Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

41

PREDICTION OF CENTRAL GOVERNMENT BUDGET TAX REVENUES

USING MARKOV MODEL

Merkezi Bütçe Vergi Gelirlerinin Markov Modeli ile Tahmin Edilmesi

Can Mavruk*

Ersin KIRAL**

ABSTRACT

The aim of this paper is to describe the behavior of the sample data and to

predict the realization rates of tax revenues by one step stochastic Markov chain model.

The realization rates of the tax revenues are estimated by using 2000-2014 gross annual

data extracted from TR Revenue Administration. Four Markov models are constructed

for the realization rates of every tax revenue. The realization probabilities for the year

2016 are predicted by constructing probability matrices of transitions between classes

described for every model. Revenues are also forecasted by the product of the initial

probability matrix and transition probability matrix. Limiting matrix of predictions are

found. The best Markov model was found by estimating the sum of mean square errors

for every model. The results are compared and interpreted.

Keywords: Tax Revenues, Transition Probabilities, Markov Analysis, Budget Forecast

ÖZET

Bu makalenin amacı örnek verinin davranışını tanımlamak ve bir adımlı

stokastik Markov zinciri modeli ile vergi gelirleri kalemlerinin gerçekleşme oranlarını

tahmin etmektir. Gelir İdaresi Başkanlığı 2000-2014 brüt yıllık verileri kullanılarak

vergi gelirlerinin gerçekleşme olasılığı hesaplanmıştır. Her verginin gerçekleşme

oranları için dört Markov modeli oluşturulmuştur. Her model için belirlenen sınıflar

arası geçiş olasılıkları matrisleri oluşturularak 2016 yılı gerçekleşme olasılıkları tahmin

edilmiştir. Ayrıca gelirler başlangıç matrisi ve geçiş olasılıkları matrisinin çarpımı ile

tahminlenmiştir. Tahminlerin limit matrisleri bulunmuştur. En iyi Markov modeli hata

karelerinin ortalamasının hesaplanmasıyla bulunmuştur. Sonuçlar karşılaştırılarak

yorumlanmıştır.

Anahtar Kelimeler: Vergi gelirleri, Geçiş Olasılıkları, Markov Analizi, Bütçe Tahmin

Introduction

Prediction of central government budget tax revenues has a great importance in

planning the distribution of revenues to public expenditures. Tax revenues are generated

from taxes collected from income, property, goods, services and foreign trade. The

proportion of tax incomes in general budget revenues has been increasing

* Öğr.Gör., Lecturer of Mathematics and Statistics, Nigde University, Vocational

School of Social Sciences, [email protected] ** Yrd.Doç.Dr., Assistant Professor of Operations Research, Cukurova University,

School of Business and Economics Dept. of Econometrics, [email protected]

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

42

(www.ekodialog.com>konular>genel_butce 8.12.2015). Even though tax incomes have

increased over time, the realization rates show a decreasing to stationary or increasing to

stationary behavior. Since public expenditures are also increasing by time, an increase

in realization rates is also expected. Otherwise, indirect tax items would be increased to

cover increasing public expenditures, which brings a heavy load to public. Tax increase

and revaluation rates are determined by Turkish Statistical Institute (TUIK) from twelve

month mean of domestic producer price index (dppi) in October

(http://www.zaman.com.tr/ekonomi_2015-yilinda-vergiler-yuzde-1011-oraninda-

artacak_2255169.html 10.12.2015). As of January 1st 2016, motor vehicle tax, stamp

duty tax, environmental tax, fees, traffic fines and tax fines will increse by the

revaluation rate 5.58% unless Council of Ministers increase or decrease this rate

(http://www.hurriyet.com.tr/2016-vergi-artis-oranlari-belli-oldu-40009417 9.12.2016).

Sub-items of tax revenues are individual income tax, corporate income tax, property tax,

inheritance and gift tax, motor vehicle tax, value added tax, special consumption tax,

banking and insurance transaction taxes, tax on wagering, special communication tax,

tax on customs, VAT on imports and stamp duty tax. In this paper, tax revenues are

analyzed and predicted by four Markov Models. The best of the four has the least sum

of the mean square errors. Predictions of tax revenues are expected to be stationary and

to have a limiting matrix.

Literature

Baasch et. al (2010) used Markov models to quantify transitions between

successional stages. They presented a solution for converting multivariate ecological

time series into transition matrices and demonstrate the applicability of this approach for

a data set that resulted from monitoring the succession of sandy dry grassland in a post-

mining landscape. They analyzed five transition matrices, four one-step matrices

referring to specific periods of transition (1995–1998, 1998–2001, 2001–2004, 2004–

2007), and one matrix for the whole study period (stationary model, 1995–2007).

Büyüktatlı et. al (2013) used initial allocations of investment program with

actual spending percentages from the years of 1998-2009 of Turkish Atomic Energy

Institute (TAEK) to predict annual allowances from Ministry of Energy and Natural

Resources. An estimated percentage of realization of investment program for 2011 and

results are interpreted with Markov analysis.

Cavers and Vasudevan (2015) directed graph representation of a Markov chain

model to study global earthquake sequencing leads to a time series of state-to-state

transition probabilities that includes the spatio-temporally linked recurrent events in the

recordbreaking sense. A state refers to a configuration comprised of zones with either the occurrence or non-occurrence of an earthquake in each zone in a pre-determined

time interval. Grimshaw and Alexander (2011) used a Markov chain model to forecast

outstanding balance of loans in each delinquency state. For that they used a markov

chain Xn as the delinquency state of a loan in month n and a Markov Chain model for

loan accounts that are ‘current’ this month having a probability of moving next month

into ‘current’, ‘delinquent’ or ‘paid-off’ states. They forecasted ‘one month ahead’

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

43

portfolio delinquency balance for a portfolio of loans where each loan is ni months from

origination this month i=1,...,N.

Lazri et.al (2015) adopted a Markovian approach to discern the probabilistic

behaviour of the time series of the drought. A transition probability matrix was

constructed from drought distribution maps. Markov transition probability formula for

four states and a simulation model with an initial probability vector was used to

calculate the drought distribution area in the future.

Lukić et. al. (2013) used the stochastic method based on a Markov chain

model to predict the annual precipitation in the territory of South Serbia for the period

2009-2013. For this purpose, the precipitation data rainfall recorded on the four

synoptic stations were used for the period 1980-2010.

