A Reality Check for Canadian Industry and Government

DECEMBER 2012

CANADA’S MANUFACTURING LABOUR MARKET:

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 1 |

Leadership makes the difference

Manufacturing is one of Canada’s most important economic sectors by almost all statistical measurements, including being a leader in GDP, imports, exports, research and development, and employment.

As!a!result, manufacturing plays a critical role in the economic success of each province, as well as the country as a whole.

Today, manufacturers directly employ more than one in every 10 working Canadians and pay over $1.84 billion every week in salaries. While the business outlook for Canadian industry is positive for the next three to "ve years, com-panies are facing a variety of challenges, both domestically and internationally. The most pressing challenge for companies is growing business by "nding new customers in new markets, they have a number of major concerns about their future success. Companies’ ability to meet these challenges lies with a number of critical factors, especially with their ability to attract and retain the necessary labour with the right skills to support their innovation, productivity and growth. However, a key concern businesses are met with is growing labour problems, which are only expected to worsen over the next "ve years.

According to the national Management Issues Survey conducted by Canadian Manufacturers & Exporters (CME) in spring 2012, nearly 50 per cent of companies state they face labour shortages today across a wide range of occupations, with most occupational areas appear set to worsen over the next "ve years. Occupations such as sales and marketing, skilled production, general manage-ment and engineering are deemed to be the most critical for companies’ suc-cess over the next "ve years. However, those areas also are the ones in which companies are most concerned about labour shortages. These shortages have a signi"cant impact on manufacturing operations in Canada, including constraining growth, restricting investment and forgoing production.

Canadian companies require more labour with stronger skill sets across occupational classi"cations from both domestic and international sources if they are to "ll the current and expected labour shortages. While Canadian companies, governments, employers and the education system have taken several steps to address these challenges, everyone must work more aggressively if Canada is to prosper, innovate, and take advantage of the economic opportunities over the next decade.

Introduction and Summary

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 2 |

Leadership makes the difference

In the spring of 2012, CME, along with partner organizations in the Canadian Manufacturing Coalition, surveyed Canada’s business community to better understand current business conditions and the outlook companies forecast

for their businesses over the next three to "ve years. While asking about these conditions, the survey provided an opportunity to examine what the priorities were for business in terms of investment policies and government programs aimed at growing the economy coast-to-coast.

In total, 649 individual responses formed the results of the Management Issues Survey (MIS). The data collected is one of the largest recent surveys of manufac-turers in Canada and the only one available that provides a clear picture of the current state of the sector.

The companies responding to the survey represent a broad cross-section of the manufacturing sector and related service providers with all sizes of companies, in all regions of Canada. Clear from the results is Canadian companies’ common view of challenges and solutions. Whether headquartered in Canada or abroad, whether a small company or a global multinational, whether annual sales ex-ceeded $1 million or $500 million, companies have a united vision on issues and potential options for addressing them.

Companies are continuing to deal with a myriad of pressures impacting their operations and business decisions. Their primary concerns and most pressing challenges are issues they have little in#uence over, such as the strength of local and international markets, the continued strength of the Canadian dollar, and the cost and stable supply of raw materials to make their products.

They are also dealing with pressures which they have a more direct in#uence over, such as labour shortages, regulatory burdens, product and process innova-tions, supply chain management and infrastructure.

Despite these pressures, companies are very optimistic and are anticipating growth in most aspects of their business, including production volumes, sales, exports, and pro"tability. These expectations are directly tied to their con"dence in increasing investment in research and development, in new processes and more productive machinery and equipment, and in their people over the next three years. These investments are centered on one priority: satisfying existing customers and developing new clients at home and abroad.

This customer base is continuing to shift, along with the supply base for Canadian companies. Showing the deep integration of Canada-US manufactur-ing, respondents indicated their market for purchasing and sales is heavily focused on their home province and into the United States. However, this will begin to shift in the coming years as the US market is expected to remain weak. Companies are increasingly looking to "nd new customers in offshore markets like!Europe, China, and Brazil.

Summary of CME’s 2012–2013 Management Issues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 3 |

Leadership makes the difference

Companies responding to the survey noted a primary factor for investment was proximity to customers and strength of the local market. The challenge for Canada, then, is: with shifting customer bases, how do we secure the production at home to satisfy these sales abroad?

Given Canada’s market size and the mobility of capital, Canada must be the ab-solute best in the world at attracting investment. Canada can, and must, do better if it is going to take advantage of the optimism expressed by Canadian industry in the survey. While a number of priorities for action emerged and will need to be addressed, the top priorities for action by both government and industry have been identi"ed as the following:

1. Strengthen investment policies through supportive programs and taxation aimed at productivity and attracting investments in machinery and equipment, innovation, and R&D.

2. Strengthen the labour market by introducing training tax credits and improving the education system to be more in line with industry needs domestically while reforming the immigration system to "ll the needs of industry that cannot be met at home.

3. Strengthen economic integration with the United States by fully implementing the Perimeter Security and Economic Competitiveness Action Plan and ag-gressively pursue a reciprocal government procurement agreement.

4. Support market diversi"cation by focusing on trade agreements that work to eliminate structural and regulatory barriers to trade into priority markets as well as providing better support mechanisms for companies looking to develop new markets.

5. Reduce the regulatory burden to support investment by streamlining and speeding approval processes, reducing compliance costs, and eliminating duplication between jurisdictions, especially the US.

While the detailed analysis and results of the MIS are available at www.cme-mec.ca, this study and analysis focuses on labour market issues identi"ed by respondents to the survey and the impact of labour and skills issues on manufacturing competitiveness and investment in Canada. In order to complete the analysis for this report, this study also examines the broader role that manufacturing plays in Canada’s labour market.

