Prepared by Debby Bloom-Hill CMA, CFM

CHAPTER 8CHAPTER 8

Pricing Decisions, Analyzing Customer Profitability, and

Activity-Based Pricing

Pricing Decisions, Analyzing Customer Profitability, and

Activity-Based Pricing

Slide 8-2

Pricing DecisionsPricing Decisions

Pricing decisions are often the most difficult decisions that managers face

Pricing decisions examined in this chapter include Profit maximizing price from the

standpoint of economic theory Pricing of special orders Marking up costs and target costing Measuring customer profitability

and activity based pricing

Slide 8-3

The Profit Maximizing PriceThe Profit Maximizing Price Economic theory suggests that the

quantity demanded is a function of the price that is charged

Generally, the higher the price, the lower the quantity demanded If managers can estimate the

quantity demanded at various prices, determining the optimal price is straightforward

Slide 8-4 Learning objective 1: Compute the profit maximizing price for a product or service

The Profit Maximizing PriceThe Profit Maximizing Price

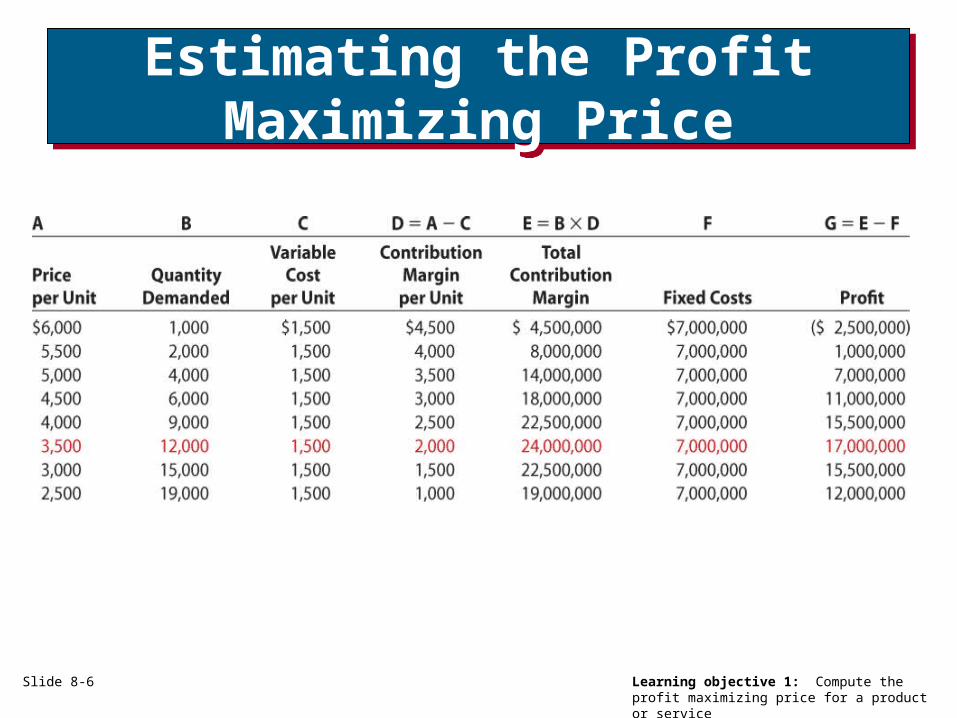

To calculate the profit maximizing price: Subtract unit variable costs from

price to obtain the contribution margin

Multiply the contribution margin by the quantity demanded

Subtract fixed costs and estimate profits

Select the price with the highest profit

Slide 8-5 Learning objective 1: Compute the profit maximizing price for a product or service

Estimating the Profit Maximizing Price

Estimating the Profit Maximizing Price

Slide 8-6 Learning objective 1: Compute the profit maximizing price for a product or service

Estimating DemandEstimating Demand

The most difficult part of determining the profit maximizing price is determining the demand function A number of approaches can be

used Sales managers in various regions

could estimate the total quantity demanded at various prices

The product could be test marketed with a number of potential customers at various prices

Slide 8-7 Learning objective 1: Compute the profit maximizing price for a product or service