Usher (1979) discussed that complex non-random or Markovian processes are

likely to characterize ecological successions, the transition probability matrix elements

not being constant but being functions either of the abundance, or of the rate of change

of abundance, of a recipient class.

Methodology: Markov Model

Markov chain is a stochastic process which is described by a transition matrix

of transition probabilities from one state into another state (Vantika and Pasaribu, 2014,

p.2).

A discrete time process {Xn,n = 0,1,2,...} with discrete state space Xn ∈ {0, 1,

2, ...} is a Markov chain if it has the Markov property: P(Xn+1=j | Xn=i, Xn−1 = in−1, ...,X0

= i0) = P(Xn+1=j|Xn=i) = p(i,j) where p(i,j) depends only on the states i,j, and not on the

time n or the previous states” (dept.stat.lsa.umich.edu/~ionides/620/notes/markov

_chains.pdf 15.12.2015). The numbers p(i,j) are called the transition probabilities of the

chain. (galton.uchicago.edu/~lalley/Courses/312/MarkovChains.pdf 15.12.2015).

One step probability is pij=P(X1=j | X0=i) (İlarslan, 2014, s.6190). In a first

order Markov chain, the state at any time instant depends only on the state immediately

preceding it, and hence is defined as a single-dependence chain and m step probability

is pm

ij =P(Xm=j | X0=i).

Construction of Transition Probabilities

Transition probability matrices are estimated for 2000-2014 for sub-items of

tax revenues. The estimator of the transition probabilities is the relative frequency of the

actual transitions from phase i to phase j, i.e. the observed transitions have to be divided

by the sum of the transitions to all other phases (Lipták, 2011, p.141)

In this paper, j ijijij nnP / where i, j = A, B, C, D, E and nij is the number of

observed transitions from i to j and j ijn is the sum of observed transitions from i to j.

Frequency distribution of the realization rate intervals must be mutually

exclusive (nonoverlapping) and class width must be equal for each interval (Bluman,

2014, p.45-46). Transition probabilities from Xi to Xj, i, j = 0,1,2,…,n, can be

constructed as the following matrix (Taha, 2000, p.726)

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

44

nnnn

n

n

ij

PPP

PPP

PPP

P

...

...

...

21

22221

11211

Since pij are constant and independent of time (time homogeneous), matrix Pij

= P is called a stochastic matrix. Pij probabilities must satisfy the following conditions:

njiPij ,...,2,1,0 nipi

ij ,...,2,11

Prediction

Given that data at time n is in state X0 and that the data will be in one of states

Xn ∈ {0,1,2,...} at time n+1, then the data at time n+2 can be predicted. Given initial

probability P(X0 = i) = pi for every i, the required probability is matrix multiplication pi

kjk ikPP . Equivalently, next year’s probability distribution matrix can be predicted by

Qn+1 = Qn P n = 0,1,2,3,… (1)

Initial probability matrices for four Markov models are 1xj row matrices. Stationary

prediction matrices Qn+1 have a limiting matrix Q, which can be written as QQnn

lim .

Best of Four Markov Models

For every year of the sample and for every Markov model, mean square error

(mse) is calculated by

n

i

ii rrn 1

2ˆ

1 where i is the number of states, nnn PQQ 1

ˆ

nrrrr ˆˆˆˆ321 is predicted realization rate at time n+1 and nn rrrQ 21 is

observed realization rate at time n. The least mse gives the best Markov model.

Statistical Significance of the Models

Variations between observed and expected frequencies can be tested by

constructing a contingency table of frequency distribution of transitions between the

states at 0,05 significance level with a degree of freedom.

To validate Markov model, for every year, the value of the χ2 statistic is

computed based on the null hypothesis, H0: model is valid. At 0,05 level of significance

and with the degrees of freedom, the χ2 critical value and χ

2 test value are estimated.

The null hypothesis is not rejected whenever χ2 test value is less than the critical value.

Test values are calculated by iii i rrr ˆ/)ˆ( 22 where i is the number of

categories, and ir and

ir̂ are the actual and estimated values, respectively.

Income Tax

Income tax targeted, collected (http://www.gib.gov.tr/sites/default/files/fileadmin/user_

upload/VI/GBG/Tablo_47.xls.htm, http://www.gib.gov.tr/sites/default/files/fileadmin/

user_upload/VI/GBG/Tablo_44.xls.htm, http://www.gib.gov.tr/sites/default/files/

fileadmin/user_upload/VI/GBG/Tablo_46.xls.htm, http://www.gib.gov.tr/sites/default

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

45

/files/fileadmin/user_upload/VI/GBG/Tablo_45.xls.htm 5.12.2015) and realization rates

for the years 2000-2014 are given in Table 2. In the last fifteen years the highest rate in

income tax realized was 113,7% in 2001 and the lowest realized was 85.1% in 2009.

Targeted income tax has increased every year except the year 2010. Tax collection has

increased every year between 2000-2014. While targeted income tax was increasing

4,47 billion TL per year on average, tax collection was also increasing 4,88 billion TL

per year on average.

Income Tax Markov Models and Transition Probability Matrices

Income tax realization rates from smallest to largest are classified as E,D,C,B,

A in model 1, D, C, B, A in model 2, C, B, A in model 3 and B, A in model 4. For years

between 2000 and 2014 table 2 shows that realization rates are over 100% in three

categories of model 1, in two categories of model 2, in two categories of model 3.

Table 1. Income Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

108.3 ≤ r

102.5 ≤ r ≤ 108.2

96.7 ≤ r ≤ 102.4

90.9 ≤ r ≤ 96.6

r ≤ 90.8

A

B

C

D

E

0 1/2 0 0 1/2 106.7 ≤ r A

B

C

D

1/3 1/3 0 1/3

1/5 2/5 2/5 0 0 99.5 ≤ r ≤ 106.6

1/3 1/2 0 1/6

2/5 2/5 0 0 1/5 92.3 ≤ r ≤ 99.4

1/3 2/3 0 0

0 0 0 0 0 r ≤ 92.2

0 0 1 0

0 0 1 0 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

104.3 ≤ r

A

B

C

2/5 2/5 1/5 99.5 ≤ r

A

B

C

7/9 2/9

94.7 ≤ r ≤ 104.2

4/7 2/7 1/7 r ≤ 99.4 B 3/5 2/5

r ≤ 94.6

0 1 0

For the years 2000-2014, the realization rates of income tax, classes and

transitions for four Markov models are shown in Table 2.