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 4 |

Leadership makes the difference

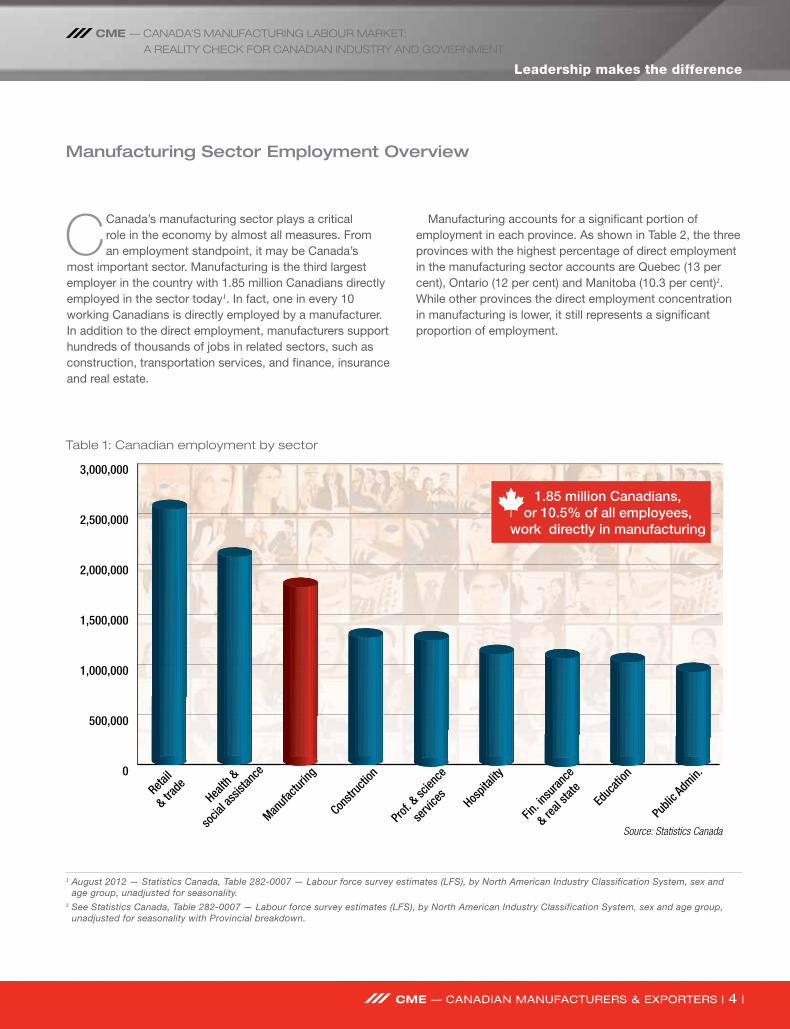

CCanada’s manufacturing sector plays a critical role in the economy by almost all measures. From an employment standpoint, it may be Canada’s

most important sector. Manufacturing is the third largest employer in the country with 1.85 million Canadians directly employed in the sector today1. In fact, one in every 10 working Canadians is directly employed by a manufacturer. In addition to the direct employment, manufacturers support hundreds of thousands of jobs in related sectors, such as construction, transportation services, and "nance, insurance and real estate.

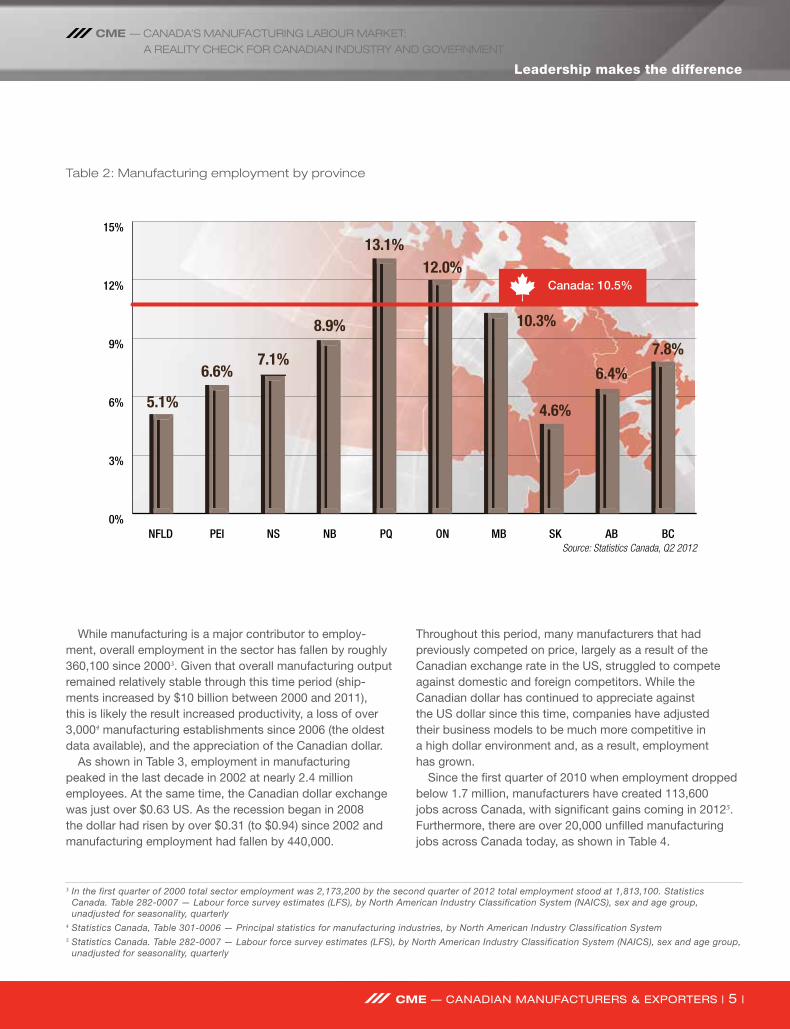

Manufacturing accounts for a signi"cant portion of employment in each province. As shown in Table 2, the three provinces with the highest percentage of direct employment in the manufacturing sector accounts are Quebec (13 per cent), Ontario (12 per cent) and Manitoba (10.3 per cent)2. While other provinces the direct employment concentration in manufacturing is lower, it still represents a signi"cant proportion of employment.

Manufacturing Sector Employment Overview

Table 1: Canadian employment by sector

1 August 2012 — Statistics Canada, Table 282-0007 — Labour force survey estimates (LFS), by North American Industry Classification System, sex and age group, unadjusted for seasonality.

2 See Statistics Canada, Table 282-0007 — Labour force survey estimates (LFS), by North American Industry Classification System, sex and age group, unadjusted for seasonality with Provincial breakdown.

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 5 |

Leadership makes the difference

While manufacturing is a major contributor to employ-ment, overall employment in the sector has fallen by roughly 360,100 since 20003. Given that overall manufacturing output remained relatively stable through this time period (ship-ments increased by $10 billion between 2000 and 2011), this is likely the result increased productivity, a loss of over 3,0004 manufacturing establishments since 2006 (the oldest data available), and the appreciation of the Canadian dollar.

