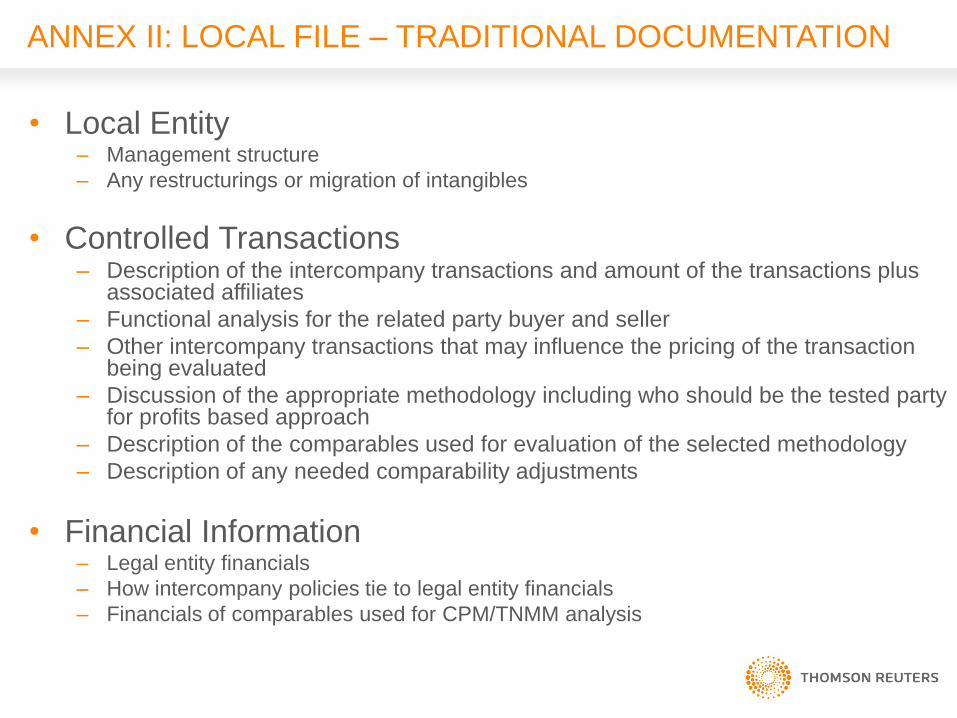

ANNEX II: LOCAL FILE – TRADITIONAL DOCUMENTATION

• Local Entity – Management structure

– Any restructurings or migration of intangibles

• Controlled Transactions – Description of the intercompany transactions and amount of the transactions plus

associated affiliates

– Functional analysis for the related party buyer and seller

– Other intercompany transactions that may influence the pricing of the transaction being evaluated

– Discussion of the appropriate methodology including who should be the tested party for profits based approach

