Leading Age – June 12, 2013

Diana JamisonWilliam Altavilla

William McMorran

Planned Giving Risk Management for CFOs

JTMH/JTM/ESCJTMH founded in 1963 & opened Canterbury WoodsIn 1965, Episcopal Senior Communities (ESC) was formed

Canterbury Woods transferred 5 more CCRC communities were added; St. Paul’s Towers, Los Gatos

Meadows, Spring Lake Village, San Francisco Towers, Webster House6 affordable communities; Oak Center Towers, Presidio Gates, Jennings

Court, and Lytton Garden Communities

2002 ESC formed Episcopal Senior Communities FoundationPrimary purpose is to raise funds for ESC communitiesAdminister those funds for the needs of the communities & its residents

JTM/Episcopal Senior Communities6 Continuing Care Retirement Communities, with the

following accommodations1,025 Independent Living95 Assisted Living10 Memory Support376 Skilled Nursing

Affordable Housing accommodations626 Independent Living50 Assisted Living

Home and Community Based Services ProgramsSenior Produce Markets, Senior Resources, Senior Center Without

Walls, Affordable Housing ProgramsServicing over 11,000 seniors in 6 countiesWith over 700 volunteers

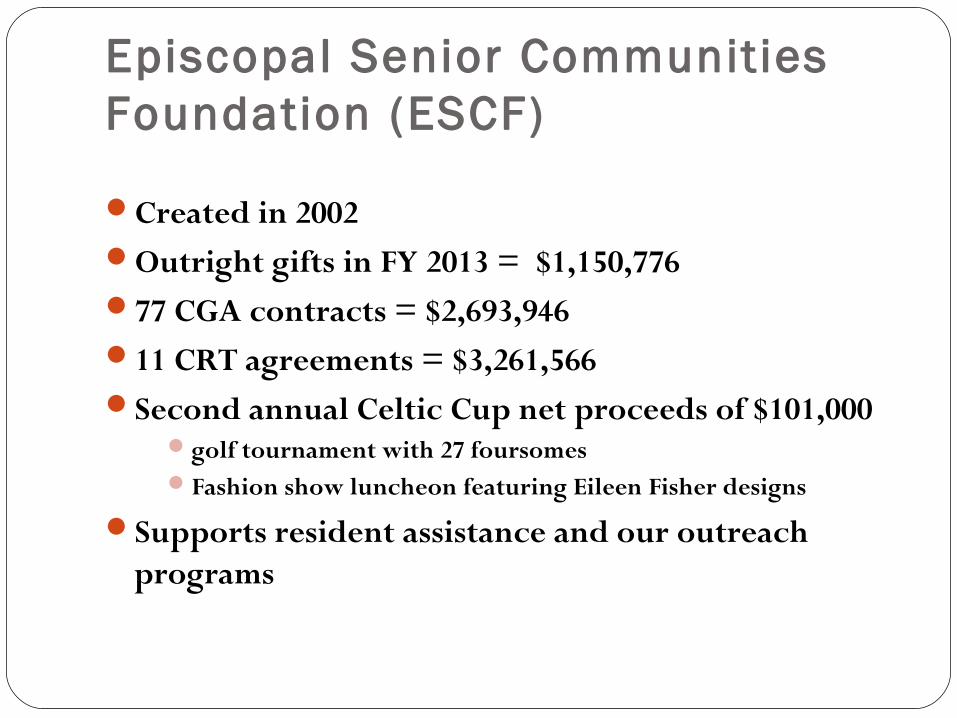

Episcopal Senior Communities Foundation (ESCF)

Created in 2002Outright gifts in FY 2013 = $1,150,77677 CGA contracts = $2,693,94611 CRT agreements = $3,261,566Second annual Celtic Cup net proceeds of $101,000

golf tournament with 27 foursomesFashion show luncheon featuring Eileen Fisher designs

