PerformanceReview

Metropolitan St. Louis SewerDistrict Pension Plan

3rd Quarter 2014

Pavilion Advisory Group Inc.227 W. Monroe Street, Suite 2020Chicago, IL 60606Phone: 312-798-3200Fax: 312-902-1984www.pavilioncorp.com

1 Performance Summary 1

2 Asset Class Diversification 18

3 Manager Evaluation 24

4 Calendar Year Performance 64

5 Capital Markets Review 66

6 Appendix 74

Table of Contents

Performance Summary

1

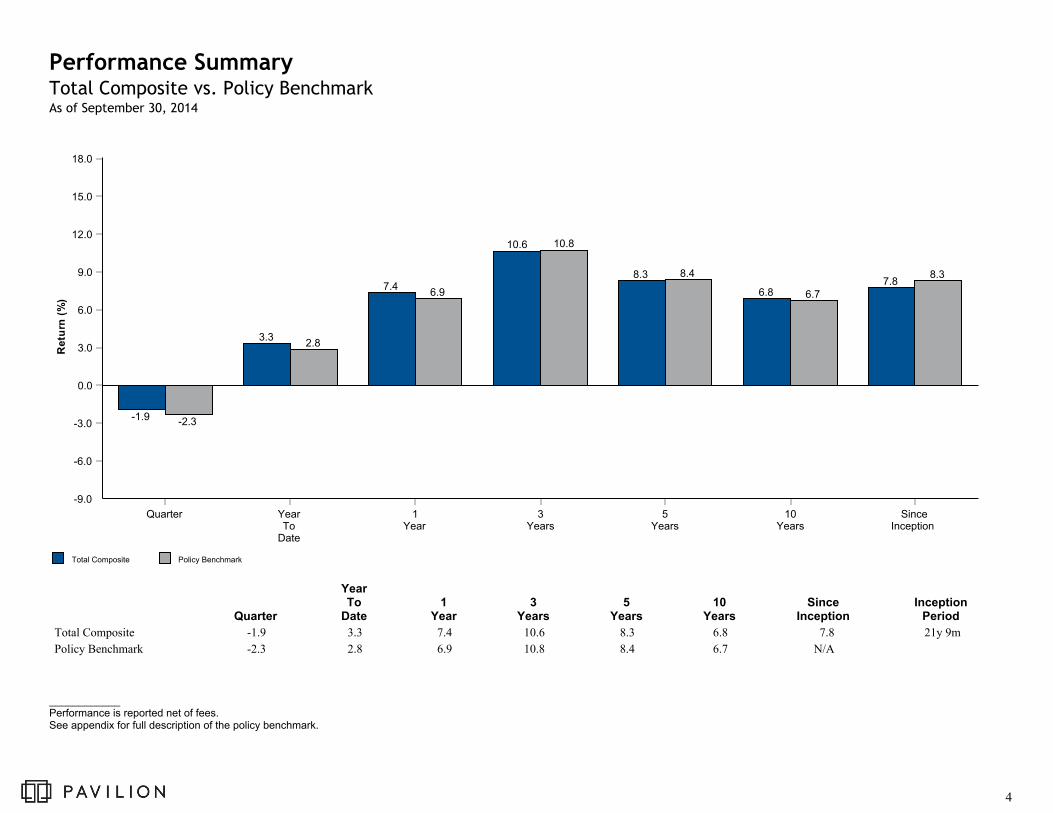

Performance Summary - September 2014During the third quarter, the Metropolitan St. Louis Sewer District declined -1.9%, outperforming the Policy Benchmark return of -2.3%. On a trailing one-year basis, the Plan returned7.4%, outpacing the Policy Benchmark by 50 basis points.

Asset Class DiversificationThe Finance Committee approved new asset allocation policy targets and allowable asset class ranges at the February 2014 meeting. Current asset allocation was within investment policyranges and very close to targets.

Manager EvaluationDuring the third quarter, the following managers notably outperformed their respective benchmarks: T. Rowe Price Institutional Large-Cap Growth, Kennedy Mid Cap Value,TimesSquare Small Cap Growth Fund, Morgan Stanley International Equity Fund, Brandywine Global Opportunistic Fixed Income, and UBS Trumbull Property Fund. Third quarterperformance was negatively impacted by the following managers as they underperformed their respective benchmarks: Holland Large Cap Growth, Penn Capital, GMO Asset AllocationFund, and PIMCO All Asset Fund.

Capital Markets ReviewIt was a difficult quarter in the capital markets. U.S. large cap equities posted modest gains while small cap equities severely underperformed. International equity declined across foreignmarkets, with developed markets underperforming emerging markets. Fixed income volatility returned to the market highlighted by a flight to quality in long term rates. Local currencyinternational debt performed the poorly due to a strengthening U.S. dollar. An expansion of Russia’s invasion of Ukraine, Israel’s military actions to clear Gaza of missiles and tunnelsused by attackers, and ISIS conquering territory across Iraq caused investors to pull monies out of Europe and Asia for the perceived safety of the U.S. dollar and Treasury bonds.

The rapid ascent of the U.S. dollar sent foreign investment values sharply lower versus their local-currency returns. A wave of economic weakness enveloped Europe, Japan, Brazil, Chinaand many smaller countries. The European Central Bank (ECB) inched closer toward purchasing asset-backed bonds, while further lowering its deposit rate to -0.2%. With the Germaneconomy near a zero-growth rate and countries such as Greece and Spain pleading for an end to austerity, the Eurozone economy offered little near-term outlook for growth. Hopes turnedto the ECB to offer a Federal Reserve style bailout and inflate the flagging economy, though the bank has been reluctant to put plans into action based on German leaders’ protests. Theimpending culmination of the Federal Reserve’s asset purchases was a late-quarter headwind for stocks.

The U.S. economy faced a perplexing mix of economic readings. The unemployment rate fell to 5.9%, though the number of workers leaving the workforce remained dauntingly high.Retail sales were choppy, yet on an upward trend. A steep drop in oil prices, brought on by increased U.S. production, will be a negative for upcoming energy spending, due to fallinggasoline prices, but will be a broader benefit for the economy.

Recommendations or Action ItemsPavilion downgraded PIMCO’s manager rating status from “negative watch” to “sell.” Pavilion initially downgraded PIMCO to “negative watch” in January following the departure of co-CIO Mohamed El-Erian, and noted we would closely monitor the firm for organizational stability, asset flows, and performance. PIMCO has not made clear improvements in these areas,and the departure of Bill Gross creates a multitude of future unknowns for the firm. Pavilion recommends termination of the PIMCO All Asset Fund in the Pension Plan due to poorperformance and organizational issues and instability. The fund has approximately $10.1 million invested as of September 30, 2014.

Pavilion is conducting a hedge fund of funds manager search for two managers. The hedged equity manager search is complete and Pavilion recommends hiring the Lighthouse GlobalLong/Short Equity Fund to replace the PIMCO All Asset fund. The multi-strategy hedge fund of funds is still in progress with additional managers requiring analysis and further duediligence. Pavilion will bring a second recommendation to the Committee when the work is complete and the Secretary-Treasurer has conducted the appropriate due diligence on managersearch projects.

Pension Plan Executive Summary

2

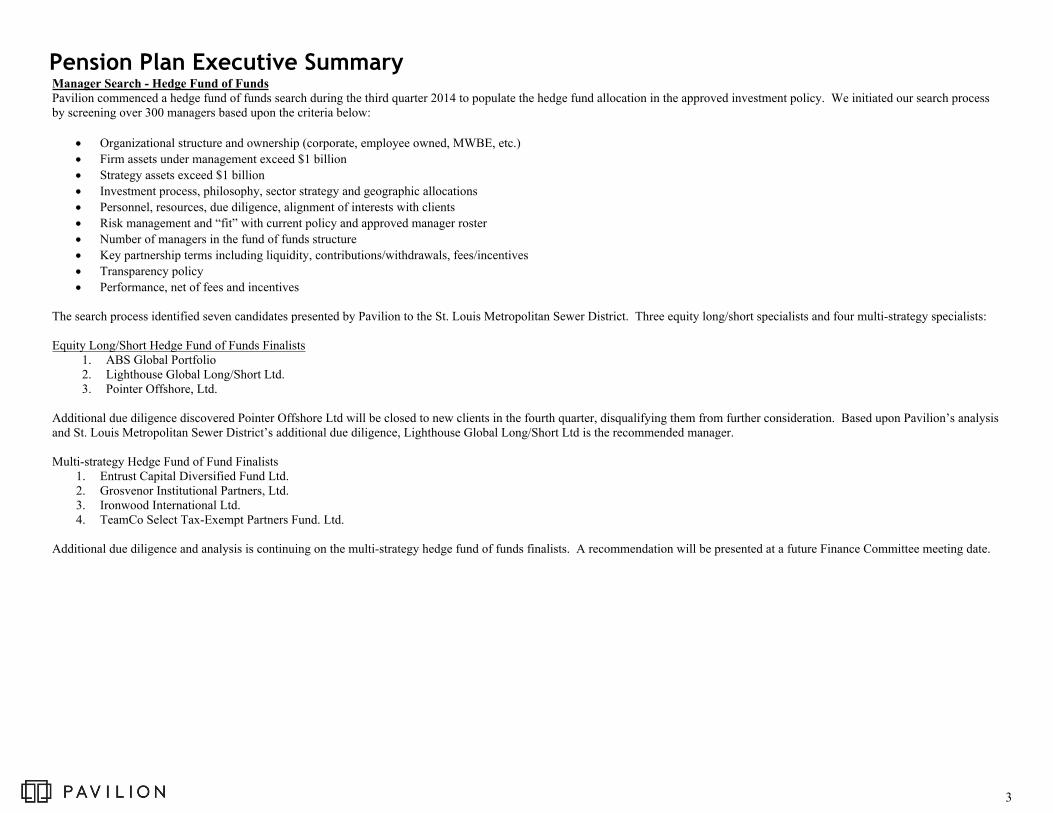

Pension Plan Executive SummaryManager Search - Hedge Fund of FundsPavilion commenced a hedge fund of funds search during the third quarter 2014 to populate the hedge fund allocation in the approved investment policy. We initiated our search processby screening over 300 managers based upon the criteria below:

· Organizational structure and ownership (corporate, employee owned, MWBE, etc.)

· Firm assets under management exceed $1 billion

· Strategy assets exceed $1 billion

· Investment process, philosophy, sector strategy and geographic allocations

· Personnel, resources, due diligence, alignment of interests with clients

· Risk management and “fit” with current policy and approved manager roster

· Number of managers in the fund of funds structure

· Key partnership terms including liquidity, contributions/withdrawals, fees/incentives

· Transparency policy

· Performance, net of fees and incentives

The search process identified seven candidates presented by Pavilion to the St. Louis Metropolitan Sewer District. Three equity long/short specialists and four multi-strategy specialists:

Equity Long/Short Hedge Fund of Funds Finalists1. ABS Global Portfolio2. Lighthouse Global Long/Short Ltd.3. Pointer Offshore, Ltd.

Additional due diligence discovered Pointer Offshore Ltd will be closed to new clients in the fourth quarter, disqualifying them from further consideration. Based upon Pavilion’s analysisand St. Louis Metropolitan Sewer District’s additional due diligence, Lighthouse Global Long/Short Ltd is the recommended manager.

Multi-strategy Hedge Fund of Fund Finalists1. Entrust Capital Diversified Fund Ltd.2. Grosvenor Institutional Partners, Ltd.3. Ironwood International Ltd.4. TeamCo Select Tax-Exempt Partners Fund. Ltd.

Additional due diligence and analysis is continuing on the multi-strategy hedge fund of funds finalists. A recommendation will be presented at a future Finance Committee meeting date.

3

Total Composite Policy Benchmark

0.0

3.0

6.0

9.0

12.0

15.0

18.0

-3.0

-6.0

-9.0

Re

turn

(%)

Quarter YearTo

Date

1Year

3Years

5Years

10Years

SinceInception

-2.3

2.8

6.9

10.8

8.4

6.7

8.3

-1.9

3.3

7.4

10.6

8.3

6.87.8

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Total Composite -1.9 3.3 7.4 10.6 8.3 6.8 7.8 21y 9m

Policy Benchmark -2.3 2.8 6.9 10.8 8.4 6.7 N/A

Performance SummaryTotal Composite vs. Policy BenchmarkAs of September 30, 2014

____________Performance is reported net of fees.See appendix for full description of the policy benchmark.

4

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

24.0R

etu

rn

Quarter

YearTo

Date1

Year3

Years5

Years7

Years10

Years

Total Composite -1.9 (89) 3.3 (79) 7.4 (94) 10.6 (94) 8.3 (95) 4.9 (60) 6.8 (46)¢£

5th Percentile 0.2 6.2 13.0 15.8 11.5 6.3 8.0

1st Quartile -0.7 4.9 11.4 14.5 10.6 5.7 7.4

Median -1.1 4.2 10.2 13.6 10.0 5.2 6.8

3rd Quartile -1.5 3.4 9.0 12.6 9.4 4.6 6.4

95th Percentile -2.2 2.2 7.1 10.2 8.2 3.4 5.9

Performance ComparisonAll Public Plans <= $500 milAs of September 30, 2014

_________________________Performance is reported net of fees.Parentheses contain percentile rankings.Calculation based on monthly periodicity.