– Description of the comparables used for evaluation of the selected methodology

– Description of any needed comparability adjustments

• Financial Information – Legal entity financials

– How intercompany policies tie to legal entity financials

– Financials of comparables used for CPM/TNMM analysis

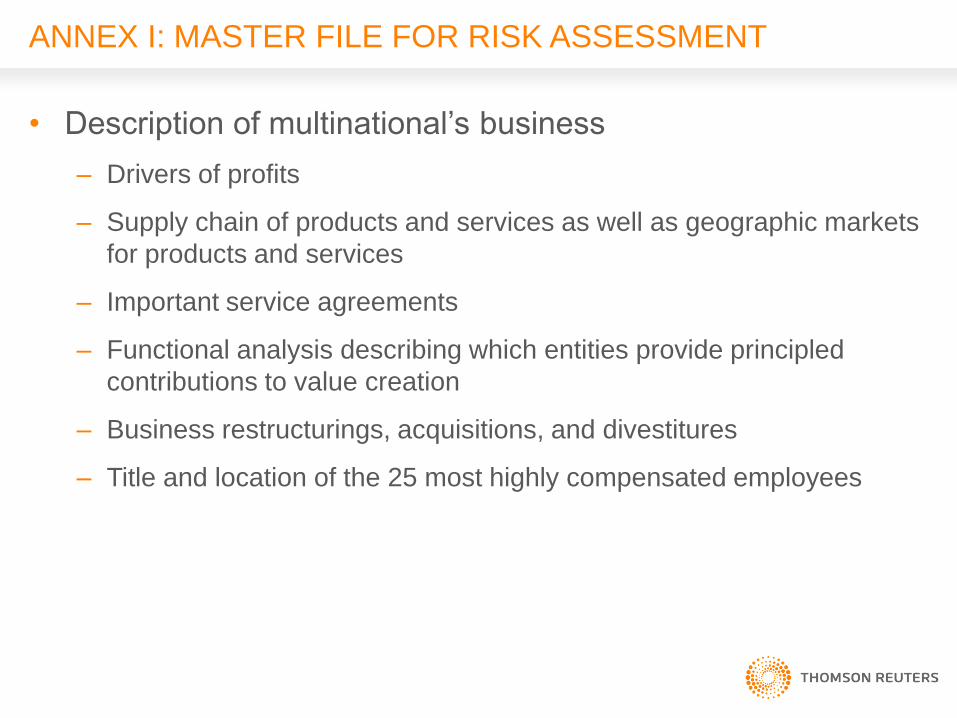

ANNEX I: MASTER FILE FOR RISK ASSESSMENT

• Description of multinational’s business

– Drivers of profits

– Supply chain of products and services as well as geographic markets

for products and services

– Important service agreements

– Functional analysis describing which entities provide principled

contributions to value creation

– Business restructurings, acquisitions, and divestitures

– Title and location of the 25 most highly compensated employees

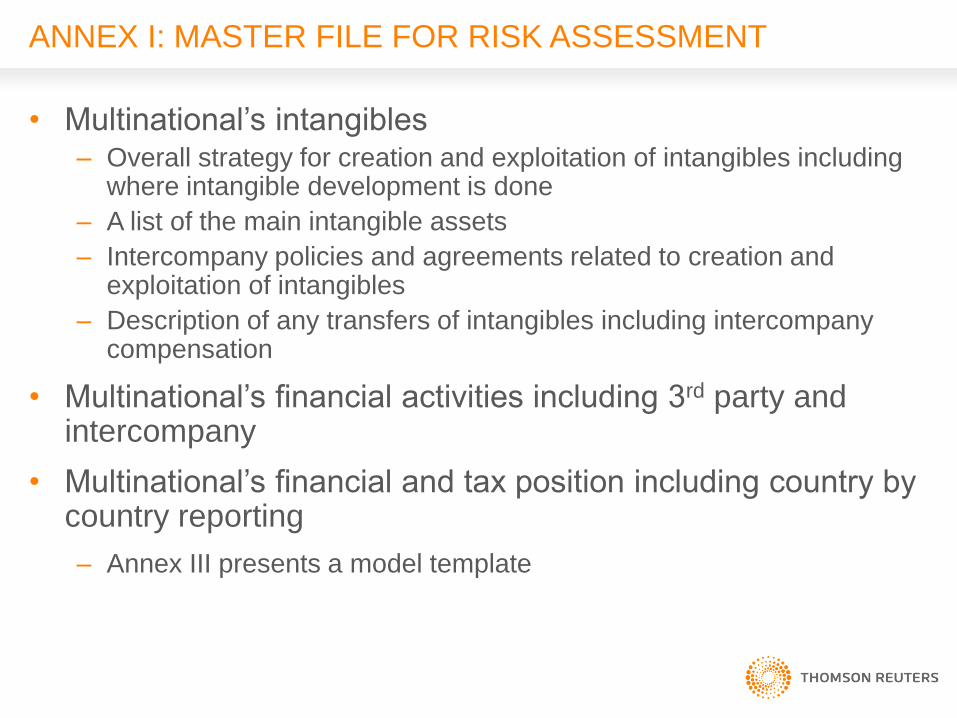

ANNEX I: MASTER FILE FOR RISK ASSESSMENT

• Multinational’s intangibles – Overall strategy for creation and exploitation of intangibles including

where intangible development is done

– A list of the main intangible assets

– Intercompany policies and agreements related to creation and exploitation of intangibles

– Description of any transfers of intangibles including intercompany compensation

• Multinational’s financial activities including 3rd party and intercompany

• Multinational’s financial and tax position including country by country reporting

