8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 1/32

THE OIL & GAS

GLOBAL SALARYGUIDE 2011Global salaries and recruiting trends.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 2/32

2 | Oil & Gas Salary Guide 2011

Contents

4 Managing Director Reports

6 A Global Perspective

Section One - Salary Information9 Salary Trends

10 Overview

11 Salaries

Section Two - Industry Benefits14 Overview

15 Top Beneits by Company Type

16 Top Beneits by Region

Section Three - Industry Employment19 Overview

20 Diversity

21 Movement o Workorce

22 Experience and Tenure24 Employment Mix

26 Staing Levels

Section Four - Economic Outlook28 Overview

29 Salaries

THANK YOUWe would like to express our gratitude to all those organisations and individuals who participatedin the collection o data or this year’s survey. More than 10,000 people responded which wascertainly overwhelming. This has ensured that we can produce an inormative document to help

support your business decisions.

Disclaimer: The Oil & Gas Global Salary Guide 2011 is representative o a value added service to our clients and candidates. Whilst every care is taken in the collection andcompilation o data, the survey is interpretive and indicative, not conclusive. Thereore inormation should be used as a guideline only and should not be reproduced intotal or by section without written permission rom Hays.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 3/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 4/32

MATT UNDERHILL

MANAGING DIRECTOR REPORT

“The comparison o salaries between our 2010 and 2011 guides appears tobe a good measure o the pace and strength o each country’s respectiverecovery within the industry.”

I am delighted to introduce this year’s salary guide and am particularly pleased to report that the guide is bigger and better than last year’s.We were inundated with responses to our survey so irstly a big thank you to all those who took the time to contribute.

Since our inaugural launch last year the interest in this guide has been enormous. It seems such a document has ound a signiicant place inthe industry or those wishing to understand where the market sits in terms o remuneration and employment trends.

Taking a global view o the igures we could summarise by saying the average permanent remuneration has remained steady. This howeverwould be misleading when considering the changes in economic ortunes between individual countries and the luctuations in salaries wehave seen within the year.

The data or this year’s guide was collected during September and October 2010 by which time most o the world’s economies were in ullrecovery. This said we know rom our own recruitment activities that movements in permanent salaries do take time to wash through theindustry. So whilst the industry recovered towards the end o 2009, salaries continued to all until early 2010, beore starting to climb againlater in the year. Thereore the comparison o salaries between our 2010 and 2011 guides appears to be a good measure o the pace andstrength o each country’s respective recovery within the oil and gas market.

The last two years have seen a huge number o overseas employees laid o as demand ell through the recession. While some o this slackwas taken back up in 2010, those at the bottom o the career ladder suered most. Thereore it is no coincidence that salaries ell urthest incountries that traditionally provide lower cost labour to the industry.

In line with this trend we also saw a huge amount o repatriation o high skilled labourrom all parts o the globe, with many taking up positions at home or retiring rom theindustry altogether. Again these industry trends were relected in the igures with alling

levels o overseas workers and tenure dropping. At the other end o the spectrum, andexceeding the number o increased retirements, we also saw a big drop in new entries tothe industry. So paradoxically experience levels actually increased.

Contractor rates are in essence a great deal more reactive to changes in the industry andthereore ollowed the recovery with less delay. Consequently we have seen growth acrossthe board o between 10 and 20 per cent with only a ew cases going against the trend.This said there is still some way to go beore day rates recover topre-recession levels.

The data does show continuing use o temporary contractors. In such a luctuating marketthis should perhaps be no surprise. We also ound that the expat package is ar rom dyingout; a trend we eel goes against that o other industries.

We are pleased to see optimism in the industry continues to rise ater a couple o toughyears. This optimism has yet to overheat the market and consequently it is a good marketor both recruiters and job seekers. Whilst there are still plenty o opportunities available,rates and remuneration are not being inlated to untenable levels.

Finally I would like to thank our partners, Oil and Gas Job Search, without which we wouldnot have been able to map out the industry as we have done. I would also like to thank allthose that worked on collating and producing such a great document this year.

Matt Underhill, Managing Director, Hays Oil & Gas

4 | Oil & Gas Salary Guide 2011

Matt Underhill

Managing Director, Hays Oil & Gas

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 5/32

DUNCAN FREER

MANAGING DIRECTOR REPORT

“I was extremely pleased that almost 11,000 industry proessionals rommore than 20 diferent disciplines completed the survey. This equates to avery impressive increase on the previous year.”

We are again delighted to partner with Hays to deliver to the industry the second issue othe Global Oil and Gas Salary Guide.

Our objective is to provide both recruiters and job seekers with a better understanding othe approximate levels o pay, beneits and conidence that currently exist in the market. Inso doing, employers and employees can ensure they are getting value or money in theiremployment dealings. Clearly, undertaking a global survey within such a large industry isno small task, and equally to drill down into speciic roles or geographic regions wouldstart to render the data inaccurate. We have thereore concentrated on the averages orgroups o employees in the industry deined by: which country they are working in andwhere they are rom; the discipline area in which they work; how much experience theyhave; and how they are employed (i.e. permanent sta or temporary contract).

Last year’s inaugural guide was completed by over 7,000 participants with the resultsbeing published in February 2010. Following publication, we oered ree access via theOilandgasjobsearch and Hays websites. This led to over 35,000 downloads within the irstmonth o launch. The eedback rom our candidates and clients was very encouraging andit quickly became apparent that we had created a document without compare in theindustry, and its insights and level o detail was attracting huge levels o interest. Thisencouraged us to repeat the undertaking and once again we approached our customersand users to complete a detailed survey that would orm the basis o the 2011 guide. Initiallevels o participation were astounding and I was extremely pleased that almost 11,000industry proessionals rom more than 20 dierent disciplines completed the survey. Thisequates to a very impressive increase on the previous year.