5

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

16.0

20.0

24.0R

etu

rn

Quarter

YearTo

Date1

Year3

Years5

Years7

Years10

Years

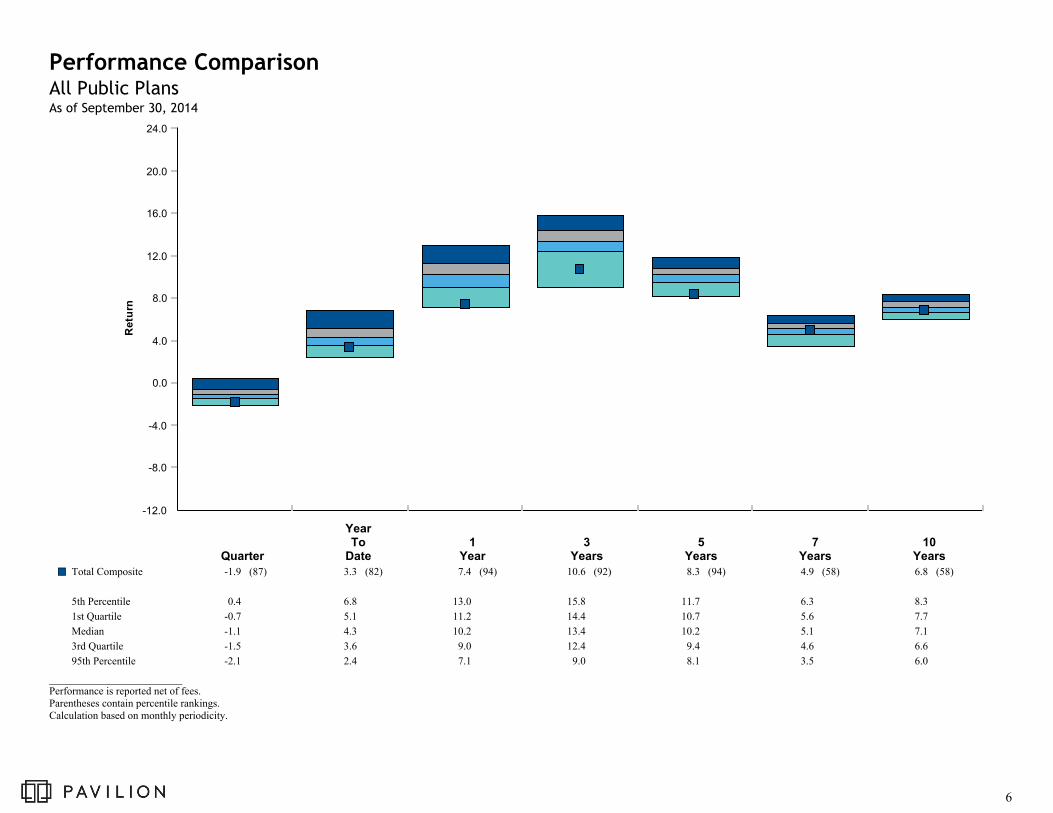

Total Composite -1.9 (87) 3.3 (82) 7.4 (94) 10.6 (92) 8.3 (94) 4.9 (58) 6.8 (58)¢£

5th Percentile 0.4 6.8 13.0 15.8 11.7 6.3 8.3

1st Quartile -0.7 5.1 11.2 14.4 10.7 5.6 7.7

Median -1.1 4.3 10.2 13.4 10.2 5.1 7.1

3rd Quartile -1.5 3.6 9.0 12.4 9.4 4.6 6.6

95th Percentile -2.1 2.4 7.1 9.0 8.1 3.5 6.0

Performance ComparisonAll Public PlansAs of September 30, 2014

_________________________Performance is reported net of fees.Parentheses contain percentile rankings.Calculation based on monthly periodicity.

6

3 Years 5 Years

5.0

7.0

9.0

11.0

13.0

14.0

Retu

rn (%

)

5.0 5.7 6.4 7.1 7.8 8.5 9.0

Risk (Standard Deviation %)

Policy Benchmark(7.7 , 8.4)

Total Composite(7.8 , 8.3)

5.0

7.0

9.0

11.0

13.0

14.0

Retu

rn (%

)

5.0 5.7 6.4 7.1 7.8 8.5 9.0

Risk (Standard Deviation %)

Policy Benchmark(6.7 , 10.8)

Total Composite(6.9 , 10.6)

Performance SummaryRisk and Return SummaryAs of September 30, 2014

7

Allocation

MarketValue

($) %

Performance(%)

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Total Composite 250,168,126 100.0 -1.9 3.3 7.4 10.6 8.3 6.8 7.8 21y 9m

Policy Benchmark -2.3 2.8 6.9 10.8 8.4 6.7 N/A

Total Equity Composite 102,579,206 41.0 -1.7 3.5 12.1 N/A N/A N/A 16.2 1y 1m

MSCI AC World IMI -2.7 3.6 11.3 17.4 10.9 8.1 15.9

Domestic Equity Composite 68,026,916 27.2 -0.1 (13) 5.4 (19) 16.1 (15) N/A N/A N/A 19.3 (N/A) 1y 1m

Russell 3000 Index 0.0 (11) 7.0 (8) 17.8 (9) 23.1 (14) 15.8 (12) 8.4 (33) 20.3 (N/A)

Broad Equity Peer Group Median -1.4 3.9 13.6 20.9 14.0 8.0 N/A

Large-Cap Equity Composite 53,317,156 21.3 1.0 (28) 6.7 (40) 18.0 (33) 21.6 (49) 14.3 (49) 8.1 (42) 8.7 (N/A) 11y 4m

Russell 1000 Index 0.7 (35) 8.0 (19) 19.0 (22) 23.2 (26) 15.9 (20) 8.5 (33) 9.1 (N/A)

Large-Cap Equity Peer Group Median 0.1 6.0 16.4 21.5 14.3 7.8 N/A

Small-Cap Equity Composite 14,709,760 5.9 -3.8 (8) 1.0 (7) 9.6 (10) 22.9 (27) 17.1 (11) 11.1 (5) 11.9 (N/A) 11y 4m

Russell 2000 Index -7.4 (65) -4.4 (50) 3.9 (53) 21.3 (47) 14.3 (51) 8.2 (44) 9.8 (N/A)

Small-Cap Equity Peer Group Median -6.6 -4.4 4.2 20.8 14.3 8.0 N/A

International Equity Composite 34,552,290 13.8 -4.7 (31) -0.2 (39) 4.5 (46) N/A N/A N/A 10.2 (N/A) 1y 1m

MSCI AC World ex USA Index -5.3 (52) 0.0 (36) 4.8 (41) 11.8 (60) 6.0 (57) 7.1 (63) 11.1 (N/A)

International Equity Peer Group Median -5.2 -0.8 4.3 12.2 6.3 7.4 N/A

Developed International Equity Composite 27,171,164 10.9 -5.0 (27) -0.7 (34) 4.9 (40) 14.5 (32) 7.4 (38) 6.3 (59) 5.2 (N/A) 15y 5m

MSCI EAFE Index -5.9 (53) -1.4 (44) 4.3 (52) 13.6 (48) 6.6 (55) 6.3 (58) 4.0 (N/A)

Developed International Equity Peer Group Median -5.8 -1.7 4.3 13.6 6.8 6.6 N/A

Emerging International Equity Composite 7,381,126 3.0 -3.5 (44) 1.9 (57) 3.6 (62) 7.7 (60) 4.8 (46) N/A 8.9 (46) 9y 6m

MSCI Emerging Markets Index -3.5 (44) 2.4 (47) 4.3 (52) 7.2 (66) 4.4 (52) 10.7 (37) 9.2 (34)

Emerging Markets Equity Peer Group Median -3.7 2.2 4.4 8.1 4.5 10.0 8.5

Fixed Income Composite 87,074,484 34.8 -1.7 (100) 3.0 (43) 3.3 (45) 4.4 (21) 5.2 (29) 5.4 (10) 5.1 (14) 11y 3m

Barclays Intermediate U.S. Government/Credit 0.0 (37) 2.2 (73) 2.2 (73) 2.0 (82) 3.4 (77) 4.0 (74) 3.8 (74)

Intermediate Duration Fixed Income Peer Group Median -0.1 2.6 3.0 2.9 4.5 4.6 4.4

Performance SummaryTotal Pension Fund Asset Allocation and PerformanceAs of September 30, 2014

_________________________Performance is reported net of fees.

8

Performance SummaryTotal Pension Fund Asset Allocation and PerformanceAs of September 30, 2014

Allocation

MarketValue

($) %

Performance(%)

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Tactical Asset Allocation Composite 25,034,719 10.0 -2.8 2.5 6.9 9.8 7.7 6.7 6.4 11y 4m

65% MSCI World (Net) / 35% BC Aggregate -1.3 4.0 9.3 12.4 8.7 6.6 7.3

Alternatives Composite 10,088,586 4.0 -2.9 4.5 4.8 N/A N/A N/A 6.0 1y 1m

3 Month T-Bills + 3% 0.8 2.3 3.0 3.1 3.1 4.6 3.0

Real Estate Composite 13,188,272 5.3 2.9 7.5 9.6 9.3 10.0 6.7 4.9 8y 4m

NCREIF Fund Index-Open End Diversified Core Equity 0.0 5.4 8.6 10.9 11.3 6.4 4.5

Real Assets Composite 10,896,322 4.4 -8.0 -0.3 2.4 1.9 N/A N/A 1.8 4y 6m

Wellington DIH Multi-Asset Inflation Index -8.1 -1.1 0.4 1.5 2.3 4.9 1.0

Cash Account 1,306,537 0.5 0.0 0.0 0.1 0.1 -0.3 1.5 1.4 11y 4m

BofA Merrill Lynch 3 Month U.S. T-Bill 0.0 0.0 0.0 0.1 0.1 1.6 1.5

_________________________Performance is reported net of fees.

9

Allocation

MarketValue

($) %

Performance(%)

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Domestic Large-Cap Equity Managers

Vanguard Windsor II 14,123,604 5.6 -0.2 (47) 7.4 (26) 17.7 (34) 22.8 (36) 14.8 (33) 8.0 (39) 6.6 (N/A) 13y 5m

Russell 1000 Value Index -0.2 (47) 8.1 (17) 18.9 (22) 23.9 (22) 15.3 (24) 7.8 (42) 6.6 (N/A)

Large-Cap Value Equity Peer Group Median -0.3 6.1 16.2 21.8 14.0 7.5 N/A

Vanguard Institutional Index Fund 12,433,727 5.0 1.1 (25) 8.3 (15) 19.7 (17) 23.0 (30) 15.7 (24) 8.1 (42) 4.9 (64) 15y

S&P 500 1.1 (25) 8.3 (15) 19.7 (16) 23.0 (29) 15.7 (24) 8.1 (42) 4.9 (65)

Large-Cap Equity Peer Group Median 0.1 6.0 16.4 21.5 14.3 7.8 5.6

T. Rowe Price Inst. Large-Cap Core Growth 13,819,925 5.5 1.8 (29) 4.8 (62) 18.2 (33) 24.6 (11) 17.4 (15) 9.0 (40) 23.9 (N/A) 1y 7m

Russell 1000 Growth Index 1.5 (38) 7.9 (21) 19.1 (24) 22.4 (36) 16.5 (24) 8.9 (42) 21.7 (N/A)

Large-Cap Growth Equity Peer Group Median 1.1 5.5 16.7 21.5 15.1 8.5 N/A

Holland Large Cap Growth 12,939,900 5.2 1.2 (47) 5.2 (55) 15.7 (62) 19.5 (76) 15.1 (51) 8.1 (60) 17.2 (N/A) 1y 7m

Russell 1000 Growth Index 1.5 (38) 7.9 (21) 19.1 (24) 22.4 (36) 16.5 (24) 8.9 (42) 21.7 (N/A)

Large-Cap Growth Equity Peer Group Median 1.1 5.5 16.7 21.5 15.1 8.5 N/A

Domestic Small-Cap Equity Managers

Kennedy Mid Cap Value 8,384,999 3.4 -2.3 (21) 11.9 (1) 20.9 (1) 24.8 (14) 17.7 (7) N/A 11.6 (1) 6y 9m