– Annex III presents a model template

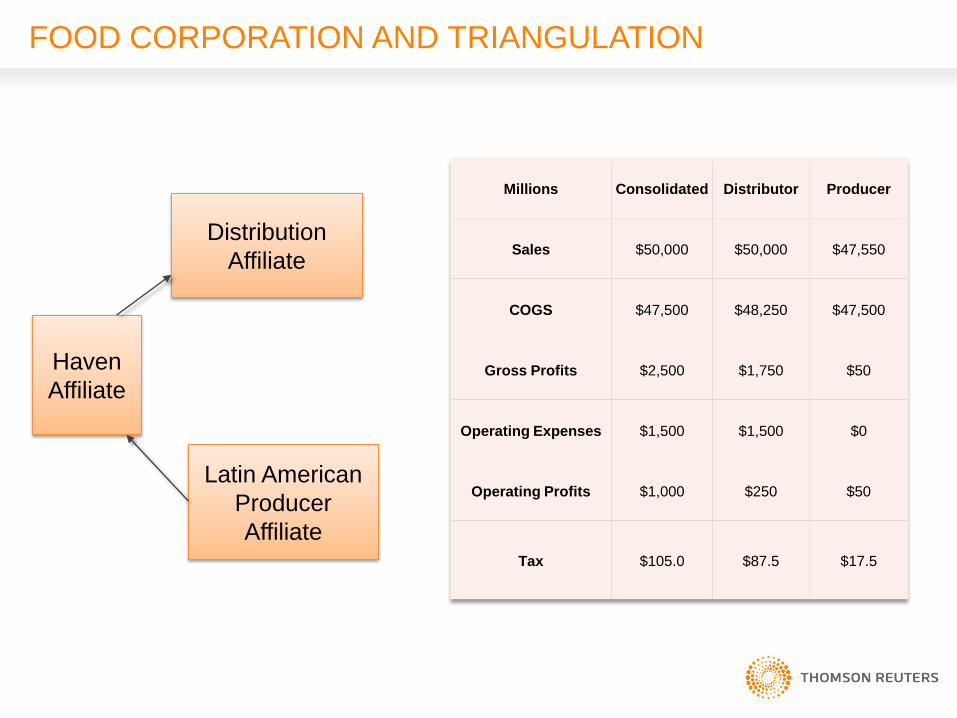

FOOD CORPORATION AND TRIANGULATION

Millions Consolidated Distributor Producer

Sales $50,000 $50,000 $47,550

COGS $47,500 $48,250 $47,500

Gross Profits $2,500 $1,750 $50

Operating Expenses $1,500 $1,500 $0

Operating Profits $1,000 $250 $50

Tax $105.0 $87.5 $17.5

Distribution

Affiliate

Latin American

Producer

Affiliate

Haven

Affiliate

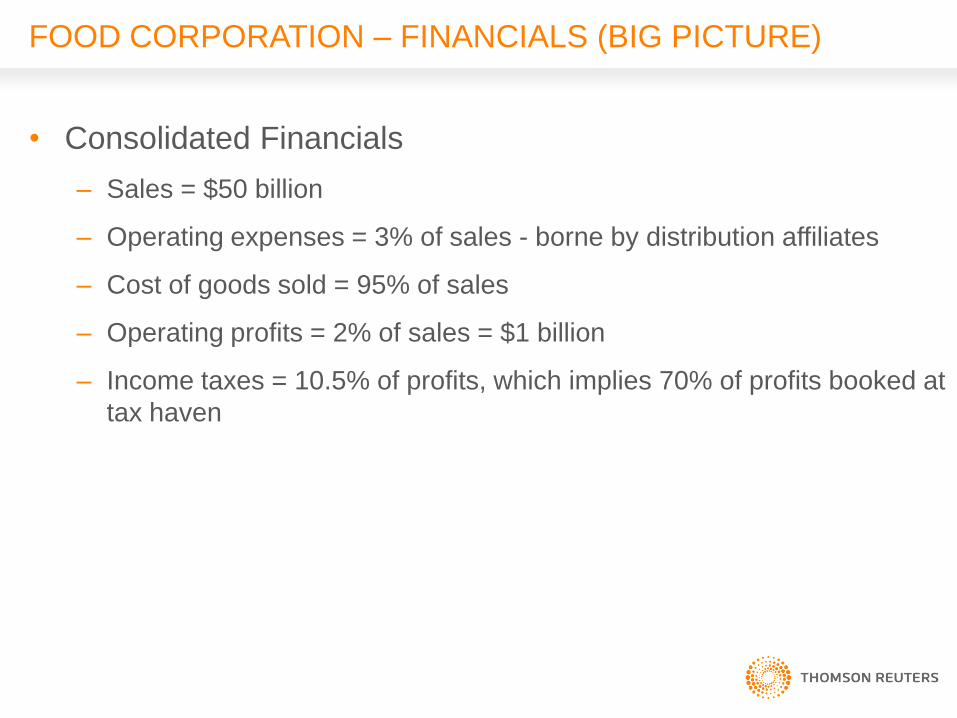

FOOD CORPORATION – FINANCIALS (BIG PICTURE)

