Overcoming barriers to CCS

through international

collaboration

Toby Lockwood

IEA Clean Coal Centre webinar, 27 Sep 2017

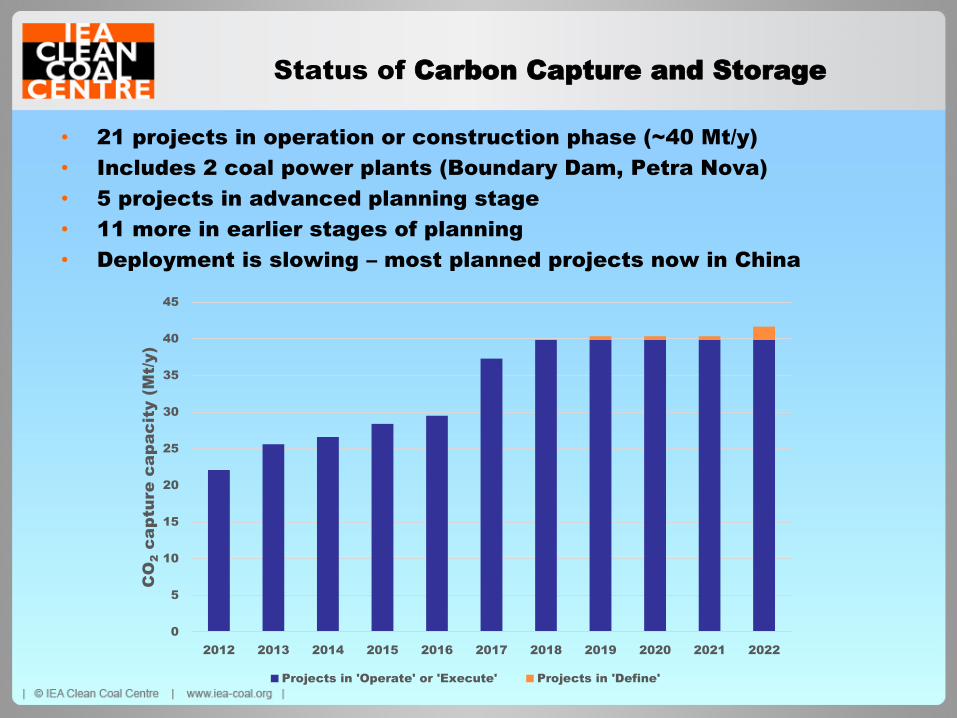

Status of Carbon Capture and Storage

• 21 projects in operation or construction phase (~40 Mt/y)

• Includes 2 coal power plants (Boundary Dam, Petra Nova)

• 5 projects in advanced planning stage

• 11 more in earlier stages of planning

• Deployment is slowing – most planned projects now in China

0

5

10

15

20

25

30

35

40

45

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

CO

2c

ap

ture

ca

pa

cit

y (

Mt/

y)

Projects in 'Operate' or 'Execute' Projects in 'Define'

Secrets of success

• 10 of the operating projects are related to natural gas processing

• Nearly all projects are commercial EOR projects

• Only 5 active projects use dedicated saline aquifer storage of

CO2 (Sleipner, Snøhvit, Quest, Illinois Industrial, Gorgon)

• 4 of these are led by oil and gas (O&G) companies

• The two successful coal power projects (and recently halted

Kemper) involve EOR and low-cost fuel supply

• Challenging for fossil power sector to invest in current climate

(low load factors)

What are the barriers to

broader applications of

CCS?