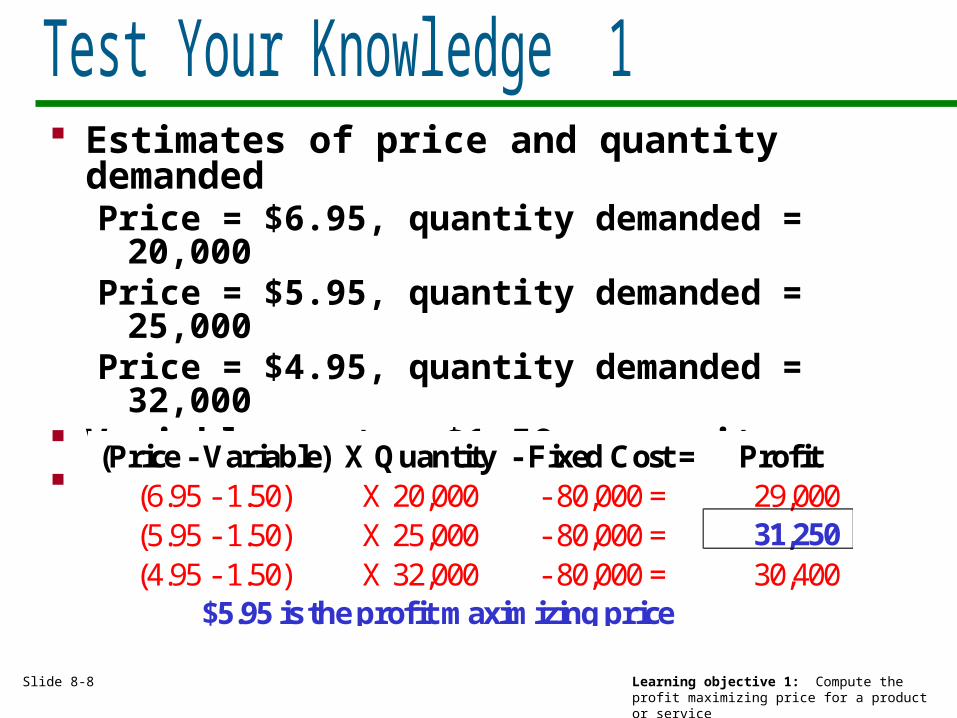

Estimates of price and quantity demandedPrice = $6.95, quantity demanded =

20,000Price = $5.95, quantity demanded =

25,000Price = $4.95, quantity demanded =

32,000 Variable cost = $1.50 per unit Fixed cost = $80,000

Find the profit maximizing price

Slide 8-8 Learning objective 1: Compute the profit maximizing price for a product or service

(Price - Variable) X Quantity - Fixed Cost = Profit(6.95 - 1.50) X 20,000 - 80,000 = 29,000 (5.95 - 1.50) X 25,000 - 80,000 = 31,250 (4.95 - 1.50) X 32,000 - 80,000 = 30,400

$5.95 is the profit maximizing price

Pricing Special OrdersPricing Special Orders

Special orders are for goods and services not considered part of a company’s normal business Price charged will not affect prices

charged in the normal course of business

The company may be better off charging a price that is below full cost

Slide 8-9 Learning objective 2: Perform incremental analysis related to pricing a special order

Pricing Special OrdersPricing Special Orders

The special order decision presents two alternatives Accept Reject

Income from the main business is the same under both alternatives It is not incremental and need not

be considered in the special order

Slide 8-10 Learning objective 2: Perform incremental analysis related to pricing a special order

Pricing Special OrdersPricing Special Orders

Need to consider incremental revenues and incremental costs The incremental revenue is the

revenue associated with the special order

Incremental costs can include Direct materials Direct labor Variable overhead Incremental fixed costs

Slide 8-11 Learning objective 2: Perform incremental analysis related to pricing a special order