• Consolidated Financials

– Sales = $50 billion

– Operating expenses = 3% of sales - borne by distribution affiliates

– Cost of goods sold = 95% of sales

– Operating profits = 2% of sales = $1 billion

– Income taxes = 10.5% of profits, which implies 70% of profits booked at

tax haven

FOOD CORPORATION – FINANCIALS (BIG PICTURE)

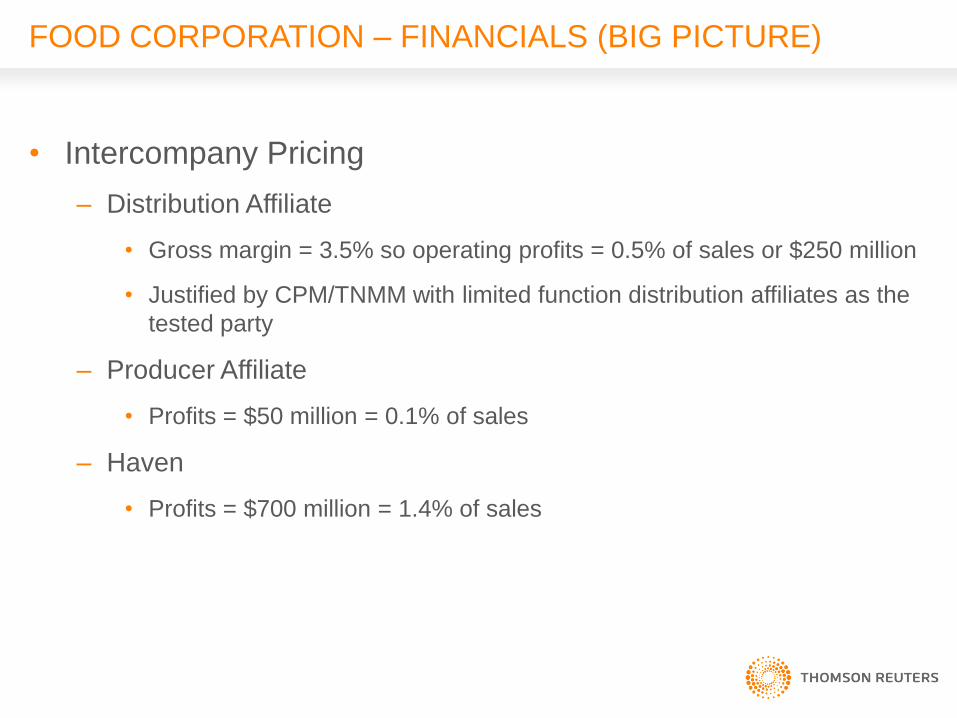

• Intercompany Pricing

– Distribution Affiliate

• Gross margin = 3.5% so operating profits = 0.5% of sales or $250 million

• Justified by CPM/TNMM with limited function distribution affiliates as the

tested party

– Producer Affiliate

• Profits = $50 million = 0.1% of sales

– Haven

• Profits = $700 million = 1.4% of sales

FOOD CORPORATION – IMPORTANT DETAILS

• Multiple Affiliates

– Several distribution affiliates globally but main one is in U.S.