Tablo 2. Income Tax (000 TL) and Classification of Realization Rates and Transitions

Year Targeted Collected

Real.

Rate

(%)

Class M1 Class M2 Class M3 Class M4

2000 6.276.000 6.212.977 99 C C B B

2001 10.186.000 11.579.424 113,7 A CA A CA A BA A BA

2002 15.401.000 13.717.660 89,1 E AE D AD C AC B AB

2003 17.196.918 17.063.761 99,2 C EC C DC B CB B BB

2004 18.655.000 19.689.593 105,5 B CB B CB A BA A BA

2005 21.170.000 22.817.530 107,8 B BB A BA A AA A AA

2006 29.071.000 31.727.644 109,1 A BA A AA A AA A AA

2007 36.922.897 38.061.543 103,1 B AB B AB B AB A AA

2008 38.780.119 39.249.867 101,2 C BC B BB B BB A AA

2009 46.598.274 39.668.595 85,1 E CE D BD C BC B AB

2010 42.927.809 41.969.451 97,8 C EC C DC B CB B BB

2011 48.951.204 51.092.935 104,4 B CB B CB A BA A BA

2012 56.710.510 58.797.752 103,7 B BB B BB B AB A AA

2013 65.483.652 65.914.727 100,7 C BC B BB B BB A AA

2014 73.289.337 79.451.776 108,4 A CA A BA A BA A AA

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

46

Prediction For Income Tax Realization Rate

Given that 2014 income tax realization rate 108.4% is in state A and that income

tax will be in one of states A, B, C, D or E in 2015, income tax realization rate for 2016

is predicted.

Tablo 3. Income Tax Realization Rates Predictions for 2016

Realization

Interval (%)

M1

Pred.

Realization

Interval (%)

M2

Pred.

Realization

Interval (%)

M3

Pred.

Real. Int.

(%)

M4

Pred.

r ≤ 90.8 0 r < 92.2 0.17 r ≤ 94.6 0,14 r ≤ 99.4 0,26

90.9 ≤ r ≤ 96.6 0 92.3 ≤ r ≤ 99.4 0,33 94.7 ≤ r ≤ 104.2 0,47 99.5 ≤ r 0,74

96.7 ≤ r ≤ 102.4 0,70 99.5 ≤ r ≤ 106.6 0,28 104.3 ≤ r 0,39

102.5 ≤ r ≤ 108.2 0,20 106.7 ≤ r 0,22

108.3 ≤ r 0,10

Stationarity of Income Tax Predictions

Predictions are estimated in Excel by formula (1) for all models. According to

four models, all probabilities become stationary in 2031, 2026, 2022 and 2020

respectively.

Statistical Significance of The Model For Income Tax

In model 1 of income tax, variations between observed and expected

frequencies can be tested by constructing a contingency table of frequency distribution

of transitions between the states at 0,05 significance level with 16 df. Since chi square

test value 11,23 is less than critical value 26,296, H0 is not rejected. This shows that

there is no significant variations. The values in paranthesis in the Table 4 are expected

frequencies which are found from (row sum X column sum)/total. Table 4 shows that in

model 1 transitions in higher realization states are stable and in lower states rates are

improving.

Table 4. Contingency Table of Observed and Expected Income Tax Rates of Model 1. A B C D E Total

A 0 (0,43) 1 (0,71) 0 (0,57) 0 1 (0,29) 2

B 1 (1,07) 2 (1,79) 2 (1,43) 0 0 (0,71) 5

C 2 (1,07) 2 (1,79) 0 (1,43) 0 1 (0,71) 5

D 0 0 0 0 0 0

E 0 (0,43) 0 (0,71) 2 (0,57) 0 0 (0,29) 2

Total 3 5 4 0 2 14

Corporate Tax

Corporate tax targeted, collected and realization rates for years 2000-2014 are

given in Table 6. In the last fifteen years the highest corporate tax rate realized was

175% in 2001 when targeted at the lowest and the lowest realized was 71,2 in 2000.

Targeted corporate tax has increased every year except the years 2001, 2005, 2007 and

2010. Tax collection has increased every year between 2000-2014 except in 2013 when

it had a slight decrease. While targeted corporate tax was increasing 2 billion TL per

year on average, tax collection was also increasing 2,2 billion TL per year on average.

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

47

But, the realization rate was decreasing by approximately 1,5% per year in the given

period.

Corporate Tax Transition Probability Matrices

In four categories of model 1, in three categories of model 2, in all categories

of model 3 and model 4, realization rates are over 100% between 2000 and 2014.

Table 5. Corporate Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real. Interval (%) A B C D

154,4 ≤ r

133,6 ≤ r ≤ 154,3

112,8 ≤ r ≤ 133,5

92 ≤ r ≤ 112,7

r ≤ 91,9

A

B

C

D

E

.5 0 0 .5 0 149,2 ≤ r A

B

C

D

.5 0 .5 0

0 0 0 0 0 123,2 ≤ r ≤ 149,1 0 0 0 1

0 0 1/3 1/3 1/3 97,2 ≤ r ≤ 123,1 0 1/7 5/7 1/7

0 0 1/6 4/6 1/6 r ≤ 97,1 1/4 0 3/4 0

1/3 0 1/3 1/3 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

140,8 ≤ r A

B

C

.5 0 .5 123,2 ≤ r A

B

C

1/3 2/3

105,8 ≤ r ≤ 140,7 0 .5 .5 r ≤ 123,1 B 2/11 9/11

r ≤ 105,7 1/6 1/2 1/3

For the years 2000-2014, the realization rates of corporate tax, classes and

transitions for four Markov models are shown in Table 6.

Table 6. Corporate Tax (000 TL) and Classification of Realization Rates and Transitions

Year Targeted Collected Real.