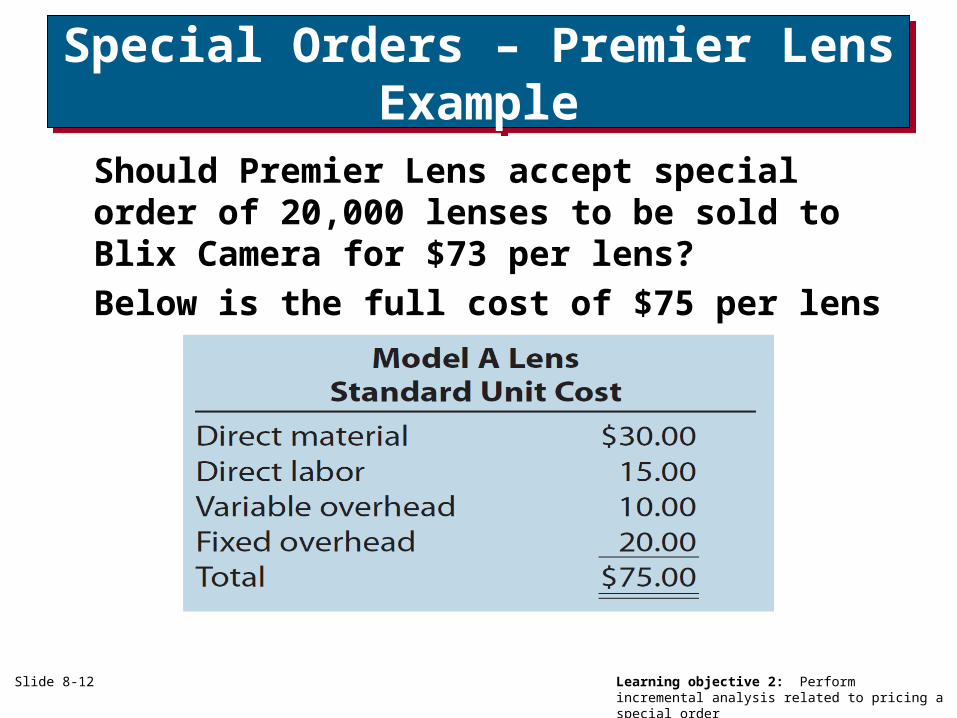

Special Orders – Premier Lens Example

Special Orders – Premier Lens Example

Should Premier Lens accept special order of 20,000 lenses to be sold to Blix Camera for $73 per lens?Below is the full cost of $75 per lens

Slide 8-12 Learning objective 2: Perform incremental analysis related to pricing a special order

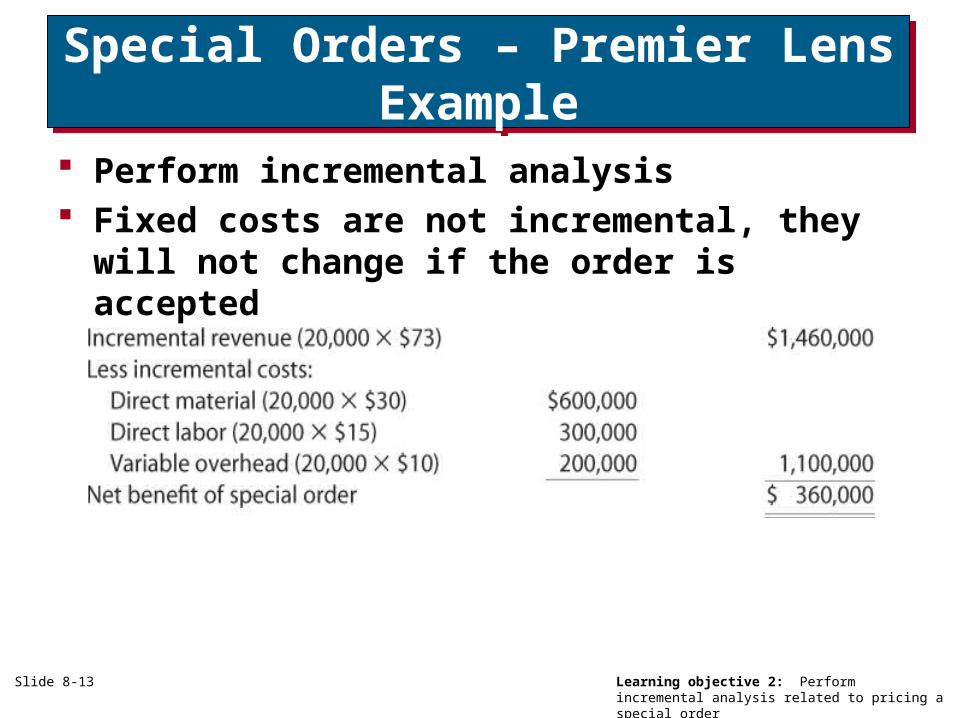

Special Orders – Premier Lens Example

Special Orders – Premier Lens Example

Perform incremental analysis Fixed costs are not incremental, they

will not change if the order is accepted

Slide 8-13 Learning objective 2: Perform incremental analysis related to pricing a special order