• We suggested transfer pricing to distribution affiliates may be

defensible with a CPM/TNMM analysis

– Several products coming from various Latin American affiliates

• Argentina supplies grains and soybeans

• Brazil supplies sugar

FOOD CORPORATION – IMPORTANT DETAILS

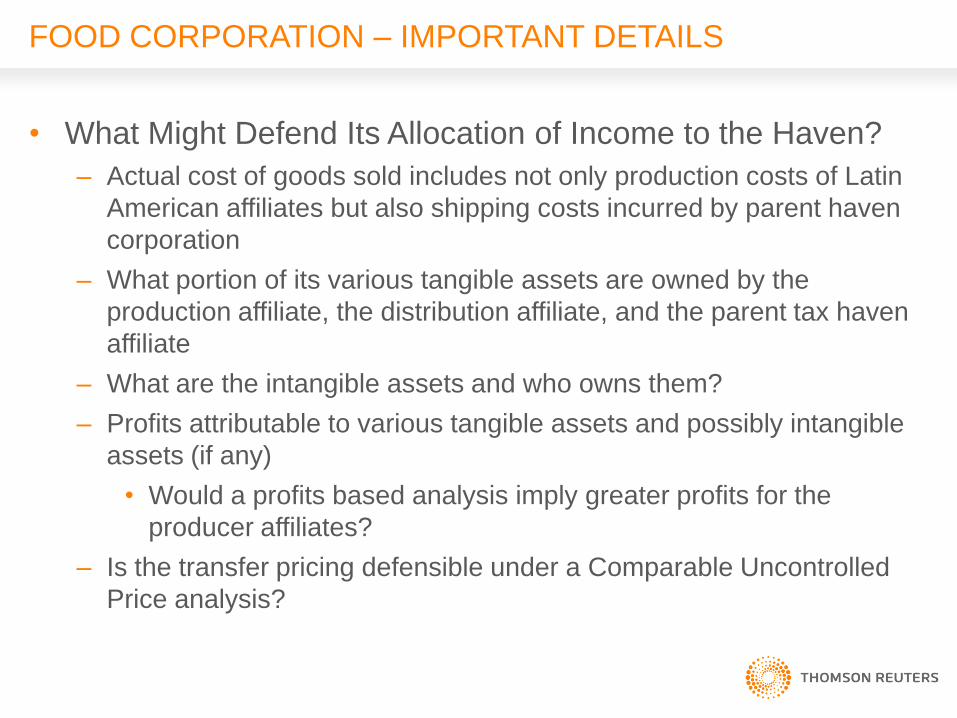

• What Might Defend Its Allocation of Income to the Haven?

– Actual cost of goods sold includes not only production costs of Latin

American affiliates but also shipping costs incurred by parent haven

corporation

– What portion of its various tangible assets are owned by the

production affiliate, the distribution affiliate, and the parent tax haven

affiliate

– What are the intangible assets and who owns them?

– Profits attributable to various tangible assets and possibly intangible

assets (if any)

• Would a profits based analysis imply greater profits for the

producer affiliates?

– Is the transfer pricing defensible under a Comparable Uncontrolled

Price analysis?

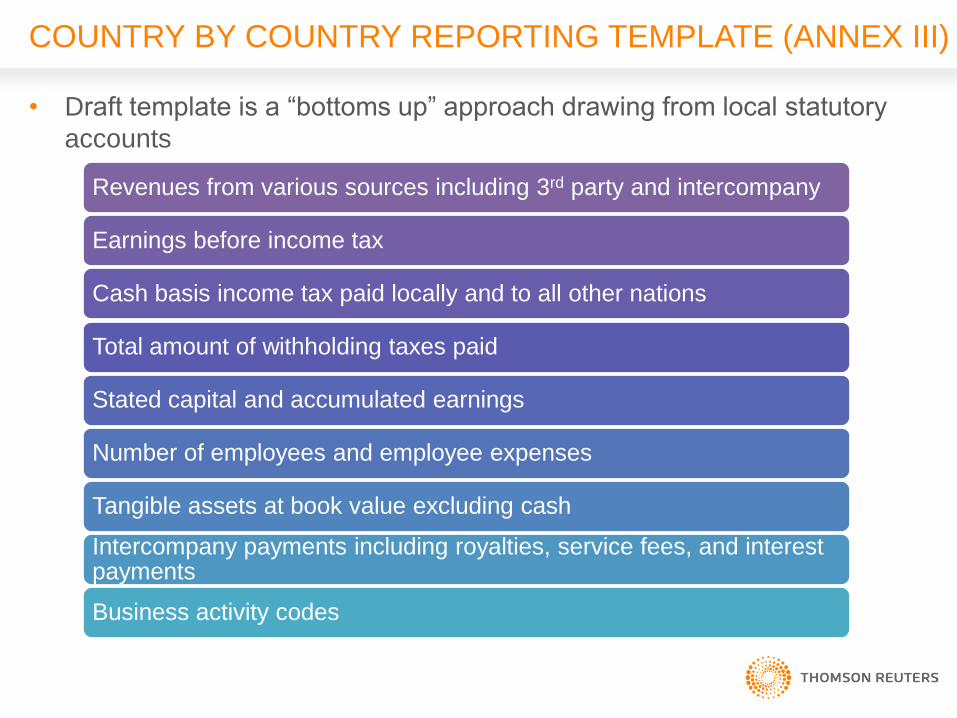

COUNTRY BY COUNTRY REPORTING TEMPLATE (ANNEX III)