Rate

(%)

Class MM1 Class MM2 Class MM3 Class MM4

2000 3.309.000 2.356.787 71,2 E D C B

2001 2.100.000 3.675.665 175 A EA A DA A CA A BA

2002 3.595.000 5.575.495 155,1 A AA A AA A AA A AA

2003 8.918.160 8.645.345 96,9 D AD D AD C AC B AB

2004 9.335.000 9.619.359 103 D DD C DC C CC B BB

2005 8.890.000 11.401.986 128,3 C DC B CB B CB A BA

2006 14.756.000 12.447.354 84,4 E CE D BD C BC B AB

2007 14.410.186 15.718.474 109,1 D ED C DC B CB B BB

2008 16.976.161 18.658.195 109,9 D DD C CC B BB B BB

2009 22.611.359 20.701.805 91,6 E DE D CD C BC B BB

2010 20.071.108 22.854.846 113,9 C EC C DC B CB B BB

2011 25.359.580 29.233.725 115,3 C CC C CC B BB B BB

2012 30.035.121 32.111.820 106,9 D CD C CC B BB B BB

2013 32.043.560 31.434.581 98,1 D DD C CC C BC B BB

2014 33.892.413 35.163.517 103,8 D DD C CC C CC B BB

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

48

Realization Rates and Transition Probability Matrices of Other Tax Revenues

Table 7. Property Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real. Interval (%) A B C D

134,5 ≤ r

123,1 ≤ r ≤ 134,4

111,7 ≤ r ≤ 123

100,3 ≤ r ≤ 111,6

r ≤ 100,2

A

B

C

D

E

0 0 0 .5 .5 r ≤ 103 A

B

C

D

0 0 .5 .5

0 0 0 0 0 103,1 ≤ r ≤ 117,2 0 0 0 0

0 0 0 1 0 117,3 ≤ r ≤ 131,4 0 0 .25 .75

0 0 0 .4 .6 131,5 ≤ r 1/8 0 1/8 6/8

1/6 0 1/6 1/6 3/6

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

r ≤ 103 A

B

C

0 0 1 117,3 ≤ r

A

B

C

0 1

103,1 ≤ r ≤ 117,2 0 0 1 r ≤ 117,2

B 1/12 11/12

117,3 ≤ r ≤ 131,4 1/11 1/11 9/11

Table 8. Inheritance and Gift Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real. Interval (%) A B C D

125,7 ≤ r

108,6 ≤ r <125,6

91.5 ≤ r < 108,5

74,4 ≤ r < 91,4

r < 74,3

A

B

C

D

E

1/3 0 2/3 0 0 121,5 ≤ r A

B

C

D

.25 .75 0 0

0 1/3 1/3 0 1/3 100,1 ≤ r ≤ 121,4

.2 .4 .2 .2

2/5 1/5 2/5 0 0 78,7 ≤ r ≤ 100

1 0 0 0

0 0 0 0 0 r ≤ 78,6 0 1/3 1/3 1/3

0 1/3 1/3 0

/

6

1/3

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

114,1 ≤ r

A

B

C

1/3 1/2 1/6 100,1 ≤ r

A

B

C

7/9 2/9

85,8 ≤ r ≤ 114,2

3/5 2/5 0 r ≤ 100 B 3/5 2/5

r ≤ 85,7 1/3 1/3 1/3

Table 9. Motor Vehicle Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

110,8 ≤ r

105,5 ≤ r ≤110,7

100,2 ≤ r ≤105,4

94,9 ≤ r ≤ 100,1

r ≤ 94,8

A

B

C

D

E

0 0 1 0 0 109,7 ≤ r A

B

C

D

0 0 1 0

0 .5 .25 .25 0 103 ≤ r ≤109,6

0 4/5 1/5 0

0 0 4/6 2/6 0 96,3 ≤ r ≤ 102,9

0 0 4/6 2/6

1/3 0 1/3 0 1/3 r ≤ 96,2 .5 .5 0 0

0 1 0 0 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

107,4 ≤ r

A

B

C

0 1 0 102,9 ≤ r

A

B

C

4/6 2/6

98,5 ≤ r ≤ 107,3

1/9 6/9 2/9 r ≤ 102,8 B 2/8 6/8

r ≤ 98,4 1/3 1/3 1/3

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

49

Table 10. Value Added Tax Included Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

109.8 ≤ r

105.4 ≤ r ≤ 109.7

101 ≤ r ≤ 105.3

96.6 ≤ r ≤ 100.9

r ≤ 96.5

A

B

C

D

E

0 0 1 0 0 108.7 ≤ r A

B

C

D

0 1/2 0 1/2

0 0 0 0 1 103.2 ≤ r ≤ 108.6

1/2 0 1/2 0

1/4 1/4 1/2 0 0 97.7 ≤ r ≤ 103.1

1/6 2/6 3/6 0

0 0 2/5 3/5 0 r ≤ 97.6

0 0 1/2 1/2

0 0 0 1/3 2/3

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

106.8 ≤ r

A

B

C

0 1/2 1/2 103.3 ≤ r

A

B

C

1/2 1/2

99.5 ≤ r ≤ 106.7 2/5 3/5 0 r ≤ 103.2 B 3/10 7/10

r ≤ 99.4 0 2/7 5/7

Table 11. Special Consumption Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

102,6 ≤ r

98,7 ≤ r ≤ 102,5

95,4 ≤ r ≤ 98,6

91,8 ≤ r ≤ 95,3

r ≤ 91,7

A

B

C

D

E

1/3 0 2/3 0 0 101,7 ≤ r A

B

C

D

2/3 1/3 0 0

0 1/3 1/3 0 1/3 97,2 ≤ r ≤ 101,6

1/4 1/4 1/2 0

2/5 1/5 2/5 0 0 92,7 ≤ r ≤ 97,1

0 1/3 1/3 1/3

0 0 0 0 0 r ≤ 92,6 1 0 0 0

0 1/3 1/3 0 1/3

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

100,2 ≤ r

A

B

C

1 0 0 97,2 ≤ r

A

B

C

5/7 2/7

94,2 ≤ r ≤ 100,1

0 4/5 1/5 r ≤ 97,1

B 2/4 2/4

r ≤ 94,1

½ 0 1/2

Table 12. Banking and Insurance Transaction Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