Russell Midcap Value Index -2.6 (28) 8.2 (7) 17.5 (6) 24.7 (15) 17.2 (10) 10.2 (16) 8.5 (24)

Mid-Cap Value Equity Peer Group Median -4.1 1.6 10.0 21.4 14.6 8.9 7.4

TimesSquare Small Cap Growth Fund 6,324,761 2.5 -5.7 (46) -11.1 (89) -2.9 (88) 20.0 (52) 15.9 (28) 11.6 (6) 9.9 (N/A) 12y 8m

Russell 2000 Growth Index -6.1 (56) -4.0 (33) 3.8 (30) 21.9 (38) 15.5 (34) 9.0 (30) 7.6 (N/A)

Small-Cap Growth Equity Peer Group Median -5.8 -5.5 1.9 20.1 14.7 8.0 N/A

Developed International Equity Manager

Morgan Stanley International Equity Fund I 27,171,164 10.9 -5.0 (27) -0.8 (36) 4.7 (43) 14.5 (33) 7.4 (38) 6.5 (55) 5.2 (57) 9y 6m

MSCI EAFE Index -5.9 (53) -1.4 (44) 4.3 (52) 13.6 (48) 6.6 (55) 6.3 (58) 5.1 (62)

International Equity Peer Group Median -5.8 -1.7 4.3 13.6 6.8 6.6 5.4

Emerging Markets Equity Manager

Morgan Stanley Emerging Markets Fund I 7,381,126 3.0 -3.5 (44) 1.9 (57) 3.7 (61) 7.7 (59) 4.8 (45) 10.4 (42) 8.9 (45) 9y 6m

MSCI Emerging Markets Index -3.5 (44) 2.4 (47) 4.3 (52) 7.2 (66) 4.4 (52) 10.7 (37) 9.2 (34)

Emerging Markets Equity Peer Group Median -3.7 2.2 4.4 8.1 4.5 10.0 8.5

Performance SummaryManager Asset Allocation and PerformanceAs of September 30, 2014

_________________________Performance is reported net of fees.

10

Performance SummaryManager Asset Allocation and PerformanceAs of September 30, 2014

Allocation

MarketValue

($) %

Performance(%)

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Fixed Income Managers

Income Research 35,723,915 14.3 -0.1 (40) 2.5 (63) 2.5 (65) 2.9 (51) 4.0 (60) 4.9 (25) 5.4 (24) 13y 3m

Barclays Intermediate U.S. Government/Credit 0.0 (37) 2.2 (73) 2.2 (73) 2.0 (82) 3.4 (77) 4.0 (74) 4.7 (60)

Intermediate Duration Fixed Income Peer Group Median -0.1 2.6 3.0 2.9 4.5 4.6 4.8

Penn Capital 12,764,809 5.1 -2.2 (81) 2.0 (93) 5.6 (88) 8.4 (93) 8.9 (84) N/A 6.6 (87) 9y 3m

BofA Merrill Lynch US High Yield, Cash Pay Index -1.9 (54) 3.5 (40) 7.1 (39) 10.9 (46) 10.3 (35) 8.1 (25) 8.2 (25)

High Yield Fixed Income Peer Group Median -1.9 3.3 6.9 10.8 10.0 7.6 7.7

Loomis Credit Asset Fund 4,986,911 2.0 -0.6 (55) 3.9 (13) 6.3 (9) 8.8 (1) N/A N/A 8.0 (1) 4y 7m

50% BC Credit / 25% S&P LSTA / 25% BY High Yield -0.6 (54) 4.2 (12) 6.1 (9) 6.8 (10) 7.3 (1) 6.2 (9) 6.9 (1)

Alternative Credit Focus Funds Peer Group Median -0.5 1.8 3.6 4.1 5.2 4.3 4.4

Brandywine Global Opportunistic Fixed Income 22,103,853 8.8 -2.0 (54) 6.2 (9) 5.9 (21) 5.6 (20) 7.6 (3) N/A 6.7 (9) 9y 9m

Citigroup World Government Bond -3.8 (82) 1.0 (82) -0.1 (91) -0.5 (95) 1.6 (91) 4.1 (71) 3.3 (77)

Global Fixed Income Peer Group Median -1.8 2.5 3.3 2.9 4.2 4.9 4.3

Pictet Emerging Local Currency Debt Fund 11,494,996 4.6 -5.5 (43) -1.0 (72) -2.5 (70) 0.8 (85) N/A N/A 0.8 (85) 3y

JPM GBI-EM Global Diversified -5.7 (58) 0.0 (42) -1.5 (42) 2.2 (40) 4.4 (15) 8.8 (N/A) 2.2 (40)

Emerging Markets (LC) Fixed Income Peer Group Median -5.6 -0.3 -1.9 1.9 3.8 N/A 1.9

Tactical Asset Allocation Manager

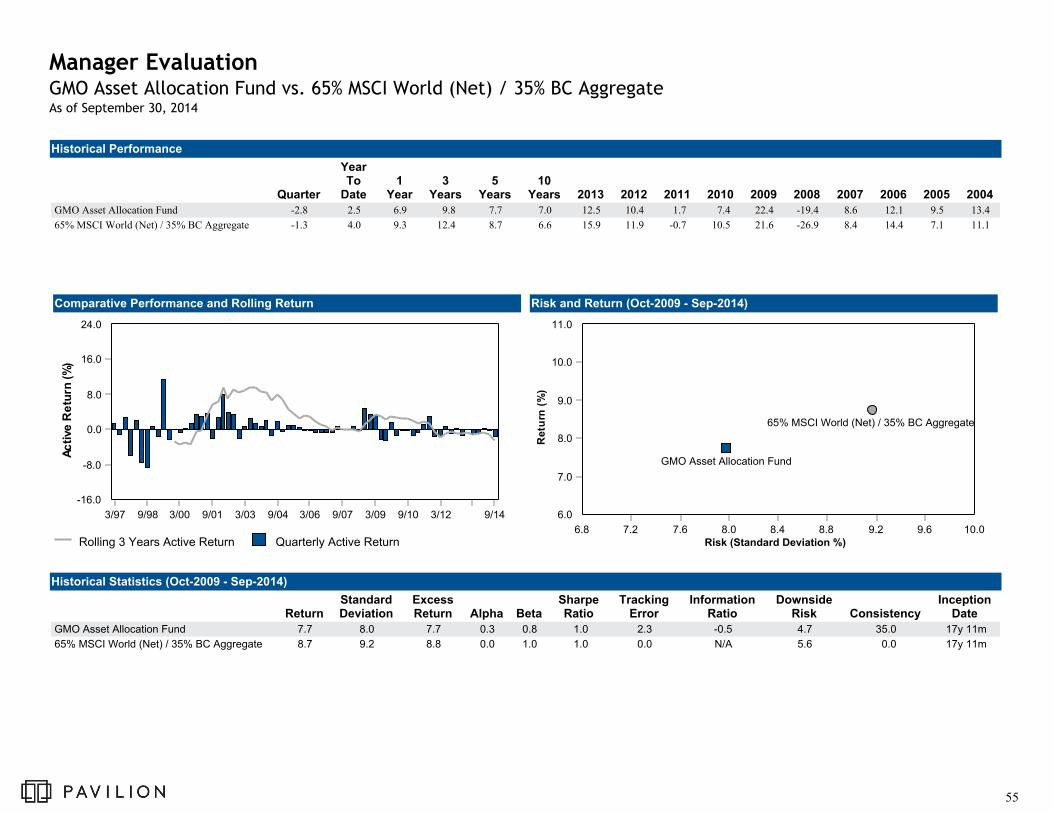

GMO Asset Allocation Fund 25,034,719 10.0 -2.8 (67) 2.5 (59) 6.9 (62) 9.8 (61) 7.7 (66) 7.0 (30) 6.0 (37) 8y 2m

65% MSCI World (Net) / 35% BC Aggregate -1.3 (35) 4.0 (37) 9.3 (35) 12.4 (33) 8.7 (47) 6.6 (38) 5.6 (50)

IM Flexible Portfolio (MF) Median -1.9 3.2 7.8 10.7 8.6 6.1 5.6

_________________________Performance is reported net of fees.

11

Performance SummaryManager Asset Allocation and PerformanceAs of September 30, 2014

Allocation

MarketValue

($) %

Performance(%)

Quarter

YearTo

Date1

Year3

Years5

Years10

YearsSince

InceptionInception

Period

Alternatives Manager

PIMCO All Asset Fund I 10,088,586 4.0 -2.9 3.8 5.2 8.0 7.5 6.4 6.1 8y 9m

Barclays U.S. Treasury Inflation Notes: 1-10 Year -2.0 1.9 0.6 0.9 3.4 4.0 4.2

Real Estate Manager

UBS Trumbull Property Fund 13,188,272 5.3 2.9 7.5 9.6 9.3 10.0 6.7 4.9 8y 4m

NCREIF Fund Index-Open End Diversified Core Equity 0.0 5.4 8.6 10.9 11.3 6.4 4.5

Real Asset Manager

Wellington Diversified Inflation Hedges 10,896,322 4.4 -8.0 -0.3 2.4 1.9 N/A N/A 1.8 4y 6m

Wellington DIH Multi-Asset Inflation Index -8.1 -1.1 0.4 1.5 2.3 4.9 1.0

Cash Account 1,306,537 0.5 0.0 0.0 0.1 0.1 -0.3 1.5 1.4 11y 4m

BofA Merrill Lynch 3 Month U.S. T-Bill 0.0 0.0 0.0 0.1 0.1 1.6 1.5

Total Composite 250,168,126 100.0 -1.9 3.3 7.4 10.6 8.3 6.8 7.8 21y 9m

_________________________Performance is reported net of fees.

12

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

Retu

rn (%

)

12.0 13.0 14.0 15.0 16.0 17.0 18.0 19.0 20.0 21.0 22.0

Risk (Standard Deviation %)

Russell 2000 Growth

Russell Midcap Value

Russell 1000 Growth

S&P 500 Russell 1000 Value

Holland Large Cap Growth

Kennedy Mid Cap Value

TimesSquare Small Cap Growth

Vanguard Windsor II Fund

Vanguard Institutional Index Fund

T. Rowe Price Inst. Large-Cap Core Growth

Performance SummaryRisk and Return Summary - Equity Managers5 Years Ending September 30, 2014

13

0.0

1.5

3.0

4.5

6.0

7.5

9.0

10.5

12.0

Re

turn

(%)

0.0 1.5 3.0 4.5 6.0 7.5 9.0 10.5 12.0 13.5

Risk (Standard Deviation %)

50% BC Credit / 25% S&P LSTA / 25% BY High Yield

JPM GBI-EM Global Diversified

Citigroup World Government Bond

BofA Merrill Lynch US High Yield, Cash Pay Index

BC Intermediate U.S. Government/Credit

Penn Capital

Income Research

Brandywine Global

Performance SummaryRisk and Return Summary - Fixed Income Managers5 Years Ending September 30, 2014

14

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Re

turn

(%)

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0

Risk (Standard Deviation %)

90 Day U.S. Treasury Bill

Barclays U.S. Treasury Inflation Notes: 1-10 Year

NCREIF Fund Index-Open End Diversified Core Equity

Wellington DIH Multi-Asset Inflation Index

65% MSCI World (Net) / 35% BC Aggregate

UBS TPF

PIMCO All AssetGMO

Performance SummaryRisk and Return Summary - Alternative Managers5 Years Ending September 30, 2014

15

Manager Compliance ChecklistThird Quarter 2014

Managers

Vanguard

Windsor

Vanguard

Institutional

T. Rowe

Price Holland Kennedy TimesSquare

Morgan

Stanley Int'l

Morgan

Stanley EM

Organizational/Product Issues

No material changes to investment team + + + + + + - +No material organizational changes + + + + + + + +

Accounting or regulatory concerns + + + + + + + +

Currently in adherence to guidelines + + + + + + + +

Portfolio characteristics meet stylistic expectations + + + + + + + +

Relative Performance 1

Three-year return better than benchmark - N/A + - + - + +Three-year ranking better than peer group median + + + - + - + -

Five year return better than benchmark - N/A + - + + + +

1 Manager performance is evaluated net of investment management fees.

+ + + + +

Five year ranking better than peer group median + + + - + + + +

Performance status + + + + + + + +

Date performance status changed

Summary status Sell + + + + + + Sell

Date summary status changed 4Q13 4Q13

16

Manager Compliance ChecklistThird Quarter 2014

Managers

Income

Research Penn Loomis

Brandywine

Global Pictet GMO PIMCO UBS Wellington

Organizational/Product Issues

No material changes to investment team + + + - + + - + +No material organizational changes + + + + + + + + +