The 2011 guide diers rom last year’s in that we have been able to provide details on thesalary trends o dierent types o jobs in a range o locations by using last year as abenchmark. We have also included more data in the beneits and packages section: alwaysan emotive subject. In addition, we have expanded the number o countries in this year’sguide to over 50 which means that we have now covered the majority o the ‘signiicant’oil and gas locations.

As is demonstrated in our igures a level o conidence has been restored to many o the global energy markets evidenced by there-emergence o the oil sands activity in Canada and the Australian market leading the way with several huge projects passing inalinvestment decision (with more to come in 2011). The South East Asian markets have also seen strong expansion in exploration andproduction to satisy growing demand. One o the other main points rom the guide is that a greater number o proessionals are moreoptimistic about the uture even in light o the diicult market conditions elsewhere. With greater stability in the oil price and moreconidence in inancial markets, I am equally as optimistic about the industry or 2011 and beyond.

Oilandgasjobsearch has mirrored the industry as a whole over the last 12 months with an increase in jobs posted, applications to jobs and amassive leap in the number o site users. We have ar more clients than we did last year and this again is a sign o the increased conidencein the sector. We have recently opened a new oice in Australia to help ulill the needs o our Australian and Paciic based clients andcandidates. We are also looking to expand in the Middle East during 2011.

I am sure that the detailed content o the guide will prove to be an invaluable source o data or many in the industry rom recruiters to jobseekers alike.

I would like to take this opportunity to thank our partners, Hays Oil & Gas, and all the participants who took the time to complete the survey.

Duncan Freer, Managing Director, Oil and Gas Job Search

Oil & Gas Salary Guide 2011 | 5

Duncan FreerManaging Director, Oil and Gas Job Search

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 6/32

6 | Oil & Gas Salary Guide 2011

A GLOBAL PERSPECTIVE

Alberta

Strengthening oil pricegives oil sands new lie in

Western Canada.

North Sea

Several new discoveries give

the region hope that a slow

decline o the North Seaindustry can be reversed.Optimism returns as the

region has a stronger than

expected recovery rom theglobal recession o 2009.

West Africa

Increasing production and

exploration activity provides

the region with muchneeded orward revenues.

However the riches on

ofer bring conflict as allstakeholders struggle to

maximise their returns.

Gulf of Mexico

Massive blow out on the

Deepwater Horizon oil rigtakes 11 lives and creates an

environmental nightmare

at 1500 metres below the

surace. The well takes 12weeks to cap and stalls

the American ofshore

exploration industry.

Brazil Coast

Further discoveries in the pre

salt fields of Eastern Brazil

add urther uel to a growingofshore market. Local ship

yards kick into overdrive to

make sure the fields can be

adequately serviced withFPSO’s and support vessels.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 7/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 8/32

8 | Oil & Gas Salary Guide 2011

SECTION ONE

SALARY INFORMATION

Over 20 per cent o employers expect salaries

to increase by more than 10 per cent in the next12 months.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 9/32

Salary Survey 2011 | 9

Three quarters o respondentsexpect salaries to increase in thenext 12 months.

Just over hal the respondentsreceived a pay increase in thelast 12 months.

SALARY TRENDSSALARY INFORMATION

Reduced

Remained static

Risen less than 5%

Risen more than 5%

10.5%

39.7%

20.4%

29.4%

12%

44%16%

28%

2010

2011

Decrease

Remain static

Increase up to 5%

Increase more than5% but less than 10%Increase morethan 10%

3.1%

21.9%

28.0%

25.3%

21.6%

4%

28%

26%

23%

19%

2010

2011

In the last 12 month has your salary:

In the next 12 months, do you expect salaries to:

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 10/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 11/32

Algeria

Angola

Argentina

Australia

Azerbaijan

Bahrain

Brazil

Canada

China

Colombia

Egypt

France

IndiaIndonesia

Iran

Iraq

Italy

Japan

Kazakhstan

Korea

Kuwait

Libya

Malaysia

Mexico

Netherlands

New Zealand

Nigeria

Norway

Oman

Pakistan

Papua New Guinea

Philippines

Poland

Portugal

Qatar

Romania

Russia

Saudi ArabiaSingapore

South Africa

Spain

Sudan

Trinidad & Tobago

Turkey

Turkmenistan

United Arab Emirates

United Kingdom

USA

Venezuela

Vietnam

Yemen

42,900 430 93,400 770

33,500 410 108,500 1,040

66,000 N/A 119,000 660

143,700 1,080 144,600 1,020

37,900 490 141,600 960

56,000 N/A 75,000 570

99,500 570 99,500 780

129,900 970 111,400 910

49,400 540 109,900 910

49,700 440 177,500 1,590

44,000 440 121,300 990

106,000 830 111,300 930

35,600 400 104,400 69041,800 430 125,000 930

40,900 390 83,400 470

21,700 280 94,800 1,060

73,900 730 88,600 740

N/A 580 128,300 1,050

32,400 390 129,400 1,060

120,800 560 130,400 1,010

N/A 550 72,900 640

42,300 440 87,400 820

50,200 490 109,900 740

57,900 530 95,700 780

124,300 1,280 107,500 880

107,200 860 101,400 1,190

39,600 460 126,200 940

130,300 1,290 119,800 1,020

40,400 580 72,200 610

25,500 360 60,300 1,300

31,200 300 197,200 1,000

37,600 390 135,000 1,270

54,100 460 77,500 1,010

N/A 340 N/A 920

69,000 550 77,300 610

38,900 450 120,000 570

63,000 550 127,800 1,020

61,200 480 65,200 54066,300 500 98,500 720

76,200 630 92,500 540

77,000 570 93,800 900

36,800 450 62,000 720

49,700 440 184,700 1,290

68,200 500 82,600 470

N/A N/A N/A 1,060

61,200 610 69,200 550

86,700 820 76,300 670

117,000 840 110,700 870

59,700 520 111,200 890

29,600 240 140,400 1,080

23,300 290 97,800 870

Imported LabourLocal Labour

CountryAverage

annual salary

Average

daily rate

Average

annual salary

Average

daily rate

Oil & Gas Salary Guide 2011 | 11

SALARIESSALARY INFORMATION

Notes: All igures are base salaries, quoted in US dollars. Annual salaries to the nearest one hundred, daily rates to the nearest ten.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 12/32

Notes: All igures are base salaries, quoted in US dollars. Annual salaries to the nearest one hundred, daily rates to the nearest ten.