131,6 ≤ r

114,2 ≤ r ≤ 131,5

96,8 ≤ r ≤ 114,1

79,4 ≤ r ≤ 96,7

r ≤ 79,3

A

B

C

D

E

1/2 0 1/2 0 0 127,1 ≤ r A

B

C

D

1/3 0 1/3 1/3

0 1/3 1/3 0 1/3 105,4 ≤ r ≤ 127

1/3 0 2/3 0

1/5 1/5 2/5 1/5 0 83,7 ≤ r ≤ 105,3

1/7 1/7 5/7 0

0 0 1/3 2/3 0 r ≤ 83,6

0 1 0 0

0 0 1 0 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

119,8 ≤ r

A

B

C

1/4 1/2 1/4 105,4 ≤ r

A

B

C

2/6 4/6

90,9 ≤ r ≤ 119,7

1/3 2/3 0 r ≤ 105,3 B 3/8 5/8

r ≤ 90,8

0 1 0

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

50

Table 13. Tax on Wagering Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

111,5 ≤ r

103,2 ≤ r ≤111,6

94,7 ≤ r ≤103,1

86, 2 ≤ r ≤ 94,6

r ≤ 86,1

A

B

C

D

E

1/2 0 1/2 0 0 109,5 ≤ r A

B

C

D

1/3 0 1/3 1/3

1/2 0 0 0 1/2 98,9 ≤ r ≤ 109,4

1 0 0 0

0 1 0 0 0 88,3 ≤ r ≤ 98,8

1/4 1/2 1/2 0

0 1/2 12 0 0 r ≤ 88,2

0 0 1 0

0 0 1 0 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

105,9 ≤ r

A

B

C

1/4 1/2 1/4 98,9 ≤ r

A

B

C

1/2 1/2

91,8 ≤ r ≤ 105,8

1/2 1/2 0 r ≤ 98,8 B 3/5 2/5

r ≤ 91,7

0 1 0

Table 14. Special Communication Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

125,9 ≤ r

111,9 ≤ r ≤ 125,8

97,9 ≤ r ≤ 111,8

83,9 ≤ r ≤ 97,8

r ≤ 83,8

A

B

C

D

E

0 0 1 0 0 122,4 ≤ r A

B

C

D

0 1 0 0

0 0 0 0 0 104,9 ≤ r ≤ 122,3

0 0 1 0

0 0 1/4 1/2 1/4 87,4 ≤ r ≤ 104,8

1/9 1/9 2/3 1/9

1/7 0 4/7 2/7 0 r ≤ 87,3

0 0 1/2 1/2

0 0 0 1 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

116,5 ≤ r

A

B

C

0 0 1 104,9 ≤ r

A

B

C

1/2 1/2

93,2 ≤ r ≤ 116,4

1/8 5/8 2/8 r ≤ 104,8 B 1/11 10/11

r ≤ 93,1 0 3/4 1/4

Table 15. Tax on Customs Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

116,1 ≤ r

104,6 ≤ r ≤ 116

93,1 ≤ r ≤ 104,5

81,6 ≤ r ≤ 93

r ≤ 81,5

A

B

C

D

E

0 1/3 1/3 1/3 0 113,3 ≤ r A

B

C

D

0 2/3 1/3 0

2/3 0 0 1/3 0 98,9 ≤ r ≤ 113,2

2/5 0 2/5 1/5

0 0 1/3 0 2/3 84,5 ≤ r ≤ 98,8

2/4 1/4 0 1/4

2/3 1/3 0 0 0 r ≤ 84,4 0 1/2 1/2 0

0 1/2 0 1/2 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

108.5 ≤ r

A

B

C

2/5 2/5 1/5 98.8 ≤ r

A

B

C

1/2 1/2

89,3 ≤ r ≤ 108,4

1/5 1/5 3/5 r ≤ 98.7 B 4/6 2/6

r ≤ 89,2 3/4 1/4 0

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

51

Table 16. VAT on Imports Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

130,3 ≤ r

114,7 ≤ r ≤ 130,2

99,1 ≤ r ≤ 114,6

83,5 ≤ r < 99

r ≤ 83,4

A

B

C

D

E

0 0 0 1 0 126,4 ≤ r A

B

C

D

0 0 0 1

0 1/2 0 1/2 0 106,9 ≤ r ≤ 126,3

0 1/4 3/4 0

0 0 3/5 2/5 0 87,4 ≤ r ≤ 106,8

0 2/7 4/7 1/7

0 0 3/5 1/5 1/5 r ≤ 87,3 0 1/2 1/2 0

0 1 0 0 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

119,7 ≤ r

A

B

C

0 1/2 1/5 106,8 ≤ r

A

B

C

1/5 4/5

93,8 ≤ r ≤ 119,6

0 3/7 4/7 r ≤ 106,7 B 3/9 6/9

r ≤ 93,7 1/5 4/5 0

Table 17. Stamp Duty Tax Markov Models and Transition Probability Matrices

Markov Model 1 Transition Matrix Markov Model 2 Transition Matrix

Real.Interval (%) A B C D E Real.Interval (%) A B C D

115,8 ≤ r

108,2 ≤ r ≤ 115,7

100,6 ≤ r ≤ 108,1

93 ≤ r ≤ 100,5

r ≤ 92,9

A

B

C

D

E

0 0 0 1/2 1/2 113,9 ≤ r A

B

C

D

0 1/4 1/4 2/4

0 1/4 1/4 1/2 0 104,4 ≤ r ≤ 113,8

0 0 1/2 1/2

0 1 0 0 0 94,9 ≤ r ≤ 104,3

2/3 0 1/3 0

1/5 1/5 0 2/5 1/5 r ≤ 94,8 1/5 1/5 1/5 2/5

0 1/2 0 1/2 0

Markov Model 3 Transition Matrix Markov Model 4 Transition Matrix

Real. Interval (%) A B C Real. Interval (%) A B

110,6 ≤ r A

B

C

1/6 3/6 2/6 104,3 ≤ r

A

B

C

1/6 5/6

98 ≤ r ≤ 110,5

1/2 0 1/2 r ≤ 104,2

B 4/8 4/8

r ≤ 97,9 1/2 0 1/2

Predictions of Tax Revenues for 2016

Given that 2014 tax realization rate in a state and this tax will be in one of states

A, B, C, D or E in 2015, realization rates matrices are predicted for 2016 by formula (1).