Accounting or regulatory concerns + + + + + + + + +

Currently in adherence to guidelines + + + + + + + + +

Portfolio characteristics meet stylistic expectations + + + + + + + + +

Relative Performance 1

Three-year return better than benchmark + - + + - - + - +

Three-year ranking better than peer group median - - + + - - N/A N/A N/A

Five year return better than benchmark + - N/A + N/A - + - N/A

1 Manager performance is evaluated net of investment management fees.

Five year return better than benchmark + - N/A + N/A - + - N/A

Five year ranking better than peer group median - - N/A + N/A - N/A N/A N/A

Performance status + - + + - - + + +

Date performance status changed 4Q13 4Q13 3Q14

Summary status + Sell Sell + Sell Sell Sell + +

Date summary status changed 4Q13 4Q13 4Q13 4Q13 4Q13

17

Asset Class Diversification

18

September 30, 2014 : $250,168,126

Target Allocation Actual Allocation Allocation Differences

0.0% 6.0% 12.0% 18.0% 24.0% 30.0% 36.0% 42.0%-6.0 %-12.0 %

Cash Account$1,306,537

Real Asset Composite$10,896,322

Real Estate Composite$13,188,272

Alternatives Composite$10,088,586

Tactical Asset Allocation Composite$25,034,719

Fixed Income Composite$87,074,484

Emerging International Equity Composite$7,381,126

Developed International Equity Composite$27,171,164

Small-Cap Equity Composite$14,709,760

Large-Cap Equity Composite$53,317,156

0.0%

5.0%

5.0%

4.0%

10.0%

35.0%

3.0%

11.0%

6.0%

21.0%

0.5%

4.4%

5.3%

4.0%

10.0%

34.8%

3.0%

10.9%

5.9%

21.3%

0.5%

-0.6 %

0.3%

0.0%

0.0%

-0.2 %

0.0%

-0.1 %

-0.1 %

0.3%

Asset Class DiversificationInvestment Policy AllocationAs of September 30, 2014

19

Asset Class/Type Manager

Total Assets

($, mil.) as of

9/30/2014

Percent of

Total

Target

Allocation

Weighting

Relative to

Target

Allowable

Range

Total Assets

($, mil.) as of

7/1/2014

Large-Cap Equity $53.3 21.3% 21.0% + 0.3% 15 - 25% $55.9

Core Vanguard Institutional $12.4 5.0% 6.0% - 1.0% $12.3

Value Vanguard Windsor $14.1 5.6% 5.0% + 0.6% $16.0

Growth T. Rowe Price $13.8 5.5% 5.0% + 0.5% $13.6

Growth Holland $12.9 5.2% 5.0% + 0.2% $14.0

Small-Cap Equity $14.7 5.9% 6.0% - 0.1% 2 - 8% $15.6

Value Kennedy $8.4 3.4% 3.0% + 0.4% $8.9

Growth TimesSquare $6.3 2.5% 3.0% - 0.5% $6.7

International Equity $34.6 13.8% 14.0% - 0.2% $36.3

Developed Morgan Stanley $27.2 10.9% 11.0% - 0.1% 5 - 15% $28.6

Emerging Markets Morgan Stanley $7.4 3.0% 3.0% - 0.0% 2 - 8% $7.6

Fixed Income $87.1 34.8% 35.0% - 0.2% $88.5

Asset Class DiversificationInvestment Program StructureAs of September 30, 2014

Fixed Income $87.1 34.8% 35.0% - 0.2% $88.5

Domestic Core Income Research $35.7 14.3% 14.0% + 0.3% 10 - 20% $35.7

High Yield Penn Capital $12.8 5.1% 5.0% + 0.1% 0 - 7% $13.0

Opportunistic Credit Loomis $5.0 2.0% 2.0% - 0.0% 0 - 5% $5.0

Global Brandywine Global $22.1 8.8% 9.0% - 0.2% 4 - 14% $22.5

Emerging Markets Debt Pictet $11.5 4.6% 5.0% - 0.4% 0 - 7% $12.2

Tactical $25.0 10.0% 10.0% + 0.0% $25.8

Balanced GMO $25.0 10.0% 10.0% + 0.0% 0 - 12% $25.8

Alternatives $10.1 4.0% 4.0% + 0.0% $10.4

Absolute Return PIMCO $10.1 4.0% 4.0% + 0.0% 0 - 7% $10.4

Hedge Funds TBD $0.0 0.0% -- -- 0 - 20% $0.0

Real Estate $13.2 5.3% 5.0% + 0.3% $12.8

Real Estate UBS Trumbull $13.2 5.3% 5.0% + 0.3% 0 - 10% $12.8

Real Asset $10.9 4.4% 5.0% - 0.6% $11.8

Real Asset Wellington $10.9 4.4% 5.0% - 0.6% 0 - 10% $11.8

Cash $1.3 0.5% 0.0% + 0.5% $1.3

Cash Account Cash Account $1.3 0.5% 0.0% + 0.5% $1.3

Total $250.2 100.0% 100.0% + 0.0% $258.4

*Totals may not add to exactly 100.0% due to rounding.

20

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

British American Tobacco PLC 1.2 0.3 1.0 -3.8

Reckitt Benckiser Group PLC 1.2 0.1 1.1 0.6

Sanofi 1.2 0.3 0.9 6.5

Apple Inc 1.2 1.4 -0.2 9.0

Nestle SA, Cham Und Vevey 1.2 0.6 0.6 -5.1

Unilever NV 1.2 0.2 1.0 -8.1

Gilead Sciences Inc 1.1 0.4 0.7 28.4

Amazon.com Inc 1.1 0.3 0.8 -0.7

Google Inc (Class C) 1.0 0.4 0.6 0.4

Novartis AG 1.0 0.5 0.5 4.2

% of Portfolio 11.4 4.4

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 78,402 78,388

Median Mkt. Cap ($M) 12,427 1,393

Price/Earnings ratio 19.2 16.7

Price/Book ratio 3.0 2.5

5 Yr. EPS Growth Rate (%) 14.1 14.4

Current Yield (%) 1.9 2.5

Debt to Equity 1.7 1.0

Number of Stocks 960 8,511

Beta - 1.00

Consistency - -

Sharpe Ratio - -

Information Ratio - -

Up Market Capture - -

Down Market Capture - -

Sector Weights (%)

Total Equity Composite MSCI AC World IMI

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Other

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.0

2.0

1.6

1.8

4.2

17.1

10.6

13.9

15.9

7.7

11.4

13.6

0.0

0.0

3.2

3.5

6.1

13.4

11.4

11.0

21.6

8.9

8.9

12.0

Distribution of Market Capitalization (%)

Total Equity Composite MSCI AC World IMI

0.0

10.0

20.0

30.0

40.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

31.1 31.3

22.8

14.8

0.0

31.830.9

25.2

10.2

2.0

Equity Portfolio - CharacteristicsTotal Equity Composite vs. MSCI AC World IMIAs of September 30, 2014

21

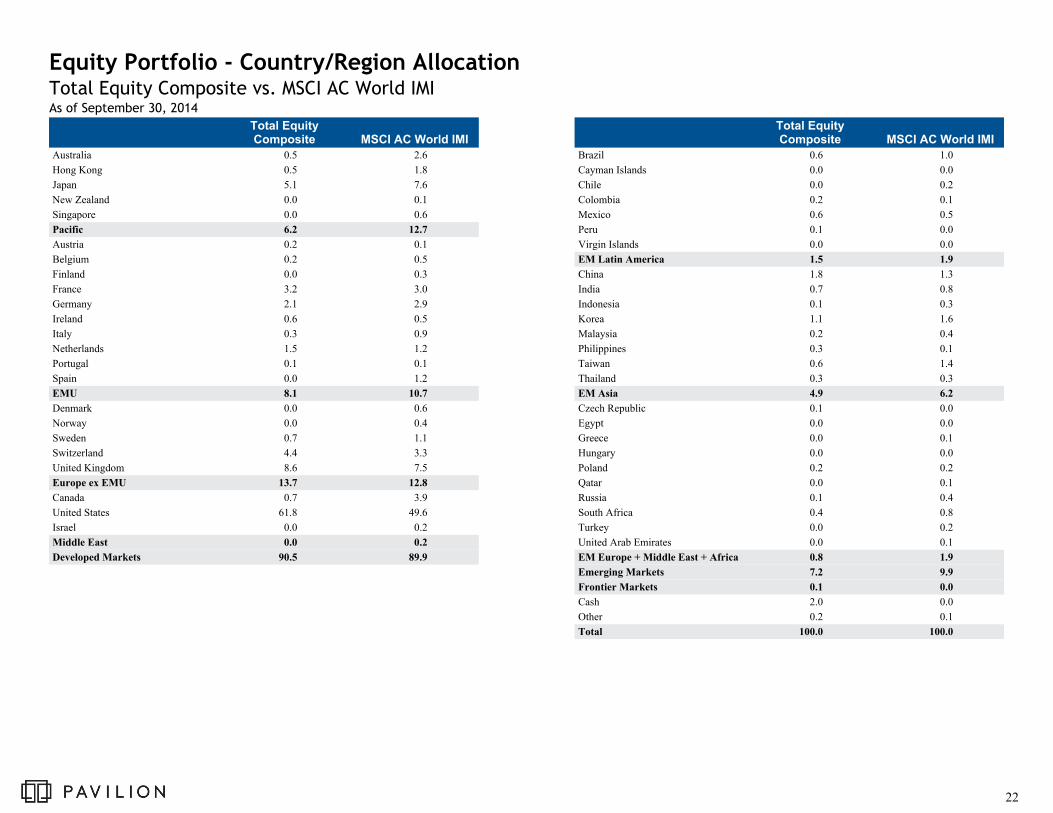

Total EquityComposite MSCI AC World IMI

Australia 0.5 2.6

Hong Kong 0.5 1.8

Japan 5.1 7.6

New Zealand 0.0 0.1

Singapore 0.0 0.6

Pacific 6.2 12.7

Austria 0.2 0.1

Belgium 0.2 0.5

Finland 0.0 0.3

France 3.2 3.0

Germany 2.1 2.9

Ireland 0.6 0.5

Italy 0.3 0.9

Netherlands 1.5 1.2

Portugal 0.1 0.1

Spain 0.0 1.2

EMU 8.1 10.7

Denmark 0.0 0.6

Norway 0.0 0.4

Sweden 0.7 1.1

Switzerland 4.4 3.3

United Kingdom 8.6 7.5

Europe ex EMU 13.7 12.8

Canada 0.7 3.9

United States 61.8 49.6

Israel 0.0 0.2

Middle East 0.0 0.2

Developed Markets 90.5 89.9

Total EquityComposite MSCI AC World IMI

Brazil 0.6 1.0

Cayman Islands 0.0 0.0

Chile 0.0 0.2

Colombia 0.2 0.1

Mexico 0.6 0.5

Peru 0.1 0.0

Virgin Islands 0.0 0.0

EM Latin America 1.5 1.9

China 1.8 1.3

India 0.7 0.8

Indonesia 0.1 0.3

Korea 1.1 1.6

Malaysia 0.2 0.4

Philippines 0.3 0.1

Taiwan 0.6 1.4

Thailand 0.3 0.3

EM Asia 4.9 6.2

Czech Republic 0.1 0.0

Egypt 0.0 0.0

Greece 0.0 0.1

Hungary 0.0 0.0

Poland 0.2 0.2

Qatar 0.0 0.1

Russia 0.1 0.4

South Africa 0.4 0.8

Turkey 0.0 0.2

United Arab Emirates 0.0 0.1

EM Europe + Middle East + Africa 0.8 1.9

Emerging Markets 7.2 9.9

Frontier Markets 0.1 0.0

Cash 2.0 0.0

Other 0.2 0.1

Total 100.0 100.0

Equity Portfolio - Country/Region AllocationTotal Equity Composite vs. MSCI AC World IMIAs of September 30, 2014

22

Portfolio Characteristics

Maturity Distribution (%)

Credit Quality Distribution (%)

Risk Characteristics - 3 Years

Sector Distribution (%)