As shown in Table 3, employment in manufacturing peaked in the last decade in 2002 at nearly 2.4 million employees. At the same time, the Canadian dollar exchange was just over $0.63 US. As the recession began in 2008 the dollar had risen by over $0.31 (to $0.94) since 2002 and manufacturing employment had fallen by 440,000.

Throughout this period, many manufacturers that had previously competed on price, largely as a result of the Canadian exchange rate in the US, struggled to compete against domestic and foreign competitors. While the Canadian dollar has continued to appreciate against the US!dollar since this time, companies have adjusted their!business models to be much more competitive in a!high!dollar environment and, as a result, employment has!grown.

Since the "rst quarter of 2010 when employment dropped below 1.7 million, manufacturers have created 113,600 jobs across Canada, with signi"cant gains coming in 20125. Furthermore, there are over 20,000 un"lled manufacturing jobs across Canada today, as shown in Table 4.

Table 2: Manufacturing employment by province

3 In the first quarter of 2000 total sector employment was 2,173,200 by the second quarter of 2012 total employment stood at 1,813,100. Statistics Canada. Table 282-0007 — Labour force survey estimates (LFS), by North American Industry Classification System (NAICS), sex and age group, unadjusted for seasonality, quarterly

4 Statistics Canada, Table 301-0006 — Principal statistics for manufacturing industries, by North American Industry Classification System5 Statistics Canada. Table 282-0007 — Labour force survey estimates (LFS), by North American Industry Classification System (NAICS), sex and age group,

unadjusted for seasonality, quarterly

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 6 |

Leadership makes the difference

2,400,000

2,200,000

2,000,000

1,800,000

1,600,000

1,400,000

$ 1.10

$ 1.00

$ 0.90

$ 0.80

$ 0.70

$ 0.60

$ 0.50

Q1 2

000

Q3 2

000

Q1 2

001

Q3 2

001

Q1 2

002

Q3 2

002

Q1 2

003

Q3 2

003

Q1 2

004

Q3 2

004

Q1 2

005

Q3 2

005

Q1 2

006

Q3 2

006

Q1 2

007

Q3 2

007

Q1 2

008

Q3 2

008

Q1 2

009

Q3 2

009

Q1 2

010

Q3 2

010

Q1 2

011

Q3 2

011

Q1 2

012

Q3 2

012

Man

ufac

turin

g Em

ploy

men

t

jobs

dollar

Cana

dian

$ E

xcha

nge

Source: Statistics Canada

Table 3: Canadian manufacturing employment vs. exchange rate

Table 4: Canadian job vacancies by sector

Manufacturing is not only among the largest employ-ers in Canada, but the wages in manufacturing are also amongst the highest in any sector. In August 2012, the mining, oil and gas sector paid the highest average weekly salary with an average of $1,886. The utilities sector paid

the second!highest at $1,595 per week, and professional and!scienti"c services paid an average of $1,256 a week ranking third overall. Manufacturing employees are the tenth highest earners in Canada, earning more than $996 per week on average.

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 7 |

Leadership makes the difference

$500.00

$700.00

$900.00

$1,100.00

$1,300.00

$1,500.00

$1,700.00

$1,900.00

Fores

try &

loggin

g

Trans

port &

wareho

using

Manufa

cturin

g

Educ

ation

Finan

ce &

insura

nce

Constr

uctio

nPu

blic

admini

strati

on

Info &

cultu

ral

compa

nies

Manag

emen

t

of co

mpanie

s

Prof. &

scien

ti!c

servi

ces

Utilitie

s

Mining

, qua

rrying

,

oil & ga

s

Manufacturing employeesearn $996 per week

Source: Statistics Canada; August 2012

Table 5: Average weekly salary by sector

Given the number of people employed in the sector, and!the average weekly salary paid to those workers, manufacturing has the highest weekly payroll across all sectors in Canada paying on average over $1.84 billion in

salaries6. The retail sector has the second highest payroll average with $1.83 billion in salaries and the health and social assistance sector ranks third with over $1.75 billion in weekly average!salaries.

6 Based on August 2012 data from Statistics Canada of 1.85 million manufacturing employees earning an average weekly salary of $996.18

Table 6: Canadian average weekly payroll by sector

$000

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

$1,600,000,000

$1,800,000,000

$2,000,000,000

Mining

, qua

rrying

,

oil & ga

s

Fores

try, lo

gging

Utilitie

s

Hospit

ality

Other s

ervice

s

Trans

port &

wareho

using

Info &

cultu

ral

indus

tries

Educ

ation

Publi

c adm

inistr

ation

Finan

ce & in

suran

ce

Constr

uctio

n

Prof. &

scien

ti!c

servi

ces

Health

and

socia

l assi

stanc

e

Retail &

trade

Manufa

cturin

g

Canadian manufacturerspay $1.84 billion weekly

in salaries

Source: CME based on Statistics Canada data

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 8 |

Leadership makes the difference

CME’s Management Issues Survey examined a variety!of factors relating to competitiveness, investment climate, government programs and

policies, and the views of Canada’s manufacturing sector on these issues. When examining the results relating to the challenges companies face today along with the most important factors impacting investment decisions, it is clear labour market issues are among the most critical facing Canadian industry.

The most pressing challenges Canadian companies identi-"ed are competition in their primary markets and maintaining and growing their market share, with 56 per cent of respond-ents noting this was a top issue, as shown in Table 7. The continued strength of the Canadian dollar remains a concern for Canadian companies, with 47 per cent naming this issue a top priority, ranking as the second most pressing concern. Attracting and retaining labour ranked as the third largest challenge with 46 per cent of respondents stating it was a top concern.

Labour Market Realities for Manufacturers: Results from the Management Issues Survey

0 10 20 30 40 50 60Interprovincial trade barriers

Other

Attracting investment and/or new product mandates

Access to global suppliers under competitive conditions (price, import duties)

Expanding production capacity outside Canada

Tariffs and duties on goods and services exports

Cost and reliability of energy supply

Expanding production capacity inside Canada

Regulatory barriers to entering foreign markets

Accessing credit and/or cost of business !nancing

Regulations causing delays in investment,expansion and/or product approvals domestically

Compliance costs in dealing with regulations and environment

Bringing new or improved products or services to market

Supply chain management and logistics

Cost and/or availability of raw materials

Developing new markets

Global economic conditions

Attracting or retaining labour

Strength of the Canadian dollar

Increased competition in primary markets (maintain market share)

(per cent)Source: CME Management Issues Survey — respondents could choose !ve answers

47% 56%

46%41%

36%28%

24%23%

22%16%

15%

13%13%

13%12%

9%8%7%7%

5%

Table 7: Most pressing challenges companies face

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 9 |

Leadership makes the difference

While many of these issues are outside the control of companies (such as the strength of the Canadian dollar), many of the issues and concerns selected are either within the control of the respondents themselves (supply chain management), within the control of government ( regulatory barriers), or within the in#uence and responsibility of both the companies and the government (attracting and retaining!labour).