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

52

Table 18. 2016 Prediction of Tax Revenues A B C D E A B C D E

Inco

me

Tax

M1 0,10 0,20 0,70 0,00 0,00

Co

rpo

rate

Tax

0,06 0 0,22 0,56 0,17

M2 0,22 0,28 0,33 0,17 0,04 0,10 0,62 0,24

M3 0,39 0,47 0,14 0,14 0,42 0,44

M4 0,74 0,26 0,21 0,79

Pro

per

ty

Tax

M1 0,08 0,00 0,08 0,40 0,44

IGT

0,29 0,15 0,49 0,00 0,07

M2 0,09 0,00 0,19 0,72 0,33 0,38 0,15 0,14

M3 0,07 0,07 0,86 0,44 0,46 0,10

M4 0,08 0,92 0,74 0,26

MV

T M1 0,00 0,50 0,25 0,25 0,00

VA

T

Incl

ud

e

0,12 0,13 0,50 0,00 0,25

M2 0,00 0,40 0,60 0,00 0,08 0,42 0,25 0,25

M3 0,15 0,67 0,19 0,24 0,56 0,20

M4 0,35 0,65 0,40 0,60

Sp

ecia

l

Con

Tax

M1 0,12 0,13 0,50 0,00 0,25

BIT

T 0,20 0,20 0,40 0,20 0,00

M2 0,08 0,42 0,25 0,25 0,33 0,00 0,67 0,00

M3 0,24 0,56 0,20 0,33 0,67 0,00

M4 0,40 0,60 0,36 0,64

Tax

on

Wag

erin

M1 0,25 0,00 0,75 0,00 0,00

Sp

ecia

l

Co

m T

ax 0,07 0,00 0,35 0,52 0,06

M2 0,34 0,00 0,33 0,33 0,07 0,19 0,61 0,13

M3 0,50 0,38 0,12 0,08 0,58 0,34

M4 0,55 0,45 0,13 0,87

Tax

on

Cu

stom

s

M1 0,45 0,11 0,11 0,11 0,22

VA

T o

n

Imp

ort

s

0,00 0,00 0,60 0,32 0,08

M2 0,43 0,08 0,27 0,22 0,00 0,31 0,61 0,08

M3 0,39 0,29 0,32 0,11 0,64 0,25

M4 0,58 0,42 0,29 0,71

Sta

mp

Du

ty T

ax M1 0,08 0,23 0,05 0,46 0,18

M2 0,22 0,17 0,28 0,33

M3 0,33 0,25 0,42

M4 0,33 0,67

A Better Model For Tax Revenues

Sum of mean square errors for a better model of each tax revenue is given in

table 19. Values in bold indicates the better model.

Table 19. Tax Revenues SMSE Tax Revenues Sum of Mean Square Errors (SMSE)

Model 1 Model 2 Model 3 Model 4

Income tax 2,61 3,65 3,89 5,07

Corporate tax 3,52 3,26 4,80 3,97

Property Tax 2,62 2,36 2,08 2,69

Inheritence and Gift Tax 3,21 4,28 4,75 4,30

Motor Vehicle Tax 3,04 4,21 4,99 4,75

Vat Included 2,91 3,45 4,66 4,14

Special Consumption Tax 2,60 3,14 2,50 3,69

Banking and Insurance Tax 3,02 3,42 3,89 3,83

Tax on Wagering 2,30 2,79 3,14 2,80

Special Communication Tax 2,12 3,08 4,33 2,33

Tax on Customs 3,83 4,26 4,77 4,61

Vat on Imports 2,61 3,88 5,00 4,51

Stamp Duty Tax 3,54 4,15 4,22 3,67

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

53

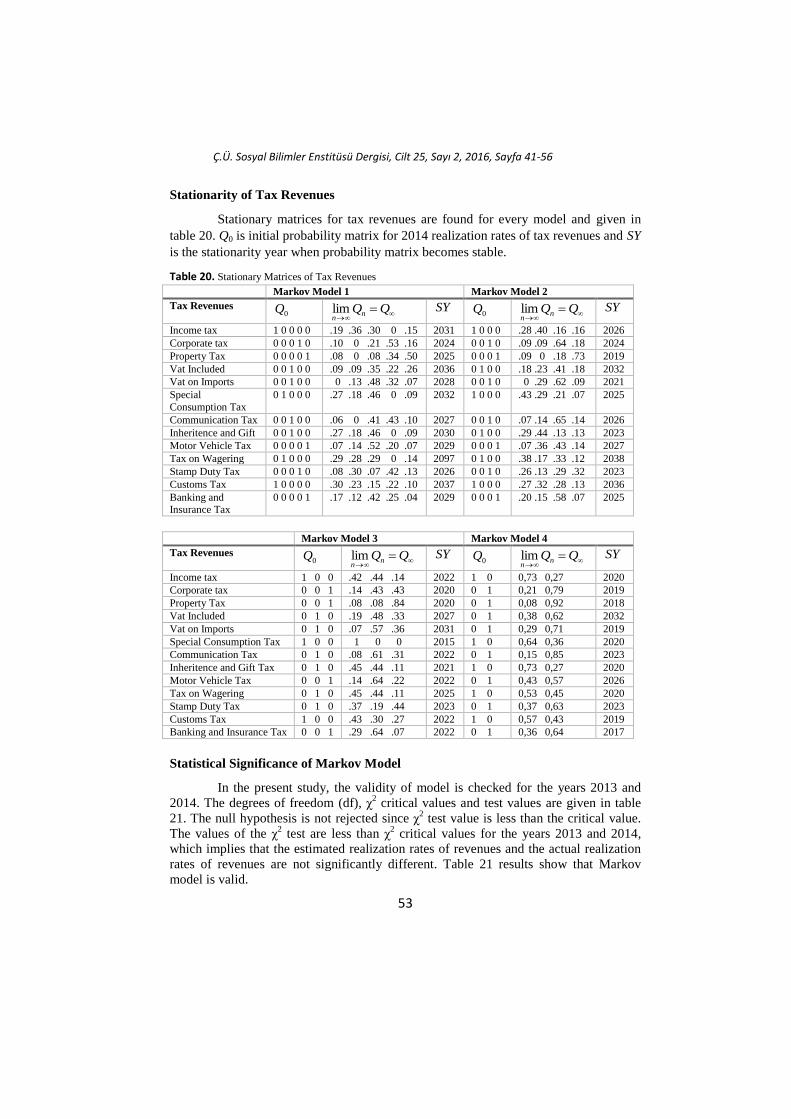

Stationarity of Tax Revenues

Stationary matrices for tax revenues are found for every model and given in

table 20. Q0 is initial probability matrix for 2014 realization rates of tax revenues and SY

is the stationarity year when probability matrix becomes stable.