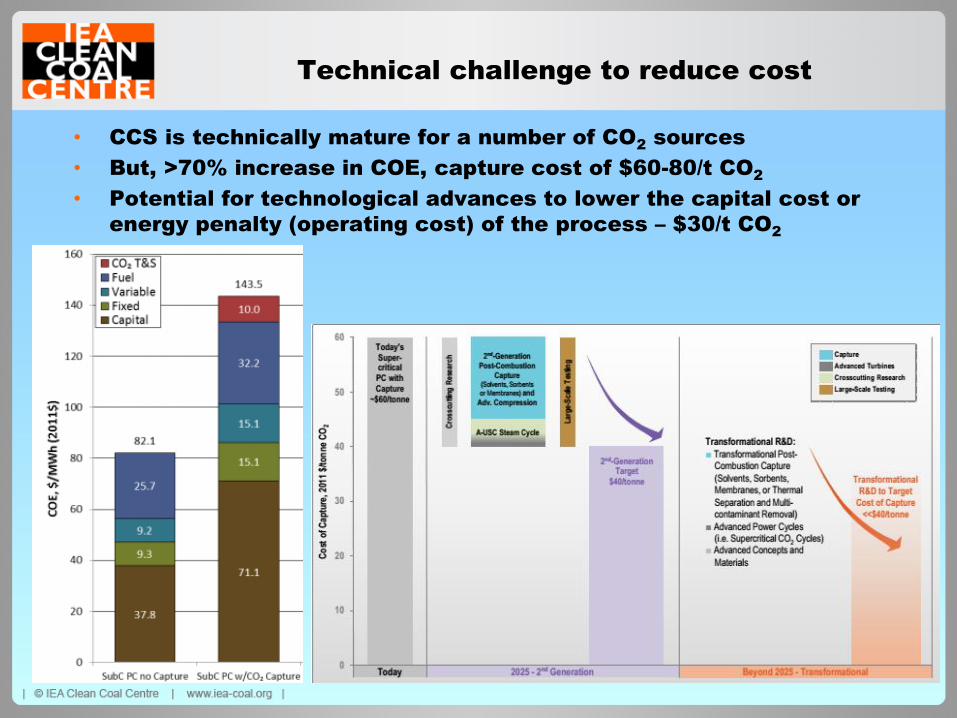

Technical challenge to reduce cost

• CCS is technically mature for a number of CO2 sources

• But, >70% increase in COE, capture cost of $60-80/t CO2

• Potential for technological advances to lower the capital cost or

energy penalty (operating cost) of the process – $30/t CO2

Economic barriers and potential drivers

Project financing

• High entry costs and lead times relative to other low-carbon

technologies: large plant (not modular), storage appraisal, need for

substantial transport and storage infrastructure

• High cost of finance for first-of-a-kind projects

• Most demonstrations have relied on state grants or loan guarantees

• Export credit agencies can play a role (e.g. Petra Nova)

Regulatory drivers

• Power purchase agreements, e.g. feed-in tariffs (UK)

• Tax credits for stored CO2 (USA)

• CO2 markets (EU ETS, Quebec, California, Chinese pilot schemes)

• CO2 emissions tax (Norway)

• CO2 cap (Canada, UK – usually promotes gas-fired generation)

Carbon price insufficient for early demonstrations – need targeted

incentives (like renewables) to overcome ‘valley of death’

Many successful CCS projects have also been driven by long-term

company strategy to preserve fossil fuel markets

Regulatory and risk

CCS implementation requires regulations governing issues such as:

• Site selection, monitoring, and closure

• Long-term liability of stored CO2 (usually transfers to government)

These are largely in place in USA, Canada, Australia, EU.

Less-developed legislation in Asia may be a barrier to investment.

Problematic risks for CCS industry

• ‘Cross-chain’ risk – when the emitter defaults on obligation to

storage company or vice versa

• Leakage risk – potentially unquantifiable and uninsurable risk of

CO2 leak, e.g., future cost of EU ETS credits

• Policy uncertainty – will financial support remain?

Reasons for market failures

• Infrastructure: Challenging to promote shared transport and storage

infrastructure without certain emission sources and vice versa

• Multi-sector nature: ‘Full-chain’ projects often need complex

partnerships between O&G industry and power industry – different

expertise

• Oil and gas industry companies are uniquely able to manage some

‘full-chain’ projects alone (Shell, BP, Statoil, Chevron)