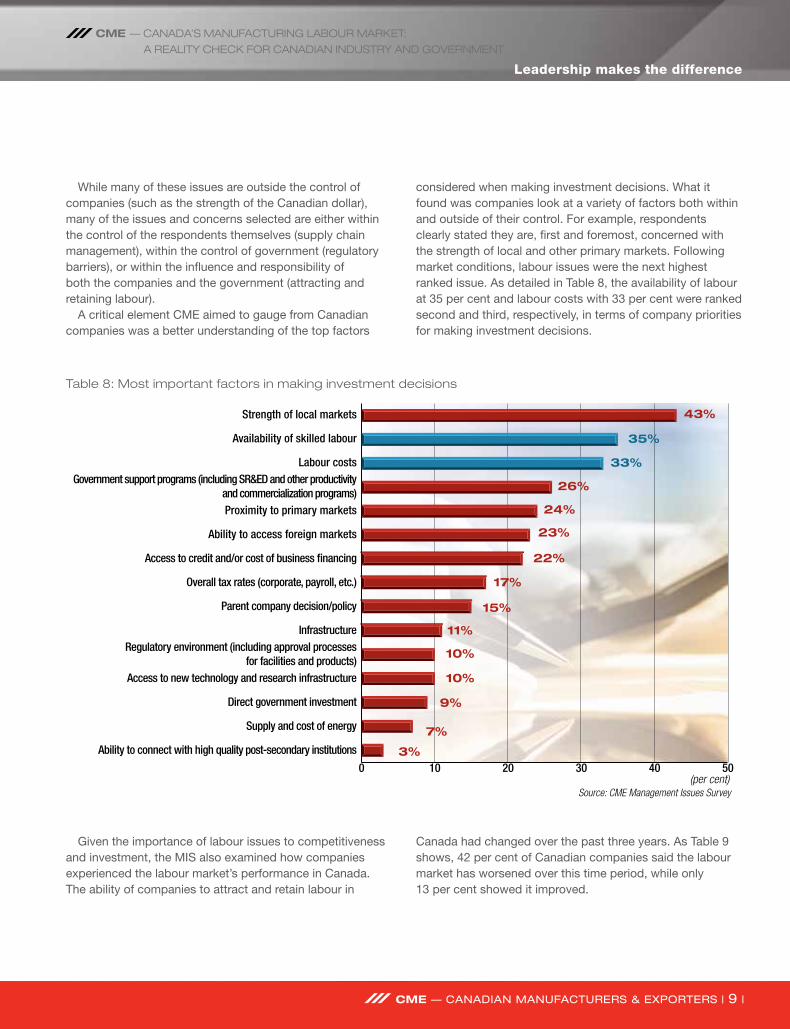

A critical element CME aimed to gauge from Canadian companies was a better understanding of the top factors

considered when making investment decisions. What it found was companies look at a variety of factors both within and outside of their control. For example, respondents clearly stated they are, "rst and foremost, concerned with the strength of local and other primary markets. Following market conditions, labour issues were the next highest ranked issue. As detailed in Table 8, the availability of labour at 35 per cent and labour costs with 33 per cent were ranked second and third, respectively, in terms of company priorities for making investment decisions.

0 10 20 30 40 50Ability to connect with high quality post-secondary institutions

Supply and cost of energy

Direct government investment

Access to new technology and research infrastructure

Regulatory environment (including approval processesfor facilities and products)

Infrastructure

Parent company decision/policy

Overall tax rates (corporate, payroll, etc.)

Access to credit and/or cost of business !nancing

Ability to access foreign markets

Proximity to primary markets

Government support programs (including SR&ED and other productivityand commercialization programs)

Labour costs

Availability of skilled labour

Strength of local markets

35%

43%

33%

26%

24%

23%

22%

17%

15%

11%

10%

10%

9%

7%

3%

(per cent)Source: CME Management Issues Survey

Table 8: Most important factors in making investment decisions

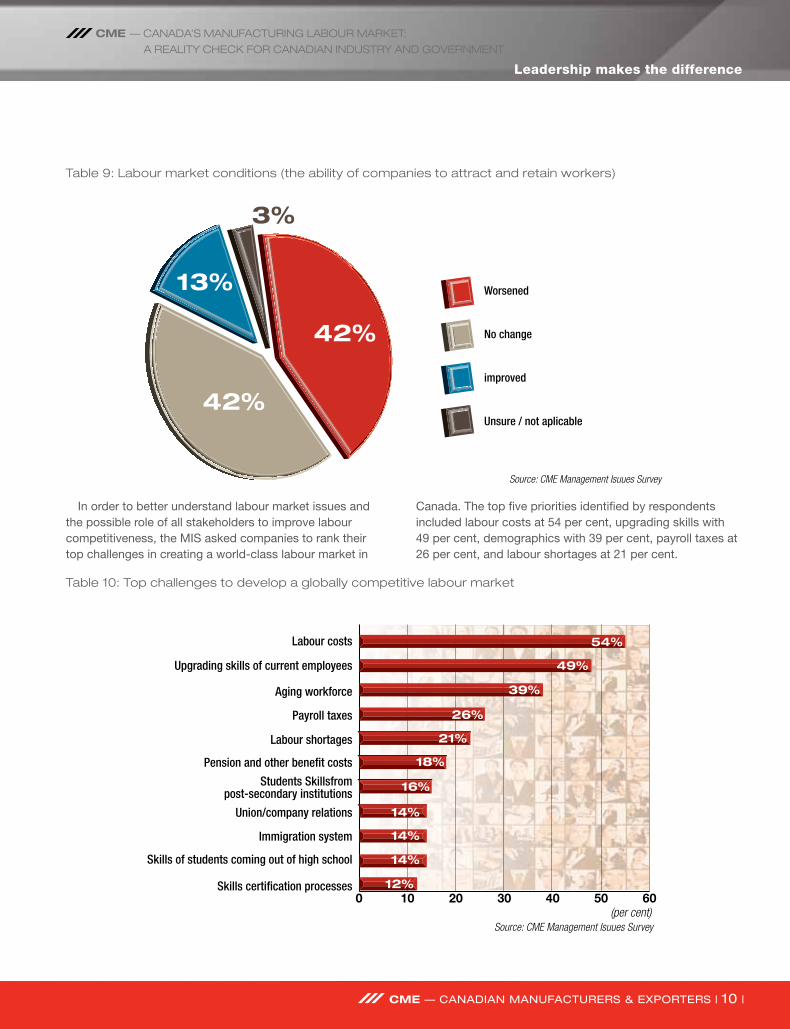

Given the importance of labour issues to competitiveness and investment, the MIS also examined how companies experienced the labour market’s performance in Canada. The ability of companies to attract and retain labour in

Canada had changed over the past three years. As Table 9 shows, 42 per cent of Canadian companies said the labour market has worsened over this time period, while only 13!per!cent showed it improved.