Table 20. Stationary Matrices of Tax Revenues Markov Model 1 Markov Model 2

Tax Revenues 0Q

QQnnlim SY

0Q

QQn

nlim SY

Income tax 1 0 0 0 0 .19 .36 .30 0 .15 2031 1 0 0 0 .28 .40 .16 .16 2026

Corporate tax 0 0 0 1 0 .10 0 .21 .53 .16 2024 0 0 1 0 .09 .09 .64 .18 2024

Property Tax 0 0 0 0 1 .08 0 .08 .34 .50 2025 0 0 0 1 .09 0 .18 .73 2019

Vat Included 0 0 1 0 0 .09 .09 .35 .22 .26 2036 0 1 0 0 .18 .23 .41 .18 2032

Vat on Imports 0 0 1 0 0 0 .13 .48 .32 .07 2028 0 0 1 0 0 .29 .62 .09 2021

Special

Consumption Tax

0 1 0 0 0 .27 .18 .46 0 .09 2032 1 0 0 0 .43 .29 .21 .07 2025

Communication Tax 0 0 1 0 0 .06 0 .41 .43 .10 2027 0 0 1 0 .07 .14 .65 .14 2026

Inheritence and Gift 0 0 1 0 0 .27 .18 .46 0 .09 2030 0 1 0 0 .29 .44 .13 .13 2023

Motor Vehicle Tax 0 0 0 0 1 .07 .14 .52 .20 .07 2029 0 0 0 1 .07 .36 .43 .14 2027

Tax on Wagering 0 1 0 0 0 .29 .28 .29 0 .14 2097 0 1 0 0 .38 .17 .33 .12 2038

Stamp Duty Tax 0 0 0 1 0 .08 .30 .07 .42 .13 2026 0 0 1 0 .26 .13 .29 .32 2023

Customs Tax 1 0 0 0 0 .30 .23 .15 .22 .10 2037 1 0 0 0 .27 .32 .28 .13 2036

Banking and Insurance Tax

0 0 0 0 1 .17 .12 .42 .25 .04 2029 0 0 0 1 .20 .15 .58 .07 2025

Markov Model 3 Markov Model 4

Tax Revenues 0Q

QQnnlim SY

0Q

QQn

nlim SY

Income tax 1 0 0 .42 .44 .14 2022 1 0 0,73 0,27 2020

Corporate tax 0 0 1 .14 .43 .43 2020 0 1 0,21 0,79 2019

Property Tax 0 0 1 .08 .08 .84 2020 0 1 0,08 0,92 2018

Vat Included 0 1 0 .19 .48 .33 2027 0 1 0,38 0,62 2032

Vat on Imports 0 1 0 .07 .57 .36 2031 0 1 0,29 0,71 2019

Special Consumption Tax 1 0 0 1 0 0 2015 1 0 0,64 0,36 2020

Communication Tax 0 1 0 .08 .61 .31 2022 0 1 0,15 0,85 2023

Inheritence and Gift Tax 0 1 0 .45 .44 .11 2021 1 0 0,73 0,27 2020

Motor Vehicle Tax 0 0 1 .14 .64 .22 2022 0 1 0,43 0,57 2026

Tax on Wagering 0 1 0 .45 .44 .11 2025 1 0 0,53 0,45 2020

Stamp Duty Tax 0 1 0 .37 .19 .44 2023 0 1 0,37 0,63 2023

Customs Tax 1 0 0 .43 .30 .27 2022 1 0 0,57 0,43 2019

Banking and Insurance Tax 0 0 1 .29 .64 .07 2022 0 1 0,36 0,64 2017

Statistical Significance of Markov Model

In the present study, the validity of model is checked for the years 2013 and

2014. The degrees of freedom (df), χ2 critical values and test values are given in table

21. The null hypothesis is not rejected since χ2 test value is less than the critical value.

The values of the χ2 test are less than χ

2 critical values for the years 2013 and 2014,

which implies that the estimated realization rates of revenues and the actual realization

rates of revenues are not significantly different. Table 21 results show that Markov

model is valid.

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

54

Table 21. Validity of Tax Revenues 2013 2014

Tax Revenues df Χ20,05

Crit.V

Χ20,05

Test V

H0:

Valid

df Χ20,05

Crit.V

Χ20,05

Test V

H0:

Valid

Income tax 2 5,991 1,12 Accept 2 5,991 2,03 Accept

Corporate tax 1 3,841 0,17 Accept 2 5,991 4 Accept

Property Tax 2 5,991 0,29 Accept 2 5,991 0,25 Accept

Vat Included 1 3,841 2 Accept 1 3,841 3,5 Accept

Vat on Imports 1 3,841 0,75 Accept 1 3,841 0,75 Accept

Special Consumption Tax 1 3,841 0,67 Accept 1 3,841 0,5 Accept

Communication Tax 2 5,991 1 Accept 2 5,991 0,75 Accept

Inheritence and Gift Tax 1 3,841 0,4 Accept 1 3,841 0,33 Accept

Motor Vehicle Tax 1 3,841 0,5 Accept 1 3,841 0,4 Accept

Tax on Wagering 1 3,841 2 Accept 1 3,841 1 Accept

Stamp Duty Tax 1 3,841 1 Accept 1 3,841 0,5 Accept

Customs Tax 1 3,841 1 Accept 1 3,841 0,5 Accept

Banking and Insurance Tax 1 3,841 0,8 Accept 1 3,841 0,5 Accept

Findings, Discussion and Results

According to transition matrices, transitions of tax revenues are declining in

higher states and improving in lower states. 2016 predictions with respect to middle

state using the better models are given in table 22.

Table 22. Tax Revenue Predictions For 2016 According to Better Models

Tax Revenues

Better

Markov

Model

Realization Rate r

(%)

Predictions For 2016

According to Better Models

Probability

(%)

1 – Probability

(%)

Income tax 1 C or higher 96,7 ≤ r 100 0

Corporate tax 2 C or higher 97,2 ≤ r 76 24

Property Tax 3 B or higher 103,1 ≤ r 14 86

Inheritence and Gift Tax 1 C or higher 91,5 ≤ r 93 7

Motor Vehicle Tax 1 C or higher 100,2 ≤ r 75 25

Vat Included 1 C or higher 101 ≤ r 75 25

Special Consumption Tax 3 B or higher 94,2 ≤ r 80 20

Banking and Insurance Tax 1 C or higher 96,8 ≤ r 80 20

Tax on Wagering 1 C or higher 94,7 ≤ r 100 0

Special Communication Tax 1 C or higher 97,9 ≤ r 42 58

Tax on Customs 1 C or higher 93,1 ≤ r 67 33

Vat on Imports 1 C or higher 99,1 ≤ r 60 40

Stamp Duty Tax 1 C or higher 100,6 ≤ r 36 74

According to model 1 of income tax, the probabilities of five states will be

stable in 2031. Income tax rate more likely will be realized at 102.5% or higher in the

long run. Probability of income tax rate greater than 108.3% is improving from 10% in

2016 to a stable 19.05%. Probability of income tax rate between 102.5% and 108.2% is

improving from 20% in 2016 to a stable 35.71%. Probability of 96.7 ≤ r ≤ 102.4 is

decreasing from 70% to a stable 29.76%. Other tax revenues predictions are compared

in table 23.