EPCM - Engineering, procurement and construction management;

HSE - Health, saety and environment; QA/QC - Quality assurance/quality control.

Business Development/ CommercialConstruction/ Installation

Downstream Operations Management

Drilling

Electrical

Estimator/ Cost Engineer

Geoscience

Health, Safety and Environment (HSE)

Logistics

Marine/Naval

Mechanical

Piping

Process (chemical)

Production Management

Project Controls

Quality Assurance/Quality Control (QA/QC)

Reservoir/ Petroleum Engineering

Structural

Subsea/ Pipelines

Supply Chain/ Procurement

Technical Safety

Instrumentation, Controls & Automation

Maintenance

ConsultancyContractor

EPCM

Equipment Manufacture and Supply

Global Super Major

Oil Field Services

Operator

42,000 60,600 93,900 146,40034,700 46,600 81,000 125,900

45,200 56,900 83,900 115,900

46,700 59,100 94,600 131,800

35,900 49,100 77,900 109,400

30,700 50,800 80,500 106,300

41,500 64,900 93,700 138,000

36,300 52,300 86,500 115,100

34,700 45,400 72,300 86,900

54,900 64,500 92,200 115,900

34,800 47,400 70,500 107,300

30,500 42,300 66,500 101,200

34,400 50,400 77,600 126,400

43,400 75,800 95,900 124,700

44,600 59,900 94,600 124,100

38,500 49,800 83,000 110,700

45,000 58,100 86,500 109,600

42,600 47,100 84,100 111,100

46,600 89,100 122,600 137,400

39,300 51,500 79,900 115,500

34,400 48,500 87,700 108,900

42,600 50,600 70,800 112,000

23,300 33,200 57,900 112,900

44,800 57,400 92,600 129,70039,600 53,900 82,000 114,600

43,900 54,900 84,300 139,600

36,400 55,400 75,200 100,000

53,400 71,000 107,500 136,400

39,200 50,900 77,300 97,400

45,300 70,700 103,600 141,300

Years of experience

Discipline area

Company type

10 to 19

10 to 19

20 +

20 +

0 to 4

0 to 4

5 to 9

5 to 9

SALARIESSALARY INFORMATION

12 | Salary Survey 2011

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 13/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 14/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 15/32

Salary Survey 2011 | 15

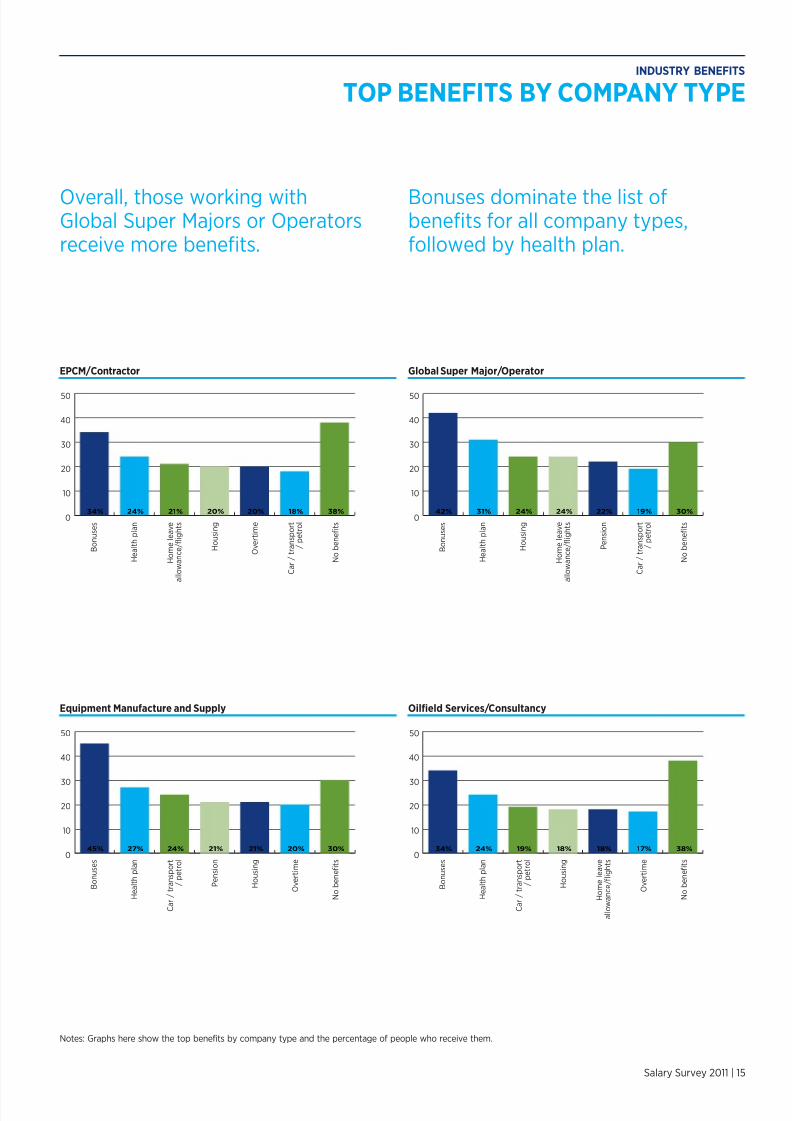

TOP BENEFITS BY COMPANY TYPEINDUSTRY BENEFITS

Bonuses dominate the list obenefits or all company types,ollowed by health plan.