Total Fixed Income Composite

Barclays Intermediate U.S. Government/Credit

0.0

25.0

50.0

75.0

100.0

AAA AA ABBB BB B

CCC NR

64.9

6.6

14.3 14.2

0.0 0.0 0.0 0.0

26.4

9.9

18.621.5

10.3 11.1

0.6 1.6

Portfolio Benchmark

Effective Duration 4.6 3.9

Avg. Maturity 7.4 4.2

Avg. Quality A+ AA

Yield To Maturity (%) 3.8 1.7

ConsistencySharpeRatio

InformationRatio

UpMarket

Capture

DownMarket

Capture

Total Fixed Income Composite 63.9 1.0 0.7 185.6

Barclays Intermediate U.S. Government/Credit 0.0 1.0 N/A 100.0

90 Day U.S. Treasury Bill 38.9 N/A -1.0 1.0

Total Fixed Income Composite

Barclays Intermediate U.S. Government/Credit

0.0

25.0

50.0

75.0

100.0

Treasu

ries

TIPS

Agenc

ies

Credi

t

Hig

h Yie

ldM

BSABS

Non-U

S

Emer

ging

Munic

ipal

s

Cas

h

Oth

er

CMBS

56.4

0.06.0

24.5

0.0 0.0 0.0

10.6

2.4 0.0 0.0 0.0 0.0

24.6

0.0 0.3

17.9 15.4

2.7 3.3

14.8

3.8 1.2 4.0 5.8 6.2

Total Fixed Income Composite

Barclays Intermediate U.S. Government/Credit

0.0

15.0

30.0

45.0

60.0

< 1 Yr

1 < 3 Yrs

3 < 5 Yrs

5 <

10 Yrs

10 <

20 Yrs

> 20

Yrs

0.0

41.7

26.4

31.9

0.0 0.03.9

22.420.3

39.5

6.5 7.4

Fixed Income Portfolio - CharacteristicsTotal Fixed Income Composite vs. Barclays Intermediate U.S. Government/CreditAs of September 30, 2014

23

Manager Evaluation

24

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Vanguard Windsor II -0.2 7.4 17.7 22.8 14.8 8.0 30.8 16.8 2.8 10.7 27.2 -36.6 2.3 18.4 7.2 18.4

Russell 1000 Value Index -0.2 8.1 18.9 23.9 15.3 7.8 32.5 17.5 0.4 15.5 19.7 -36.8 -0.2 22.2 7.1 16.5

Large-Cap Value Equity Peer Group Median -0.3 6.1 16.2 21.8 14.0 7.5 31.7 15.0 -1.5 13.5 25.4 -37.3 2.9 16.6 6.1 12.5

Vanguard Windsor II Rank 47 26 34 36 33 39 61 28 17 86 41 44 55 35 36 6

14.0

14.5

15.0

15.5

16.0

Re

turn

(%)

14.5 14.6 14.7Risk (Standard Deviation %)

Russell 1000 Value Index

Vanguard Windsor II

Vanguard Windsor II Russell 1000 Value Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 8.0 16.0-8.0-16.0

UtilitiesTelecommunication Services

OtherMaterials

Information TechnologyIndustrials

Health CareFinancials

EnergyConsumer Staples

Consumer DiscretionaryCash

-1.90.40.3

-1.81.7

-1.24.3

-8.0-1.6

3.11.82.9

Allocation(Total: 0.4)

0.0 0.2 0.4-0.2-0.4

0.10.00.00.0

0.10.0

0.1-0.2

0.10.1

0.00.0

Stock(Total: -0.1)

0.0 0.4 0.8-0.4-0.8

-0.10.00.00.00.0

0.40.3

-0.1-0.3-0.3

-0.20.0

Vanguard Windsor II

0.0 0.3 0.6 0.9-0.3-0.6

0.00.0

0.00.1

0.10.40.4

-0.2-0.2-0.2

-0.20.0

Manager EvaluationVanguard Windsor II vs. Russell 1000 Value IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

25

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Microsoft Corp 3.0 1.4 1.7 11.9

JPMorgan Chase & Co 2.7 2.3 0.4 5.3

Pfizer Inc 2.6 1.9 0.7 0.5

Intel Corp 2.6 1.6 1.0 13.5

Wells Fargo & Co 2.5 2.5 0.0 -0.6

Johnson & Johnson 2.3 2.6 -0.3 2.6

Medtronic Inc 2.3 0.6 1.6 -2.4

Citigroup Inc 2.3 1.6 0.7 10.0

WellPoint Inc 2.2 0.3 1.9 11.6

Philip Morris International Inc 2.2 0.6 1.6 0.1

% of Portfolio 24.6 15.3

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 109,816 112,109

Median Mkt. Cap ($M) 22,184 6,878

Price/Earnings ratio 15.7 16.5

Price/Book ratio 2.2 2.0

5 Yr. EPS Growth Rate (%) 16.0 11.2

Current Yield (%) 2.7 2.4

Debt to Equity 1.2 0.9

Number of Stocks 258 690

Beta (5 Years, Monthly) 0.97 1.00

Consistency (5 Years, Monthly) 43.33 1.00

Sharpe Ratio (5 Years, Monthly) 1.10 1.11

Information Ratio (5 Years, Monthly) -0.20 -

Up Market Capture (5 Years, Monthly) 96.40 -

Down Market Capture (5 Years, Monthly) 95.70 -

Sector Weights (%)

Vanguard Windsor II Russell 1000 Value Index

0.0 8.0 16.0 24.0 32.0 40.0

Other

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.3

2.3

3.8

2.7

1.6

13.3

8.5

17.3

21.4

10.6

9.4

8.9

0.0

0.0

6.0

2.3

3.3

9.4

10.2

13.5

29.2

12.9

7.1

6.2

Distribution of Market Capitalization (%)

Vanguard Windsor II Russell 1000 Value Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

42.4

31.3

20.1

6.2

0.0

45.4

35.1

15.6

1.7 2.3

Manager EvaluationVanguard Windsor II vs. Russell 1000 Value IndexAs of September 30, 2014

*Portfolio characteristics as of 12/31/2013.

26

Historical Performance

Three Year Rolling Percentile Ranking Relative Performance

Historical Statistics (Oct-2009 - Sep-2014)

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Vanguard Institutional Index 1.1 8.3 19.7 23.0 15.7 8.1 32.3 16.0 2.1 15.0 26.6 -37.0 5.5 15.8 4.9 10.9

S&P 500 Index 1.1 8.3 19.7 23.0 15.7 8.1 32.4 16.0 2.1 15.1 26.5 -37.0 5.5 15.8 4.9 10.9

Large-Cap Equity Peer Group Median 0.1 6.0 16.4 21.5 14.3 7.8 32.4 14.6 -1.0 14.0 27.8 -37.5 6.2 13.3 5.9 10.2

Vanguard Institutional Index Rank 25 15 17 30 24 42 51 36 22 38 56 45 55 32 62 44

Cumulative Annualized Over/Under Relative Performance

Over/Under Performance

0.0

0.1

0.2

-0.1

-0.2

Re

turn

(%)

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Vanguard Institutional Index S&P 500 Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

ReturnStandardDeviation

ExcessReturn Alpha Beta

SharpeRatio

TrackingError

InformationRatio

DownsideRisk Consistency

InceptionDate

Vanguard Institutional Index 15.7 14.1 15.8 0.0 1.0 1.1 0.0 -1.3 8.1 15.0 15y

S&P 500 Index 15.7 14.1 15.8 0.0 1.0 1.1 0.0 N/A 8.1 0.0 15y

90 Day U.S. Treasury Bill 0.1 0.0 0.0 0.1 0.0 N/A 14.1 -1.1 0.0 20.0 15y

Manager EvaluationVanguard Institutional Index vs. S&P 500 IndexAs of September 30, 2014

27

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Apple Inc 3.4 3.4 0.0 9.0

Exxon Mobil Corp 2.3 2.3 0.0 -5.9

Microsoft Corp 2.2 2.2 0.0 11.9

Johnson & Johnson 1.7 1.7 0.0 2.6

General Electric Co 1.5 1.5 0.0 -1.7

Wells Fargo & Co 1.4 1.4 0.0 -0.6

Berkshire Hathaway Inc 1.3 1.4 -0.1 9.1

Procter & Gamble Co (The) 1.3 1.3 0.0 7.4

JPMorgan Chase & Co 1.3 1.3 0.0 5.3

Chevron Corp 1.3 1.3 0.0 -7.8

% of Portfolio 17.7 17.8

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 129,536 129,536

Median Mkt. Cap ($M) 17,195 17,148

Price/Earnings ratio 18.6 18.6

Price/Book ratio 2.9 2.9

5 Yr. EPS Growth Rate (%) 14.6 14.5

Current Yield (%) 2.0 2.0

Debt to Equity 1.2 1.2

Number of Stocks 504 502

Beta (5 Years, Monthly) 1.00 1.00

Consistency (5 Years, Monthly) 28.33 1.00

Sharpe Ratio (5 Years, Monthly) 1.18 1.18

Information Ratio (5 Years, Monthly) -1.11 -

Up Market Capture (5 Years, Monthly) 99.95 -

Down Market Capture (5 Years, Monthly) 100.05 -

Sector Weights (%)

Vanguard Institutional Index S&P 500 Index

0.0 5.0 10.0 15.0 20.0 25.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

3.0

2.4

3.5

19.7

10.3

13.9

16.3

9.7

9.5

11.7

3.0

2.4

3.5

19.7

10.3

13.9

16.3

9.7

9.5

11.7

Distribution of Market Capitalization (%)

Vanguard Institutional Index S&P 500 Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

48.7

34.7

16.1

0.5

48.7

34.7

16.1

0.5

Manager EvaluationVanguard Institutional Index vs. S&P 500 IndexAs of September 30, 2014

28

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

T. Rowe Price LCC Growth 1.8 4.8 18.2 24.6 17.4 9.0 41.4 18.5 1.5 16.4 43.0 -42.6 13.0 9.1 4.0 7.3

Russell 1000 Growth Index 1.5 7.9 19.1 22.4 16.5 8.9 33.5 15.3 2.6 16.7 37.2 -38.4 11.8 9.1 5.3 6.3

Large-Cap Growth Peer Group Median 1.1 5.5 16.7 21.5 15.1 8.5 34.6 14.6 -0.8 15.3 33.4 -38.3 13.8 7.1 6.2 7.7

T. Rowe Price LCC Growth Rank 29 62 33 11 15 40 12 16 27 39 14 78 55 33 69 56

15.3

16.2

17.1

18.0

18.9

Re

turn

(%)

13.5 14.0 14.5 15.0 15.5 16.0 16.5 17.0Risk (Standard Deviation %)

Russell 1000 Growth Index

T. Rowe Price LCC Growth

T. Rowe Price LCC Growth Russell 1000 Growth Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 15.0 30.0-15.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-0.1

-1.9-0.4

-6.3

2.3

4.82.3

-1.2

-8.4

8.30.6

Allocation(Total: 0.1)

0.0 0.3 0.6-0.3-0.6

0.0

0.00.0

-0.2

-0.1

0.3-0.1

0.1

0.1

-0.10.0

Stock(Total: 0.2)

0.0 0.5 1.0-0.5-1.0

0.0

0.00.1

-0.1

0.0

0.50.4

-0.3

0.1

-0.40.0

T. Rowe Price LCC Growth

0.0 0.5 1.0 1.5-0.5-1.0

0.0

-0.10.1

-0.2

-0.1

0.80.3

-0.1

0.1

-0.40.0

Manager EvaluationT. Rowe Price Large-Cap Core Growth vs. Russell 1000 Growth IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

29

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Amazon.com Inc 4.3 1.2 3.1 -0.7

Gilead Sciences Inc 4.0 1.6 2.4 28.4

Priceline.Com Inc 3.1 0.6 2.6 -3.7

Google Inc (Class C) 2.8 1.6 1.2 0.4

Google Inc 2.8 1.6 1.2 0.6

McKesson Corp 2.7 0.4 2.3 4.7

Biogen Idec Inc 2.6 0.8 1.8 4.9

Facebook Inc 2.5 1.5 1.0 17.5

Baidu Inc 2.4 0.0 2.4 16.8

Danaher Corp 2.4 0.1 2.2 -3.4

% of Portfolio 29.5 9.4

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 83,008 116,514

Median Mkt. Cap ($M) 26,144 8,528

Price/Earnings ratio 28.8 21.9

Price/Book ratio 5.3 4.9

5 Yr. EPS Growth Rate (%) 21.2 17.8

Current Yield (%) 0.6 1.5

Debt to Equity 6.2 1.4

Number of Stocks 137 674

Beta (5 Years, Monthly) 1.11 1.00

Consistency (5 Years, Monthly) 55.00 1.00

Sharpe Ratio (5 Years, Monthly) 1.12 1.20

Information Ratio (5 Years, Monthly) 0.29 -

Up Market Capture (5 Years, Monthly) 108.54 -

Down Market Capture (5 Years, Monthly) 111.19 -

Sector Weights (%)

T. Rowe Price Large-Cap Core Growth

Russell 1000 Growth Index

0.0 8.0 16.0 24.0 32.0 40.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

1.4

0.0

0.4

3.6

22.2

13.0

21.2

7.4

3.8

2.1

24.9

0.0

0.1

2.4

4.2

28.4

11.9

13.6

5.1

5.7

10.3

18.2

Distribution of Market Capitalization (%)