Supports resident assistance and our outreach programs

Wills and Estates

Since 2000 we have had approximately 50 gifts from Wills and/or Estates

Totaling over $2,000,000

With an average gift amount of $43,000

Purpose of gifts range from General Community Funds to Capital projects

Managing CGA RiskCA department of Insurance regulations

Establish Reserve fund with investment restrictionLarge cap equities, government backed bonds

10/90 until 2005 After 2005 DOI amended to 50/50

ESCF’s Investment Policy is 30/70Average 60.4% of original gift at maturityNet amount $869KAverage gift size $37K

Protecting CGA Risk ExposureFollow ACGA rates

Rates designed to result in residuum of ≥ 50%Minimizes/relieves need for actuaries

PPA DisclosuresTo be provided to prospective donor in advance of giftContain information about the gift annuity & issuing charity

Monitor market values/exposure quarterlyCFO reviewInvestment Committee

Market new gifts steadilyEnsure that staff and operations meet all regulatory

requirements

Protecting CRT Risk ExposureFocus on Unitrusts over Annuity trusts

Use outside counsel for legal documentsAvoid generic fill-in formsDocument needs to support the plan

Make sure that donor uses own advisorsEnsure that donors requirements are met

Document everything

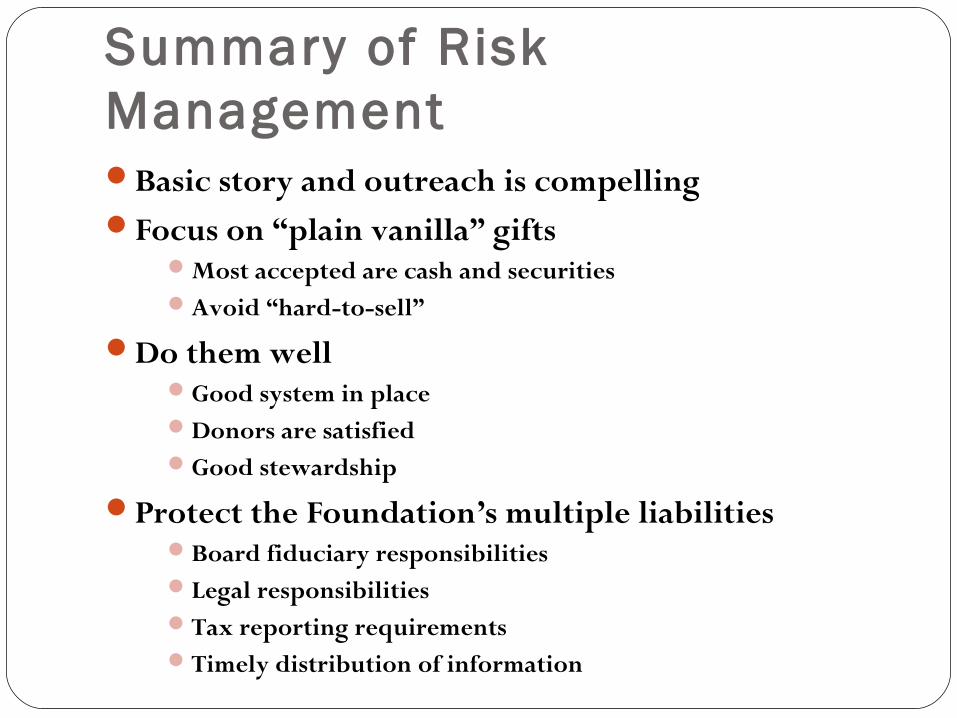

Summary of Risk ManagementBasic story and outreach is compellingFocus on “plain vanilla” gifts

Most accepted are cash and securitiesAvoid “hard-to-sell”

Do them wellGood system in placeDonors are satisfiedGood stewardship

Protect the Foundation’s multiple liabilitiesBoard fiduciary responsibilitiesLegal responsibilitiesTax reporting requirementsTimely distribution of information

Core Principals

• Donative Intent

• Primacy of Donor(s) needs

• Timeliness of Response

Responsible stewardship

Defining Risk

Legal Issues with EstatesInurement / Undue influenceTax/AuditInvestment RiskFiduciary OversightEnvironmental Pushing the Envelope