Overall, those working withGlobal Super Majors or Operatorsreceive more benefits.

Global Super Major/Operator

Oilfield Services/Consultancy

0

10

20

30

40

50

B o n u s e s

H e a l t h p l a n

H o m e l e a v e

a l l o w a n c e / fl i g h t s

H o u s i n g

O v e r t i m e

C a r / t r a n s p o r t

/ p e t r o l

N o b e n e fi t s

34% 24% 21% 20% 20% 18% 38%

0

10

20

30

40

50

B o n u s e s

H e a l t h p l a n

C a r / t r a n s p o r t

/ p e t r o l

P e n s i o n

H o u s i n g

O v e r t i m e

N o b e n e fi t s

45% 27% 24% 21% 21% 20% 30%

0

10

20

30

40

50

B o n u s e s

H e a l t h p l a n

H o u s i n g

H o m e l e a v e

a l l o w a n c e / fl i g h t s

P e n s i o n

C a r / t r a n s p o r t

/ p e t r o l

N o b e n e fi t s

42% 31% 24% 24% 22% 19% 30%

0

10

20

30

40

50

B o n u s e s

H e a l t h p l a n

C a r / t r a n s p o r t

/ p e t r o l

H o u s i n g

H o m e l e a v e

a l l o w a n c e / fl i g h t s

O v e r t i m e

N o b e n e fi t s

34% 24% 19% 18% 18% 17% 38%

EPCM/Contractor

Equipment Manufacture and Supply

Notes: Graphs here show the top beneits by company type and the percentage o people who receive them.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 16/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 17/32

Salary Survey 2011 | 17

On average, those working in the Middle East receive the most benefitswhile those in Australasia receive the least.

INDUSTRY BENEFITS

TOP BENEFITS BY REGION

Middle EastOn average, beneits received by those working in theMiddle East are valued at 38% o their total package:

South AmericaOn average, beneits received by those working inSouth America are valued at 35% o their total package:

0

10

20

30

40

50

B o n u s e s

P e n s i o n

H e a l t h p l a n

C a r / t r a n s p o r t

/ p e t r o l

O v e r t i m e

M e a l a l l o w a n c e

N o b e n e fi t s

16% 15% 11% 8% 6% 5% 43%

0

10

20

30

40

50

H e a l t h p l a n

B o n u s e s

P e n s i o n

O v e r t i m e

C a r / t r a n s p o r t

/ p e t r o l

M e a l a l l o w a n c e

N o b e n e fi t s

29% 28% 17% 13% 11% 11% 30%

0

10

20

30

40

50

B o n u s e s

H o u s i n g

H o m e l e a v e

a l l o w a n c e / fl i g h t s

H e a l t h p l a n

O v e r t i m e

C a r / t r a n s p o r t

/ p e t r o l

N o b e n e fi t s

42% 32% 30% 27% 24% 22% 23%

0

10

20

30

40

50

B o n u s e s

H e a l t h p l a n

M e a l a l l o w a n c e

T r a i n i n g

P e n s i o n

C a r / t r a n s p o r t

/ p e t r o l

N o b e n e fi t s

36% 30% 19% 19% 17% 17% 24%

EuropeOn average, beneits received by those working inEurope are valued at 15% o their total package:

North AmericaOn average, beneits received by those working inNorth America are valued at 23% o their total package:

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 18/32

SECTION THREE

INDUSTRY EMPLOYMENT

There was a tide o repatriation over the

past 12 months as experienced sta returnedhome to seek work.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 19/32

Salary Survey 2011 | 19

DIVERSITYGenderThe industry is still heavily dominated by male employees, and theseigures are consistent with our own experience o emaleparticipation within the industry. Clearly the trend line on thispercentage will make or interesting reading in uture years withmore women encouraged to enter the industry.

Age bracketWhilst most o the demographics provided by the survey are whatyou would expect, we know rom other industries that the numbero under 25’s in the industry is comparatively low. Whether thismerely relects a higher need or tertiary qualiications in theindustry or actually reveals an underinvestment in people being

brought into the industry is open or debate. Again we will monitorthis igure closely in coming years.

Based in country of originThere is an increase in locally based employees with 58.1% workingin their country o origin versus 54.4% or last year. These iguresreinorce the trend through 2009 and early 2010 that saw many inthe industry return to their home country. This tide o repatriationwas driven by a great number o experienced sta and contractorsbeing laid o through the downturn. Many o these returned hometo seek work, and did so successully as the market reboundedthrough 2010.

Analysing the igures urther we also ound some evidence o anabove average level o early retirements particularly within thosecontractors on higher day rates rom high paying countries.

MOVEMENT OF WORKFORCEThe trend or repatriation through 2009/10 aected all o theigures. This is highlighted with the sharp decreases in oreignimports in Asia, Arica and Europe. Only Australasia and the MiddleEast showed an increase in oreign imports, relecting the tworegions’ quick recovery rom the downturn.