• However, even this sector is reluctant to engage in a high-risk

enterprise when returns are small

• Characterisation of new storage sites is time-consuming, expensive,

and needs to take place before any final investment decision or

revenue stream

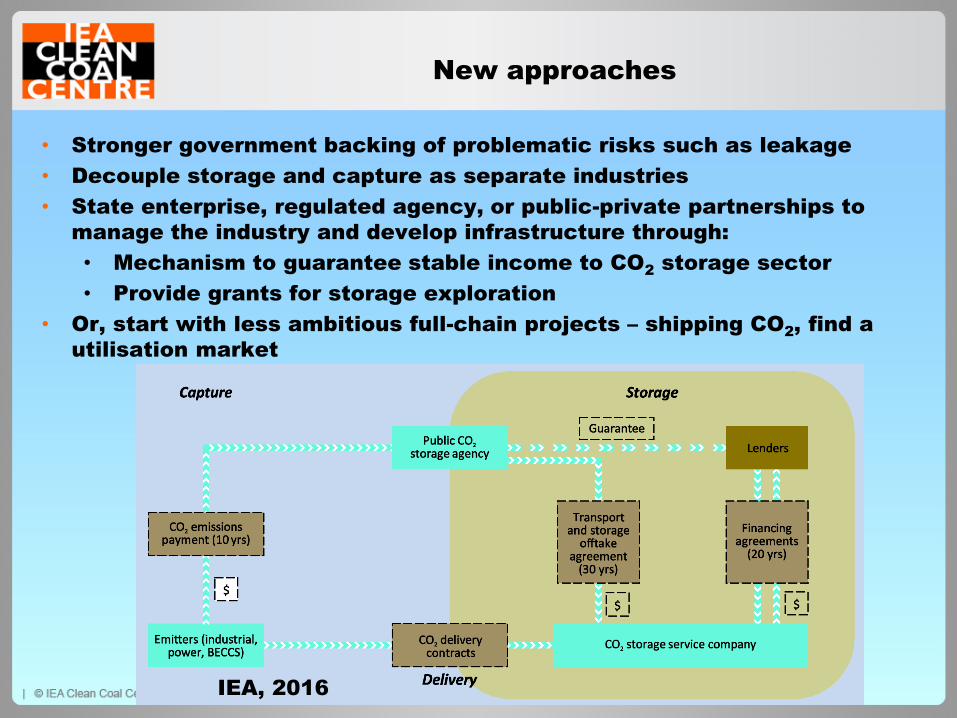

New approaches

• Stronger government backing of problematic risks such as leakage

• Decouple storage and capture as separate industries

• State enterprise, regulated agency, or public-private partnerships to

manage the industry and develop infrastructure through:

• Mechanism to guarantee stable income to CO2 storage sector

• Provide grants for storage exploration

• Or, start with less ambitious full-chain projects – shipping CO2, find a

utilisation market

IEA, 2016

Public acceptance

• Strong public opposition was encountered 2009-2011 in the

Netherlands and Germany

• Improved public engagement strategies (and perhaps lack of

onshore demos in Europe) have avoided significant further

opposition

• However, CCS is a relatively unpopular climate change solution –

political action and investment may require stronger public backing

COP20 in Lima

International collaboration

Collaboration can be multilateral or bilateral, involving

governments, academia, or private sector

May involve shared funds, resources, knowledge, or in-kind support

Motivation

• Joint research and knowledge sharing

• Mobilise political resources

• Promote CCS-favourable policy and regulations in new regions

• Promote dissemination and uptake of CCS R&D

• Capacity building

• Enable manufacturers to invest in new regions

• Build mutual trust (nations not acting alone on CCS)

• Improve the global image of CCS

Barriers to international collaboration

• Intellectual property rights

• Conflicting motivations and goals

• Administrative and organisational differences across borders

Forms of international collaboration

• International organisations

• Membership of national governments (and other sponsors)

• Often focus on capacity building in countries with little experience

of CCS

• Advocate favourable regulations and policy

• Suggest R&D directions for global research community

• Improving awareness and understanding of CCS

Many of the new approaches and policies described for CCS have been

developed by international organisations

• Bilateral agreements

• Project-specific collaboration

• Research networks

Carbon Sequestration Leadership Forum

26 country ministerial-level initiative for encouraging CCS

development by identifying and managing multilateral research

collaborations. Current goals:

• Enhanced communications for CCS

• Global collaboration on large-scale CCS projects

• Enabling financing for CCS projects

• Development of 2nd and 3rd gen. CCS technology

• Global collaboration to assess geological storage resources

Key achievements:

• Financing framework for CCS in developing

world

• Report to 2008 G8 summit led to CCS

deployment targets

• Technology roadmap

• Promoting knowledge exchange between

key projects

• Capacity building fund and academic

community task force

Global CCS Institute

• Set up in 2009 by Australian Government

• Now a private organisation with diverse membership

(national/regional governments, industry, research institutes, NGO)

• Provides advice and knowledge sharing to improve acceptance of

CCS, increase commercial opportunities, grow political support

• Annual Global Status of CCS and online databases track deployment

of new pilot and demonstration projects

• Communication, education, and capacity building initiatives, e.g.