• Draft template is a “bottoms up” approach drawing from local statutory

accounts

Revenues from various sources including 3rd party and intercompany

Earnings before income tax

Cash basis income tax paid locally and to all other nations

Total amount of withholding taxes paid

Stated capital and accumulated earnings

Number of employees and employee expenses

Tangible assets at book value excluding cash

Intercompany payments including royalties, service fees, and interest payments

Business activity codes

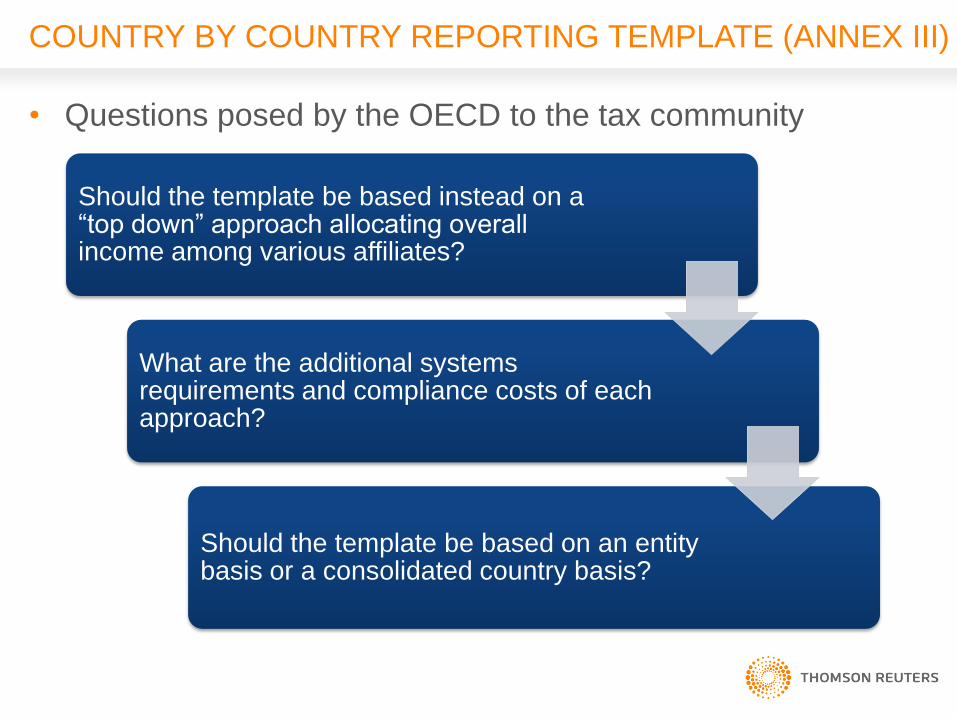

COUNTRY BY COUNTRY REPORTING TEMPLATE (ANNEX III)

• Questions posed by the OECD to the tax community

Should the template be based instead on a “top down” approach allocating overall income among various affiliates?

What are the additional systems requirements and compliance costs of each approach?

Should the template be based on an entity basis or a consolidated country basis?