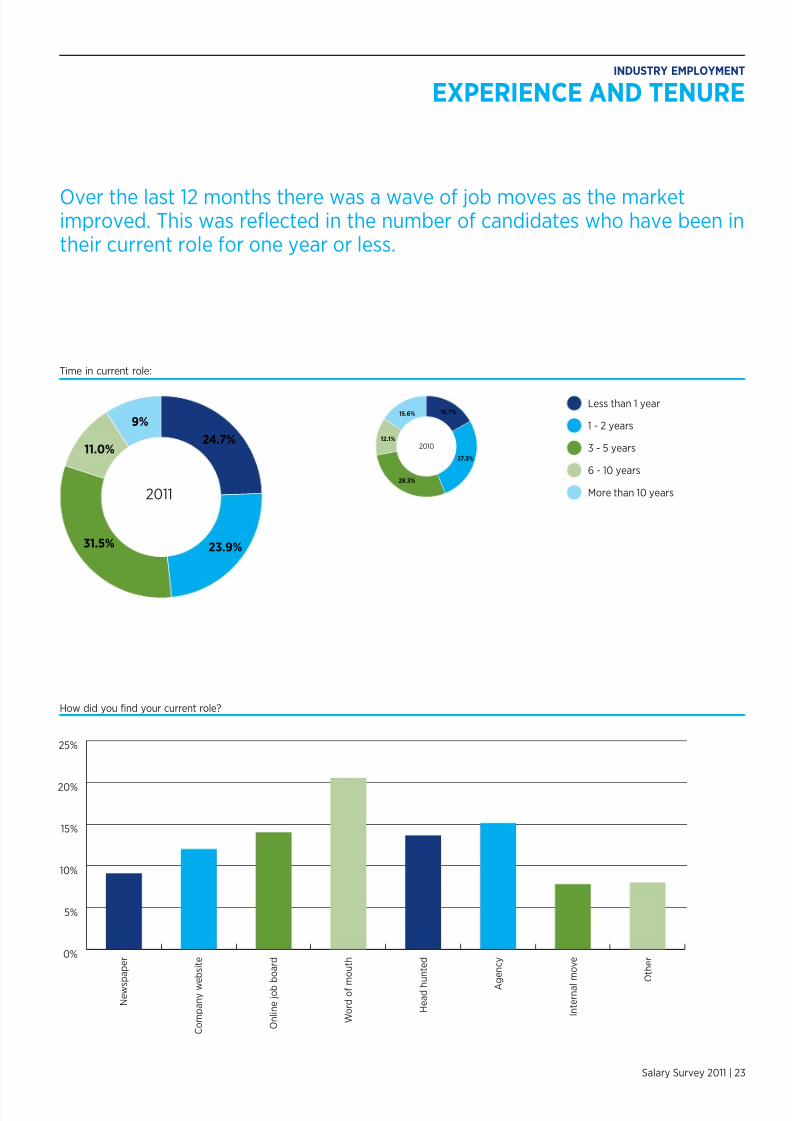

YEARS OF EXPERIENCEConsistent with the previous year’s downturn there is a sharp all innew comers to the industry reducing those with less than our yearsexperience to just under 20% o the workorce.

Whilst demand or those with less experience was weak we did seeemployers take advantage o an experience rich market and a waveo job moves lowed through the industry as the market improved.This was relected in the numbers in their current role or one yearor less, with the total climbing sharply rom last year’s 16.8% to thisyear’s igure o 24.7%. In general there was an equally sharp drop

or those in their current role or more than 10 years, againindicating the layo o experienced highly paid individuals thatoccurred whilst the recession was at its depth, and the act thatmany o them never returned to the workorce.

Clearly worldwide demand or oil and gas is not on the wane, and inthe longer term such periods o neglect in bringing new talent intothe industry will surely hamper growth. With the availability o skillsdropping, those already in the industry will undoubtedly be the onesto beneit with rising salaries and day rates.

EMPLOYMENT MIX BY COMPANY TYPEThere are some consistent trends in employment through the industrywhen reviewing employment mix. These are namely an increase in thepercentage o those employed on a permanent basis, and acorresponding decrease in the use o contractors. With contractor dayrates running at nearly double that o permanent sta salaries (on a‘cash or cash’ basis and assuming a ull 240 days a year worked) it isnot diicult to understand why employers sought to take advantage osuch a candidate rich market through 2009 and 2010. The drop inusing contractors covers all company types. Interestingly most o thisdrop is or those contracted through agencies however Oil FieldServices companies buck this trend with an increase in agency use butsharp decreases in direct contractors.