Commonwealth EdisonCommonwealth Edison

Slide 8-14 Learning objective 2: Perform incremental analysis related to pricing a special order

Which of the following is true?a. In pricing special orders, fixed costs

typically are not relevantb. In pricing special orders, fixed costs

typically are relevant

Answer: aFixed costs typically are not relevant

Slide 8-15 Learning objective 2: Perform incremental analysis related to pricing a special order

Cost-Plus PricingCost-Plus Pricing

With a cost plus approach, the company starts with an estimate of product cost Typically excluding any selling or

administrative costs Adds a markup to arrive at a price

that allows for a reasonable level of profit

Slide 8-16 Learning objective 3: Explain the cost-plus approach to pricing and why it is inherently circular for manufacturing firms

Cost-Plus PricingCost-Plus Pricing

Advantages The cost plus approach is simple to

apply The company will earn a reasonable

profit if a sufficient quantity can be sold at the specified price

The approach also has limitations

Slide 8-17 Learning objective 3: Explain the cost-plus approach to pricing and why it is inherently circular for manufacturing firms

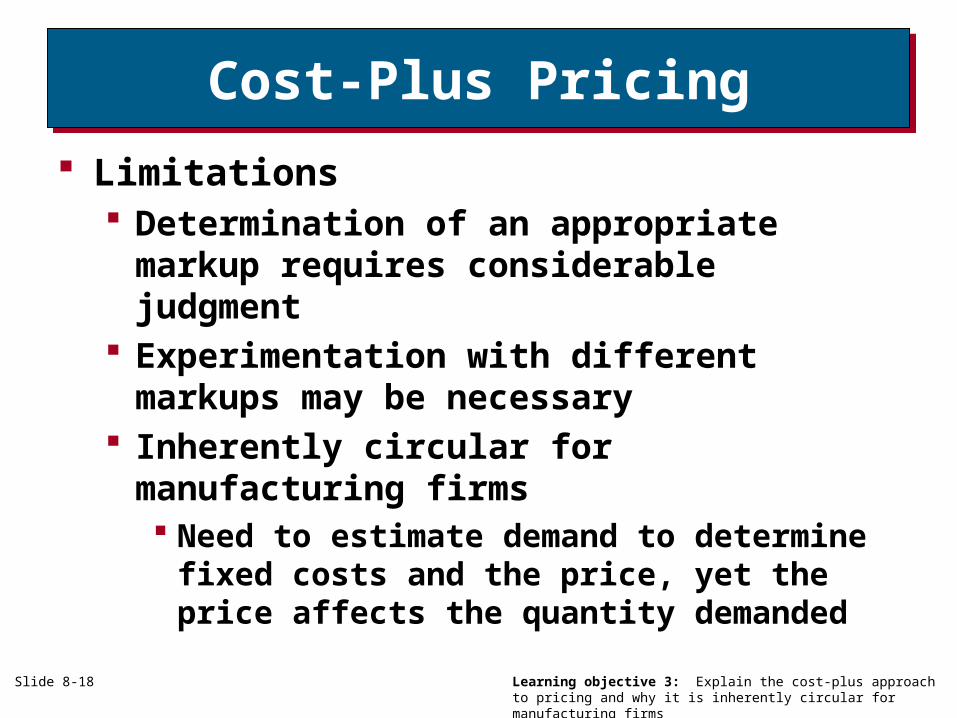

Cost-Plus PricingCost-Plus Pricing

Limitations Determination of an appropriate

markup requires considerable judgment

Experimentation with different markups may be necessary

Inherently circular for manufacturing firms Need to estimate demand to determine

fixed costs and the price, yet the price affects the quantity demanded

Slide 8-18 Learning objective 3: Explain the cost-plus approach to pricing and why it is inherently circular for manufacturing firms