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

55

Table 23. Comparison of 2016 Predictions To Stationary Matrices According to Better Models

Tax Revenues

Better

Markov

Model

Comparison of 2016 Predictions To Stationary Matrices

According to Better Models

2016 Prediction Stationary Matrix SY

Income tax 1 .10 .20 .70 0 0 .19 .36 .30 0 .15 2031

Corporate tax 2 .04 .10 .62 .24 .09 .09 .64 .18 2024

Property Tax 3 .07 .07 .86 .08 .08 .84 2020

Inheritence and Gift Tax 1 .29 .15 .49 0 0 .27 .18 .46 0 .09 2030

Motor Vehicle Tax 1 0 .50 .25 .25 0 .07 .14 .52 .20 .07 2029

Vat Included 1 .12 .13 .50 0 .25 .09 .09 .35 .22 .26 2036

Special Consumption Tax 3 .24 .56 .20 1 0 0 2015

Banking and Insurance Tax 1 .20 .20 .40 .20 0 .17 .12 .42 .25 .04 2029

Tax on Wagering 1 .25 0 .75 0 0 .29 .28 .29 0 .14 2097

Special Communication Tax 1 .07 0 .35 .52 .06 .06 0 .41 .43 .10 2027

Tax on Customs 1 .45 .11 .11 .11 .22 .30 .23 .15 .22 .10 2037

Vat on Imports 1 0 0 .60 .32 .08 0 .13 .48 .32 .07 2031

Stamp Duty Tax 1 .08 .23 .05 .46 .18 .08 .30 .07 .42 .13 2026

This study can be used to predict the other sub-items of tax revenues. Central

government can take the advantages of this study in the planning and improvement of

tax collection process.

Resources

Usher M.B, Jun., 1979, Markovian Approaches to Ecological Succession, Journal of

Animal Ecology, 48(2):413-426

Taha H.A, Yöneylem Araştırması, 6.baskıdan çeviri, Literatür Yayıncılık, 2000: 726

Yeh HW, Chan W, Symanski E, Davis B.R, 2010, Estimating Transition Probabilities

for Ignorable Intermittent Missing Data in a Discrete-Time Markov Chain,

Communications in Statistics-Simulation and Computation, 39(2):433-448

Baasch A, Tischew S and Bruelheide H, June 2010, Twelve years of succession on

sandy substrates in a post-mining landscape: A Markov chain analysis,

Ecological Applications, 20(4):1136-1147

Grimshaw S.D, Alexander W.P, 2011, Markov Chain Models for Deliquency:

Transition Matrix Estimation and Forecasting, John Wiley&Sons, Applied

Stochastic Models in Business and Industry, 27: 267-279

Lipták K, 2011, The Application Of Markov Chain Model To The Description Of

Hungarian Labor Market Processes, Zarządzanie Publiczne 4(16):133–149

Büyüktatlı F, İşbilir S, Çetin E.İ, 2013, Markov Analizi ile Yıllık Ödeneklere Bağlı Bir

Tahmin Uygulaması, Uluslararası Alanya İşletme Fakültesi Dergisi (5):1-8

Lukić P.,Gocić M., Trajković S., 2013, Prediction of annual precipitation on the

territory of south Serbia using markov chains, Bulletin of the Faculty of

Forestry, 108: 81-92.

Ç.Ü. Sosyal Bilimler Enstitüsü Dergisi, Cilt 25, Sayı 2, 2016, Sayfa 41-56

56

Bluman A.G, 2014, Elemantary Statistics, McGraw Hill Education, New York

Vantika S., Pasaribu U.S, 2014, Application of Markov Chain To the Pattern of

Mitochondrical Deoxyribonucleic Acid Mutations, AIP Conference Proc. 1589, 296

İlarslan K, 2014, Hisse Senedi Fiyat Hareketlerinin Tahmin Edilmesinde Markov

Zincirlerinin Kullanılması: IMKB 10 Bankacılık Endeksi İşletmeleri Üzerine

Ampirik Bir Çalışma, E-Journal of Yaşar University, 9(35): 6099-6260

Cavers M.S., Vasudevan K., 2015, Brief Communication: Earthquake sequencing:

Analysis of Time Series constructed from the Markov Chain Model, Nonlinear

Process Geophysics, 22:589-599

Lazri M., Ameur S., Brucker J.M., Lahdir M. and Sehad M., Analysis of drought areas

in northern Algeria using Markov chains, February 2015, J. Earth Syst. Sci.

124(1):61–70

http://www.gib.gov.tr/sites/default/files/fileadmin/user_upload/VI/GBG/Tablo_47.xls.ht

m 5.12.2015

http://www.gib.gov.tr/sites/default/files/fileadmin/user_upload/VI/GBG/Tablo_44.xls.ht

m 5.12.2015

http://www.gib.gov.tr/sites/default/files/fileadmin/user_upload/VI/GBG/Tablo_46.xls.ht

m 5.12.2015

http://www.gib.gov.tr/sites/default/files/fileadmin/user_upload/VI/GBG/Tablo_45.xls.ht

m 5.12.2015

www.ekodialog.com>konular>genel_butce 8.12.2015

http://www.hurriyet.com.tr/2016-vergi-artis-oranlari-belli-oldu-40009417 9.12.2016

http://www.zaman.com.tr/ekonomi_2015-yilinda-vergiler-yuzde-1011-oraninda-

artacak_2255169.html 10.12.2015

galton.uchicago.edu/~lalley/Courses/312/MarkovChains.pdf 15.12.2015

dept.stat.lsa.umich.edu/~ionides/620/notes/markov_chains.pdf 15.12.2015