provides ‘CO2degrees’ educational material

• Prepares reports (project case studies etc.) and runs numerous

workshops and meetings

International Energy Agency

• A leading provider of information on all energy issues and policy

advocate – aims to satisfy the ‘energy trilemma’

• Funded by 29 OECD member countries

• Leading advocate of CCS – maintains that it should account for

~12% of the total emissions reduction required in its ‘2 degree

scenario’ to 2050

• Key reports: 2009 CCS roadmap based on G8 target of 20

demonstrations (updated 2013), ‘20 years of CCS’ (2016), 2014

regulatory review

• Runs a number of workshops and meetings on CCS

IEA Energy Technology Networks

IEA Greenhouse Gas R&D Programme

• Established 1991, a collaborative research programme with a

focus on CCS technologies

• Produces technical studies and other reports

• Runs the major biennial GHGT conference, as well as smaller

conferences and network meetings on specific areas of research

• Sponsored research at the Weyburn-Midale demonstration project

• Runs a CCS summer school for young researchers

IEA Clean Coal Centre

• Established 1975, looks at all technologies enabling cleaner use of

coal, including CCS (as applied to coal power plant and coal-using

industries)

• Produces technical reviews and market reports

• Runs the biennial CCT conference (CCS and other coal

technologies), and a series of workshops on specific research

areas

Zero Emissions Platform (ZEP)

Since 2005, a EU-based stakeholder group representing energy

industry, research institutes and NGOs. Goals are to:

• Enable CCS as a key technology for combating climate change

• Make CCS technology commercially viable by 2020 via an EU-

backed demonstration programme

• Accelerate R&D into next-generation CCS technology and its

wide deployment post-2020

ZEP has driven EU policy on CCS, through reports and political

engagement.

Key achievements:

• Contributed to EU’s Strategic Energy Plan (SET)

• Contributed to EU CCS Directive

• Proposed 12 demo target adopted by the EU

• Recommended European Energy Programme for Recovery and

NER300 funding schemes

Mission Innovation

• Launched at COP21, 23 participating states pledged to double

their funding to clean energy R&D to 2020

• Carbon capture is one of seven ‘Innovation Challenges’ (leads:

USA and Saudi Arabia)

• Focus on developing new, low TRL, ‘transformational’

technologies (complement CSLF focus on demonstration)

• Workshop for 200-300 CCS experts in Houston, 25-29 Sep 2017

• Will look at capture, storage, utilisation, and cross-cutting themes

• A workshop report will identify establish current state-of-the-art,

identify key research priorities and gaps, opportunities for

collaboration, and help direct R&D funding

Bilateral initiatives

• Based on memorandum of understanding (MoU) between

governments

• Many examples feature an OECD country active in CCS research and

China:

• Could allow highly developed research programmes and

technology providers access to China’s cheaper manufacturing

and larger CCS market

• Help build CCS capacity in China

• Increased access to real project experience for researchers on

both sides

• Bilateral collaboration also exists between OECD countries wishing

to pool research resources and knowledge, e.g. US-Norway

collaboration on CCUS:

• Generally involve knowledge sharing or collaborative research

projects rather than funded demonstration projects

USA-China Clean Energy Research Centre

Advanced Coal Technology Consortium

Established in 2009 as a collaboration between large US and Chinese

consortia of academic and industry players (19 US, 16 Chinese)

Phase I: 2011 - 2015, Phase II: 2016 -

• Established ‘Technology Management Platform’ for protecting IP

• Collaboration between Huaneng and Duke Energy on IGCC demo and

post-combustion pilots

• Collaboration between Yanchang Oil and US universities evaluating

the Ordos basin and EOR pilot – leading to Yanchang demo

• Gemeng International and LP Amina collaboration to build 50 MW

demo coal-to-chemicals facility in Shanxi

• Raised political awareness of CCS, helped collaboration within China

Issues (from WRI analysis, 2016):

• Many research papers resulted, but few patents or products

• Mismatched goals – e.g. US companies seeking to enter Chinese

market, Chinese companies seeking engineering data

• Some US companies withdrew

• Needs to be more industry driven to realise large projects

UK-China (Guangdong) CCUS centre

2013 MoU between UKCCSRC, Scottish CCS, Guangdong Low-

carbon Technology and Industry Research Centre and the Clean

Fossil Energy Development Institute. Aims to:

• Promote joint research and development

• Provide advice for local and regional governments

• Move rapidly towards demonstration of CCUS in China

Most work on CRP’s Haifeng coal

plant in Guangdong

• GEPDI and U Edinburgh

completed CCS ready design for

two new units at Haifeng

• Planning joint test centre at

Haifeng for new solvent and

membrane technologies and

operator training

• Conducted public outreach in the

province

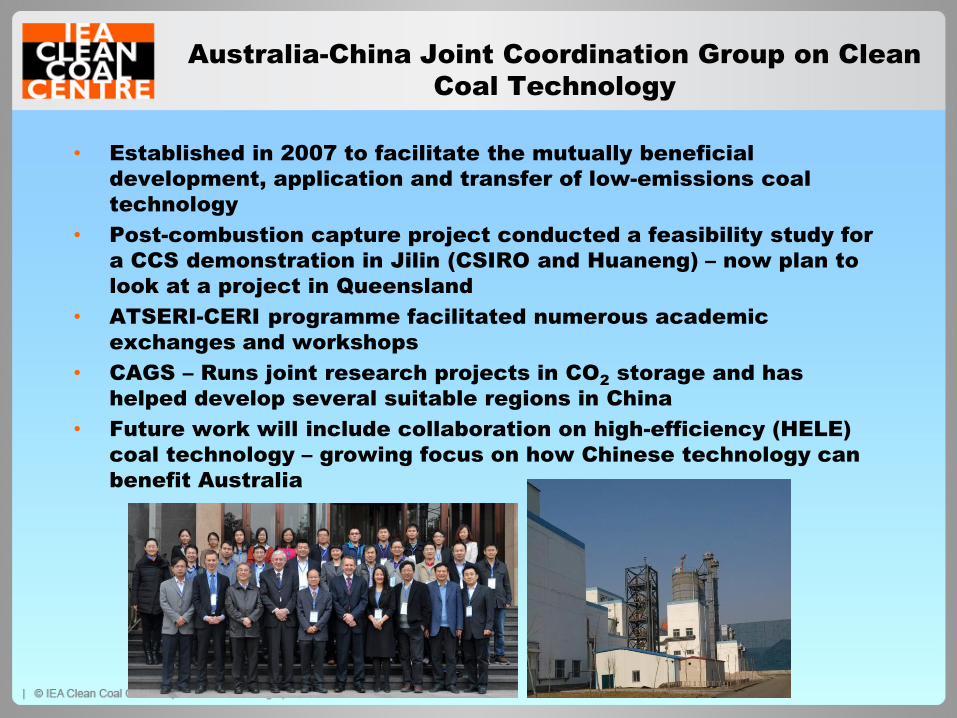

Australia-China Joint Coordination Group on Clean

Coal Technology

• Established in 2007 to facilitate the mutually beneficial

development, application and transfer of low-emissions coal

technology

• Post-combustion capture project conducted a feasibility study for

a CCS demonstration in Jilin (CSIRO and Huaneng) – now plan to

look at a project in Queensland

• ATSERI-CERI programme facilitated numerous academic

exchanges and workshops

• CAGS – Runs joint research projects in CO2 storage and has

helped develop several suitable regions in China

• Future work will include collaboration on high-efficiency (HELE)