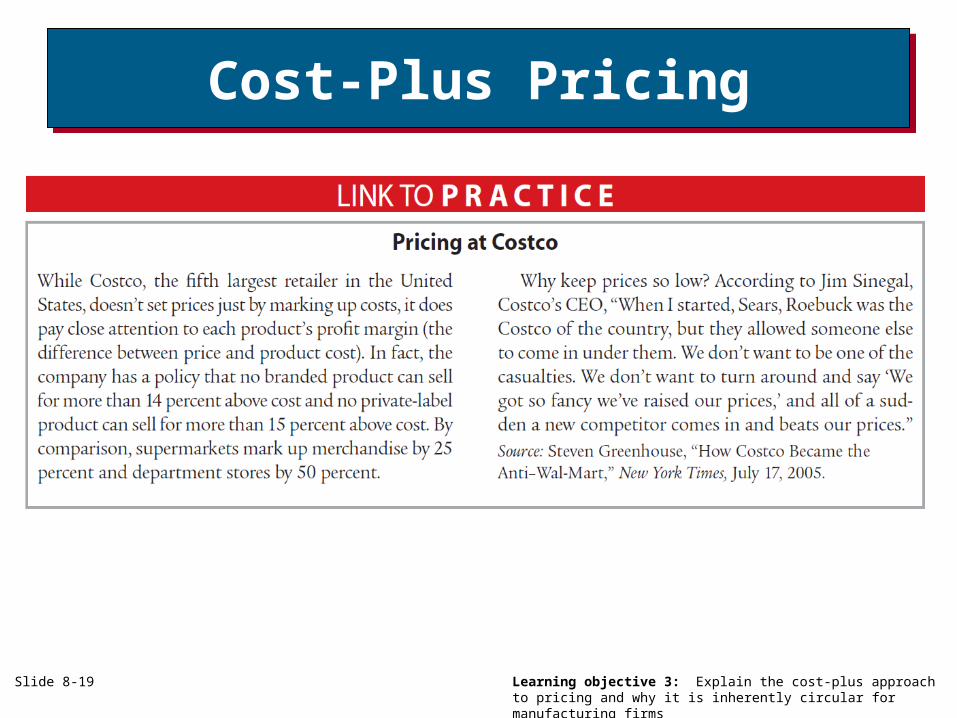

Cost-Plus PricingCost-Plus Pricing

Slide 8-19 Learning objective 3: Explain the cost-plus approach to pricing and why it is inherently circular for manufacturing firms

All of the following are limitations of cost plus pricing except

a. Determination of the markup percentage requires judgment

b. Is inherently circular for manufacturing firms

c. Experimentation may be necessaryd. Cost plus is simple to apply

Answer: dSimplicity is an advantage of cost plus

pricingSlide 8-20 Learning objective 3: Explain the cost-plus approach to pricing and why