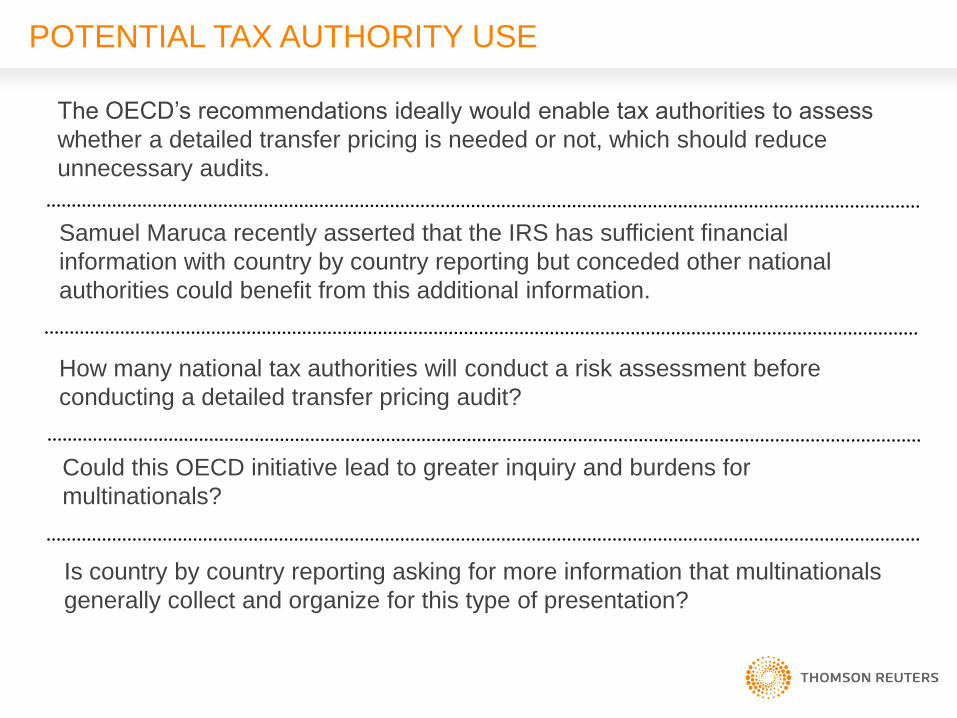

POTENTIAL TAX AUTHORITY USE

The OECD’s recommendations ideally would enable tax authorities to assess

whether a detailed transfer pricing is needed or not, which should reduce

unnecessary audits.

Samuel Maruca recently asserted that the IRS has sufficient financial

information with country by country reporting but conceded other national

authorities could benefit from this additional information.

How many national tax authorities will conduct a risk assessment before

conducting a detailed transfer pricing audit?

Could this OECD initiative lead to greater inquiry and burdens for

multinationals?

Is country by country reporting asking for more information that multinationals

generally collect and organize for this type of presentation?

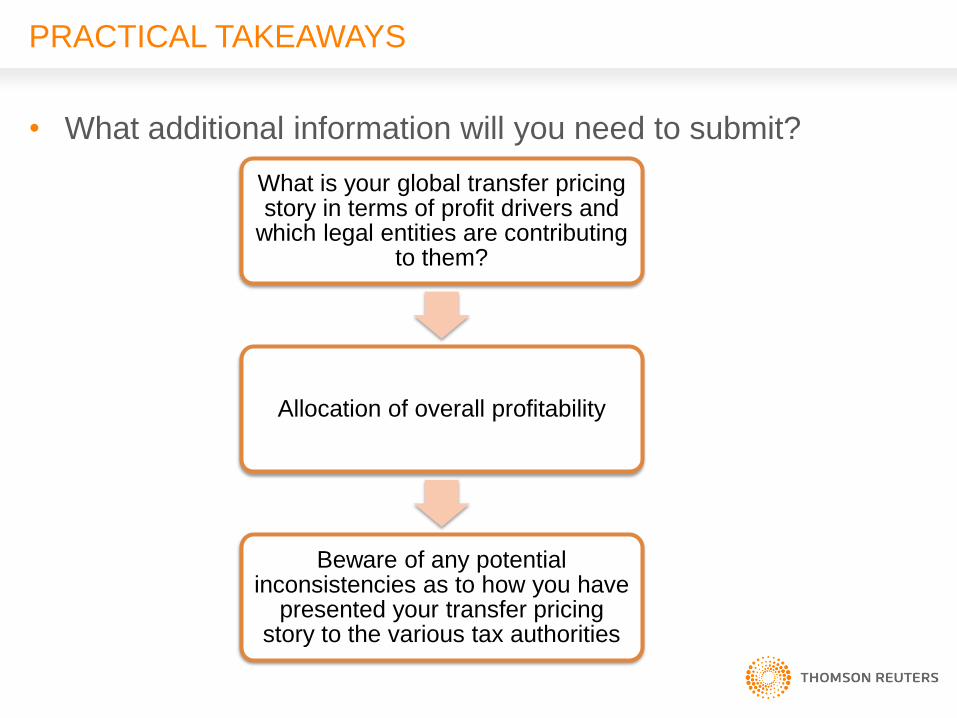

PRACTICAL TAKEAWAYS

• What additional information will you need to submit?

What is your global transfer pricing story in terms of profit drivers and

which legal entities are contributing to them?