T. Rowe Price Large-Cap Core Growth

Russell 1000 Growth Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

43.0

31.4

21.3

4.2

0.0

34.7

44.4

19.6

0.01.4

Manager EvaluationT. Rowe Price Large-Cap Core Growth vs. Russell 1000 Growth IndexAs of September 30, 2014

30

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

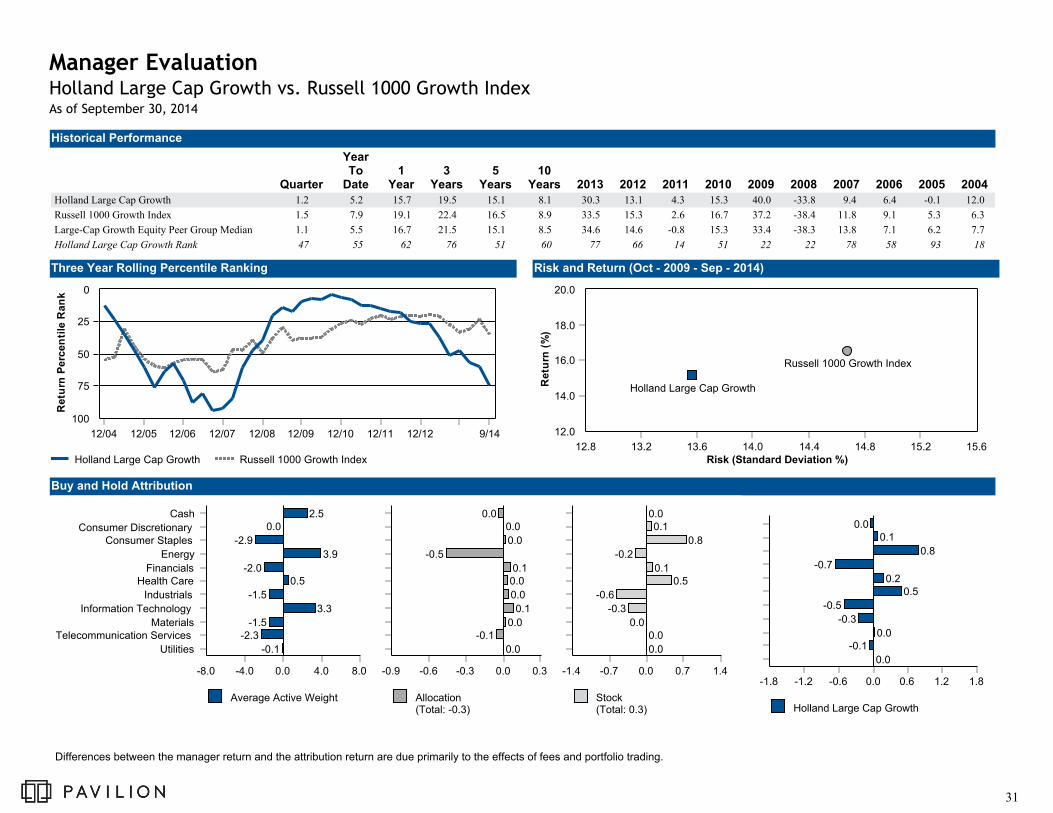

Holland Large Cap Growth 1.2 5.2 15.7 19.5 15.1 8.1 30.3 13.1 4.3 15.3 40.0 -33.8 9.4 6.4 -0.1 12.0

Russell 1000 Growth Index 1.5 7.9 19.1 22.4 16.5 8.9 33.5 15.3 2.6 16.7 37.2 -38.4 11.8 9.1 5.3 6.3

Large-Cap Growth Equity Peer Group Median 1.1 5.5 16.7 21.5 15.1 8.5 34.6 14.6 -0.8 15.3 33.4 -38.3 13.8 7.1 6.2 7.7

Holland Large Cap Growth Rank 47 55 62 76 51 60 77 66 14 51 22 22 78 58 93 18

12.0

14.0

16.0

18.0

20.0

Re

turn

(%)

12.8 13.2 13.6 14.0 14.4 14.8 15.2 15.6Risk (Standard Deviation %)

Russell 1000 Growth Index

Holland Large Cap Growth

Holland Large Cap Growth Russell 1000 Growth Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 4.0 8.0-4.0-8.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-0.1

-2.3-1.5

3.3

-1.5

0.5-2.0

3.9

-2.9

0.02.5

Allocation(Total: -0.3)

0.0 0.3-0.3-0.6-0.9

0.0

-0.10.0

0.1

0.0

0.00.1

-0.5

0.0

0.00.0

Stock(Total: 0.3)

0.0 0.7 1.4-0.7-1.4

0.0

0.00.0

-0.3

-0.6

0.50.1

-0.2

0.8

0.10.0

Holland Large Cap Growth

0.0 0.6 1.2 1.8-0.6-1.2-1.8

0.0

-0.10.0

-0.3

-0.5

0.50.2

-0.7

0.8

0.10.0

Manager EvaluationHolland Large Cap Growth vs. Russell 1000 Growth IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

31

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Qualcomm Inc. 4.3 1.2 3.1 -5.1

Google Inc (Class C) 4.0 1.6 2.4 0.4

Visa Inc 3.9 1.1 2.9 1.5

Citrix Systems Inc. 3.8 0.1 3.7 14.1

Gilead Sciences Inc 3.7 1.6 2.1 28.4

Apple Inc 3.6 5.9 -2.3 9.0

Priceline.Com Inc 3.5 0.6 2.9 -3.7

Amazon.com Inc 3.4 1.2 2.2 -0.7

Adobe Systems Inc 3.3 0.3 2.9 -4.4

Range Resources Corp. 3.1 0.1 3.0 -22.0

% of Portfolio 36.4 13.7

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 94,418 116,514

Median Mkt. Cap ($M) 38,377 8,528

Price/Earnings ratio 24.5 21.9

Price/Book ratio 4.7 4.9

5 Yr. EPS Growth Rate (%) 16.1 17.8

Current Yield (%) 1.0 1.5

Debt to Equity 0.6 1.4

Number of Stocks 49 674

Beta (5 Years, Monthly) 0.94 1.00

Consistency (5 Years, Monthly) 48.33 1.00

Sharpe Ratio (5 Years, Monthly) 1.14 1.20

Information Ratio (5 Years, Monthly) -0.43 -

Up Market Capture (5 Years, Monthly) 93.80 -

Down Market Capture (5 Years, Monthly) 95.85 -

Sector Weights (%)

Holland Capital Management Russell 1000 Growth Index

0.0 8.0 16.0 24.0 32.0 40.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

2.9

0.0

0.0

3.1

31.0

10.4

12.9

3.7

8.7

8.8

18.5

0.0

0.1

2.4

4.2

28.4

11.9

13.6

5.1

5.7

10.3

18.2

Distribution of Market Capitalization (%)

Holland Capital Management Russell 1000 Growth Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

43.0

31.4

21.3

4.2

0.0

34.531.7

27.8

3.1 2.9

Manager EvaluationHolland Capital Management vs. Russell 1000 Growth IndexAs of September 30, 2014

32

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

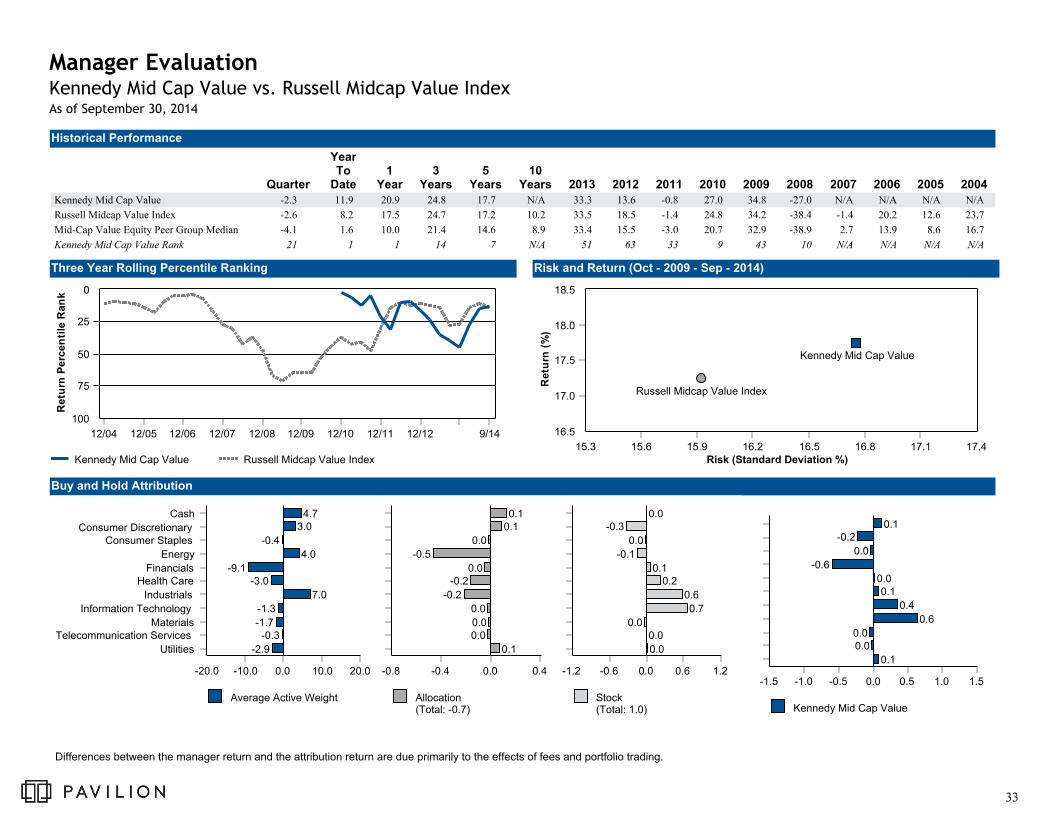

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Kennedy Mid Cap Value -2.3 11.9 20.9 24.8 17.7 N/A 33.3 13.6 -0.8 27.0 34.8 -27.0 N/A N/A N/A N/A

Russell Midcap Value Index -2.6 8.2 17.5 24.7 17.2 10.2 33.5 18.5 -1.4 24.8 34.2 -38.4 -1.4 20.2 12.6 23.7

Mid-Cap Value Equity Peer Group Median -4.1 1.6 10.0 21.4 14.6 8.9 33.4 15.5 -3.0 20.7 32.9 -38.9 2.7 13.9 8.6 16.7

Kennedy Mid Cap Value Rank 21 1 1 14 7 N/A 51 63 33 9 43 10 N/A N/A N/A N/A

16.5

17.0

17.5

18.0

18.5

Re

turn

(%)

15.3 15.6 15.9 16.2 16.5 16.8 17.1 17.4Risk (Standard Deviation %)

Russell Midcap Value Index

Kennedy Mid Cap Value

Kennedy Mid Cap Value Russell Midcap Value Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 10.0 20.0-10.0-20.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-2.9

-0.3-1.7

-1.3

7.0

-3.0-9.1

4.0

-0.4

3.04.7

Allocation(Total: -0.7)

0.0 0.4-0.4-0.8

0.1

0.00.0

0.0

-0.2

-0.20.0

-0.5

0.0

0.10.1

Stock(Total: 1.0)

0.0 0.6 1.2-0.6-1.2

0.0

0.00.0

0.7

0.6

0.20.1

-0.1

0.0

-0.30.0

Kennedy Mid Cap Value

0.0 0.5 1.0 1.5-0.5-1.0-1.5

0.1

0.00.0

0.6

0.4

0.10.0

-0.6

0.0

-0.20.1

Manager EvaluationKennedy Mid Cap Value vs. Russell Midcap Value IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

33

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Hospira Inc 2.5 0.3 2.2 1.3

Cadence Design Systems Inc 2.3 0.0 2.3 -1.6

Trinity Industries Inc. 2.3 0.1 2.2 7.1

Foot Locker Inc. 2.3 0.2 2.0 10.2

Reinsurance Group of America Inc. 2.2 0.1 2.1 2.0

Community Health Systems Inc 2.2 0.2 2.0 20.8

NetApp Inc 2.2 0.3 1.8 18.2

Helmerich & Payne Inc. 2.1 0.1 2.0 -15.1

Lincoln National Corp 2.1 0.5 1.6 4.5

UGI Corp 2.1 0.2 1.9 1.9

% of Portfolio 22.3 2.0

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 8,272 11,123

Median Mkt. Cap ($M) 6,684 5,613

Price/Earnings ratio 18.6 18.5

Price/Book ratio 2.2 1.9

5 Yr. EPS Growth Rate (%) 13.0 11.2

Current Yield (%) 1.7 2.2

Debt to Equity 0.5 0.9

Number of Stocks 57 566

Beta (5 Years, Monthly) 1.02 1.00

Consistency (5 Years, Monthly) 58.33 1.00

Sharpe Ratio (5 Years, Monthly) 1.14 1.14

Information Ratio (5 Years, Monthly) 0.16 -

Up Market Capture (5 Years, Monthly) 101.16 -

Down Market Capture (5 Years, Monthly) 98.85 -

Sector Weights (%)