coal technology – growing focus on how Chinese technology can

benefit Australia

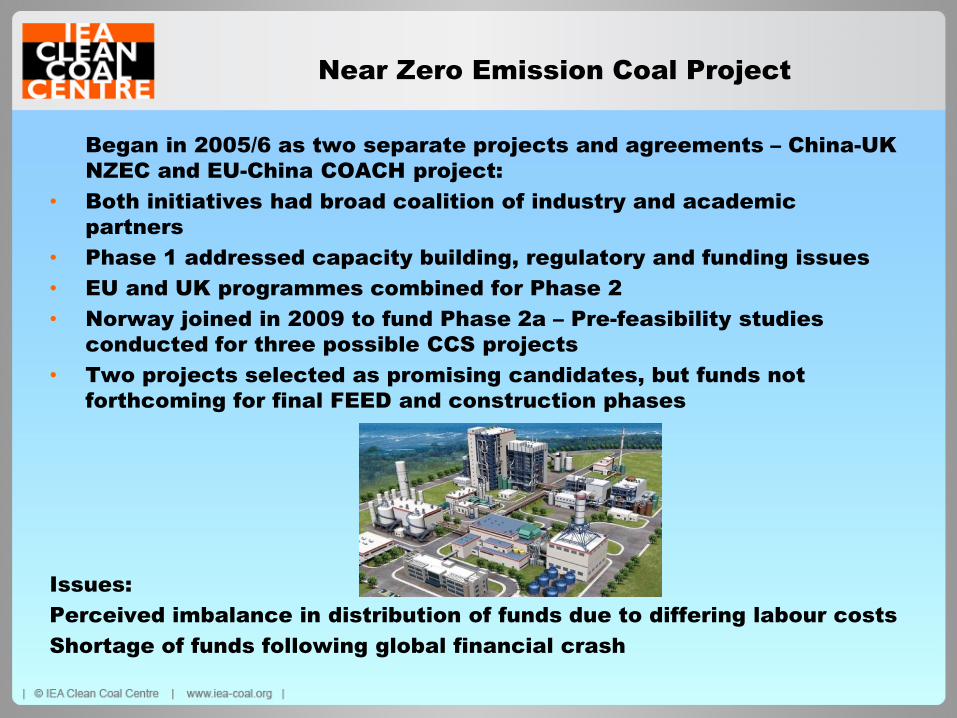

Near Zero Emission Coal Project

Began in 2005/6 as two separate projects and agreements – China-UK

NZEC and EU-China COACH project:

• Both initiatives had broad coalition of industry and academic

partners

• Phase 1 addressed capacity building, regulatory and funding issues

• EU and UK programmes combined for Phase 2

• Norway joined in 2009 to fund Phase 2a – Pre-feasibility studies

conducted for three possible CCS projects

• Two projects selected as promising candidates, but funds not

forthcoming for final FEED and construction phases

Issues:

Perceived imbalance in distribution of funds due to differing labour costs

Shortage of funds following global financial crash

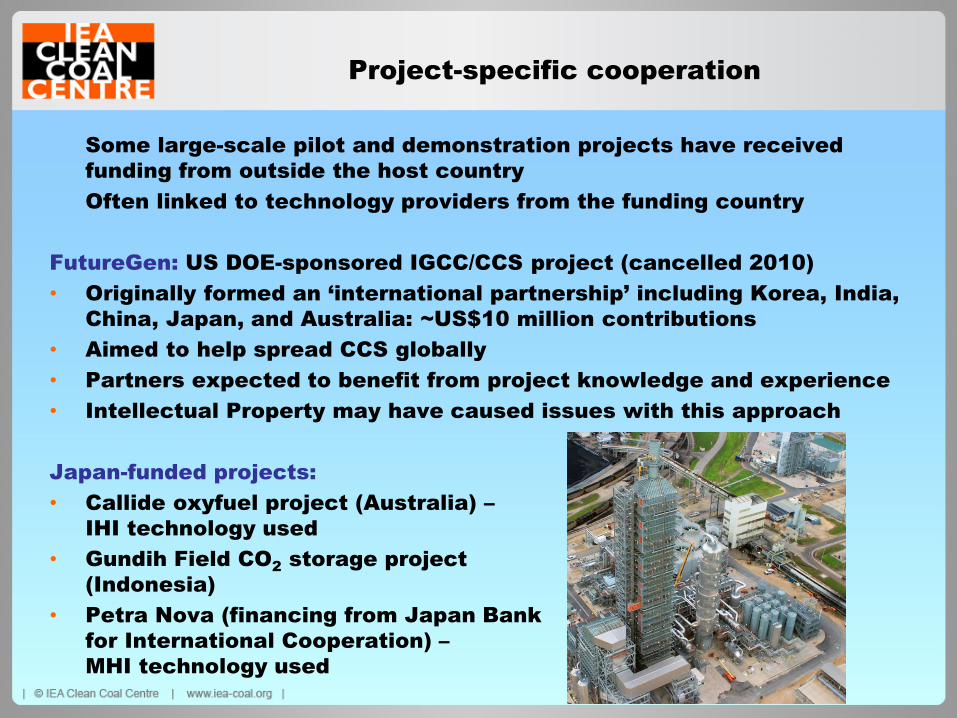

Project-specific cooperation

Some large-scale pilot and demonstration projects have received

funding from outside the host country

Often linked to technology providers from the funding country

FutureGen: US DOE-sponsored IGCC/CCS project (cancelled 2010)