Allocation of overall profitability

Beware of any potential inconsistencies as to how you have

presented your transfer pricing story to the various tax authorities

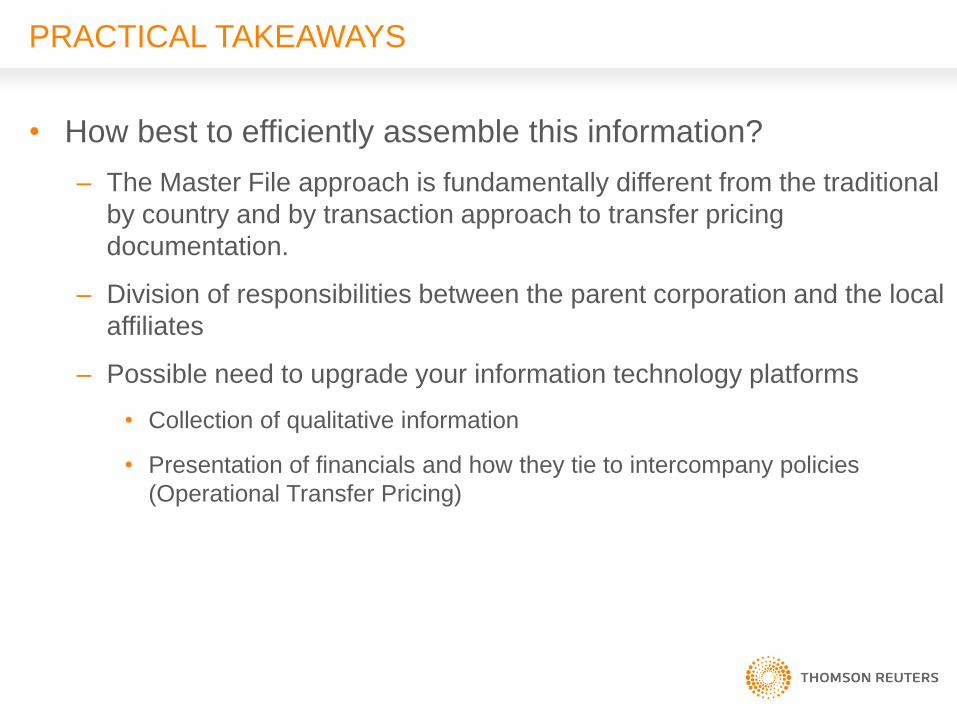

PRACTICAL TAKEAWAYS

• How best to efficiently assemble this information?

– The Master File approach is fundamentally different from the traditional

by country and by transaction approach to transfer pricing

documentation.

– Division of responsibilities between the parent corporation and the local

affiliates

– Possible need to upgrade your information technology platforms

• Collection of qualitative information

• Presentation of financials and how they tie to intercompany policies

(Operational Transfer Pricing)

OPERATIONAL TRANSFER PRICING

• Reporting policy to reporting and defending results -

Challenges

– Ad hoc, spreadsheet intensive process frequently performed by

multiple parties

– Attempting to capture activity which cuts across traditional

reporting lines and is often assessed at unique levels - not

otherwise captured in statutory or management reporting

– Collection and merging of non-accounting, non-system data with

financial information

– Reconciling the results demanded by differing policies

– Review and QA of unsystematic process – internal audit and TP

defense challenges

• Prospect of country-by-country requirements – New

Challenges

– Need to segment centralized results or aggregate local data

– Competing standards and reporting levels

– TP process considerations: centralized vs. decentralized

– Potential need for increased granularity in TP monitoring and reporting

OPERATIONAL TRANSFER PRICING

TRANSFER PRICING SYSTEMS EVOLUTION

• To meet changing TP disclosure demands will require new systems capabilities – Ability to bridge TP policy to existing accounting infrastructure(s)

– Tying together varying systems in different regions and pooling data from wide range of sources

– Seamless integration of local non-financial data

– Automation of the data collection, processing, computations and reporting – maintaining security

– Systemization of TP computations

– Conversion of TP analyses into actionable accounting entries – link policy to results

– Robust audit trail – ability to trace and defend data and calculations used

– Need for increased clarity and flexibility in data - viewing TP transactions and results at multiple levels and split into varying segments

– Flexibility to present the same data to meet numerous, customized formats

OPERATIONAL TRANSFER PRICING IN PRACTICE

• Global Auto Company – Integration of data from over 50 General Ledger systems

– Monitors TP by functional segment, country and legal entity, with transparency into all intercompany transactions

• Diversified Technology, Media and Information Firm

– Management of close to 20 different TP policies

– Segmentation of analysis by both legal entity and business line

• Major Pharmaceutical Manufacturer – Tracking of TP results across 90 different product groups

– Management of true-ups and pricing corrections across entire supply-chain

– Merging of historical and forecasting systems for more complete assessment of TP position

QUESTIONS?