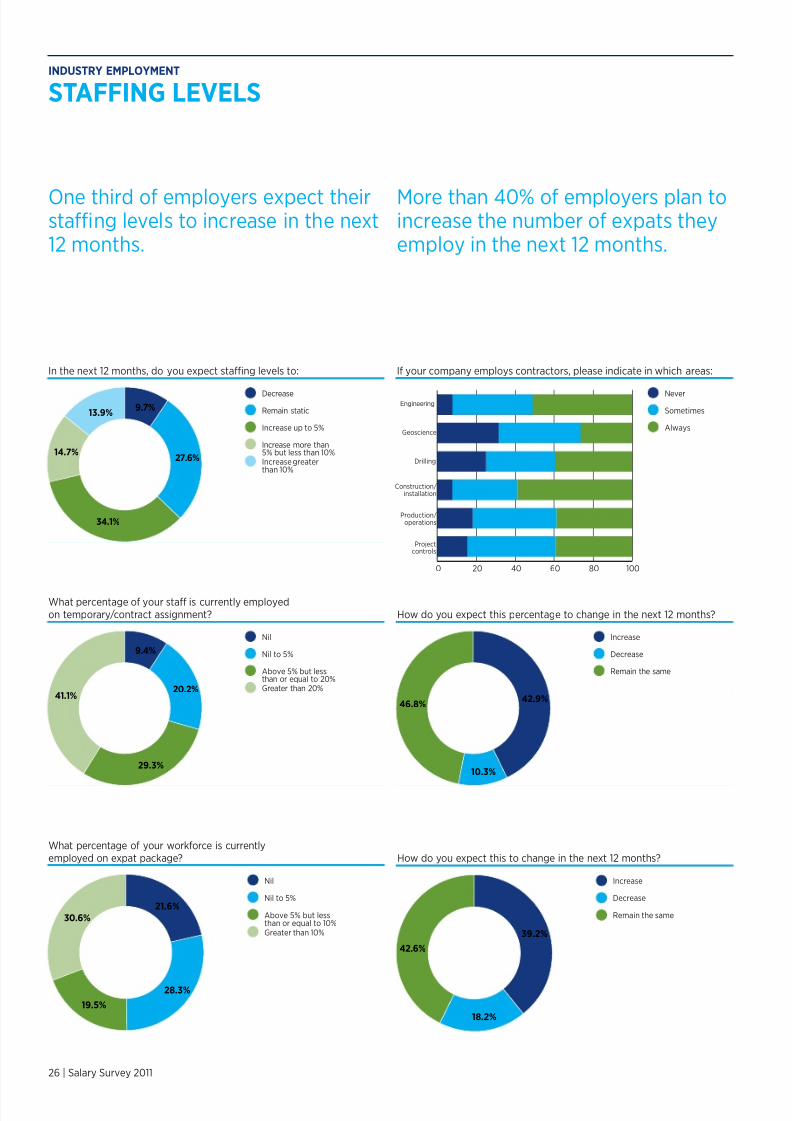

STAFFING LEVELSOnce again ollowing on rom last year’s results respondents arepositive about the immediate uture o the industry with less than10% expecting any decrease in staing levels over the next year.

Somewhat surprisingly there is a marked increase in expat packagesin the industry. This is despite most market commentary predictinga phasing out o such employment as local talent capabilities rise.The orward expectations on the use o expats looks likely tocontinue too, with nearly 43% expecting increases in the next yearverses only 10.3% showing a decrease.

The use o contractors continues to rise in the industry with 41% orespondents indicating that 20% or more o their sta are employedon a temporary/contract basis as opposed to ull time sta. Againwe see this trend continuing with over 39% o respondentsexpecting this to increase verses only 18% decrease.

As would be expected the use o contractors and temporaryemployment continues to be widespread through all sectors o theindustry with those disciplines returning the highest utilisation useshown on page 26.

OVERVIEW

“Respondents were positive about the immediate uture o the industry withless than 10% expecting any decrease in sta ng levels over the next year.”

INDUSTRY EMPLOYMENT

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 20/32

20 | Salary Survey 2011

The highest percentage o womenin oil and gas are working inbusiness development.

The number o people workingin their country o origin increasedby 3.7%.

DIVERSITYINDUSTRY EMPLOYMENT

9 2 . 9 %

7 . 1 %

Male Female

5 8 . 1 %

4 1 . 9 %

Yes No

5 4 . 4 %

4 5 . 6 %

Yes No

Business DevelopmentCommercialProject Controls

Health, Saety andEnvironment (HSE)Supply Chain/ Procure

Geoscience

Other

14.0%

8.6%

7.2%

5.7%

5.4%

59.0%

Diversity o sta:

Are you based in your country o origin?2011 2010

Women in oIl and gas:

Age bracket:

0%

5%

10%

15%

20%

25% Male

Female

a n d u n d e r

2 5 - 2 9

3 0 - 3 4

3 5 - 3 9

4 0 - 4 4

4 5 - 4 9

5 5 - 5 9

5 0 - 5 4

5 a n d o v e r

6 0 - 6 4

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 21/32

Salary Survey 2011 | 21

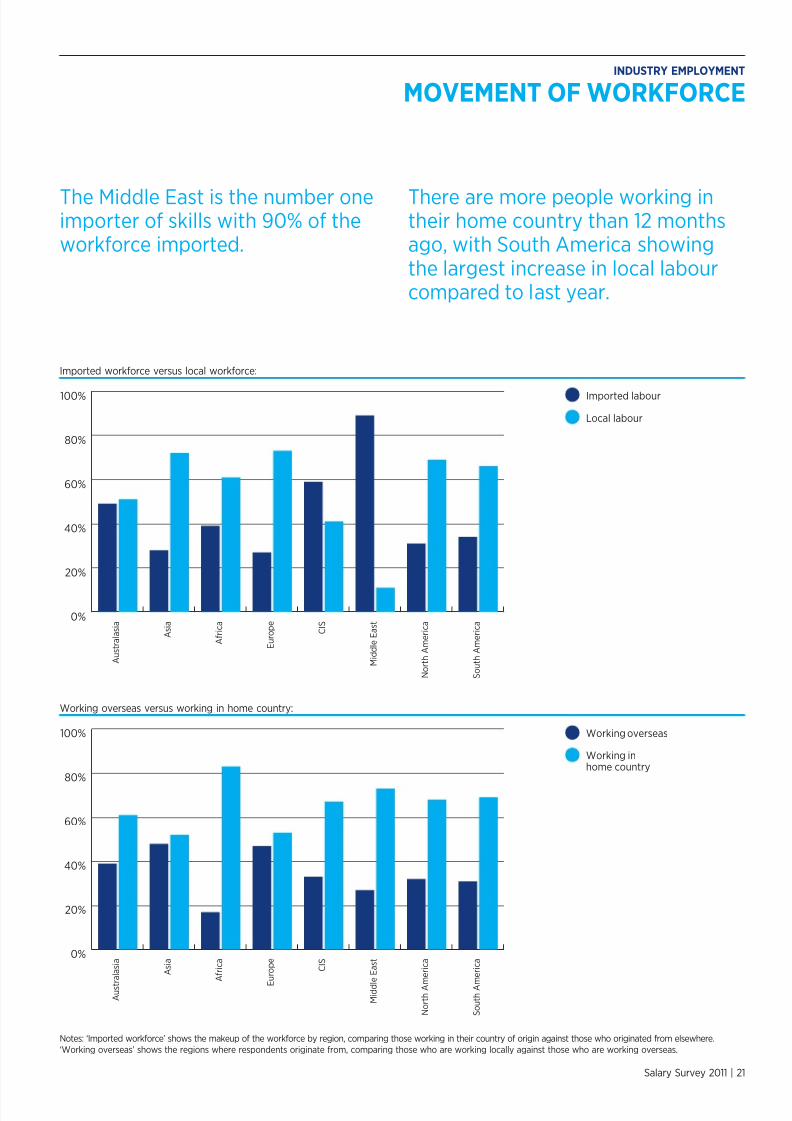

The Middle East is the number oneimporter o skills with 90% o theworkorce imported.

There are more people working intheir home country than 12 monthsago, with South America showingthe largest increase in local labourcompared to last year.

MOVEMENT OF WORKFORCEINDUSTRY EMPLOYMENT

Imported workorce versus local workorce:

Working overseas versus working in home country:

A u s t r a l a s i a

A s i a

A f r i c a

E u r o p e

M i d d l e E a s t

N o r t h A m e r i c a

S o u t h A m e r i c a C

I S

Imported labour

Local labour

0%

20%

40%

60%

80%

100%

A u s t r a l a s i a

A s i a

A f r i c a

E u r o p e

M i d d l e E a s t

N o r t h A m

e r i c a

S o u t h A m

e r i c a C

I S0%

20%

40%

60%

80%

100% Working overseas

Working inhome country

Notes: ‘Imported workorce’ shows the makeup o the workorce by region, comparing those working in their country o origin against those who originated rom elsewhere.

‘Working overseas’ shows the regions where respondents originate rom, comparing those who are working locally against those who are working overseas.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 22/32

22 | Salary Survey 2011

There was a sharp all in newcomers to the industry, reducing those withless than our years experience to just under 20% o the workorce.

EXPERIENCE AND TENUREINDUSTRY EMPLOYMENT

0 - 4

5 - 9

10 - 19

20 +

19.9%

28.5%

22.8%

28.8%

14.8%

18.7%

26.7%

39.8%

16.9%

25.6%

31.7%

25.8%

26.5%

22.0%

19.3%

32.2%

24.2%

21.6%

25.8%

28.4%

Years o experience:

For specific discipline areas:Construction/ Installation

Project Controls

Geoscience

Subsea/ Pipelines

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 23/32

Salary Survey 2011 | 23

Over the last 12 months there was a wave o job moves as the marketimproved. This was reflected in the number o candidates who have been intheir current role or one year or less.

INDUSTRY EMPLOYMENT

EXPERIENCE AND TENURE

How did you ind your current role?

Less than 1 year

1 - 2 years

3 - 5 years

6 - 10 years

More than 10 years

23.9%

24.7%11.0%

31.5%

9%

27.3%

16.7%

12.1%

28.3%

15.6%

2010

2011

N e w s p

a p e r

C o m p a n y w e

b s i t e

O n l i n e j o b b

o a r d

W o r d o f m

o u t h

A g

e n c y

I n t e r n a l m o v e

O t h e r

H e a d h u n t e d

0%

5%

10%

15%

20%

25%

Time in current role:

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 24/32

24 | Salary Survey 2011

Permanent/ull time staf levels have increased by an average o 2.7%across all company types in comparison to other employment.

EMPLOYMENT MIXINDUSTRY EMPLOYMENT

Global Super Major Operators

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

GlobalSuper Major

Operators

EPCM

Equipmentmanuacturer

& supplier

Oil FieldServices

Consultancy

Contractors

Permanent

Permanent /part timeContracteddirectContractedthrough agency

0% 20% 40% 60% 80% 100%

Employment mix by company type:

Percentage change from 2010 to 2011

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 25/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 26/32

26 | Salary Survey 2011

More than 40% o employers plan toincrease the number o expats theyemploy in the next 12 months.

One third o employers expect theirsta ng levels to increase in the next12 months.

STAFFING LEVELSINDUSTRY EMPLOYMENT

I your company employs contractors, please indicate in which areas:

What percentage o your workorce is currentlyemployed on expat package? How do you expect this to change in the next 12 months?

Decrease

Remain static

Increase up to 5%

Increase more than5% but less than 10%Increase greaterthan 10%

9.7%

27.6%

34.1%

14.7%

13.9%

Nil

Nil to 5%

Above 5% but lessthan or equal to 20%Greater than 20%

9.4%

20.2%

29.3%

41.1%

Increase

Decrease

Remain the same

42.9%

10.3%

46.8%

Nil

Nil to 5%

Above 5% but lessthan or equal to 10%Greater than 10%

21.6%

28.3%

19.5%

30.6%

Increase

Decrease

Remain the same

39.2%

18.2%

42.6%

0 20 40 60 80 100

Never

Sometimes

Always

Engineering

Geoscience

Drilling

Construction/installation

Production/operations

Projectcontrols

In the next 12 months, do you expect staing levels to:

What percentage o your sta is currently employedon temporary/contract assignment? How do you expect this percentage to change in the next 12 months?

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 27/32

Oil & Gas Salary Guide 2011 | 27

SECTION FOUR

ECONOMIC OUTLOOK

More than hal o respondents describe

their outlook in the current employmentmarket as positive.

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 28/32

28 | Salary Survey 2011

The Middle East will be a key ocus or hal the respondents operations overthe next 12 months.