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 10 |

Leadership makes the difference

In order to better understand labour market issues and the possible role of all stakeholders to improve labour competitiveness, the MIS asked companies to rank their top challenges in creating a world-class labour market in

Canada. The top "ve priorities identi"ed by respondents included labour costs at 54 per cent, upgrading skills with 49!per cent, demographics with 39 per cent, payroll taxes at 26 per cent, and labour shortages at 21 per cent.

Unsure / not aplicable

improved

No change

Worsened

42%

42%

13%

3%

Source: CME Management Isuues Survey

Table 9: Labour market conditions (the ability of companies to attract and retain workers)

Table 10: Top challenges to develop a globally competitive labour market

0 10 20 30 40 50 60Skills certi!cation processes

Skills of students coming out of high school

Immigration system

Union/company relations

Students Skillsfrompost-secondary institutions

Pension and other bene!t costs

Labour shortages

Payroll taxes

Aging workforce

Upgrading skills of current employees

Labour costs

49%

54%

39%

26%

21%

18%

16%

14%

14%

14%

12%

(per cent)Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 11 |

Leadership makes the difference

A provincial breakdown of this question shows these primary concerns are shared across Canada. Respondents from the provinces of Alberta, British Columbia, Ontario, and Quebec all stated their primary concern was labour costs, and noted upgrading skills and the aging workforce were in the top three issues. New Brunswick, Nova Scotia, and P.E.I. all share a greater concern for the aging workforce and population. Manitoba’s primary concern is upgrading the skills of the current labour force, with the aging popula-tion coming in second. Respondents from Newfoundland selected the aging workforce and labour costs equally.

To better understand these priority issues, the survey asked for company responses on many of these identi"ed challenges in building a globally competitive workforce. The!results provided substantial information on several of the!key concerns raised by companies in creating a world-class competitive workforce, including skills shortages, employee training and skills development demographics, and labour mobility.

1. Skill requirements and shortages: The success of companies is directly tied to the skills and!abilities of their employees and a wide variety of skill sets are required to successfully run any

operation. While few would argue skilled production is central to the!growth of Canadian industry, many may be surprised!to learn that sales, marketing and customer service is the occupational segment in which respondents identi"ed the most important to the prosperity of their business. Respondents listed sales, marketing and customer service (29 per cent), skilled production (25!per cent), and management and administration (17!per cent) as the top three most important occupational segments for the growth of their businesses over the next "ve years.

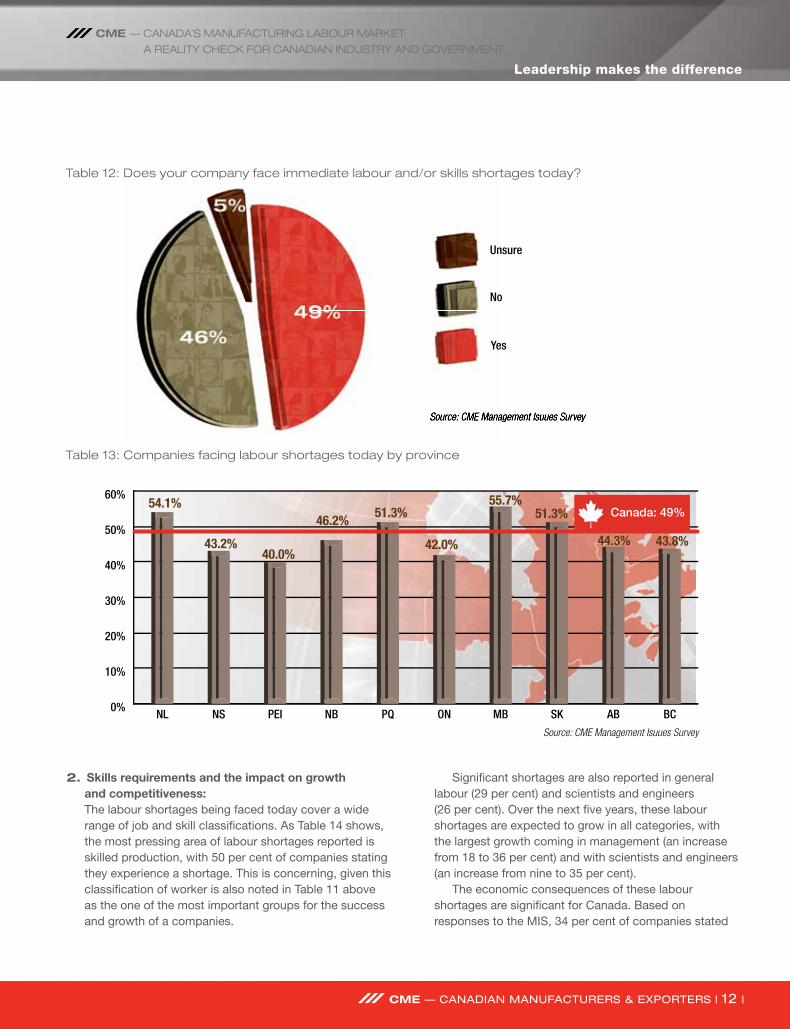

To better understand labour needs today in these occupations and the possible shortages of workers, companies were asked if they faced labour shortages. Nearly 50 per cent of companies surveyed indicated they faced a labour shortage today.

When examining shortages at the provincial level, Manitoba had the highest percentage of companies stating they experienced a labour shortage today at 55.7!per cent, followed by Newfoundland and Labrador at 54.1 per cent, and then Saskatchewan at 51.3 per cent. Alberta, the province most identi"ed as having labour shortages, ranked below the national average with!44.3 per cent.