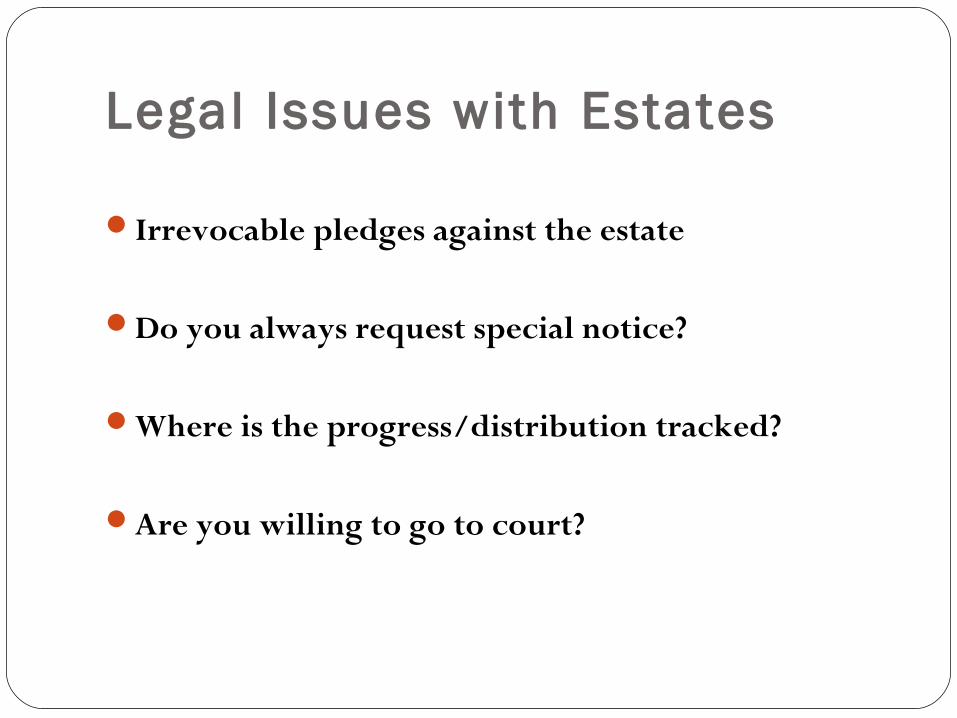

Legal Issues with Estates

Irrevocable pledges against the estate

Do you always request special notice?

Where is the progress/distribution tracked?

Are you willing to go to court?

Inurement & Undue Influence

A benefit to the donor or the Community?

Donor’s ability to make decision?

Appropriate safeguards?

Tax and Audit Risks

Make sure that donors receive accurate 1099s and K-1s ASAP – Save time and calls

File all reports timely

What will the auditors ask?

What will the auditors say?

Investment Risk - CRTs

You are not at risk the same as with CGAs

CRUTs should never exhaust themselves

Hard to manage CRUT donor expectations

CRATs can and DO exhaust themselves

CRUTs vs. CRATS

CRUT pays a fixed percentage, re-calculated annually. This offers inflation protection

CRUT payout must allow a 10% charitable deduction

CRAT pay a fixed amount based on initial gift value.CRAT payout must have less than 5% chance of

exhaustion

The Perfect CRUT Story*

Resident donated appreciated bonds = $100K to an 8% CRUT in 1990

One year she received 8% of $92,000

One year she received 8% of $154,000

At her death in 2009, gift was $114,000 *Past performance no indicator of future results and the experience in one case is not representative of all cases

CRT Investment Considerations

Balance income to donors with future value to Community

Generally a 60/40 allocation is good

Other considerations (high payout or FLIP) may influence specific gift management

Investment Risk - CGAs

Is there a clear investment policy?

Are there state-specific requirements?

Do you meet all your states’ requirements?