OVERVIEW

The good news or the industry is that the majority o respondentsare conident about the state o the employment market. This year54.8% are positive or extremely positive which is a modest increaseon last year’s igure o 50.1%. However we do not yet see the levelso enthusiasm in the market that indicate job seekers are once againully in the ascendancy (with the exception o a ew markets), and itmay take a ew months more o sustained growth beore thismaterialises.

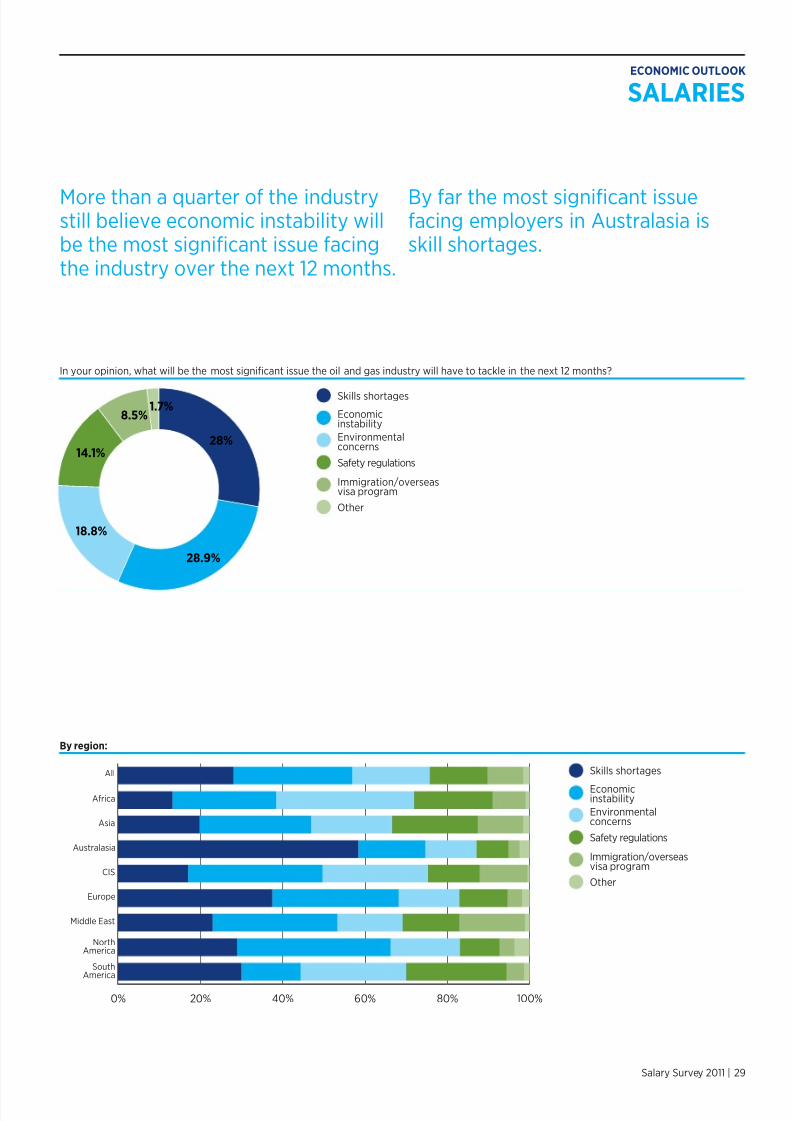

It will also take some time or the ull eects o the downturn towash through the industry and be orgotten. With nearly 29% orespondents still believing that economic instability is the majorconcern over the next twelve months, it is clearly not yet behind us.

It is perhaps not surprising, given the events o the last year, thatmany in the industry are also concerned or the environment andsaety. Time will tell whether this concern is maintained through tonext year.

ECONOMIC OUTLOOK

Outside o your own regional area, which geographic areas will be a key ocus or your operations over the next 12 months?

C e n t r a l A s i a

E a s t A s i a

A u s t r a l a s i a

E a s t e r n a n d

C o n t i n e n t a l

E u r o p e

U K a n d

N o r t h e r n

E u r o p e

M i d d l e E a s t

S o u t h

A m e r i c a

N o r t h

A m e r i c a

O t h e r

A f r i c a0%

10%

20%

30%

40%

50%

Negative

Neutral

Positive

Extremely positive

11.8%

33.4%45.1%

9.7%15.8%

34.1%

43.6%

6.5%

2010

2011

How would you describe your conidence in the current employment market?

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 29/32

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 30/32

30 | Oil & Gas Salary Guide 2011

ABOUT OIL AND GAS JOB SEARCH

Oil and Gas Job Search is the premier global oil and gas industry job site.We are a one stop solution or your job search and recruitment needs.

When it comes to locating the best oil and gas jobs and the bestcandidates in the worldwide oil and gas industry, Oil and Gas Job Search isthe most efective online solution available.

Oil and Gas Job Search launched in 2000 and is now firmly established asthe world’s leading online resource or the oil and gas industry.

The site currently logs over 300,000 visitors every month. Our candidatedatabase eatures more than 320,000 resumes and is growing at the rateo over 10,000 per month.

320,000+ resumes o proessional candidates on our database

10,000+ additional candidates every month

9,000+ jobs posted on the website every month

1,000+ clients located in all major oil and gas locations

10+ years in business

www. oilandgasjobsearch.com

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 31/32

180,000+TEMPORARY AND CONTRACT STAFF ENGAGED EACH WEEK

50,000+PEOPLE PLACED IN PERMANENT JOBS EACH YEAR

6,000+RECRUITING EXPERTS WORLDWIDE

270+OFFICES ACROSS 30 COUNTRIES

41+YEARS OF EXPERIENCE

Oil & Gas Salary Guide 2011 | 31

ABOUT HAYS

8/3/2019 Ong Salary

http://slidepdf.com/reader/full/ong-salary 32/32