Kennedy Capital Management Russell Midcap Value Index

0.0 8.0 16.0 24.0 32.0 40.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

3.5

8.7

0.0

3.8

12.8

15.6

6.1

23.8

8.0

2.0

15.8

0.0

11.9

0.3

7.1

10.8

9.5

9.3

32.2

5.4

3.4

10.0

Distribution of Market Capitalization (%)

Kennedy Capital Management Russell Midcap Value Index

0.0

25.0

50.0

75.0

100.0

$20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

12.1

67.3

20.6

0.01.6

67.9

27.0

3.5

Manager EvaluationKennedy Capital Management vs. Russell Midcap Value IndexAs of September 30, 2014

34

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

TimesSquare Small Cap Growth -5.7 -11.1 -2.9 20.0 15.9 11.6 47.7 13.1 2.6 27.3 35.7 -32.3 10.0 16.5 13.4 11.1

Russell 2000 Growth Index -6.1 -4.0 3.8 21.9 15.5 9.0 43.3 14.6 -2.9 29.1 34.5 -38.5 7.0 13.3 4.2 14.3

Small-Cap Growth Equity Peer Group Median -5.8 -5.5 1.9 20.1 14.7 8.0 44.7 12.7 -2.7 27.7 34.5 -40.6 9.9 9.9 5.8 11.3

TimesSquare Small Cap Growth Rank 46 89 88 52 28 6 31 47 14 53 46 11 49 14 10 53

14.8

15.2

15.6

16.0

16.4

16.8

Re

turn

(%)

17.8 18.0 18.2 18.4 18.6 18.8 19.0 19.2Risk (Standard Deviation %)

Russell 2000 Growth Index

TimesSquare Small Cap Growth

TimesSquare Small Cap Growth Russell 2000 Growth Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 15.0 30.0-15.0-30.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-0.2

-0.7-3.7

6.6

9.2

-10.1-0.1

-0.5

-0.1

-3.93.5

Allocation(Total: -0.1)

0.0 0.4 0.8-0.4-0.8

0.0

0.00.0

0.1

-0.2

-0.30.0

0.1

0.0

0.10.2

Stock(Total: 0.3)

0.0 0.5 1.0 1.5-0.5-1.0

0.0

0.0-0.2

0.7

-0.1

0.5-0.2

-0.2

0.1

-0.20.0

TimesSquare Small Cap Growth

0.0 0.4 0.8 1.2-0.4-0.8

0.0

0.0-0.1

0.8

-0.3

0.2-0.2

-0.2

0.1

-0.10.2

Manager EvaluationTimesSquare Small Cap Growth vs. Russell 2000 Growth IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

35

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Solera Holdings Inc 2.1 0.0 2.1 -15.8

Albany International Corp. 1.9 0.0 1.9 -9.9

WEX Inc 1.9 0.5 1.4 5.1

On Assignment Inc 1.9 0.2 1.7 -24.5

Ultimate Software Group Inc 1.9 0.5 1.4 2.4

Air Methods Corp 1.8 0.3 1.5 7.5

j2 Global Inc 1.7 0.3 1.4 -2.4

Henry (Jack) & Associates Inc. 1.6 0.0 1.6 -6.0

CoStar Group Inc 1.6 0.0 1.6 -1.7

Team Health Holdings Inc 1.6 0.5 1.1 16.1

% of Portfolio 18.0 2.3

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 2,093 1,847

Median Mkt. Cap ($M) 1,577 785

Price/Earnings ratio 25.1 24.2

Price/Book ratio 3.4 3.7

5 Yr. EPS Growth Rate (%) 13.7 17.4

Current Yield (%) 0.5 0.6

Debt to Equity 0.5 -5.5

Number of Stocks 107 1,151

Beta (5 Years, Monthly) 0.85 1.00

Consistency (5 Years, Monthly) 53.33 1.00

Sharpe Ratio (5 Years, Monthly) 0.97 0.86

Information Ratio (5 Years, Monthly) -0.01 -

Up Market Capture (5 Years, Monthly) 87.44 -

Down Market Capture (5 Years, Monthly) 77.39 -

Sector Weights (%)

TimesSquare Small Cap Growth Russell 2000 Growth Index

0.0 8.0 16.0 24.0 32.0 40.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

1.0

0.0

0.9

1.6

32.4

24.6

12.7

7.2

3.9

3.8

11.9

0.0

0.2

0.8

5.4

25.9

14.7

21.7

7.6

4.7

3.9

15.2

Distribution of Market Capitalization (%)

TimesSquare Small Cap Growth Russell 2000 Growth Index

0.0

50.0

100.0

150.0

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

0.7

99.3

0.03.6

95.5

1.0

Manager EvaluationTimesSquare Small Cap Growth vs. Russell 2000 Growth IndexAs of September 30, 2014

36

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Morgan Stanley International Equity -5.0 -0.8 4.7 14.5 7.4 6.5 20.4 19.6 -7.6 6.1 21.6 -33.1 9.8 22.5 6.5 20.0

MSCI EAFE Index -5.9 -1.4 4.3 13.6 6.6 6.3 22.8 17.3 -12.1 7.8 31.8 -43.4 11.2 26.3 13.5 20.2

International Equity Peer Group Median -5.8 -1.7 4.3 13.6 6.8 6.6 20.8 18.4 -13.7 11.6 33.5 -44.4 11.9 25.2 15.0 18.5

Morgan Stanley International Equity Rank 27 36 43 33 38 55 54 35 10 88 92 1 66 76 100 38

5.6

6.4

7.2

8.0

8.8

Re

turn

(%)

13.2 13.8 14.4 15.0 15.6 16.2 16.8 17.4Risk (Standard Deviation %)

MSCI EAFE Index

Morgan Stanley International Equity

Morgan Stanley International Equity MSCI EAFE Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 15.0 30.0-15.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-3.9

-3.30.7

2.2

-5.6

3.7-7.1

0.8

13.6

-3.22.1

Allocation(Total: 0.3)

0.0 0.2 0.4-0.2-0.4

0.0

0.00.0

0.1

0.1

0.2-0.1

0.0

-0.2

0.10.1

Stock(Total: 0.6)

0.0 0.5 1.0-0.5-1.0

0.0

0.1-0.2

0.1

0.1

0.10.0

0.1

0.5

-0.10.0

Morgan Stanley International Equity

0.0 0.3 0.6 0.9-0.3-0.6

0.0

0.0-0.3

0.2

0.1

0.3-0.1

0.1

0.4

0.00.1

Manager EvaluationMorgan Stanley International Equity vs. MSCI EAFE IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

37

Total Attribution

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8-0.1-0.2-0.3-0.4-0.5

Pacific

Other

North America

Middle East

Europe ex EMU

EMU

EM Asia

Cash

-0.2

0.0

-0.1

0.0

0.5

0.5

0.0

0.1

Performance Attribution

Average Active Weight

0.0 10.0 20.0-10.0-20.0

Pacific

Other

North America

Middle East

Europe ex EMU

EMU

EM Asia

Cash

-10.3

-0.3

1.5

-0.5

11.9

-5.6

1.4

2.1

Allocation(Total: 0.0)

0.0 0.2 0.4-0.2-0.4-0.6

-0.2

0.0

-0.1

0.0

0.0

0.2

0.0

0.1

Stock(Total: 0.9)

0.0 0.2 0.4 0.6 0.8

0.1

0.0

0.0

0.0

0.5

0.3

0.0

0.0

Manager EvaluationMorgan Stanley International Equity vs. MSCI EAFE Index1 Quarter Ending September 30, 2014

38

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

British American Tobacco PLC 4.7 0.8 3.9 -3.8

Reckitt Benckiser Group PLC 4.6 0.4 4.2 0.6

Nestle SA, Cham Und Vevey 4.5 1.8 2.7 -5.1

Sanofi 4.4 1.0 3.4 6.5

Unilever NV 4.4 0.5 3.9 -8.1

Novartis AG 3.6 1.7 1.9 4.2

Roche Holding AG 3.2 1.6 1.5 -0.7

Diageo PLC 2.8 0.6 2.2 -7.6

SAP AG Systeme Anwendungen 2.5 0.5 1.9 -6.6

Toyota Motor Corp 2.4 1.3 1.2 -0.9

% of Portfolio 37.0 10.3

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 79,836 64,782

Median Mkt. Cap ($M) 30,670 8,932

Price/Earnings ratio 17.5 15.5

Price/Book ratio 2.7 2.1

5 Yr. EPS Growth Rate (%) 7.1 13.5

Current Yield (%) 3.0 3.3

Debt to Equity 1.2 1.2

Number of Stocks 71 901

Beta (5 Years, Monthly) 0.89 1.00

Consistency (5 Years, Monthly) 48.33 1.00

Sharpe Ratio (5 Years, Monthly) 0.55 0.46

Information Ratio (5 Years, Monthly) 0.17 -

Up Market Capture (5 Years, Monthly) 93.77 -

Down Market Capture (5 Years, Monthly) 88.19 -

Sector Weights (%)

Morgan Stanley International Equity MSCI EAFE Index

0.0 6.0 12.0 18.0 24.0 30.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

2.4

0.0

1.6

7.7

7.0

6.9

14.7

18.5

7.6

24.4

9.1

0.0

3.9

4.9

7.7

4.7

12.5

11.2

25.7

6.9

10.9

11.6

Distribution of Market Capitalization (%)

Morgan Stanley International Equity MSCI EAFE Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

28.5

40.8

26.3

4.4

0.0

36.1 36.8

23.7

1.02.4

Manager EvaluationMorgan Stanley International Equity vs. MSCI EAFE IndexAs of September 30, 2014

39

Morgan StanleyInternational Equity MSCI EAFE Index

Australia 2.0 7.5

Hong Kong 0.6 2.9

Japan 18.9 21.0

New Zealand 0.0 0.1

Singapore 0.0 1.5

Pacific 21.5 33.1

Austria 0.0 0.2

Belgium 0.0 1.3

Finland 0.0 0.9

France 10.5 9.4

Germany 7.9 8.7

Ireland 0.9 0.3

Italy 1.0 2.4

Netherlands 5.3 3.0

Portugal 0.0 0.2

Spain 0.0 3.6

EMU 25.6 30.0

Denmark 0.0 1.6

Norway 0.0 0.8

Sweden 2.4 3.1

Switzerland 15.7 9.2

United Kingdom 29.8 21.4

Europe ex EMU 47.9 36.1

Canada 1.4 0.0

United States 0.0 0.0

Israel 0.0 0.6

Middle East 0.0 0.6

Developed Markets 96.3 99.7

Morgan StanleyInternational Equity MSCI EAFE Index

Brazil 0.0 0.0

Cayman Islands 0.0 0.0

Chile 0.0 0.0

Colombia 0.0 0.0

Mexico 0.0 0.0

Peru 0.0 0.0

Virgin Islands 0.0 0.0

EM Latin America 0.0 0.0

China 1.3 0.0

India 0.0 0.0

Indonesia 0.0 0.0

Korea 0.0 0.0

Malaysia 0.0 0.0

Philippines 0.0 0.0

Taiwan 0.0 0.0

Thailand 0.0 0.0

EM Asia 1.3 0.0

Czech Republic 0.0 0.0

Egypt 0.0 0.0

Greece 0.0 0.0

Hungary 0.0 0.0

Poland 0.0 0.0

Qatar 0.0 0.0

Russia 0.0 0.0

South Africa 0.0 0.0

Turkey 0.0 0.0

United Arab Emirates 0.0 0.0

EM Europe + Middle East + Africa 0.0 0.0

Emerging Markets 1.3 0.0

Frontier Markets 0.0 0.0

Cash 2.4 0.0

Other 0.0 0.3

Total 100.0 100.0

Manager EvaluationMorgan Stanley International Equity vs. MSCI EAFE IndexAs of September 30, 2014

40

Historical Performance

Buy and Hold Attribution

Risk and Return (Oct - 2009 - Sep - 2014)Three Year Rolling Percentile Ranking

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Morgan Stanley Emerging Markets -3.5 1.9 3.7 7.7 4.8 10.4 -0.8 20.2 -18.4 18.5 69.5 -56.4 41.6 38.0 34.5 24.1

MSCI Emerging Markets Index -3.5 2.4 4.3 7.2 4.4 10.7 -2.6 18.2 -18.4 18.9 78.5 -53.3 39.4 32.2 34.0 25.6

Emerging Markets Equity Peer Group Median -3.7 2.2 4.4 8.1 4.5 10.0 -1.1 19.5 -19.2 19.2 74.0 -54.5 37.4 32.3 32.9 24.9

Morgan Stanley Emerging Markets Rank 44 57 61 59 45 42 47 39 41 55 69 71 25 16 41 60

3.6

4.0

4.4

4.8

5.2

5.6

Re

turn

(%)

15.0 15.5 16.0 16.5 17.0 17.5 18.0 18.5Risk (Standard Deviation %)

MSCI Emerging Markets Index

Morgan Stanley Emerging Markets

Morgan Stanley Emerging Markets MSCI Emerging Markets Index

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

Average Active Weight

0.0 4.0 8.0-4.0-8.0-12.0

Utilities

Telecommunication ServicesMaterials

Information Technology

Industrials

Health CareFinancials

Energy

Consumer StaplesConsumer Discretionary

Cash

-3.5

2.0-5.1

0.4

1.5

2.00.9

-4.4

1.3

2.52.3

Allocation(Total: 0.9)

0.0 0.2 0.4-0.2-0.4

0.0

0.20.2

0.0

0.0

0.30.0

0.2

0.0

-0.10.1

Stock(Total: -0.8)

0.0 0.5 1.0-0.5-1.0

0.0

-0.50.2

-0.6

0.2

-0.2-0.3

0.4

0.0

0.20.0

Morgan Stanley Emerging Markets

0.0 0.5 1.0 1.5-0.5-1.0-1.5

0.0

-0.40.4

-0.6

0.2

0.1-0.3

0.5

0.0

0.10.1

Manager EvaluationMorgan Stanley Emerging Markets vs. MSCI Emerging Markets IndexAs of September 30, 2014

Differences between the manager return and the attribution return are due primarily to the effects of fees and portfolio trading.