• Originally formed an ‘international partnership’ including Korea, India,

China, Japan, and Australia: ~US$10 million contributions

• Aimed to help spread CCS globally

• Partners expected to benefit from project knowledge and experience

• Intellectual Property may have caused issues with this approach

Japan-funded projects:

• Callide oxyfuel project (Australia) –

IHI technology used

• Gundih Field CO2 storage project

(Indonesia)

• Petra Nova (financing from Japan Bank

for International Cooperation) –

MHI technology used

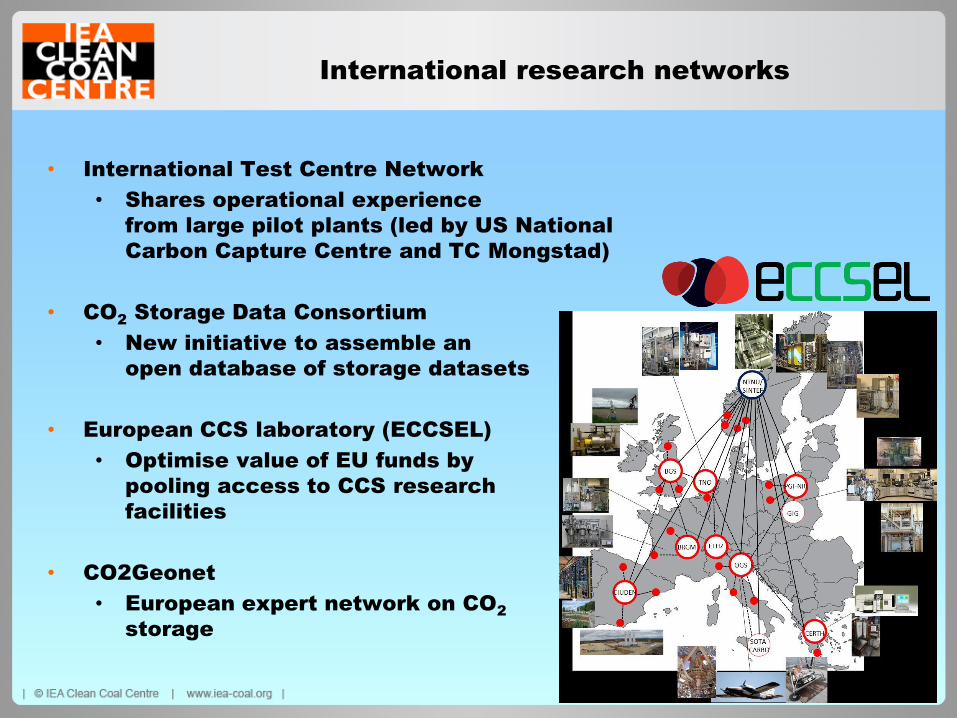

International research networks

• International Test Centre Network

• Shares operational experience

from large pilot plants (led by US National

Carbon Capture Centre and TC Mongstad)

• CO2 Storage Data Consortium

• New initiative to assemble an

open database of storage datasets

• European CCS laboratory (ECCSEL)

• Optimise value of EU funds by

pooling access to CCS research

facilities

• CO2Geonet

• European expert network on CO2

storage

Closing remarks

• CCS faces some unique and challenging barriers to wider

deployment

• Transformational technology can play a role in reducing costs.

However, CCS will still require favourable policy, appropriate

regulations and better structuring of risk

• Strong incentive for countries to act together to avoid a competitive

disadvantage and pool limited resources

• CCS is also a highly cross-discipline technology – collaboration

between different industry sectors is critical

• International organisations have played a crucial role in

championing CCS and driving CCS policy around the world

• Many initiatives are research focussed – need still greater

coordination on more significant challenge of gaining sufficient

public and political support to harness adequate funding

Closing remarks II

• Research and major tech. providers are centred in regions with

declining fossil fuel use and high deployment costs, so need to

work more closely with Asia and coal-dependent, developing

countries

• Bilateral projects with China have largely been insufficiently

funded to result in CCS demonstrations, but may have paved the

way – raised awareness of CCS and established project expertise

• However, difficult to expect action from China alone, when

deployment is slowing in the OECD

• Is the time right for an internationally funded demonstration in the

developing world?