It’s your $$ if contract zeroes out

How It’s Supposed to Work

ACGA model is 45/50/5

Expected return is 4.25%

Assumption of 1% for investment/admin

Rates project a 50% residuum

Sample CGA Results ‘02-’12*

1. 44.59% $27,7712. 48.89% $51,4003. 60.47% $37,8394. 58.5% $13,7505. 80.08% $50,1976. 20.41% $19,822**

** Long-term problems now corrected

*Past performance no indicator of future results

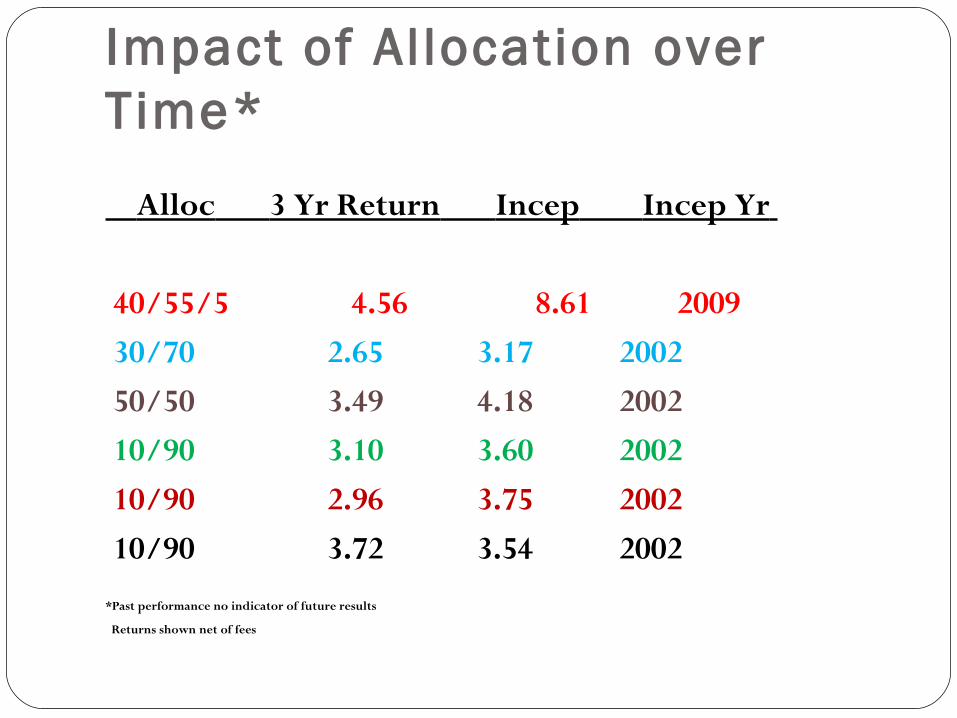

Impact of Al location over Time*

Alloc 3 Yr Return Incep Incep Yr

40/55/5 4.56 8.61 2009 30/70 2.65 3.17 2002 50/50 3.49 4.18 2002 10/90 3.10 3.60 2002 10/90 2.96 3.75 2002 10/90 3.72 3.54 2002

*Past performance no indicator of future results

Returns shown net of fees

Refundable Deposits

Can you create new gifts?

Variety of opportunities including:

- Outright gift

- Testamentary Gift

- Gift creating a CGA

Devil in the Details

Reality hinges on several factors including:

Initial contract and bond covenants

Formulas for discounting NPV

Depositor interest

Cost of $$

Expectancy for Female aged 80

Pick What’s Best!

• SOA Annuity 2000 w/ 1% Decline 11.9• SOA Annuity 2000 w/o 1% 11.3• IRA Uniform Table 10.2• CGA Annuity Table 9.5• SSA Expectancy w/ 1% Decline 9.3• SSA Expectancy w/o 1% Decline 8.9

Actuarial Evaluation for 8283????

Fiduciary Oversight

Fundraisers and CFOs talk different languages

Board members have high expectations

Keeping up with donors can be difficult

Testing innovative strategies with gift models

Pushing the Envelope

Getting gifts at any cost or payout

Encountering environmental problems

Deal making

Losing sight of mission

Planned Giving Risk Megacepts

Donative intent rules all decisions

Donors AND Auditors must be happy

Risk can be minimized

Benefits can be significant