41

Total Attribution

0.0 0.3 0.6 0.9 1.2 1.5 1.8 2.1-0.3-0.6-0.9-1.2-1.5-1.8-2.1

Pacific

Other

North America

Frontier Markets

Europe ex EMU

EMU

EM Latin America

EM Europe + Middle East + Africa

EM Asia

Cash

-0.1

-0.1

-0.1

0.2

-0.1

-1.0

0.8

0.2

0.4

0.1

Performance Attribution

Average Active Weight

0.0 5.0 10.0 15.0-5.0-10.0-15.0

Pacific

Other

North America

Frontier Markets

Europe ex EMU

EMU

EM Latin America

EM Europe + Middle East + Africa

EM Asia

Cash

-2.4

1.7

1.3

1.3

2.0

5.3

-0.1

-6.4

-5.0

2.3

Allocation(Total: -0.9)

0.0 0.5 1.0-0.5-1.0-1.5-2.0

-0.2

-0.1

0.0

0.2

-0.1

-1.0

0.0

0.3

-0.1

0.1

Stock(Total: 1.1)

0.0 0.4 0.8 1.2 1.6-0.4-0.8

0.1

0.0

-0.2

0.0

0.0

0.0

0.8

-0.1

0.5

0.0

Manager EvaluationMorgan Stanley Emerging Markets vs. MSCI Emerging Markets Index1 Quarter Ending September 30, 2014

42

Top Ten Equity Holdings

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)

Tencent Holdings LTD 2.5 1.9 0.5 -2.5

Taiwan Semiconductor Manufacturing 2.3 2.5 -0.2 -4.7

BRF - Brasil Foods S.A. 2.2 0.4 1.9 -1.1

Bank of China Ltd 2.2 0.9 1.3 0.1

Samsung Electronics Co Ltd 1.8 3.1 -1.3 -14.3

Cemex SAB de CV 1.6 0.4 1.2 -1.4

America Movil SA De CV, Mexico 1.6 1.1 0.5 22.4

Alfa SAB De CV 1.5 0.3 1.3 23.6

Naspers Ltd 1.5 1.1 0.4 -6.1

China Mobile Ltd 1.5 1.8 -0.3 21.0

% of Portfolio 18.7 13.5

Portfolio Characteristics

Portfolio Benchmark

Wtd. Avg. Mkt. Cap ($M) 31,729 38,575

Median Mkt. Cap ($M) 9,106 5,444

Price/Earnings ratio 14.4 11.9

Price/Book ratio 2.6 2.1

5 Yr. EPS Growth Rate (%) 16.6 15.5

Current Yield (%) 2.2 2.8

Debt to Equity 1.0 0.9

Number of Stocks 155 834

Beta (5 Years, Monthly) 0.90 1.00

Consistency (5 Years, Monthly) 51.67 1.00

Sharpe Ratio (5 Years, Monthly) 0.36 0.32

Information Ratio (5 Years, Monthly) 0.03 -

Up Market Capture (5 Years, Monthly) 91.56 -

Down Market Capture (5 Years, Monthly) 88.50 -

Sector Weights (%)

Morgan Stanley Emerging Markets MSCI Emerging Markets Index

0.0 8.0 16.0 24.0 32.0 40.0

Cash

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

1.9

0.2

8.5

4.0

15.1

8.0

2.9

30.5

7.9

9.6

11.5

0.0

3.5

7.7

8.3

16.7

6.6

2.1

27.5

10.2

8.3

8.9

Distribution of Market Capitalization (%)

Morgan Stanley Emerging Markets MSCI Emerging Markets Index

0.0

15.0

30.0

45.0

60.0

>$75 Bil $20 Bil - $75 Bil

$5 Bil - $20 Bil

$0 - $5 Bil

Cash

17.5

28.0

38.6

15.8

0.0

13.4

26.5

38.9

19.2

1.9

Manager EvaluationMorgan Stanley Emerging Markets vs. MSCI Emerging Markets IndexAs of September 30, 2014

43

Morgan StanleyEmerging Markets

MSCI EmergingMarkets Index

Australia 0.0 0.0

Hong Kong 3.1 6.4

Japan 0.2 0.0

New Zealand 0.0 0.0

Singapore 0.5 0.1

Pacific 3.8 6.5

Austria 2.3 0.0

Belgium 0.0 0.0

Finland 0.0 0.0

France 0.0 0.0

Germany 0.0 0.0

Ireland 0.0 0.0

Italy 0.0 0.0

Netherlands 0.5 0.0

Portugal 0.8 0.0

Spain 0.0 0.0

EMU 3.5 0.0

Denmark 0.0 0.0

Norway 0.0 0.0

Sweden 0.0 0.0

Switzerland 1.1 0.0

United Kingdom 0.8 0.0

Europe ex EMU 1.9 0.0

Canada 0.0 0.0

United States 1.5 0.1

Israel 0.0 0.0

Middle East 0.0 0.0

Developed Markets 10.7 6.6

Morgan StanleyEmerging Markets

MSCI EmergingMarkets Index

Brazil 8.4 10.3

Cayman Islands 0.0 0.0

Chile 0.6 1.5

Colombia 2.8 1.0

Mexico 7.7 5.4

Peru 1.2 0.3

Virgin Islands 0.0 0.0

EM Latin America 20.7 18.5

China 10.1 12.7

India 9.1 7.1

Indonesia 1.2 2.7

Korea 14.5 15.0

Malaysia 2.4 3.9

Philippines 3.8 1.2

Taiwan 8.0 12.0

Thailand 3.6 2.4

EM Asia 52.7 56.9

Czech Republic 1.1 0.2

Egypt 0.0 0.3

Greece 0.0 0.7

Hungary 0.0 0.2

Poland 3.3 1.7

Qatar 0.5 0.6

Russia 1.0 4.6

South Africa 5.3 7.4

Turkey 0.0 1.6

United Arab Emirates 0.0 0.6

EM Europe + Middle East + Africa 11.0 17.9

Emerging Markets 84.4 93.4

Frontier Markets 1.3 0.0

Cash 1.9 0.0

Other 1.6 0.0

Total 100.0 100.0

Manager EvaluationMorgan Stanley Emerging Markets vs. MSCI Emerging Markets IndexAs of September 30, 2014

44

Historical Performance

Three Year Rolling Percentile Ranking Risk and Return (Oct-2009 - Sep-2014)

Historical Statistics (Oct-2009 - Sep-2014)

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Income Research -0.1 2.5 2.5 2.9 4.0 4.9 -0.9 5.9 5.6 6.2 14.4 0.8 7.4 4.5 2.8 3.7

Barclays Intermediate U.S. Government/Credit 0.0 2.2 2.2 2.0 3.4 4.0 -0.9 3.9 5.8 5.9 5.2 5.1 7.4 4.1 1.6 3.0

Intermediate Duration Fixed Income Peer Group Median -0.1 2.6 3.0 2.9 4.5 4.6 -0.6 5.1 4.6 6.1 9.8 -1.8 5.5 4.0 1.5 2.6

Income Research Rank 40 63 65 51 60 25 61 41 28 49 24 29 9 14 1 19

2.5

3.0

3.5

4.0

4.5

5.0

Re

turn

(%)

2.1 2.2 2.3 2.4 2.5Risk (Standard Deviation %)

Barclays Intermediate U.S. Government/Credit

Income Research

Income Research

Barclays Intermediate U.S. Government/Credit

0

25

50

75

100

Re

turn

Pe

rce

nti

le R

an

k

12/04 12/05 12/06 12/07 12/08 12/09 12/10 12/11 12/12 9/14

ReturnStandardDeviation

ExcessReturn Alpha Beta

SharpeRatio

TrackingError

InformationRatio

DownsideRisk Consistency

InceptionDate

Income Research 4.0 2.3 3.9 0.8 0.9 1.7 0.7 0.8 1.0 65.0 17y 8m

Barclays Intermediate U.S. Government/Credit 3.4 2.4 3.3 0.0 1.0 1.4 0.0 N/A 1.0 0.0 17y 8m

90 Day U.S. Treasury Bill 0.1 0.0 0.0 0.1 0.0 N/A 2.4 -1.4 0.0 20.0 17y 8m

Manager EvaluationIncome Research vs. Barclays Intermediate U.S. Government/CreditAs of September 30, 2014

45

Credit Quality Distribution (%)

Income Research

Barclays Intermediate U.S. Government/Credit

0.0

25.0

50.0

75.0

100.0

AAA AA ABBB BB B

Below

B

Not Rat

ed

64.9

6.6

14.3 14.2

0.0 0.0 0.0 0.0

51.4

9.5

17.720.9

0.0 0.0 0.0 0.6

Portfolio Characteristics

Portfolio Benchmark

Effective Duration 3.7 3.9

Avg. Maturity 4.3 4.2

Avg. Quality AA- AA

Yield To Maturity (%) 2.0 1.7

Sector Distribution (%)

Income Research

Barclays Intermediate U.S. Government/Credit

0.0

25.0

50.0

75.0

100.0

Treasu

ries

TIPS

Agenc

ies

Credi

t

Hig

h Yie

ldM

BSABS

Non-U

S

Emer

ging

Munic

ipal

s

Cas

h

Oth

er

CMBS

56.4

0.06.0

24.5

0.0 0.0 0.0

10.6

2.4 0.0 0.0 0.0 0.0

23.6

0.0 0.8

37.4

0.03.7

7.6

0.0 0.0 2.4 0.6

9.414.6

Maturity Distribution (%)

Income Research

Barclays Intermediate U.S. Government/Credit

0.0

15.0

30.0

45.0

60.0

< 1 Yr

1 < 3 Yrs

3 < 5 Yrs

5 <

10 Yrs

10 <

20 Yrs

> 20

Yrs

0.0

41.7

26.4

31.9

0.0 0.00.0

37.0

30.4 30.6

2.00.0

Manager EvaluationIncome Research vs. Barclays Intermediate U.S. Government/CreditAs of September 30, 2014

46

Historical Performance

Three Year Rolling Percentile Ranking Risk and Return (Oct-2009 - Sep-2014)

Historical Statistics (Oct-2009 - Sep-2014)

Quarter

YearTo

Date1

Year3

Years5

Years10

Years 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004

Penn Capital -2.2 2.0 5.6 8.4 8.9 N/A 5.9 13.3 4.2 15.0 37.5 -21.0 1.8 8.9 N/A N/A

BofA Merrill Lynch US High Yield, Cash Pay Index -1.9 3.5 7.1 10.9 10.3 8.1 7.4 15.4 4.5 15.2 56.3 -26.2 2.2 11.6 2.8 10.8

High Yield Fixed Income Peer Group Median -1.9 3.3 6.9 10.8 10.0 7.6 7.4 15.3 4.0 14.7 47.3 -24.3 2.6 10.7 3.1 10.4

Penn Capital Rank 81 93 88 93 84 N/A 78 80 46 41 79 25 74 84 N/A N/A

6.0

8.0

10.0

12.0