it is inherently circular for manufacturing firms

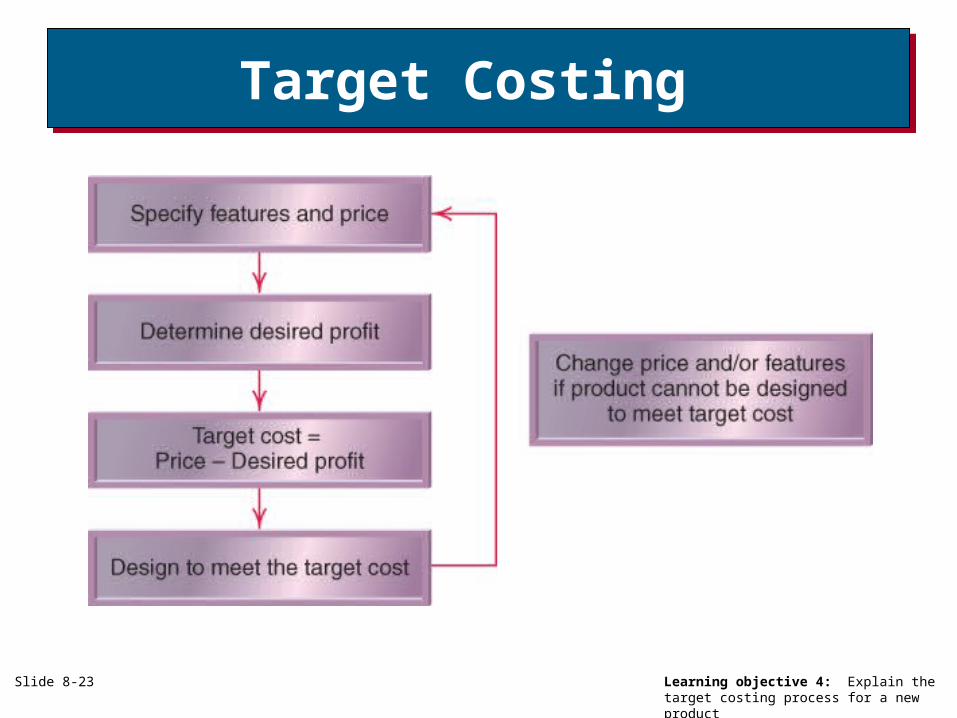

Target Costing Target Costing

Slide 8-21 Learning objective 4: Explain the target costing process for a new product

Once a product is designed it is difficult to make changes that reduce costs 80% of a product’s costs cannot be

reduced once it is designed Product features drive costs

Target costing Integrated approach to determine

features, price, costs and design to ensure a profit

Target Costing Target Costing

Slide 8-22 Learning objective 4: Explain the target costing process for a new product

The process begins with an analysis of competing products This leads to a specification of

features and price attractive to customers

The second step is to specify a desired level of profit

Then the engineering department with input from the cost accounting department develops a design that can be produced at a cost which will earn the desired level of profit

Target Costing Target Costing

Slide 8-23 Learning objective 4: Explain the target costing process for a new product

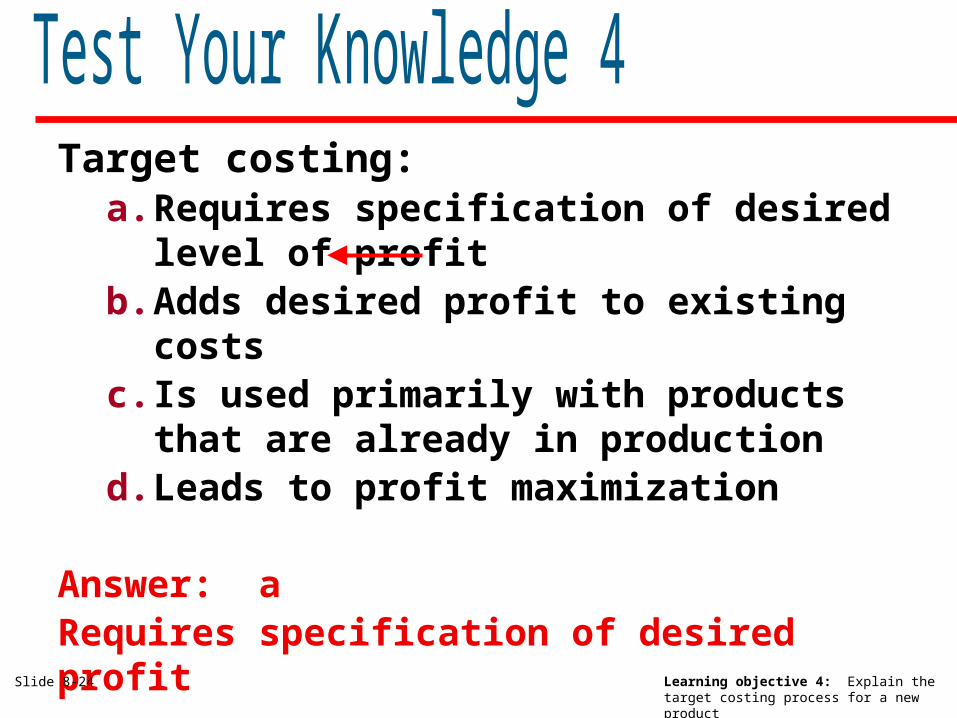

Target costing:a. Requires specification of desired

level of profitb. Adds desired profit to existing

costsc. Is used primarily with products

that are already in productiond. Leads to profit maximization

Answer: aRequires specification of desired profit

Slide 8-24 Learning objective 4: Explain the target costing process for a new product