Sales,marketing

andcustomer service

Skilled production(welders,

machinists,operators)

Scientists,engineers,

R&Dtechnicians

Managementand

administration

Generallabour

Productionsupport

(IT, maintenance)

5%

9%

16% 17%

25%29%

Table 11: Most important occupations for success and growth over the next !ve years

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 12 |

Leadership makes the difference

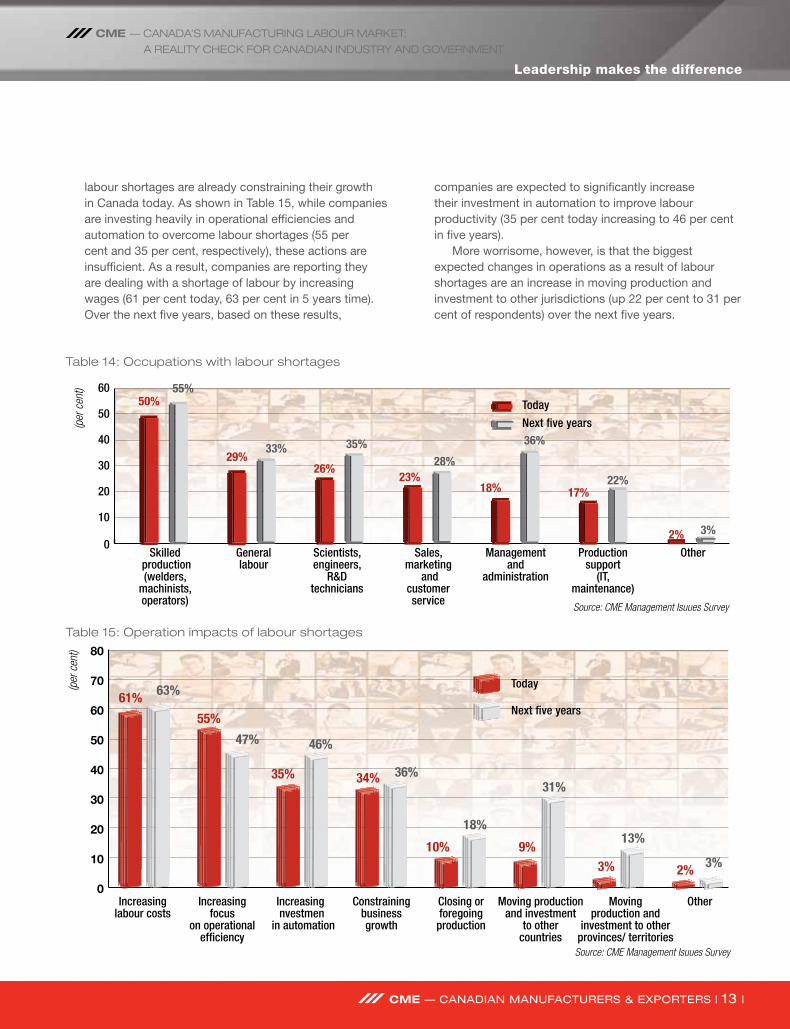

2. Skills requirements and the impact on growth and competitiveness: The labour shortages being faced today cover a wide range of job and skill classi"cations. As Table 14 shows, the most pressing area of labour shortages reported is skilled production, with 50 per cent of companies stating they experience a shortage. This is concerning, given this classi"cation of worker is also noted in Table 11 above as the one of the most important groups for the success and growth of a companies.

Signi"cant shortages are also reported in general labour (29 per cent) and scientists and engineers (26 per!cent). Over the next "ve years, these labour shortages are expected to grow in all categories, with the largest growth coming in management (an increase from 18 to 36 per cent) and with scientists and engineers (an!increase from nine to 35 per cent).

The economic consequences of these labour shortages are signi"cant for Canada. Based on responses to the MIS, 34 per cent of companies stated

Source: CME Management Isuues SurveySource: CME Management Isuues Survey

Unsure

No

Yes

Table 12: Does your company face immediate labour and/or skills shortages today?

Table 13: Companies facing labour shortages today by province

0%

10%

20%

30%

40%

50%

60%

BCABSKMBONPQNBPEINSNL

Canada: 49%

43.2%

54.1%

40.0%

46.2% 51.3%

42.0%

55.7%51.3%

44.3% 43.8%

Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 13 |

Leadership makes the difference

labour shortages are already constraining their growth in!Canada today. As shown in Table 15, while companies are investing heavily in operational ef"ciencies and automation to overcome labour shortages (55 per cent and 35 per cent, respectively), these actions are insuf"cient. As a result, companies are reporting they are dealing with a shortage of labour by increasing wages (61!per cent today, 63 per cent in 5 years time). Over!the!next "ve years, based on these results,

companies are expected to signi"cantly increase their!investment in automation to improve labour productivity (35 per cent today increasing to 46 per cent in "ve years).

More worrisome, however, is that the biggest expected changes in operations as a result of labour shortages are an increase in moving production and investment to other jurisdictions (up 22 per cent to 31 per cent of respondents) over the next "ve years.

0

10

20

30

40

50

60

Next !ve yearsToday

OtherProductionsupport

(IT,maintenance)

Managementand

administration

Sales,marketing

andcustomerservice

Scientists,engineers,

R&Dtechnicians

Generallabour

Skilled production(welders,

machinists,operators)

29%

50%

26%23%

18% 17%

2%

55%

33% 35%28%

36%

22%

3%

(per

cen

t)

Source: CME Management Isuues Survey

Table 14: Occupations with labour shortages

Table 15: Operation impacts of labour shortages

0

10

20

30

40

50

60

70

80

Next !ve years

Today

OtherMovingproduction and

investment to otherprovinces/ territories

Moving productionand investment

to othercountries

Closing orforegoingproduction

Constrainingbusinessgrowth

Increasing nvestmen

in automation

Increasingfocus

on operationalef!ciency

Increasinglabour costs

55%61%

35% 34%

10% 9%3% 2%

63%

47% 46%

36%

18%

31%

13%

3%

(per

cen

t)

Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 14 |

Leadership makes the difference

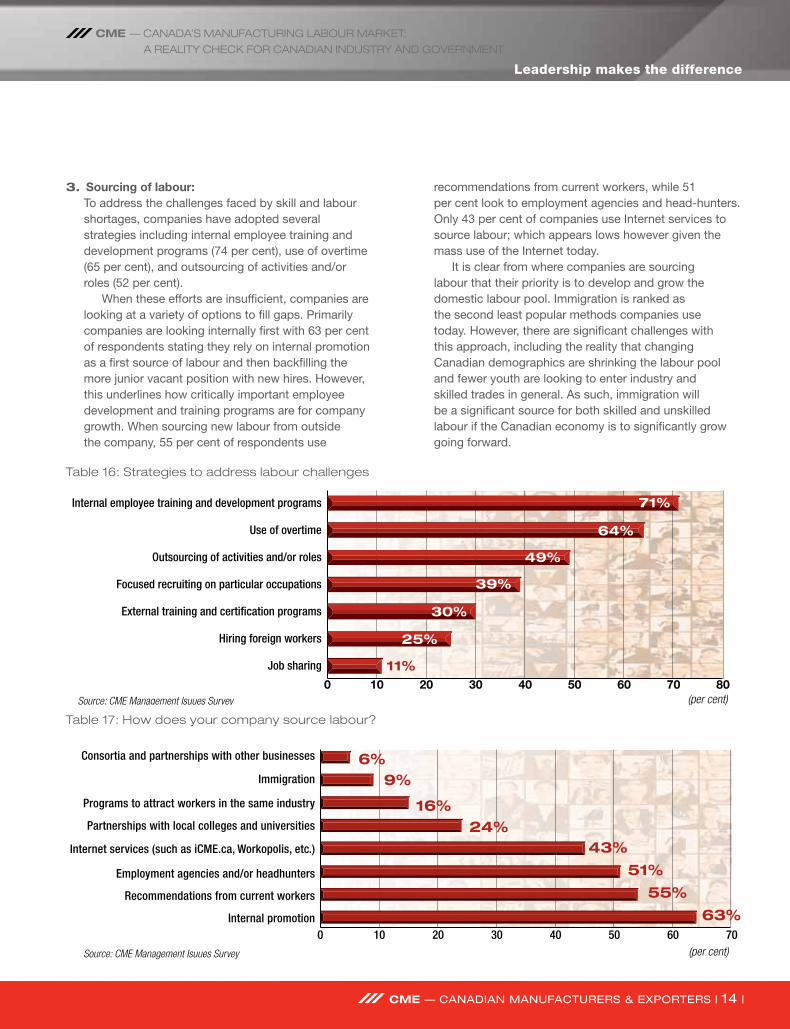

3. Sourcing of labour: To address the challenges faced by skill and labour shortages, companies have adopted several strategies including internal employee training and development!programs (74 per cent), use of overtime (65!per!cent), and outsourcing of activities and/or roles!(52 per cent).

When these efforts are insuf"cient, companies are looking at a variety of options to "ll gaps. Primarily companies are looking internally "rst with 63 per cent of respondents stating they rely on internal promotion as a "rst source of labour and then back"lling the more junior vacant position with new hires. However, this underlines how critically important employee development and training programs are for company growth. When!sourcing new labour from outside the company, 55!per!cent of respondents use

recommendations from!current workers, while 51 per!cent look to employment agencies and head-hunters. Only!43!per!cent of companies use Internet services to source labour; which appears lows however given the mass use of the!Internet today.

It is clear from where companies are sourcing labour!that their priority is to develop and grow the domestic labour pool. Immigration is ranked as the second least popular methods companies use today. However, there are signi"cant challenges with this approach, including the reality that changing Canadian!demographics are shrinking the labour pool and fewer youth are looking to enter industry and skilled trades in general. As such, immigration will be a signi"cant source for both skilled and unskilled labour if the Canadian economy is to signi"cantly grow going!forward.

0 10 20 30 40 50 60 70 80

Job sharing

Hiring foreign workers

External training and certi!cation programs

Focused recruiting on particular occupations

Outsourcing of activities and/or roles

Use of overtime

Internal employee training and development programs

64%

71%

49%

39%

30%

25%

11%

(per cent)Source: CME Management Isuues Survey

Table 16: Strategies to address labour challenges

Table 17: How does your company source labour?

0 10 20 30 40 50 60 70Internal promotion

Recommendations from current workers

Employment agencies and/or headhunters

Internet services (such as iCME.ca, Workopolis, etc.)

Partnerships with local colleges and universities

Programs to attract workers in the same industry

Immigration

Consortia and partnerships with other businesses 6%9%

16%24%

43%51%

55%63%

(per cent)Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 15 |

Leadership makes the difference

4. Training and skills development: Companies have clearly identi"ed employee training as critical in terms of addressing labour shortages as well as building a globally competitive workforce. As noted earlier, companies primarily rely on internal promotion as a source of "lling labour gaps. As such, it is not surprising companies are investing heavily in employee training across the country. In fact, 56 per cent of respondents are spending between one and "ve per cent of their total revenues on employee training today, while nine per cent are spending more than six per cent. Only 35 per cent of companies are spending less than one per cent of total revenues on training.

Companies provide a wide range of employee training today either in-house or with the support of third parties. Over 95 per cent of companies currently provide orientation for new employees, health and safety training, and training in technical skills. However, companies are reporting that despite the need for training in these areas, training will decrease over the next three years. In fact, fewer than 70 per cent of companies are stating they will offer training in these areas in three years time. In most areas of training inquired on, companies are stating less training will be offered in three years than is offered now. This includes areas seen as critical to the

success of companies such as technical training and customer service and sales. The one area of training where CME sees an increase is in language training, which will increase from 62 per cent today to 69 per cent in the next three years. This likely re#ects an expectation that companies will need to source more labour through immigration and from countries where English or French are not the "rst language.

Given the importance of training for corporate success both today and growth in the future, it is critical to understand the measures that would encourage companies to provide more training to their employees. When asking companies to select three possible options to encourage more training, two answers stood out as a the highest priorities; training tax credits with 63 per cent of respondents and direct funds to support training from 59 per cent of companies. Given the importance of internal promotion, the upcoming challenges facing companies due to aging management, and the impending decline of training provided by companies, it is no surprise companies would be motivated to provide!more training if offered these motivational supports. The third most often selected option was a reduction in payroll taxes which was selected by 35!per!cent of respondents.