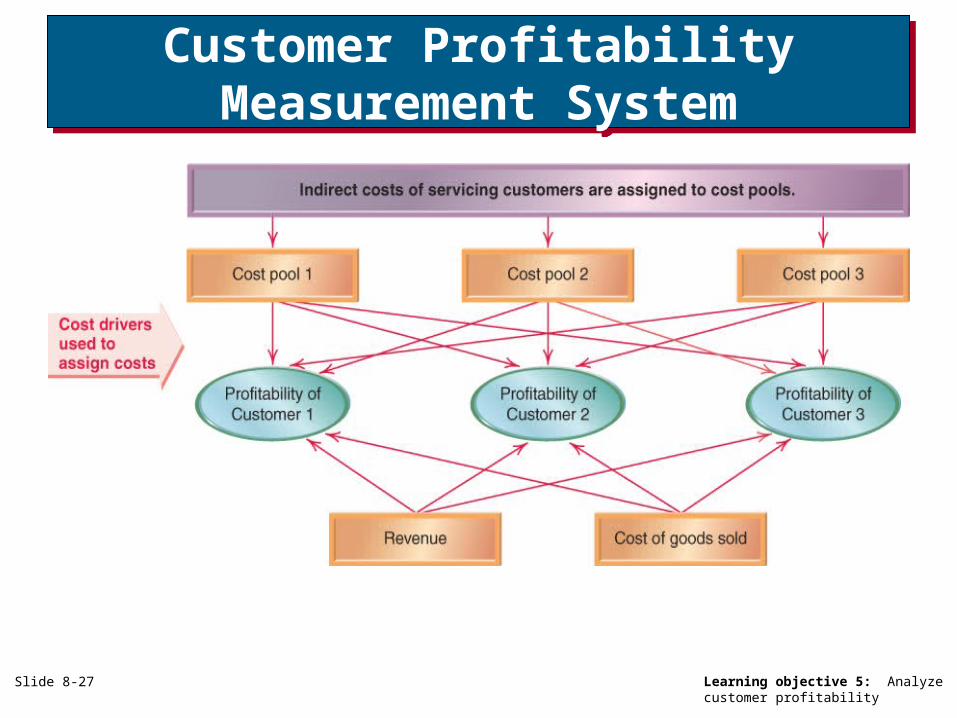

Analyzing Customer Profitability

Analyzing Customer Profitability

Customer Profitability Measurement System (CPM) Indirect costs of servicing customers

are assigned to cost pools Indirect costs include processing orders, handling returns, and shipments

Costs are allocated to specific customers using cost drivers to determine customer profitability Subtracting these costs and product costs from customer revenue yields a measure of customer profitability

Slide 8-25 Learning objective 5: Analyze customer profitability

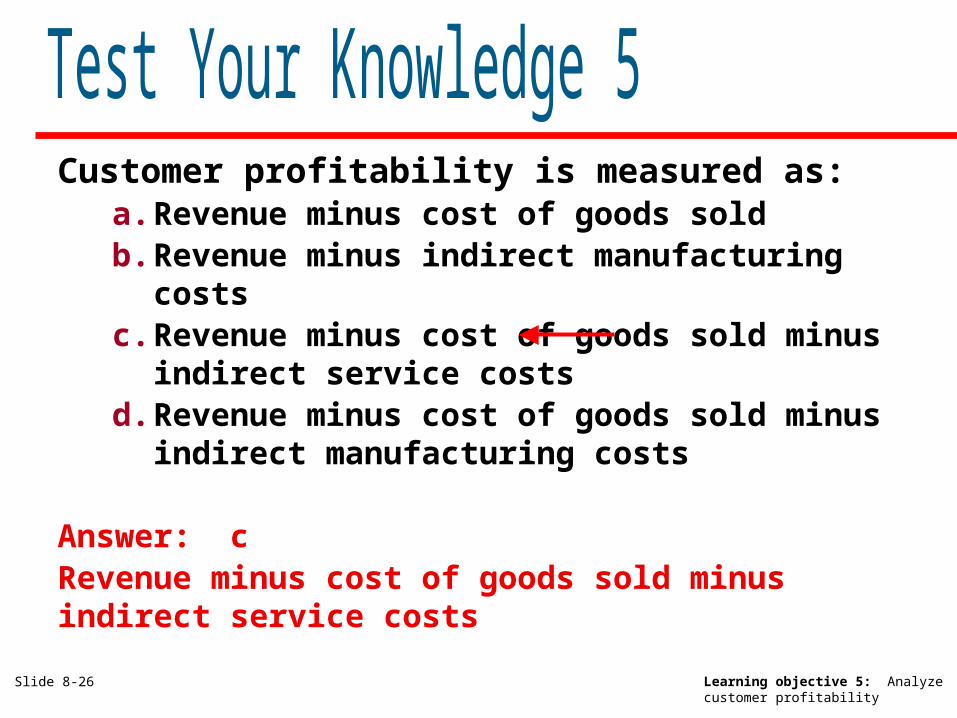

Customer profitability is measured as:a. Revenue minus cost of goods soldb. Revenue minus indirect manufacturing

costsc. Revenue minus cost of goods sold minus

indirect service costsd. Revenue minus cost of goods sold minus

indirect manufacturing costs

Answer: cRevenue minus cost of goods sold minus indirect service costs

Slide 8-26 Learning objective 5: Analyze customer profitability

Customer Profitability Measurement SystemCustomer Profitability Measurement System

Slide 8-27 Learning objective 5: Analyze customer profitability

Cost Pools and Cost Drivers to Service Customers

Cost Pools and Cost Drivers to Service Customers

Slide 8-28 Learning objective 5: Analyze customer profitability

Customer Profitability AnalysisCustomer Profitability Analysis

Slide 8-29 Learning objective 5: Analyze customer profitability

CostRevenue Quantity Amount Quantity AmountLess COGS 732,600 727,650 Gross margin (666,000) (661,500) Less indirect costs 66,600 66,150

Internet orders $1.20 / order 165 (198) 0 0Fax orders $4.50 / order 20 (90) 320 (1,440) Line items $0.90 / item 2,500 (2,250) 5,100 (4,590) Miles $0.36 / mile 1,200 (432) 3,300 (1,188) Weight $0.40 / pound 900 (360) 870 (348) Items returned $0.80 / item 210 (168) 910 (728)

Profit 63,102 57,856 Profit as a percent of sales 8.61% 7.95%

Customer 1 Customer 2

A customer profitability measurement (CPM) system:

a. Allocates indirect costs to individual customers

b. Traces revenue to individual customersc. Traces cost of goods sold to individual

customersd. All of the above are true

Answer: dAll of the above are true

Slide 8-30 Learning objective 5: Analyze customer profitability

Customer Profitability AnalysisCustomer Profitability Analysis

Slide 8-31 Learning objective 5: Analyze customer profitability

Customer Profitability and Performance Measures

Customer Profitability and Performance Measures

Some examples of performance measures that will drive managers to improve customer profitability Percent of customers who are not

profitable Dollar loss for customers who are not

profitable Average profit per customer Number of customer service requests

per 100 customers Percent of customers who return items Dollar value of returned items

Slide 8-32 Learning objective 5: Analyze customer profitability

Activity-Based PricingActivity-Based Pricing

Customers are presented with separate prices for services they request in addition to the cost of goods purchased Customers will carefully consider

the services they request May lead them to impose less cost

on the supplier Also called menu-based pricing

Slide 8-33 Learning objective 6: Explain the activity-based pricing approach

Activity-Based PricingActivity-Based Pricing

Customers might object as the price they pay should cover these costs Ways to deal with this resistance

Lower prices slightly and then encourage customers to make fewer but larger purchases

Customers could be encouraged to limit the variety of goods they order

Activity-based pricing could be used only on the least profitable customers

Slide 8-34 Learning objective 6: Explain the activity-based pricing approach

Pricing DecisionsPricing Decisions

Slide 8-35 Learning objective 6: Explain the activity-based pricing approach

CopyrightCopyright © 2010 John Wiley & Sons, Inc. All rights

reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Slide 8-36