Table 18: Per cent of revenue spend on employee training

More than 10%

6%–10%

1%–5%

Less than 1%

35%

56%

6% 3%

Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 16 |

Leadership makes the difference

Management

0 20 40 60 80 100

Next three yearsCurrently Provided

Orientation

Health and safety

Technical skills

LEAN

Teamwork

Customer service

Business development

Computer skills

Communication

Language

Essential skills (literacy, math)

Other

65%

62%

75%

76%

77%

78%

78%

78%

80%

87%

96%

96%

97%

69%

62%

71%

75%

74%

73%

71%

70%

70%

61%

67%

69%

69%

(per cent)Source: CME Management Isuues Survey

Table 19: Type of employee training provided

Table 20: Which incentives would encourage increased training:

0 10 20 30 40 50 60 70 80

Better information on training

Increased collaboration with other !rms

Online training programs

Government training programs

Programs targeting industry needs

Better partnerships with the education system

In-house training programs

Lower payroll and taxes

Funds to support training

Training tax credits

59%

63%

35%

26%

22%

17%

14%

14%

11%

8%

(per cent)Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 17 |

Leadership makes the difference

5. Demographics: As noted in Table 10, companies see Canadian demographics as a major threat to their ability to create a globally competitive workforce, ranking the issue as the third highest priority with 39 per cent. Most concerningly, as shown in Table 21, two of the occupational segments identi"ed as the most important for the success and growth of businesses over the next "ve years in Canada as a whole are also where the impact of the aging workforce is expected to be felt the most: skilled production (38 per cent) and management and administration (31 per cent).

Across the country, the impact of demographics varies signi"cantly, with the eastern provinces ranking demographics as more important to their future competi-tiveness than the rest of the country, as shown in Table 22.

Not surprisingly, the provinces with the highest median ages are also those in which companies are most concerned with the impact of demographics on their operations. Canada’s eastern provinces, along with!Quebec and BC, have a higher median age than Canada as a whole, and a considerably higher median age than the prairie provinces.

There is also a direct relationship in most provinces between the median age of the population and the labour!market participation rate. While Canada’s overall labour market participation rate is nearly 70 per!cent, Canada’s eastern provinces (except P.E.I.) along with Quebec and BC, have the lowest labour force participation rates across Canada.

Skilled production(welders,

machinists,operators)

Management andadministration

Generallabour

Scientists,engineers,

R&D technicians

Sales, marketingand customer service

Production support(IT, maintenance)

1%

7% 8%

15%

31%

38%

Source: CME Management Isuues Survey

Table 21: Which occupational segment will the aging workforce have the greatest impact on your operations over the next !ve years?

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 18 |

Leadership makes the difference

0%

10%

20%

30%

40%

50%

60%

70%

BCABSKMBONPQNBNSPEINL

Canada: 39%

55%49%

65%

51%

44%41%

35% 36%

43%40%

Source: CME Management Isuues Survey

Table 22: Importance of demographics on the workforce by province

Table 23: Median age by province

25

30

35

40

45

50

BCABSKMBONPQNBNSPEINL

Canada: 40

4444 43 4442

4038 38

36

42

Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 19 |

Leadership makes the difference

6. Labour mobility: Labour mobility is often cited as a major problem in Canada, both in terms of the movement of workers domestically between provinces as well as bringing foreign workers into the country. As companies become!more globally focused, and as labour shortages continue to increase, the ability of companies to source!labour from a variety of locations will be critical to!their continued success and growth. In the survey, CME speci"cally asked for feedback on the level of!restrictions on labour mobility that companies are facing, as well as which occupational segments are most!affected.

Despite signi"cant attention to these issues over the past number of years by governments, businesses and labour groups, domestic labour mobility in a number of critical professions remains problematic. Companies report signi"cant challenges with the mobility of domestically trained workers in almost all classi"cations of workers between provinces. While internationally trained workers show less mobility challenges, this is likely due to the reality that companies have a higher percentage of domestically trained labour than internationally trained. The occupational segment of scientists, engineers and R&D technicians faces more labour mobility challenges than other occupations across the internationally trained worker classi"cations.

0

20

40

60

80

100

Domesticallytrained

Internationallytrained

OtherProduction support(IT, maintenance)

Scientists, engineers,

R&D technicians

Sales, marketingand customer

service

Generallabour

Managementand

administration

Skilled production(welders, machinists,

operators)

30%29%

45%

26%17%

28%

12%

82% 81%71%

82% 90% 82%

10%

(per

cen

t)

Source: CME Management Isuues Survey

Table 25: Restrictions on labour mobility

Table 24: Canadian labour force participation rates

40%

45%

50%

55%

60%

65%

70%

75%

BCABSKMBONPQNBNSPEINL

Canada: 66.8%64%

60%

68%

63%65% 67%

69% 69% 74%

65%

Source: CME Management Isuues Survey

CME — CANADA’S MANUFACTURING LABOUR MARKET: A REALITY CHECK FOR CANADIAN INDUSTRY AND GOVERNMENT

CME — CANADIAN MANUFACTURERS & EXPORTERS | 20 |

Leadership makes the difference

Summary Analysis and Conclusions:

The functioning of Canada’s labour market is a clear and present priority for Canadian manufacturers. Without an effectively functioning labour market, Canadian companies will struggle to compete, innovate and grow

domestically and internationally. While companies are reporting signi"cant labour shortages today, it is expected to get much worse as Canadian demographics continue to shift, resulting in fewer people in the workforce.

Canadian companies have taken on a variety of tactics to overcome labour and skills shortages including increasing training, using the immigration system, the use of overtime, outsourcing some activities, and investing in new machinery and equipment to automate production and improve productivity wherever possible. However, they are concerned about their ability to maintain and grow their operations in Canada.

While companies must do more to improve their own situations, governments at all levels clearly play a central role in the creation of a globally competitive workforce, including supporting the development of the domestic labour pool and increasing the supply of foreign workers. Governments, too, have been active in attempting to address these concerns, introducing a variety of measures aimed at improving Canada’s labour market performance.

However, given the results of this survey and the ongoing concerns of Canadian manufacturers, governments, industry and academia must work together to address these issues so Canadian industry can continue to grow and play a central role in Canada’s economy.

About CME

Canadian Manufacturers & Exporters (CME) is Canada’s largest industry and trade association representing businesses in all sectors of manufacturing and exporting activity across Canada. Our mandate is to promote the competitiveness of Canadian manufacturers and the success of Canada’s goods and services exporters in markets around the world.

Connect with CME Twitter: @cme_mec, @mfgjobscanada

YouTube: www.youtube.com/manufacturingTV LinkedIn: Canadian Manufacturers & Exporters